Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.82 Billion |

| Market Size (2031) | USD 20.02 Billion |

| Growth Rate (2026 - 2031) | 4.80% CAGR |

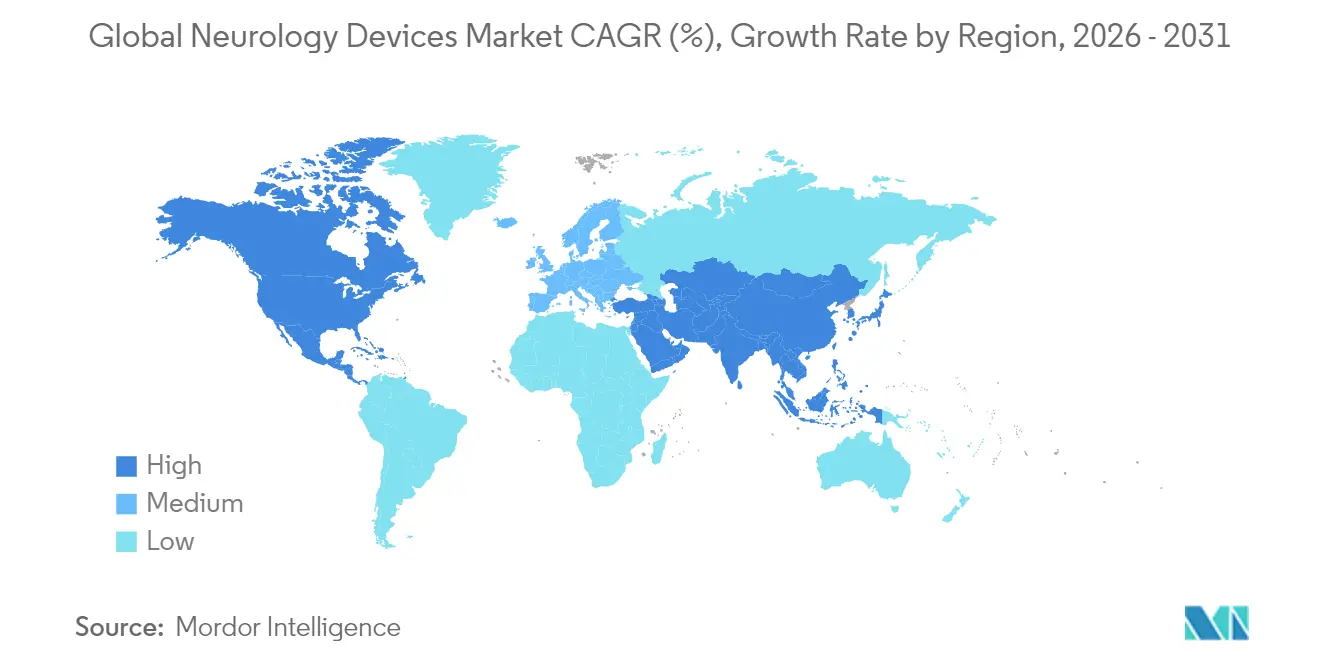

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

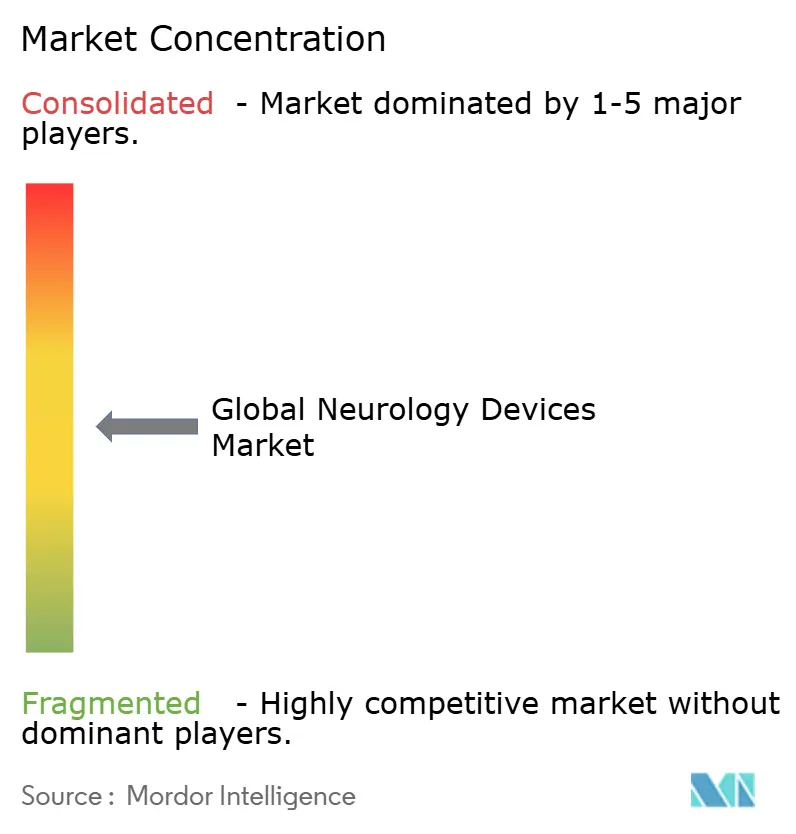

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Neurology Devices Market Analysis by Mordor Intelligence

Neurology Devices market size in 2026 is estimated at USD 15.82 billion, growing from 2025 value of USD 15.10 billion with 2031 projections showing USD 20.02 billion, growing at 4.80% CAGR over 2026-2031. Growth reflects a shift from episodic, hospital-centric interventions to data-rich, predictive care models powered by artificial intelligence and closed-loop neuro-stimulation systems. Demand widens as stroke, Parkinson’s disease, epilepsy and chronic pain remain high-priority public-health issues, and as aging populations intensify the neurological disease burden. Capital inflows, accelerated FDA clearances for adaptive stimulators and breakthroughs in mechanical thrombectomy catheters add momentum, while reimbursement code updates for closed-loop devices reduce payer friction in key markets. Conversely, supply-chain risks around rare-earth magnets and bismuth alloys, together with surgeon shortages in low- and middle-income countries, temper the Neurology Devices market’s full potential.

Key Report Takeaways

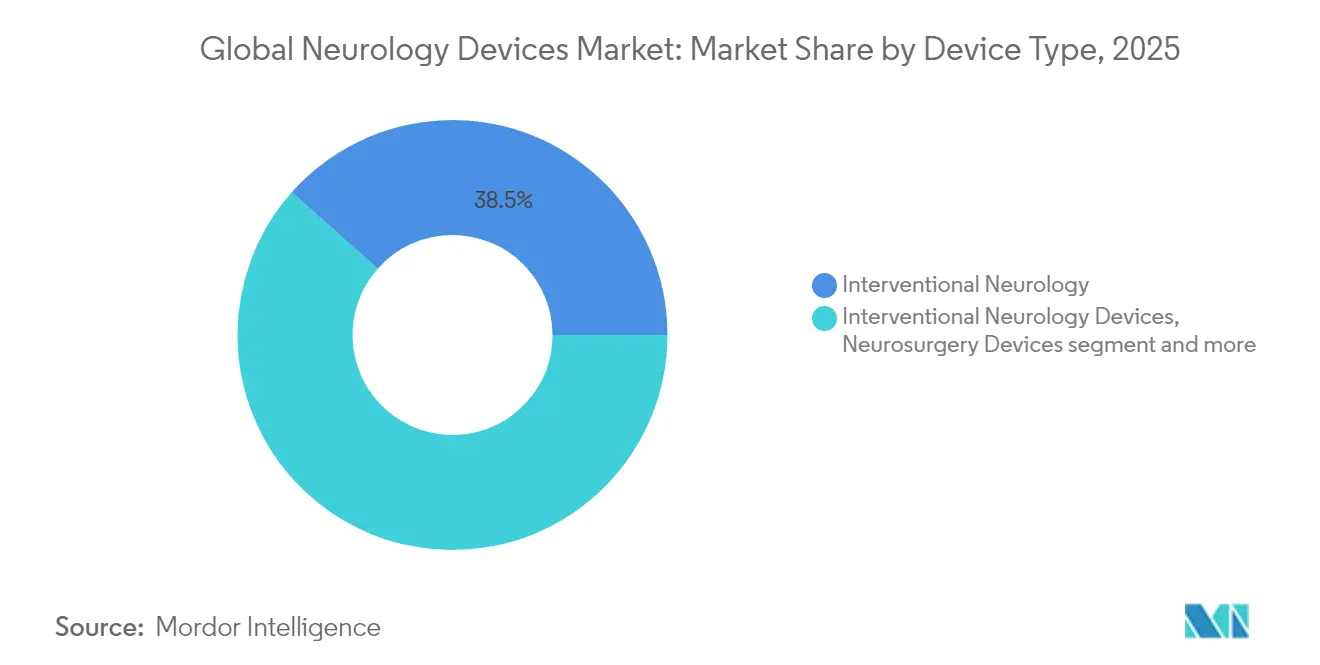

• By device type, interventional neurology led with 38.78% Neurology Devices market share in 2024, whereas neuro-rehabilitation & wearables post the fastest 5.34% CAGR through 2030.

• By application, stroke management accounted for 44.30% of the Neurology Devices market size in 2024; epilepsy treatment is projected to expand at a 5.88% CAGR to 2030.

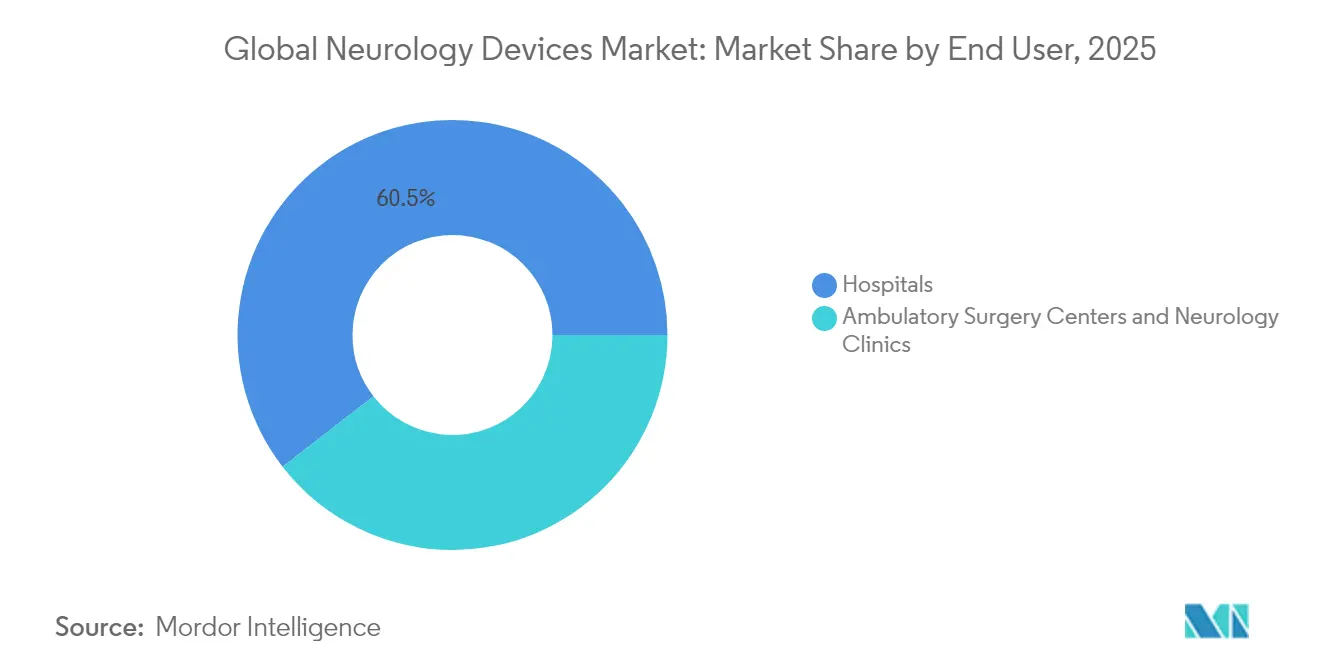

• By end user, hospitals held 61.29% Neurology Devices market share in 2024, while home-care settings register the quickest 6.48% CAGR through 2030.

• By geography, North America commanded 40.67% revenue share in 2024; Asia-Pacific is set to climb at a 7.13% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurology Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of neuro-vascular & neuro-degenerative disorders | +1.2% | Global, highest in North America, Europe, Japan | Long term (≥ 4 years) |

| Technological advances in minimally invasive & image-guided devices | +0.9% | North America & EU leading; APAC adoption accelerating | Medium term (2–4 years) |

| Expanding healthcare spend & neuro-rehab reimbursement schemes | +0.7% | North America & EU core; selective APAC markets | Medium term (2–4 years) |

| AI-enabled closed-loop neuro-stimulation platforms | +0.8% | Global; early adoption in US, Germany, China | Short term (≤ 2 years) |

| Wearable EEG & at-home neuro-monitoring | +0.6% | Global; strong in telehealth-ready markets | Short term (≤ 2 years) |

| Remote-care pilots in neuromodulation | +0.4% | China, Japan; spill-over to emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neuro-vascular & Neuro-degenerative Disorders

Neurological conditions now affect 43% of the global population, expanding the addressable pool for therapeutic devices. . Stroke remains paramount: large-vessel occlusions represent up to 40% of ischemic cases and demand rapid thrombectomy solutions. Post-viral neurological sequelae following COVID-19 and other pathogens further elevate device utilization. Given these epidemiologic realities, the Neurology Devices market continues to prioritise high-efficacy interventions and scalable chronic-disease monitoring strategies.

Technological Advances in Minimally Invasive & Image-Guided Devices

Fourth-generation aspiration catheters, steerable micro-catheters and 300 mT/m gradient MRI scanners shorten procedure time and elevate diagnostic precision. Real-time algorithms embedded in thrombectomy devices improve first-pass success and reduce downstream costs. Interplay of robotics, augmented reality and AI prompts faster learning curves for neurosurgeons, helping address workforce deficits. By raising clinical thresholds, technology upgrades consolidate share for R&D-intensive firms and reinforce entry barriers, affecting long-tail suppliers in the Neurology Devices industry.

Expanding Healthcare Spend & Neuro-rehab Reimbursement Schemes

The United States earmarks 40% of global medical-device spend, with 2025 coding changes (CPT 0735T, 0736T) explicitly covering adaptive stimulators and pulsed RF ablation. Europe’s Diagnosis-Related Group refinements boost post-stroke rehabilitation reimbursement, while Japan’s National Health Insurance now funds home EEG kits. Yet payers cap coverage for emerging modalities such as taVNS, signalling the need for stronger health-economic dossiers. As a result, commercial traction hinges on demonstrable cost offsets, not only technical novelty, within the Neurology Devices market.

Wearable EEG & At-Home Neuro-monitoring Creating New Outpatient Revenue

Miniaturised earbud EEG sensors record data continuously over 24 hours to identify subclinical seizures, reducing inpatient telemetry days by 28% and freeing capacity for acute cases [1]Source: IOP Publishing, “A personalized earbud for non-invasive long-term EEG monitoring,” iopscience.iop.org . Commercial payers in the US reimburse remote EEG reviews at USD 125 per session, creating annuity-style revenue. In Europe and Australia, tele-neurology platforms integrate cloud analytics for early relapse warnings in multiple-sclerosis patients. Consequently, device makers diversify into software-as-a-service, blurring lines between hardware sales and digital-health subscriptions in the Neurology Devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & procedure cost burden | -0.8% | Global; acute in emerging markets | Long term (≥ 4 years) |

| Lengthy & complex regulatory approval cycles | -0.6% | Global; jurisdiction-dependent | Medium term (2–4 years) |

| Shortage of interventional neuro-surgeons | -0.5% | Africa, Southeast Asia | Long term (≥ 4 years) |

| Supply-chain risk for rare-earth materials | -0.3% | Global; China-centric sourcing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device & Procedure Cost Burden

Spinal cord stimulation implants cost USD 35,000–70,000, while revisions add USD 15,000-25,000, limiting penetration among under-insured cohorts Journal of Pain Research. Explant rates hover near 10% owing mainly to efficacy loss, raising total-cost-of-ownership anxieties. In India, detachable coils for aneurysm repair attract import duties of 10%, compounding affordability hurdles MD+DI. Such cost vectors slow adoption despite clinical need.

Lengthy & Complex Regulatory Approval Cycles

Class-III neuro devices may spend 180-365 days in premarket review, extending cash-burn periods for innovators Greenlight Guru. Europe’s MDR elongates time-to-market further through mandatory clinical-benefit demonstration and post-market surveillance audits. Small firms without predicate devices face disproportionate delays, tilting competitive advantage toward established multinationals within the Neurology Devices industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Interventional Neurology Dominates Despite Rehabilitation Surge

Interventional systems captured 38.45% Neurology Devices market share in 2025 as mechanical thrombectomy and flow-diverter implants became standard of care for acute ischemic stroke. Data from the EXCELLENT registry showed final reperfusion rates of 94.5% with the EMBOTRAP retriever, reinforcing physician confidence. Neurodiagnostic monitors, cerebrospinal-fluid shunts and neuro-stimulation implants collectively anchor hospital procurement budgets, while platform upgrades, such as steerable micro-catheters, keep capital-replacement cycles brisk.

Rehabilitation & wearable devices, posting a 5.18% CAGR, increasingly enable post-operative and chronic-disease monitoring at home. In-ear EEG wearables capture seizure precursors, reducing emergency admissions and widening recurring-service revenue. Competitive barriers here hinge on data-analytics IP rather than hardware, inviting tech entrants. Consequently, incumbent catheter and shunt suppliers diversify portfolios to hedge against slower growth in mature theatre-based products.

By Application: Stroke Management Leadership Challenged by Epilepsy Innovation

Stroke care remained pivotal, accounting for 43.88% of the Neurology Devices market size in 2025 through widespread reimbursement of thrombectomy and aspiration catheters. Stanford’s milli-spinner device achieved >90% clot-removal success, illustrating ongoing advances that anchor this segment’s revenue. Yet procedure volumes hinge on rapid hospital arrival, prompting parallel investment in ambulance-based CT scanners.

Epilepsy therapies grow fastest at 5.66% CAGR, powered by adaptive deep-brain stimulators and responsive neuro-stimulation implants that tailor pulses to real-time cortical signals. Broader FDA approvals and home EEG diagnostics expand candidacy pools beyond refractory cases, threatening to narrow stroke’s dominance over the projection period.

By End User: Hospital Dominance Erodes as Home-care Gains Momentum

Hospitals held 60.49% Neurology Devices market share in 2025, underpinned by operating-room infrastructure and intensive-care monitoring needs. Complex interventions, from aneurysm clipping to spinal cord stimulator implantation, still require inpatient settings and multi-disciplinary teams.

Home-care, rising at a 6.17% CAGR, leverages wearable EEG patches and portable rTMS helmets weighing 3 kg, enabling therapy during daily activities Nature Communications. Medicare’s remote-physiologic-monitoring codes reimburse EEG data reviews, improving commercial viability. As device usability improves, the Neurology Devices market progressively decouples volume growth from brick-and-mortar facilities.

Geography Analysis

North America led revenue with 40.27% share in 2025 on the back of robust payer coverage, highly skilled neurologists and R&D ecosystems. Canada’s single-payer model funds nationwide closed-loop SCS trials, while Mexico accelerates MRI procurement via public-private partnerships.

Asia-Pacific posts the quickest 6.92% CAGR, propelled by China’s BCI roadmap and Japan’s remote-care pilots. Government grants subsidise domestic flow-diverter manufacturing, reducing import reliance and bolstering local champions. India logs double-digit growth in detachable-coil sales as its ageing cohort expands, although affordability gaps persist.

Europe remains a steady contributor, emphasising clinical-value demonstration under Medical Device Regulation. Germany’s rising hydrocephalus incidence fuels shunt demand, whereas the United Kingdom pilots AI-triaged stroke pathways that may scale continent-wide. Meanwhile, Switzerland’s potential recognition of FDA approvals streamlines dual-market launches, benefiting US-centric manufacturers.

Competitive Landscape

The Neurology Devices market remains moderately fragmented as the key players hold around half of the total revenue. Medtronic leads neuro-stimulation and stroke intervention, reinforced by the FDA’s first adaptive DBS approval in 2025. Stryker’s USD 4.9 billion takeover of Inari Medical strengthens its vascular-device continuum, adding FlowTriever to its clot-removal suite[2]Source: Stryker Investor Relations, “Stryker completes acquisition of Inari Medical,” investors.stryker.com. Globus Medical’s USD 250 million Nevro purchase delivers pain-therapy scale and closed-loop IP MedTech Dive.

Strategic alliances increasingly blend imaging, AI and hardware. Philips partners with Nvidia to embed neural-network accelerators in BlueSeal MRI scanners, cutting scan time and improving triage accuracy MedTech Dive. GE HealthCare pushes head-only MRI systems with asymmetrical gradient coils for 50% higher neuro-resolution GE HealthCare. Venture funding remains buoyant: neurotech startups secured USD 2.3 billion across 129 deals in 2024, signalling investor appetite for white-space plays in adaptive stimulation and brain–computer interfaces Neurotechnology.

Smaller firms specialise: Imperative Care focuses on Zoom aspiration catheters, Synchron advances endovascular BCIs, and Cerenovus refines aspiration catheter geometry. To compete, incumbents extend service layers such as remote programming and predictive analytics, forging sticky ecosystems. Intellectual-property estates, regulatory muscle and health-economic validation together shape durable advantage in the evolving Neurology Devices industry.

Global Neurology Devices Industry Leaders

Boston Scientific Corporation

Stryker Corporation

B. Braun Melsungen AG

Medtronic PLC

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Medtronic earned FDA clearance for the first adaptive deep-brain stimulation system for Parkinson’s disease

- January 2025: LivaNova filed PMA for the aura6000 hypoglossal nerve stimulator after positive OSPREY trial data

- November 2024: GE HealthCare received 510(k) clearance for SIGNA MAGNUS head-only MRI system with 300 mT/m gradients

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global neurology devices market as revenue generated from new, finished equipment that prevents, diagnoses, monitors, or treats disorders of the central and peripheral nervous systems. This includes neurostimulation, interventional neurology, neurosurgical, cerebrospinal-fluid management, neuro-diagnostic, and neuro-rehabilitation and wearable devices sold through any clinical channel worldwide, valued at end-user transfer price.

Scope exclusion: disposable consumables, imaging reagents, and software-only analytics are not counted.

Segmentation Overview

- By Device Type

- Neurostimulation Devices

- Interventional Neurology Devices

- Neurosurgery Devices

- Cerebrospinal Fluid Management Devices

- Neurodiagnostic & Monitoring Devices

- Neuro-rehabilitation & Wearables

- By Application

- Stroke Management

- Chronic Pain & Movement Disorders

- Epilepsy

- Neuro-degenerative Diseases

- Traumatic Brain & Spinal Injuries

- By End User

- Hospitals

- Ambulatory Surgery Centers

- Neurology Clinics

- Home-care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed neurosurgeons, interventional radiologists, hospital supply managers, and reimbursement consultants across North America, Europe, Asia-Pacific, and Latin America. Conversations clarified average procedure counts, replacement cycles, and likely price erosion, enabling our team to fine-tune model assumptions and stress-test preliminary totals.

Desk Research

We started with public datasets from bodies such as the WHO Neurological Disorders Observatory, OECD Health Statistics, UN Comtrade shipment codes 9018 31 and 9018 90 for electro-medical apparatus, and import tariff books maintained by the USITC. Further inputs came from specialty societies (World Federation of Neurosurgical Societies, Stroke Alliance for Europe) and regulatory filings that disclose installed base or device clearances. Company 10-Ks and investor decks supplied pricing corridors, while news screens on Dow Jones Factiva helped us trace launch timelines. These sources illustrate, but do not exhaust, the evidence pool consulted.

Two gaps remained: regional device mix and real-world utilization, so we explored patents on Questel and sales intelligence on D&B Hoovers to refine adoption curves before cross-checking numbers against hospital procurement portals. Many other references were reviewed to validate and clarify datapoints.

Market-Sizing and Forecasting

A top-down pool built from procedure volumes, stroke prevalence, and neuro OR capacity was reconciled with selective bottom-up supplier roll-ups and sampled ASP times unit checks. Key variables like ischemic stroke incidence, deep-brain stimulation implant rates, average length of stay after neurovascular surgery, export trends of neurodiagnostic units, and Medicare reimbursement shifts anchor the model. Multivariate regression links these drivers with historic revenues, and scenario analysis frames upside or downside cases. Where bottom-up trails lacked depth, gaps were bridged by region-specific penetration factors vetted during expert calls.

Data Validation and Update Cycle

Outputs pass automated variance scans, peer review, and a senior analyst sign-off. We refresh every twelve months, with rapid interim updates when product recalls, major guidelines, or reimbursement revisions materially change market math.

Why Mordor's Neurology Devices Baseline Earns Decision-Makers' Trust

Published estimates differ because firms pick distinct product baskets, price levels, and refresh rhythms. We disclose our scope upfront and apply a consistent currency year so users can trace every jump.

Key gap drivers include varied inclusion of wearable neurotech, contrasting assumptions on average selling price decay, differing base years, and uneven update frequency that skews rapidly innovating segments such as neurovascular thrombectomy.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.10 B (2025) | Mordor Intelligence | - |

| USD 14.30 B (2024) | Global Consultancy A | Wider CAGR applied without procedure controls |

| USD 23.70 B (2023) | Industry Association B | Includes imaging capital assets outside neurology scope |

| USD 25.30 B (2024) | Regional Consultancy C | Uses list prices, updates biennially |

The comparison shows why Mordor's disciplined scope definition, yearly refresh, and dual-path sizing yield a balanced, transparent baseline that managers can rely on when allocating capital or planning product strategy.

Key Questions Answered in the Report

How big is the Global Neurology Devices Market?

The Global Neurology Devices Market size is expected to reach USD 15.82 billion in 2026 and grow at a CAGR of 4.80% to reach USD 20.02 billion by 2031.

What is the current Global Neurology Devices Market size?

In 2026, the Global Neurology Devices Market size is expected to reach USD 15.82 billion.

Who are the key players in Global Neurology Devices Market?

Boston Scientific Corporation, Stryker Corporation, B. Braun Melsungen AG, Medtronic PLC and Abbott Laboratories are the major companies operating in the Global Neurology Devices Market.

Which is the fastest growing region in Global Neurology Devices Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Neurology Devices Market?

In 2025, the North America accounts for the largest market share in Global Neurology Devices Market.

What years does this Global Neurology Devices Market cover, and what was the market size in 2025?

In 2025, the Global Neurology Devices Market size was estimated at USD 15.82 billion. The report covers the Global Neurology Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Neurology Devices Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: