Electric Wiring Interconnection Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

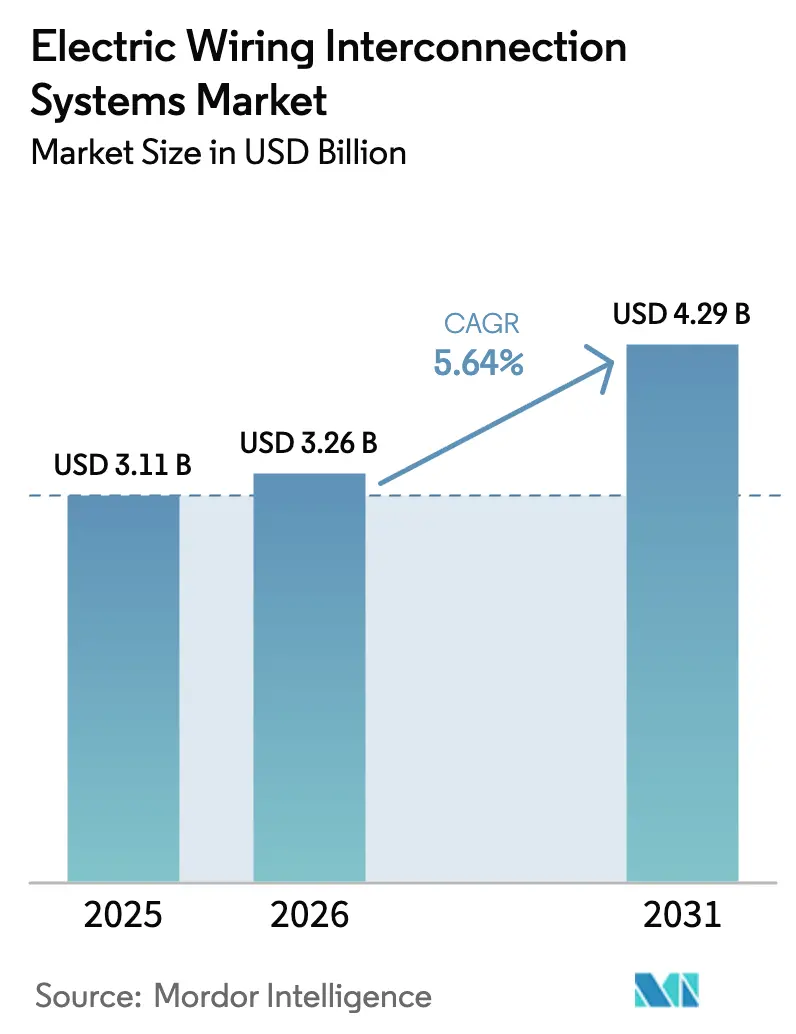

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 4.29 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

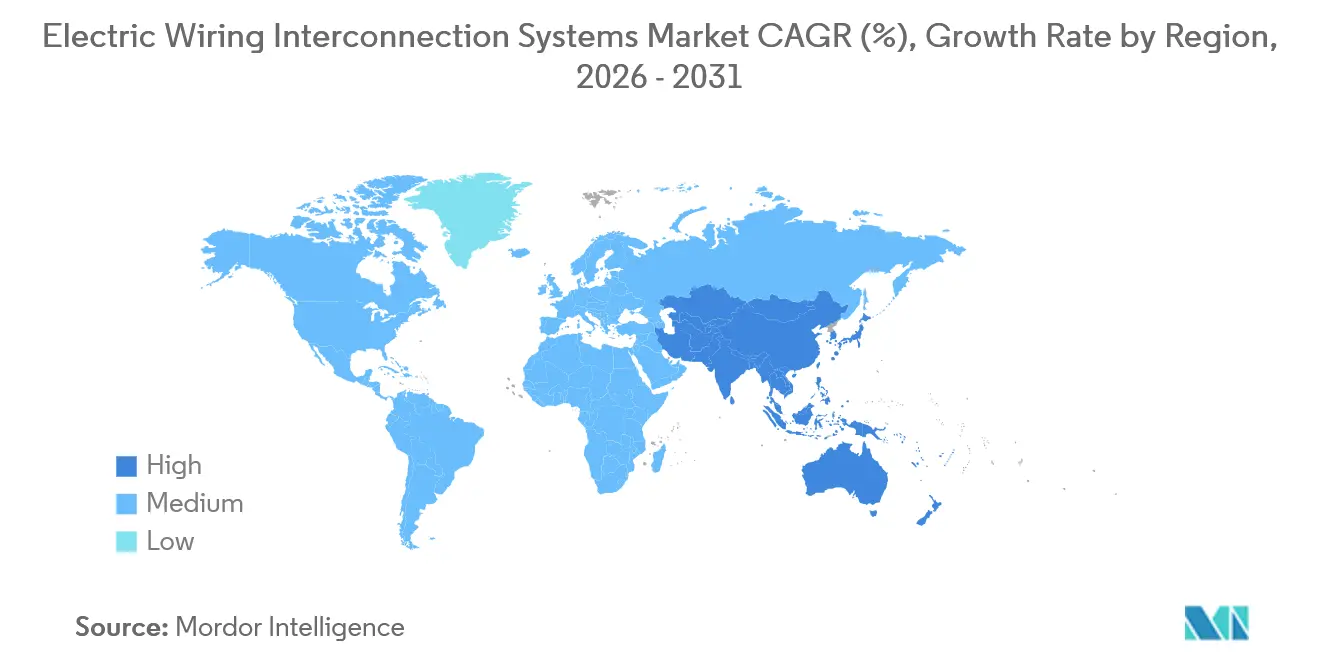

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Wiring Interconnection Systems Market Analysis by Mordor Intelligence

The Electric Wiring Interconnection Systems market is projected to expand from USD 3.11 billion in 2025 to USD 3.26 billion in 2026. Furthermore, it is forecast to reach USD 4.29 billion by 2031, with a CAGR of 5.64% over 2026-2031. Escalating aircraft electrification, stricter EWIS-specific safety rules, and record commercial backlogs keep demand resilient, even as raw-material volatility and certification bottlenecks cloud short-term visibility. Tier-1 suppliers remain shielded by long qualification cycles. Smaller specialists are winning design wins in high-temperature wire insulation, liquid-cooled cable assemblies, and additive-manufactured routing brackets that lower part counts. Momentum also comes from airlines racing to fit gigabit Wi-Fi, USB-C seat power, and Ka-band satellite terminals, each retrofit adding several kilometers of new cabling. Meanwhile, megawatt-scale propulsion projects, such as Airbus’s ZEROe, hybrid-electric regional demonstrators, and the US Air Force’s Next Generation Air Dominance fighter, are pushing voltage levels toward 1,080 VDC, opening up entirely new opportunities for fault-tolerant bus architectures. The Electric Wiring Interconnection Systems market, therefore, benefits from a rare mix of multi-decade production visibility and continuous technology refresh cycles.

Key Report Takeaways

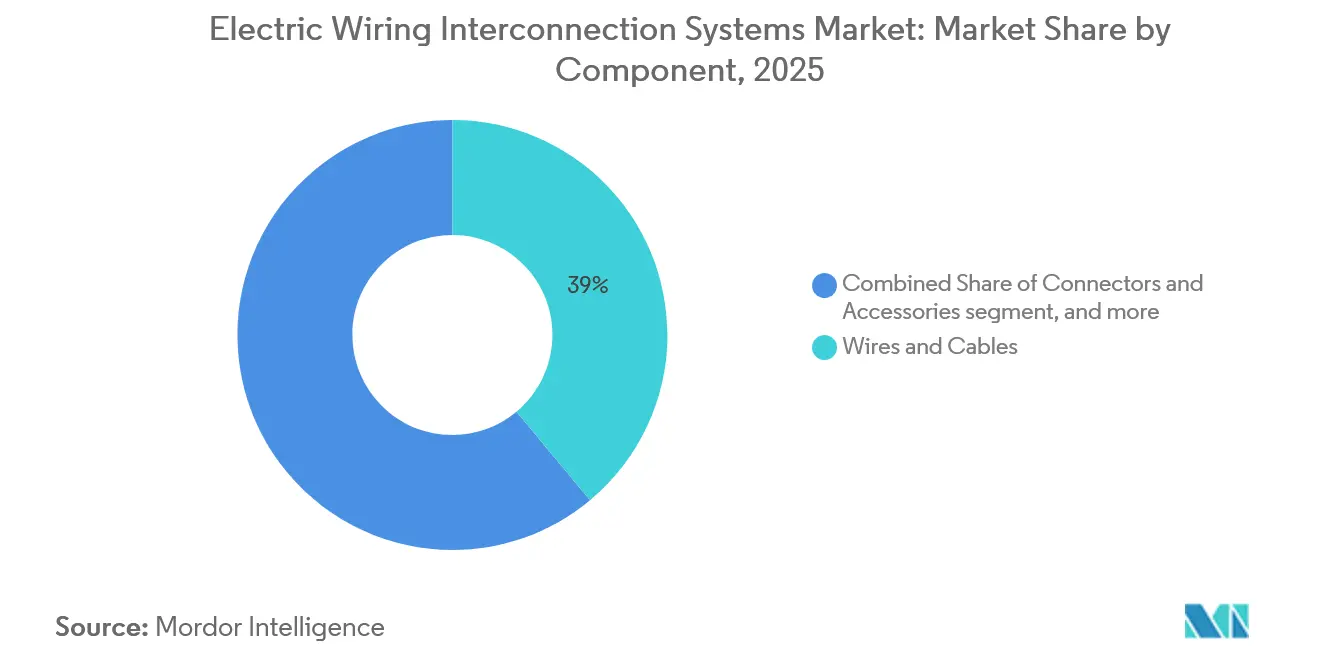

- By component, wires and cables captured 38.95% of the Electric Wiring Interconnection Systems market share in 2025, while connectors and accessories are projected to expand at a 5.87% CAGR through 2031.

- By platform, fixed-wing aircraft accounted for 63.55% of the Electric Wiring Interconnection Systems market size in 2025, whereas unmanned aerial systems are forecast to grow at an 8.50% CAGR to 2031.

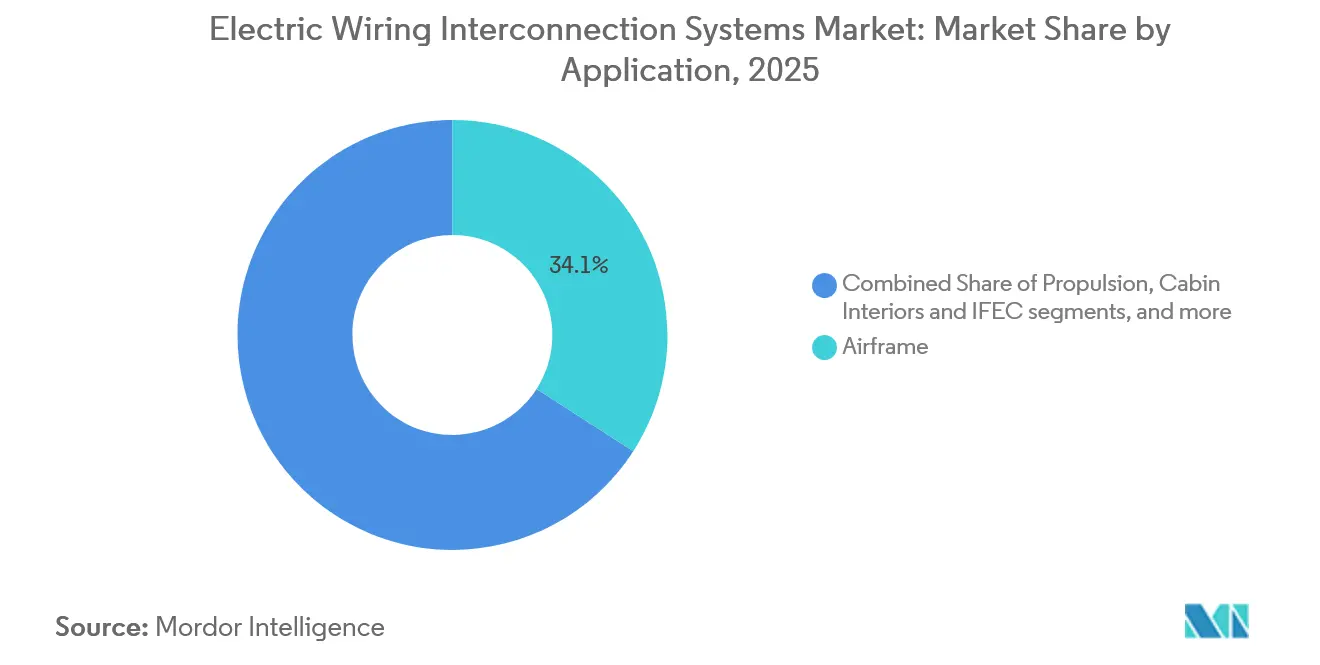

- By application, airframe circuits held a 34.10% revenue share in 2025; however, cabin interiors and IFEC harnesses are projected to advance at a 7.35% CAGR through 2031.

- By end-user, OEM deliveries secured 73.45% of 2025 revenue; however, the aftermarket is predicted to expand at a 6.44% CAGR through 2031 as operators retrofit their fleets to meet the latest EWIS directives.

- By geography, North America commanded a 39.70% share in 2025; the Asia-Pacific region posted the fastest growth rate of 6.46% through 2031, as COMAC and HAL expanded their local supply chains.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Wiring Interconnection Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global aircraft production backlog | +1.2% | North America and Europe dominate, global spill-over | Medium term (2–4 years) |

| Transition to more-electric and hybrid aircraft | +1.5% | Early adoption in Europe and North America, global later | Long term (≥4 years) |

| Tightening EWIS safety mandates | +0.9% | FAA and EASA jurisdictions lead, global adoption | Short term (≤2 years) |

| High-speed IFEC data networks | +0.7% | Premium retrofits in North America and Middle East | Medium term (2–4 years) |

| Modular plug-and-play harness architectures | +0.6% | OEM-driven in North America and Asia-Pacific | Medium term (2–4 years) |

| Additive-manufactured wire-routing brackets | +0.3% | North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surging Global Aircraft Production Backlog

Boeing and Airbus had more than 14,200 firm orders by mid-2025, providing the Electric Wiring Interconnection Systems (EWIS) market with roughly seven years of locked-in demand. Each 737 MAX, A320neo, 787, or A350 requires 40-60 km of wiring, ensuring high baseline volume for harness vendors. Semiconductor and engine shortages have stretched delivery schedules, allowing suppliers to negotiate multi-year price agreements that smooth out revenue fluctuations. Regional programs such as Embraer’s E2-series and COMAC’s C919 add geographic diversity and reduce overreliance on two Western primes. With most backlogs concentrated in North America and Europe, certified Tier-1 vendors retain a clear cost-of-qualification advantage, while newcomers in the Asia-Pacific region face longer approval cycles.

Transition to More-electric and Hybrid-electric Aircraft

Airbus’s ZEROe hydrogen demonstrator, the EU-funded HECATE test beds, and US military megawatt projects raise baseline voltage toward 1,080 VDC, demanding liquid-cooled cables and aluminum conductors with composite overwraps. [1]Source: Airbus, “ZEROe Program Overview,” airbus.com IHI’s 2025 study cited continuous 1 MW operation needing dielectric fluids rated to 200 °C. [2]Source: IHI Corporation, “Aircraft Electrification Technology Paper,” ihi.co.jp Higher voltage slashes conductor cross-section and saves weight, yet creates arc-fault hazards that require solid-state breakers and zonal segregation. Harness designers are responding with aluminum alloys that reduce weight by 30% compared to copper, and with embedded fiber sensors that report temperature in real-time. Military platforms seeking directed-energy weapons further amplify the technical stakes and reward niche expertise in high-voltage technology.

Tightening EWIS-Specific Aviation Safety Mandates

FAA 14 CFR Part 25 Subpart H, finalized in 2024, now obliges arc-fault circuit breakers, wire separation, and new flammability thresholds. EASA’s CS-25 amendment mirrors those rules and adds smoke-density limits under ASTM E662. Carriers operating aging narrowbodies must retrofit or reroute harnesses before 2027, creating a spike in aftermarket inspection kits. Advisory Circular AC 25.1701-1 forces rerouting of critical circuits through fire-resistant conduits, driving demand for specialized sleeves and clamps. Rotary-wing and eVTOL special conditions now extend similar redundancy rules to helicopters, broadening the scope of compliance.

High-Speed IFEC Data Networks Demanding New Cabling

Passenger demand for gigabit Wi-Fi drives airlines to install Ku- and Ka-band satellite terminals, which require Category 6A Ethernet cables and fiber backbones. ARINC 791/792 revisions specify an insertion loss of less than 0.5 dB at 500 MHz and require a 100-watt USB-C power supply to be located under the seat. Widebody retrofits add 2–3 km of new wiring per aircraft during heavy checks. Emirates and Qatar Airways have led adoption, moving to fiber in trunks and hybrid connectors at seat tracks. The switch creates space for suppliers offering hybrid optical-copper interfaces and hermetically sealed terminals that resist cabin-pressure cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and specialty alloy price volatility | -0.8% | Asia-Pacific and South America most exposed | Short term (≤2 years) |

| Move toward wireless avionics networks | -0.4% | Early trials in North America and Europe | Long term (≥4 years) |

| Certification delays for composite conductors | -0.5% | FAA and EASA bottlenecks delay global roll-out | Medium term (2–4 years) |

| Re-use of legacy harnesses in retrofits | -0.6% | Mature fleets in North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Copper and Specialty Alloy Price Volatility

LME copper exceeded USD 10,000 per metric ton in 2024, adding 25–30% premiums to aerospace-grade C11000 and C10100 billets. Harness firms hedge with six-month forwards; engine or avionics delays expose them to spot spikes that shave 3-5 points off margins. [3]Source: London Metal Exchange, “Copper Price Dashboard,” lme.com Nickel and silver for connector platings have followed a similar rollercoaster, with nickel jumping 40% in early 2025 due to Indonesian export caps. Substituting aluminum lowers costs by 50% but requires 60% thicker cross-sections and new flammability tests, which slows approvals and limits the substitution window.

Move Toward Wireless Avionics Networks

The ITU cleared 4.2-4.4 GHz for Wireless Avionics Intra-Communications in 2024, and Airbus and Boeing flight-tested 100 Mbps links for non-critical sensors. While WAIC could reduce point-to-point wiring by 5-10% by 2035, the FAA and EASA have not finalized certification pathways. Concerns persist over electromagnetic interference with navigation and the absence of deterministic fail-safe protocols. The near-term impact is therefore muted, but suppliers closely monitor the space to avoid stranded copper assets. Early deployments will initially appear in the cabin and cargo bays, rather than in the flight-control circuits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Connectors Advance Modular Upgrades, While Wires and Cables Dominate Volume

Connectors, accessories, terminals, and protection materials now define the fastest-growing pillar of the Electric Wiring Interconnection Systems market. Wires and cables commanded the largest 38.95% share of the Electric Wiring Interconnection Systems market in 2025, underscoring their ubiquity across flight-control, propulsion, and cabin subsystems. Commodity pricing pressure looms for low-power runs, yet high-temperature zones above 200 °C still justify 40–50% premiums for nickel-plated copper or silver-plated aluminum conductors. Terminals and splices, which capture 12–15% of component value, are benefiting from FAA AC 43.13-1B crimp-quality mandates that push automated presses to hold contact resistance below 5 milliohms (mΩ). Protective materials such as heat-shrink tubing, EMI braids, and P-clamps are shifting to flame-retardant polymers that meet ASTM E662 smoke limits without halogen additives, aligning with EU chemical rules. Other niche items, including pressure seals and bonding straps, serve engine nacelles and fuel-tank zones where MIL-STD-810 explosion-proof ratings apply.

Connectors and accessories represent the fastest-growing slice, projected to expand at a 5.87% CAGR to 2031 as modular architectures demand higher pin counts, hermetic sealing, and liquid-cooled interfaces for 1,000 VDC megawatt buses. MIL-DTL-38999 circular connectors rated to 500 A are migrating from fighters to commercial UAS, where rapid payload swaps outweigh their 20% cost premium. TE Connectivity’s 1,000-amp model, launched in 2025, embeds temperature sensors and arc-fault detection to protect hybrid-electric regional aircraft powertrains. Terminals and splices now include real-time force monitoring, reducing defect rates from 2% to below 0.5% and enabling lifetime warranties for high-cycle applications. Protective sleeves increasingly use graphene-doped polymers that boost abrasion resistance while trimming weight by 10%, although certification costs confine uptake to premium platforms. Together, these shifts underscore a component mix tilted toward higher-value, high-function parts even as baseline wire volumes remain dominant.

By Platform: UAS Lead Growth While Fixed-Wing Dominates Volume

Fixed-wing programs delivered 63.55% of 2025 revenue, anchored by narrowbody lines producing 1,200 aircraft and widebodies adding another 300 units. Each A320neo or 737 MAX embeds 40 km of cable, and every 787 or A350 carries closer to 60 km, guaranteeing baseline volume. Regional jets and turboprops fill slot-constrained routes, using retrofit harness kits that integrate synthetic vision and ADS-B. Military transport and fighter production, including 150 F-35s annually, provides a steady stream of stealth-coated harness packages and electromagnetic launch circuitry.

Unmanned aerial systems are the fastest-growing sub-platform at an 8.50% CAGR through 2031. Military ISR drones, agricultural survey craft, and last-mile delivery networks favor plug-and-play payload bays, elevating connector density and EMI shielding needs. Weight matters more than ever, with design targets below 10 W per gram prompting the use of composite-overwrap cables and aluminum conductors. Commercial quadcopters utilize automotive-grade connectors to keep the total harness cost under USD 500, but military variants adhere to hermetically sealed interfaces for use in contested environments. The twin-track platform dynamic preserves volume dominance for fixed-wing jets while shifting marginal growth and technology experimentation to unmanned systems.

By Application: Cabin Connectivity Outpaces Structural Wiring

Airframe wiring, which encompasses flight controls, landing gear, and environmental control systems, accounted for 34.10% of the revenue in 2025. These circuits prioritize reliability, utilizing polyimide insulation rated to 260 °C and featuring quadruple redundancy. Avionics systems contribute up to 28% of application revenue, migrating from ARINC 429 buses to Ethernet-based AFDX for higher throughput. Propulsion harnesses operate in vibration zones, requiring stainless-steel conduits and flame-resistant sleeving.

Cabin interiors and IFEC harnesses are the fastest-growing application cluster, expanding at a 7.35% CAGR as passengers demand 4K streaming and 100-watt seat power. Each widebody retrofit adds 2-3 km of Category 6A cable plus fiber trunks. Power-distribution harnesses are modernizing from 115 VAC 400 Hz to ±270 V DC buses, introducing arc-fault breakers and solid-state controllers that isolate faults within 10 ms. Battery-management harnesses for lithium-ion packs debut on APU-less taxi systems, layering cell-level temperature and voltage telemetry into the wiring plan. Overall, connectivity-driven retrofits are increasing demand for high-bandwidth, high-power lines, which benefits suppliers of shielded coaxial and fiber assemblies.

By End-User: Retrofit Momentum Narrows the Gap with OEM Supply

OEM delivery channels still dominate, with 73.45% of 2025 revenue locked into supplier lists that last the entire program life. Design reviews establish part numbers years before first flight, erecting high switching costs that exceed USD 5 million per airframe. Long-term agreements provide price stability, yet they require suppliers to absorb USD 2-10 million of non-recurring engineering costs per platform. Production has plateaued at around 1,500 narrowbodies and 300 widebodies per year due to engine and avionics bottlenecks, limiting pure OEM expansion.

The aftermarket, however, is expected to grow at a 6.44% CAGR through 2031, driven by mandatory EWIS inspections, arc-fault upgrades, and high-speed connectivity retrofits. MRO shops invest in automated reflectometry rigs that reduce inspection time from 80 to 20 hours, supporting narrow-body fleets that average 18 years of service. Distributors like Arrow and Heilind aggregate thousands of part numbers, leveraging their scale to secure volume discounts and mitigate raw material volatility. Operators often favor partial refurbishment over full-harness swaps, a drag on revenue per aircraft; yet, the sheer size of the aging fleet tips the balance toward steady aftermarket expansion.

Geography Analysis

North America led the Electric Wiring Interconnection Systems market with a 39.70% slice in 2025, anchored by Boeing’s narrowbody and widebody production in Washington and by defense lines in Texas and California. The United States contributes 85% of regional turnover and benefits from a deep supplier base that spans wire extrusion, connector machining, and final assembly. Canadian volume flows from Bombardier’s Global 7500 and Pratt & Whitney Canada turboprops, both of which require extreme-temperature harnesses for Arctic operations. Mexico’s clusters in Querétaro and Sonora specialize in labor-intensive wire processing, shipping 70% of output northward. FAA Subpart H compliance has prompted US operators to invest USD 150,000-300,000 per narrowbody in harness upgrades, thereby amplifying aftermarket revenues.

The Asia-Pacific is the fastest-growing geography, advancing at a 6.46% CAGR through 2031, driven by COMAC’s C919 ramp-up and India’s Regional Connectivity Scheme. China aims for 150 annual C919 deliveries by 2028, each embedding wiring sourced 60–70% from North America or Europe due to certification gaps. India’s civil fleet grows by 8% annually, spurring the retrofit of avionics packages that add 50–100 kg of new wiring per aircraft. Japan and South Korea contribute 15–18% of regional turnover, tied to the SpaceJet and KF-21 programs, which utilize fiber-optic data buses. Fragmented local suppliers often lack FAA approvals, but joint ventures with Western Tier-1 Suppliers are narrowing the gap.

Europe, South America, and the Middle East and Africa combine for roughly one-third of global revenue. Airbus' final assembly lines in Toulouse, Hamburg, and Seville keep Europe at the forefront. South America relies heavily on Embraer’s E2 aircraft, though macro volatility constrains broader growth. Middle Eastern carriers are driving premium cabin retrofits that require fiber and high-power seat tracks. Africa remains the smallest market, with 90% of demand concentrated in South Africa and Kenya, where MRO infrastructure is limited. Across all sub-regions, rising EWIS compliance costs and connectivity upgrades ensure that the Electric Wiring Interconnection Systems market continues to expand, even as newly built delivery rates remain flat.

Competitive Landscape

The Electric Wiring Interconnection Systems market exhibits moderate concentration, with key players including TE Connectivity, Safran, Amphenol, RTX (Collins Aerospace), and GKN Aerospace. These companies maintain their market position through long-term contracts with major players, including Boeing, Airbus, and defense primes. Vertical integration enables these vendors to manage wire extrusion, connector machining, and final harness assembly within a single operation, reducing coordination complexities for OEMs. Additionally, certification cycles, which typically span 18-36 months and require USD 2-10 million in non-recurring engineering costs, create significant barriers to entry for new competitors.

Smaller specialists, including Ducommun, Latecoere, and Radiall, focus on niche areas such as composite-overwrap harnesses, additive-manufactured brackets, and high-frequency IFEC connectors. For instance, GE Aerospace’s titanium brackets for the GE9X engine demonstrated that additive manufacturing can reduce lead times from 12 weeks to 3 days while eliminating 35 fasteners. Similarly, L3Harris offers plug-and-play mission pods that utilize standardized wiring, creating opportunities for expertise in quick-change connectors. Strategic initiatives in the market often involve mergers and acquisitions for geographic expansion, as well as investments in automated testing to reduce warranty costs and improve operational efficiency.

Despite ongoing innovation, the market remains conservative due to the safety-critical nature of certification processes, which discourages radical changes in system architecture. Consequently, advancements tend to be incremental, focusing on areas such as higher temperature insulation, liquid-cooled connectors, embedded sensors, and enhanced installation tooling. The Electric Wiring Interconnection Systems market rewards both scale and specialization, with established players protecting high-volume programs and emerging disruptors targeting opportunities where electrification or autonomy necessitate new solutions.

Electric Wiring Interconnection Systems Industry Leaders

TE Connectivity Corporation

GKN plc

RTX Corporation

Amphenol Corporation

LATECOERE S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: GKN Aerospace and Anduril Industries UK have signed an agreement to collaborate on next-generation uncrewed aerial vehicle (UAV) solutions for UK defense programs, strengthening the country’s sovereign capability. GKN Aerospace announced a strategic teaming agreement with Anduril Industries UK, a leading autonomous platform provider, to accelerate the development of advanced UAV and rotorcraft technologies for UK defense programs. The partnership will target key UK contracts expected in early 2026, delivering modern capabilities while reinforcing the UK’s sovereign industrial base. The industrial partnership is initially targeting the UK Government’s upcoming Land Autonomous Collaborative Platform (ACP) contract and the British Army’s Project NYX, focused on a next-generation uncrewed rotorcraft for the UK. Alongside GKN Aerospace and Anduril Industries UK, Archer is expected to contribute its eVTOL expertise to Project NYX. Under the collaboration, GKN Aerospace will lead structural design and integration work, leveraging its expertise in aerostructures, electrical wiring interconnection systems (EWIS), and aerospace engineering. A significant portion of the work is expected from GKN Aerospace’s Cowes facility, supported by its recent GBP 10 million investment in the site, including the latest cleanrooms, processing equipment, and training facilities to support growth in advanced new platforms.

- June 2025: GKN Aerospace and Archer announced an expanded collaboration to manufacture key airframe components for Archer’s Midnight eVTOL aircraft in the UK. This development signifies a strategic step in scaling production capabilities for sustainable aviation technologies. By leveraging GKN Aerospace’s expertise in lightweight aerostructures and electrical systems, the partnership aims to meet stringent performance and certification standards, reinforcing Archer’s commercial readiness. The collaboration also highlights the growing role of advanced manufacturing in the electric air mobility market, aligning with industry trends toward sustainability and innovation while strengthening the UK’s position as a hub for advanced aerospace manufacturing.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Electric Wiring Interconnection Systems (EWIS) market as revenue generated by certified wires, cables, clamps, splices, connectors, and protective materials that route power or data inside fixed-wing, rotary-wing, and unmanned aircraft across civil and defense fleets. According to Mordor Intelligence analysts, only factory-installed kits and regulator-approved retrofit packs supplied to aircraft OEMs or licensed MROs are counted.

Scope Exclusion: Automotive, rail, marine, and industrial harnesses are outside this assessment.

Segmentation Overview

- By Component

- Wires and Cables

- Connectors and Accessories

- Terminals and Splices

- Protective Materials and Clamps

- Others(Pressure Seals, Electrical bonding Devices tec.)

- By Platform

- Fixed-Wing

- Commercial Aviation

- Narrow-body Aircraft

- Wide-Body Aircraft

- Regional Transport Aircraft

- Bussiness and General Avaition

- Bussiness Jets

- Light Aircraft

- Military Avaition

- Fighter Aircraft

- Transport Aircraft

- Special Mission Aircraft

- Commercial Aviation

- Rotary Wing

- Commercial Helicopters

- Military Helicopters

- Unmmaned Aerial Systems (UAS)

- Fixed-Wing

- By Application

- Airframe

- Avionics and Mission Systems

- Propulsion

- Cabin Interiors and IFEC

- Power Distribution

- By End-User

- OEM

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team held structured interviews with harness engineers, tier-one integrators, avionics inspectors, and procurement heads across North America, Europe, and Asia-Pacific. These discussions refined installed-meter estimates, aftermarket replacement timing, and regional pricing before we locked assumptions.

Desk Research

We opened with data sets from IATA, FAA, EASA, EUROCAE, UN Comtrade code 8807, and yearly delivery tables issued by Airbus and Boeing, then overlaid insights from corporate 10-Ks, aerospace trade journals, Dow Jones Factiva news flow, and D&B Hoovers supplier filings. These sources anchored baseline volumes and transaction values; many additional public records supported finer checks.

Market-Sizing & Forecasting

We applied a top-down build that multiplies annual aircraft deliveries, in-service fleet counts, and average EWIS value per platform, then cross-checked it with sample bill-of-material roll-ups and channel price probes. Key variables like narrow-body backlog, flight-hour utilization, meter-per-airframe benchmarks, copper price curves, and mandated inspection intervals feed a multivariate regression projecting demand through 2030. Bottom-up gaps are bridged by proportional allocation based on historical replacement ratios.

Data Validation & Update Cycle

Outputs pass variance scans versus trade statistics and supplier disclosures, followed by peer review. We refresh the model each year and re-run it when order-book shocks or regulatory shifts occur, so clients receive the latest vetted view.

Why Mordor's Electric Wiring Interconnection Systems Baseline Earns Trust

Published estimates often diverge because firms stretch scope, mix list and net prices, or freeze currency early.

By anchoring figures to certified aviation installs and updating once order books move, Mordor delivers a steady, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.10 B (2025) | Mordor Intelligence | - |

| USD 7.20 B (2024) | Global Consultancy A | Adds marine and ground-vehicle wiring, blends OEM plus aftermarket at catalog prices |

| USD 9.40 B (2024) | Industry Association B | Bundles automotive looms and assumes uniform 4 percent annual price uplift |

| USD 6.60 B (2022) | Trade Journal C | Older base year, lumps connectors and terminal hardware with EWIS |

These contrasts show that when scope and price filters drift, totals swing widely; Mordor's disciplined definition, live refresh cadence, and dual-track validation make its numbers the dependable starting point for planners.

Key Questions Answered in the Report

What is the current size and growth outlook for the Electric Wiring Interconnection Systems market?

The market is valued at USD 3.26 billion in 2026 and is set to reach USD 4.29 billion by 2031, posting a 5.64% CAGR.

Which component segment is expanding the fastest?

Connectors and accessories segment is expected to grow at a 5.87% CAGR through 2031 as modular architecture adoption accelerates.

How will unmanned aerial systems influence future EWIS demand?

UAS platforms are forecast to expand at an 8.50% CAGR through 2031, creating demand for lightweight, EMI-hardened harnesses.

Why are aftermarket sales becoming more important?

FAA and EASA mandates require older fleets to retrofit harnesses, pushing the aftermarket to a 6.44% CAGR through 2031.

What technology trends will reshape EWIS designs?

High-voltage liquid-cooled cables, additive-manufactured brackets, and hybrid fiber-optic connectors are leading innovations.

Page last updated on: