Fault Current Limiter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.21 Billion |

| Market Size (2031) | USD 8.82 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

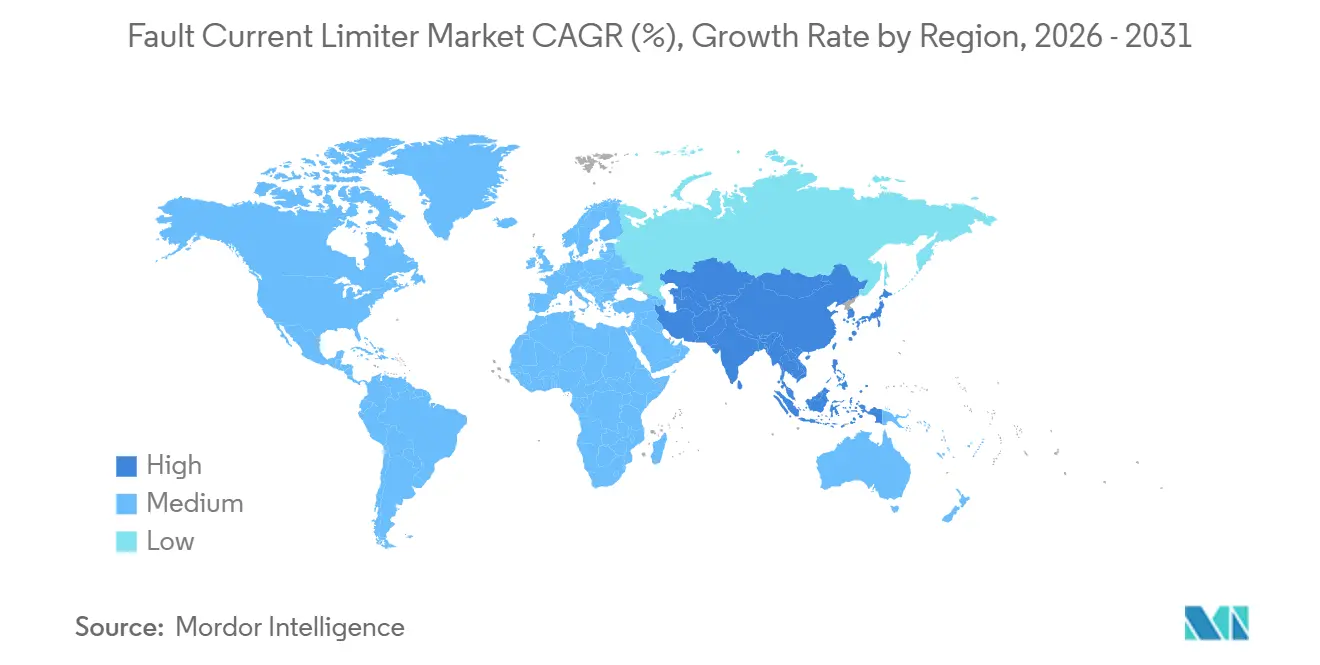

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fault Current Limiter Market Analysis by Mordor Intelligence

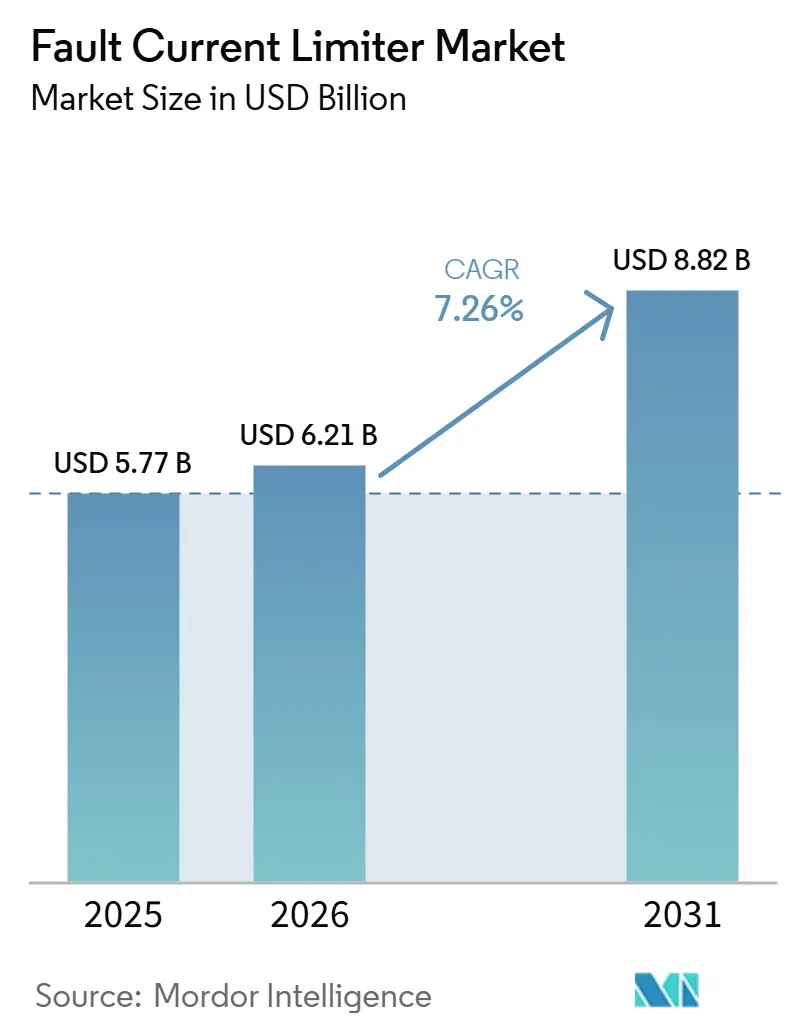

The Fault Current Limiter Market size was valued at USD 5.77 billion in 2025 and is estimated to grow from USD 6.21 billion in 2026 to reach USD 8.82 billion by 2031, at a CAGR of 7.26% during the forecast period (2026-2031). Utilities now view fault-current management as essential for renewable interconnection and data center uptime, driving consistent demand for related equipment. The cost of second-generation high-temperature superconducting (HTS) wire dropping below USD 50 per kA-m has made superconducting devices more widely adopted, while silicon-carbide solid-state designs meet the sub-millisecond response requirements of medium-voltage corridors. Large-scale grid modernization initiatives in China and Japan secure long-lead orders, while regulatory reforms in regions such as California, Germany, and New South Wales enable faster cost recovery, reducing the historical tendency of utilities to delay investments. Vendor competition now focuses on wire performance, cryogenic efficiency, and semiconductor switching speed, indicating a shift toward a technology-driven market rather than one dominated by commodity pricing.

Key Report Takeaways

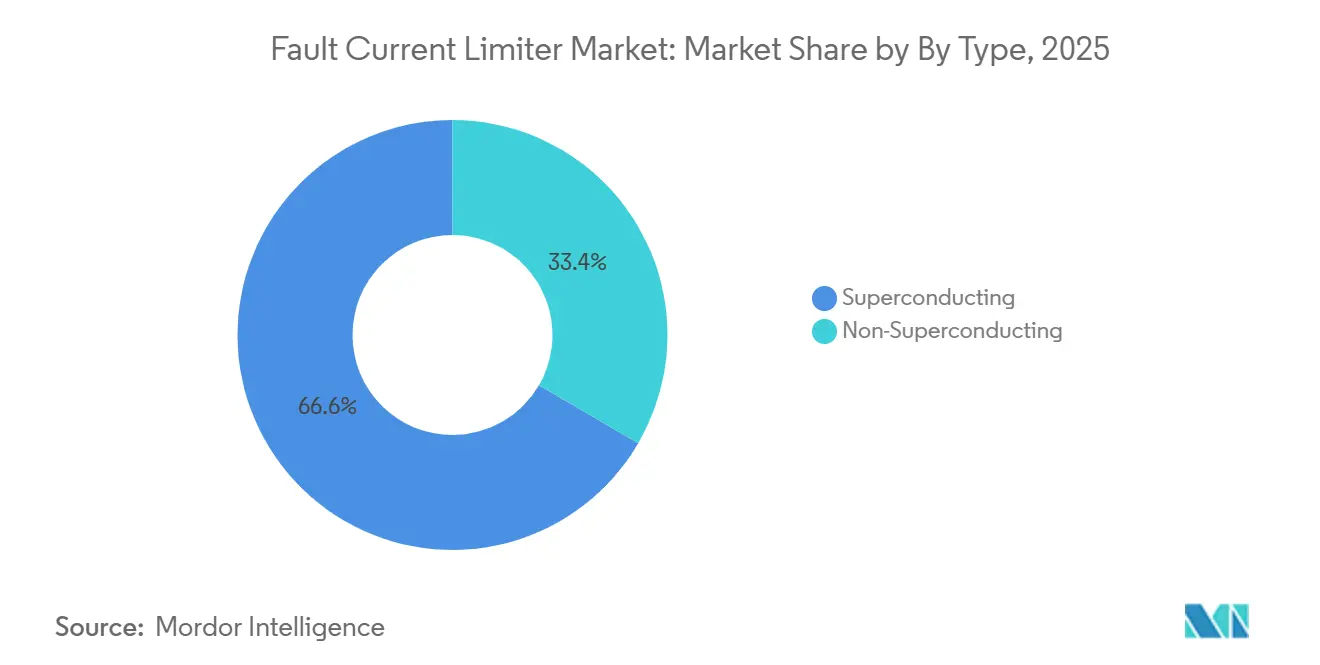

- By type, superconducting devices led with 66.6% of the fault current limiter market share in 2025, while solid-state designs are projected to expand at a 7.6% CAGR through 2031.

- By voltage level, high-voltage (>36 kV) installations commanded 72.8% share of the fault current limiter market size in 2025, whereas medium-voltage (1-36 kV) units are set to advance at a 9.1% CAGR through 2031.

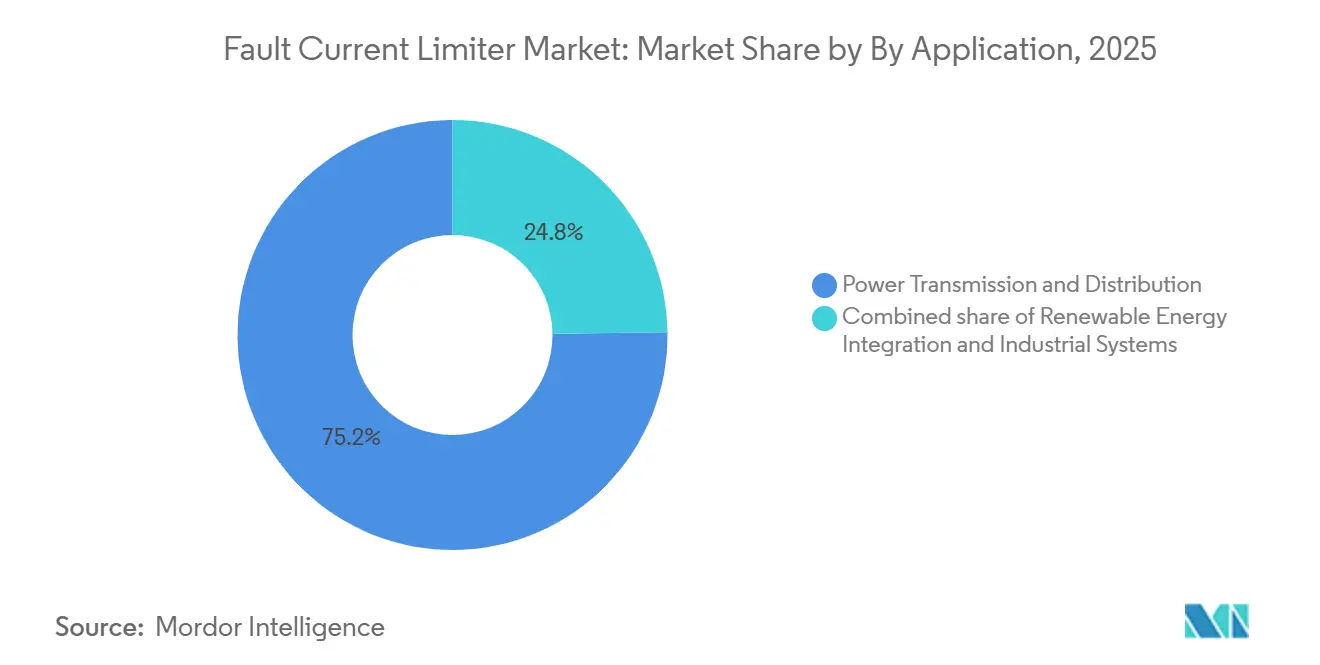

- By application, transmission and distribution accounted for a 75.2% share of the fault current limiter market size in 2025, and renewable energy integration is expected to grow at a 12.4% CAGR through 2031.

- By end-user, utilities held 37.4% spending share in 2025, while transportation infrastructure is expected to progress at a 10.2% CAGR through 2031.

- By geography, Asia-Pacific captured 44.3% revenue in 2025 and is forecast to post the fastest regional CAGR at 7.5% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fault Current Limiter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid grid-capacity expansion mandates (post-2025) | +1.80% | Asia-Pacific core, spill-over to Middle East and South America | Medium term (2-4 years) |

| Surge in renewable energy fault-current incidents | +1.50% | Global, with concentration in Europe offshore wind zones and China solar corridors | Short term (≤ 2 years) |

| Ageing T&D infrastructure in OECD economies | +1.20% | North America and Europe | Long term (≥ 4 years) |

| Mandatory arc-flash safety regulations in data-centres | +0.90% | North America and Europe, early adoption in Singapore and Australia | Medium term (2-4 years) |

| Commercialisation of REBCO HTS wire below USD 50 kA-m cost | +1.00% | Global, with manufacturing concentrated in United States, Japan, and Germany | Medium term (2-4 years) |

| MVDC adoption for offshore wind export cables | +0.80% | Europe (North Sea, Baltic Sea), Asia-Pacific (Taiwan Strait, Yellow Sea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Grid-Capacity Expansion Mandates Drive Near-Term Procurement

Regulators in China, India, and the Gulf Cooperation Council have mandated a 15%-25% expansion in transmission capacity by 2028. However, many substations in these regions are already operating beyond their original interrupting ratings. The State Grid Corporation of China has included fault current limiters in its 2025 purchasing code for all new 220 kV renewable-zone substations. This measure ensures a steady order flow while reducing breaker upgrade capital expenditures by up to 60%. In July 2025, a network event in the Czech Republic caused currents to surge to 63 kA on equipment rated for 50 kA, prompting Central European utilities to accelerate their purchase schedules. By installing fault current limiters, breaker replacements can be deferred by 8-12 years, smoothing capital expenditures and reducing regulatory pressures.

Renewable Energy Fault-Current Incidents Shift Protection Philosophy

Aggregated inverters deliver sustained, semiconductor-limited fault currents that complicate relay coordination. The Nan’ao three-terminal VSC-HVDC project showed a 53% current reduction within 7 ms using a 160 kV superconducting limiter.(1)IEEE Power & Energy Society, “Resistive SFCL Performance in Nan’ao VSC-HVDC,” ieee.org Germany's VDE FNN guideline, issued in October 2025, mandates the inclusion of impedance-limiting devices in large photovoltaic and battery plants. Grid operators, particularly those with renewable penetration exceeding 50%, prioritize fault-limiting over fault-clearing as the primary measure to prevent significant voltage sags.

Ageing T&D Infrastructure in OECD Economies Creates Retrofit Demand

Breakers installed in North America and Europe between 1970 and 1995 were designed to handle fault currents of 25-40 kA but are now encountering levels exceeding 50 kA. ABB's IS-limiter, tested by UK networks, can interrupt fault currents in less than 1 millisecond at levels up to 210 kA, thereby extending the operational life of switchgear by 15-20 years. The European Union's 2024 resilience regulations classify fault current limiters as reinforcement, enabling accelerated depreciation schedules and reducing the payback period to 7 years for incentive-regulated utilities.

Commercialisation of REBCO HTS Wire Unlocks Utility-Scale Projects

In 2024, HTS wire prices dropped below USD 50 per kA-m, making superconducting limiters economically viable for applications above 100 MVA. American Superconductor reported FY 2024 revenue of USD 222 million, with approximately 10% attributed to limiter-grade wire. Pulled-laser and MOCVD processes increased production capacity fivefold between 2020 and 2025, enabling utilities to place orders for multi-kilometer batches with reliable lead times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cryogenic OPEX for utility-scale SFCLs | -0.70% | Global, with higher impact in regions lacking liquid-nitrogen infrastructure (Middle East, Africa, South America) | Medium term (2-4 years) |

| Absence of IEC/IEEE type-testing protocols above 63 kA | -0.50% | Global, with concentration in Asia-Pacific and Europe where >63 kA projects are planned | Short term (≤ 2 years) |

| Procurement risk from HTS tape supply concentration | -0.40% | Global, with highest impact in Asia-Pacific and Europe dependent on U.S. and Japanese suppliers | Medium term (2-4 years) |

| Utilities' CAPEX deferral culture amid rate-base pressure | -0.60% | North America and Europe, where regulatory lag discourages preemptive investment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cryogenic OPEX for Utility-Scale SFCLs Limits Adoption in Emerging Markets

Maintaining a temperature of 77 K incurs an annual cost of USD 20,000-30,000 per device. In regions without established liquid-nitrogen logistics, supply costs can be 2-3 times higher, extending the payback period to over 15 years. Korea Electric Power's 22.9 kV pilot recorded an average cryocooler power consumption of 8 kW, resulting in an annual cost of approximately USD 7,000 based on local electricity tariffs, emphasizing the sensitivity of operational expenses. Closed-cycle cryocoolers and materials operating above 90 K are currently in the pilot phase and are not expected to be commercialized before 2028.

Utilities’ CAPEX Deferral Culture Amid Rate-Base Pressure Delays Technology Adoption

Utilities in North America and Europe frequently delay new deployments until standards organizations release detailed type-testing protocols. According to the U.S. Department of Energy, current laboratories are unable to conduct tests combining above 63 kA and over 245 kV within a single facility, which extends approval timelines. Under pressure to avoid perceptions of overspending, decision-makers often opt for incremental reinforcements, restricting the short-term adoption of advanced limiters despite their demonstrated technical advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Superconducting Devices Still Dominate but Solid-State Growth Accelerates

Superconducting units accounted for 66.6% of the fault current limiter market share in 2025, driven by their capability to reduce currents by 50%-70% within 2-5 milliseconds while occupying 40% less space compared to reactors. In contrast, solid-state designs are projected to grow at a CAGR of 7.6% through 2031, supported by silicon-carbide switches that interrupt currents in less than 200 microseconds and eliminate the need for cryogenic maintenance. The fault current limiter market size for superconducting devices is projected to climb alongside REBCO wire cost declines, yet their share will slip as data-center, rail, and MVDC buyers favor maintenance-free electronics.(2)Nexans, “Rail-Specific SFCL Deployment on Belfort-Delle,” nexans.com

Solid-state limiters leverage traction-inverter supply chains, enabling companies like ABB, Eaton, and Schneider Electric to provide integrated protection solutions. Inductive-resistive hybrids continue to serve a retrofit niche, particularly in cases where utilities prioritize simplicity over response speed. A trend of technology convergence is evident, with vendors developing hybrid superconducting-solid-state stacks to handle duties exceeding 100 kA, where no single topology is adequate. As utilities increasingly demand modular and digitally monitored assets, platform flexibility is emerging as a more critical factor than physical performance alone.

By Voltage Level: Medium-Voltage Solutions Gain Momentum in Distributed Grids

High-voltage systems (above 36 kV) accounted for 72.8% of revenue in 2025. However, medium-voltage demand is growing at a compound annual growth rate (CAGR) of 9.1%, driven by factors such as rooftop solar installations, battery storage systems, and 400 kW-plus electric vehicle (EV) chargers, which increase distribution fault levels beyond breaker limits. The medium-voltage segment of the fault current limiter market is projected to nearly double in size by 2031, narrowing the value gap with high-voltage systems. For example, LS Electric’s 22.9 kV modular superconducting fault current limiter (SFCL) reduces the footprint by 70% compared to traditional air-core reactors and can be integrated into existing pad-mount enclosures.

The adoption of high-voltage systems remains dependent on standardized testing. Until the International Electrotechnical Commission (IEC) extends testing protocols beyond 63 kA, growth in this segment is expected to remain moderate. Additionally, medium-voltage direct current (MVDC) offshore wind export cables operating at ±30-80 kV are challenging traditional classifications, requiring high-voltage energy absorption capabilities within a medium-voltage framework. Vendors capable of scaling a single design across voltage ranges from 12 kV to 220 kV with standardized controls are well-positioned to capture a significant market share.

By Application: Renewable Integration Surpasses Traditional T&D Growth

In 2025, the transmission and distribution segment accounted for 75.2% of revenue, driven by the retrofit wave in legacy substations. Meanwhile, renewable energy plants are experiencing a compound annual growth rate (CAGR) of 12.4%, as grid codes mandate inverter-based resources to remain operational during faults. Germany's VDE FNN regulation incorporates limiters into future photovoltaic (PV) and energy storage projects, ensuring consistent procurement pipelines. Additionally, industrial complexes and semiconductor manufacturing facilities prioritize millisecond isolation to avoid costly downtime, supporting mid-single-digit growth in this segment.

Renewable energy developers are increasingly specifying limiters during engineering, procurement, and construction (EPC) bidding processes to secure grid-connection permits. This approach transforms what was previously a post-commissioning retrofit into an upfront capital expenditure. As a result, ordering cycles are accelerating, and vendors are shifting toward offering integrated inverter-protection solutions through EPC channels rather than relying on utility master agreements.

By End-User: Transportation Outpaces All Other Segments

Utilities accounted for 37.4% of spending in 2025, maintaining their dominant position. However, rail, metro, and EV-charging infrastructure are projected to grow at an annual rate of 10.2% through 2031. SNCF Réseau’s Belfort-Delle installation demonstrated significant rail traction improvements, encouraging similar projects across Asia’s high-speed rail corridors. Data centers and semiconductor fabrication facilities, categorized under commercial end-users, achieve the highest unit margins as operators view current limiters as essential safeguards against downtime and regulatory penalties.

Transportation projects increasingly incorporate limiters with regenerative braking systems and medium-voltage direct current (MVDC) overhead lines. This approach often bypasses utility approval processes, enabling faster project implementation. Additionally, the growing procurement expertise of non-utility buyers is diversifying vendor pipelines and mitigating revenue risks associated with fluctuations in utility budgets.

Geography Analysis

The Asia-Pacific region is projected to account for a 44.3% market share in 2025 and is expected to register the highest regional CAGR of 7.5% through 2031. China's requirement for limiters in all 220 kV renewable-zone substations and Japan's superconducting rail projects provide sustained demand visibility over multiple years. Korea Electric Power’s 22.9 kV trial underscores regional willingness to deploy cryogenic solutions where grid density justifies premium equipment.

In Europe, demand is primarily driven by offshore wind projects and HVDC (High Voltage Direct Current) rollouts. For example, NKT’s 525 kV Scottish links, contracted for January 2026, demonstrate how converter-station specifications now routinely include current limiters. Regulatory clarity under the RIIO-ED2 framework in the United Kingdom and incentive mechanisms within Germany’s Energiewende are contributing to a steady increase in adoption.

In North America, demand remains lower as investor-owned utilities have historically deferred capital expenditures. However, states like California and New York have permitted out-of-rate-case recovery for limiter installations, which is expected to strengthen the 2026-2028 project pipeline. In the Middle East, Oman’s planned deployment in June 2025 marks an early adoption effort aimed at avoiding expensive breaker replacements. Meanwhile, South America is still in the early stages, but updates to grid codes in Brazil and Chile, requiring fault-ride-through capabilities after 2027, indicate potential growth beyond the forecast period.

Competitive Landscape

The market is moderately concentrated, with key players focusing on distinct technological advancements. Superconducting specialists such as American Superconductor, SuperPower, and Zenergy Power compete on high-temperature superconducting (HTS) performance and cryogenic efficiency. Meanwhile, solid-state companies like Eaton and Schneider Electric utilize their power-electronics portfolios to achieve sub-200 µs interruption times without relying on liquid nitrogen. American Superconductor’s acquisition of Megatran in August 2024 has expanded its transformer capabilities, enabling the company to offer comprehensive substation packages and strengthen its appeal to utilities seeking single-vendor solutions.

Emerging players such as Israel’s GridON and South Korea’s LS Electric are introducing innovative approaches. GridON’s Horizon 2020 project aims to reduce unit costs by 25%-50% through the use of advanced magnetic alloys. LS Electric, on the other hand, is testing modular superconducting fault current limiters (SFCLs) in collaboration with Korea Electric Power, with plans to target Southeast Asian microgrids. The industry’s technology roadmaps are converging on hybrid superconducting-solid-state systems capable of interrupting currents exceeding 100 kA, addressing scenarios where no single technology is sufficient.

Intellectual property challenges are on the horizon, as key patents held by American Superconductor are set to expire after 2027. This could lower entry barriers for Asian wire manufacturers scaling metal-organic chemical vapor deposition (MOCVD) production lines. In response, vendors are prioritizing long-term service contracts and digital monitoring solutions to secure recurring revenue streams beyond hardware sales.

Fault Current Limiter Industry Leaders

ABB Ltd

Siemens Energy AG

Nexans SA

Toshiba ESS

American Superconductor Corporation (AMSC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NKT has secured contracts with SSEN Transmission for two 525 kV HVDC turnkey transmission links in northern Scotland. These include the Western Isles link, spanning 170 kilometers with a capacity of 1.8 GW, and the Spittal to Peterhead link, covering 210 kilometers with a capacity of 2.0 GW. The total order value is approximately EUR 2.0 billion (around USD 2.1 billion). Both projects will involve the installation of fault current limiters at converter stations to protect semiconductor valves from DC-side faults. Commissioning is planned for 2030.

- February 2025: LS Electric presented HypergridNX, an integrated superconducting power solution, at Elecs Korea and the Korea Smart Grid Expo 2025. This solution combines superconducting fault current limiters and superconducting cables, specifically designed for hyperscale AI data centers housing over 100,000 servers. It reduces fault currents within 1 to 2 milliseconds, improving power reliability and efficiency for large-scale internet data centers.

- June 2024: ABB secured contracts from Red Eléctrica to supply synchronous condensers aimed at enhancing grid stability in the Canary and Balearic Islands during the renewable energy transition.

- May 2024: The geomagnetic storm in the United Kingdom caused geomagnetically induced currents exceeding 60 amperes in multiple substations, underscoring the grid's vulnerability to space weather events.

Global Fault Current Limiter Market Report Scope

A Fault Current Limiter (FCL) is a protective device in electrical power systems designed to automatically restrict the high current that flows during a short circuit or fault. It acts as a rapid, high-impedance barrier, typically within half a cycle, to prevent equipment damage, enhance grid stability, and reduce the interrupting rating required for circuit breakers.

The fault current limiter market report is segmented by type, voltage level, application, end-user, and geography. By type, the market is segmented into superconducting and non-superconducting. By voltage level, the market is segmented into medium voltage (1-36 kV) and high voltage (above 36 kV). By application, the market is segmented into power transmission and distribution, industrial systems, and renewable energy integration. By end-user, the market is segmented into utilities, industrial, commercial, and transportation. The report also covers the market size and forecasts for the fault current limiter market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Superconducting |

| Non-Superconducting |

| Medium Voltage (1 to 36 kV) |

| High Voltage (Above 36 kV) |

| Power Transmission and Distribution |

| Industrial Systems |

| Renewable Energy Integration |

| Utilities |

| Industrial |

| Commercial |

| Transportation (Rail, E-Mobility Hubs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Superconducting | |

| Non-Superconducting | ||

| By Voltage Level | Medium Voltage (1 to 36 kV) | |

| High Voltage (Above 36 kV) | ||

| By Application | Power Transmission and Distribution | |

| Industrial Systems | ||

| Renewable Energy Integration | ||

| By End-User | Utilities | |

| Industrial | ||

| Commercial | ||

| Transportation (Rail, E-Mobility Hubs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the fault current limiter market?

The fault current limiter market size stands at USD 6.21 billion in 2026 and is projected to reach USD 8.82 billion by 2031.

Which technology leads global installations?

Superconducting fault current limiters commanded 66.6% revenue share in 2025, though solid-state devices are the fastest-growing segment.

Why are data-center operators investing in fault current limiters?

New arc-flash safety rules and uptime targets push hyperscale facilities to install limiters that cut fault currents within 1-2 ms, reducing hazard levels and unplanned outages.

Which region shows the fastest growth?

Asia-Pacific is forecast to expand at 7.5% CAGR through 2031, propelled by state-mandated deployments in China, Japan, and South Korea.

How do fault current limiters help renewable plants?

They limit inverter fault currents, enabling photovoltaic and battery assets to meet grid-code ride-through requirements without tripping offline.

Page last updated on: