Electroplating Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

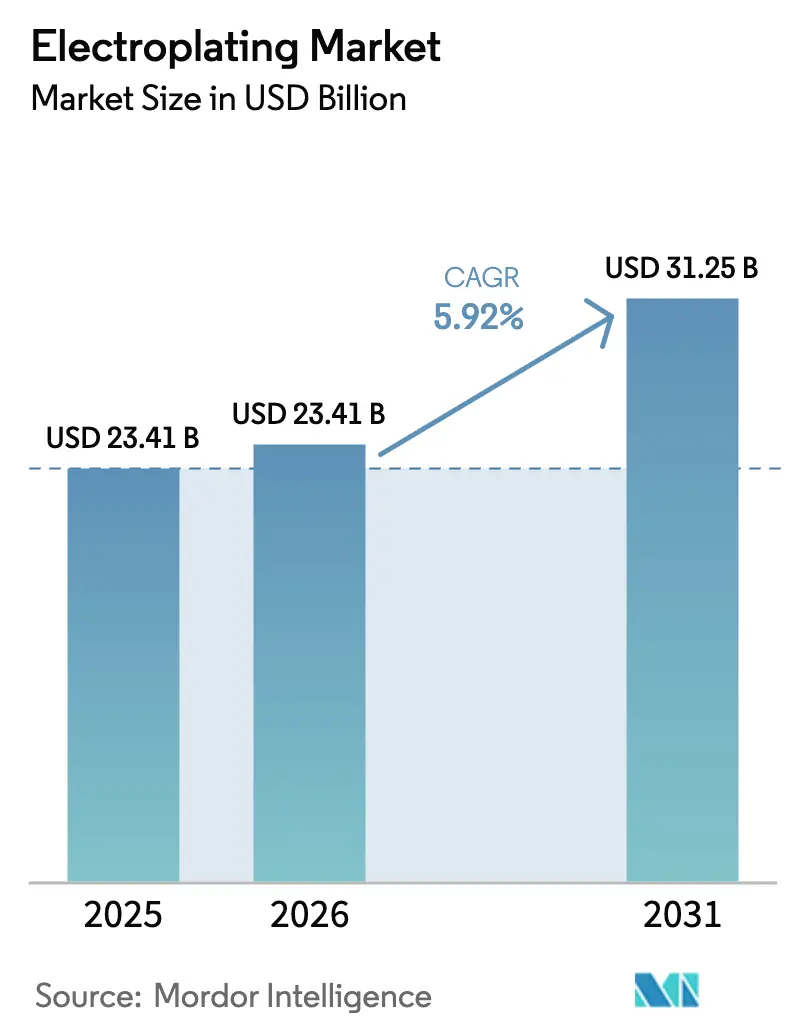

| Market Size (2026) | USD 23.41 Billion |

| Market Size (2031) | USD 31.25 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

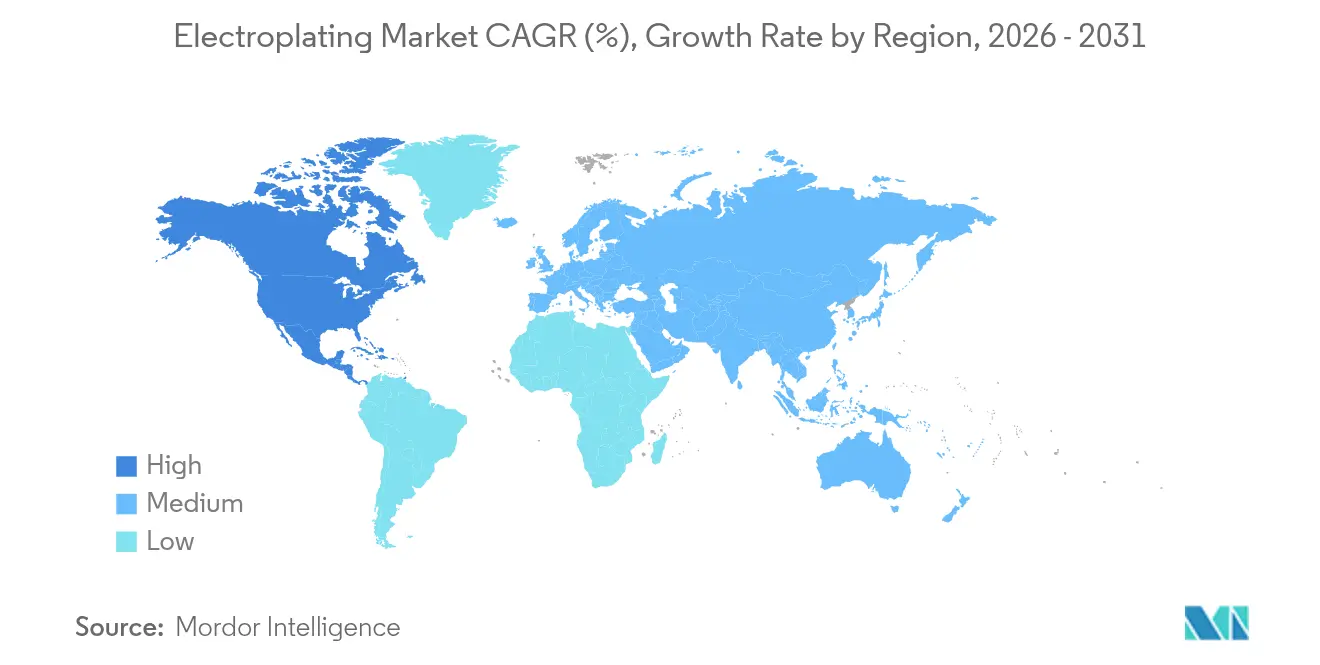

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

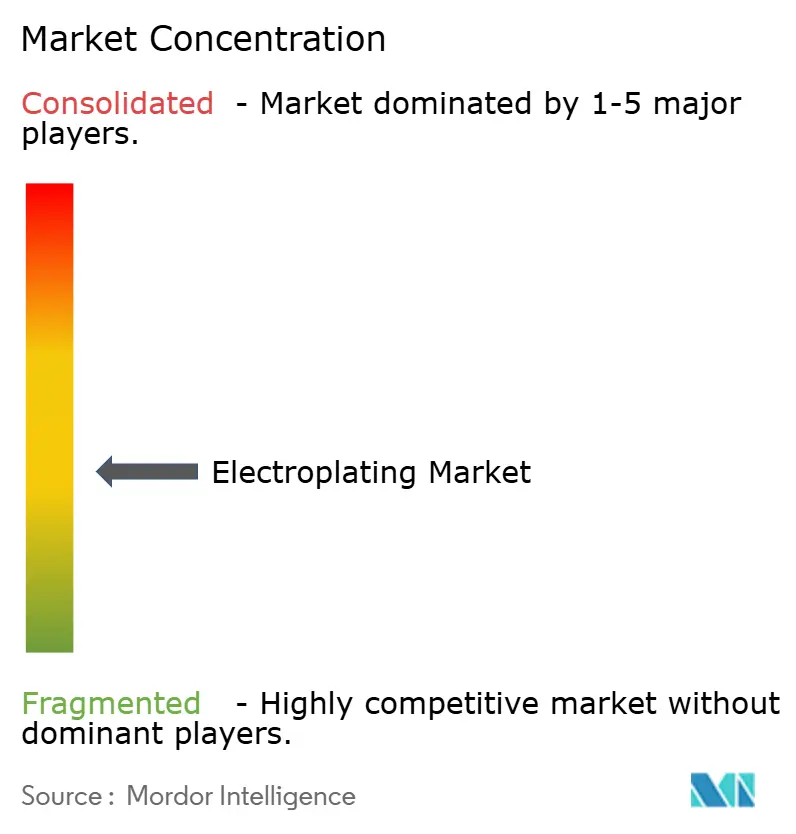

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electroplating Market Analysis by Mordor Intelligence

The electroplating market size in 2026 is estimated at USD 23.41 billion, growing from 2025 value of USD 22.1 billion with 2031 projections showing USD 31.25 billion, growing at 5.92% CAGR over 2026-2031. Persistently high demand for wear-resistant, conductive, and corrosion-proof coatings across electronics, automotive, semiconductor packaging, and industrial equipment sustained growth even when nickel and palladium prices swung sharply and when regulators tightened chromium rules. Miniaturization in consumer devices, the rollout of 5G base-station clusters, and expanding electric-vehicle power-electronics needs all lifted orders for multilayer finishes that combine nickel, palladium, and gold. Investments tied to the CHIPS Act encouraged local suppliers in North America and Europe to install inline reel-to-reel lines fitted with real-time bath-chemistry controls, while Asia-Pacific maintained volume leadership through its dense supply chain and smelter capacity. Concurrently, California’s fast-approaching 2027 decorative chromium sunset date spurred accelerated trials of trivalent systems that pair compliance with hardness and brightness equal to legacy hexavalent baths.

Key Report Takeaways

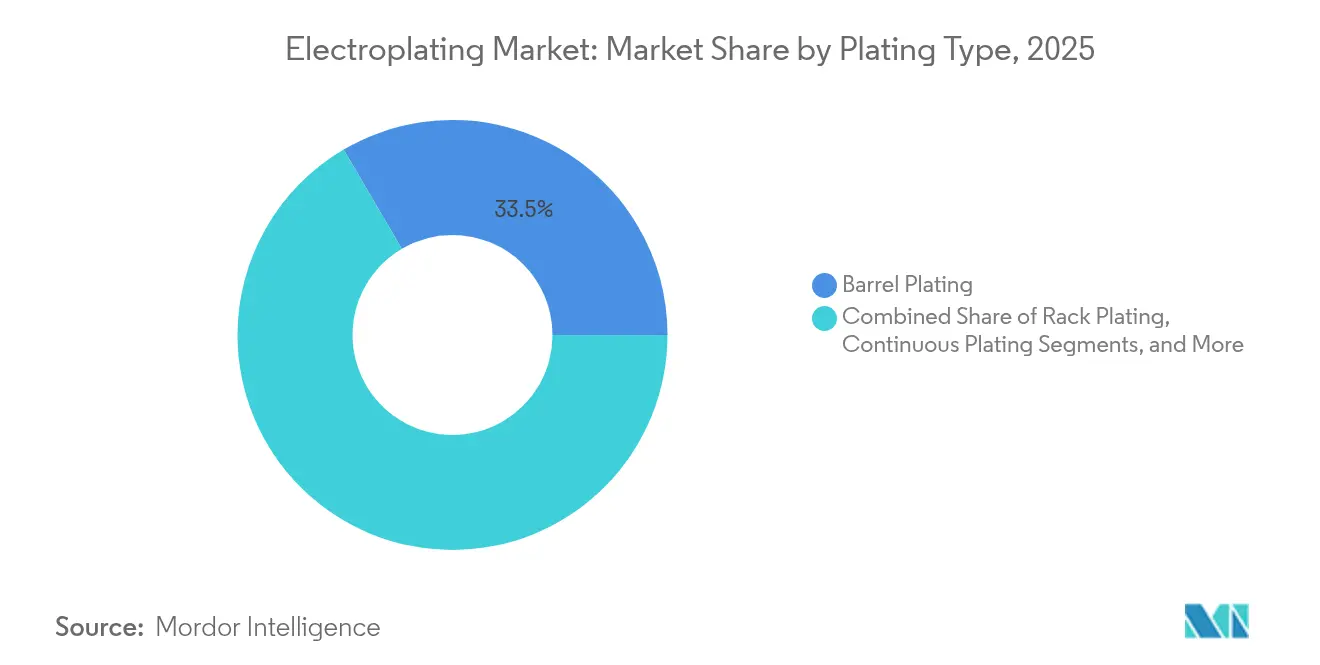

- By plating type, barrel processes led with 33.45% revenue share of the electroplating market in 2025, whereas in-line reel-to-reel systems are projected to expand at an 8.35% CAGR through 2031.

- By functional application, performance-driven coatings dominated with 63.20% of the electroplating market share in 2025, and this segment is set to advance at an 7.72% CAGR to 2031.

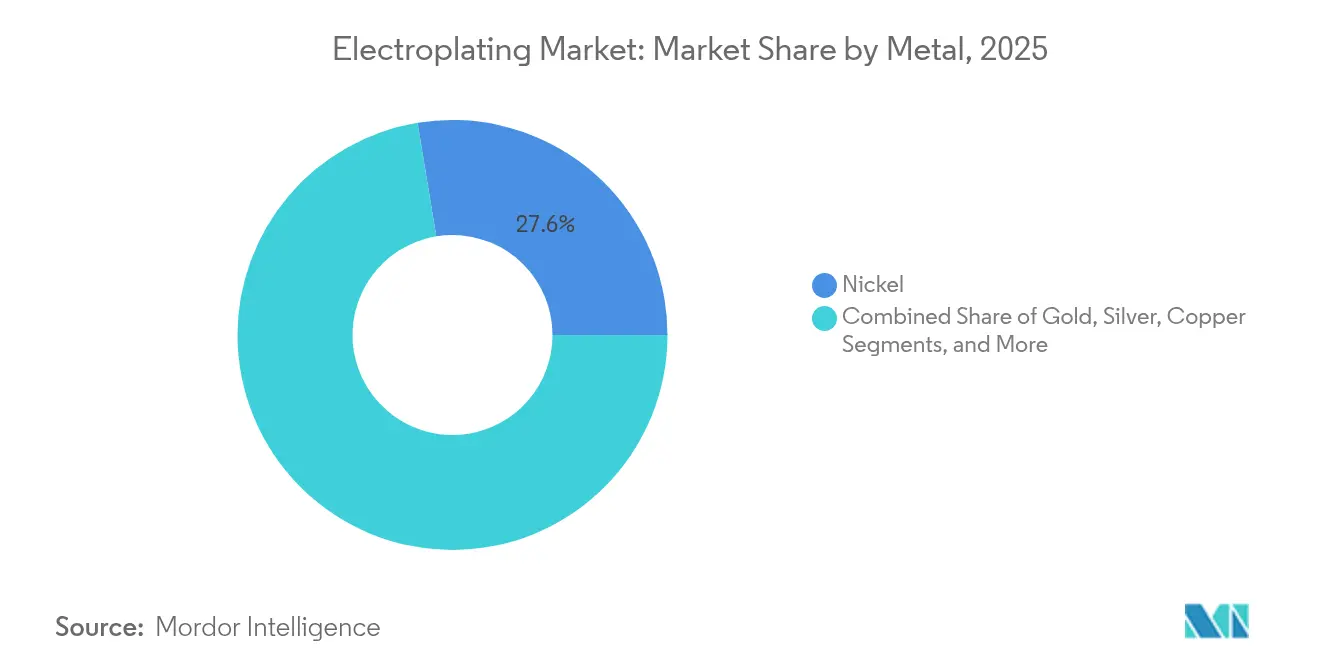

- By metal, nickel accounted for 27.60% of the electroplating market share in 2025; palladium is expected to post the fastest 9.05% CAGR between 2026 and 2031.

- By end-user industry, electrical and electronics captured 37.30% of the electroplating market in 2025, while semiconductor packaging is forecast to grow at a 10.35% CAGR to 2031.

- By geography, Asia-Pacific held 47.40% of the electroplating market in 2025, and North America is projected to record the quickest 7.25% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electroplating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong demand from EV & ADAS-grade connectors | +1.8% | Global, with concentration in APAC, North America, and Europe | Medium term (2-4 years) |

| Lightweighting push in automotive replacing machined parts | +1.2% | North America, Europe, APAC | Medium term (2-4 years) |

| Miniaturisation in wearables & hearing-aids | +0.9% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| 5G infrastructure densification (small-cells, PCB finishes) | +1.1% | North America, Europe, APAC | Medium term (2-4 years) |

| On-shoring of semiconductor packaging lines in US/EU | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Demand from EV and ADAS-Grade Connectors

Global electric-vehicle output ramp-ups and the spread of advanced driver-assistance systems had raised connector reliability requirements through 2024. Tier-1 harness suppliers therefore specified multilayer nickel–palladium–gold stacks that resisted vibration, high currents, and thermal cycling, while MacDermid Alpha research reported widespread SiC and GaN adoption that required thermally robust plating chemistries for power-module leads.[1]MacDermid Alpha, “Future Trends of Power Electronics in the EV Market,” macdermidalpha.com

Lightweighting Push in Automotive Replacing Machined Parts

Automakers pursuing fuel-economy credits and extended EV range substituted plated engineering plastics for machined zinc or steel parts, cutting component mass by up to 70%. Surface-and-Coatings data showed Tesla and global OEMs scaling chrome-look ABS fascia, grill, and interior parts, while copper and nickel strike layers safeguarded EMI shielding on molded housings.

Miniaturization in Wearables and Hearing-Aids

Hearing-aid receivers and smart-watch health sensors shipped in 2024 with sub-100-µm features that depended on pulse-plated copper and gold films for signal integrity. MEMS studies confirmed that denser electroplated coils delivered stronger haptic feedback in compact footprints, and biocompatible gold-platinum finishes preserved long-term implant safety.

5G Infrastructure Densification

Small-cell deployments required multiple high-frequency printed-circuit boards per unit, each benefiting from ultra-smooth copper and immersion-gold layers to curb insertion loss up to 39 GHz. Pulse-reverse regimes and inline roughness sensors lowered skin-effect losses, sustaining the quality of millimeter-wave links in Europe, North America, and selected APAC metro corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nickel and palladium price volatility | -0.8% | Global | Short term (≤ 2 years) |

| REACH and US EPA Cr-VI bans tightening from 2026 | -0.6% | North America, Europe | Medium term (2-4 years) |

| Skill-gap in high-precision plating workforce | -0.4% | Global, with acute impact in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nickel and Palladium Price Volatility

During 2024, LME nickel experienced single-session jumps above 20%, and high-purity supply remained finely balanced, pressuring electrodeposit users. Nornickel’s 2023 report noted that electroplating-grade nickel stayed tight even as low-grade matte entered surplus, forcing shops to hedge or adopt duplex nickel–cobalt alternatives.[2]Nornickel, “2023 Annual Report,” nornickel.com

REACH and US EPA Cr-VI Bans Tightening from 2026

The EU’s updated authorisation sunset dates and the US EPA’s pending effluent plan accelerated demand for trivalent chromium systems. California mandated that decorative lines cease hexavalent use by January 2027 and functional lines by 2039, compelling aerospace and defense contractors to fund exhaustive salt-spray and fatigue testing on trivalent replacements.[3]California Air Resources Board, “Final Statement of Reasons – Chrome ATCM,” arb.ca.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plating Type: Inline Systems Revolutionize Throughput

Barrel units commanded a 33.45% revenue lead in 2025 as bulk fastener, spring, and clip orders relied on economical tumbling batches. Servo-hoists tied to Automotion 8000 PLCs used optical encoders that improved position accuracy to ±0.5 mm, reducing carry-over drag-out during changeovers. Inline reel-to-reel systems, by contrast, are projected to post an 8.35% CAGR through 2031 as semiconductor leadframes, flexible circuits, and ribbon connectors demand micro-ampere-second current control and 0–20 m/min variable web speed.

Inline equipment increasingly integrates pH, metal-ion, and surfactant probes feeding closed-loop controllers that maintain thickness variation within ±3 %, sharpening yield on fine-pitch parts. Continuous strip lines address long-component sectors such as architectural trim, while rack units remain indispensable for turbine blades and chassis busbars requiring selective masking. Numerous mid-size job shops in Asia-Pacific added overhead-transport robots with vision alignment, shrinking labor footprints, and readying legacy barrel plants for automated second-shift operation.

By Functional Application: Performance Drives Growth

Functional finishes covered 63.20% of the electroplating market in 2025 and are set to grow 7.72% annually, reflecting industry preference for coatings that raise corrosion resistance, wear life, or electrical performance rather than simple decorative appeal. Duplex nickel, electroless nickel phosphorus, and trivalent hard-chrome variants all moved from pilot to production scale, aided by Atotech cell designs that cut misting and slash fume scrubber loads.

While the decorative segment remained smaller, it saw Research and Development in ionic-liquid bath chemistries that eliminated cyanide and delivered novel color ranges for wearables and automotive interiors. Research documented enhanced cobalt–nickel alloy brightness at lower current densities, raising interest among jewelry OEMs seeking gold-tone aesthetics with thin precious-metal strike layers. The convergence of functional and decorative demands emerged in premium consumer electronics, where bezel plating required both <0.2 µm roughness and distinctive tones.

By Metal: Palladium Surges on Semiconductor Demand

Nickel held a 27.60% electroplating market share in 2025, underpinned by its use in high-phosphorus electroless baths that formed diffusion-barrier layers on EV battery plates. Automotive core suppliers migrated from hard chrome toward electroless nickel-boron to meet REACH timelines without sacrificing wear resistance. Palladium is forecast to expand at a 9.05% CAGR through 2031 as through-silicon-via caps, copper pillars, and high-frequency connector pins prioritize low-contact-resistance, corrosion-proof finishes.

Selective plating systems governed by Patent US20140102906A1 allowed shops to restrict palladium to bonding pads, trimming precious-metal spend by up to 55%. Gold continued to dominate high-reliability socket markets, silver catered to RF filters, copper remained the backbone for multilayer builds, zinc satisfied general hardware, chromium transitioned to trivalent formulas, and tin assured solderability in canning and electronics.

By End-User Industry: Semiconductor Packaging Leads Growth

Electrical and electronics products represented 37.30% of the electroplating market in 2025, spanning smartphone connectors, industrial sensors, and power-supply heat sinks. Multilayer nickel–nickel-phosphorus–gold stacks sustained solder joint reliability in humid environments, while duplex nickel barrier layers preserved signal integrity during 5G frequency jumps. Semiconductor packaging is projected to grow at 10.35% per year as chip makers extend copper pillar, TSV, and micro-bump densities for 2.5-D integration, leveraging horizontal plating lines that improved hydrodynamics and suppressed voiding.

Medical-device innovators plated platinum-iridium onto implantable electrodes to maintain electrochemical stability under prolonged stimulation cycles. Automotive tier suppliers relied on duplex nickel and high-phosphorus electroless coatings to extend drivetrain component life. Aerospace and defense contractors performed fatigue-critical chrome-free cadmium replacement trials, and industrial machinery builders applied heavy-duty nickel–cobalt for hydraulic rod protection.

Geography Analysis

Asia-Pacific accounted for 47.40% of the electroplating market in 2025, anchored by dense PCB, connector, and metal-forming ecosystems. China’s count of specialist electroplating parks rose from 150 in 2021 to 162 in 2023, mirroring provincial grants that subsidised wastewater-recycling upgrades. Copper cathode output climbed 14.27% year-on-year in April 2025 as new Guangxi smelters ramped up, securing feedstock for strip lines. Hangzhou’s 2024 directive mandated closed-loop rinsing and drag-out recovery to curb nickel emissions below 0.5 mg L-1.

North America, projected to achieve a 7.25% CAGR, benefited from semiconductor reshoring grants and automotive electrification. New Hampshire’s advanced-manufacturing workforce expanded 16.5% between 2017 and 2022 as local shops installed robotic hoist lines for aerospace barrel applications.

Europe prioritised sustainability and innovation amid strict REACH oversight. The European Investment Bank’s 2024/2025 report stated that administrative compliance costs averaged 1.8% of turnover, pushing firms toward digital QA logs and galvanic bath analytics that shortened audit preparation times.

South America and the Middle East and Africa, though smaller, added zinc-nickel and duplex nickel capacity for mining, oil-field, and rail hardware as construction investments in 2024 raised demand for corrosion-proof components.

Competitive Landscape

The electroplating market showed moderate fragmented global ownership in 2024, with five multinational chemistry suppliers holding roughly 45% share, while thousands of regional job shops and captive OEM lines handled customised orders. MacDermid Enthone’s June 2025 acquisition of RM Plating extended its nickel–palladium capability for EV connectors and underlined consolidation among process-chemical majors.

Atotech’s DynaSmart line shipped with inline thickness sensors and AI-guided additive dosing, reducing scrap by up to 8 percentage points during 2024 pilot runs at European automotive suppliers. ACM Research’s horizontal ECP platform captured close to 30% of China’s advanced copper-fill tool demand by April 2025, helping local fabs broaden TSV and redistribution-layer capacity.

White-space entrants pursued chromium-free hard coats, PFAS-free wetting agents, and ionic-liquid decorative systems. Patent filings for selective-area plating heads that meter precious-metal deposition only onto functional pads further signalled cost-downs that could democratise palladium usage. Surveys showed 86% of North American finishers expected revenue gains in 2025, although 56% cited skilled-operator shortages; collaborative robots are therefore being integrated for load/unload and masking tasks.

Electroplating Industry Leaders

Autotech Deutschland GmbH

MacDermid Enthone Industrial Solutions (Enthone Inc.)

JCU Corporation

Pioneer Metal Finishing LLC

Uyemura and Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DYCONEX committed CHF 7 million to upgrade copper and gold lines for 7-µm subtractive-process boards.

- April 2025: ACM Research broadened its horizontal ECP tool suite, consolidating roughly 30% domestic share in China.

- March 2025: California Air Resources Board finalized the 2027/2039 Cr-VI phase-out timetable, accelerating trivalent chromium adoption.

- February 2025: Oerlikon Surface Solutions disclosed CHF 1.5 billion (USD 1.69 billion) 2024 organic sales, citing PVD growth in aerospace.

- January 2025: US EPA published Preliminary Effluent Guidelines Plan 16, flagging PFAS monitoring for electroplating wastewater.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electroplating market as all contract and in-house operations in which a metal layer is deposited onto conductive substrates through electrolytic baths, using barrel, rack, reel-to-reel, and brush equipment across automotive, electronics, machinery, jewelry, and aerospace lines.

Scope exclusion: electroless plating, chemical conversion coatings, and standalone surface-treatment chemicals are left out to avoid double counting.

Segmentation Overview

- By Plating Type

- Barrel Plating

- Rack Plating

- Continuous Plating

- In-line (Reel-to-Reel) Plating

- By Functional Application

- Decorative

- Functional

- By Metal

- Gold

- Silver

- Copper

- Zinc

- Nickel

- Chromium

- Palladium

- Tin

- By End-user Industry

- Automotive

- Electrical and Electronics

- Semiconductor Packaging

- Aerospace and Defense

- Industrial Machinery

- Medical Devices

- Jewellery and Luxury Goods

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview plating line supervisors, chemical formulators, procurement heads, and regional association officers across Asia-Pacific, North America, and Europe. Their insight on throughput, outsourcing ratios, and upcoming trivalent chromium timelines closes data gaps and lets us verify secondary trends in real time.

Desk Research

Mordor analysts first retrieve multi-year trade and production data from UN Comtrade, Eurostat Prodcom, the US Census Current Industrial Reports, and China Customs, which outline metal flow into plating shops. Industry bodies such as the National Association for Surface Finishing and the International Nickel Study Group help us gauge alloy substitutions and bath chemistries. Company 10-Ks, environmental filings, and news archived in Dow Jones Factiva refine average-selling-price (ASP) ranges, while D&B Hoovers and Questel supply revenue splits and patent counts that signal process upgrades. These sources are illustrative; many additional repositories inform our desk work.

Market-Sizing & Forecasting

A single top-down reconstruction starts with plated-metal demand derived from vehicle builds, smartphone and PCB output, connector volumes, and jewelry production. It then aligns these totals with import-export flows and capacity utilization to set the 2025 baseline. Select bottom-up checks, sampled job-shop revenues and ASP × line-hour estimates, anchor assumptions before the two views are reconciled. Key variables tracked include light-vehicle assemblies, 5G handset share, average gold and nickel loadings per PCB, chromium-phase-out milestones, and LME nickel prices. A multivariate regression supported by scenario analysis extends the model through 2030; sizable outliers trigger a fresh call with respondents.

Data Validation & Update Cycle

Outputs face dual-analyst variance tests against independent trade dashboards, followed by manager sign-off. The study refreshes annually, with interim updates when metal price shocks or regulatory events materially shift forecasts.

Why Mordor's Electroplating Baseline Commands Reliability

Published market values frequently diverge because firms differ on included coating types, ASP progression, and refresh cadence.

Key gap drivers we observe are: exclusion of continuous reel lines by some publishers, reliance on static 2023 prices versus our live ASP surveys, treatment of decorative chrome lines, and whether captive OEM plating is counted when estimating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.12 B | Mordor Intelligence (2025) | - |

| USD 21.47 B | Regional Consultancy A (2025) | Omits reel-to-reel capacity; carries 2023 ASPs forward. |

| USD 22.93 B | Trade Journal B (2025) | Adds hybrid metal-finishing totals, double-counting small job shops. |

| USD 19.40 B | Global Publisher C (2023) | Uses earlier base year and drops captive OEM plating. |

In summary, our disciplined scoping, live ASP validation, and yearly fieldwork give decision-makers a balanced, transparent baseline that traces back to observable production metrics and repeatable steps.

Key Questions Answered in the Report

How large will the electroplating market be by 2031?

The electroplating market size is projected to reach USD 31.25 billion by 2031, up from USD 23.41 billion in 2026.

Which application segment is expanding the fastest?

Semiconductor packaging is expected to record a 10.35% CAGR because chipmakers need dense copper pillars and TSV fills for 2.5-D and 3-D integration.

Why are reel-to-reel systems gaining share in the electroplating market?

They deliver continuous, tightly controlled deposition on strip materials, improving yield and speed for lead frames and flexible circuits while supporting inline bath monitoring.

How are regulations changing chromium plating practices?

California mandated a switch from hexavalent to trivalent chromium by 2027 for decorative and 2039 for functional lines, mirroring broader REACH and EPA actions.

What metals lead electroplating usage today?

Nickel held 27.60% of the electroplating market share in 2025 due to its versatile corrosion resistance, while palladium is seeing the quickest growth because of semiconductor and automotive-connector demand.

What challenges do finishers face with raw-material costs?

Volatile nickel and palladium pricing complicates long-term contracts, prompting selective-area plating and alternative alloy adoption to stabilize margins.

Page last updated on: