Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Industrial Optoelectronics Market is Segmented by Device Type (LED, Laser Diode, Image Sensors, and More), Wavelength Range (Ultraviolet, Visible, and More), Technology (Compound Semiconductors, Silicon Photonics, and More), Application (Industrial Automation and Robotics, and More), End-Use Industry (Manufacturing, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

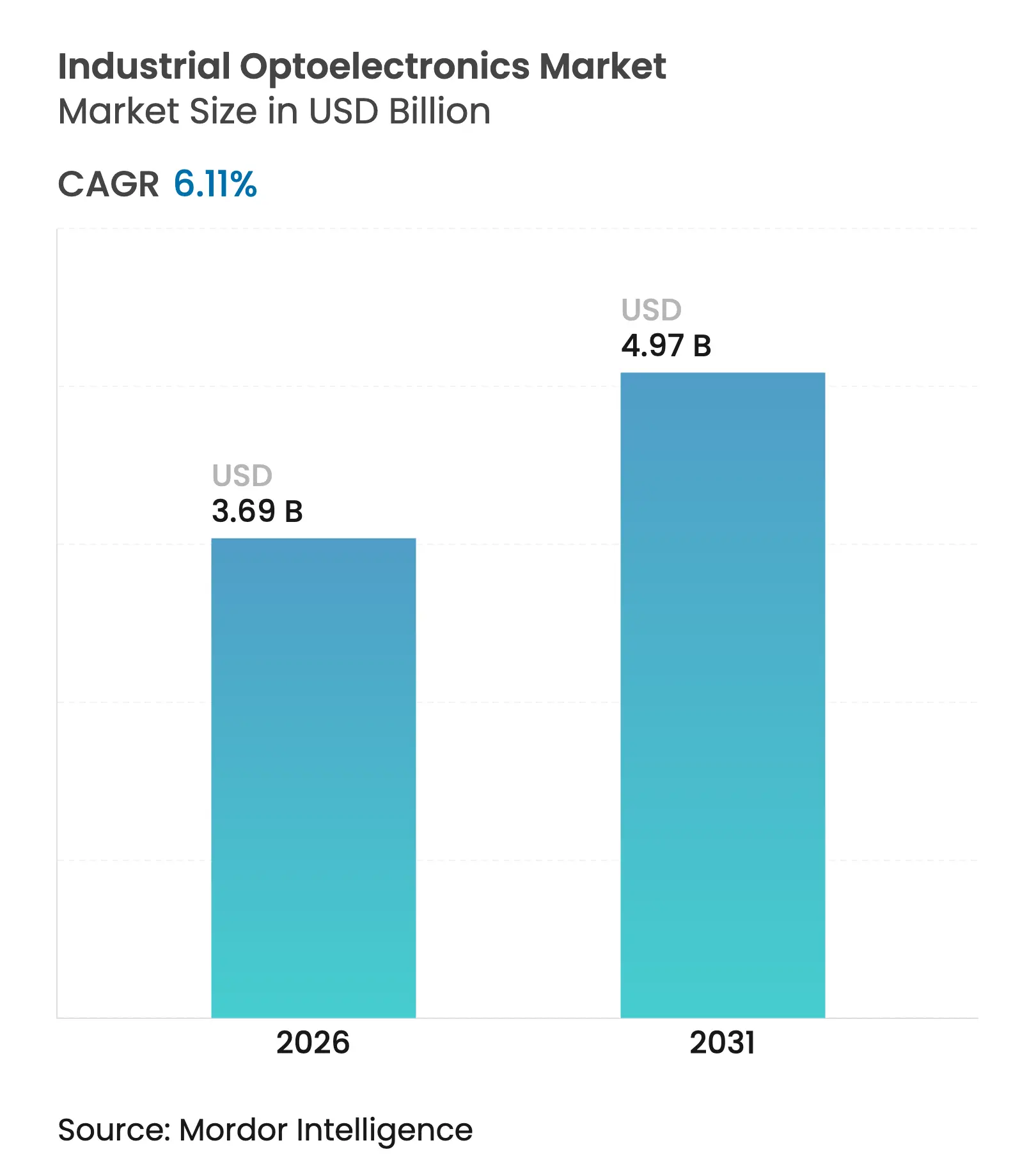

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 4.97 Billion |

| Growth Rate (2026 - 2031) | 6.11 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The industrial optoelectronics market size was valued at USD 3.48 billion in 2025 and estimated to grow from USD 3.69 billion in 2026 to reach USD 4.97 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031). Surging deployment of image sensors, laser diodes, and optical interconnects across smart-factory programs has accelerated adoption even in cost-sensitive verticals. Manufacturers pursuing Industry 4.0 strategies relied on real-time optical data to raise throughput, drive predictive maintenance, and lower scrap, thereby sustaining steady demand despite cyclical capital-equipment spending. Wide-bandgap compound semiconductors, silicon photonics, and explosion-proof LED luminaires broadened use cases in harsh environments, while government incentives in East Asia compressed innovation cycles and cut payback periods. Supply-chain localization in the United States and Europe, combined with rising materials scarcity, prompted vertical integration strategies among device makers, signaling a shift toward tighter control of wafer capacity and critical minerals.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid Adoption of Machine Vision-Enabled Quality

Inspection Across Discrete Manufacturing

Rapid Adoption of Machine Vision-Enabled Quality

Inspection Across Discrete Manufacturing

| +1.6% | Global, with a concentration in East Asia and North America | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.6%

|

Geographic Relevance

:

Global, with a concentration in East Asia and North

America

|

Impact Timeline

:

Medium term (2-4 years)

|

Government-Funded Smart-Factory Initiatives in East Asia

Government-Funded Smart-Factory Initiatives in East Asia

| +1.2% | China, Japan, South Korea | Medium term (2-4 years) | |||

Transition to SiC/GaN Compound Semiconductors Enabling

High-Temperature Industrial Lasers

Transition to SiC/GaN Compound Semiconductors Enabling

High-Temperature Industrial Lasers

| +0.9% | North America, Europe, Japan | Long term (≥ 4 years) | |||

Integration of Optical Interconnects in Industrial Edge

Data Centers

Integration of Optical Interconnects in Industrial Edge

Data Centers

| +0.7% | North America, Europe, East Asia | Medium term (2-4 years) | |||

Rising Demand for Explosion-Proof LED Luminaires in Oil

and Gas Facilities

Rising Demand for Explosion-Proof LED Luminaires in Oil

and Gas Facilities

| +0.6% | Middle East, North America, Russia | Short term (≤ 2 years) | |||

Growing Deployment of Photovoltaic Sensors in Autonomous

Mobile Robots

Growing Deployment of Photovoltaic Sensors in Autonomous

Mobile Robots

| +0.5% | Global, with a concentration in manufacturing hubs | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Adoption of Machine-Vision Quality Inspection

High-speed cameras coupled with AI algorithms reduced semiconductor-line scrap by 40% in pilot deployments, transforming inspection from end-of-line checks to in-process control.[1]Association for Advancing Automation, “Advancing Quality Control with AI-Powered Machine Vision,” automate.org Continuous learning models updated parameters without downtime, enabling micrometer-level defect detection in smartphone battery assembly and facilitating earlier fault containment. Contact image sensors and 250-megapixel cameras captured transient phenomena that traditional optics missed, positioning adaptive vision as a default requirement in electronics factories. Vendors now bundle sensing hardware with edge AI modules, satisfying latency thresholds while trimming bandwidth needs. Demand for such integrated systems underpinned the steady expansion of the industrial optoelectronics market across discrete manufacturing.

Government-Funded Smart-Factory Programs in East Asia

China earmarked nearly CNY 1 trillion for robotics and high-tech ventures, funneling capital toward optoelectronic deployments that accelerate productivity targets. South Korea’s Manufacturing Innovation 3.0 scheme broadened access to vision-guided marine-equipment lines, while Japan’s Economic Security Promotion Act prioritized domestic sourcing of GaN wafers. Coordinated policies shortened ROI cycles for small and mid-size enterprises, allowing faster adoption of optical sensors, LiDAR, and intelligent lighting. The resulting regional ecosystem enabled cross-border technology transfers that raised collective competitiveness and cemented Asia-Pacific’s dominance in the industrial optoelectronics market.

Shift to SiC/GaN Compound Semiconductors

SiC and GaN devices operated at junction temperatures above 150 °C, allowing 24/7 laser cutting without auxiliary chillers and cutting floor-space costs. Infineon’s 300 mm GaN platform increased die output 2.3-fold per wafer, creating scale economics that narrow the cost gap with silicon. Compound devices unlocked new infrared welding heads and quantum sensors, driving a near-13% CAGR in the broader compound segment to 2030. Leading suppliers expanded epitaxy capacity in the United States and Europe to hedge geopolitical risks, a strategy that kept high-power modules flowing into the industrial optoelectronics market despite material shortages.

Optical Interconnects in Industrial Edge Data Centers

NVIDIA’s co-packaged optics demonstrated 800 G links that lowered energy per bit and met sub-millisecond control-loop demands for AI-driven factories. Early adopters in semiconductor fabs used optical backplanes to synchronize plasma chambers, adjusting recipes in real time. Scalable edge racks equipped with pluggable 1.6 T modules positioned to handle the vision data growth forecast at sixfold over five years. As copper backplanes approached signal-integrity limits, optical fabrics became the default for next-generation controllers, anchoring the industrial optoelectronics market’s communications boom.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Capital-Intensive Wafer-Level Packaging for

High-Resolution CMOS Imagers

Capital-Intensive Wafer-Level Packaging for

High-Resolution CMOS Imagers

| -1.1% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-1.1%

|

Geographic Relevance

:

Global, with higher impact in emerging markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Thermal Management Challenges in High-Power IR Emitters

Thermal Management Challenges in High-Power IR Emitters

| -0.9% | Global | Short term (≤ 2 years) | |||

Supply Constraints of Rare-Earth Phosphors for UV-C Lamps

Supply Constraints of Rare-Earth Phosphors for UV-C Lamps

| -0.7% | Global, with higher impact in regions dependent on imports | Medium term (2-4 years) | |||

Stringent EMC/EMI Compliance Impeding Optocoupler Design

Complexity

Stringent EMC/EMI Compliance Impeding Optocoupler Design

Complexity

| -0.6% | Europe, North America, Japan | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Capital-Intensive Wafer-Level Packaging for CMOS Imagers

Next-generation 250-megapixel sensors required through-silicon vias and vacuum cavities that inflated capex, slowing greenfield adoption in price-sensitive regions. Foundry slots remained tight, and tool amortization stretched beyond typical three-year payback expectations, curbing new entrants. Tier-1 OEMs absorbed costs via vertical integration, but SMEs delayed upgrades, tempering near-term growth for the industrial optoelectronics market.

Thermal Management Challenges in High-Power IR Emitters

Heat-flux densities exceeding 1,000 W/cm² pushed conventional heat sinks to their limits, cutting emitter lifetime and wavelength stability. Industrial furnace probes required graphite absorbers with 630 W m⁻¹ K⁻¹ conductivity, yet a mismatch in thermal expansion complicated assembly. Resulting reliability concerns slowed rollouts of IR sensing lines, particularly in developing economies with limited thermal-design expertise.

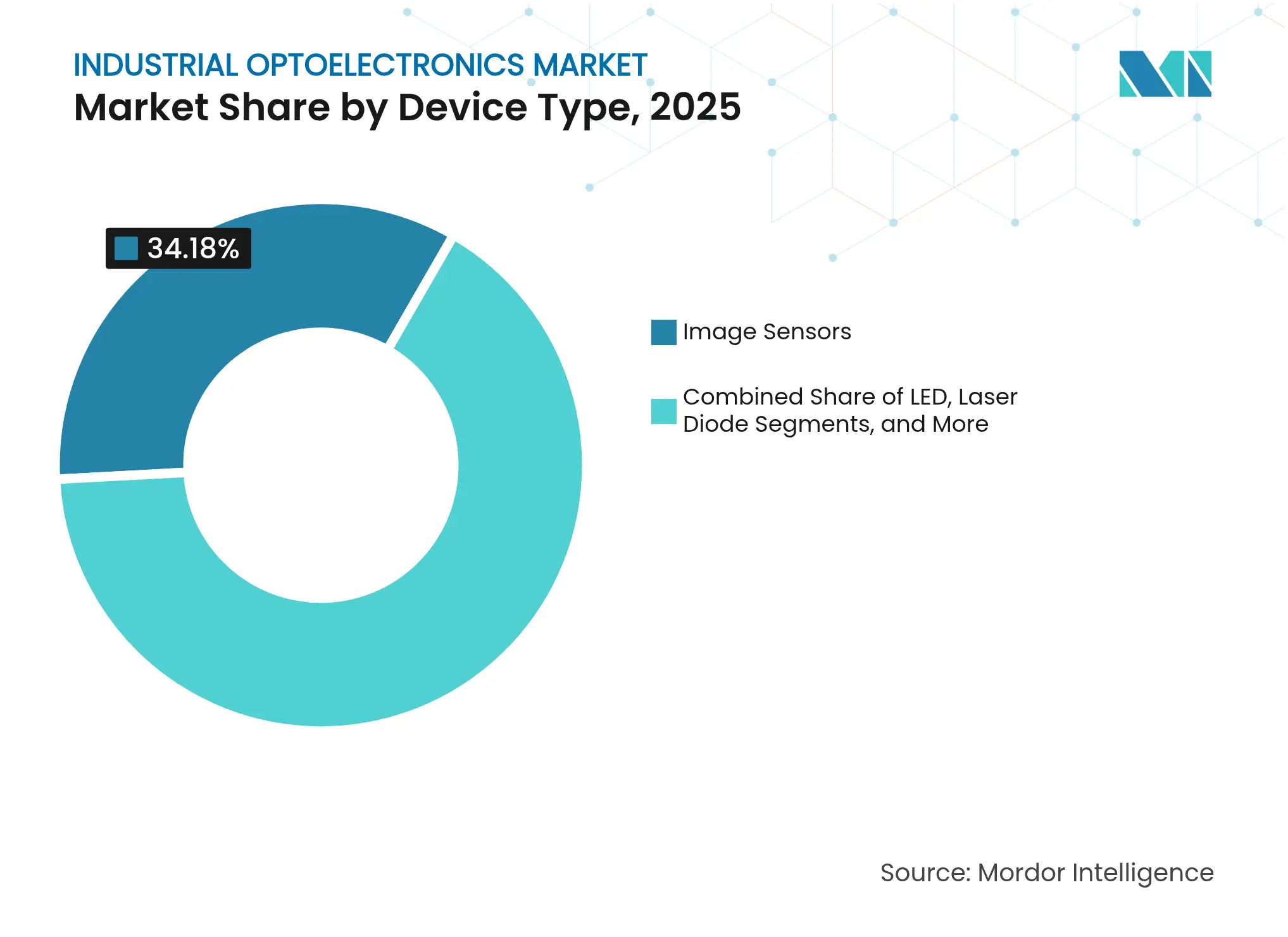

By Device Type: Image Sensors Enable Intelligent Manufacturing

Image sensors commanded 34.18% of the industrial optoelectronics market in 2025, underpinning most vision-guided robotics and inline inspection cells. The segment’s industrial optoelectronics market size expanded alongside edge AI co-processors that removed external servers, cutting latency and bandwidth overhead. Vendors released 250-megapixel CMOS units for semiconductor lithography checks, while line-scan cameras accelerated web inspections in battery-foil coating lines. Laser diodes, though smaller in revenue, posted the fastest 10.95% CAGR as factories adopted LiDAR for AMR navigation and photonics links for edge racks. LED packages sustained solid demand for hazardous-area luminaires in petrochemical facilities. Optocoupler revenues held steady despite tighter EMC rules that complicated design optimization. Photovoltaic cells gained visibility as energy-harvesting nodes in remote sensor clusters across chemical plants. Emerging categories such as OLED indicators and optical modulators remained niche but hinted at new user-interface and high-speed switching opportunities.Software-defined inspection boosted pull-through for accessory optics and embedded lighting, reinforcing image sensors’ platform role in the industrial optoelectronics market. Suppliers leveraged consumer-phone volume scales to drive pixel costs lower and expand usage in small-batch production lines. Wafer-level packaging investments, however, stretched ROI timelines in lower-margin sectors, a restraint partly mitigated by East Asian subsidies for smart-factory upgrades. Overall, device-type diversification produced a balanced revenue mix that cushioned the industrial optoelectronics market against cyclical downturns.

Note: Segment shares of all individual segments available upon report purchase

By Wavelength Range: UV Applications Drive Specialized Growth

Visible-light devices retained a 52.05% share thanks to entrenched machine-vision, HMI, and illumination applications. Nevertheless, ultraviolet components delivered the fastest 12.42% CAGR, buoyed by demand for disinfection chambers and photolithography steppers. UV-C emitting phosphors such as Cr³⁺-doped Na₃AlF₆ achieved 75% quantum yield, extending lamp life in water-treatment skids and thus lifting the industrial optoelectronics market size for this niche. Near-infrared sensors broadened moisture-detection and hyperspectral sorting deployments, while affordable SWIR cameras unlocked value in pharmaceutical blister inspections. Long-wave infrared modules, though smaller in revenue, became indispensable for predictive-maintenance thermography across metal plants.Graphene thermal emitters integrated into silicon waveguides signalled the future miniaturization of IR systems. However, heat-dissipation difficulties slowed roll-out of higher-power IR arrays, reflecting the earlier restraint. Wavelength diversification reduced market risk, ensuring that weakness in one spectral band did not cascade across the entire industrial optoelectronics market.

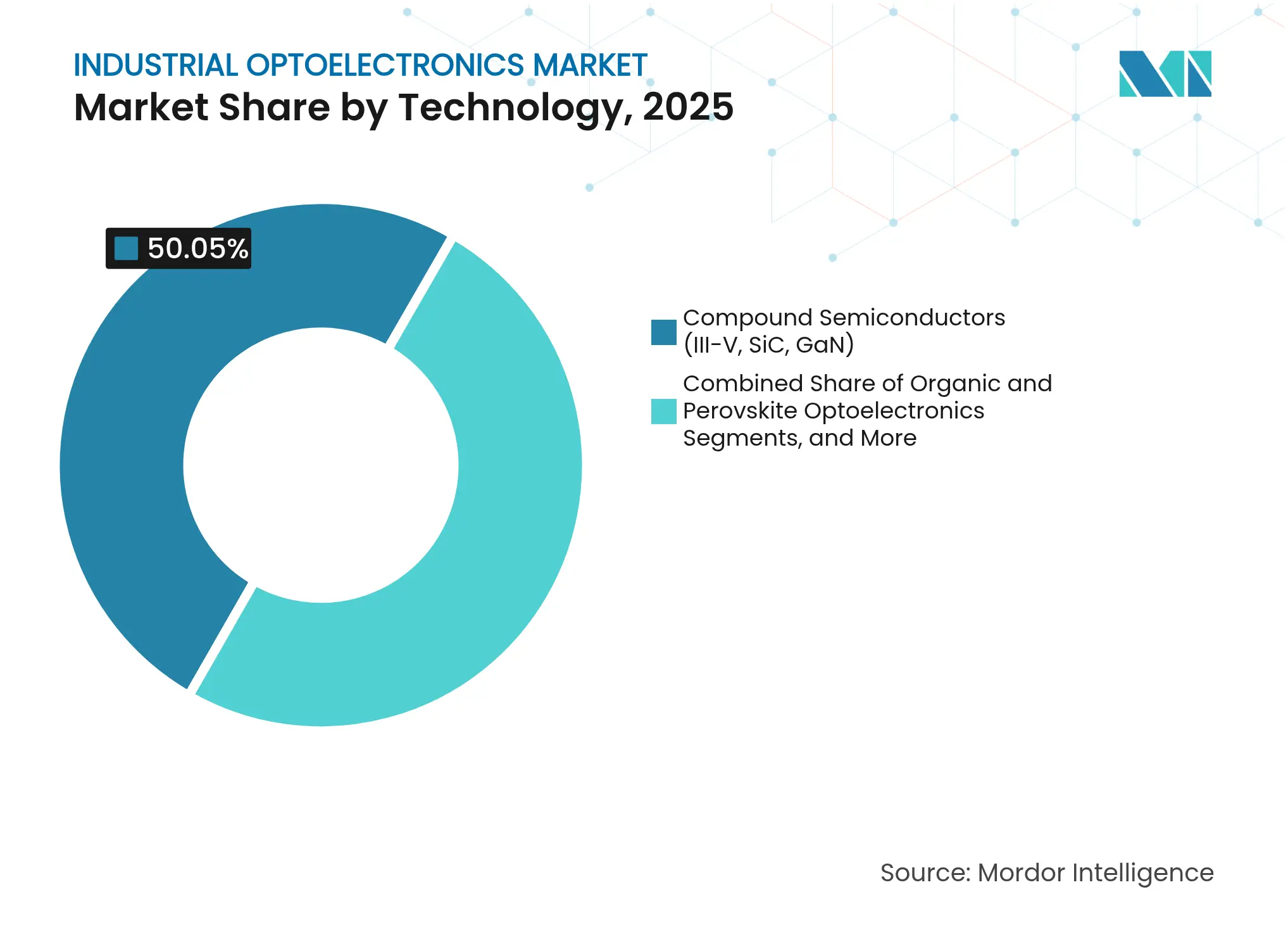

By Technology: Silicon Photonics Transforms Integration Paradigms

Compound semiconductors—III-V, SiC, GaN—commanded 50.05% industrial optoelectronics market share in 2025 due to superior thermal performance in lasers and high-brightness LEDs. Yet, silicon photonics recorded the highest 13.55% CAGR as CPO, and on-chip waveguides offered up to 70% power savings in edge data-center links. Early adopters co-packaged ADCs with Mach-Zehnder modulators, creating single-package PLCs for gigahertz control loops. MEMS-based tuning elements improved adaptive optics in metrology tools, while perovskite photodiodes emerged in large-area conformable sensors for curved surfaces.The industrial optoelectronics market size for silicon photonics remained modest in absolute terms but benefited from leveraging conventional 300 mm CMOS lines, slashing marginal cost curves. Conversely, organic optoelectronics wrestled with longevity issues in harsh industrial conditions. Overall, the technology mixes signalled convergence between electronic and photonic realms, expanding value pools inside the industrial optoelectronics market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Optical Communications Reshape Industrial Networks

Industrial automation and robotics contributed 28.55% of total revenue in 2025, reflecting widescale deployment of AMRs, collaborative robots, and vision-guided manipulators. Optical communication and interconnects, however, posted the quickest 13.12% CAGR as plants embraced edge AI clusters processing multiple terabytes of vision data per shift. Machine-vision inspection cells migrated from 1 GbE to 25 Gb optical links to avoid bottlenecks, while low-power VCSEL arrays replaced copper in backplanes. Sensor fusion for AMRs combined LiDAR, stereo depth, and ultrasonic inputs, spurring incremental demand for multichannel optical transmitters.Lighting applications were upgraded to explosion-proof LED floodlights that met IECEx and ATEX rules, especially in petrochemical complexes. Power-harvesting modules fed wireless sensors in remote pipelines, while spectral-analysis equipment adopted compact laser modules for inline compositional checks. Together, diversified use cases reinforced the resilience of the industrial optoelectronics market amid varying capital-spending cycles.

By End-Use Industry: Manufacturing Leads Digital Transformation

Manufacturing accounted for 40.76% of 2025 revenue as vision-enabled lines drove zero-defect ambitions. High-speed imaging captured micro-cracks during EV-battery tab welding, reducing field failures and underpinning the industrial optoelectronics market’s expansion. The industrial optoelectronics market share held by manufacturing segments remained above 40% through 2025, supported by incentives to modernize small factories in China and South Korea. Automotive and mobility applications registered a 10.38% CAGR as LiDAR shipments for driver-assist functions approached 18 million units in 2025. Aerospace and defense demanded radiation-hardened sensors, while energy and utilities upgraded substations with optical current transformers.Logistics hubs installed barcode imagers and AMR fleets to meet e-commerce surges, leveraging optoelectronic navigation stacks. Healthcare adopted multispectral cameras for tissue analysis, and mining deployed fiber-optic seismic arrays for safety. The breadth of customers kept the industrial optoelectronics market from over-dependence on any one vertical.

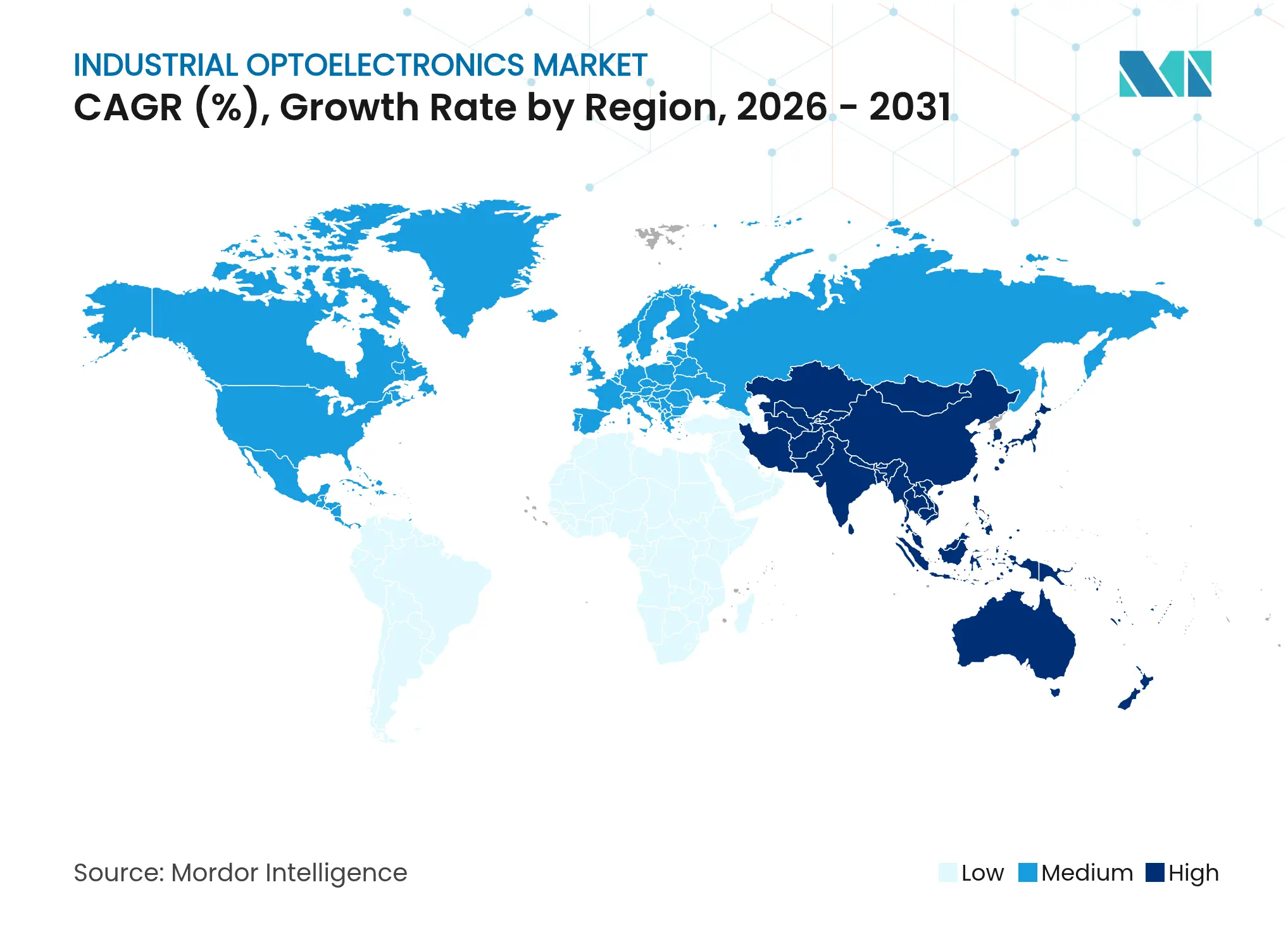

Asia-Pacific captured 46.12% of the global industrial optoelectronics market in 2025, buoyed by its dense electronics supply chain and sizable state incentives. China’s semiconductor revenue reached USD 179.5 billion in 2023 and continued climbing despite export-control headwinds, underpinning steady regional demand for vision sensors and laser components. South Korea’s Manufacturing Innovation 3.0 program accelerated smart-factory retrofits, and Japanese firms upgraded compound-semiconductor fabs under economic-security mandates. Taiwan’s focus on GaN and SiC sustains leadership in wide-bandgap devices. Trade shows such as LASER World of PHOTONICS CHINA 2025 showcased 1,200 vendors, illustrating deep ecosystem strength.North America ranked second, supported by 13,700 new automotive robot installs in 2024 and federal incentives for reshoring wafer capacity. Texas Instruments introduced opto-emulators that lowered BOM and accelerated design-in for high-voltage drives. Silicon-photonics start-ups tapped CHIPS-Act funding, bringing additional wafer-level capacity online and insulating domestic buyers from Asia-centric supply disruptions. Canada’s focus on clean-tech manufacturing drove the uptake of UV-C disinfection and infrared sensing in process industries.Europe retained a sizeable industrial optoelectronics market, anchored by precision-manufacturing leaders in Germany and the Netherlands. ZEISS generated EUR 11 billion (USD 12.4 billion) in 2024 across lithography optics and metrology, injecting sustained demand for high-end photonic modules. EU carbon-reduction targets spurred the adoption of energy-efficient LED lighting and optical power monitoring. However, stringent EMC rules extended design cycles for optocouplers, tempering near-term shipments.The Middle East and Africa prioritized explosion-proof lighting in oil and gas fields, with LED floodlights replacing metal-halide fixtures to cut maintenance. South America experienced growing automotive-robot adoption in Brazil’s assembly plants, complemented by LiDAR-based ore-grade scanners in mining operations. While smaller in value, these regions offered double-digit growth pockets that diversified revenue streams for global suppliers and strengthened the overall industrial optoelectronics market.

Market Concentration

The industrial optoelectronics market remained moderately fragmented. Ams Osram AG, Coherent Corp., and Broadcom Inc. competed across multiple device tiers, yet smaller innovators thrived in niches such as UV-C emitters and MEMS tunable optics. Coherent’s Finisar acquisition fortified its vertically integrated photonics portfolio and improved control over indium phosphide wafer supply. Applied Optoelectronics recorded USD 99.9 million Q1 2025 sales, up from USD 40.7 million a year earlier, showing the benefit of proprietary epitaxy in optical-transceiver demand spikes.[4]Applied Optoelectronics, “Applied Optoelectronics Reports Q1 2025 Results,” investors.ao-inc.com

Vendors pursued forward integration into vision software and AI inference, bundling hardware-software suites to lock in customers. Infineon’s GaN wafer breakthrough promised lower cost-per-watt modules, while MACOM’s DoD-funded GaN-on-SiC line targeted high-frequency, high-voltage chips for harsh environments. BluGlass staked early ground in narrow-linewidth GaN lasers for quantum sensing, a white-space segment with limited incumbent presence.

Competitive intensity sharpened in silicon photonics, where start-ups leveraged existing CMOS fabs to undercut discrete optics on cost and power. At the same time, chronic shortages of rare-earth phosphors and compound substrates pushed leading players to secure long-term supply contracts, reinforcing barriers to entry. Overall, technology road-map execution, supply-chain resilience, and AI-enabled feature sets emerged as primary differentiators within the industrial optoelectronics market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE )

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Optoelectronic devices are electronic devices and systems that involve the study, detection, and control of light. They are considered a sub-field of photonics and are used to convert electrical energy into light or vice versa.

The study tracks the revenue accrued through the sale of industrial optoelectronics by various players worldwide. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market.

The industrial optoelectronics market is segmented by device type (LED, laser diode, image sensors, optocouplers, photovoltaic cells, and other device types) and geography (United States, Europe, China, Japan, Korea, Taiwan, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.