Circuit Breaker And Fuses Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.66 Billion |

| Market Size (2031) | USD 24.23 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

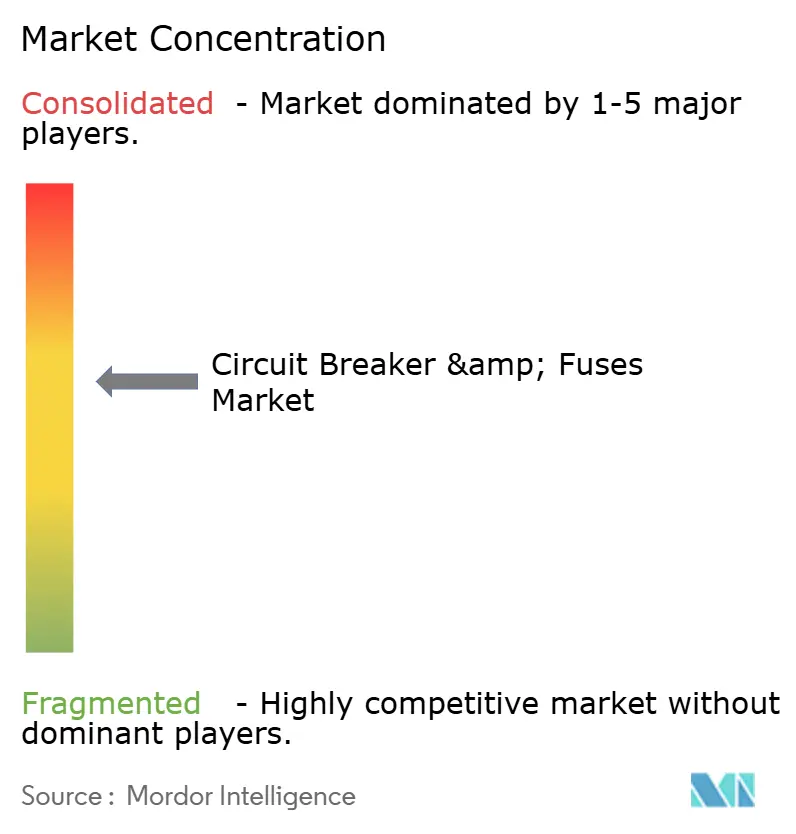

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Circuit Breaker And Fuses Market Analysis by Mordor Intelligence

The circuit breaker and fuses market size is expected to grow from USD 17.61 billion in 2025 to USD 18.66 billion in 2026 and is forecast to reach USD 24.23 billion by 2031 at 5.36% CAGR over 2026-2031. Robust electrification mandates across emerging economies, accelerating renewable-energy rollouts, and hyperscale data center expansion are converging to keep demand for reliable overcurrent and fault-interruption devices on a steady upward trajectory. Utilities continue to favor medium-voltage switchgear that harmonizes with 11 kV to 36 kV distribution networks, while data-center operators are piloting 380 V direct-current architectures that require ultra-fast hybrid breakers. At the same time, digital-twin simulations and embedded condition-monitoring sensors are shifting the competitive focus from pure hardware margins to life-cycle software services. Regional specialists in China and South Korea are widening the pricing gap by delivering vacuum interrupters 20%-30% below Western equivalents, intensifying competition in cost-sensitive tenders.

Key Report Takeaways

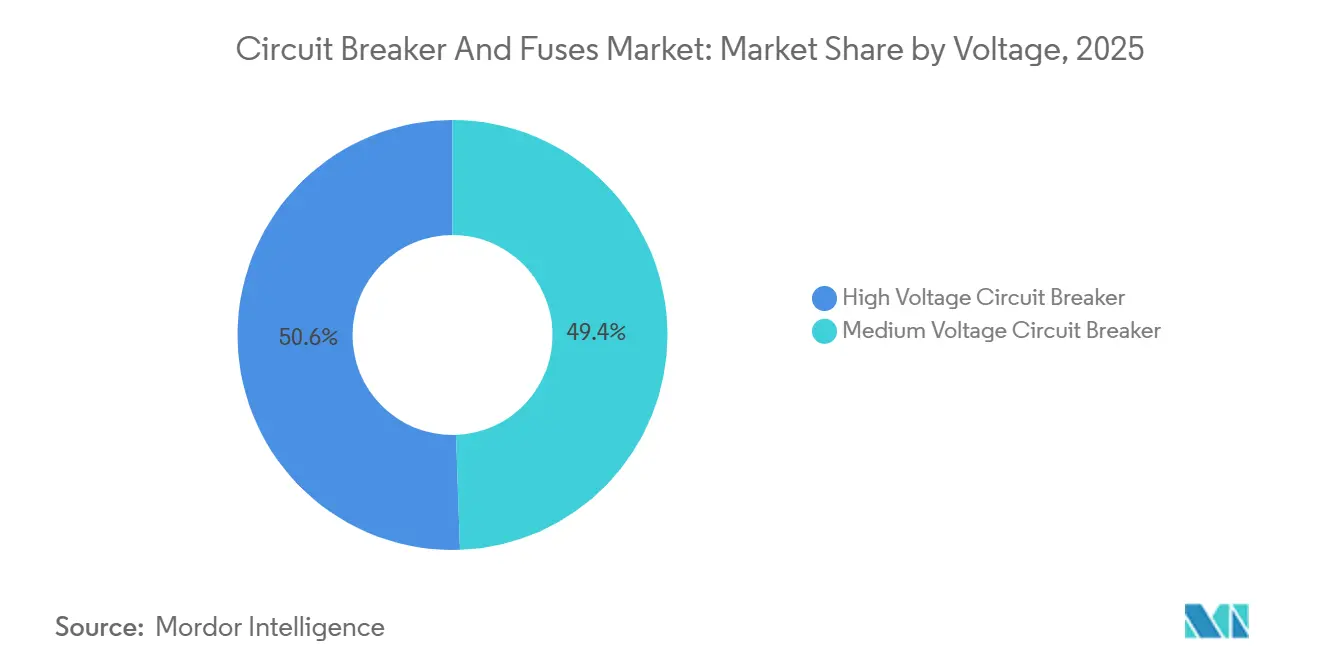

- By voltage, the medium-voltage segment accounted for a 49.44% revenue share in 2025, while high-voltage devices are expected to post a 5.77% CAGR through 2031.

- By arc-quenching media, vacuum technology captured 38.73% of the 2025 circuit breaker and fuses market share, whereas gas-SF6 breakers are forecast to expand at a 6.13% CAGR.

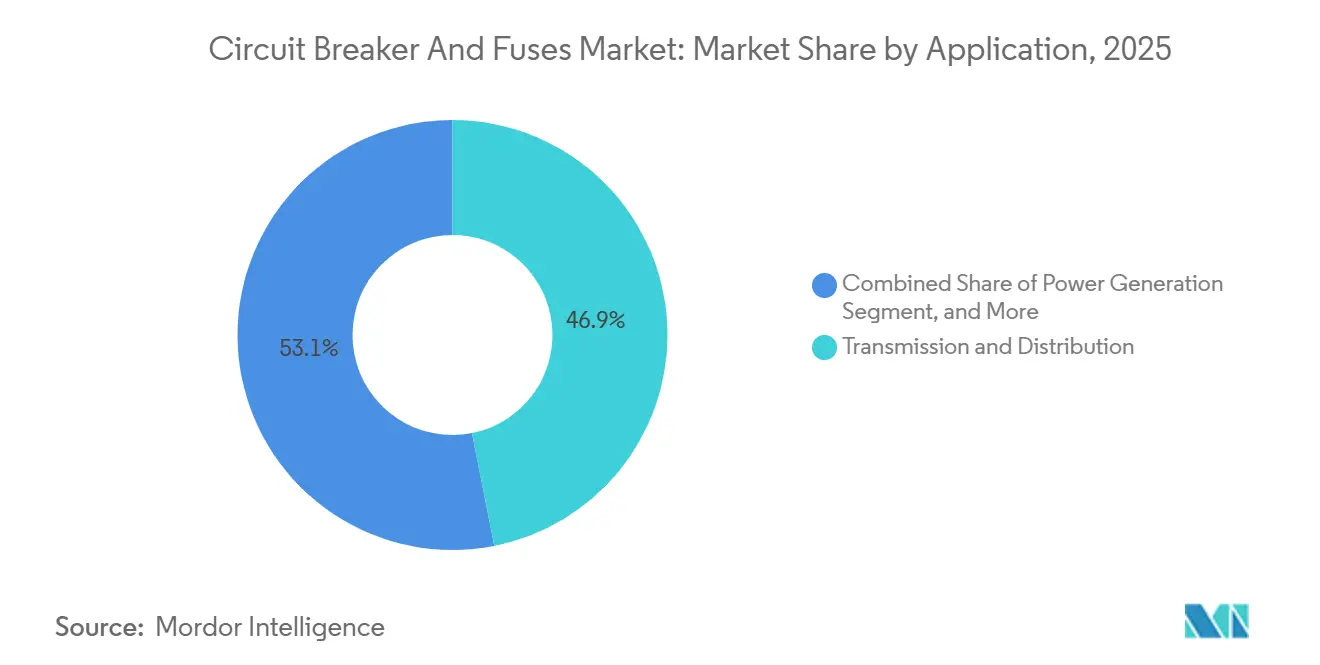

- By application, transmission and distribution dominated with 46.89% of 2025 revenues, yet power generation is projected to rise at a 6.57% CAGR.

- By installation environment, outdoor units accounted for 63.38% of sales in 2025 and are set to grow by 5.81% a year through 2031.

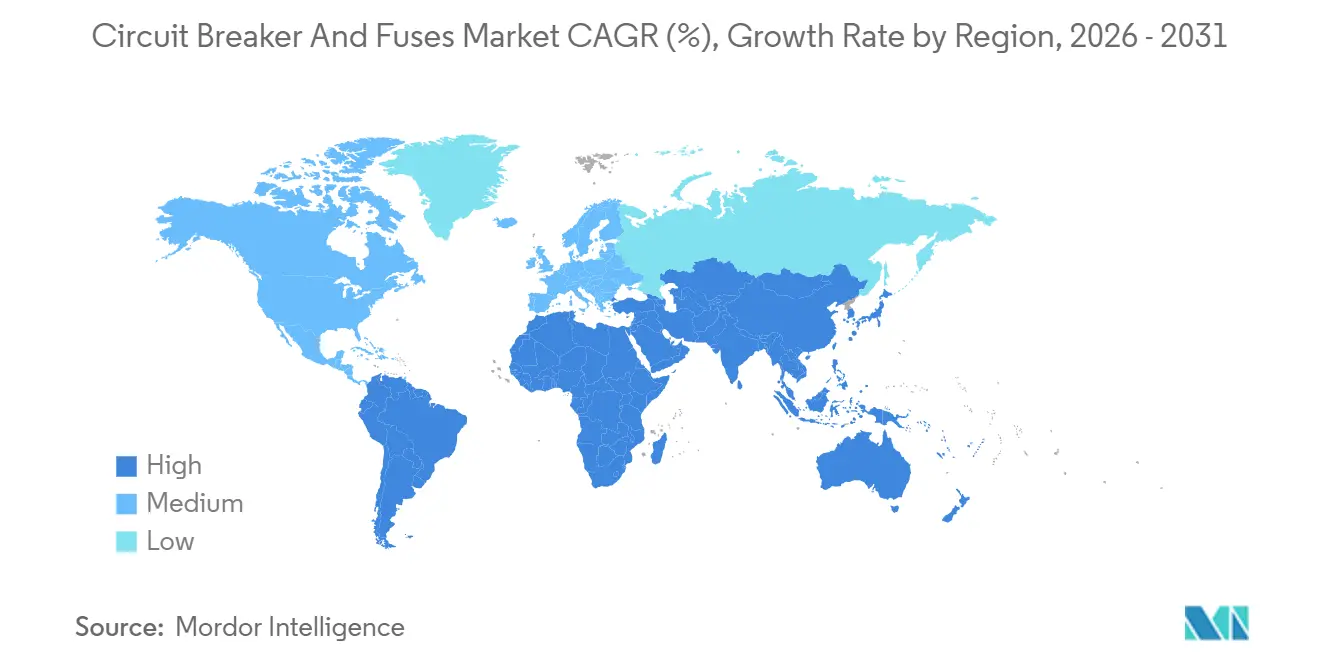

- By geography, Asia-Pacific accounted for 42.36% of global demand in 2025, while the Middle East is poised for the fastest 6.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Circuit Breaker And Fuses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Access to Electricity in Developing Countries | +1.2% | Sub-Saharan Africa, South Asia, Southeast Asia | Long term (≥ 4 years) |

| Strong Growth of Construction and Developmental Activities | +1.0% | Asia-Pacific core, Middle East, North America | Medium term (2-4 years) |

| Growing Investments in Renewable and Energy Storage | +1.3% | Global, with concentration in EU, China, US | Medium term (2-4 years) |

| Modernization of Aging Transmission and Distribution Infrastructure | +0.9% | North America, Europe, Japan | Long term (≥ 4 years) |

| Surge in Data Center Build-outs Requiring High-Speed DC Circuit Protection | +0.8% | North America, Europe, Asia-Pacific hyperscale hubs | Short term (≤ 2 years) |

| Electrification of Off-Highway Machinery Boosting Demand for High-Voltage DC Breakers | +0.5% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Access to Electricity in Developing Countries

Electrification programs in South Asia and sub-Saharan Africa are stimulating sustained demand for modular low-cost protection devices that tolerate voltage swings and high ambient temperatures. Between 2019 and 2024, 685 million people gained an electricity connection, 42% via mini-grids or solar-home systems, a shift that favors fuse-switch combinations rated below 400 A.[1]International Energy Agency, “Electricity Access Progress,” iea.org India’s Saubhagya scheme electrified 28 million households, yet technical losses above 20% in select states are prompting utilities to retrofit feeders with smart reclosers that cut truck-roll costs. Donor-funded grid extension in Nigeria and Kenya increasingly specifies IEC 62271 compliance, channeling tenders toward manufacturers with accredited test portfolios. As rural grids mature, interim devices will be replaced by higher-interrupting-capacity units, anchoring a multi-decade replacement cycle. For suppliers, bundling training and after-sales diagnostics is becoming an effective strategy to lock in annuity revenue.

Strong Growth of Construction and Developmental Activities

Asia-Pacific and Middle Eastern construction booms continue to amplify sales of breakers with arc-fault and ground-fault functions now embedded as code-mandated safeguards. China’s urbanization rate reached 66.2% in 2025, adding 12 million urban residents each year, each requiring about 1.5 kW of residential load capacity.[2]National Bureau of Statistics of China, “Urbanization Data 2025,” stats.gov.cn The resulting high-rise surge has spurred the adoption of prefabricated panels that integrate miniature breakers, residual-current devices, and surge protectors, cutting on-site labor by roughly 30%. Saudi Arabia’s USD 500 billion NEOM platform and Qatar’s Lusail district together anchor a USD 2.8 trillion regional project pipeline that increasingly specifies ring-main units for mixed-use clusters. In North America, the Infrastructure Investment and Jobs Act earmarked USD 73 billion for resilient grid links, funneling orders toward outdoor breakers certified for seismic and wildfire zones. New safety codes, notably NFPA 70E 2025, enforce arc-rated switchgear in commercial buildings, lifting average selling prices 15%-20%.

Growing Investments in Renewable and Energy Storage

Global renewable additions reached 507 GW in 2025, with solar PV representing 60% of the total, and each megawatt requiring up to 12 string-level DC breakers.[3]International Renewable Energy Agency, “Global Renewable Additions 2025,” irena.org Offshore wind developers are specifying 66 kV subsea collection systems fitted with corrosion-resistant gas-insulated switchgear to avoid costly vessel interventions. Utility-scale battery projects totaled 65 GWh of new capacity in 2025 and demand bi-directional DC breakers that interrupt 20 kA within 5 ms, an envelope only vacuum or emerging silicon-carbide modules can meet reliably. Chinese brands such as Chint and Delixi captured 38% of Asia-Pacific low-voltage sales in 2025 by co-locating breaker plants near battery factories, tightening supply chain linkages. Going forward, grid operators will procure advanced protection schemes that enable higher renewable penetration without stability trade-offs, though regulatory divergence will shape adoption velocity.

Surge in Data-Center Build-outs Requiring High-Speed DC Circuit Protection

Hyperscale facilities consumed 460 TWh in 2025, and AI workloads have quadrupled rack densities to 50 kW, making fast-clearing faults critical. Operators are piloting 380 V DC buses that remove multiple conversion stages but create continuous-current fault profiles lacking zero crossings. Hybrid mechanical-semiconductor breakers achieving sub-2 ms interruption are therefore being co-developed by suppliers and hyperscalers; Eaton’s partnership with Microsoft and ABB’s project with Google are leading examples. Early deployments show 8%-12% efficiency gains and up to 25% floor-space savings compared with traditional AC-centric designs. The short-term uplift is strongest in North America and Europe, yet Chinese cloud providers are expanding regionally as Singapore relaxes its moratorium on new sites, opening secondary demand hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Environmental and Safety Regulations Affecting SF6 Switchgear | -0.7% | European Union, California, Japan | Medium term (2-4 years) |

| Rising Investments in Smart Grid Vision | -0.3% | North America, Europe, Australia | Long term (≥ 4 years) |

| Volatility in Raw Material Prices | -0.6% | Global | Short term (≤ 2 years) |

| Increasing Preference for Solid-State Protection in EV Fast-Charging Networks | -0.4% | Europe, China, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Environmental and Safety Regulations Affecting SF6 Switchgear

The European Union’s updated F-Gas Regulation bans new SF6 installations above 24 kV in urban areas from 2026 and targets a 55% cut in emissions by 2030. California followed with a 1% leakage cap and mandatory sensor-based monitoring that adds USD 8,000-15,000 to each switchgear lineup. Utilities now face retrofit bills between EUR 500,000 and EUR 2 million per bay, stretching capital budgets already burdened by renewable connections. SF6-free alternatives, such as fluoronitrile or dry-air mixtures, require 10%-15% larger clearances, increasing enclosure size and material cost. Japan’s voluntary program aims for a 30% cut by 2030, but the lack of penalties is delaying progress. The regulatory divergence is fragmenting global supply chains and complicating inventory management for multinational suppliers.

Volatility in Raw Material Prices

Copper prices swung 20% in 2025, trading between USD 8,200 and USD 10,400 per metric ton after mine disruptions in Chile and EV-driven demand spikes. The hot-rolled steel coil price jumped from USD 720 to USD 890 per ton as India imposed export tariffs to preserve domestic supply. Aluminum faced supply constraints when Chinese smelters curtailed output, sending prices 14% above 2024 averages and forcing European fabricators to source higher-cost Middle Eastern metal. Meanwhile, China's export quotas for neodymium and dysprosium keep rare-earth prices volatile, exposing vacuum interrupter makers. Contractors operating on fixed-price multi-year transmission projects are feeling the squeeze first, with some mid-tier Indian and Brazilian suppliers reporting negative operating margins in late 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: Medium-Voltage Remains the Anchor of Utility Spending

Medium-voltage devices secured 49.44% of the circuit breaker and fuses market in 2025 and remain the backbone of utility distribution, industrial substations, and commercial campuses where 11 kV-36 kV ratings dominate. Utilities prefer vacuum interrupters that cut maintenance visits and shrink substation footprints up to 40%. Conversely, high-voltage breakers above 145 kV are projected to grow 5.77% annually as China, India, and the Middle East pursue UHVDC corridors linking distant renewable zones to load centers. Low-voltage fuses continue to dominate residential panels due to simplicity and USD 2-USD 8 unit costs, while high-voltage fuses protect instrument transformers and capacitor banks tied to new grid expansions in Southeast Asia.

Gas-SF6 units maintain dominance in ultra-high-voltage links, given dielectric strength 2.5 times that of air, though fluoronitrile blends are gaining a toehold in Europe. The segment is thus dual-tracked: utilities in mature economies are testing SF6-free gear, while price-sensitive markets still install legacy gas units. Oil breakers are slowly being phased out of new builds, except in parts of Africa, whereas molded-case models are replacing air circuit breakers with electronic trips that reduce nuisance trips by 25%.

By Arc-Quenching Media: Vacuum Leads, SF6 Grows Fastest

Vacuum technology held a 38.73% market share in the circuit breaker and fuses market in 2025, buoyed by 30,000-operation contact life and 15-year maintenance intervals that lower total ownership costs by 40% versus oil designs. State Grid China procured 1.2 million vacuum interrupters in 2025 for rural electrification, underscoring the momentum in volume. Gas-SF6 breakers, though under regulatory scrutiny, are still clocking the fastest 6.13% CAGR because alternative media have yet to match SF6 performance above 145 kV, especially in offshore wind systems that prioritize compactness.

Oil units linger primarily in legacy African and South Asian grids, where operators prioritize compatibility over environmental risk. Air breakers continue to serve low-voltage motor-control centers, but Ethernet-enabled molded cases are starting to cannibalize share by offering real-time diagnostics. Solid-state breakers, leveraging silicon-carbide MOSFETs, remain confined to mission-critical data centers and EV fast-charging hubs due to their 3-5× per-ampere price premium.

By Application: Transmission and Distribution Dominates, Power Generation Climbs

Transmission and distribution accounted for 46.89% of 2025 revenue share of the circuit breaker and fuses market, as utilities replace aging fleets and embed bidirectional protection for distributed generation. However, power-generation deployments are rising at a 6.57% CAGR on the back of gigawatt-scale solar parks in India, next-generation SMRs in the United States, and European offshore wind, where switchgear must withstand salt spray and 5 g vibration loads.

Industrial complexes are adopting predictive-maintenance-ready breakers tied to Eaton’s Power Xpert and ABB Ability, cutting unplanned downtime 10%-15%. Construction sites favor portable panels with GFCIs, a niche that rose 8% in 2025 as stricter rules took hold in the European Union and Australia. Transportation and marine electrification add incremental demand for 1,000 V DC breakers in rolling stock and hybrid propulsion systems. Consumer electronics remain a small but growing niche, with miniature thermal-magnetic units now integrated into EV charging cables and residential solar inverters.

By Installation Environment: Outdoor Equipment Retains the Majority Share

Outdoor units accounted for 63.38% of the 2025 circuit breaker and fuses market revenues and are forecast to grow 5.81% annually as utilities prioritize compact, weatherproof enclosures that reduce land take and avoid HVAC costs. Gas-insulated outdoor designs dominate harsh-climate regions, achieving 40-year lifespans with minimal service intervention. In the Middle East, aluminum housings with solar-reflective coatings are standard to survive 50 °C ambient temperatures. Indoor systems prevail in data centers and underground substations, where noise levels are kept below 65 dB, and space constraints dictate vacuum or air breakers.

Seismic qualification is now a purchase differentiator; California utilities require IEEE 693 compliance up to 1.5 g. Offshore wind brings hybrid requirements: subsea units need IP68 ingress ratings, while topside platforms demand stainless-steel enclosures that resist salt spray. Modular bay designs are being adopted for both indoor and outdoor installations, enabling incremental expansion and trimming upfront capital by 20%-30%. Arc-resistant switchgear per IEC 62271-200 Annex A, although adding USD 30,000-USD 60,000 per lineup, is increasingly mandated by insurers in North America and Europe.

Geography Analysis

Asia-Pacific wielded a 42.36% share of the circuit breaker and fuses market in 2025, powered by China’s CNY 520 billion (USD 72.8 billion) transmission investment, India’s INR 3.03 trillion (USD 37 billion) modernization outlay, and Southeast Asia’s goal of 95% electrification by 2030. Chinese manufacturers such as Chint, Delixi, and Tengen supplied 62% of domestic low-voltage demand by pricing vacuum interrupters 25%-35% below multinational offers. India’s renewable build-out surpassed 175 GW in 2025, spurring DC breaker procurement for solar parks and battery storage corridors, with Siemens India and Larsen & Toubro securing contracts totaling over USD 800 million.

The Middle East, growing at a market-leading 6.39% CAGR, benefits from Saudi Arabia’s USD 500 billion NEOM vision, the UAE’s Barakah nuclear expansion, and Qatar’s LNG terminal enlargement, all of which need explosion-proof or corrosion-resistant switchgear. Desalination complex upgrades to variable-frequency drives now specify harmonic-rated breakers, a niche expanding at 9% annually. Africa’s average electrification rate reached 57% in 2025, but sub-Saharan countries excluding South Africa stand at 48%, underscoring the need for mini-grid and hybrid solar-diesel solutions. South Africa’s Eskom awarded ZAR 12 billion (USD 650 million) in 2025 for substation retrofits requiring SF6-free gear and digital relays.

North America and Europe remain replacement-driven, though policy-driven volumes rose. The United States’ Infrastructure Act allocated USD 73 billion to resilient transmission-class breakers, many of which are arc-resistant and IoT-enabled. Germany’s Energiewende required 8,900 km of new lines by 2025, often deploying gas-insulated substations in dense areas where land costs exceed EUR 1 million (USD 1.13 million) per hectare. South America’s growth hinges on Brazil’s hydroelectric refurbishments and Argentina’s Vaca Muerta shale-gas ties, which need high-altitude breakers tested above 3,000 m.

Regulatory Landscape

Compliance is anchored around IEC and regionally adopted derivatives that govern circuit breakers and low-voltage fuse performance, testing, and safety. IEC 60269-1 (Edition 5) was published in August 2024 for low-voltage fuses, covering AC circuits up to 1,000 V and DC circuits up to 1,500 V, and IEC 60269-2 (Edition 5.2) was published in June 2024 for industrial fuses used by authorized persons, reinforcing breaking-capacity and application-specific requirements that affect PV, storage, and industrial panel designs.

For circuit breakers, the 2025 edition of EN IEC 60947-2 (published February 2025, replacing the 2016 fifth edition) introduced technical revisions that raise the bar on EMC and dielectric testing. This is pushing manufacturers toward updated qualification and documentation cycles, particularly for digitally monitored and DC-adjacent applications. In North America, UL continues to refresh safety frameworks for fuses, with ANSI/UL 248-14 (Edition 3) published in March 2026 for supplemental fuses (60 A or less), supporting continued harmonization and re-testing needs for global suppliers selling into multi-standard environments.

Value Chain Analysis

The value chain spans upstream metals and specialty materials (copper, aluminum, steel, rare-earth inputs for interrupter-related components) and a second layer of critical electronics (sensors, communication modules, digital isolators, and power-management ICs) that support intelligent trip units and condition monitoring. Manufacturing includes interrupter assembly (vacuum or gas-insulated), contact and arc-chute fabrication, molded housings, calibration, and certification testing to IEC/EN IEC/UL requirements, followed by switchgear integration for medium- and high-voltage lineups and panel/OEM integration for low-voltage applications.

Distribution moves through direct utility and EPC tendering for transmission and distribution projects, along with electrical distributors and OEM channels for building and industrial demand. Aftermarket services (spares, retrofit kits, diagnostics software) are taking a larger share of delivered value. Recent supply-chain stress has been most visible in electronics-linked inputs, with lead-time spikes for circuit protection devices and semiconductors reported into March 2026 (upper bounds around 40 weeks). Supplier price actions also feed into bill-of-materials pressure for smart breakers and connected switchgear, including TE Connectivity list-price increases implemented on January 5, 2026 (5%-12%) and Texas Instruments increases effective February 1, 2026 (15%-85% on selected digital isolators and power-management ICs). Single-node disruptions remain relevant as well, including Littelfuse declaring force majeure on July 28, 2025 after a fire at Indium Corporation’s Suzhou facility impacted supply for specific overvoltage suppressor products used in protection and interface circuits.

Competitive Landscape

The circuit breaker and fuses market is moderately concentrated: the top five players - ABB, Siemens, Schneider Electric, Eaton, and Mitsubishi Electric - commanded around 48% of global revenue in 2025. Competitive differentiation has shifted toward software-enabled maintenance, digital twin modeling, and modular platforms rather than raw interrupt ratings. ABB has deployed more than 200 SF6-free bays across European substations, integrating sensor suites that feed its Ability analytics stack. Schneider Electric’s EcoStruxure couples breaker telemetry with building-management systems, securing multi-site service contracts that lower total client energy costs 10%.

Siemens’ partnership with Microsoft on digital substations shows how cloud analytics are becoming integral to protection gear. Hitachi Energy and Google are piloting switchgear tailored for GPU and TPU clusters, highlighting the data-center pivot. Chinese challengers Chint and Delixi already hold 38% of Asia-Pacific low-voltage demand by co-locating plants near battery and solar component hubs, thinning Western margins in volume segments.

In 2025, patent activity saw a significant uptick, reflecting growing innovation in hybrid DC-breakers. Both Mitsubishi Electric and Toshiba submitted over 40 applications each to the Japan Patent Office for hybrid DC-breakers, demonstrating their commitment to advancing this technology. The ongoing standards work by IEC TC 17 on DC breakers exceeding 1,500 V is poised to spur broader adoption across industries, especially once harmonized test protocols are established. These developments are expected to play a crucial role in addressing the increasing demand for efficient and reliable DC power systems.

Circuit Breaker And Fuses Industry Leaders

ABB Ltd

Siemens AG

Schneider Electric SE

Eaton Corporation Inc

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An emerging pull is forming around high-speed DC fault protection and protection coordination in data centers, battery storage, and new DC distribution architectures, where conventional electromechanical interruption characteristics do not match continuous-current fault profiles. Siemens introduced the SENTRON 3QD2 semiconductor circuit breaker as part of a direct-current portfolio in April 2026, and Siemens and Infineon later partnered to integrate 1,200 V CoolSiC MOSFET modules into the SENTRON 3QD2 platform in June 2026. Together, these steps connect breaker roadmaps to power-semiconductor ecosystems and support productization aimed at microsecond-class interruption for AI data centers and DC grids.

A second opportunity area is software-led life-cycle services and predictive maintenance for molded case and medium-voltage fleets. This is backed by published technical validation of sensor fusion and machine-learning methods for contact and health assessment in May 2026, and by published work on intelligent breaker fault diagnosis using embedded communications and deep learning in December 2025. Separately, regulatory pressure on SF6 use, including the European Union F-Gas direction affecting new installations above 24 kV in urban areas from 2026, expands addressable demand for SF6-free alternatives and retrofit programs. This creates room for suppliers with proven vacuum, fluoronitrile, or dry-air portfolios and accredited test capabilities to win tenders that bundle equipment with commissioning, monitoring, and analytics.

Recent Industry Developments

- June 2026: Siemens and Infineon Technologies announced the integration of Infineon 1,200 V CoolSiC MOSFET power modules into the Siemens SENTRON 3QD2 semiconductor circuit breaker platform. The integration improves the performance envelope for ultrafast protection demanded by AI data centers and DC distribution, tightening the linkage between breaker platforms and power-semiconductor supply ecosystems.

- July 2025: ABB introduced a new circuit breaker positioned for higher resilience in AI data centers and advanced manufacturing environments. The product direction highlights how vendors are using faster protection, diagnostics, and system integration to defend share as rack densities and power quality requirements rise in digital infrastructure.

- April 2024: Schneider Electric unveiled the Resi9 Energy Center retrofit offering for prosumer homes. The offering reflects continued product development aimed at residential electrification and distributed-energy upgrades, where panel retrofits and protection coordination support incremental demand for low-voltage protection devices.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue earned from circuit breakers and electrical fuses used to protect electrical circuits across residential, commercial, industrial, and utility settings. The sizing reflects sales of these devices across common voltage classes and installation environments.

Scope exclusions: We exclude installation labor, testing services, and broader switchgear assemblies when they are priced and sold as complete packaged systems.

Segmentation Overview

- By Voltage

- High Voltage Circuit Breakers

- Medium Voltage Circuit Breakers

- By Arc Quenching Media Type

- Vacuum Circuit Breakers

- Oil Circuit Breakers

- Air Circuit Breakers

- Gas-SF6 Circuit Breakers

- By Application

- Transmission and Distribution

- Construction

- Industrial

- Power Generation

- Consumer Electronics

- Other Applications

- By Installation Environment

- Indoor

- Outdoor

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the demand pool for electrical protection equipment, and then checking it against supply side signals that can be verified in public records. We leaned on official and non-paywalled sources such as the International Energy Agency for grid and power trends, the World Bank for construction and industrial output indicators, UN Comtrade for trade flows of relevant electrical apparatus, and national energy regulators for transmission and distribution build-out plans.

To translate those signals into a market model, we also reviewed product standards and safety guidance from bodies such as IEC and NFPA, along with peer-reviewed papers discussing arc-quenching media trends and SF6 reduction efforts. Company annual reports, investor decks, and reputed press were used to understand portfolio mix and regional exposure, and paid subscriptions were referenced selectively for company financials, patent databases, and import-export shipment-level views to cross-check directionally. The sources mentioned above are illustrative and not exhaustive, and many other references were consulted for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating the sizing logic around voltage classes, installation environments, and application split (utilities, construction, industrial loads, and electronics-related uses). We spoke with a mix of manufacturers, distributors, EPC participants, and utility or facility stakeholders across major regions, and then used their inputs to confirm assumptions on price movement, replacement cycles, and the pace of technology shifts such as vacuum adoption and SF6-related transitions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 31% | EMEA: 34% |

| Smaller Players: 15% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

The core sizing is built using a top-down and bottom-up blend, where electricity network expansion, electrification activity, and construction-led load additions are converted into a realistic demand pool for protection devices by voltage class and end use. Results are then checked with selective bottom-up approximations, such as sampled price x unit ranges from channel conversations, supplier revenue splits from public filings, and trade flow directionality, and then totals are adjusted where the checks show clear gaps.

A few market fingerprints are used as consistent model inputs, including transmission and distribution capex direction, renewable additions and grid connection activity, data center build-outs that influence low-voltage and fast-acting protection needs, replacement and maintenance cycles in industrial facilities, and the mix shift in arc-quenching media (vacuum versus gas-SF6) that impacts average selling prices. When data points are missing for smaller countries, we fill gaps by using proxy indicators like electricity consumption growth, urban construction output, and import dependency patterns, and then confirm the reasonableness with interview feedback.

For forecasting, scenario analysis is applied around grid investment timing and industrial activity, and it is supported by trend smoothing on the historical run-rate of key inputs. The final forecast path is aligned to what experts expect for pricing progression, regulatory pressure on specific technologies, and the near-term cadence of utility tenders and project awards.

Data Validation & Update Cycle

To validate outputs, we compare the modeled totals against independent signals like trade movement, public company regional revenue direction, and project announcements tied to transmission, distribution, and large construction. Outliers are reviewed region by region, and if a variance cannot be explained through price, mix, or timing, assumptions are revisited and respondents are re-contacted to resolve the mismatch.

Before sign-off, the model goes through multiple analyst checks that look for unit consistency, year-over-year jumps, and share movements that do not match known market events. Reports are refreshed annually, and interim updates are made when material events occur, such as regulatory changes impacting SF6 usage or sharp shifts in utility spending. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Circuit Breaker and Fuses Market Sizing Compared With Other Published Estimates

Published market values for circuit breakers and fuses can look far apart, even when they are talking about the same general equipment. The differences usually come from what is counted as product revenue, the year chosen for sizing, and how prices are handled across voltage classes and regions.

The main gap comes from whether packaged switchgear line items and installation-heavy project value are included, and in Mordor Intelligence modeling, only the device-level circuit breakers and fuses are counted, with pricing tracked by voltage and arc-quenching mix rather than EPC contract totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.61 B (2025) | |

| Industry Publisher A | USD 18.43 B (2025) | The estimate appears to use a wider basket that can blend equipment value with broader project and installation context, and it does not clearly separate device-only revenue from packaged switchgear and turnkey delivery. |

| Research Outlet B | USD 17.33 B (2025) | The figure is directionally close but the longer forecast window and different growth assumptions can pull the current-year value down, especially if pricing progression and voltage mix shifts are treated more conservatively. |

Across the three figures, most of the spread is explained by scope handling and by how pricing is projected across low, medium, and high voltage applications. By keeping the market tied to device revenues and checking totals against practical demand signals, the final value stays traceable to repeatable inputs rather than bundled project numbers.

Key Questions Answered in the Report

What is the projected value of the circuit breaker and fuses market by 2031?

The market is forecast to reach USD 24.23 billion by 2031, reflecting a 5.36% CAGR over 2026-2031.

Which voltage category currently holds the largest share of demand?

Medium-voltage breakers held the largest individual revenue share at 49.44% in 2025, anchored by their ubiquity in utility distribution networks.

How are environmental rules affecting SF6-filled switchgear?

The European Union and California have imposed strict emission caps and installation bans that are accelerating the shift toward fluoronitrile and vacuum-based alternatives.

Why are hyperscale data centers adopting hybrid DC breakers?

AI-heavy workloads push rack power densities up to 50 kW, requiring sub-2 ms fault clearing that hybrid mechanical-semiconductor designs can deliver while trimming conversion losses.

Which region is expected to grow the fastest through 2031?

The Middle East is projected to register the highest CAGR at 6.39%, driven by mega-projects such as Saudi Arabia’s NEOM and the UAE’s Barakah nuclear expansion.

What competitive edge are leading vendors pursuing?

Market leaders are embedding digital-twin models and predictive analytics into breakers, shifting revenue toward life-cycle services and away from one-off hardware sales.

Page last updated on: