Automotive Fuse Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

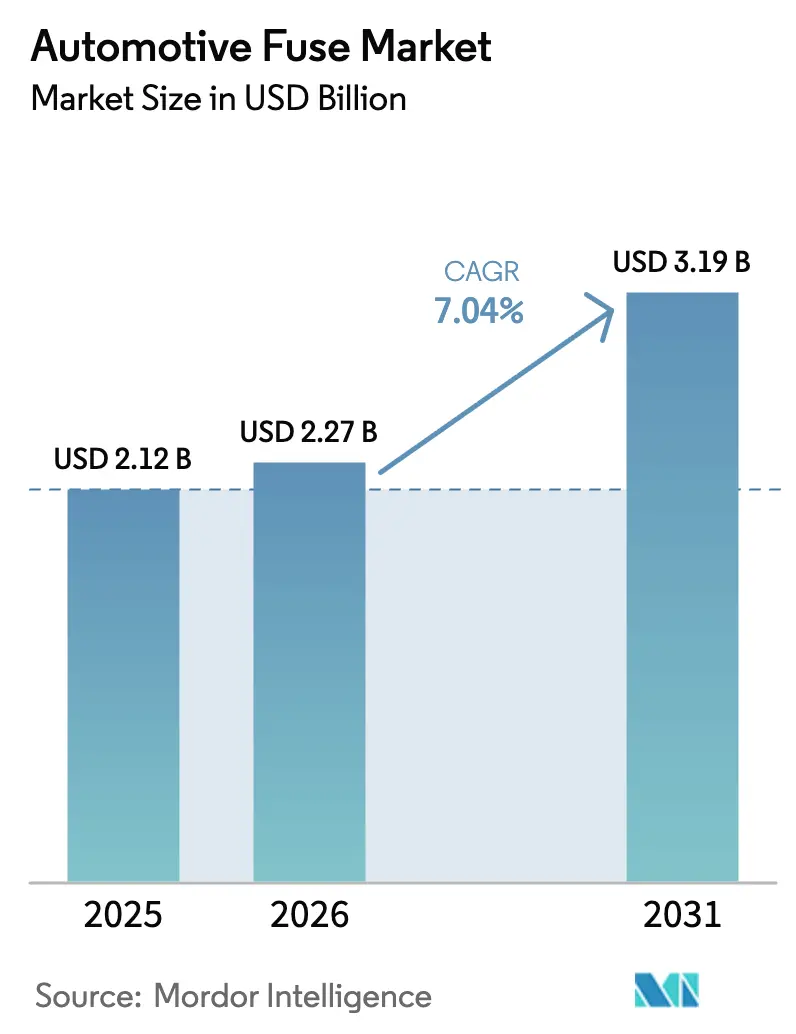

| Market Size (2026) | USD 2.27 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Fuse Market Analysis by Mordor Intelligence

The automotive fuse market size was valued at USD 2.12 billion in 2025 and estimated to grow from USD 2.27 billion in 2026 to reach USD 3.19 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031). Rapid vehicle electrification, growth in 48 V architectures, and rising electronic content per vehicle collectively encourage OEMs to specify advanced over-current protection that moves beyond legacy blade designs. High-voltage battery packs rated up to 1,000 V now dominate new EV platforms, prompting fuse makers to adapt materials, melting elements, and thermal management for safe DC interruption. OEM preference for smart, self-resettable units accelerates the transition toward electronic fusing while regulators tighten rules that favor qualified, traceable components. The dual effect of stricter safety norms and expanding on-board computing drives consistent demand across passenger, commercial, and specialty vehicle programs.

Key Report Takeaways

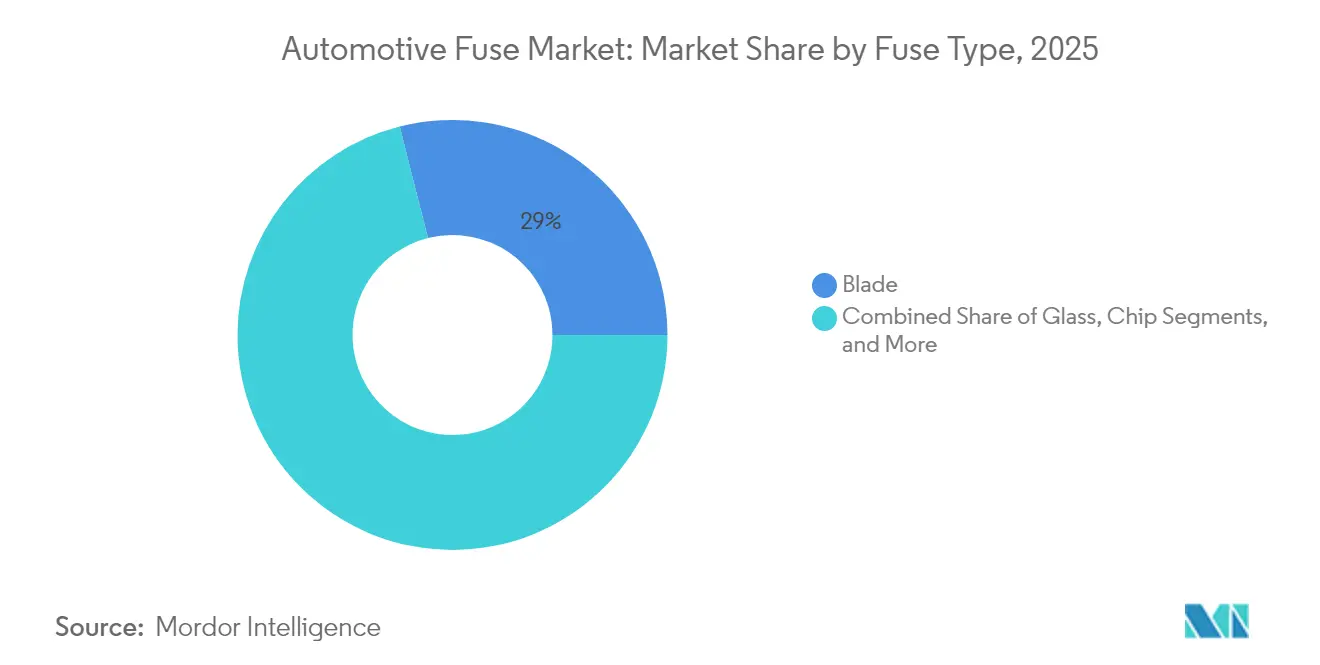

- By fuse type, blade fuses led with 28.95% of the automotive fuse market share in 2025, while high-voltage fuses are forecast to grow at an 8.59% CAGR through 2031.

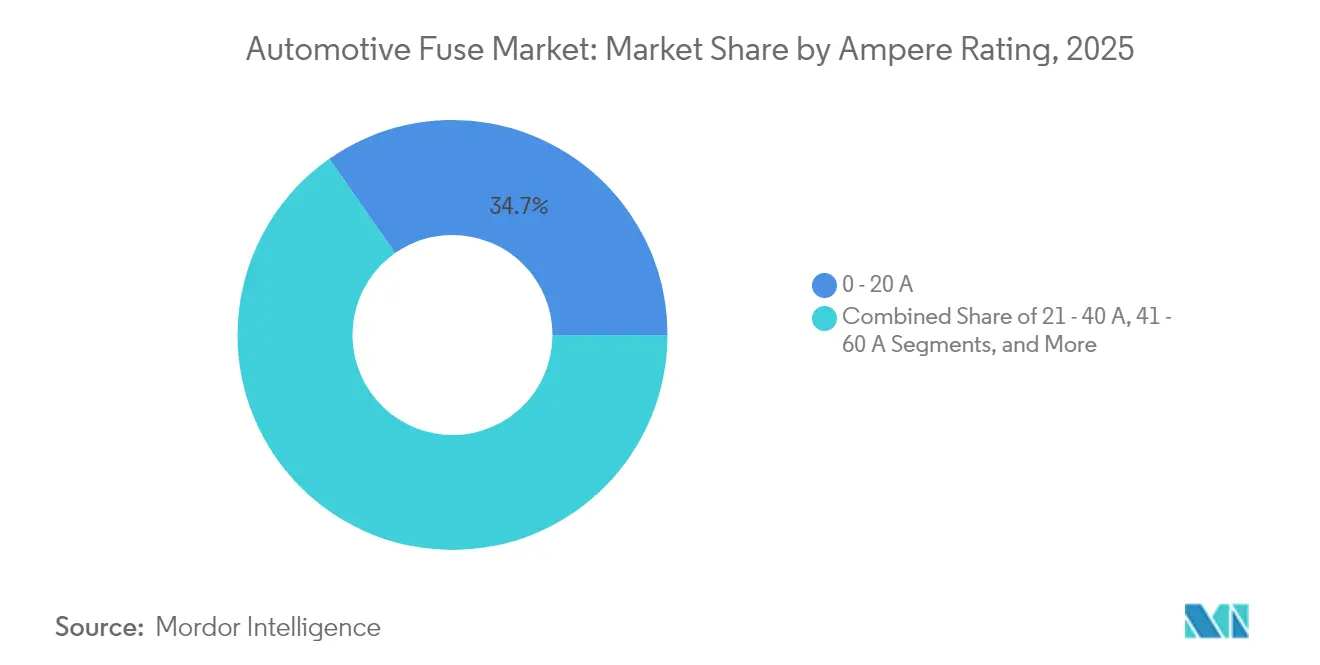

- By ampere rating, the 0–20 A class captured 34.72% share of the automotive fuse market size in 2025, and the > 60 A class is advancing at an 8.76% CAGR to 2031.

- By vehicle type, passenger cars held 60.65% revenue share in 2025; battery electric vehicles will expand at a 8.95% CAGR during the forecast period.

- By geography, Asia-Pacific commanded a 62.70% share in 2025 and is projected to post a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Fuse Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in electric-vehicle production volume | +2.1% | China, Europe, North America | Medium term (2-4 years) |

| Higher electronic content per vehicle (ADAS, infotainment) | +1.8% | Premium segments globally | Long term (≥ 4 years) |

| Stringent safety norms mandating circuit-protection devices | +1.3% | Europe, North America, and expanding to the Asia-Pacific | Medium term (2-4 years) |

| Growth of connected commercial-vehicle telematics | +0.9% | North America, Europe, adoption in Asia-Pacific | Long term (≥ 4 years) |

| Adoption of 48 V mild-hybrid architectures | +0.7% | Europe, China, expanding globally | Medium term (2-4 years) |

| OEM shift toward smart self-resettable fuse modules | +0.4% | Premium segments globally, early adoption in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Electric-Vehicle Production Volume Drives Specialized Protection Demand

Electric-vehicle momentum is reshaping every layer of the automotive fuse market. Battery packs now operate at 400 V, 800 V, or even 1,000 V, forcing manufacturers to deliver fuses with DC interrupting capacities up to 30 kA and robust I²t values that stay stable across wide temperature windows. High-energy charging events create significant thermal stress, so vapor-phase solder, ceramic bodies, and silver elements are used to maintain low resistance under continuous load. The segment additionally boosts demand for pyrotechnic battery-disconnect fuses that open within 2 milliseconds during collisions, a capability now commercialized by Eaton.[1]Source: Eaton, “EV Pyro Fuse,” eaton.com Together, these requirements shift the automotive fuse market toward higher unit price points and deeper supplier qualification cycles.

Higher Electronic Content per Vehicle Amplifies Protection Requirements

Modern driver-assistance suites combine cameras, radars, and lidar sensors that draw varying peak currents during data acquisition. A single Level 2+ platform can host 100+ control units that each require primary and secondary over-current devices. Analog Devices highlights the need for low-profile fuses capable of withstanding cold-crank inrush without nuisance trips while still clearing short circuits within milliseconds.[2]Source: Analog Devices, “ADAS and Safety Solutions,” analog.comThe shift to software-defined vehicles keeps multiple power domains active at all times, leading to miniaturized surface-mount fuses rated up to 1,000 V DC in 5 × 20 mm footprints. Continuous connectivity heightens expectations for zero-downtime electrical architectures, which in turn stimulates demand for smart fuse modules that relay real-time current data to central gateways.[3]Source: Aptiv, “What Is Smart Fusing?,” aptiv.com

Stringent Safety Norms Mandate Advanced Circuit Protection

Global Technical Regulation No. 20 and ISO 8820-8 set minimum performance thresholds covering interrupt rating, temperature rise, and vibration durability for high-voltage fuses.[4]Source: Global Forum for Harmonization of Vehicle Regulations, “Electric Vehicle Safety GTR,” globalautoregs.com Compliance requires multilayer protection: pack level, module level, and charger inlet level. Extensive third-party testing elevates entry barriers for unqualified suppliers, steering OEM sourcing toward established players with AEC-Q200 track records. The National Highway Traffic Safety Administration’s make-inoperative prohibition further drives genuine part replacement throughout the vehicle life cycle. Together, these mandates secure recurring revenue streams for certified fuse vendors and stabilize quality benchmarks across the automotive fuse market.

Adoption of 48 V Mild-Hybrid Architectures Creates Intermediate Voltage Opportunities

Europe-led adoption of 48 V electrification bridges the gap between 12 V legacy and 400 V high-voltage systems. TE Connectivity reports that board-level current demands in 48 V domains can exceed 200 A during start-stop and e-booster events. Specialized mini-blade and bolt-on fuses rated 60–125 V DC ensure safe energy flow while fitting existing fuse boxes. These architectures enable regenerative braking and torque assist in mainstream models, multiplying fuse attachment points across auxiliary compressors, electric turbochargers, and power steering modules. The mid-voltage zone thus adds depth to the automotive fuse market without cannibalizing traditional 12 V requirements.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising preference for solid-state power-distribution units | -1.4% | Premium segments in developed markets | Long term (≥ 4 years) |

| Shrinking ICE vehicle parc in mature markets | -1.1% | North America, Europe, Japan | Medium term (2-4 years) |

| Limited standardization of high-amp micro-blade formats | -0.6% | Global, with fragmentation across regions | Medium term (2-4 years) |

| Ceramic-substrate supply-chain concentration | -0.3% | Global dependency on Asia-Pacific suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Solid-State Power-Distribution Units Challenges Traditional Fuses

Semiconductor-based e-fuses interrupt faults within microseconds and recover by command, eliminating physical replacement cycles. They integrate current sensing, thermal shutdown, and diagnostics that align with zonal architectures favored by premium EV makers. The cost premium and cooling complexity restrict use to higher trim levels today, but falling silicon prices signal a gradual spread into mid-market models. Conventional fuse suppliers respond by embedding sense resistors and digital interfaces into familiar housings to slow share erosion. This technology tug-of-war will temper volume growth for passive fuse formats even as total protection spending climbs.

Shrinking ICE Vehicle Production in Mature Markets Constrains Traditional Fuse Demand

Passenger car parc growth in the United States and Western Europe has flattened, with vehicle ages reaching 12 years or more. As OEMs accelerate EV launches, production lines for combustion models face consolidation, reducing yearly demand for low-voltage blade and cartridge fuses. Association of Equipment Manufacturers notes that component vendors now pivot toward aftermarket channels where replacement cycles extend further than original equipment demand. While electrified platforms inject high-value fuse opportunities, the net unit volume from ICE decline removes a structural layer of baseline growth from the automotive fuse market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuse Type: High-Voltage Variants Gain Momentum

The fuse-type hierarchy continues to evolve. Blade designs remained dominant with a 28.95% automotive fuse market share in 2025 due to low cost and entrenched distribution. Nevertheless, high-voltage cylinders, EV-specific bolt-ins, and pyrotechnic links together post an 8.59% CAGR, outpacing every other category. The automotive fuse market size for high-voltage devices benefits from the rising 400 V and 800 V battery pack adoption. OEM engineers favor silver-plated terminals and sand-filled bodies for stable arc extinction across wide ambient ranges. In response, Littelfuse released the 823A SMD fuse rated at 1,000 V DC, combining miniaturization with 63 A continuous current capability.

Innovation also manifests in smart micro-blade fuses equipped with integrated current sensors. These units enable predictive maintenance analytics within zonal gateways and are gaining pilot adoption in European premium brands. Glass tube fuses retain small niches in aftermarket accessories, while slow-blow formats protect HVAC blowers and seat-adjust motors where startup inrush peaks. Chip fuses ride the adoption wave of compact control modules, especially in radar and camera ECUs that demand low inductance and high surge capability.

By Ampere Rating: > 60 A Class Sees Fastest Growth

Low-current 0–20 A fuses formed 34.72% of overall shipments in 2025, covering interior lighting, infotainment, and mid-tier ADAS domains. As EV architectures mature, powertrain inverters and onboard chargers create fresh demand at 400–600 A levels. This trend propels the > 60 A bracket to an 8.76% CAGR and lifts the automotive fuse market size for high-current devices. Sand-filled ceramic barrels with silver alloy elements dominate here because they keep the temperature rise below 90 °C at full load. ISO 8820 committee revisions now recommend extra insulation creepage for devices above 500 A at 1,000 V.

Mid-range 21–60 A segments still carry steering pumps, door modules, and 48 V e-turbo feeds. As mild hybrids proliferate, 48 V belt-starter generators draw 180 A peak, prompting modules that stack two 125 A links in parallel. Fuse vendors exploit this mix by offering modular holders that accept various ratings without retooling wiring harnesses. Continuous densification of electronics keeps every ampere band relevant, ensuring balanced revenue streams across the automotive fuse market.

By Vehicle Type: Electrified Platforms Shape Protection Profiles

Passenger cars captured 60.65% of worldwide revenue in 2025, backed by strong volumes in China and North America. Battery electric cars, vans, and SUVs register a 8.95% CAGR through 2031, lifting the automotive fuse market size for high-voltage components. Pack protection uses bolt-on fusible links at the module and string levels. Commercial trucks evolve in parallel, adding 48 V and 800 V subsystems for e-axle drives that require multiple fuse families.

Hybrid and plug-in hybrid models act as a bridge, hosting both 12 V blade and 400 V cylindrical fuses in a single vehicle. Fuel-cell prototypes introduce yet another layer that demands hydrogen sensor guarding and high-voltage, low-temperature endurance. Each drivetrain pathway enlarges the total attachment points per vehicle, balancing any unit loss from shrinking pure ICE cohorts. The result sustains aggregate growth across the entire automotive fuse market.

Geography Analysis

Asia-Pacific maintained a 62.70% share in 2025 and is forecast to have a 9.05% CAGR through 2031. Continuous EV policy support in China and the local presence of tier-one electronics suppliers shorten development cycles, so new fuse formats reach mass production rapidly. Japan advances semiconductor materials that underpin compact surface-mount fuses, while South Korea leverages lithium-ion battery dominance to co-develop pack protection devices with global OEMs.

North America shows stable but opportunity-rich dynamics. U.S. automakers invest in large battery pickup and delivery van lines, each equipped with dual-stage pyro fuses. The newly approved Inflation Reduction Act credits on domestically produced EVs accelerate adoption, bolstering regional demand for high-value protection modules. Canadian tier-twos escalate aluminum wire harness production, creating incremental requirements for compatible terminal plating on fuse leads.

Europe maintains a leadership stance on safety regulation and premium vehicle export. Euro NCAP integrates ADAS availability into its star rating, driving electronic redundancy and multiple fuse layers. German suppliers push smart power distribution units that blend solid-state switches and removable links, reflecting the region’s early migration toward zonal architectures.

Emerging Middle East and African assembly clusters remain small today but attract investment for knock-down EV kits that will need localized fuse sourcing. Collectively, the geographic spread preserves growth potential across the global automotive fuse market.

Competitive Landscape

The automotive fuse market features moderate fragmentation. Littelfuse, Eaton, and Mersen retain broad portfolios spanning low-voltage blades to 1,000 V EV cylinders, giving them scale economies in tooling and testing. Littelfuse’s 823A Series SMD launch underscores a pivot toward compact, high-voltage formats that support battery management systems. Eaton, by contrast, leans on pyro-fuse technology that interrupts 20 kA short-circuit currents within 2 milliseconds, addressing crash isolation needs.

Semiconductor houses, such as onsemi, inject competition through fully electronic e-fuses that integrate current sensing and reset logic. These solutions appeal to OEMs pursuing wire-count reduction via zonal designs. TE Connectivity and Aptiv fast-track adaptable fuse holders and smart junction boxes that simplify upgrading from mechanical to solid-state units. Meanwhile, Gentex widens its portfolio through acquisitions that add audio and biometric modules, signaling convergence between protection, sensing, and infotainment.

Strategic partnerships center on material innovation. Ceramic substrate specialists such as Shandong Sinocera collaborate with fuse makers to deliver low-thermal-resistance bodies needed for 350 kW charging sessions. ISO and IEC committees sustain technical barriers that shield incumbents by mandating rigorous test programs. Overall, players that marry diagnostics, high-voltage tolerance, and global certification retain a competitive advantage in the growing automotive fuse market.

Automotive Fuse Industry Leaders

Littelfuse, Inc.

Eaton Corporation plc (Bussmann)

Mersen S.A.

AEM Components, Inc.

Pacific Engineering Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Littelfuse released TPSMB-L automotive TVS diodes aimed at 800 V battery-management systems.

- March 2025: Littelfuse introduced the 823A Series AEC-Q200 SMD fuse rated at 1,000 V DC for battery-management and DC-DC converter circuits.

- February 2025: Eaton launched dual-trigger EV Pyro Fuses that disconnect high-voltage packs within 2 milliseconds during crash events

- January 2025: American Axle & Manufacturing agreed to acquire Dowlais Group, parent of GKN Automotive, to strengthen e-drive and driveline expertise.

Global Automotive Fuse Market Report Scope

Automotive fuses safeguard a vehicle's wiring and electrical components. Typically set at 32 volts DC, these fuses can also operate at 42 volts. Housed in one or more fuse boxes, they are usually located on one side of the engine compartment or under the dashboard near the steering wheel. These fuses protect against short circuits and overcurrents, disconnecting the circuit upon detecting potentially dangerous current levels. The study monitors the revenue generated by the global sales of automotive fuse markets.

The automotive fuse market is segmented by type (blade, glass, slow blow, high-voltage fuses, chip fuse, other types), type of vehicle (passenger cars ((traditional-ICE)), commercial vehicles ((traditional-ICE)), electric/hybrid vehicles), and geography (North America [United States and Canada], Europe [Spain, Germany, and France, rest of Europe], Asia-Pacific [China, India, Japan, rest of Asia-Pacific], Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Blade |

| Glass |

| Slow-Blow |

| High-Voltage |

| Chip |

| Other Fuse Types |

| 0 – 20 A |

| 21 – 40 A |

| 41 – 60 A |

| > 60 A |

| Passenger Cars |

| Commercial Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Plug-in Hybrid Vehicles |

| Fuel-Cell and Other New-Energy Vehicles |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Fuse Type | Blade | ||

| Glass | |||

| Slow-Blow | |||

| High-Voltage | |||

| Chip | |||

| Other Fuse Types | |||

| By Ampere Rating | 0 – 20 A | ||

| 21 – 40 A | |||

| 41 – 60 A | |||

| > 60 A | |||

| By Vehicle Type | Passenger Cars | ||

| Commercial Vehicles | |||

| Battery-Electric Vehicles | |||

| Hybrid and Plug-in Hybrid Vehicles | |||

| Fuel-Cell and Other New-Energy Vehicles | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the automotive fuse market in 2026?

The automotive fuse market size is USD 2.27 billion in 2026 and is projected to reach USD 3.19 billion by 2031.

What is the expected growth rate for automotive fuses?

The market is on track for a 7.04% CAGR during 2026-2031, fueled by vehicle electrification and higher electronic content.

Which fuse type is growing fastest?

High-voltage fuses, used in 400 V and 800 V EV battery packs, are advancing at an 8.59% CAGR.

Which region dominates demand for automotive fuses?

Asia-Pacific holds a 62.70% share in 2025 and is forecast to have the fastest regional CAGR of 9.05%.

Page last updated on: