Privacy Filters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

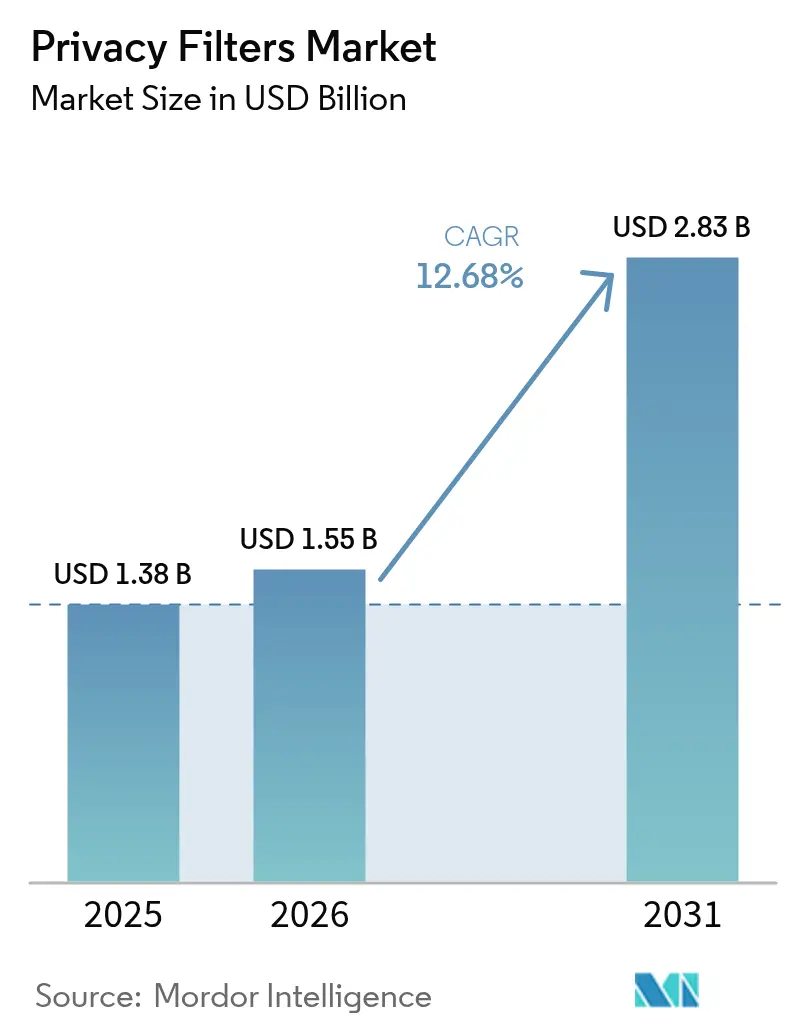

| Market Size (2026) | USD 1.55 Billion |

| Market Size (2031) | USD 2.83 Billion |

| Growth Rate (2026 - 2031) | 12.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

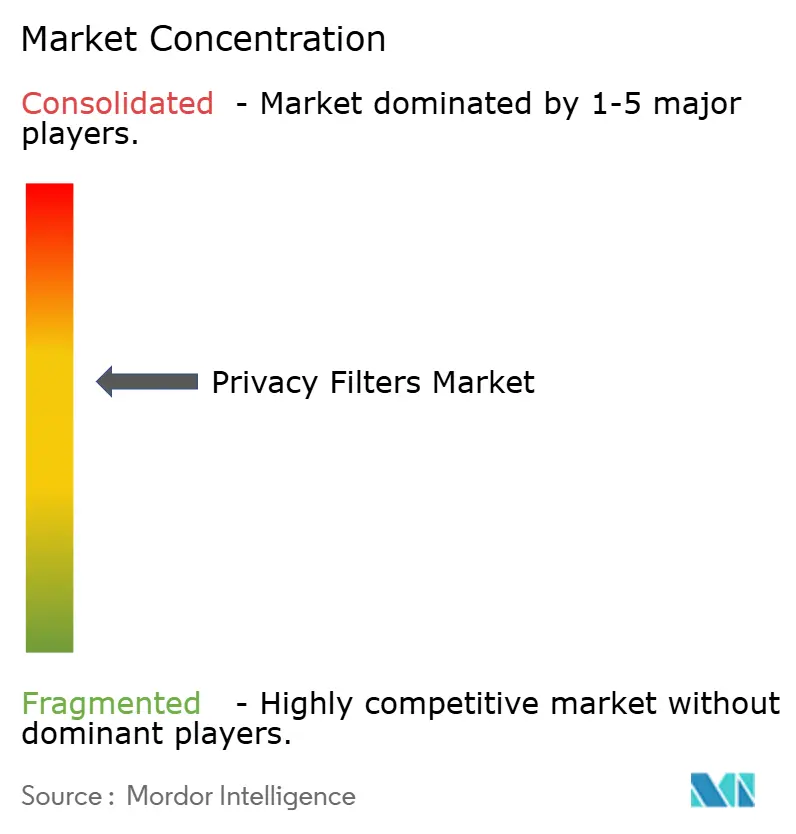

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Privacy Filters Market Analysis by Mordor Intelligence

The privacy filters market size is expected to grow from USD 1.38 billion in 2025 to USD 1.55 billion in 2026 and is forecast to reach USD 2.83 billion by 2031 at 12.68% CAGR over 2026-2031. Heightened regulatory scrutiny, increasing adoption of hybrid work, and stable commercial device shipments are converging to shift privacy filters from optional accessories to mandated controls in corporate governance frameworks. Enterprises now view visual data leakage as a compliance breach that can result in fines, reputational damage, and contract penalties. Healthcare upgrades to electronic health-record workstations, defense interest in switchable electrochromic panels, and original equipment manufacturer (OEM) integration strategies further expand the privacy filters market by embedding optical security at the hardware level. Competitive positioning favors brands with proprietary microlouver or nanostructure film expertise; however, regional fragmentation persists, as online marketplaces enable low-cost entrants.

Key Report Takeaways

- By product type, 2-way privacy filters captured a 49.10% market share of the privacy filters market in 2025, whereas 4-way privacy solutions are expected to advance at a 13.54% CAGR through 2031.

- By material technology, microlouver film filters captured a 60.73% market share of the privacy filters market in 2025, whereas Nanotechnology-Based Filters are expected to advance at a 13.35% CAGR through 2031.

- By device size, the 15-24 inch screens category accounted for a 54.20% market share of the privacy filters market in 2025, and screens above 24 inches screens are expected to expand at a 13.28% CAGR through 2031.

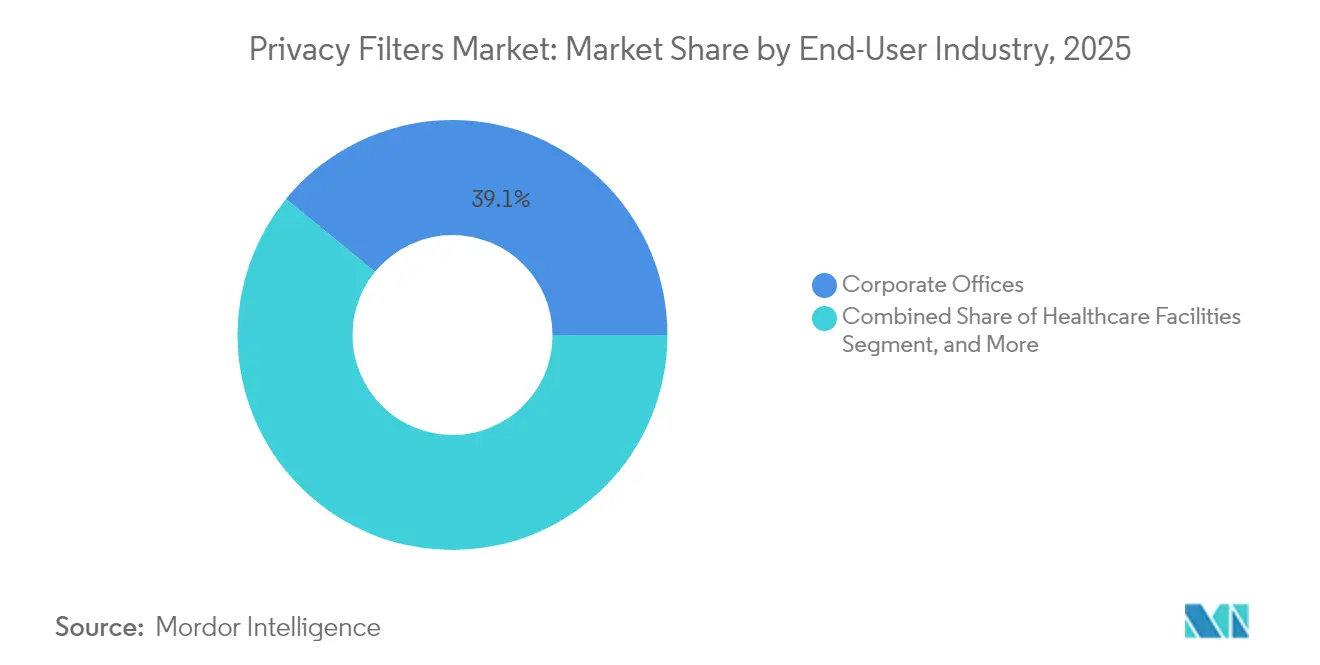

- By end-user industry, corporate offices led with 39.10% market share of the privacy filters market in 2025, while healthcare facilities are forecast to post a 13.58% CAGR through 2031.

- By distribution channel, online retail held a 45.00% market share of the privacy filters market in 2025; however, direct OEM integration is projected to grow at a 13.18% CAGR through 2031.

- By geography, North America captured a 33.20% market share of the privacy filters market in 2025, whereas the Asia Pacific is expected to advance at a 13.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Privacy Filters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Data Privacy Regulations in Corporate Environments | +2.8% | Global, with enforcement concentration in North America and EU | Medium term (2-4 years) |

| Rising Remote and Hybrid Working Trends | +2.3% | Global, particularly North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Increasing Laptop and Tablet Shipments Globally | +1.9% | Global, with commercial segment growth in Asia-Pacific and North America | Medium term (2-4 years) |

| Expanding Healthcare IT Investments | +1.7% | North America and Europe core, spillover to Middle East and Asia-Pacific | Medium term (2-4 years) |

| Integration of Privacy Filters into OEM Display Manufacturing Lines | +1.4% | Global, led by manufacturing hubs in China, Taiwan, South Korea | Long term (≥ 4 years) |

| Adoption of Smart Electrochromic Privacy Technologies for Defense Applications | +1.2% | North America, Europe, Middle East defense sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Data Privacy Regulations in Corporate Environments

European Union regulators imposed fines of EUR 4.1 billion (USD 4.4 billion) in 2024 for GDPR violations, with 18% of cases involving visual data exposure. The U.S. Federal Trade Commission revised the Gramm-Leach-Bliley Safeguards Rule to require documented controls against screen eavesdropping.[1]Federal Trade Commission, “FTC Announces Final Amendments to Safeguards Rule,” ftc.gov Canada, Mexico, and UAE authorities enacted parallel mandates, prompting multinational firms to adopt privacy filters across global offices for audit uniformity. Procurement teams now list optical screens alongside encryption and multifactor authentication in security budgets. This regulatory alignment keeps the privacy filters market on a steep adoption curve as fines escalate and audit cycles shorten.

Rising Remote and Hybrid Working Trends

Hybrid work blurs the perimeter; employees handle sensitive data in cafes, on trains, and in shared spaces. Screen exposure in public venues heightens the risk, yet only one-third of employers supply visual privacy accessories, creating a secondary demand wave from staff who self-purchase. Online retail fulfills these fragmented orders, sustaining 45.63% channel share in 2024. Airlines, rail operators, and hospitality chains have begun adding embedded privacy panels to seat-backs and lobby kiosks, demonstrating how mobility expands the privacy filters market beyond the traditional desk environment.

Increasing Laptop and Tablet Shipments Globally

Commercial laptop refreshes stabilized in 2024, with a 3% uptick in enterprise procurement despite softer consumer sales. Each new corporate device typically ships with a security toolkit that now includes a privacy screen, turning hardware lifecycle management into a recurring revenue engine for aftermarket vendors. Tablets used in healthcare, retail, and field services are increasingly specifying touch-screen-compatible privacy films to comply with data-use policies defined in sector guidelines issued by the HHS in 2024.[2]U.S. Department of Health and Human Services, “HIPAA Security Rule Guidance,” hhs.gov Penetration in emerging economies remains low, positioning Asia-Pacific and Latin America as greenfield territories once local data-protection acts mature.

Expanding Healthcare IT Investments

Hospitals invested USD 224 billion in IT in 2024, funding the expansion of electronic health records, telehealth, and cybersecurity upgrades. HIPAA technical-safeguard guidance explicitly calls for workstation privacy in shared clinical zones. Procurement managers now bundle privacy filters with endpoint-security suites, replacing ad-hoc buys with multiyear service contracts that cover installation, screen calibration, and lifecycle recycling. Aging populations in North America, Europe, and East Asia are driving the construction of new clinics that incorporate privacy screens at the blueprint stage, solidifying healthcare as the fastest-growing vertical in the privacy filters market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Desktop Monitor Refresh Cycles in Developed Markets | -1.6% | North America and Western Europe | Short term (≤ 2 years) |

| Price Sensitivity Among Consumer Buyers | -1.3% | Global, acute in price-conscious markets of South Asia, Africa, Latin America | Short term (≤ 2 years) |

| Compatibility Challenges with Curved and Foldable Displays | -0.9% | Global, concentrated in premium consumer segments | Medium term (2-4 years) |

| Environmental Concerns Over Disposal of Polycarbonate-Based Filters | -0.7% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Desktop Monitor Refresh Cycles in Developed Markets

Extended monitor lifespans cut replacement-trigger events that historically drove privacy-filter sales, especially for screens larger than 24 inches. Organizations prioritizing laptops for mobile teams defer desktop rollouts, shrinking the immediate addressable base. Vendors respond with retrofit kits and magnetic frames aimed at aging fleets; however, the structural tilt toward mobile devices tempers growth in the legacy segment of the privacy filter market.

Price Sensitivity Among Consumer Buyers

E-commerce marketplaces showcase generic privacy screens priced up to 60% below premium brands, eroding margins and diluting differentiation. Budget-focused shoppers rarely value antimicrobial coatings, ISO ergonomic certification, or extended warranties. This dynamic forces established vendors to emphasize enterprise and healthcare accounts while trimming consumer SKU counts. Persistent cost competition is expected to weigh on average selling prices even as unit volumes rise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: 4-Way Filters Accelerate in Collaborative Spaces

4-way designs enable omnidirectional shielding, meeting the demands of open-plan offices, trading floors, and public kiosks. The privacy filters market size for 4-way products is poised to expand rapidly because viewing angles from all sides require protection. In 2025, two-way models still accounted for 49.10% of revenue, yet their dominance is waning as hot desking grows. Vendors differentiate through touch-screen compatibility and blue-light reduction coatings that preserve image brightness while meeting ergonomic norms.

Electrochromic implementations, though currently niche, reduce attachment friction and support instant toggling between collaboration and privacy modes. The defense and finance sectors are early adopters, validating premium price points that reach three times the cost of conventional units. As OEMs embed microlouver or electrochromic layers at panel assembly, aftermarket clip-on demand is expected to shift toward specialized use cases rather than broad fleet coverage, reshaping future channel mix in the privacy filters market.

By Material Technology: Nanostructures Challenge Microlouver Leadership

Microlouver film, underpinned by 3M’s proprietary light-control technology, captured 60.73% revenue in 2025. It remains the benchmark for clarity versus the trade-off of dimming. However, nanostructure metasurfaces demonstrated 30% thickness reduction while sustaining contrast, an advantage for ultrathin laptops and foldables. Nanotech adoption, with a forecast near 13.35% CAGR, promises lighter devices and simplified recycling pathways, addressing polycarbonate waste concerns highlighted in the EU Circular Economy Action Plan.

Electrochromic polymers introduce dynamic opacity control but also pose disposal issues related to circuitry. Material selection now intertwines with environmental policy; bio-based polycarbonates are attracting European buyers seeking to comply with extended producer responsibility directives. Such shifts create opportunities for upstream partnerships between optical-film makers and display fabs, anchoring long-term supply agreements that stabilize component pricing across the privacy filter market.

By Device Size: Large-Format Adoption Mirrors Multi-Monitor Workflows

The privacy filter market share for 15-24 inch screens stood at 54.20% in 2025, reflecting the prevalence of laptops and standard desktops. Yet ultra-wide and curved panels above 24 inches will outpace overall growth at a 13.28% CAGR as engineers, traders, and creatives demand expansive canvases. Magnetic rail systems and modular panels now accommodate exotic ratios of 21:9 and 32:9 without adhesive residue.

Below-15-inch tablets and convertibles face commoditization, but rugged healthcare and field-service tablets typically incorporate integrated privacy layers as part of their IP65 builds. ISO 9241-305 updates on character legibility require careful luminance tuning; excessive dimming increases the risk of eye strain. Vendors with in-house optical labs retain an edge by calibrating filters to maintain brightness on high-nit HDR monitors while still achieving 30-degree viewing cutoffs, underscoring performance variability across the privacy filters market.

By End-User Industry: Healthcare Leads Compliance-Driven Expansion

Hospital systems accelerated buying after HHS clarified HIPAA workstation safeguards, making privacy screens a checklist item during EHR upgrades. Consequently, healthcare’s 13.58% projected CAGR outpaces corporate office renewals. Financial services maintain baseline demand due to Gramm-Leach-Bliley controls, while the government pilots electrochromic displays for classified workflows.

Educational institutions often adopt filters in testing centers and libraries, but they frequently face budget constraints. Corporate deployments remain the largest segment due to the sheer scale of the workforce, yet future momentum is tilting toward regulated verticals that cannot defer compliance investments. The shift underscores how legislation reshapes spending priorities, reinforcing the centrality of healthcare to the privacy filters market.

By Distribution Channel: OEM Integration Redefines Delivery Models

Online retail continues to hold the highest transaction volume due to its convenience and price transparency. Yet direct OEM integration, tracking a 13.18% CAGR, positions embedded privacy as a premium upsell. HP’s Sure View, Lenovo’s ThinkShutter, and Dell’s built-in microlouver monitors allow for software toggles, eliminating the need for clip-on solutions.

Offline retail continues to serve immediate-need purchases but faces shrinking foot traffic. Managed service providers bundle filters with fleet rollouts, consolidating procurement and securing multiyear maintenance revenue. As embedded solutions mature and cost differentials narrow, aftermarket accessories will shift toward replacement parts, niche devices, and specialized coatings, altering the competitive landscape within the privacy filter market.

Geography Analysis

North America commanded 33.20% of 2025 revenue, propelled by HIPAA mandates and updated Gramm-Leach-Bliley rules that classify visual privacy as a required safeguard. High device ownership and the adoption of zero-trust cybersecurity amplify baseline demand. Federal agencies standardize privacy screens across their field offices, and state privacy statutes, such as the California Privacy Rights Act, spur private-sector purchases to avoid enforcement penalties.

The Asia-Pacific region is expected to register the fastest growth at 13.62% through 2031, as the implementation of China’s Personal Information Protection Law and India’s Digital Personal Data Protection Act raises compliance thresholds. Rapid IT infrastructure rollouts, increasing laptop penetration, and government digitization projects expand the install base. OEMs with fabs in Taiwan and South Korea integrate privacy layers during assembly, reducing import costs for regional buyers.

Europe enforces stringent GDPR penalties, positioning privacy filters as a form of insurance against multi-million-euro fines. ISO standards on display ergonomics converge with green policy pushes for recyclable materials, influencing procurement criteria toward nanostructured films. Middle East nations, such as the UAE and Saudi Arabia, mirror GDPR frameworks, fueling adoption in banking and public-sector digital services. Africa and South America exhibit emerging demand; South Africa’s POPIA and Brazil’s LGPD establish legal baselines that multinational firms must adhere to, facilitating early-stage deployments.

Competitive Landscape

The privacy filters market is moderately concentrated, with 3M, Targus, and Kensington collectively accounting for roughly 40%-45% of the revenue in 2024. They leverage patented microlouver films, established channel partners, and OEM co-branding. They invest in R and D to develop thinner layers, antimicrobial coatings, and touch-friendly surfaces that withstand heavy stylus use. Regional manufacturers in China, India, and Southeast Asia flood e-commerce with budget alternatives, capturing price-sensitive consumers but struggling to penetrate enterprise bids that require ISO and IEC certifications.

Display makers such as BOE Technology and LG Display are integrating privacy optics at the panel level, partnering with material innovators for nanostructure or electrochromic solutions. HP has patented a liquid-crystal privacy layer that automatically dims based on ambient light, demonstrating cross-industry collaboration between laptop OEMs and component specialists. Smaller entrants like PanzerGlass differentiate through antimicrobial features, while Tech Armor focuses on blue-light and fingerprint resistance for mobile devices. As embedded panels become mainstream, aftermarket players must pivot toward adaptable kits for legacy equipment or co-develop integrated variants, thereby intensifying M&A activity in materials science and optical-film coating.

Privacy Filters Industry Leaders

3M Company

Targus Inc.

Dell Technologies Inc.

HP Inc.

Fellowes Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: HP released an AI-driven adaptive privacy screen for its EliteBook line that automatically narrows or widens the viewing angle based on ambient light and user proximity sensors.

- July 2025: Targus launched a modular privacy filter designed for 34-inch curved monitors, using magnetic rails that allow tool-free installation in under 60 seconds.

- April 2025: LG Display began mass production of integrated nanostructure privacy layers for 16-inch notebooks, supplying initial batches to two top-five PC OEMs.

- January 2025: 3M debuted an ultra-thin microlouver film that reduces brightness loss by 25% and supports factory lamination for OLED laptop panels.

Global Privacy Filters Market Report Scope

The Privacy Filters Market is Segmented by Product Type (2-Way Privacy Filters, 4-Way Privacy Filters, Touch-Screen Optimized Filters, Integrated OEM Privacy Displays), Material Technology (Microlouver Film Filters, Nanotechnology-Based Filters, Electrochromic Switchable Filters), Device Size (Less than or equal to 15 Inch Screens,15–24 Inch Screens, Above 24 Inch Screens), End-User Industry (Corporate Offices, Healthcare Facilities, Financial Services, Government Agencies, Educational Institutions), Distribution Channel (Online Retail, Offline Retail, Direct OEM Integration),.and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

| 2-Way Privacy Filters |

| 4-Way Privacy Filters |

| Touch-Screen Optimized Filters |

| Integrated OEM Privacy Displays |

| Microlouver Film Filters |

| Nanotechnology-Based Filters |

| Electrochromic Switchable Filters |

| Less than or equal to 15 Inch Screens |

| 15–24 Inch Screens |

| Above 24 Inch Screens |

| Corporate Offices |

| Healthcare Facilities |

| Financial Services |

| Government Agencies |

| Educational Institutions |

| Online Retail |

| Offline Retail |

| Direct OEM Integration |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | 2-Way Privacy Filters | ||

| 4-Way Privacy Filters | |||

| Touch-Screen Optimized Filters | |||

| Integrated OEM Privacy Displays | |||

| By Material Technology | Microlouver Film Filters | ||

| Nanotechnology-Based Filters | |||

| Electrochromic Switchable Filters | |||

| By Device Size | Less than or equal to 15 Inch Screens | ||

| 15–24 Inch Screens | |||

| Above 24 Inch Screens | |||

| By End-User Industry | Corporate Offices | ||

| Healthcare Facilities | |||

| Financial Services | |||

| Government Agencies | |||

| Educational Institutions | |||

| By Distribution Channel | Online Retail | ||

| Offline Retail | |||

| Direct OEM Integration | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the privacy filters market?

The privacy filters market size is USD 1.55 billion in 2026.

How fast will the privacy filters market grow by 2031?

It is projected to rise at a 12.68% CAGR and reach USD 2.83 billion by 2031.

Which end-user vertical is expanding most quickly?

Healthcare facilities lead growth with a forecast 13.58% CAGR through 2031.

Why are 4-way privacy filters gaining traction?

Open-plan offices and hot-desking expose screens from all directions, driving demand for omnidirectional protection.

What regions show the strongest future demand?

Asia-Pacific is expected to register the highest regional CAGR of 13.62% due to new data-protection laws and rapid device adoption.

How are OEMs influencing market dynamics?

Display manufacturers integrate privacy layers directly into panels, boosting direct OEM integration channels and reducing aftermarket friction.

Page last updated on: