Endoscopic Stricture Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

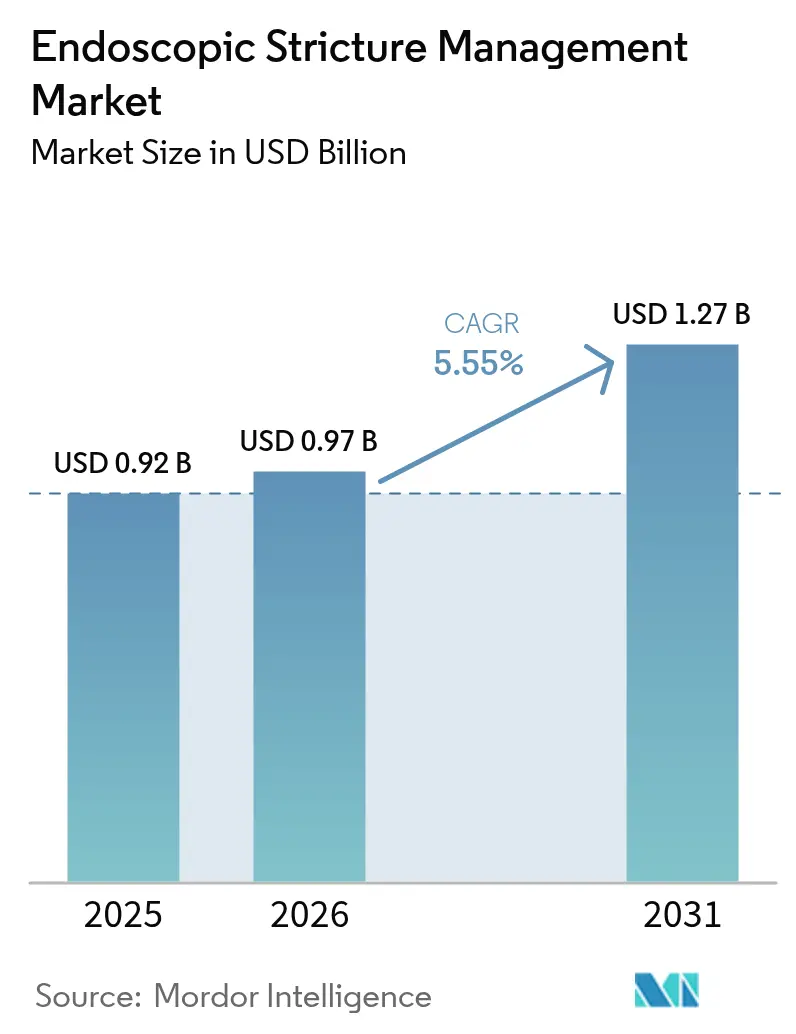

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

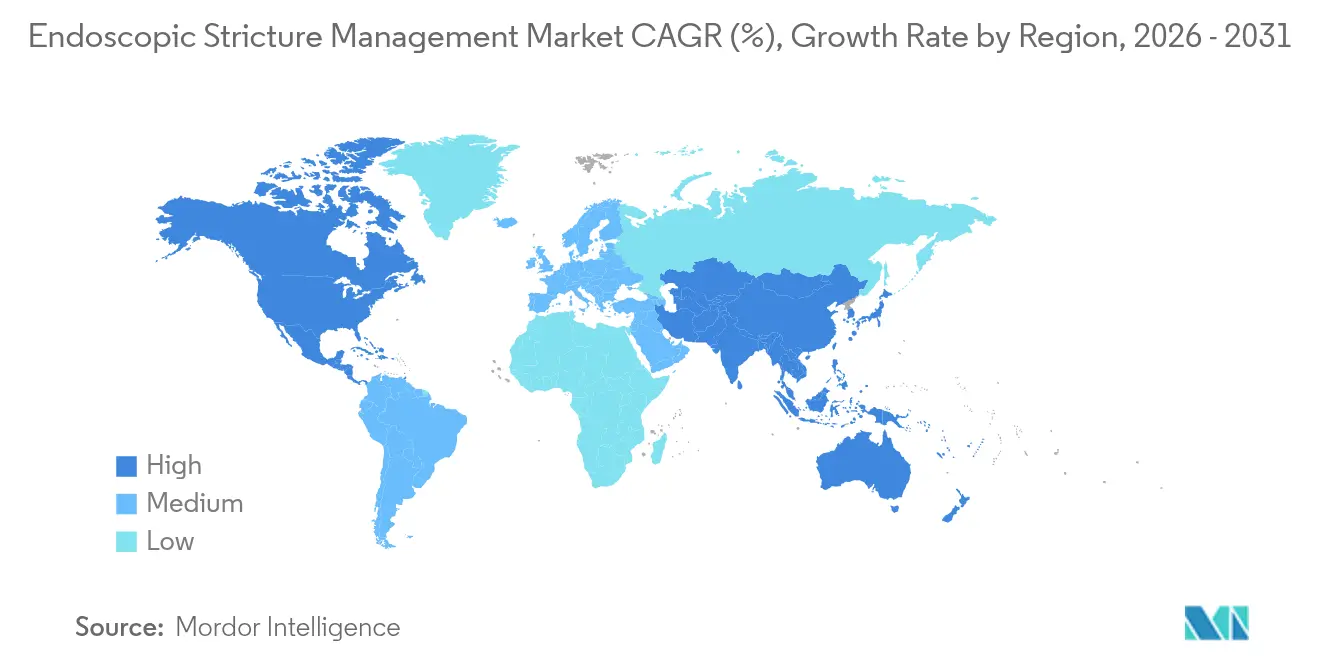

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

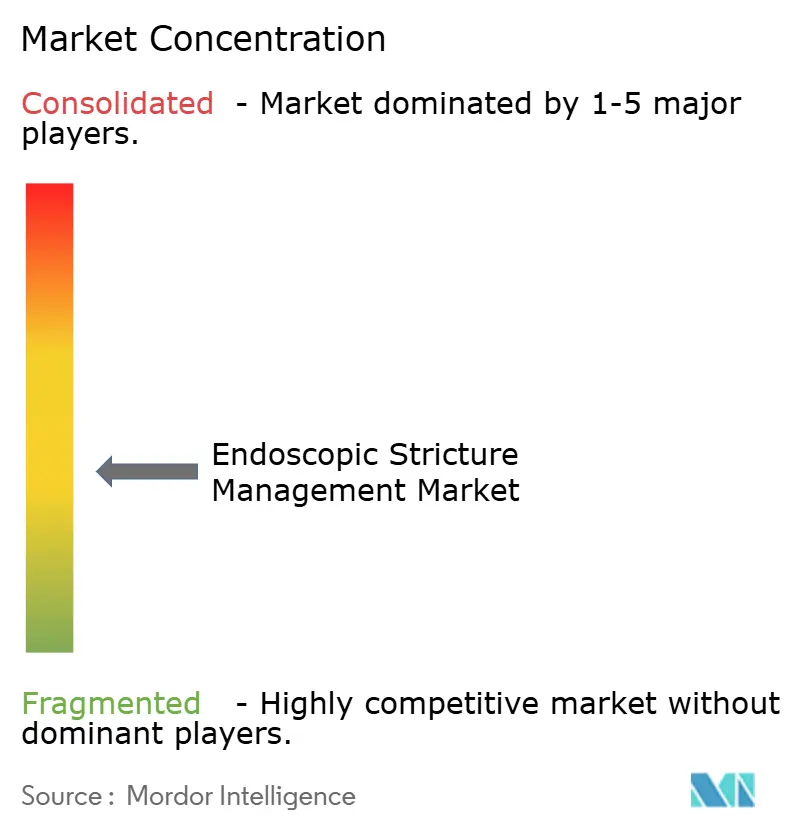

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Endoscopic Stricture Management Market Analysis by Mordor Intelligence

Endoscopic stricture management market size in 2026 is estimated at USD 0.97 billion, growing from 2025 value of USD 0.92 billion with 2031 projections showing USD 1.27 billion, growing at 5.55% CAGR over 2026-2031. Expanding outpatient capacity, rapid device innovation, and payer support for minimally invasive treatments are steering hospitals and physicians away from open surgery toward endoscopic solutions. Balloon dilators, drug-coated platforms, biodegradable stents, and lumen-apposing metal stents shorten recovery times and lower complication risks, which aligns with payer incentives to cut inpatient costs. A steady rise in gastrointestinal strictures among older adults keeps procedure volumes growing, while ambulatory surgical centers (ASCs) capture a rising share of cases once restricted to inpatient wards. Competitive intensity is building as major suppliers broaden portfolios, vertical integration gains momentum, and emerging companies secure investment for next-generation technologies [1]Karl Storz SE & Co. KG, "Acquisition of Asensus Surgical by KARL STORZ," karlstorz.com.

Key Report Takeaways

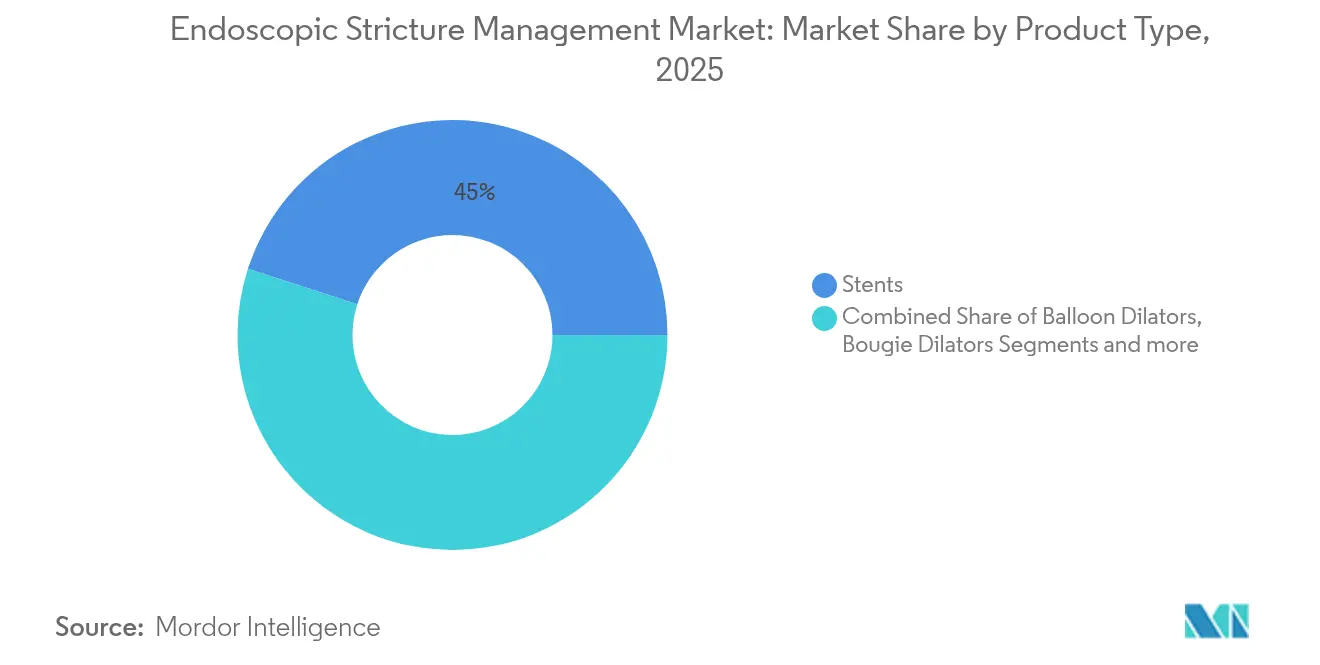

- By product type, stents led with 45.02% revenue share in 2025; balloon dilators are projected to expand at a 6.31% CAGR through 2031.

- By stricture location, esophageal procedures held 51.01% of the Endoscopic stricture management market share in 2025, while duodenal interventions are on track for a 6.29% CAGR through 2031.

- By end-user, hospitals accounted for 61.98% of the Endoscopic stricture management market size in 2025; ASCs are advancing at a 6.33% CAGR to 2031.

- By procedure setting, inpatient cases represented 69.12% share of the Endoscopic stricture management market size in 2025, whereas outpatient cases are rising at a 6.38% CAGR through 2031.

- By geography, North America led with 40.97% revenue share in 2025; Asia-Pacific is forecast to register the fastest 6.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Endoscopic Stricture Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing geriatric population & rising GI-stricture burden | +1.8% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Preference for minimally invasive endoscopic dilation | +1.5% | Global, led by developed markets | Medium term (2-4 years) |

| Continuous product innovation with multi-stage balloons & biodegradable stents | +1.2% | North America & EU, expanding into Asia-Pacific | Medium term (2-4 years) |

| Expanding reimbursement for outpatient stricture procedures | +0.8% | North America, selective EU markets | Short term (≤ 2 years) |

| Early clinical success of lumen-apposing metal stents | +0.6% | Global, led by North America & Europe | Medium term (2-4 years) |

| Emergence of patient-managed self-dilation protocols | +0.4% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population & Rising GI-Stricture Burden

Esophageal stricture prevalence reached 203.1 cases per 100,000 among commercially insured adults and 1,123.5 cases per 100,000 in Medicare beneficiaries, driving USD 1.39 billion in annual costs [2]Angela Z. Xue, "Prevalence and Costs of Esophageal Strictures in the United States," Clinical Gastroenterology and Hepatology, sciencedirect.com. Older patients often present with reflux-induced strictures or anastomotic scarring that require repeated dilations or stenting. Untreated strictures lead to malnutrition and aspiration, creating additional system costs. As longevity rises across developed economies, healthcare planners anticipate heavier reliance on endoscopic treatment pathways that cost less than surgical reconstruction yet deliver durable results.

Preference for Minimally Invasive Endoscopic Dilation

Endoscopic balloon dilation achieves 67.1% success in urethral strictures and improves maximum urinary flow, while drug-coated balloons show 77.8% freedom from re-intervention at two years versus 23.6% for standard therapy. Patient demand for fast recovery and lower pain dovetails with payer pressure to limit inpatient stays [3]Xiaoyu Li, "Balloon dilation for the treatment of male urethral strictures: a systematic review and meta-analysis," BMJ Open, bmjopen.bmj.com. Hospitals and ASCs invest in advanced scopes and dilation platforms, and younger gastroenterologists—trained heavily in therapeutic endoscopy—are driving faster adoption in daily practice.

Continuous Product Innovation: Multi-Stage Balloons & Biodegradable Stents

Five-year data from the ROBUST I trial show 58% functional success and 71.7% freedom from repeat intervention with paclitaxel-coated balloons for recurrent bulbar urethral strictures. Biodegradable stents remove the need for second-look removal procedures, while lumen-apposing metal stents (LAMS) achieve 97% technical success for pancreatic fluid collections and minimize migration risk. Venture backing is strong: Sotelix raised USD 1.7 million for therapeutic endoscopy, and Fractyl Health secured FDA Breakthrough Device Designation for its Revita system.

Expanding Reimbursement for Outpatient Stricture Procedures

The Centers for Medicare & Medicaid Services adjusted payment rules to encourage procedure migration from hospital outpatient departments to ASCs, prompting 21% projected volume growth through 2034 with gastroenterology a principal driver. Private payers mirror these moves, approving premium devices such as drug-coated balloons when total cost of care falls. Value-based contracts further reward providers who move appropriate cases to outpatient settings without readmissions.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & procedure costs | -1.1% | Global, acute in emerging markets | Medium term (2-4 years) |

| Shortage of trained interventional endoscopists | -0.9% | Global, severe in rural and developing regions | Long term (≥ 4 years) |

| Safety concerns over off-label LAMS use in benign strictures | -0.7% | Global, heightened in North America & EU | Short term (≤ 2 years) |

| Limited long-term data for drug-coated balloon approvals | -0.5% | Global, regulatory bottlenecks in key markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device & Procedure Costs

Premium-priced LAMS and drug-coated balloons exceed capital budgets in many emerging economies, and payers often hesitate to grant quick coverage when long-term savings remain unproven. Hospitals juggle needs across cardiology, oncology, and surgery, often delaying purchases of advanced endoscopy systems. Utilization management controls can restrict access, slowing the Endoscopic stricture management market in cost-sensitive regions.

Shortage of Trained Interventional Endoscopists

The European Society of Gastrointestinal Endoscopy mandates 250 supervised EUS procedures for competence, yet many programs lack volume and mentors. Rural areas worldwide struggle to attract specialists, forcing patients to travel to tertiary centers and inflating wait times. As experienced endoscopists retire faster than new fellows graduate, workforce gaps may widen through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stents Dominate While Balloons Accelerate

Stents controlled 45.02% of the Endoscopic stricture management market in 2025 owing to their established role in maintaining luminal patency when strictures are complex or malignant. Balloon dilators lead growth at a 6.31% CAGR thanks to drug-coated surfaces and controllable inflation profiles. The Endoscopic stricture management market size for stents is projected to expand steadily, yet balloons increasingly capture repeat procedures as physicians value their lower perforation risk. Boston Scientific’s CRE balloon platform improves fluoroscopic visibility, while Merit Medical’s Wrapsody stent extends use into dialysis access, signaling cross-specialty opportunity. Bougie dilators continue to decline as single-use economics and controlled dilation favor balloons. Drug-coated balloons incorporating paclitaxel showed 77.8% freedom from repeat procedure in the ROBUST III trial, encouraging physicians to adopt them in recurrent benign strictures. Biodegradable stents eliminate removal procedures, and LAMS address migration with wider flanges.

The emerging “others” category—incision devices, anti-scarring injectables, and AI-guided dilation platforms—remains a small slice but attracts venture interest. Suppliers design devices that fit both hospital and ASC workflows, focusing on reusability and lower per-case cost to widen adoption across income settings. As patent cliffs approach for early-generation metal stents, companies differentiate through coatings, delivery ergonomics, and evidence bundles that document real-world savings.

By Stricture Location: Esophageal Dominance Faces Duodenal Challenge

Esophageal cases held 51.01% share in 2025, reflecting reflux prevalence and post-surgical anastomotic scarring. The Endoscopic stricture management market share for esophageal disease stays high because benign strictures often require multiple dilations over a lifetime. Duodenal procedures, however, grow at a 6.29% CAGR through 2031 as improved imaging and device-assisted enteroscopy increase detection of small-bowel lesions. Olympus earned FDA clearance for its EZ1500 series scopes with extended depth-of-field optics, improving duodenal lesion visibility. Biliary strictures remain steady, treated mainly with stent placement.

Cross-specialty uptake in urology, hepatology, and colorectal surgery supports the “others” bucket, where urethral and pancreatic applications adopt balloon and stent know-how from gastroenterology. Location drives therapy choice: benign esophageal strictures prefer balloons first, while malignant obstructions move directly to metal stents. In Asia-Pacific, higher prevalence of biliary and duodenal strictures nudges R&D toward devices sized for narrower lumens common in that population set.

By End-user: Hospital Dominance Challenged by ASC Growth

Hospitals retained 61.98% market share in 2025 thanks to full ICU backup, multidisciplinary support, and the ability to handle emergency perforations. Yet ASCs grow at 6.33% CAGR as payers incent providers to move routine dilations and stent exchanges to lower-cost sites. The Endoscopic stricture management market size flowing through ASCs is expected to climb steadily to 2031. Site-neutral payment rules narrow reimbursement gaps and boost surgeon preference for ASC schedules that minimize after-hours staffing. Hospitals respond by opening hospital-owned ASCs or joint ventures. Physician offices and specialty clinics form the small “others” group, enabled by compact high-definition towers and single-operator cholangioscopes that fit outpatient rooms.

ASC workflows demand devices that are quick to set up, single-use where infection risk is high, and packaged with simple staff training. Manufacturers tailor balloon inflation systems with pre-set pressures and color-coded gauges for ASC technicians. Hospitals, meanwhile, invest in capital-intensive EUS towers and robotics for complex procedures, anchoring premium device sales in tertiary centers.

By Procedure Setting: Outpatient Surge Reshapes Care Delivery

Inpatient procedures still made up 69.12% of cases in 2025, reflecting case complexity, comorbidities, and the need for overnight observation. Outpatient volumes, however, are rising at 6.38% CAGR through 2031 as anesthesia protocols, hemostatic powders, and rapid-acting reversal agents reduce risk. Medicare data show ASCs treated 3.3 million beneficiaries in 2022 with USD 6.1 billion in spend, highlighting scale.

The Endoscopic stricture management market continually adapts: device makers shrink catheter profiles for same-day recovery, and remote monitoring platforms allow safe discharge. Hospitals keep the sickest patients, including those with variceal bleeding or complex strictures at high perforation risk. The “others” setting group—mainly extended-stay recovery centers—remains niche but may gain ground as bundled payments encourage one-stop episodes of care.

Geography Analysis

North America captured 40.97% of Endoscopic stricture management market revenue in 2025 and remains the technology bellwether. Medicare site-neutral rules and broad private payor alignment nurture outpatient migration, while strong fellowship pipelines ensure a deep bench of interventional endoscopists. Device makers often launch first in the United States to leverage early adopter clinics that generate pivotal data.

Asia-Pacific is forecast to lead growth with a 6.52% CAGR through 2031. China’s annual endoscopic ultrasound procedures rose from 207,166 in 2012 to 464,182 in 2019, revealing swift uptake of advanced tools even as per-capita usage trails developed nations. India rolled out AI-driven detection software that lifted adenoma detection rates in pilot sites, showing technology leapfrogging potential. Japan remains the region’s procedure volume leader, aided by universal coverage and public awareness campaigns that catch strictures earlier. Australia and South Korea invest in high-definition systems and medical tourism, luring regional patients.

Europe holds a mature yet slower-growing position. Rigorous training standards—250 supervised EUS cases for credentialing—uphold quality, but budget caps temper switching to premium DCBs and LAMS. Germany and the United Kingdom maintain strong hospital-based volumes, while Nordic countries push outpatient growth via bundled payments.

South America and the Middle East & Africa are emerging opportunity zones. Brazil’s unified procurement for public hospitals helps negotiate pricing, boosting stent access. South Africa leads sub-Saharan adoption through private-public hospital clusters, yet rural gaps remain. Tele-mentoring and modular endoscopy suites aim to solve workforce shortages in these regions.

Competitive Landscape

The Endoscopic stricture management market features moderate fragmentation. Boston Scientific, Olympus, and Cook Medical anchor global share with broad catalogs and KOL ties. They defend position through iterative upgrades—coatings, delivery ergonomics, and hybrid visualization—and by offering service bundles that smaller firms struggle to match. Mid-sized players such as Merit Medical and Conmed focus on niche balloons and ancillary tools, often partnering with distributors in emerging markets.

Vertical integration is accelerating. KARL STORZ acquired Asensus Surgical for USD 0.35 per share in 2024 to blend digital laparoscopy with endoscopy workflows, enhancing the LUNA robotic platform. In February 2025 Teleflex paid EUR 760 million for BIOTRONIK’s vascular intervention unit, adding drug-coated balloons and scaffold technology to its access portfolio. These moves aim to offer turnkey therapeutic pathways rather than single instruments.

Start-ups target white spaces: Sotelix raised USD 1.7 million for therapeutic endoscopy devices, and Fractyl Health secured breakthrough status for its Revita metabolic intervention system. AI-guided navigation, robotic manipulators, and personalized dilation plans form the next competitive frontier. Top players invest heavily in training platforms to lock in brand loyalty, while recurring-revenue service contracts cushion pricing pressure in commodity segments.

Endoscopic Stricture Management Industry Leaders

-

Boston Scientific Corporation

-

Merit Medical Systems

-

CONMED Corporation

-

Cook Medical LLC

-

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex announced acquisition of BIOTRONIK’s vascular intervention business for EUR 760 million, adding drug-coated balloons and a resorbable metallic scaffold to its portfolio.

- August 2024: KARL STORZ completed acquisition of Asensus Surgical for USD 0.35 per share, integrating robotic and digital solutions to strengthen the LUNA platform.

- April 2024: GIE Medical began enrollment in the PATENT-B study evaluating the ProTractX3 transluminal drug-coated balloon for chronic benign bowel strictures.

Global Endoscopic Stricture Management Market Report Scope

Endoscopic stricture refers to an abnormal narrowing or blocking of sections of a tract or canal due to the presence of a tumor or a scar. These strictures are usually treated with endoscopy, a minimally invasive medical method to investigate and operate procedures without making large incisions with the help of various dilation devices and stents.

The Endoscopic Stricture Management Market is Segmented by Type (Balloon Dilators, Stents, and Bougie Dilators), Application (Esophageal, Biliary, and Other Applications), End-user (Hospitals, Ambulatory Surgical Centers, and Other End-users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Balloon Dilators |

| Bougie Dilators |

| Stents |

| Others |

| Esophageal |

| Biliary |

| Duodenal |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Others |

| Inpatient |

| Outpatient |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Balloon Dilators | |

| Bougie Dilators | ||

| Stents | ||

| Others | ||

| By Stricture Location | Esophageal | |

| Biliary | ||

| Duodenal | ||

| Others | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Others | ||

| By Procedure Setting | Inpatient | |

| Outpatient | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Endoscopic stricture management market?

The market is valued at USD 0.97 billion in 2026 and is projected to reach USD 1.27 billion by 2031 at a 5.55% CAGR.

Which product segment is growing fastest?

Balloon dilators are the fastest-growing segment with a 6.31% CAGR through 2031, driven by drug-coated technology and lower per-procedure costs.

Why are ASCs gaining share in stricture management procedures?

Site-neutral reimbursement rules and patient demand for same-day discharge are pushing routine dilations and stent exchanges into ASCs, which operate at lower cost than hospitals.

Which region shows the strongest growth potential?

Asia-Pacific is forecast for the quickest expansion at 6.52% CAGR due to rising procedure volumes in China, India, and Southeast Asia.

What are the main restraints on market growth?

High device prices, shortage of trained interventional endoscopists, and limited long-term data for innovative coatings and stents slow adoption, especially in emerging markets.

How fragmented is the competitive landscape?

The market is moderately fragmented with top companies controlling just over half of global revenue, leaving room for start-ups to disrupt niches such as AI-guided navigation and biodegradable stents.

Page last updated on: