Epilepsy Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

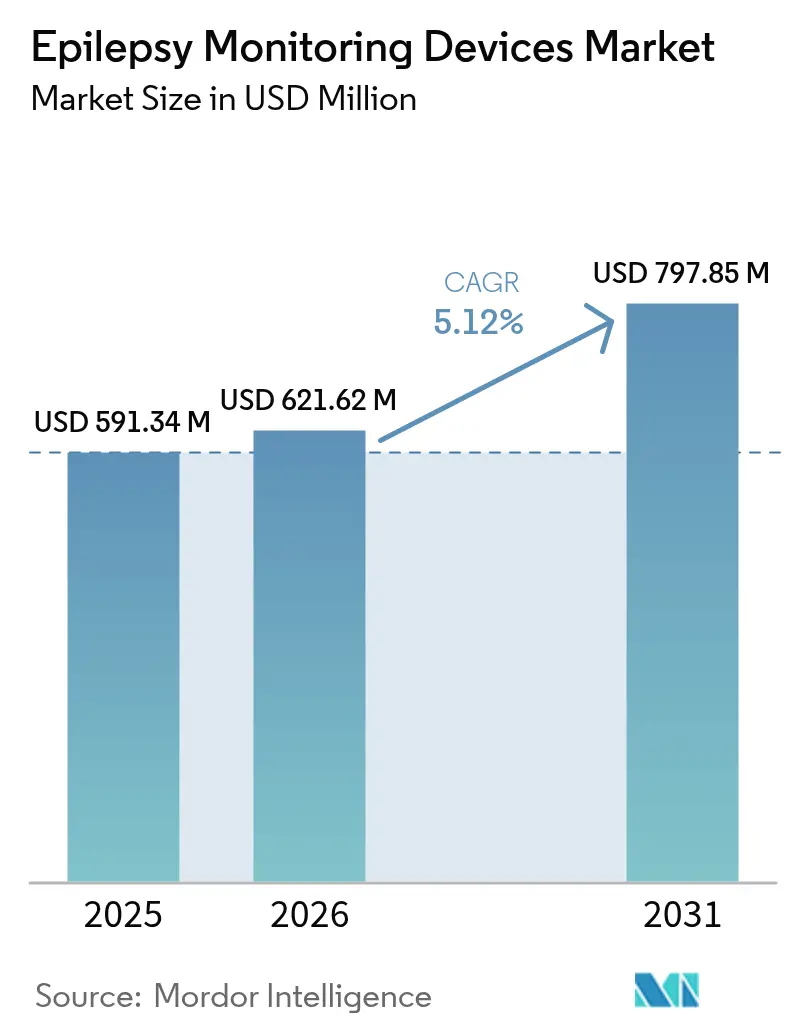

| Market Size (2026) | USD 621.62 Million |

| Market Size (2031) | USD 797.85 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

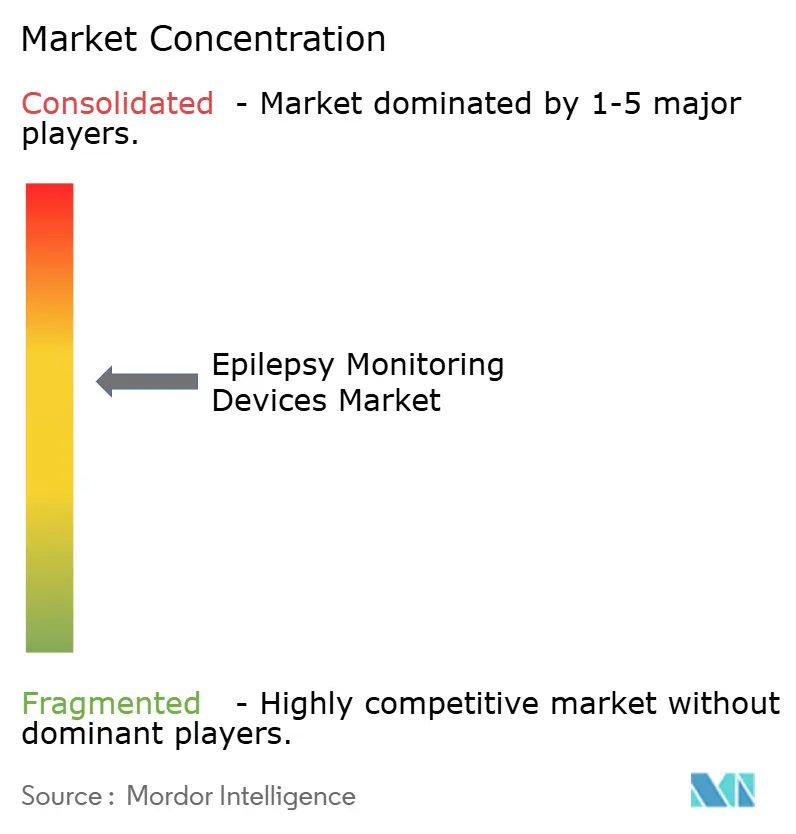

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epilepsy Monitoring Devices Market Analysis by Mordor Intelligence

The epilepsy monitoring devices market size in 2026 is estimated at USD 621.62 million, growing from 2025 value of USD 591.34 million with 2031 projections showing USD 797.85 million, growing at 5.12% CAGR over 2026-2031. Growth stems from the deployment of artificial-intelligence-enabled seizure forecasting, closed-loop neurostimulation, and the widespread shift from inpatient to ambulatory monitoring. Machine-learning algorithms layered on electroencephalography (EEG) streams now deliver seizure predictions hours in advance, expanding treatment windows and elevating clinical value.[1]Elizabeth Donner & Orrin Devinsky, “Wearable Digital Health Technology for Epilepsy,” New England Journal of Medicine, nejm.org Conventional device manufacturers face intensifying competition from AI-native startups whose software-centric platforms command premium pricing. Wearable devices gain traction as patients prefer continuous home monitoring, while hospitals hold volume leadership in acute diagnostics. Regionally, North America retains spending leadership, yet Asia Pacific captures expansion momentum on the back of infrastructure investment and regulatory streamlining.

Key Report Takeaways

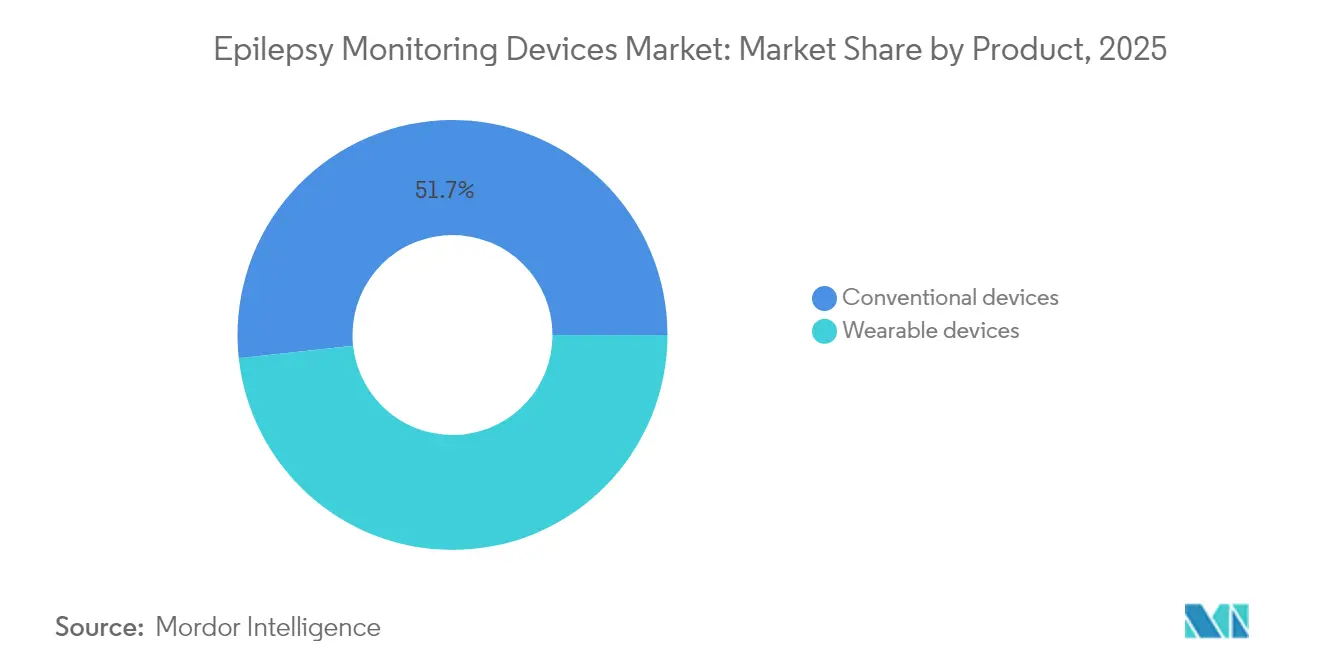

- By product category, conventional systems held 51.72% of the epilepsy monitoring devices market share in 2025, whereas wearables are projected to advance at a 9.61% CAGR through 2031.

- By technology, vagus nerve stimulation led with 36.05% revenue share in 2025; responsive neurostimulation is forecast to expand at an 8.28% CAGR to 2031.

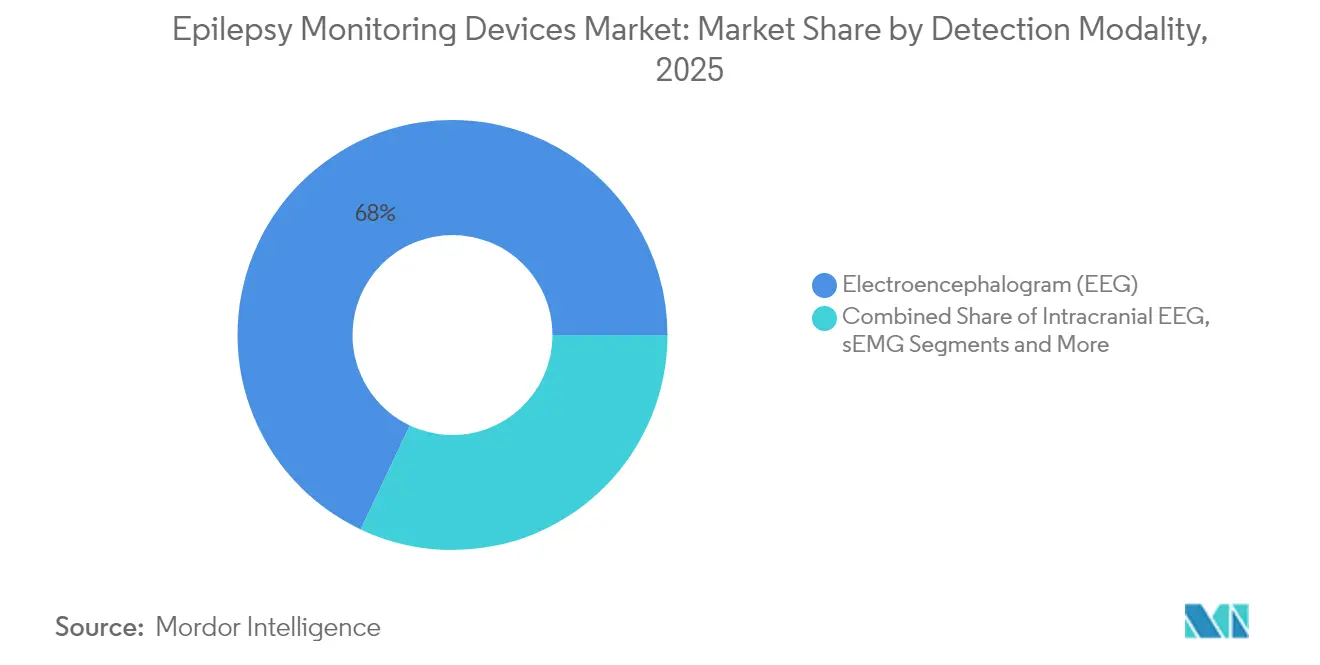

- By detection modality, EEG accounted for 67.98% of the epilepsy monitoring devices market size in 2025, while intracranial EEG shows the highest projected CAGR of 9.01% during 2026-2031.

- By end user, hospitals and ambulatory surgery centers captured 58.76% share in 2025, yet neurology centers record the fastest growth at 7.98% CAGR.

- By geography, North America dominated with 39.31% share in 2025, while Asia Pacific is set to expand at a 7.62% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Epilepsy Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of epilepsy | +0.8% | Global, with higher impact in aging populations | Long term (≥ 4 years) |

| Rising awareness of neuro-degenerative disorders | +0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growing adoption of wearable seizure-detection devices | +1.2% | Global, led by developed markets | Short term (≤ 2 years) |

| Technological advances in EEG & AI-enabled analytics | +1.4% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Integration of seizure-forecasting algorithms into tele-neurology platforms | +0.9% | Global, particularly rural and underserved areas | Medium term (2-4 years) |

| Expansion of US RPM CPT codes to epilepsy monitoring | +0.7% | United States, with potential EU adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Wearable Seizure-Detection Devices

Consumer eagerness for unobtrusive health technology has accelerated uptake of wrist-, head- and ear-worn monitors that capture EEG, electromyography (EMG) and motion signals in real time. Validation studies reported 97.7% sensitivity with merely 0.4 false positives per day.[2]Jingwei Zhang, “Multimodal wearable EEG, EMG and accelerometry measurements improve the accuracy of tonic-clonic seizure detection in-hospital,” arXiv, arxiv.org This clinical-grade accuracy—delivered without hospital admission—has motivated physicians to recommend wearables to the estimated 30% of patients whose seizures persist despite medication. Data from thousands of devices feed federated-learning models that refine population-level seizure forecasts, raising overall predictive reliability while guarding patient privacy.

Technological Advances in EEG & AI-Enabled Analytics

Deep-learning architectures including temporal convolutional networks and self-attention layers reach automated seizure-detection accuracy of 97.37%, surpassing classical signal processing benchmarks.[3]Leen Huang, “Automatic detection of epilepsy from EEGs using a temporal convolutional network with a self-attention layer,” BioMed Engineering Online, biomedical-engineering-online.biomedcentral.com Cloud platforms further upgrade performance through continuous model retraining using de-identified data. As a result, EEG systems transition from passive monitors to intelligent therapeutic hubs that trigger neurostimulation or medication reminders pre-ictally, thus justifying higher device prices and bolstering the epilepsy monitoring devices market.

Integration of Seizure-Forecasting Algorithms into Tele-Neurology Platforms

Tele-neurology programs now embed AI-driven risk scores that warn clinicians of imminent seizures, compensating for the global shortfall of neurologists. Automated EEG triage helps specialists prioritize high-risk cases, trimming wait times and broadening geographic reach. Rural clinics leverage these platforms to deliver specialist-level care without requiring patient travel, a capability that expands the epoxy monitoring devices market across underserved regions.

Expansion of US RPM CPT Codes to Epilepsy Monitoring

Reimbursement reforms in 2024 added epilepsy monitoring to remote-patient-monitoring Current Procedural Terminology codes, granting providers billable pathways for reviewing continuous data streams. Predictable revenue encourages investment in advanced EEG infrastructure, and patient co-payment coverage eases access barriers. Early adopter institutions report rising utilization of ambulatory EEG services, reinforcing the shift toward home-based care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of equipment | -1.1% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Unfavourable reimbursement policies | -0.9% | Emerging markets and select regions | Medium term (2-4 years) |

| Shortage of trained neurophysiologists | -0.7% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Stringent data-privacy rules hindering cloud-based EEG analytics | -0.6% | EU core, with global implications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Equipment

Price gaps exceeding 300% between entry-level EEG units and AI-enabled platforms deter purchases in cost-sensitive health systems. Administrators in lower-income regions often select portable, channel-limited devices that sacrifice predictive analytics to meet budget ceilings. This tiered adoption stalls penetration of high-margin systems, pressing suppliers to launch stripped-down variants aimed at volume markets while preserving premium lines for developed economies.

Stringent Data-Privacy Rules Hindering Cloud-Based EEG Analytics

The European Union’s General Data Protection Regulation classifies neural recordings as highly sensitive, imposing localization mandates and consent protocols that elevate deployment costs. Compliance demands on-premise servers or hybrid clouds, slowing algorithm updates and creating hurdles for smaller vendors. Companies with mature data-governance frameworks exploit this barrier, whereas startups often divert resources from research to legal overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wearables Challenge Conventional Dominance

Conventional systems generated 51.72% of revenue in 2025, reflecting their entrenched role in hospital diagnostics. The epilepsy monitoring devices market size for conventional equipment is projected to expand modestly alongside replacement cycles, yet competitive differentiation narrows as software features become standard. Wearables, in contrast, post a 9.61% CAGR by 2031 on the back of patient-centric design that eliminates inpatient stays. Ear-EEG headsets now hit clinical-grade performance, achieving seizure detection accuracy comparable to multi-channel scalp arrays. The epilepsy monitoring devices market benefits from hybrid offerings that pair hospital-grade baseline studies with long-duration wearables, extending monitoring coverage without inflating clinician workload.

In ambulatory care, reimbursement alignment with remote-patient-monitoring codes accelerates wearable uptake across United States practices. Suppliers integrate cloud dashboards that flag anomalies, freeing neurologists to focus on high-risk cases. Meanwhile, conventional system makers retrofit hardware with AI modules to preserve market relevance. These parallel strategies keep both product classes integral to comprehensive care pathways, although growth clearly tilts toward wearables.

By Technology: Responsive Neurostimulation Emerges as Premium Driver

Vagus nerve stimulation led revenue at 36.05% in 2025, underpinned by a two-decade safety record and broad clinical indications. The epilepsy monitoring devices market size for VNS is expected to rise steadily, supported by pediatric approvals. Responsive neurostimulation excels with an 8.28% CAGR, driven by closed-loop algorithms that deliver stimulation precisely when abnormal activity is sensed. Hospitals view RNS as a high-margin solution for medication-refractory patients, while payers recognize its cost-offset potential through seizure reduction.

Deep brain stimulation and accelerometry-only devices cover niche indications yet remain clinically essential. The competitive axis shifts from hardware prowess to software sophistication, with algorithm accuracy dictating therapeutic outcomes. Companies that couple proprietary datasets with machine-learning expertise erect defensible moats, reshaping long-term leadership in the epilepsy monitoring devices market.

By Detection Modality: EEG Dominance Faces Intracranial EEG Challenge

EEG captured 67.98% of the epilepsy monitoring devices market share in 2025, a figure rooted in its non-invasive nature and ubiquity across all care levels. Intracranial EEG, though reserved for surgical candidates, logs a 9.01% CAGR through 2031 as precision mapping of seizure foci gains urgency in drug-resistant cases. Surface electromyography and video systems retain supporting roles, complementing EEG by identifying motor manifestations that pure electrical readings may overlook.

Integrated platforms now blend these modalities, delivering holistic insights that lessen false alarms and boost diagnostic confidence. Vendors offer modular packages that hospitals can scale from standard EEG toward multimodal configurations as case complexity rises. This stepwise pathway allows progressive investment while maintaining interoperability, amplifying the addressable base for the epilepsy monitoring devices market.

By End User: Neurology Centers Capitalize on Specialization

Hospitals and ambulatory surgery centers controlled 58.76% of revenue in 2025, buoyed by emergency response capabilities and bundled reimbursement structures. However, neurology centers post an 7.98% CAGR by focusing on outpatient pathways and chronic management programs. These facilities deploy dedicated epilepsy units that seamlessly integrate diagnostics, therapy titration, and follow-up. Diagnostic centers occupy a supplementary niche, performing routine studies but lacking interventional capacity.

The epilepsy monitoring devices market increasingly rewards care settings that deliver outcome-based value. Neurology centers thus negotiate volume discounts on hardware and leverage AI dashboards to handle large caseloads efficiently. Hospitals respond by forming joint ventures with specialty clinics to preserve referral streams, fostering a collaborative rather than zero-sum competitive climate.

Geography Analysis

North America retains primacy with 39.31% of global revenue in 2025, anchored by Medicare-backed reimbursement of long-term monitoring and rapid adoption of FDA-cleared implants such as Epiminder’s Minder device. Hospital systems capitalize on RPM billing codes that align precisely with EEG data review intervals, producing immediate financial justification for capital purchases. Canada and Mexico contribute incremental gains through tele-health expansion and cross-border technology partnerships.

Asia Pacific records the highest CAGR at 7.62% through 2031. China accelerates approvals of both drugs and devices, exemplified by Fycompa’s 2024 clearance that broadened clinical interest in comprehensive management. Japan and South Korea showcase early adoption of RNS and wearable EEG, leveraging robust insurance coverage and high digital-health literacy. India’s neurologist shortage continues to hold back volume growth, yet national telemedicine networks begin to offset access barriers, hinting at accelerating uptake post-infrastructure maturation.

Europe shows moderate expansion, tempered by GDPR compliance costs that force on-premise analytics deployments. Germany and the United Kingdom lead research trials that validate AI algorithms, aiding vendor market entry. Southern European states rely on EU structural funds to modernize epilepsy centers, fostering gradual but uneven growth.

Across the Middle East and Africa, initiatives to localize medical device assembly and targeted training programs lay groundwork for future demand, though present volumes remain small relative to population need.

Competitive Landscape

The epilepsy monitoring devices market features moderate fragmentation. Incumbent EEG titans leverage distribution scale, whereas software-first entrants concentrate on predictive analytics. Strategic pivots underscore this shift: NeuroPace exited low-margin SEEG distribution to focus on proprietary responsive neurostimulation lines. Nihon Kohden acquired Ad-Tech Medical, adding intracranial electrode capability that complements its EEG portfolio. ElectroCore safeguards more than 215 patents in non-invasive vagus nerve stimulation, demonstrating the significance of intellectual property fortresses.

Convergence around multimodal monitoring spurs alliances such as Cadwell’s investment in Seer Medical, merging cloud analytics with at-home EEG hardware. Wearable innovators partner with telecom providers to secure low-latency data links vital for real-time alerts. These moves underscore the primacy of software and connectivity over pure sensor counts in shaping future leadership in the epilepsy monitoring devices market.

Epilepsy Monitoring Devices Industry Leaders

Nihon Kohden Corporation

Medtronic plc

Masimo Corporation

Compumedics Ltd

LivaNova plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Epiminder received FDA de novo clearance for the Minder implantable EEG system, enabling months of continuous brain monitoring in the United States.

- April 2025: Cadwell invested in Seer Medical to blend long-term home EEG with the company’s diagnostic portfolio, accelerating remote epilepsy care.

- November 2024: Nihon Kohden acquired a 71.4% stake in Ad-Tech Medical Instrument Corporation, adding specialized intracranial electrodes to its neurology lineup.

Global Epilepsy Monitoring Devices Market Report Scope

As per the scope of this report, an epilepsy monitoring device is a type of electronic device that can identify seizures in epilepsy conditions. The Epilepsy Monitoring Devices market is segmented by Product (Conventional Devices and Wearable Devices), Technology (Vagus Nerve stimulation, Deep brain Stimulation, Accelorometry, Responsive neurostimulation), Detection devices (Electroencephalogram, Intracranial EEG, Surface Electromyography, Video Detection systems), End User (Hospitals and Ambulatory services, Neurology centers, Diagnostic centers) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values in USD million for the above segments.

| Conventional Devices |

| Wearable Devices |

| Vagus Nerve Stimulation (VNS) |

| Deep Brain Stimulation (DBS) |

| Accelerometry |

| Responsive Neuro-stimulation (RNS) |

| Electroencephalogram (EEG) |

| Intracranial EEG (iEEG) |

| Surface Electromyography (sEMG) |

| Video Detection Systems |

| Hospitals & Ambulatory Surgery Centers |

| Neurology Centers |

| Diagnostic Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Conventional Devices | |

| Wearable Devices | ||

| By Technology | Vagus Nerve Stimulation (VNS) | |

| Deep Brain Stimulation (DBS) | ||

| Accelerometry | ||

| Responsive Neuro-stimulation (RNS) | ||

| By Detection Modality | Electroencephalogram (EEG) | |

| Intracranial EEG (iEEG) | ||

| Surface Electromyography (sEMG) | ||

| Video Detection Systems | ||

| By End User | Hospitals & Ambulatory Surgery Centers | |

| Neurology Centers | ||

| Diagnostic Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the epilepsy monitoring devices market?

The market is valued at USD 621.62 million in 2026 and is projected to rise to USD 797.85 million by 2031.

Which product type is growing fastest?

Wearable devices post the highest growth at a 9.61% CAGR, driven by continuous home-based monitoring and favorable reimbursement.

Why is responsive neurostimulation gaining attention?

RNS systems deliver closed-loop electrical stimulation when abnormal brain activity is detected, achieving superior seizure control and expanding at an 8.28% CAGR.

Which region offers the strongest growth outlook?

Asia Pacific leads with a 7.62% CAGR, reflecting infrastructure investment and streamlined regulatory approvals.

How are reimbursement policies shaping adoption?

The inclusion of epilepsy under US Remote Patient Monitoring codes created sustainable billing pathways, spurring hospital investment in continuous EEG infrastructure.

Is data privacy a barrier in Europe?

Yes, GDPR mandates strict localization of neural data, increasing deployment costs for cloud-based analytics and slowing adoption relative to North America.

Page last updated on: