Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The RF Tunable Filter Market Report is Segmented by Product Type (MEMS-Based, and More), Frequency Range (Low, and More), Tuning Mechanism (Electronic, Magnetic, and More), Integration Level (Discrete, and More), Channel Bandwidth (Narrowband, and More), Application (Avionics, Electronic Warfare, and More), End-Use Industry (Telecom Operators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

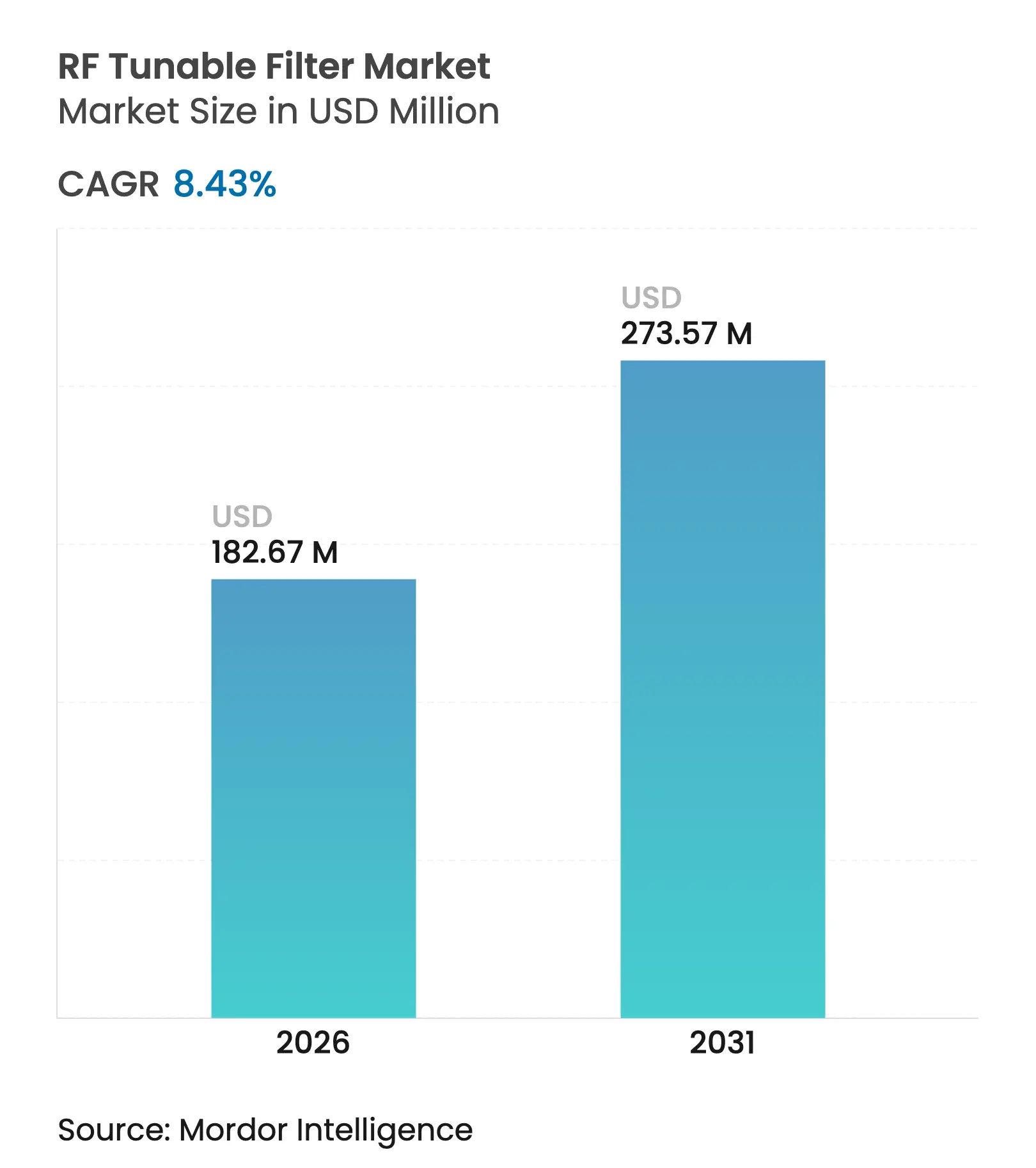

| Market Size (2026) | USD 182.67 Million |

| Market Size (2031) | USD 273.57 Million |

| Growth Rate (2026 - 2031) | 8.43 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The RF tunable filter market size is expected to grow from USD 168.47 million in 2025 to USD 182.67 million in 2026 and is forecast to reach USD 273.57 million by 2031 at 8.43% CAGR over 2026-2031. Commercial roll-outs of multi-band 5G and early 6G devices, together with increasingly dynamic spectrum policies, are moving tunable filters from optional add-ons to core elements of every new RF front-end. Network operators are demanding real-time, software-driven selectivity to limit interference when carrier aggregation and unlicensed spectrum allocations overlap. At the same time, defense and satellite customers continue to specify higher linearity and radiation tolerance, keeping premium price points for performance-led designs. Integration trends now favor system-in-package layouts that shrink size and bill-of-materials while preserving wide tuning ranges, a direction that will shape the competitive agenda throughout the decade.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Driver Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | (~) % Impact on CAGR Forecast:(~) % Impact on CAGR Forecast | Geographic Relevance:Geographic Relevance | Impact Timeline:Impact Timeline |

Surge in Reconfigurable RF-Front Ends for Multi-Band 5G/6G Smartphones Surge in Reconfigurable RF-Front Ends for Multi-Band 5G/6G Smartphones | +2.1% | Global, with concentration in Asia-Pacific manufacturing hubs | Medium term (2-4 years) | |||

Rapid Deployment of LEO Satellite Constellations Requiring Agile Filtering Rapid Deployment of LEO Satellite Constellations Requiring Agile Filtering | +1.8% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) | |||

Escalating Defense EW and Radar Modernization Budgets in United States and Asia Escalating Defense EW and Radar Modernization Budgets in United States and Asia | +1.5% | North America, Asia-Pacific core markets | Medium term (2-4 years) | |||

Miniaturization of mmWave IoT and Wearable Devices Miniaturization of mmWave IoT and Wearable Devices | +1.3% | Global, with manufacturing concentration in Asia | Short term (≤ 2 years) | |||

Regulatory Push for Dynamic Spectrum-Sharing (e.g., CBRS in the U.S.) Regulatory Push for Dynamic Spectrum-Sharing (e.g., CBRS in the U.S.) | +1.0% | North America, with spillover to Europe and Asia-Pacific | Long term (≥ 4 years) | |||

Investments in Cloud-Native, Software-Defined Radio Infrastructure Investments in Cloud-Native, Software-Defined Radio Infrastructure | +0.9% | Global, with early deployment in developed markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Reconfigurable RF Front-Ends for Multi-Band 5G/6G Smartphones

Smartphone makers now ship flagships that must cover more than 40 bands, forcing a shift from fixed filters to reconfigurable architectures. Murata’s mass-produced voltage-tunable parts let a single filter replace multiple discrete units, saving board space and easing design complexity. Research from the University of Pennsylvania on YIG filters spanning 3.4-11.1 GHz confirms technical feasibility for broadband handset usage. Collaboration between filter specialists and module vendors is accelerating so modules can ship with firmware hooks that retune passbands on demand. These partnerships shorten design cycles for phone OEMs and will entrench tunable filters in every premium handset SKU over the next product generation.

Rapid Deployment of LEO Satellite Constellations Requiring Agile Filtering

LEO operators targeting global IoT coverage need filters that adapt to Doppler shifts and shared spectrum scenarios. Studies on LPWAN links for satellites underline tighter selectivity needs when thousands of spacecraft reuse channels across latitude bands. Filters also double as sensing elements in combined radar-communications payloads, a capability highlighted in Huawei’s research roadmap for converged satellite systems file.[1]Huawei Research, “HUAWEI RESEARCH Issue 5,” file.huawei.com Electronics that retune in milliseconds will remain essential as satellite fleets expand and cross-link traffic intensifies.

Escalating Defense EW and Radar Modernization Budgets

U.S. and Asian defense agencies are funding software-defined radar that reshapes passbands in real time to avoid jammers Japan’s FPS-3ME exports to the Philippines and India’s USD 4 billion Voronezh deal confirm similar momentum in Indo-Pacific security programs. Defense primes therefore demand filters that hold phase coherency across wide temperature swings and high power levels. The spending cycle secures long-term volume for high-performance designs that carry premium pricing

Miniaturization of mmWave IoT and Wearable Devices

Green wearable sensors integrating RF harvesting prove that gain of 14.1 dB and 65% bandwidth are achievable in compact form factors. Ultra-small lithium-niobate filter chips reach millimeter-wave ranges while occupying sub-mm² footprints. Automotive V2X boards now ship dual-band filters with >38 dB rejection but PCB-friendly layouts. Such milestones confirm that miniaturization does not have to sacrifice performance and open high-volume consumer channels for the RF tunable filter market

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Yield and Reliability Challenges in Volume MEMS/BST Manufacturing Yield and Reliability Challenges in Volume MEMS/BST Manufacturing | -1.20% | Global, with concentration in Asia-Pacific manufacturing centers | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.20% | Geographic Relevance:Global, with concentration in Asia-Pacific manufacturing centers | Impact Timeline:Short term (≤ 2 years) |

Thermal Drift and Linearity Issues at High Power Base-Station Levels Thermal Drift and Linearity Issues at High Power Base-Station Levels | -0.80% | Global, affecting infrastructure deployments | Medium term (2-4 years) | |||

IP and Patent Licensing Barriers for Start-ups IP and Patent Licensing Barriers for Start-ups | -0.60% | Global, with higher impact in North America and Europe | Medium term (2-4 years) | |||

Lengthy Qualification Cycles in Aerospace and Defense Lengthy Qualification Cycles in Aerospace and Defense | -0.40% | North America, Europe, with emerging impact in Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Yield and Reliability Challenges in Volume MEMS/BST Manufacturing

Wafer-level packaging warpage and PIM stability across -10 °C to 85 °C complicate large-scale output.[2]Frontiers in Electronics, “Warpage in Wafer-Level Packaging,” frontiersin.org Lower yields raise ASPs and curb adoption in cost-sensitive handsets. Moves to 200 mm lines promise economies of scale yet introduce new process unknowns that fabs must resolve before capacity ramps fully.

Thermal Drift and Linearity Issues at High Power Base-Station Levels

Active antenna arrays require phase error below 10° and gain error under 0.5 dB, targets that today’s tunable filters struggle to keep across temperature swings.[3]IEEE, “Achieving Phase Coherency and Gain Stability,” ieeexplore.ieee.org Magnetic biasing circuits that consume zero static power mitigate thermal loads yet add design complexity. Infrastructure vendors hold off volume commitments until field trials verify linearity under worst-case power conditions.

By Product Type: MEMS Technology Leads Innovation

MEMS-based filters held the largest revenue at 34.62% in 2025, illustrating how silicon-compatible processing aligns with handset production volumes. This share positions MEMS as the volume backbone of the RF tunable filter market. BST variants, propelled by advances in ferroelectric thin films, log the fastest 8.86% CAGR and will pressure MEMS suppliers on tuning range. YIG and cavity designs stay relevant for defense radar because they deliver isolation above 70 dB, meeting stringent electronic-warfare specifications. Liquid-crystal filters are moving from lab to orbit after passing space qualification tests.

Digital and software-defined architectures widen the addressable customer base. NXP’s LA9310 shows how programmable baseband silicon can host filtering logic that eliminates separate FPGAs. MEMS-inside-CMOS processes bring under-1 pF switching elements on die with RF power handling, raising hopes that wafer-level costs will drop as CMOS fabs adopt the flow. As three-dimensional acoustic resonators gain traction, a single die could soon deliver multiband coverage that today needs several discrete parts. Competitive advantage will hinge on whose technology balances high Q, low loss and consumer-grade price points first.

Note: Segment shares of all individual segments available upon report purchase

By Frequency Range: mmWave Segment Drives Growth

High-frequency 3-30 GHz devices commanded 41.15% of the RF tunable filter market share in 2025 due to 5G mid-band deployments. Bands above 30 GHz add a 10.32% CAGR, positioning mmWave as the fastest-rising slice of the RF tunable filter market. Prototype acoustic filters hitting 50 GHz with 3.3 dB insertion loss prove that piezoelectric solutions can keep pace with silicon scaling. Meanwhile, THz-ready metasurface filters covering 240 GHz show the research trajectory for 6G.

Millimeter-wave production brings layout tolerance and package parasitic headaches. Vendors respond using integrated microstrip and thin-film lines that shrink total footprint while maintaining high rejection Bulk acoustic wave resonators on aluminum scandium nitride now deliver Q above 230 at 17-18 GHz and electromechanical coupling near 12%. When these lab results reach stacked wafer lines, the RF tunable filter market size for mmWave infrastructure will expand quickly as base stations migrate beyond 40 GHz.

By Tuning Mechanism: Electronic Control Dominates

Electronically tuned parts contributed 68.10% of revenue in 2025, underscoring buyer preference for rapid, software-driven agility. Mechanical solutions still attract 8.65% CAGR where micro-positioned cavities guarantee ultra-high linearity. Magnetic designs hold niches in harsh defense environments where electronic noise susceptibility must be minimized. Research on SOI RFIC filters shows input IP3 near 45 dBm with 5-7 dB loss, confirming that silicon platforms can meet phased array needs.

Memristor-controlled N-path filters demonstrate bandwidth tuning from 1.5 kHz to 2 kHz at 1 MHz, validating fine-grained electronic control for low-power IoT radios. Continuous tuning designs that avoid mode hopping remain a field priority, especially for mission-critical radios that cannot tolerate drops. Zero static power magnetic bias circuits add energy efficiency yet must prove reliability in volume. Suppliers that master calibration algorithms alongside hardware will gain share because OEMs want turnkey modules, not discrete parts that require extra RF expertise.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

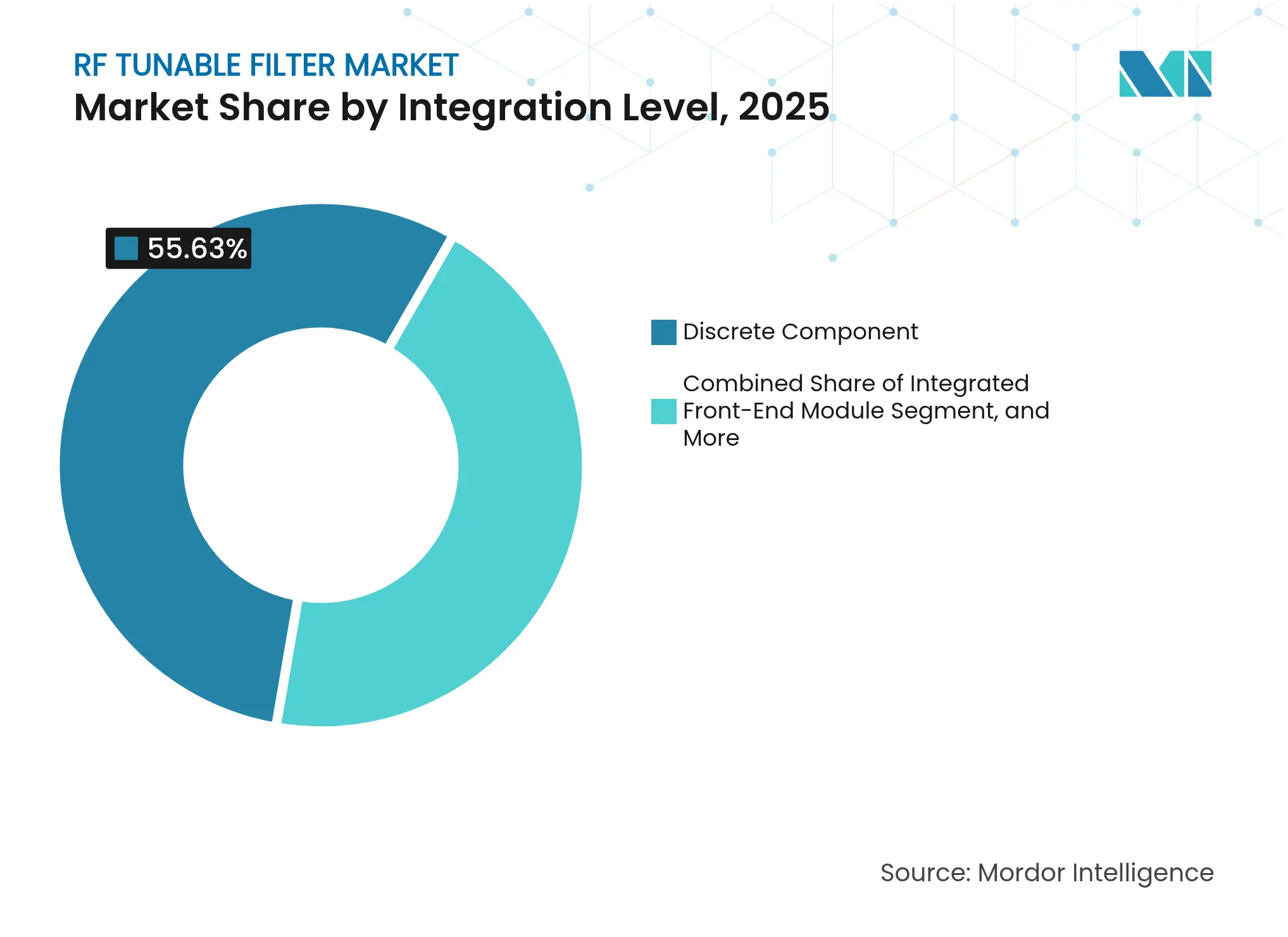

By Integration Level: System Integration Accelerates

Discrete filters still held 55.63% share of the RF tunable filter market size in 2025, a reminder that retrofit programs and test racks prefer standalone parts. System-in-package solutions post a 9.74% CAGR as phone OEMs chase smaller footprints and lower BOM counts. Damascene-electrode resonators on suspended lithium niobate prove multi-frequency capability with minimal external elements. Tower Semiconductor’s 300 mm RFSOI flow shows that Wi-Fi 7 FEMs can integrate complete pass-bands on a single die.

Miniaturized BAW filters using high-Q active inductors hit Q of 4,000 from 2 GHz to 7 GHz while fitting 0.83 × 0.75 mm² footprint. As foundries roll out 22FDX nodes, RF and digital may coexist on one substrate, simplifying automotive and IoT boards globalfoundries.com. This integration wave will lift the RF tunable filter market because every new front-end module refresh can bundle a tunable pass-band without adding extra PCB real estate.

Note: Segment shares of all individual segments available upon report purchase

By Channel Bandwidth: Wideband Applications Expand

Narrowband filters under 5% FBW supplied 47.55% revenue in 2025 for applications that value high selectivity. Yet ultra-wideband devices post a 9.18% CAGR as 5G NR, Wi-Fi 7 and future 6G profiles demand aggregated carrier widths. SV-SAW filters on LiNbO₃ substrates now reach coupling coefficients near 9% with Q above 600, enabling wideband operation for 6G cm-wave links. Tri-layer thin-film arrangements at 19.3 GHz deliver 8.5% FBW and 49 dB close-in rejection, a performance set once limited to cavity parts.

Frequency-selective surfaces covering the S-C band achieve 108.7% FBW while staying angularly stable, opening low-cost routes for large-area apertures in smart surfaces. Compact bias-controlled filters now span 1.1-3.1 GHz with a single diode network. As carrier aggregation scales, demand for tunable wideband topologies will outpace fixed units and enlarge the RF tunable filter market.

By Application: Infrastructure Leads, 5G/6G Accelerates

Wireless infrastructure maintained the highest 27.15% share in 2025 because macro cells and small cells need agile selectivity when operators refarm spectrum. 5G/6G network equipment grows 10.86% annually, making it the most attractive slice of the RF tunable filter market. Electronic warfare remains stable as defense buyers refresh jamming-resistant radios. Satellite communications lean on agile filters to cope with beam hopping across multiple gateways.

Test and measurement vendors integrate tunable filters inside vector network analyzer plug-ins that validate S-parameters and phase noise in 6G prototypes. AI-assisted test setups promise 20% faster calibration cycles, helping vendors offset longer waveguide lead times. Shipboard and avionics radios request ruggedized pass-bands that retain flat group delay across pressure swings. Because each new infrastructure generation widens instantaneous bandwidth, tunability is a must-have rather than a nice-to-have for OEMs.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End-Use Industry: Automotive Emerges as Growth Driver

Telecom operators bought 37.88% of units in 2025, underpinning macrocell densification. Automotive ranks as the quickest 9.29% CAGR segment, spurred by V2X. The V2N2X service opportunity could exceed USD 20 billion by 2030, implying steep filter volume upside. Military projects keep revenue steady with stringent qualification hurdles that defend margins.

Aerospace customers such as Teledyne e2v deliver radiation-hardened LNAs that pair with tunable filters inside space payloads. Large-scale V2X test beds already prove dual-band filters can survive urban canyon multipath. Industrial IoT gateways embrace RF harvesting so sensors can self-power small tuning elements. The upshot is that each vertical market reinforces a different value driver, enlarging total addressable demand for the RF tunable filter market.

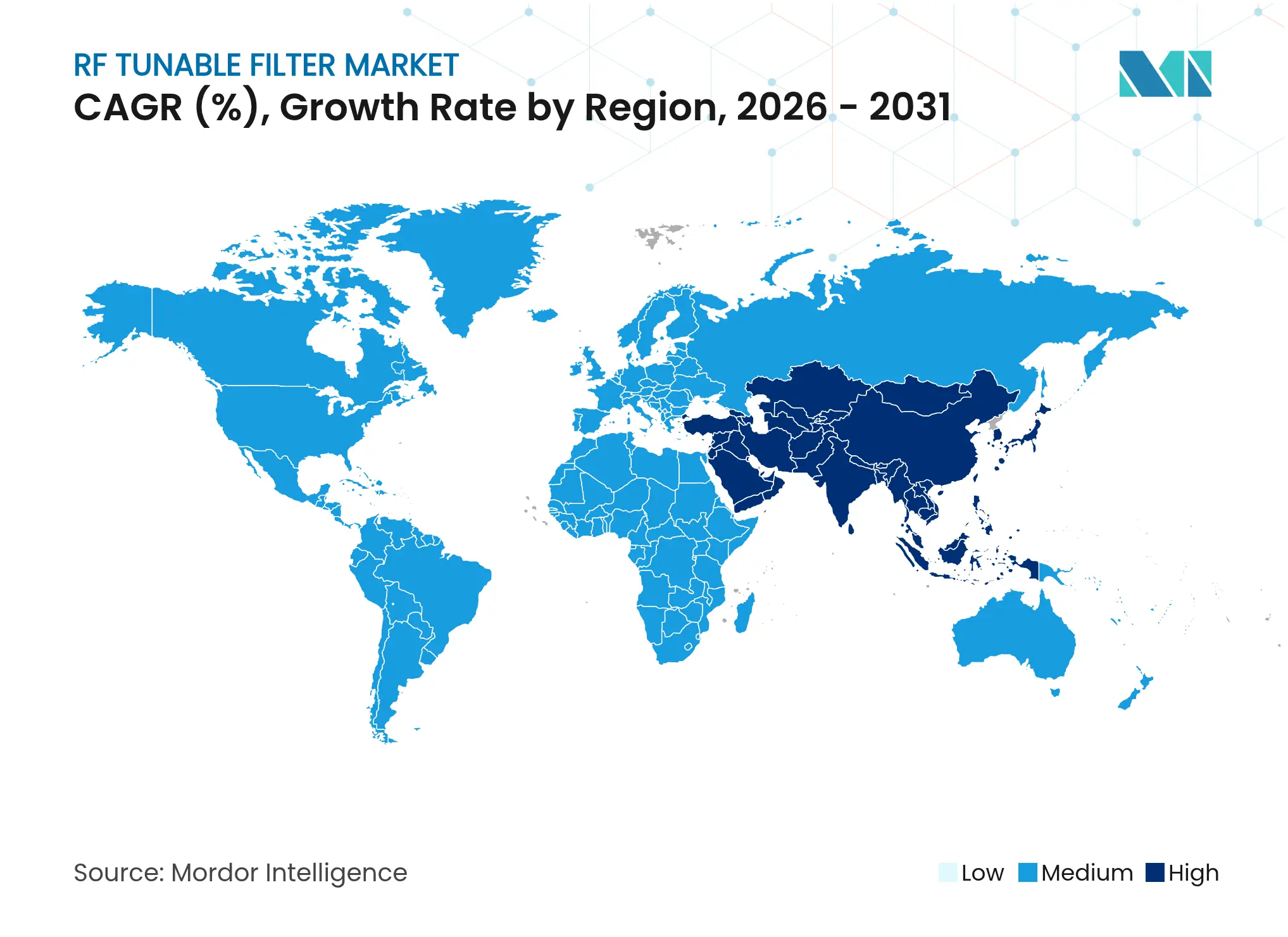

North America led with 32.10% revenue in 2025 thanks to robust defense budgets and the swift roll-out of 5G mid-band sites. CBRS usage jumped by 270,621 new devices through July 2024, with rural nodes taking 67.5% of deployments, highlighting demand for dynamic spectrum sharing filters. The U.S. Advanced Dynamic Spectrum Sharing demo in the 3.1-3.45 GHz band further pushes the RF tunable filter market toward software-defined operations. Government-funded 6G testbeds add to early purchase orders for terahertz-ready pass-bands.

Asia-Pacific logs the highest 9.05% CAGR to 2031. China approved more than 350 semiconductor projects in 2024, driving local demand for GaN and SiC RF parts that integrate tunable filters. Japan’s radar exports and India’s USD 4 billion long-range radar plan feed sustained defense orders. China’s 14th Five-Year Plan links 5G expansion to cloud data centers, a policy that lifts shipments of small-cell FEMs containing tunable filter dies.

Europe posts steady growth as its space agencies qualify liquid-crystal-based filters for the Heinrich Hertz satellite mission. Automotive OEMs in Germany and France adopt dual-band V2X modules that rely on agile filtering to share 3.5 GHz and 5.9 GHz bands. Ongoing electronic-warfare upgrades across NATO members support demand for high-linear YIG parts. Sustainability mandates push operators to seek filters with lower insertion loss, linking energy savings to carbon targets. The combination of aerospace innovation and automotive connectivity keeps European buyers active in the RF tunable filter market.

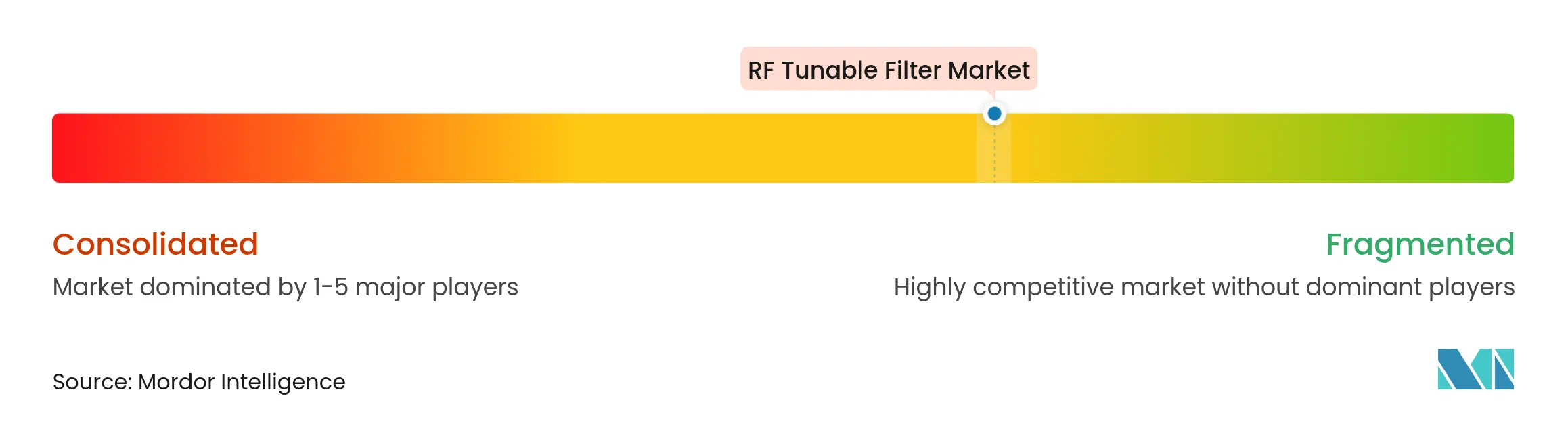

Market Concentration

The RF tunable filter market remains moderately fragmented. Incumbents such as Qorvo, Murata and Analog Devices compete against specialists including Akoustis, Resonant and several MEMS start-ups. M&A reshapes the field: Qorvo’s planned purchase of Anokiwave enhances beamforming depth while onsemi’s USD 115 million acquisition of Qorvo’s SiC JFET assets broadens power portfolios. Keysight’s forced divestiture of Spirent channel emulation assets shows regulators scrutinize concentration in adjacent RF test lines.

Technology leadership hinges on material science. MEMS-inside-CMOS promises cost drops once reliability surpasses 3 billion switching cycles. BST suppliers invest in 200 mm tooling to match handset die sizes. Litigation also shapes positioning: Qorvo secured USD 38.5 million in damages from Akoustis, underlining how patents protect differentiation. Start-ups win design-ins by offering plug-and-play software controls that reduce OEM integration effort.

Strategic alliances accelerate time-to-market. Tower Semiconductor and Broadcom co-develop Wi-Fi 7 FEMs, pushing integrated tunable filter dies onto a 300 mm RFSOI platform. GlobalFoundries and NXP tie up on 22FDX nodes for automotive that merge RF and logic on one wafer. Suppliers refine supply-chain resilience by dual-sourcing wafers and packaging in multiple geographies to hedge geopolitical risk. As integration deepens, competition will shift from discrete component pricing to system-level value propositions, pushing the RF tunable filter market toward higher entry barriers.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The RF Tunable Filter market involves the development and deployment of filters that can dynamically adjust their frequency response to select or reject specific frequency bands. These filters are essential for optimizing signal quality and efficiency in communication systems. They are widely used in applications such as 5G networks, wireless communication, aerospace, defense, and IoT devices.

The RF Tunable Filter Market is Segmented by product type (mems-based RF tunable filters, liquid crystal-based RF tunable filters, barium strontium titanate (BST)-based RF tunable filters, digital RF tunable filters, and other product type), frequency range (low frequency, medium frequency, high frequency, ultra high frequency), tuning mechanism (electronic, magnetic, mechanical), application (avionics & shipboard communication systems, electronic warfare systems, military radio systems (vehicular mount), satellite communication systems, test & measurement equipment, wireless communication infrastructure, 5g network equipment, other applications), end-use industry (telecom operators, military & defense, electronics, aerospace, automotive, and other end-use industries), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East And Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.