Atomic Clock Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

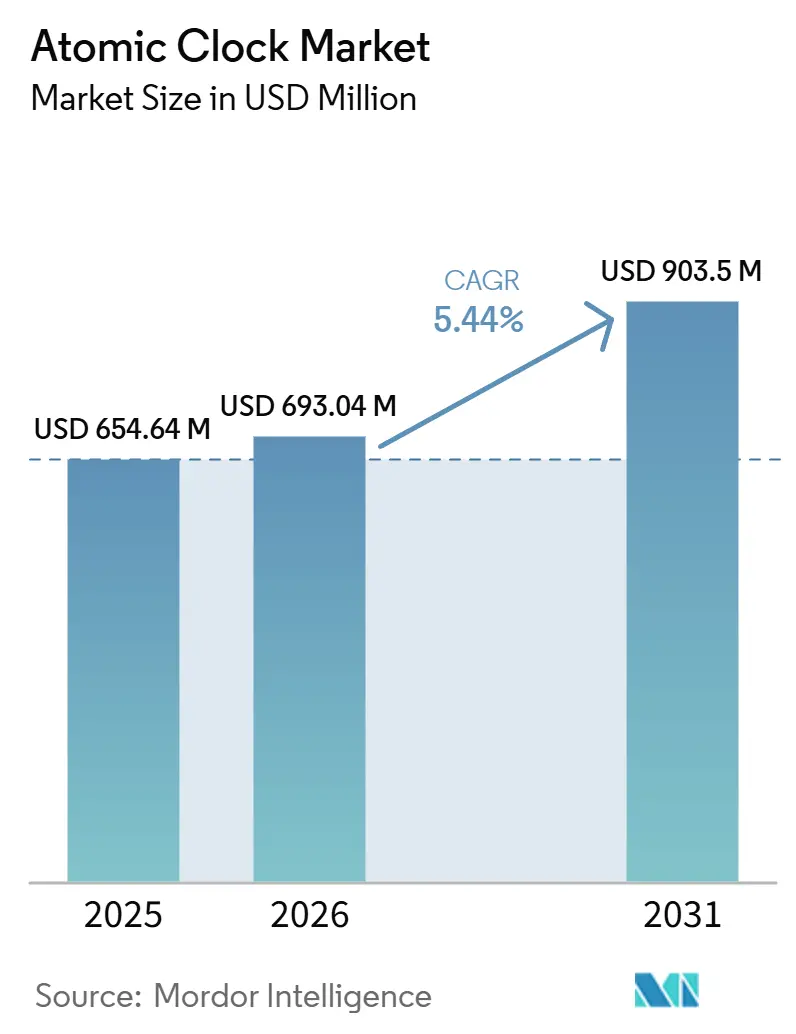

| Market Size (2026) | USD 693.04 Million |

| Market Size (2031) | USD 903.5 Million |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Atomic Clock Market Analysis by Mordor Intelligence

The atomic clock market size is expected to grow from USD 654.64 million in 2025 to USD 693.04 million in 2026 and is forecasted to reach USD 903.50 million by 2031 at a 5.44% CAGR over 2026-2031. Civil and commercial deployments gain momentum as telecom, financial services, and critical infrastructure operators embed precision timing deeper into their networks. Cesium-based frequency standards retain leadership in primary reference roles while rubidium and chip-scale platforms expand in space and defense programs where size, weight, and power priorities dominate. Navigation remains the most dynamic application, as multi-constellation receiver designs reshape specifications for holdover and interference resilience. Regional dynamics favor Asia-Pacific in growth as sovereign GNSS roadmaps scale and space programs accelerate the development of new payloads. Competition stays active with focused product launches in chip-scale, miniature rubidium, and early optical-clock offerings, alongside selective collaborations that combine hardware, time-transfer, and integration services.

Key Report Takeaways

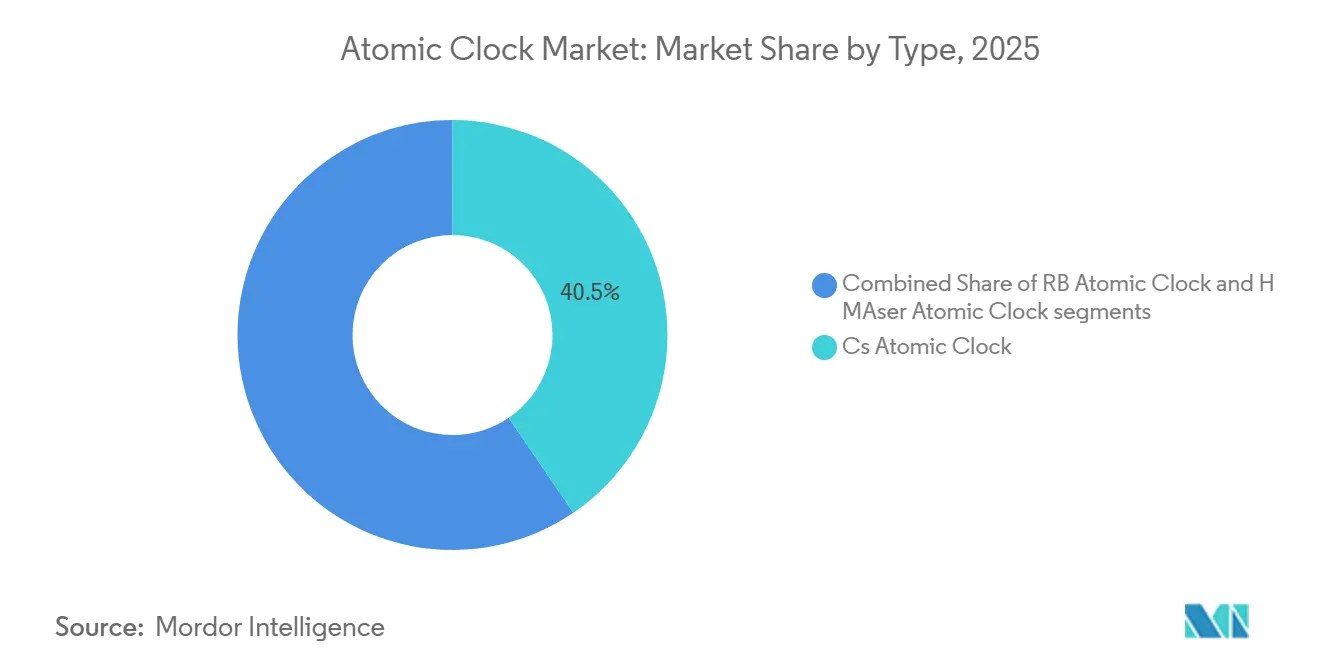

- By type, cesium-based frequency standards led the atomic clock market with 40.50% market share in 2025; cesium is projected to expand at a 5.90% CAGR through 2031.

- By end user, civil and commercial applications accounted for 45.63% in 2025; space is forecasted to expand at a 6.13% CAGR through 2031.

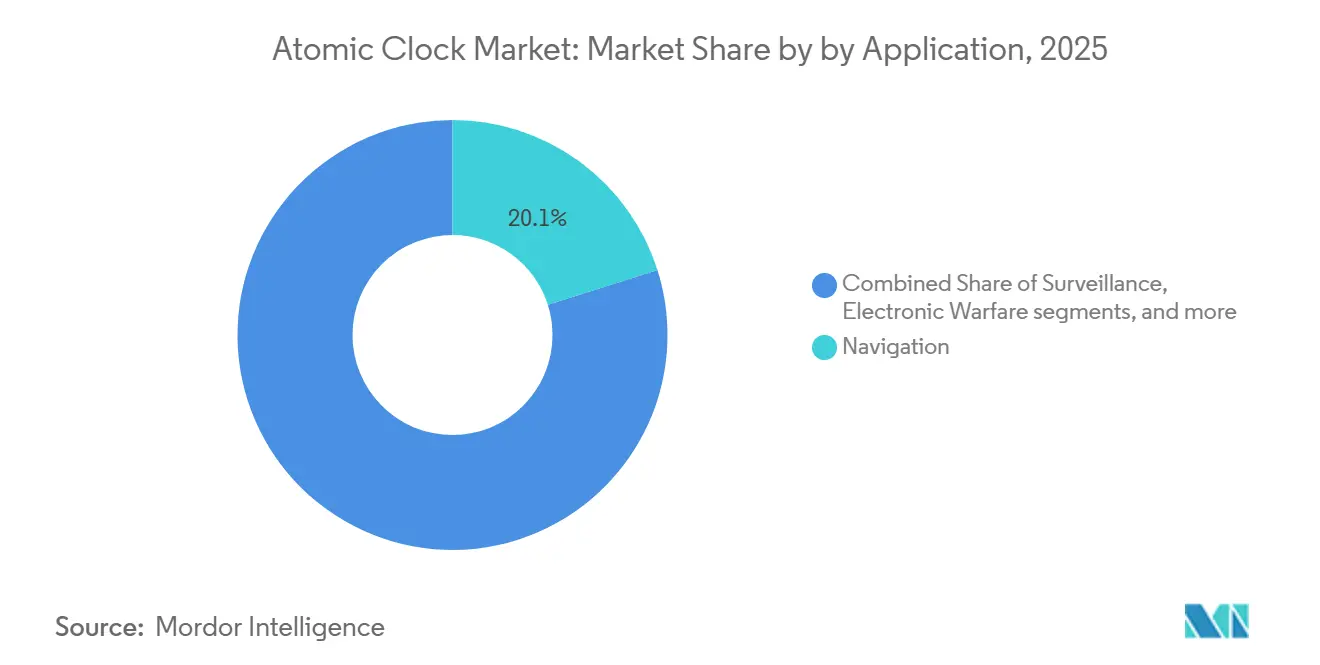

- By application, navigation accounted for 20.12% of the atomic clock market in 2025 and is expected to grow at a 6.11% CAGR through 2031.

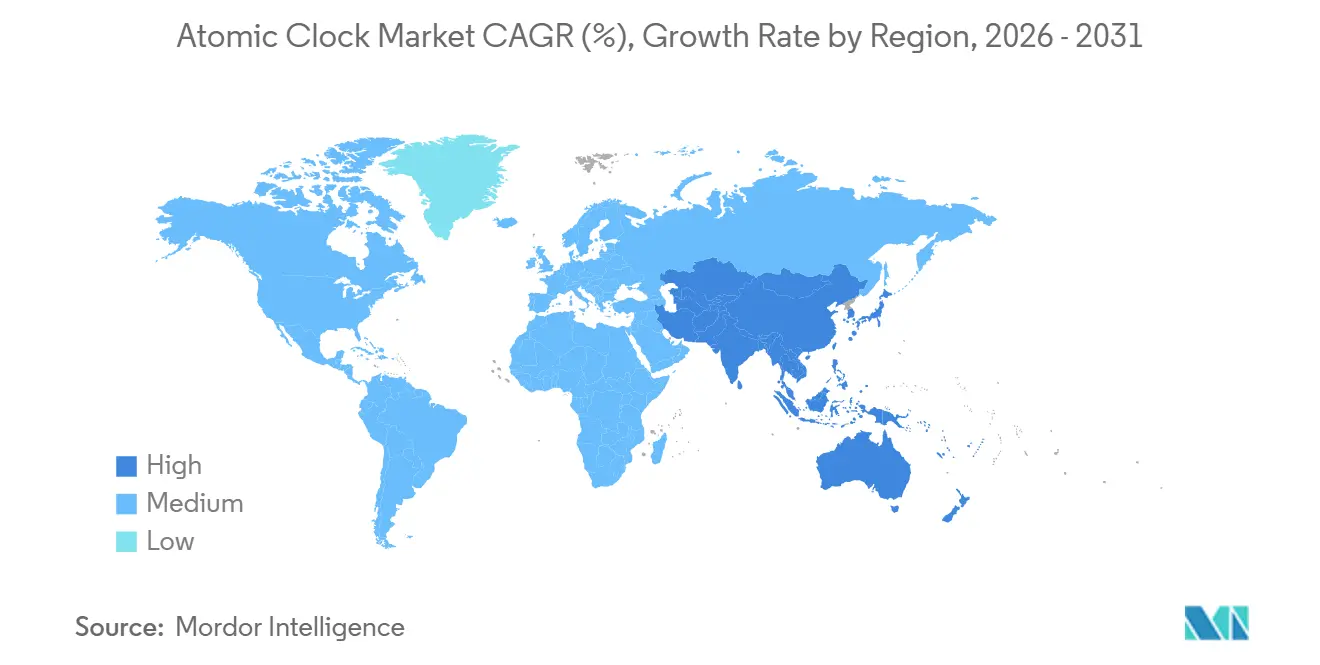

- By geography, North America held 31.91% of installed capacity in 2025; Asia-Pacific is projected to record the highest CAGR at 5.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Atomic Clock Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Satellite navigation constellation expansion | +1.2% | Global, concentrated in United States, Europe, China, India | Medium term (2-4 years) |

| Defense modernization programs and ultra-precise timing | +1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| 5G/6G network phase-synchronization requirements | +0.9% | Global, early adoption in South Korea, China, Japan, Europe, North America | Short term (≤ 2 years) |

| Quantum-sensing integration and increased R&D funding | +0.8% | North America, Europe, United Kingdom, China | Long term (≥ 4 years) |

| Growth of secure communications and electronic warfare systems | +0.7% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Emergence of chip-scale atomic clocks for IoT edge devices | +0.6% | Global, across telecom, industrial IoT, and defense handhelds | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Satellite Navigation Constellation Expansion

Expanding GNSS constellations and multi-frequency receiver design raise the bar on long-term stability and radiation tolerance for space-borne clocks, which sustains premium demand for rubidium and hydrogen-maser payloads across medium and high orbits. Lockheed Martin plans to flight test a digital atomic clock on the tenth GPS III satellite in early 2026 to push daily stability beyond the baseline for current rubidium clocks, signaling a next step in on-orbit timekeeping performance for GPS modernization.[1]Source: Lawrence Garrett, “Lockheed Martin to Test Digital Atomic Clock on Upcoming GPS III Satellite,” American Institute of Aeronautics and Astronautics, aiaa.org Europe strengthened service continuity when two Galileo spacecraft launched in December 2025, and program briefings confirm that Galileo Second Generation will add digital payloads, inter-satellite links, and experimental clock technologies to improve robustness and precision. China launched the 59th and 60th BeiDou satellites in September 2024 with upgraded hydrogen atomic clocks to validate next-generation time-frequency performance and support a BeiDou-4 roadmap toward deeper space coverage. These national investments send a clear signal that the atomic clock market will continue to benefit from satellite platform refresh cycles and broader multi-constellation adoption across user equipment.

5G/6G Network Phase-Synchronization Requirements

New radio features in 5G Advanced and early 6G roadmaps are converging on sub-nanosecond network synchronization and sub-millisecond end-to-end latency for positioning, sensing, and interactive services, directing spending toward rubidium references and high-grade time transfer at the edge. Vendor vision statements for 6G highlight the need for precise time at the physical layer to enable interactive maps and distributed intelligence. This requirement pushes operators to harden holdover and improve resilience during GNSS disruptions. This technical shift keeps the atomic clock market closely tied to telecom modernization cycles as operators upgrade base stations, deploy edge compute nodes, and extend time distribution into data centers. Public agencies also catalogue alternative and complementary PNT approaches for critical infrastructure, which sustains multi-vendor evaluation and uplifts procurement for precision timing in networks that cannot tolerate drift during signal loss.[2]Source: NTIA PNT Team, “Inventory of Complementary, Alternative, and Augmentative PNT Solutions,” National Telecommunications and Information Administration, ntia.gov As phase-coherent radio, edge inference, and time-sensitive networking scale, the atomic clock market sees broader enterprise participation beyond defense primes.

Defense Modernization Programs and Ultra-Precise Timing

Programs that enable assured PNT in contested environments are now prioritizing autonomous holdover measured in days and weeks, which sustains procurement of chip-scale clocks, miniature rubidium standards, and early optical clocks. Microchip introduced a low-noise chip-scale atomic clock with reduced power and wider temperature range in January 2025, aimed at radios, jamming systems, and unmanned platforms where SWaP remains critical. DARPA’s ROCkN program demonstrated tactical optical clocks that can sustain GPS-level timing for extended periods and enable coherent distributed sensing, highlighting a pathway for optical references in deployed environments. Frequency Electronics, through FEI-Zyfer, secured follow-on awards for high-precision airborne timing systems supporting A-PNT and specialized SIGINT architectures, with deliveries scheduled for 2027. The atomic clock market benefits as defense users move beyond periodic GPS calibration toward deeper autonomy in electronic warfare and ISR missions.

Quantum-Sensing Integration and Increased R&D Funding

Greater R&D funding for quantum sensing accelerates the migration from laboratory optical clocks to ruggedized, transportable systems that can serve navigation and precision measurement in the field. UKRI awarded GBP 14.80 million (USD 17.10 million) in late 2025 to multiple projects across quantum-enabled PNT, including cold-atom clocks and quantum time-transfer prototypes, signaling a pipeline of future products to address GNSS vulnerability. The EU’s QuRIOUS program funds training across transportable optical clocks, reflecting a strategic prioritization of quantum timekeeping capabilities for real-world applications. Infleqtion conducted flight trials and secured NASA-linked mission funding while demonstrating GPS-free timing improvements across metro fiber, broadening the use cases for optical references in networks. The AQuRA consortium aims to advance the technology readiness of optical clocks, supporting the atomic clock market as optical platforms mature alongside microwave-based standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit costs and capital expenditure intensity | -0.7% | Global, acute in emerging economies and among smaller defense contractors, affects telecom deployments | Short term (≤ 2 years) |

| Strict export-control regulations | -0.5% | United States, European Union, and cross-border transfers between NATO and non-NATO partners | Medium term (2-4 years) |

| Supply bottlenecks of enriched isotopes | -0.4% | Global, concentrated among few isotope suppliers and nuclear states | Long term (≥ 4 years) |

| Complexities in specialized infrastructure and external disruptions | -0.3% | Global, higher impact on space-qualified and radiation-hardened production lines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Unit Costs and Capital Expenditure Intensity

Pricing remains a limiting factor for mission-specific atomic clocks that require niche assemblies, long burn-in, and extensive qualification, which keeps the cost curve elevated relative to volume telecom timing. Optical lattice clocks are currently in the early stages of commercialization, with pilot production units priced at over USD 500,000. In contrast, rubidium atomic clocks used for network synchronization are available for less than USD 5,000. Chip-scale atomic clocks improve portability while operating on low power budgets, though long-term stability and drift trade-offs often require hybrid architectures that add cost and integration complexity. Program disclosures highlight performance improvements without transparent unit pricing, making competitive benchmarking difficult for new entrants and smaller integrators. Frequency Electronics’ recent awards in airborne timing underscore the strength of demand, yet per-unit cost data remains proprietary in public filings. These economics encourage selective deployments and staged rollouts as buyers balance performance, SWaP, and lifecycle support.

Strict Export-Control Regulations

Space-qualified atomic clocks often fall under USML Category XV and similar dual-use restrictions in the EU and among Wassenaar Arrangement participants, which extend licensing timelines and increase compliance costs across program tiers. The US Directorate of Defense Trade Controls outlines licensing requirements, registration fees, and penalties for violations of the International Traffic in Arms Regulations (ITAR), which influence contracting strategies and partner selection. The European Commission updated its dual-use control list in September 2025, adding new quantum-related items to further tighten oversight of high-precision timing exports.[3]Source: EC Trade, “2025 Update of the EU Control List of Dual-Use Items,” European Commission, policy.trade.ec.europa.eu Wassenaar’s 2024 update noted divergent national actions in quantum technology, leading to uneven requirements across jurisdictions. These measures lengthen subsystem approval cycles and drive greater localization, as evidenced by sovereign GNSS programs that scale domestic supplier bases to mitigate cross-border frictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cesium Commands Long-Term Reference, Rubidium Balances Cost and Portability

Cesium atomic clocks held a 40.50% share in 2025 and are projected to grow at a 5.90% CAGR through 2031, supported by their role as the primary frequency reference in metrology, defense calibration, and network master-clock duties. Cesium's standing is reinforced by national-reference upgrades, including NIST-F4, which reached 2.2 parts in 10^16 accuracy in April 2025 and contributes data to steer UTC(NIST) and support critical infrastructure timing. Vendors also advance short-term precision on cesium platforms, as shown by Oscilloquartz's enhancements to optical cesium clocks that target sub-nanosecond holdover and femtosecond stability over 1 second. In high-availability networks, cesium remains the long-term anchor, while time transfer and network architecture handle redundancy, keeping the atomic clock market oriented around hybrid clock ensembles rather than a single standard. The segment's outlook is stable because cesium underpins regulatory compliance and service-level obligations in sectors where timing integrity carries legal and operational consequences.

Rubidium and chip-scale atomic clocks make up the balance and align with space and defense missions that prize portability, power efficiency, and multi-year stability at moderate cost. Microchip's second-generation low-noise CSAC improves power and temperature resilience for field use, broadening options for unmanned systems and dismounted communications that require holdover to survive GNSS outages. Space programs continue to use rubidium and hydrogen maser clocks as complementary payloads that trade SWaP against long-term drift and aging. At the same time, on the ground, operators mix cesium, rubidium, and network-based time transfer to manage cost and performance. Chinese research institutes also target mass and power reductions in space-borne hydrogen clocks, moving from legacy 23 kg designs to new 15 kg configurations to fit next-generation satellites. Across these paths, cesium remains the primary anchor, while rubidium and CSACs expand into SWaP-constrained roles, supporting a balanced atomic clock market across platforms and mission profiles.

By End User: Civil and Commercial Installations Outstrip Defense Share, Space Accelerates

Civil and commercial installations accounted for 45.63% in 2025 as telecom networks, financial trading venues, and power utilities hardened synchronization and time-stamping. The space segment is set to grow fastest at a 6.13% CAGR through 2031 as LEO and MEO programs embed timing into spacecraft and ground stations for ranging, inter-satellite links, and service continuity. Space-based initiatives such as the Atomic Clock Ensemble in Space on the ISS test high-precision time transfer and enable new links between ground clocks with performance targets near sub-nanosecond levels. Navigation autonomy also evolves, as the Deep Space Atomic Clock program demonstrates that onboard timekeeping can reduce reliance on two-way ranging for deep-space missions. These deployments keep the atomic clock market at the center of resilient GNSS service delivery and next-generation positioning.

Defense users still represent a broad installed base across aircraft, unmanned systems, ships, submarines, and ground vehicles, which sustains steady demand for atomic references that can ride through GPS denial. Submerged navigation trials with a quantum optical wristwatch-sized payload on an extra-large uncrewed submarine validated ruggedization for naval environments and point toward future aircraft integration. DARPA’s optical timing demonstrations extend this push by enabling distributed sensors to remain coherent for extended periods without external signals. Defense-focused OEMs continue to secure contracts for airborne timing, including FEI-Zyfer’s follow-on awards in late 2025 that support assured PNT avionics. Hybrid architectures that combine quartz, rubidium, and sometimes optical elements help defense users address shock, vibration, and temperature stresses while holding tight phase alignment, which supports a resilient posture in the atomic clock market.

By Application: Navigation Leads Share, Expands Fastest on Multi-Constellation Receivers

Navigation held a 20.12% share in 2025 and is projected to grow fastest at a 6.11% CAGR through 2031 as receiver designs lock to GPS, Galileo, BeiDou, and other signals at once to suppress interference and improve continuity. China reported high adoption of BeiDou-capable devices and continued constellation expansion, supported by hydrogen-clock upgrades and a longer-term plan for extended coverage into deep space. The atomic clock market benefits as timing moves on-platform to support robust holdover during jamming and spoofing incidents that would otherwise degrade time-sensitive services. Quantum timing trials on terrestrial fiber showed measurable gains in synchronization performance without satellite input, which highlights additional paths to resilient time distribution. These trends align with the tightening of phase-alignment specifications across telecom, industrial automation, and critical infrastructure.

Non-navigation uses span electronic warfare, telemetry, communications, financial services, broadcast, and scientific instrumentation, and they rely on precise holdover and low phase noise under operational stress. Deep-space telemetry and one-way navigation gain when onboard clocks reduce latency and dependence on ground-based cues during critical mission windows. Defense sensing benefits from clock-enabled coherence across arrays that demand consistent timing for geolocation and countermeasure functions, which ties directly to optical-clock field tests in contested environments. Broadcast and media continue to use precise references to maintain frame alignment, while synchronization in data centers moves toward tighter limits to support distributed compute and storage. As more sectors operate closer to timing limits, the atomic clock market expands beyond traditional niches and integrates more deeply into digital infrastructure.

Geography Analysis

North America secured a 31.91% share in 2025 as modernization programs in defense, space, and critical infrastructure anchored a large installed base of precision timing. National reference upgrades and space-clock experiments, including NIST efforts and NASA-linked programs, reinforce the region’s leadership in metrology and deep-space navigation. Contract activity for airborne and satellite timing also continued, with OEMs announcing follow-on awards tied to assured PNT and high-precision synchronization requirements for government customers. These investments maintain demand depth in the atomic clock market while operators broaden network synchronization and time-transfer footprints.

Asia-Pacific charts the fastest trajectory, with a 5.87% CAGR from 2026 to 2031, as China validates next-generation hydrogen clocks in orbit and scales up plans for BeiDou-4 to achieve deep-space coverage by 2035. India and regional partners continue to strengthen sovereign PNT agendas and invest in timing-enhanced infrastructure across the aerospace and telecommunications sectors. Australia funded quantum-optical clock efforts for defense under AUKUS Pillar II in 2024, with deliveries planned through 2025, a signal that allied programs are diversifying their timing technology base. As national programs mix domestic development with selective imports, the atomic clock market in Asia-Pacific benefits from both policy-driven localization and commercial platform scaling.

Europe maintains steady progress with Galileo deployments and expanded experimentation in space-based time transfer and metrology. Two Galileo satellites were launched in December 2025 on an Ariane 6 to bolster constellation resilience, and ESA briefings confirm that Galileo Second Generation will add more advanced payloads and experimental clock types. ESA’s ACES mission on the ISS advances precise time transfer and links world-leading ground clocks, which helps European metrology engage with new scientific and commercial use cases. The UK continued to fund quantum-enabled PNT research in 2025, which supports a pipeline of optical-clock and time-transfer solutions for future infrastructure deployments. These activities sustain a healthy outlook for the atomic clock market in Europe across space, telecoms, and scientific domains.

Competitive Landscape

The atomic clock market is moderately consolidated with specialized suppliers across microwave and optical domains serving distinct mission sets in defense, space, and telecom. Microchip supports chip-scale deployments that require low power and broad temperature tolerance for portable and unmanned systems. Safran builds on a deep heritage in European space programs and ruggedized clocks for critical infrastructure. Oscilloquartz addresses telecom timing with enhanced cesium platforms, while Frequency Electronics focuses on precision oscillators and subsystems for airborne and satellite payloads. These roles align with program needs across SWaP constraints, radiation environments, and long-holdover requirements.

Strategic moves in 2025 and 2026 focus on product launches and ecosystem integration that bring together hardware, secure time distribution, and field services. Safran unveiled a miniature rubidium clock with a compact volume and low power draw to challenge chip-scale incumbents in UAV and LEO applications. Microchip refreshed its chip-scale portfolio with better noise and thermal performance to extend mission durations and reduce calibration cycles. Safran and Infleqtion announced a collaboration to combine an optical clock with secure time-distribution systems, which aims to deliver sub-nanosecond synchronization for GPS-denied operations in critical infrastructure and defense. This combination of precision sources and distribution networks supports new use cases while allowing phased migration from legacy timing.

Emerging players pursue photonic integration and quantum references that can deliver femtosecond-level short-term performance and resilient holdover. Vector Atomic’s rackmount optical system appears in federal inventories for PNT solutions, which signals early traction for optical references in data centers and GNSS resilience scenarios. Infleqtion raised new capital and secured NASA-linked mission work for a quantum gravity gradiometer pathfinder, while also demonstrating GPS-free timing over terrestrial networks and executing trials on an uncrewed submarine for underwater navigation. The AQuRA program’s target to push optical clocks toward greater readiness suggests that more vendors may offer deployable optical timing within the forecast period, broadening the long-term competitive set for the atomic clock market.

Atomic Clock Industry Leaders

Microchip Technology Incorporated

Safran SA

Excelitas Technologies Corp.

Leonardo S.p.A.

Oscilloquartz SA (Adtran Networks SE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: A research team from the Institute for Photonics and Advanced Sensing (IPAS) at Adelaide University successfully tested a new type of portable atomic clock at sea. This groundbreaking technology, trialed aboard a Royal Australian Navy vessel, holds promise for the next generation of navigation, communication, and scientific systems.

- December 2025: Safran Electronics & Defense and Infleqtion collaborated to advance GPS-independent quantum precision timing solutions. This partnership integrates Infleqtion’s quantum optical clock with Safran’s synchronization systems, addressing critical infrastructure needs in defense, aerospace, and telecommunications, highlighting a shift towards resilient, next-generation timing technologies in GPS-challenged environments.

- January 2025: Adtran launched the Enhanced Short-Term Unit (ESTU) precision timing module for its OSA 3300 optical cesium clocks. This upgrade addresses the absence of the passive hydrogen maser in the Western market, enhancing short-term frequency stability and positioning Adtran as a key provider of reliable timing solutions for critical industries.

Global Atomic Clock Market Report Scope

An atomic clock uses a resonator with atomic resonance frequencies. A resonator is regulated by the frequency of microwave electromagnetic radiation emitted by the quantum transition of an atom. Resonation at extremely consistent frequencies is possible, an added advantage to this approach. In terms of accuracy and precision, atomic clocks are the most accurate.

The atomic clock market is segmented by type, end user, application, and geography. By type, the market is segmented into cesium (Cs) atomic clock, rubidium (Rb) atomic clock, and hydrogen (H) maser atomic clock. By end user, the market is segmented into defense, space, and civil and commercial. By application, the market is segmented into surveillance, navigation, electronic warfare, telemetry, communication, financial trading and data centers, broadcast and media, and industrial and scientific instrumentation. The report also covers the market sizes and forecasts for the atomic clock market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Rubidium (Rb) Atomic Clock |

| Cesium (Cs) Atomic Clock |

| Hydrogen (H) Maser Atomic Clock |

| Defense | Combat Aircraft and Helicopters |

| Unmanned Vehicles | |

| Armoured Vehicles | |

| Portable Systems | |

| Naval Ships (Destroyers, Frigates) | |

| Submarines | |

| Patrol Vessels | |

| Space | |

| Civil and Commercial |

| Surveillance |

| Navigation |

| Electronic Warfare |

| Telemetry |

| Telecommunication |

| Financial Trading and Data Centers |

| Broadcast and Media |

| Industrial and Scientific Instrumentation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Rubidium (Rb) Atomic Clock | ||

| Cesium (Cs) Atomic Clock | |||

| Hydrogen (H) Maser Atomic Clock | |||

| By End User | Defense | Combat Aircraft and Helicopters | |

| Unmanned Vehicles | |||

| Armoured Vehicles | |||

| Portable Systems | |||

| Naval Ships (Destroyers, Frigates) | |||

| Submarines | |||

| Patrol Vessels | |||

| Space | |||

| Civil and Commercial | |||

| By Application | Surveillance | ||

| Navigation | |||

| Electronic Warfare | |||

| Telemetry | |||

| Telecommunication | |||

| Financial Trading and Data Centers | |||

| Broadcast and Media | |||

| Industrial and Scientific Instrumentation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the atomic clock market growth outlook to 2031?

The atomic clock market size is projected to rise from USD 693.04 million in 2026 to USD 903.50 million by 2031, reflecting a 5.44% CAGR over 2026-2031.

Which application grows the fastest in the atomic clock market to 2031?

Navigation records the fastest growth with a 6.11% CAGR over 2026-2031 as multi-constellation receivers and interference resilience raise holdover needs.

Which region leads the atomic clock market and which grows fastest?

North America leads with a 31.91% share in 2025, while Asia-Pacific charts the fastest trajectory at a 5.87% CAGR from 2026 to 2031.

Which type leads the atomic clock market and why?

Cesium-based frequency standards lead with a 40.50% share in 2025 due to primary reference roles in metrology, defense calibration, and telecom master clocks.

Which end user segment shows the highest momentum through 2031?

Space is forecasted to grow the fastest at a 6.13% CAGR, driven by constellation expansion, inter-satellite links, and precision time-transfer initiatives.

What technologies are reshaping competitive positioning in the atomic clock market?

Miniature rubidium, chip-scale advances, and early optical clocks are reshaping product roadmaps, supported by ecosystem collaborations that combine precision sources with secure distribution.

Page last updated on: