Electrophoresis Reagents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

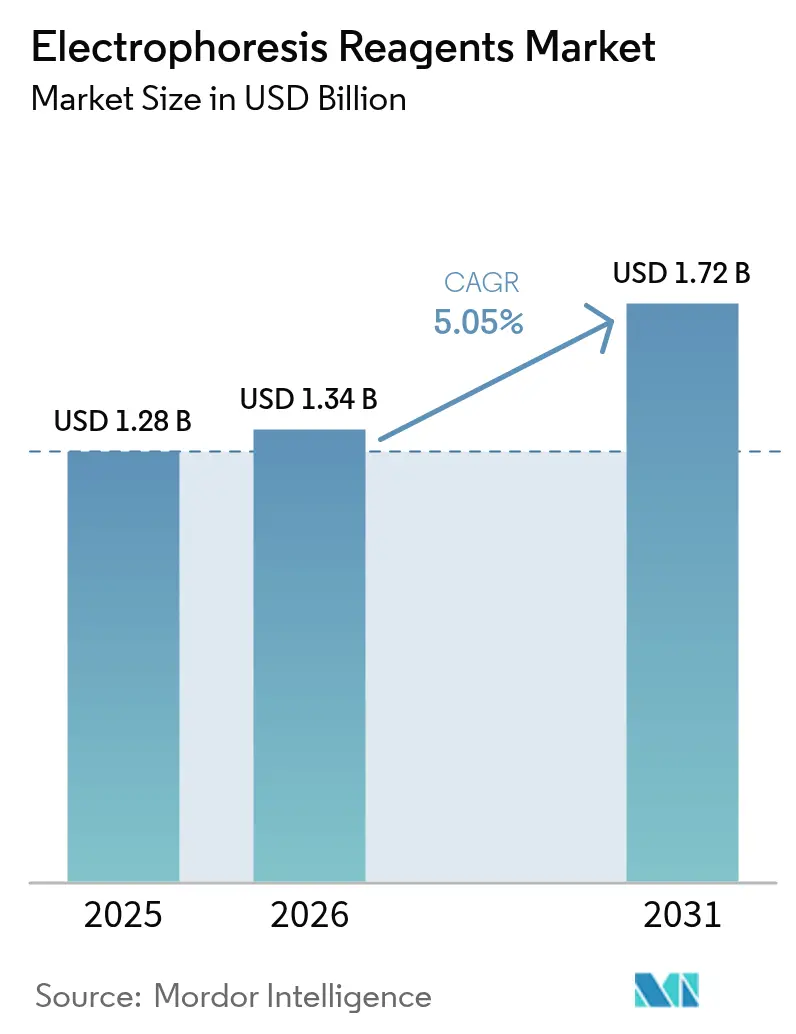

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrophoresis Reagents Market Analysis by Mordor Intelligence

The electrophoresis reagents market size is expected to grow from USD 1.28 billion in 2025 to USD 1.34 billion in 2026 and is forecast to reach USD 1.72 billion by 2031 at 5.05% CAGR over 2026-2031. Demand is now driven by long-term shifts toward precision medicine, stricter regulatory oversight, and sustained federal research funding. The United States Food and Drug Administration’s May 2024 laboratory-developed-test rule introduced a USD 566 million–USD 3.56 billion compliance burden over two decades, elevating quality thresholds that favor established reagent suppliers fda.gov. Asia-Pacific is poised to rebalance global growth as regional research hubs expand despite recent venture-financing softness. Rising adoption of greener stains, integration of AI-enabled gel analytics, and automation-heavy capillary systems further reinforce structural demand drivers for the electrophoresis reagents market.

Key Report Takeaways

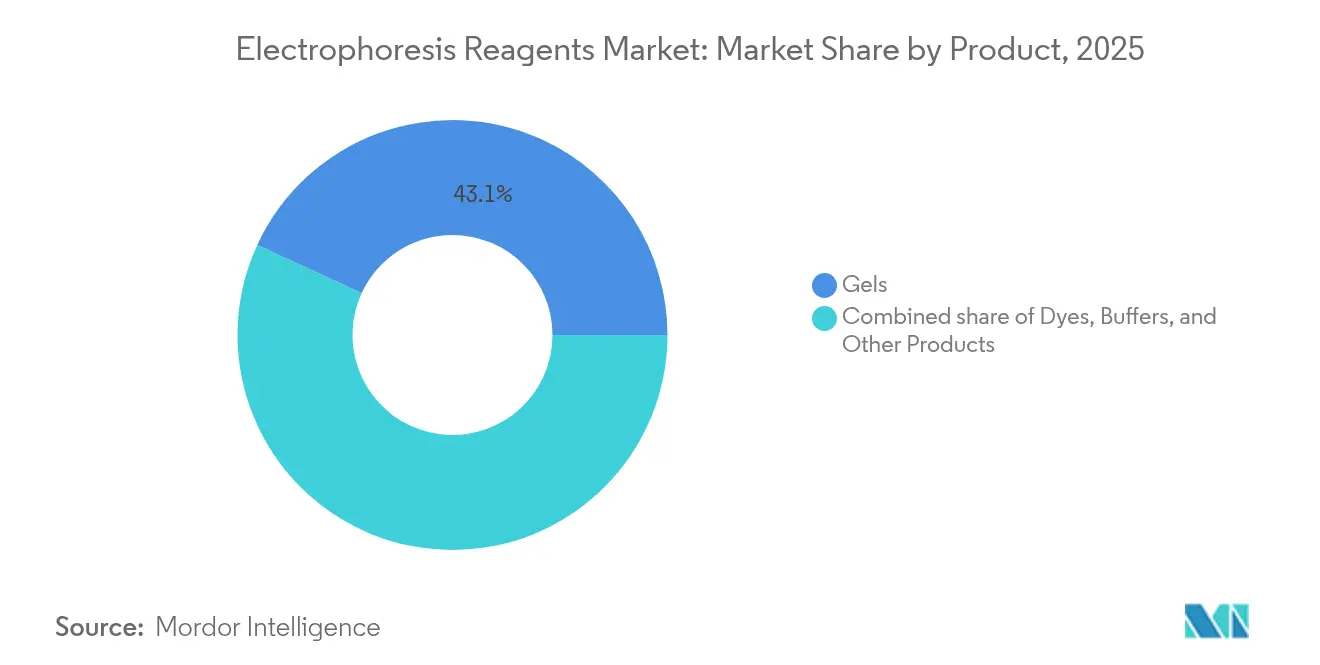

- By product, gels led with 43.12% revenue share of the electrophoresis reagents market in 2025, whereas dyes are projected to grow at a 7.74% CAGR to 2031.

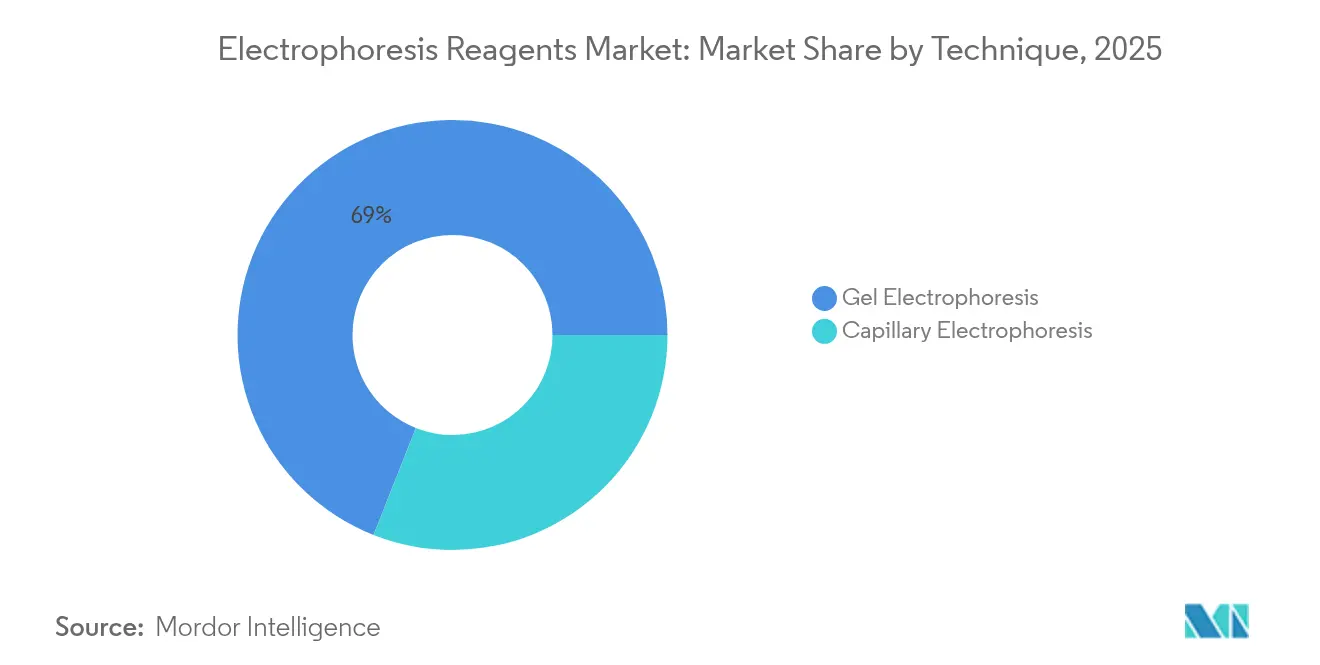

- By technique, traditional gel electrophoresis commanded 69.02% of the electrophoresis reagents market share in 2025, while capillary electrophoresis is advancing at a 7.55% CAGR through 2031.

- By end user, academic institutions held 46.32% share of the electrophoresis reagents market size in 2025; pharmaceutical and biotechnology companies are forecast to expand at an 8.42% CAGR between 2026-2031.

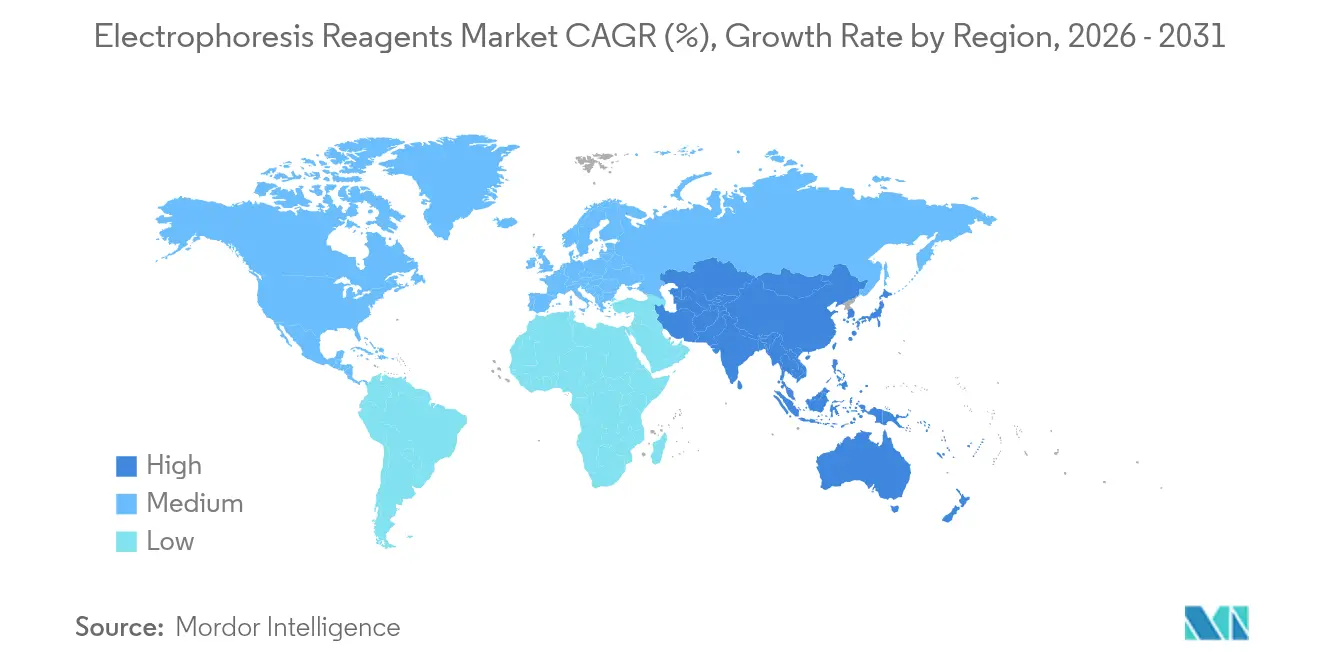

- By geography, North America contributed 39.78% of global revenue in 2025, but Asia-Pacific is projected to post the fastest 6.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrophoresis Reagents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing funding for genomic & proteomic research | +1.2% | North America, Europe, and selected Asia-Pacific economies | Medium term (2-4 years) |

| Rising prevalence of chronic diseases | +0.9% | Global, especially aging industrialized regions | Long term (≥ 4 years) |

| Technological advances in high-throughput electrophoresis | +1.1% | North America & Europe core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Growing adoption of personalized medicine | +0.8% | North America & Europe, emerging Asia-Pacific urban centers | Medium term (2-4 years) |

| Lab-on-a-chip reagent kits for point-of-care molecular testing | +0.7% | Global, early uptake in resource-constrained settings | Medium term (2-4 years) |

| Shift toward greener, non-toxic dyes & buffers | +0.4% | European Union leads; North America follows; Asia-Pacific selective | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Funding for Genomic & Proteomic Research

The National Institutes of Health allocated USD 50.3 million in 2024 to its Multi-Omics for Health and Disease Consortium, signaling a sustained preference for integrated analytical platforms that require electrophoresis reagents for reliable biomarker validation[1]National Human Genome Research Institute, “Multi-Omics for Health and Disease Consortium,” genome.gov. Expanded public funding compels suppliers to offer comprehensive, workflow-compatible product suites instead of stand-alone consumables. Private-sector co-investment magnifies these tailwinds, as pharmaceutical sponsors leverage public infrastructure for drug-discovery programs. Computational genomics now consumes 30% of the National Human Genome Research Institute’s FY2023 budget, underscoring how data-intensive research favors high-throughput electrophoresis systems capable of generating reproducible quantitative outputs for algorithmic pipelines. Together, these funding models lengthen demand visibility across the electrophoresis reagents market by anchoring purchases to multiyear research grants.

Rising Prevalence of Chronic Diseases

The global shift toward aging populations elevates diagnostic complexity, favoring high-resolution separation techniques that can detect subtle proteomic variations in early disease states. Capillary electrophoresis supports charge-variant analysis of therapeutic proteins, a critical requirement in regulatory submissions for biopharmaceuticals. In oncology, electrophoretic separation of circulating tumor DNA enables minimally invasive liquid-biopsy assays that replace tissue-based diagnostics, thereby increasing test frequency per patient episode. Preventive-care models in developed markets convert one-off diagnostic events into recurring reagent demand, translating epidemiological trends directly into higher reagent volumes for the electrophoresis reagents market.

Growing adoption of personalized medicine

Companion-diagnostic requirements tether electrophoresis demand to every targeted-therapy launch. QIAGEN’s QIAstat-Dx platform delivers one-hour genotyping, supporting real-time treatment decisions and driving point-of-care reagent consumption. Regulatory agencies mandate validated molecular characterization methods, embedding electrophoresis reagents into drug-approval dossiers and guaranteeing baseline volumes for compliant manufacturers. As individual therapy regimens replace population-based protocols, test counts per patient increase, bolstering reagent turnover across the electrophoresis reagents market.

Lab-on-a-chip reagent kits for point-of-care molecular testing

Miniaturized chip-based electrophoresis systems pack separation matrices, buffers, and detection elements into disposable cartridges. Early adoption in low-resource settings demonstrates clinical viability where traditional labs are scarce, widening geographic reach and introducing recurrent cartridge-driven revenue models. Diagnostic NGOs that deploy portable PCR and electrophoresis boxes for tuberculosis or HIV screening underscore how consumable-centric business models open incremental volumes in the electrophoresis reagents market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Time-consuming workflows & manual gel preparation | -0.8% | Global high-volume labs | Short term (≤ 2 years) |

| Availability of alternative separation technologies | -0.6% | North America & Europe lead; Asia-Pacific follows | Medium term (2-4 years) |

| Acrylamide feedstock shortages inflating reagent costs | -0.4% | Global impact, regional variance | Short term (≤ 2 years) |

| Strict disposal rules for ethidium-bromide stains | -0.3% | EU leads; North America tightening; Asia-Pacific emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Time-consuming workflows & manual gel preparation

Casting polyacrylamide gels, loading samples, and post-run staining can require up to 8 hours, making labor the most significant variable cost in high-throughput environments. Bio-Rad’s Stain-Free gels remove the staining step, but premium pricing and new-equipment needs deter adoption in budget-constrained labs. Global shortages of skilled technicians intensify workflow bottlenecks, prompting procurement teams to scrutinize total-cost-of-ownership and consider alternative technologies.

Availability of alternative separation technologies

Mass-spectrometry and chromatographic systems offer comparable sensitivity with higher multiplexing and faster run times, eroding electrophoresis’s historical process advantage. Instruments such as SIFT-MS deliver direct VOC analysis without the sample-preparation overhead intrinsic to electrophoresis. Falling MS hardware prices and AI-driven data-interpretation modules lower adoption barriers, siphoning potential growth from the electrophoresis reagents market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Gels Dominate Despite Dye Innovation

Gels accounted for 43.12% of the electrophoresis reagents market in 2025, underpinning virtually every separation workflow across DNA, RNA, and protein applications. Agarose remains a staple for nucleic-acid analysis thanks to low cost and straightforward casting, whereas polyacrylamide supports high-resolution protein work. Dye sales, though smaller, are set to climb at a 7.74% CAGR as ethidium-bromide replacements gain regulatory traction, reshaping the electrophoresis reagents market. Suppliers are differentiating gels through throughput-oriented formats; a 96-well polyacrylamide prototype published in 2024 demonstrated simultaneous horizontal electrophoresis with transfer compatibility, hinting at future multi-sample mainstream offerings. Buffer systems such as Tris/Acetate/EDTA remain entrenched industry standards because performance and cost stability outweigh incremental gains from proprietary modifications. Concurrently, newer dye platforms like Biotium’s One-Step Lumitein series integrate staining directly into gel matrices, removing wash steps and shortening protocols—a direct response to labor-shortage challenges.

By Technique: Automation Drives Capillary Growth

Conventional gels still constitute 69.02% of global technique revenue in 2025 due to legacy equipment bases and minimal operating costs, yet capillary electrophoresis is forecast at a 7.55% CAGR through 2031. The electrophoresis reagents market size for capillary systems is projected to expand as pharmaceutical developers prioritize high-resolution charge-variant analysis that meets regulatory‐filing standards. Bio-Techne’s Maurice platform automates method development and sample runs in a CFR-compliant package, reflecting workflow expectations in GMP labs. Multi-capillary instruments narrow historical throughput gaps, making capillary platforms viable for batch screening workflows previously dominated by gels. Integration with MS detection further elevates capillary-based data richness, supporting structural confirmation needs in biologic-drug development.

By End User: Pharmaceutical Acceleration Reshapes Demand

Academic and research labs retained 46.32% of 2025 revenue within the electrophoresis reagents market, driven by grant-funded exploration and training needs. Yet pharmaceutical and biotechnology companies are tracking an 8.42% CAGR to 2031, aided by expanded biologics pipelines and heavier regulatory burdens that require validated, high-throughput methods. The electrophoresis reagents market share commanded by pharmaceutical users is set to climb as FDA LDT regulations favor large diagnostic organizations capable of meeting validation and documentation costs. Clinical and reference labs form a middle tier, balancing throughput with cost controls; consolidation in this segment may shift purchase volumes toward fewer high-capacity buyers. Contract research organizations follow pharmaceutical trends, adopting capillary or microchip platforms once sponsor demand justifies capex investments.

Geography Analysis

North America generated 39.78% of 2025 revenue for the electrophoresis reagents market, anchored by robust NIH funding and a dense pharmaceutical manufacturing base. The USD 15.4 million NIH–NSF RNA research program exemplifies the public-funding mechanism that sustains reagent consumption irrespective of macroeconomic volatility. Thermo Fisher’s USD 2 billion domestic investment through 2029 underscores supplier commitment to on-shore manufacturing and R&D capacity expansion in anticipation of tax credits and reshoring incentives. Europe remains a mature yet regulation-intensive region; the Corporate Sustainability Due Diligence Directive accelerates substitution of hazardous chemicals, driving demand for greener formulations. Carl Roth’s SOLVAGREEN line of recycled solvents and bioethanol illustrates how European vendors align portfolios with regulatory commitments.

Asia-Pacific is the fastest-growing sub-market with a 6.32% projected CAGR to 2031, fueled by rising government life-science budgets and expanding biopharmaceutical capacity despite a 22% venture-finance decline since 2021. China’s domestic-equipment subsidies and India’s production-linked incentives further tilt capital spending toward regional suppliers, though intellectual-property and supply-chain security concerns encourage multinationals to pursue joint ventures or local manufacturing branches. QIAGEN’s establishment of a Riyadh hub and its memorandum with the Saudi Ministry of Health reveal how Middle East governments leverage strategic partnerships to build molecular-diagnostics ecosystems. Africa and South America remain smaller contributors; targeted donor and government health programs create episodic reagent spikes rather than smooth growth trajectories.

Competitive Landscape

The electrophoresis reagents market is moderately consolidated. Thermo Fisher Scientific has averaged USD 3.09 billion per acquisition across 54 transactions, most recently agreeing to buy Solventum’s purification unit for USD 4.1 billion in February 2025, thereby integrating upstream sample clean-up with downstream separation workflows. Agilent Technologies reorganized into market-focused business groups in 2024 and opened a California companion-diagnostics lab, reflecting a solutions-centric go-to-market approach. Bio-Rad’s pending purchase of Stilla Technologies deepens its digital-PCR capability, complementing its Stain-Free gel line for seamless end-to-end protein analysis. Competitive intensity centers on automation and ESG-aligned consumables: suppliers with AI analytics and low-toxicity chemistries secure differentiation and margin premiums. Niche entrants target white-space opportunities such as smartphone-integrated microchip electrophoresis or solvent-free gel matrices, yet patent walls and validation costs temper new-entrant scale-up prospects.

Electrophoresis Reagents Industry Leaders

Thermo Fisher Scientific Inc.

Merck KGaA

Bio-Rad Laboratories Inc.

Agilent Technologies Inc.

Qiagen N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thermo Fisher Scientific committed USD 2 billion for U.S. life-science manufacturing and R&D capacity expansion over four years.

- April 2025: QIAGEN announced three upcoming sample-prep instruments, including QIAsymphony Connect and QIAsprint Connect, to handle up to 192 samples per run.

- February 2025: Thermo Fisher agreed to acquire Solventum’s Purification & Filtration business for USD 4.1 billion, adding USD 1 billion in sales and bolstering biologics-workflow breadth.

- February 2025: Bio-Rad Laboratories moved to acquire Stilla Technologies, strengthening its digital PCR portfolio aligned with diagnostics and research.

- October 2024: Agilent Technologies introduced the Infinity III LC Series with InfinityLab Assist Technology, achieving My Green Lab ACT 2.0 ecolabel verification.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electrophoresis reagents market as all gels, dyes, buffers, molecular-weight markers, and related consumables that laboratories use to separate, visualize, or quantify DNA, RNA, and proteins through gel or capillary electrophoresis.

According to Mordor Intelligence, values are reported in USD at the manufacturer invoice level and cover 17 major countries across five regions.

Scope exclusion: Equipment, software, and contract testing services lie outside the numerical scope of this report.

Segmentation Overview

- By Product

- Gels

- Agarose Gels

- Polyacrylamide Gels

- Starch Gels

- Dyes

- Ethidium Bromide (EtBr)

- Bromophenol Blue

- SYBR Dyes

- Other Dyes

- Buffers

- Tris/Acetate/EDTA

- Tris/Borate/EDTA

- Other Buffers

- Other Products

- Gels

- By Technique

- Gel Electrophoresis

- Capillary Electrophoresis

- By End User

- Academic & Research Institutions

- Pharmaceutical & Biotechnology Companies

- Clinical & Diagnostic Laboratories

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed lab managers from academic cores, sourcing heads at pharmaceutical and biotechnology firms, and regional distributors in North America, Europe, and Asia-Pacific. The conversations tested reagent throughput assumptions, price dispersion, and the shift toward pre-cast gels, giving us fresh volume and mix insights that desktop data alone could not reveal.

Desk Research

We began by mapping the universe of reagent demand through open datasets from sources such as the US National Institutes of Health, World Health Organization health-research spending records, Eurostat trade codes for agarose and buffer preparations, and patent families retrieved via Questel that signal emerging chemistries. Company 10-Ks and investor decks provided cost trends and average selling prices, while regulatory alerts on dye safety from the US FDA and EMA helped refine adoption curves. Select metrics from D&B Hoovers and Dow Jones Factiva supplied revenue splits for leading suppliers. The sources cited above illustrate, not exhaust, the wider reading list our analysts used for validation.

Market-Sizing & Forecasting

A blended top-down and bottom-up model underpins the numbers. We reconstructed the global demand pool from publicly available production and import values, then cross-checked totals with sampled supplier roll-ups and channel feedback before finalizing the baseline value. Key variables, including laboratory R&D spending, next-generation sequencing sample volumes, price premiums for non-toxic stains, penetration of capillary systems, and regional chronic-disease incidence, drive the forecast. Multivariate regression, complemented by scenario analysis for funding swings, projects value through the forecast period. Data gaps, especially for smaller economies, were bridged with weighted proxies such as biomedical publications per capita and reagent import elasticity.

Data Validation & Update Cycle

Model outputs pass two analyst reviews, variance checks against third-party trade data, and anomaly triggers that prompt stakeholder re-contact. Reports refresh annually, and material events, such as regulatory bans and major M&A, initiate off-cycle updates so clients receive the latest view.

Why Mordor's Electrophoresis Reagents Baseline Commands Reliability

Published estimates often differ because firms choose unlike product baskets, pricing anchors, and refresh cadences.

Our disciplined scope, recurring primary touchpoints, and country-level currency realignment narrow these gaps. Key divergence drivers include whether capillary consumables are counted, how used-in-house reagents are valued, and how rapidly price erosion is baked in.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.28 B (2025) | Mordor Intelligence | - |

| USD 1.37 B (2025) | Regional Consultancy A | Wider basket that adds forensic kits and relies on a 2022 currency base |

| USD 1.22 B (2024) | Global Consultancy B | Excludes capillary reagents and projects demand from a fixed 2019 R&D growth rate |

The comparison shows that once product boundaries, price bases, and refresh timing are aligned, our midpoint estimate stands as a balanced, transparent baseline that decision-makers can retrace to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the electrophoresis reagents market?

The electrophoresis reagents market stands at USD 1.34 billion in 2026 and is projected to reach USD 1.72 billion by 2031.

Which product category leads the electrophoresis reagents market?

Gels lead with 43.12% revenue share in 2025, remaining indispensable for DNA, RNA, and protein separations.

Which technique is growing fastest in the electrophoresis reagents market?

Capillary electrophoresis is expanding at a 7.55% CAGR to 2031, driven by automation and regulatory compliance needs.

Why is Asia-Pacific important for future electrophoresis reagent sales?

Asia-Pacific is forecast to post a 6.32% CAGR through 2031 as regional research funding rises and local biopharma capacity expands.

How are sustainability trends shaping product development?

Strict disposal rules and ESG mandates are boosting demand for greener dyes and buffers, propelling specialty-dye growth within the electrophoresis reagents market.

Which end-user segment is set to outpace others by 2031?

Pharmaceutical and biotechnology companies are projected to grow at an 8.42% CAGR, reflecting lengthening biologic-drug pipelines and stringent quality requirements.

Page last updated on: