Microprocessor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

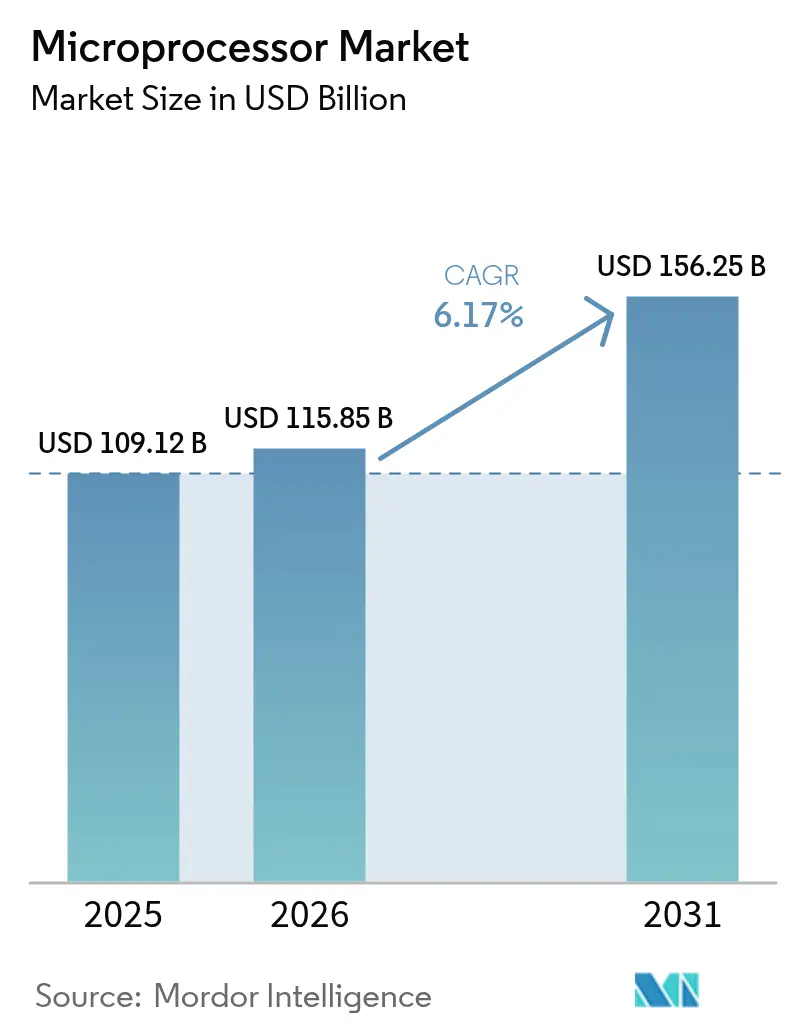

| Market Size (2026) | USD 115.85 Billion |

| Market Size (2031) | USD 156.25 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microprocessor Market Analysis by Mordor Intelligence

The microprocessor market size was valued at USD 109.12 billion in 2025 and estimated to grow from USD 115.85 billion in 2026 to reach USD 156.25 billion by 2031, at a CAGR of 6.17% during the forecast period (2026-2031). This solid trajectory reflected the sector’s ability to adapt as artificial-intelligence workloads reshaped demand patterns and spurred investment in new architectures. The adoption of below-3nm fabrication nodes, the emergence of chiplet integration strategies, and sustained government incentives collectively widened the application base. Asia-Pacific remained pivotal, accounting for a 42.3% microprocessor market share in 2024 as regional electronics and automotive production continued to rise. Graphics Processing Units led growth due to their suitability for parallel workloads, while the open RISC-V architecture recorded the fastest adoption rate among instruction sets.

Key Report Takeaways

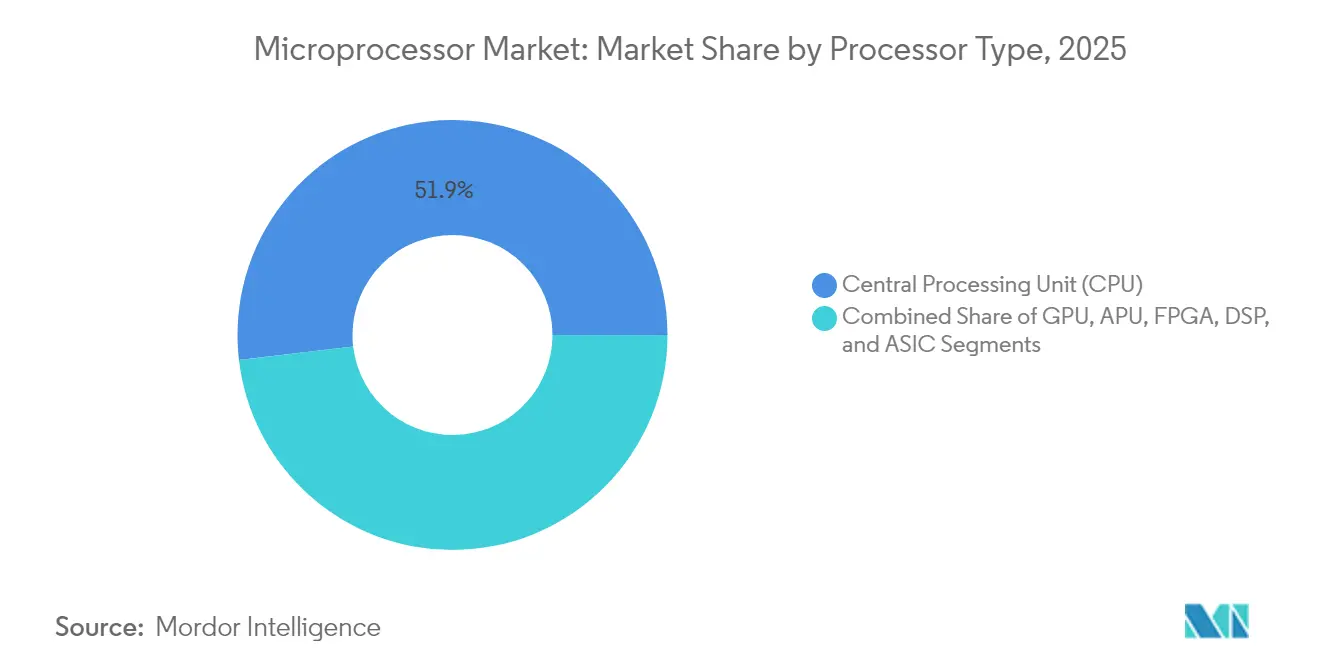

- By processor type, Central Processing Units held 51.85% of microprocessor market share in 2025, while Graphics Processing Units are projected to expand at a 9.95% CAGR to 2031.

- By instruction-set architecture, the x86 family led with 45.95% share in 2025; RISC-V is advancing at a 13.20% CAGR through 2031.

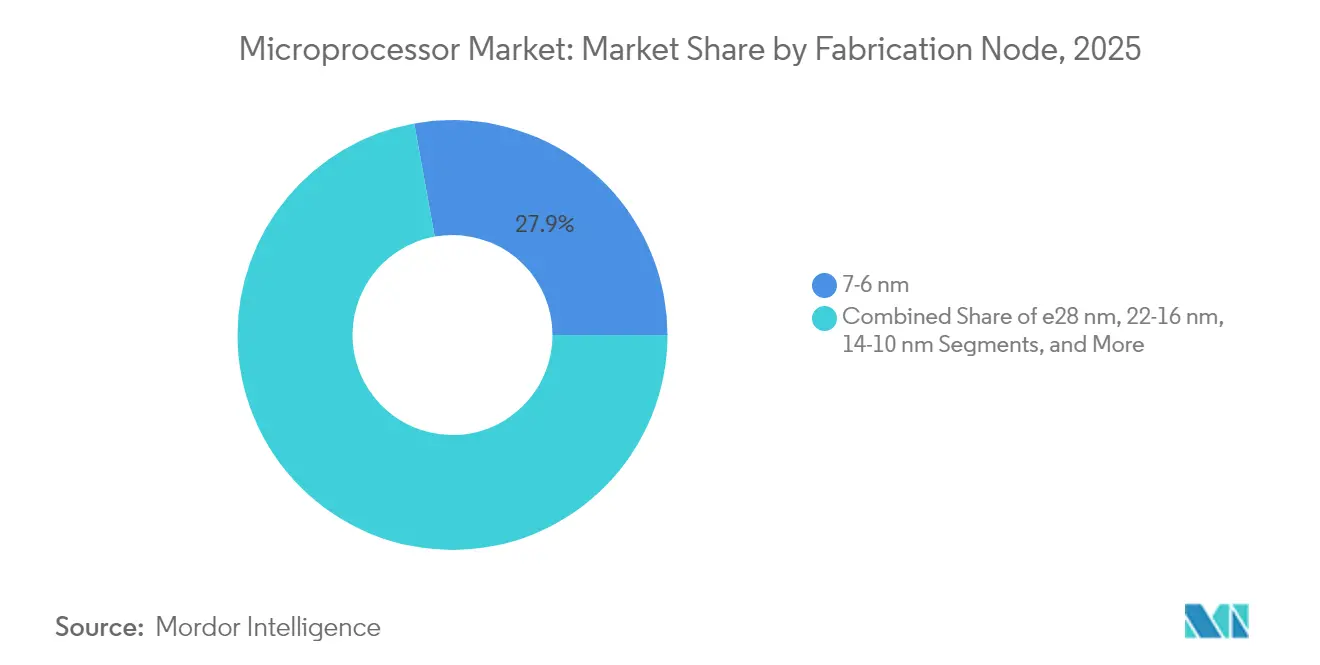

- By fabrication node, the 7-6 nm category accounted for 27.85% share of the microprocessor market size in 2025, whereas the ≤3 Nm node is forecast to grow at 18.60% CAGR between 2026 and 2031.

- By application, consumer electronics held 24.75% of the microprocessor market size in 2025; automotive and transportation are registering the fastest 15.40% CAGR through 2031.

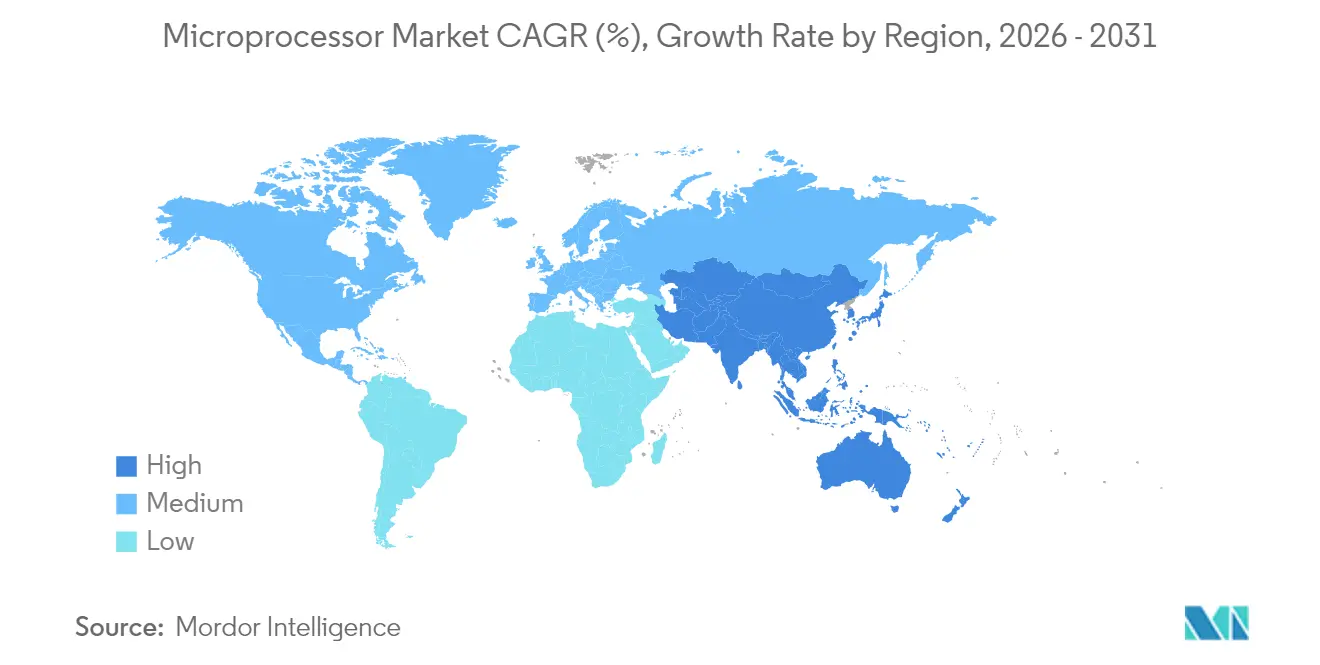

- By geography, Asia-Pacific commanded 41.95% of the microprocessor market in 2025 and is on track for the highest regional CAGR of 8.21% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microprocessor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-performance and energy-efficient processors | +0.9% | Global, with a concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Proliferation of AI accelerators and edge computing use-cases | +0.7% | Global, led by North America, China, and Europe | Short term (≤ 2 years) |

| Expansion of hyperscale data-centres and cloud workloads | +0.6% | North America, Europe, Asia-Pacific core regions | Medium term (2-4 years) |

| Electrification and ADAS adoption in automotive electronics | +0.5% | Europe, North America, and China, with spillover to emerging markets | Long term (≥ 4 years) |

| Chiplet-based heterogeneous integration is gaining traction | +0.4% | Advanced manufacturing regions: Taiwan, South Korea, United States | Medium term (2-4 years) |

| Government semiconductor incentive programmes (CHIPS-style) | +0.4% | United States, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Performance and Energy-Efficient Processors

Demand for processors that simultaneously deliver high throughput and low power consumption shaped vendor roadmaps throughout 2024 and 2025. Data-centre operators prioritized total cost of ownership, prompting designers to optimize performance per watt and integrate on-package memory to reduce latency. Consumer device makers followed suit, seeking battery-savvy chips that enable on-device AI inference without thermal throttling. The move toward smaller geometries such as 3 nm and below pushed leakage-current challenges to the forefront, intensifying cooperation between electronic-design-automation providers and foundries to balance speed and efficiency. Suppliers that delivered energy-efficient designs captured design wins in smartphones, notebooks, and industrial IoT endpoints, reinforcing this driver’s medium-term influence on the microprocessor market.

Proliferation of AI Accelerators and Edge Computing Use-Cases

Edge devices, from smart cameras to industrial robots, increasingly require embedded neural engines that eliminate dependence on cloud back-ends for inference. AMD’s Instinct MI350 accelerator family, scheduled for broad availability in late 2025, illustrated the push toward specialized AI silicon with a four-fold uplift in compute density.[1]Advanced Micro Devices, “Instinct MI350 Series Accelerators,” amd.com Device makers embedded similar engines inside general-purpose processors to address user privacy and latency expectations. As a result, demand broadened beyond data-centre GPUs to encompass low-power inference cores inside wearables and automotive control units. The short-term lift to the microprocessor market emerged as customers accelerated refresh cycles to gain AI capability.

Expansion of Hyperscale Data-Centres and Cloud Workloads

Cloud-service providers extended build-outs despite macroeconomic headwinds, banking on generative-AI demand and high-bandwidth memory advances. TSMC’s commitment to three new United States fabs and two advanced-packaging plants exemplified capacity moves aimed at meeting leading-edge chip demand. Hyperscale operators adopted heterogeneous computing racks that combine CPUs, GPUs, and custom accelerators, often connected through advanced silicon interposers. These configurations increased processor content per server, propelled orders for advanced-node wafers, and cemented a medium-term catalyst for microprocessor revenue growth.

Electrification and ADAS Adoption in Automotive Electronics

Automakers shifted electronic-control-unit budgets toward domain and zonal architectures that house high-compute processors qualified for ISO 26262 safety integrity. Radar, lidar, and camera sensor fusion demanded chips capable of deterministic real-time processing under stringent thermal envelopes. The automotive and transportation segment’s forecast 15.7% CAGR highlighted the sustained pull from electric-vehicle platforms and Level-2+ driver-assistance systems. Microchip’s radiation-tolerant PIC64-HPSC family, geared toward harsh environments, signaled how automotive and adjacent mobility segments contributed to the long-term expansion of the microprocessor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural decline in traditional PC shipments | -0.5% | Global, particularly mature markets in North America and Europe | Short term (≤ 2 years) |

| Ongoing supply-chain capacity constraints for advanced nodes | -0.4% | Global, with acute impact on Asia-Pacific manufacturing | Medium term (2-4 years) |

| Export-control/geopolitical limits on leading-edge equipment | -0.3% | China, Russia, with indirect global supply chain effects | Long term (≥ 4 years) |

| Escalating R&D costs below the 3 nm technology node | -0.2% | Advanced semiconductor regions: Taiwan, South Korea, United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Structural Decline in Traditional PC Shipments

Notebook and desktop volumes softened as enterprises extended refresh cycles and consumers turned to mobile form factors. Manufacturers confronted channel inventory corrections that depressed run-rate demand for mainstream CPUs. Vendors mitigated the impact by positioning AI-enabled PCs as a replacement catalyst, yet volume recovery remained partial through 2025. The short-term drag shaved 0.5 percentage points from the overall CAGR, yet also prompted repurposing of existing fabs toward emerging categories.

Ongoing Supply-Chain Capacity Constraints for Advanced Nodes

Despite a wave of announced fabs, effective capacity at sub-5 nm nodes lagged demand. Extreme-ultraviolet tool availability and qualified personnel shortages elongated production ramp-up timelines. SEMI noted that 18 new facilities broke ground in 2025, but most will not contribute material wafer starts before 2027.[2]SEMI, “Eighteen New Semiconductor Fabs to Start Construction in 2025,” semi.org Limited supply endowed leading foundries with pricing power, squeezing margins for fabless processor designers and imposing allocation risks that persisted into the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processor Type: GPU Acceleration Reshapes Compute Demand

The microprocessor market size for processor types showed CPUs retaining a 51.85% revenue share in 2025 as they remained indispensable for serial workloads. GPUs, however, posted a 9.95% CAGR outlook through 2031, underlining the shift toward massively parallel workloads in AI, graphics, and scientific simulation. The discrete-GPU pipeline expanded as data-centre operators added accelerator cards while consumer devices integrated low-power variants for on-device inference. APUs that fuse CPU and GPU cores on one die circled niche segments where board space and battery life mattered.

Discrete GPUs benefited from high-bandwidth-memory advances that multiplied training throughput, with hyperscalers locking in multiyear supply agreements to secure capacity. FPGAs preserved relevance in telecom infrastructure, where 5G and emerging 6G standards required programmable logic. DSPs continued to address audio and baseband processing, although some market share shifted toward general-purpose cores with embedded vector extensions. Application-specific integrated circuits claimed design wins in high-volume AI inference appliances, demonstrating that bespoke silicon can outpace programmable counterparts once volumes justify non-recurring engineering expense.

By Instruction-Set Architecture: Open Ecosystems Challenge Incumbents

The microprocessor market registered x86 chips with a 45.95% share in 2025 on the strength of decades-old software compatibility. RISC-V, buoyed by its 13.20% CAGR forecast, gained traction among cost-sensitive embedded applications and academic research initiatives that valued open standards. Arm-based designs deepened penetration in data-centre and automotive sectors, leveraging a reputation for power efficiency and a growing server-class software stack.

Vendor roadmaps illustrated divergence rather than convergence. Intel and AMD advanced x86 to sub-3 nm nodes, aiming to sustain single-thread performance leadership. RISC-V specialists emphasized domain-specific extensions, such as vector and cryptography instructions, to differentiate in IoT and AI accelerators. Arm licensees broadened custom core designs, targeting cloud workloads with chiplet-enabled multi-die packages. The proliferation of instruction sets fostered innovation in compiler technologies and toolchains, ultimately expanding developer choice and supporting a more diverse microprocessor market.

By Fabrication Node: Technology Leadership Commands Premiums

Nodes at 3 nm and below delivered the fastest 18.60% CAGR as customers embraced the energy-efficiency gains imperative for AI training clusters and mobile devices. The microprocessor market size for the mainstream 7-6 nm category remained dominant at 27.85% share in 2025 because it balanced performance and yield. Vendors leveraged proven design libraries at 7 nm to shorten time-to-market while selectively migrating flagship products to bleeding-edge processes.

Suppliers faced steep capital intensity at advanced nodes, with TSMC committing NT 1.5 trillion (USD 45.2 billion) to expand 2 nm production in Kaohsiung. Older geometries such as 22 nm and 28 nm continued to serve automotive microcontrollers, power-management ICs, and secure-element chips that prioritized robustness over raw speed. Meanwhile, research initiatives investigated 110 nm mixed-signal processes for non-binary AI accelerators, underscoring that true differentiation often arises from architecture rather than sheer transistor density.

By Application: Vehicle Electrification Leads Volume Upside

Consumer electronics accounted for 24.75% of the microprocessor market size in 2025 due to smartphone and smart-TV shipments, though annual unit growth plateaued. Automotive applications promised the strongest 15.40% CAGR as electric-vehicle penetration and higher autonomy levels drove silicon content per car. Every incremental sensor required additional compute for perception and actuation, pushing domain-controller design wins toward multicore processors with integrated neural engines.

Data-centre and enterprise servers extended processor content through heterogeneous node strategies that lined up CPU chiplets next to high-bandwidth-memory stacks. Industrial automation moved from programmable-logic-controller hierarchies to AI-enabled edge gateways that process video feeds and predictive-maintenance data on site. Aerospace, defense, and medical segments favored radiation-tolerant and safety-certified devices, areas where supply bases remained niche yet saw consistent design-in activity.

Geography Analysis

Asia-Pacific held a 41.95% share of the microprocessor market in 2025 and posted an 8.21% CAGR outlook, sustained by China’s electronics assembly scale and government-backed foundry expansion. Japan’s sensor and automotive ecosystems ensured steady demand for mixed-signal and safety-critical processors, while South Korea’s champions pressed ahead with below-3 nm node investments supported by fiscal incentives. India rolled out chip-manufacturing subsidies that encouraged multinational fabs and local design-service firms to co-locate, adding complementary demand for mid-tier nodes.

North America remained the second-largest region, buoyed by hyperscale cloud build-outs, automotive electrification, and the CHIPS Act incentives that offset capital-expenditure risk for new fabs. TSMC’s USD 165 billion commitment to three United States plants underlined how fiscal support can redirect capacity allocation to domestic soil. Canada and Mexico supported regional momentum through automotive electronics and cross-border logistics integration that shortened lead times for Tier-1 suppliers.

Europe delivered moderate expansion on the back of stringent vehicle-emissions rules and Industry 4.0 modernization. Germany’s automakers locked in strategic silicon supply agreements to safeguard ADAS roadmaps, while France and the United Kingdom tapped local research institutes to co-develop secure processors for defense and aerospace missions. The European Chips Act channeled funds into pilot lines and advanced packaging clusters that aimed to reduce dependency on overseas foundries. The Middle East and Africa trailed in absolute volumes yet registered design-win activity tied to data center projects in the Gulf states and telecom infrastructure upgrades across Africa, setting the stage for long-term participation in the wider microprocessor market.

Mordor Intelligence provides coverage of the microprocessor market across other key regional markets, including Asia Pacific and Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China and Japan incorporating local coverage and market participation, as required.

Competitive Landscape

The microprocessor market displayed moderate concentration as the top five vendors controlled a sizable but not dominant revenue share. Intel advanced multi-tile packaging to sustain generational performance increments, AMD expanded its chiplet strategy across desktop, server, and embedded lines, and NVIDIA leveraged GPU leadership to branch into data-centre CPU silicon. Specialist houses such as Cerebras pushed wafer-scale engines that targeted frontier-AI training efficiency.[4]Cerebras Systems, “Cerebras CS-3: The World’s Fastest and Most Scalable AI Accelerator,” cerebras.ai

Foundry relationships became a decisive factor because climbing mask-set costs discouraged captive manufacturing. Fabless entities forged multi-source agreements to hedge geopolitical risk, while integrated-device manufacturers highlighted vertical supply-chain control as a differentiator. Ecosystem development moved in parallel, with AMD and Arm cultivating open-source firmware stacks and reference-design platforms to accelerate customer adoption.

White-space competition surfaced in secure AI edge devices, automotive-grade inference chips, and memory-centric accelerators. Dutch startup Fortaegis pursued secure-fingerprint physical unclonable function technology, aiming to address data-integrity concerns in AI servers. Meanwhile, long-cycle aerospace projects favored niche suppliers that could certify radiation-hardened processors. The landscape thus evolved from a binary CPU duel to a multipolar contest segmented by application domain, manufacturing access, and ecosystem maturity.

Microprocessor Industry Leaders

SK Hynix

Intel Corporation

TSMC

Sony Corporation

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Texas Instruments announced a USD 60 billion investment across seven U.S. semiconductor fabs, creating an estimated 60,000 jobs.

- May 2025: TSMC announced plans to build nine new advanced wafer-manufacturing and packaging factories in 2025, projecting chip-packaging capacity growth at an 80% compound annual rate.

- March 2025: TSMC expanded its United States investment to USD 165 billion, covering three fabs, two advanced-packaging facilities, and an R&D centre.

- March 2025: Cerebras introduced the CS-3 wafer-scale AI accelerator with more than 4 trillion transistors, doubling the performance of its predecessor.

Global Microprocessor Market Report Scope

A microprocessor is an electronic component built on a single integrated circuit (IC). It consists of millions of small components that work together, such as diodes, transistors, and resistors. This chip performs a variety of purposes, including timing, data storage, and peripheral device interfacing. These integrated circuits are found in various electronic products, including servers, tablets, smartphones, and embedded devices.

The Global Microprocessor Market will provide a detailed analysis of the industry for segments including Type (APU, CPU, GPU, FPGA), Application (Consumer Electronics, Enterprise, Automotive, Industrial), and Geography. The study also provides the impact analysis of COVID-19 on the market. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Central Processing Unit (CPU) |

| Graphics Processing Unit (GPU) |

| Accelerated Processing Unit (APU) |

| Field-Programmable Gate Array (FPGA) |

| Digital Signal Processor (DSP) |

| Application-Specific Integrated Circuit (ASIC) |

| x86 |

| Arm |

| RISC-V |

| Power |

| MIPS |

| SPARC and Others |

| ≥28 nm |

| 22-16 nm |

| 14-10 nm |

| 7-6 nm |

| 5-4 nm |

| 3 nm and Below |

| Consumer Electronics |

| Datacentre and Enterprise Servers |

| Automotive and Transportation |

| Industrial Automation and Robotics |

| Aerospace and Defence |

| Healthcare and Medical Devices |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Processor Type | Central Processing Unit (CPU) | ||

| Graphics Processing Unit (GPU) | |||

| Accelerated Processing Unit (APU) | |||

| Field-Programmable Gate Array (FPGA) | |||

| Digital Signal Processor (DSP) | |||

| Application-Specific Integrated Circuit (ASIC) | |||

| By Instruction-Set Architecture | x86 | ||

| Arm | |||

| RISC-V | |||

| Power | |||

| MIPS | |||

| SPARC and Others | |||

| By Fabrication Node | ≥28 nm | ||

| 22-16 nm | |||

| 14-10 nm | |||

| 7-6 nm | |||

| 5-4 nm | |||

| 3 nm and Below | |||

| By Application | Consumer Electronics | ||

| Datacentre and Enterprise Servers | |||

| Automotive and Transportation | |||

| Industrial Automation and Robotics | |||

| Aerospace and Defence | |||

| Healthcare and Medical Devices | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the global microprocessor market?

The market was valued at USD 115.85 billion in 2026 and is projected to reach USD 156.25 billion by 2031, reflecting a 6.17% CAGR.

Which processor type is expanding the fastest?

Graphics Processing Units lead growth with a 9.95% CAGR through 2031 as AI and parallel-computing workloads rise.

Why does Asia-Pacific hold the largest regional share?

The region accounted for 41.95% of 2025 revenue thanks to its robust electronics manufacturing base and strong consumer-electronics and automotive demand.

What drives demand for sub-3 nm fabrication nodes?

AI training clusters and power-sensitive mobile devices require maximum performance per watt, pushing suppliers toward 3 nm and below processes.

How will vehicle electrification affect future processor demand?

Electric-vehicle platforms and advanced driver-assistance systems are forecast to propel automotive and transportation applications at a 15.40% CAGR to 2031.

Are open-source instruction sets such as RISC-V gaining ground?

Yes, RISC-V is the fastest-growing architecture with a 13.20% CAGR, driven by its customization flexibility and reduced vendor lock-in.

Page last updated on: