Cloud Access Security Brokers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

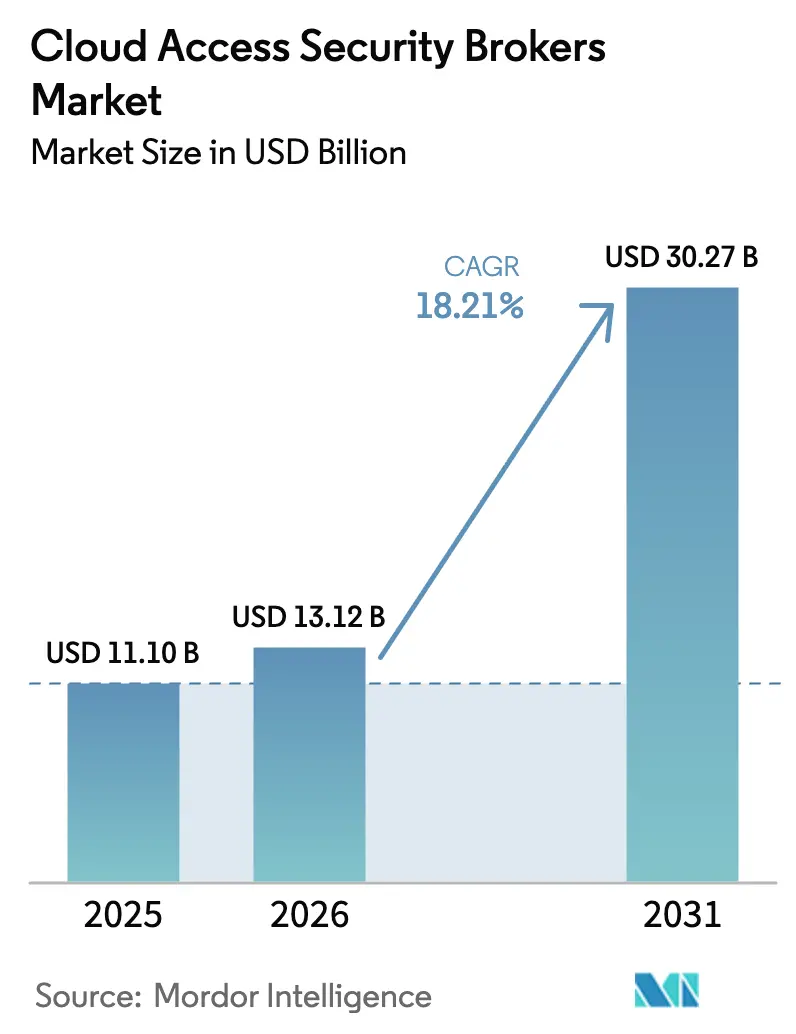

| Market Size (2026) | USD 13.12 Billion |

| Market Size (2031) | USD 30.27 Billion |

| Growth Rate (2026 - 2031) | 18.21% CAGR |

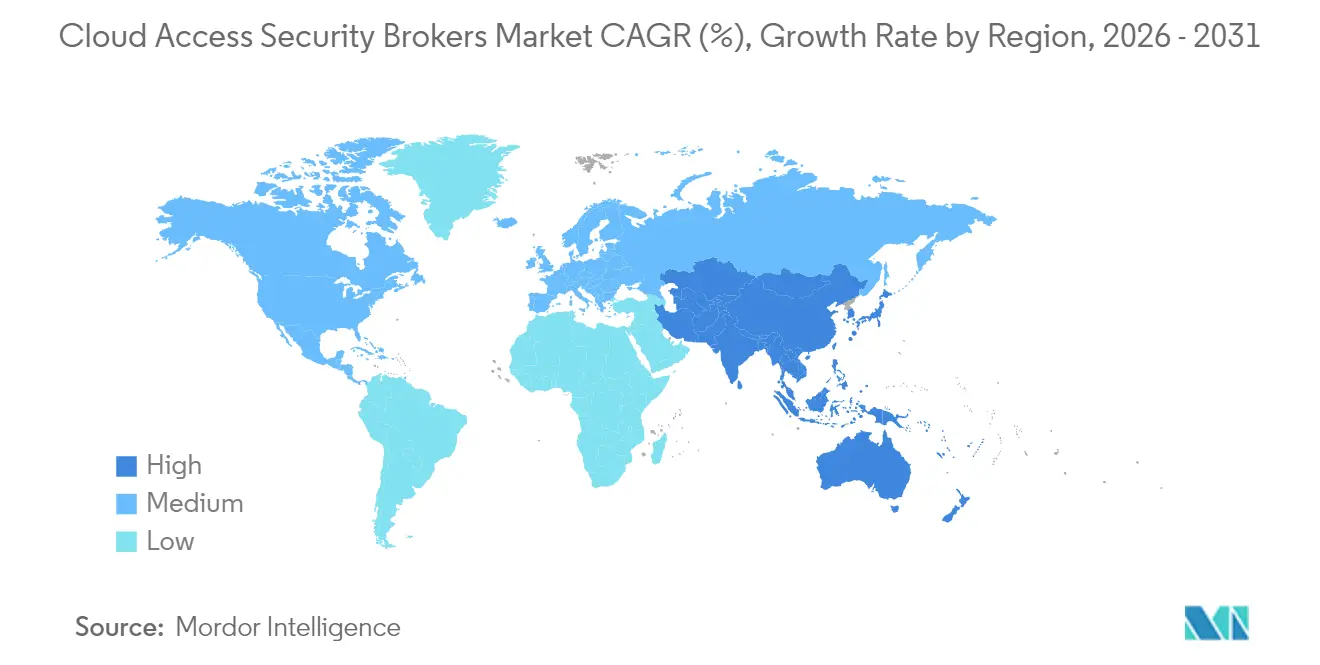

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Access Security Brokers Market Analysis by Mordor Intelligence

The Cloud Access Security Brokers market size is expected to grow from USD 11.10 billion in 2025 to USD 13.12 billion in 2026 and is forecast to reach USD 30.27 billion by 2031 at 18.21% CAGR over 2026-2031.

Enterprises are moving away from perimeter-centric defenses as the EU NIS2 directive and US Executive Order 14144 enforce Zero Trust requirements, while the adoption of generative AI elevates data governance risk. Vendors now build CASB functionality directly into secure access service edge (SASE) platforms, positioning the Cloud Access Security Brokers market as a core layer in holistic security stacks rather than an adjunct toolset. Growth also stems from higher cyber-insurance premiums that reward organizations able to document continuous cloud controls, as well as API-first integrations that simplify coverage of SaaS, IaaS, and PaaS estates. While Software-as-a-Service (SaaS) protection still dominates revenue, the accelerating shift of production workloads to cloud infrastructure signals a decisive pivot toward securing multicloud environments at scale. Intensifying competition, marked by acquisitions such as Zscaler–Avalor and CrowdStrike–Flow Security, is consolidating capabilities around data security posture management and generative-AI governance.

Key Report Takeaways

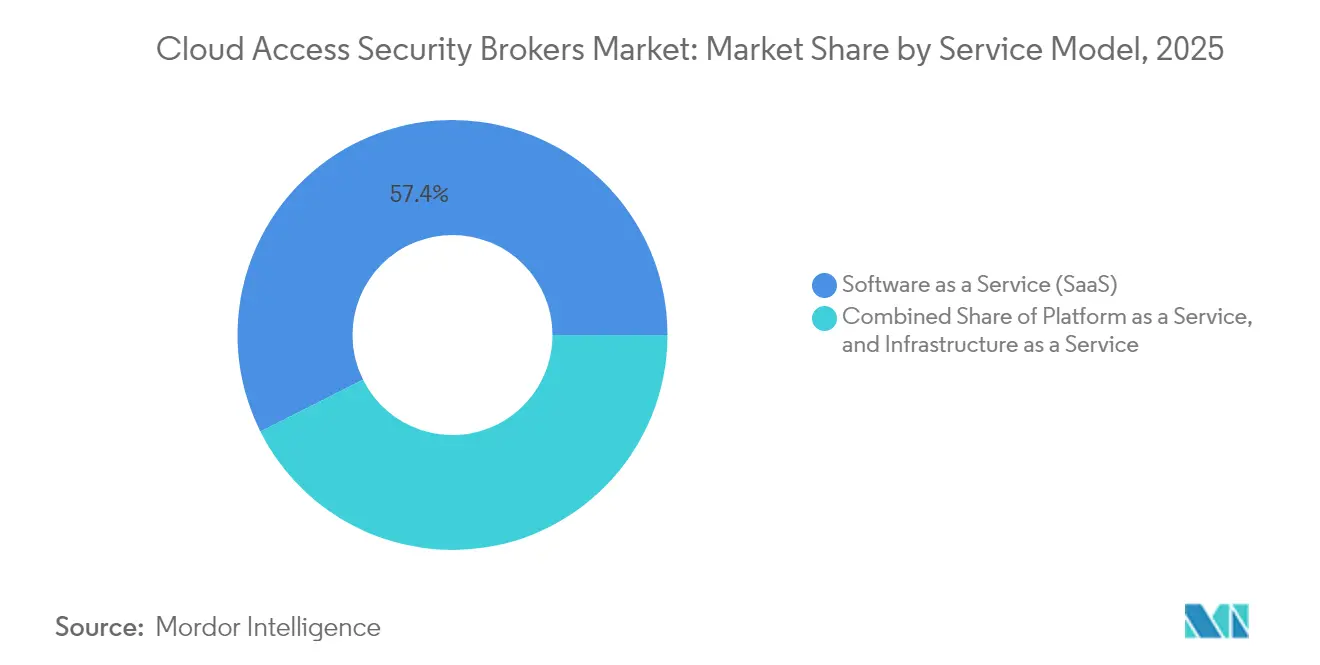

- By service model, SaaS protection led with a 57.40% revenue share of the Cloud Access Security Brokers market in 2025, whereas IaaS security is projected to rise at a 19.85% CAGR through 2031.

- By organization size, large enterprises held 62.30% of the market share in 2025, while small and medium enterprises recorded the fastest growth at an 17.65% CAGR to 2031.

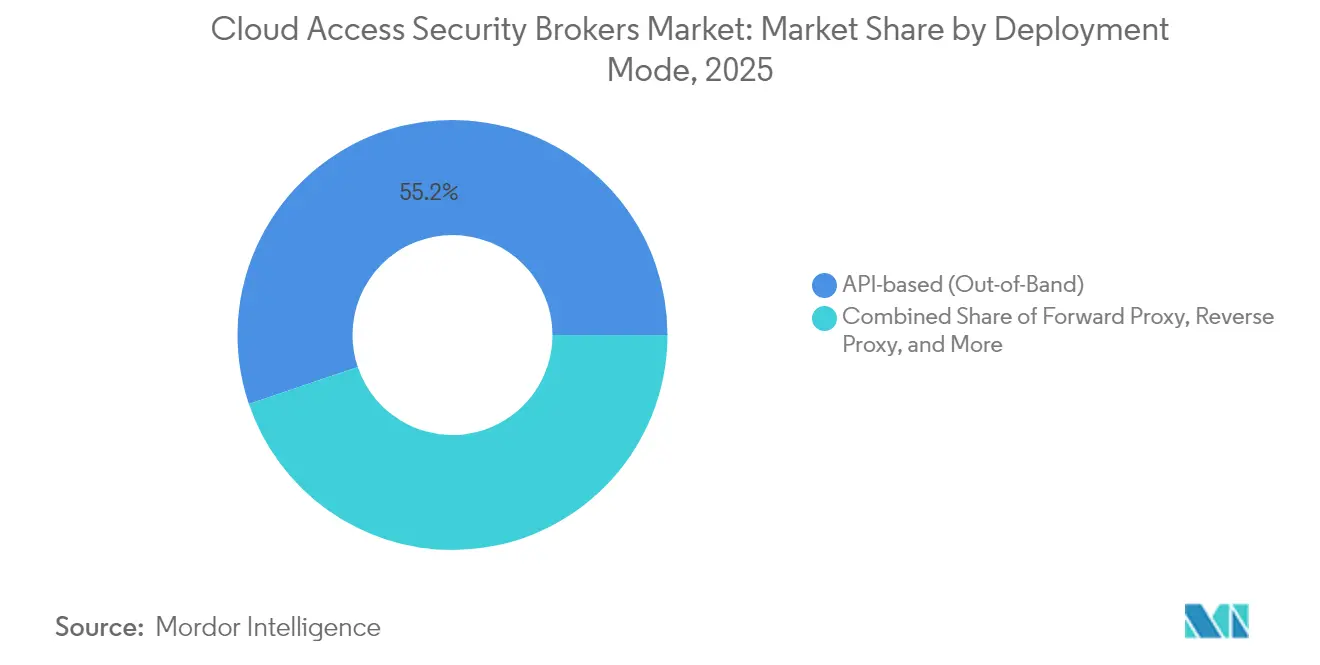

- By deployment mode, API-based implementations accounted for 55.20% of the Cloud Access Security Brokers market size in 2025, and multimode hybrid deployments are forecast to expand at a 21.75% CAGR.

- By end-user, banking, financial services, and insurance captured 21.60% of 2025 revenue, whereas manufacturing is on course for a 20.45% CAGR through 2031.

- By geography, North America contributed 36.60% of 2025 revenue, but Asia Pacific is set to post the highest regional CAGR at 19.15% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Access Security Brokers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of SaaS adoption across verticals | +3.2% | Global, with acceleration in APAC and Latin America | Medium term (2-4 years) |

| Mandates for Zero-Trust and data residency compliance | +4.1% | North America & EU leading, APAC following | Short term (≤ 2 years) |

| Surging API-first CASB integrations inside SASE stacks | +2.8% | Global, concentrated in enterprise segments | Medium term (2-4 years) |

| Higher cyber-insurance premiums driving CASB uptake | +1.9% | North America & EU primarily | Short term (≤ 2 years) |

| Convergence of DSPM with CASB | +2.3% | Global, led by data-intensive industries | Long term (≥ 4 years) |

| Industry-specific pre-trained policy packs | +1.4% | Regulated industries globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of SaaS Adoption Across Verticals

Enterprise SaaS footprints now span collaboration, CRM, and low-code development environments, creating visibility gaps that legacy firewalls cannot close. Manufacturers such as Nexteer Automotive deploy inline CASB controls to secure Office 365 workloads while preserving GDPR compliance, demonstrating cross-industry urgency to govern SaaS data flows. Healthcare providers shift electronic health records to multi-cloud designs, demanding granular policy enforcement to meet HIPAA obligations. Financial institutions tighten oversight of third-party SaaS plug-ins, making audit-ready reporting a prerequisite for vendor onboarding. Collectively, these factors heighten baseline demand across the Cloud Access Security Brokers market.

Mandates for Zero-Trust and Data Residency Compliance

Regulators elevate Zero Trust from best practice to an enforced standard. The EU NIS2 directive applies penalties up to EUR 10 million for supply-chain lapses, compelling organisations to install continuous cloud-access controls. Japan’s forthcoming five-level cybersecurity rating further codifies real-time monitoring, and Singapore’s MAS guidance points financial firms toward CASB tooling aligned with identity-centric design. In the United States, Executive Order 14144 obliges federal agencies to verify every cloud request, accelerating public-sector adoption. These overlapping mandates anchor long-term growth across the market.

Surging API-First CASB Integrations Inside SASE Stacks

Unified SASE subscriptions climbed sharply in 2025 as organisations swapped multiple point products for a converged cloud edge model. Fortinet reported USD 1.15 billion in unified-SASE ARR, exemplifying commercial appetite for blended CASB, SWG, and ZTNA functions[1]Fortinet, “Q1 2025 Earnings Release,” fortinet.com. Netskope’s tie-in with OpenAI’s ChatGPT Enterprise Compliance API shows how providers embed data-detection rules for generative-AI workflows. At the platform layer, Cisco’s pending integration of Splunk log analytics positions it to deliver full-stack cloud telemetry through a single console. API-first orchestration, therefore, lifts adoption barriers and sustains momentum for the Cloud Access Security Brokers market.

Higher Cyber-Insurance Premiums Driving CASB Uptake

Underwriters now demand proof of continuous cloud oversight before issuing policies and have raised premiums in line with exposure risk. Firms suffering incidents report average insurance-related budget jumps of 26% and channel funds directly toward CASB roll-outs that supply automated evidence of policy compliance. Banks in particular allocate 12% of IT budgets to security, up from 9.7% in 2020, and reserve sizable allocations for cloud-access governance platforms. As actuarial models mature, insurers explicitly reward organisations that implement CASB-driven data-loss prevention, turning insurance pricing into a structural growth lever for the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Configuration drift and shadow policies in multi-clouds | -2.1% | Global, acute in large enterprises | Short term (≤ 2 years) |

| High false-positive rates hurting SOC productivity | -1.8% | Global, particularly in resource-constrained organizations | Medium term (2-4 years) |

| Persistent skills gap in cloud-native security | -1.3% | Global, severe in emerging markets | Long term (≥ 4 years) |

| Vendor lock-in fears with single-vendor SASE suites | -0.9% | Enterprise segments globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Configuration Drift and Shadow Policies in Multi-Clouds

Running parallel policies across AWS, Azure, and Google Cloud increases the odds of misaligned rules that weaken enforcement. Shadow IT compounds exposure as staff adopt unsanctioned SaaS tools, leaving data outside central oversight. Japan’s 2024 security report ranks supply-chain exposures as its second-highest threat, underscoring how third-party clouds widen the attack surface[2]Information-Technology Promotion Agency, “2024 Security Assessment,” ipa.go.jp. Auditors now flag inconsistent data-loss policies during compliance reviews, and security leaders cite drift management as a top barrier to scaling CASB deployments within the Cloud Access Security Brokers market.

High False-Positive Rates Hurting SOC Productivity

SOC teams already battle alert overload; overly aggressive CASB rules can double ticket volumes and mask real-world threats. The Cloud Security Alliance notes a perception gap between vendor claims and operational reality, driving user frustration. Machine-learning engines need constant tuning to adapt to unique behaviour patterns, draining limited human resources. Unless accuracy improves, some buyers delay full-scope projects, moderating near-term growth in the Cloud Access Security Brokers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Model: IaaS Acceleration Challenges, SaaS Dominance

IaaS protection is tracking a 19.85% CAGR to 2031, whereas SaaS still represented 57.40% of revenue in 2025, reflecting legacy purchase cycles that favoured application-centric monitoring. This divergence indicates that the Cloud Access Security Brokers market size for infrastructure workloads will expand significantly as enterprises harden Kubernetes clusters and serverless functions on public clouds.

The Cloud Access Security Brokers market continues to shift toward platforms that blend CASB, CSPM, and entitlement management so DevOps teams can embed guardrails inside CI/CD pipelines. Cisco’s acquisition of DeepFactor shows large vendors stitching runtime security into their stacks, signaling renewed competition to win the next wave of IaaS-centric deals.

By Organization Size: SME Cloud-First Strategies Accelerate Adoption

SMEs posted an 17.65% CAGR forecast despite large enterprises retaining 62.30% revenue in 2025, proving cloud delivery can equalise access to enterprise-grade safeguards. Many SMEs leapfrog on-premises tooling and instead subscribe directly to converged SASE offerings that bundle CASB, reducing total ownership cost.

As adoption broadens, the Cloud Access Security Brokers industry must streamline onboarding and offer managed services that offset skills shortages. Success stories such as Grasshopper Bank show how automating compliance testing with cloud-native controls trims 50 hours per partner integration and boosts regulator confidence.

By Deployment Mode: Hybrid Approaches Gain Enterprise Traction

API-based detection accounted for 55.20% of 2025 revenue, yet multimode hybrids are expected to climb at a 21.75% CAGR. Enterprises increasingly route high-risk applications through inline proxies for immediate enforcement while retaining API feeds for retrospective analysis. The Cloud Access Security Brokers market share for multimode offerings is therefore likely to close the gap on API-only tools before 2031.

Edge computing and 5G drive further diversification as controls move closer to the user. Fortinet’s FortiSASE inline-CASB demonstrates how distributed enforcement can maintain user experience while upholding uniform policy. Vendors that flexibly orchestrate policy across proxies, APIs, and agents will set the adoption pace.

By End-User: Manufacturing Digitization Drives Vertical Expansion

BFSI retained 21.60% of 2025 spending, but manufacturing shows the highest momentum with a projected 20.45% CAGR. Factories are modernising supply-chain collaboration platforms and integrating operational technology with cloud analytics, prompting demand for context-aware controls. The Cloud Access Security Brokers market size for industrial users is therefore primed for outsized gains through 2031.

Healthcare remains another priority segment as telehealth growth elevates HIPAA compliance risk. Sentara Healthcare’s partnership with Fortinet underscores a sector-specific focus on patient data sovereignty. Vendors delivering pre-built policy packs for regulated records will strengthen their share in these expanding niches of the Cloud Access Security Brokers market.

Geography Analysis

North America held 36.60% of 2025 revenue thanks to mature cloud adoption and well-defined regulatory triggers such as Executive Order 14144, which compels all federal agencies to implement Zero Trust controls by 2025. Public-sector procurement drives early adoption, and Canadian organisations install CASB to handle cross-border data flows under provincial privacy statutes. Mexico’s rising technology investment adds regional demand, particularly among multinationals orchestrating unified policies across NAFTA corridors.

Europe accelerates investment under the dual impetus of NIS2 and GDPR. The Cloud Access Security Brokers market size for EU-based firms is poised to climb as penalties up to EUR 10 million push compliance teams toward automated monitoring. Post-Brexit UK entities fine-tune data-residency rules, while France and Germany seek sovereign cloud alignments that favour providers offering local processing.

Asia Pacific is the fastest-growing theatre at a 19.15% CAGR, fuelled by sovereign-cloud mandates and sweeping digital-transformation agendas. Japan’s Active Cyber Defense Bill and METI’s security rating scheme ratify continuous monitoring as a corporate responsibility. China’s cross-border transfer controls spur adoption of data-classification modules, and India’s expanding fintech ecosystem requires audit-ready cloud access logs. Singapore’s MAS guidelines keep financial hubs at the forefront of Zero Trust implementations, deepening regional contribution to the Cloud Access Security Brokers market.

Competitive Landscape

The Cloud Access Security Brokers market remains moderately concentrated. Netskope surpassed USD 500 million in ARR and recently secured an additional USD 401 million debt facility to accelerate SASE rollouts. Palo Alto Networks reported USD 4.5 billion in next-generation security ARR, underscoring the appetite for integrated platforms.

M&A activity soared as legacy network vendors bought cloud-native expertise. Zscaler’s USD 350 million Avalor purchase expands vulnerability analytics, while CrowdStrike’s USD 200 million Flow Security acquisition adds data-flow visibility. Cisco’s multi-billion-dollar bid for Splunk illustrates the premium attached to telemetry unification.

Emerging specialists target white-space niches such as generative-AI policy enforcement and OT data governance. Cyera’s USD 300 million funding round and Cato Networks’ AI-powered shadow-AI dashboard reflect investor conviction in differentiated use cases. Vendors able to meld identity, data, and network layers into a single policy graph are expected to capture outsized growth.

Cloud Access Security Brokers Industry Leaders

Netskope

Imperva

Palo Alto Networks (Prisma Access)

Cloudflare

Cisco (Cloudlock)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Netskope secured USD 401 million in financing from Morgan Stanley to advance SASE expansion and prepare for an anticipated IPO.

- March 2025: Zscaler finalised the USD 350 million acquisition of Avalor for data-security analytics.

- February 2025: CrowdStrike completed the USD 200 million purchase of Flow Security for cloud-data visibility.

- January 2025: JumpCloud acquired Stack Identity to enrich cloud-posture management.

Global Cloud Access Security Brokers Market Report Scope

Due to the rise in the concerns related to cloud-based applications and programs and their safety and security, the adoption of cloud access security brokers is rapidly increasing. Corporate enterprises are implementing these broker systems to ensure data security. The report also estimates the market size as well as the future growth potential across different segments, such as solution, service, service model, organization size, vertical, and region. The report also captures the effect of the pandemic on the market studied.

The Cloud Access Security Broker Market is segmented by Service Model (Infrastructure-as-a-Service, Platform-as-a-Service, and Solution-as-a-Service), Organization Size (Small and Medium Enterprises and Large Enterprises), End-user Vertical (Banking, Financial Services and Insurance (BFSI), Education, Government, Healthcare and Life Science, Manufacturing, Retail and Wholesale, Telecommunication, and IT), and Geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Infrastructure as a Service (IaaS) |

| Platform as a Service (PaaS) |

| Software as a Service (SaaS) |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| API-based (Out-of-Band) |

| Forward Proxy |

| Reverse Proxy |

| Multimode / Hybrid |

| Banking, Financial Services and Insurance (BFSI) |

| Education |

| Government |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and Wholesale |

| Telecommunication and IT |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Model | Infrastructure as a Service (IaaS) | ||

| Platform as a Service (PaaS) | |||

| Software as a Service (SaaS) | |||

| By Organization Size | Small and Medium Enterprises (SME) | ||

| Large Enterprises | |||

| By Deployment Mode | API-based (Out-of-Band) | ||

| Forward Proxy | |||

| Reverse Proxy | |||

| Multimode / Hybrid | |||

| By End-User | Banking, Financial Services and Insurance (BFSI) | ||

| Education | |||

| Government | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Retail and Wholesale | |||

| Telecommunication and IT | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected size of the Cloud Access Security Brokers market by 2031?

The market is expected to reach USD 30.27 billion by 2031 on an 18.21% CAGR.

Why are organisations investing in CASB solutions now?

Regulatory mandates such as NIS2 and US Executive Order 14144, higher cyber-insurance premiums and rapid SaaS expansion are making CASB controls a prerequisite for compliance and risk reduction.

Which deployment model is growing fastest?

Multimode hybrid deployments combining inline and API controls show the highest CAGR at 21.75% through 2031.

Which region will see the quickest growth?

Asia Pacific is projected to record a 19.15% CAGR, driven by sovereign-cloud initiatives and new data-residency regulations.

How concentrated is vendor competition?

The market is moderately concentrated; the top five vendors hold about 60% of revenue, and active M&A continues to reshape the field.

What vertical will drive the next wave of demand?

Manufacturing is expected to grow at a 20.45% CAGR as factories integrate operational technology with cloud analytics, creating new security requirements.

Page last updated on: