3D Printing In Aerospace And Defense Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

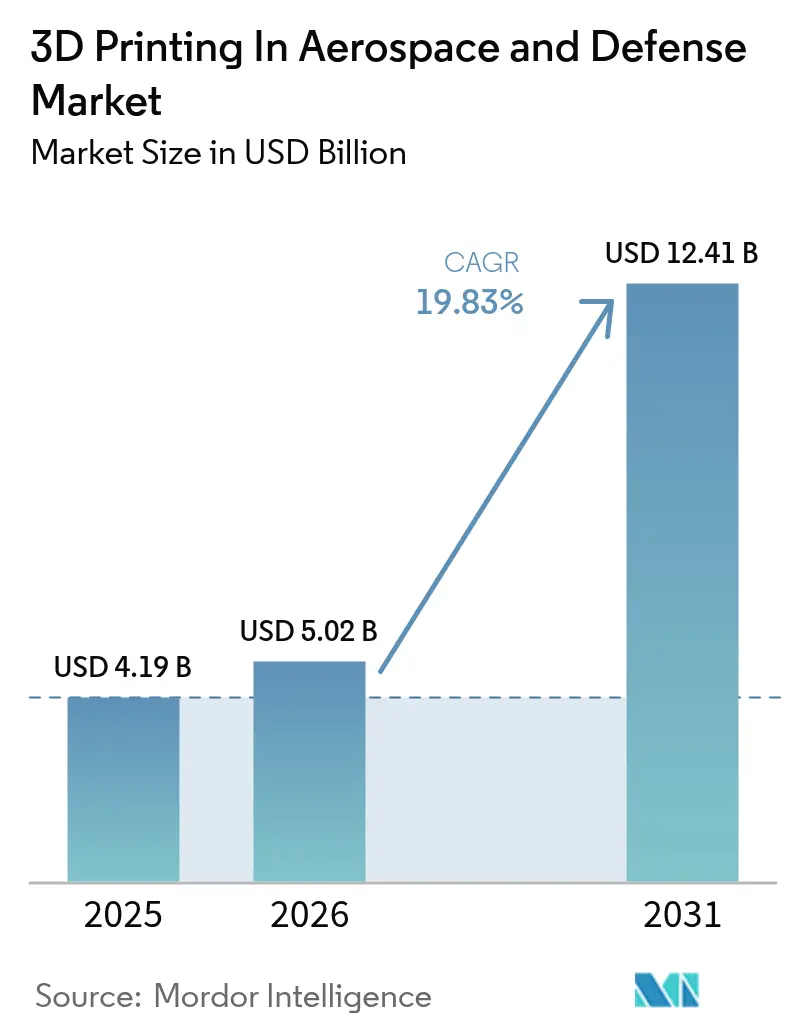

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 12.41 Billion |

| Growth Rate (2026 - 2031) | 19.83% CAGR |

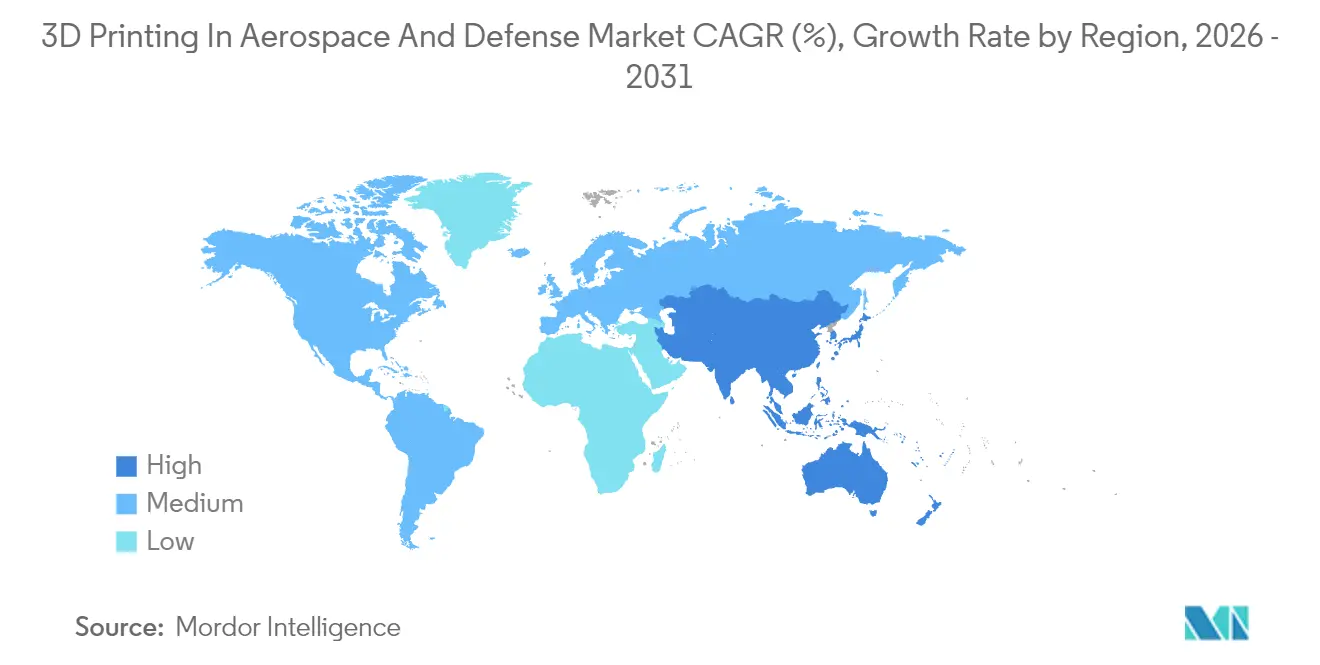

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Printing In Aerospace And Defense Market Analysis by Mordor Intelligence

3D printing in aerospace and defense market size in 2026 is estimated at USD 5.02 billion, growing from 2025 value of USD 4.19 billion with 2031 projections showing USD 12.41 billion, growing at 19.83% CAGR over 2026-2031. Rapid escalation in fuel-efficiency mandates, the need for resilient supply chains, and the maturation of next-generation manufacturing platforms propel adoption across civil, defense, and space programs. Weight-sensitive propulsion systems, serial production of cabin and structural parts, and faster qualification pathways enabled by artificial intelligence (AI) now converge to shorten time-to-market and compress development costs. Robust public funding, exemplified by the US Air Force Research Laboratory’s USD 235 million additive manufacturing (AM) innovation tranche in 2024 and NASA’s Artemis demand pull to keep North America in a leadership position.[1]Source: Air Force Research Laboratory Press Release, “Manufacturing Technology Program Awards,” afrl.af.mil Material supply agreements focused on titanium, nickel, and aluminum powders underpin ecosystem stability, while falling printer prices open participation to hundreds of tier-2 and tier-3 suppliers. Strategic equipment mergers, notably Nikon’s USD 622 million purchase of SLM Solutions, signal a shift from prototyping toward high-volume production readiness.

Key Report Takeaways

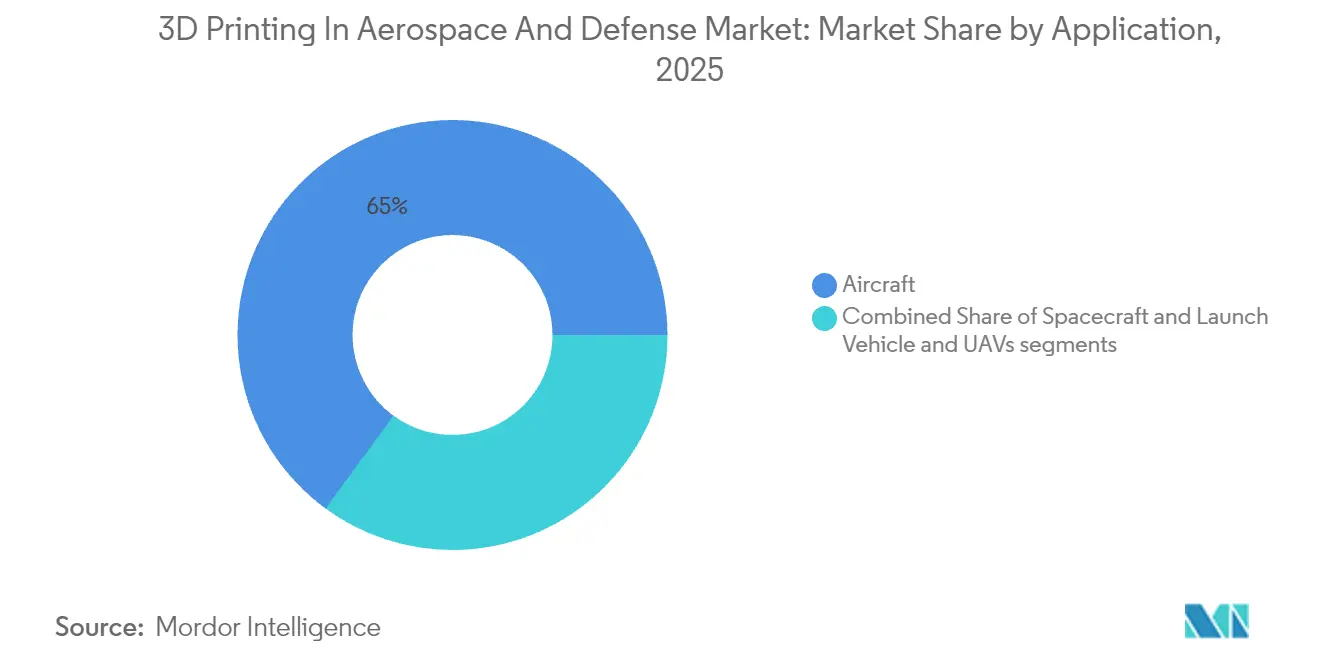

- By application, aircraft accounted for 64.95% of the aerospace 3D printing market share in 2025, while unmanned aerial vehicles (UAVs) posted the fastest 26.10% CAGR through 2031.

- By material, metal alloys captured a 60.05% share of the aerospace 3D printing market in 2025, and specialty and refractory metals are projected to grow at a 24.95% CAGR to 2031.

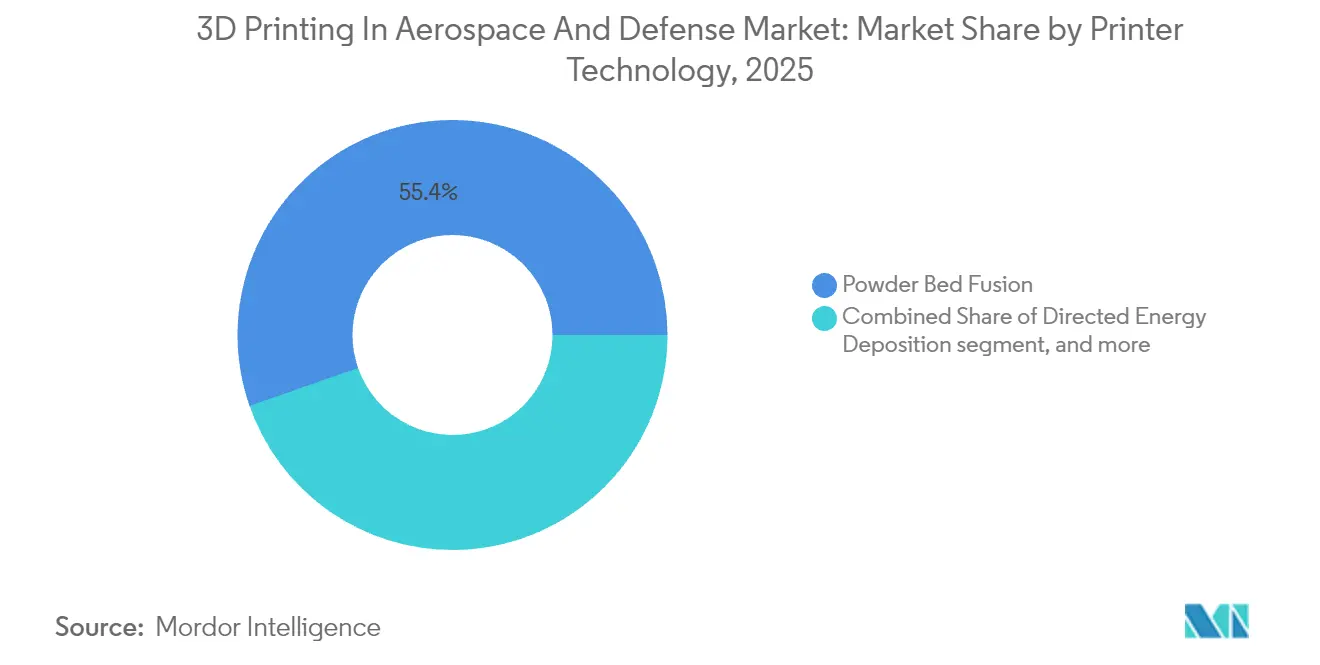

- By printer technology, powder bed fusion led with 55.35% share in 2025; directed energy deposition is advancing at a 23.70% CAGR during 2026-2031.

- By end product, engine components represented a 52.05% share of the aerospace 3D printing market in 2025, while structural components recorded the highest 22.55% CAGR through 2031.

- By printer technology, powdered fusion led with 55.35% share in 2025; directed energy deposition is advancing at a 23.70% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Printing In Aerospace And Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weight-reduction mandate for fuel-efficient fleets | +3.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Falling metal-printer and powder prices | +2.8% | Global, accelerated adoption in Asia-Pacific | Short term (≤ 2 years) |

| Defense AM-Forward funding lifts SME adoption | +3.5% | North America, expanding to allied nations | Medium term (2-4 years) |

| AI-driven qualification slashes certification lead-times | +2.1% | North America and Europe initially, global expansion | Long term (≥ 4 years) |

| In-orbital printing demand for military space assets | +1.9% | North America, China, emerging in Europe | Long term (≥ 4 years) |

| Sustainability mandates driving engine retrofits | +2.4% | Europe leading, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Weight-Reduction Mandate for Fuel-Efficient Fleets

Global aviation faces intensifying carbon goals under ICAO's CORSIA and the European Union's (EU's) Fit for 55 package, spurring manufacturers to cut airframe mass wherever possible. AM enables 40-60% weight reduction while consolidating multipart assemblies, as evidenced by GE Aerospace's LEAP fuel nozzle, which merges 20 pieces into one and trims 25% of the mass.[2]Source: GE Aerospace Communications, “LEAP Engine Fuel Nozzle Overview,” ge.com The B787 program already flies over 300 printed parts, supporting a 20% fuel-burn improvement relative to previous-generation widebodies. Complex lattice structures and internal cooling channels, impossible to machine conventionally, now pass stringent static and fatigue tests, allowing OEMs to push weight targets without compromising safety. Military programs add a tactical dimension because lighter aircraft extend range and loiter time, which is critical for next-generation fighters and long-endurance UAVs.

Falling Metal-Printer and Powder Prices

Average selling prices for production-grade metal printers fell 25-30% between 2022 and 2024, driven by competitive intensity and scaling benefits. Desktop Metal’s Shop System, priced at USD 420,000, comes roughly 40% below 2023 equivalents yet maintains AS9100-ready repeatability for steel, nickel, and titanium parts.[3]Source: Desktop Metal Product Team, “Shop System Specifications,” desktopmetal.com Parallel gains in powder recycling push reuse rates to 95-98%, slicing material spend by double-digit percentages. Höganäs AB’s Swedish capacity expansion, online since late 2024, adds thousands of metric tons of aerospace-grade titanium powder per year and narrows spot-price volatility. Lower capital thresholds enable smaller suppliers to justify AM investments for low-volume, high-mix contracts, especially in the UAV arena, where component variety is high and production runs remain modest.

Defense AM-Forward Funding Lifts SME Adoption

The US Department of Defense (DoD) earmarked USD 350 million in 2024 for AM acceleration, with the Air Force Research Laboratory (AFRL) channeled grants to small and medium enterprises and compressed seven to three years of qualification cycles. Similar initiatives under NATO’s Defence Innovation Accelerator and the UK’s Defence & Security Accelerator funnel complementary funds to allied supply bases. Financial incentives extend beyond direct cash: loan guarantees, fast-track contracting, and tax offsets lower perceived risk. Resulting supplier diversity strengthens the aerospace 3D printing market by expanding certified capacity for flight hardware at multiple tiers, making the defense industrial base more resilient.

AI-Driven Qualification Slashes Certification Lead-Times

AI models forecast material behavior with 95% accuracy, allowing regulators to accept virtual data in partial substitution for exhaustive physical testing. The FAA and NASA jointly demonstrated an eight-to-twelve-month approval route for printed brackets versus nearly two years under legacy methods. Honeywell reports 99.7% first-pass yield on turbine shrouds after embedding real-time anomaly detection powered by machine learning, eliminating costly scrap and rework. Europe echoes the trend; EASA’s latest CS-25 amendment lets AI-validated simulations offset 30% of test articles, spurring faster rollouts in A320neo and A350 lines. Virtual twins further shorten iterative design loops, pushing the aerospace 3D printing market toward genuine production cadence rather than lengthy prototyping cycles.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and powder costs for production-grade metal AM | -2.8% | Global, most acute in developing markets | Short term (≤ 2 years) |

| Stringent aerospace qualification timelines | -3.1% | Global, varying by regulatory jurisdiction | Medium term (2-4 years) |

| Titanium-powder supply-chain disruptions | -2.2% | Global, critical in Europe and Asia | Short term (≤ 2 years) |

| Cyber/IP risks from weapon-system build files | -1.7% | Defense sectors globally, highest in NATO nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Powder Costs for Production-Grade Metal AM

Even after price rationalization, turnkey systems capable of flight-hardware tolerances still cost USD 500,000-2 million, while aerospace-grade titanium or nickel powders run USD 150-300 per kg, about 30% above industrial varieties. Clean-room storage, inert-gas handling, and hot isostatic pressing double the sticker price once facilities and post-processing are counted. For suppliers in South America, Southeast Asia, and Africa, scarce financing options magnify the hurdle. The cost burden curbs expansion in regions that otherwise offer competitive labor and proximity to airframe final assembly lines, moderating the growth of the aerospace 3D printing market.

Stringent Aerospace Qualification Timelines

Critical flight parts generally require 18-36 months to meet FAA or EASA standards, dwarfing the six-to-twelve-month pathway typical in automotive applications. Documentation under DO-178C for software-driven process control alone can add a year. Full fatigue curves to 10^7 cycles must be generated for new alloys, calling for dozens of test coupons and specialized rigs that few SMEs own outright. When programs cross borders, say, a European engine supplied to a US airframer, dual authority sign-offs introduce duplicate audits and more schedule risk. Extended timelines translate into higher non-recurring engineering costs, slowing supplier willingness to invest in capacity and dampening the aerospace 3D printing adoption curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Aircraft Dominance Drives Market Leadership

Aircraft applications generated 64.95% of the aerospace 3D printing market revenue in 2025, reflecting deep penetration into cabin brackets, environmental-control ducting, and engine subassemblies. In civil fleets, every kilogram saved cuts fuel burn by roughly 0.03%, so operators welcome components that deliver double-digit weight relief while holding strength margins. The aerospace 3D printing market size for aircraft parts is projected to climb at 18.2% CAGR as single-aisle production rises above 70 aircraft per month and wide-body programs rebound. Retrofit opportunities also abound because printed replacements can match legacy form factors yet weigh considerably less, extending the lifespan of in-service fleets without extensive recertification. Airlines increasingly contract large quantities of printed cabin parts to minimize spares inventory, a practice enabled by distributed digital warehouses that store CAD files rather than physical stock.

UAVs will outpace manned platforms, expanding 26.10% annually through 2031 as defense ministries seek attritable platforms for contested environments. Short development cycles favor AM because tooling investments across several small production batches are uneconomical. Civil UAV adoption for logistics and aerial inspection also benefits; printed airframes allow rapid customization for sensor payloads or cargo bays. Together, these drivers push UAVs to deliver the most incremental revenue across the aerospace 3D printing market between 2026 and 2031.

By Material: Metal Alloys Maintain Technological Leadership

Metal alloys held 60.05% of 2025 revenue, underscoring titanium’s essential role in high-temperature zones such as combustor liners and turbine blades. AM slashes titanium buy-to-fly ratios from 15:1 to nearly 1:1, cutting raw-material waste and part cost, an unmatched advantage in metals that trade above USD 20 per kg. Stringent mechanical demands and mature qualification data sets defend the aerospace 3D printing market share for metal alloys. Nickel-based superalloys like Inconel 718 grow steadily for exhaust nozzles and hypersonic vehicle parts where creep resistance at 1,000 °C is mandatory.

Specialty and refractory metals, including niobium C103, tantalum alloys, and rhenium blends, will post a 24.95% CAGR as next-generation rocket engines and scramjets require temperature ceilings above 1,500 °C. Due to flame-smoke-toxicity compliance, high-performance polymers such as PEEK and PEI retain relevance for non-load-bearing interior parts. Still, metals dominate in any zone exposed to continuous loads or thermal cycles. Composite powders that combine aluminum with ceramic nanophases are on the horizon, yet remain a tiny share of the aerospace 3D printing market size, pending broader fatigue-data validation.

By Printer Technology: Powder-Bed Fusion Leads Market Maturity

Powder bed fusion (PBF) secured 55.35% 2025 revenue because its sub-30 µm layer heights and controlled atmospheres satisfy tight aerospace porosity limits. Multi-laser PBF platforms now reach productivity of 1,000 cm³/hr, allowing serial lots of up to 50,000 parts annually within a single cell. OEMs also value well-established parameter libraries that simplify qualification, reinforcing PBF dominance in the aerospace 3D printing market.

Directed energy deposition (DED) will chart the quickest 23.70% CAGR. Its larger melt pool supports near-net-shape build of meter-scale structures, which is attractive for wing ribs and cryogenic tanks. Deposition heads mounted on robotic arms carry out in-situ repairs, extending the life of costly turbine cases and saving millions in spare-part inventory. Material extrusion and other emerging processes remain relegated to tooling and non-critical items due to coarser resolutions, but contribute to broader adoption by offering entry-level costs for academic and tier-3 players.

By End Product: Engine Components Drive Performance Innovation

Engine components generated 52.05% of 2025 revenue, as evidenced by the LEAP nozzle, Rolls-Royce’s certified printed turbine blades, and SpaceX’s printed Raptor injectors. The aerospace 3D printing market size for engines is forecast to register a 19.05% CAGR, underpinned by the march toward higher bypass ratios and core temperatures where legacy castings fall short. Internal conformal cooling channels AM enables elevated firing temperatures, translating into 2-4% fuel-burn gains.

Structural components, though only 32.10% of revenue today, will accelerate at 22.55% CAGR due to demonstrations of topology-optimized fuselage brackets, seat tracks, and load-bearing wing ribs. Boeing’s adoption of printed titanium brackets on the B787 offers a high-visibility proof of airworthiness. Lower-criticality items-tooling inserts, trim fixtures, and low-pressure ducting-round out the remainder, providing steady if less spectacular growth.

Geography Analysis

North America controlled 43.10% of global revenue in 2025, buoyed by the presence of Boeing, Lockheed Martin, GE, and an unrivaled pipeline of defense funding. FAA Advisory Circular AC 20-170A now recognizes process simulation instead of some destructive tests, removing a major certification bottleneck. Canada’s Bombardier exploits printed interior parts to keep Learjet and Challenger cabins competitive. Mexico’s Baja California cluster leverages cost-effective labor to run powder-bed fusion lines for bracket production. US Defense AM Forward programs ensure domestic suppliers absorb early development risk, cementing regional leadership in the aerospace 3D printing market.

Europe ranks second, energized by Airbus, Rolls-Royce, Safran, and a vibrant materials-science community centered in Germany and Sweden. Europe's aerospace 3D printing market benefits from the EU Green Deal, which ties environmental targets to aircraft weight, effectively subsidizing AM adoption. EASA’s digital-thread initiatives shorten structural approvals, encouraging Lilium and Vertical Aerospace to print eVTOL airframes. France’s Toulouse cluster rallies around the R&D tax credit, seeding start-ups tackling high-temperature alloys. Meanwhile, Germany’s Fraunhofer institutes pioneer multi-laser calibration protocols that could set global PBF benchmarks.

Asia-Pacific is the fastest-growing geography at 25.95% CAGR, powered by China’s C919 ramp-up, India’s indigenization push, and Japan’s metallurgical depth. The EOS-Godrej aerospace joint venture has printed flight-qualified fuel manifolds for export-grade engines. China’s state plan earmarks AM lines for 70% of its next-generation turbofan components by 2030, establishing a formidable domestic supply chain. Mitsubishi Heavy Industries installs DED heads on five-axis mills, blending additive and subtractive steps for bulkhead repairs. South Korea’s KF-21 fighter features printed titanium bulkheads to shave structural mass. These moves anchor Asia-Pacific as a critical engine of demand in the aerospace 3D printing market.

Regulatory Landscape

Civil and defense adoption of additive manufacturing (AM) is shaped by tightening airworthiness and quality expectations, with FAA and EASA guidance and widely used standards providing the primary reference points. In the United States, the FAA continues to formalize methods of compliance for AM through its additive manufacturing guidance and Product Issues Lists (including the 2026 Q1 Small Airplane list), which can trigger Issue Paper coordination for specific AM approaches. Engine-focused oversight is also supported by FAA guidance such as AC 33.15-3 for powder bed fusion processes. In Europe, EASA Certification Memorandum CM-S-008 Issue 04 (issued 3 September 2025) frames certification effort relative to novelty, criticality, and complexity, reinforcing risk-based pathways for both structural and engine-adjacent parts.

On the defense side, procurement rules increasingly affect equipment choices and supply chains alongside technical qualification. The National Defense Authorization Act (NDAA) for Fiscal Year 2026, signed in January 2026, includes Section 849 prohibiting the US Department of Defense from contracting for certain additive manufacturing equipment produced by entities linked to China, Russia, Iran, or North Korea (with a compliance window before full enforcement). Separately, S. 2214 (Future of Defense Manufacturing Act of 2025) directs the Under Secretary of Defense for Acquisition and Sustainment to establish programs by September 30, 2026 to certify additively manufactured parts and address advanced manufacturing guidance, supporting structured qualification approaches across the defense industrial base.

Value Chain Analysis

The value chain runs across (1) digital engineering and data packages (CAD, digital twins, build files, and traceability records), (2) qualified feedstock supply for metal powders and high-performance polymers, (3) printing hardware and process parameter control, and (4) post-processing and inspection steps such as heat treatment, hot isostatic pressing, machining, and non-destructive testing. Prime contractors and OEMs (for example, Boeing, Lockheed Martin, and RTX) function as demand anchors and qualification gatekeepers, while machine OEMs, service bureaus, and specialized startups provide capacity and niche capabilities that plug into certified production systems. Operational defense demonstrations also feed into the chain by validating distributed production concepts, including the Joint Advanced Manufacturing System (JAMS) network used during RIMPAC 2026 to coordinate ship-borne and ashore metal AM assets.

Bottlenecks tend to concentrate on qualification-ready inputs and downstream finishing capacity rather than basic printing. Consistent powder chemistry and particle size control, adequate HIP and heat-treat throughput, and the availability of approved data packages for legacy or obsolete parts are recurring constraints. Certification protocols, including part-family logic, customer approvals, and audit-ready quality systems, often drive lead times and limit scaling for small and mid-tier suppliers. Programs and contracts that pull startups into prime ecosystems illustrate this expansion in practice, including Machina Labs qualifying with Lockheed Martin to produce metal structures for the JASSM platform, with production transitioning to a new 200,000-square-foot Huntsville facility.

Competitive Landscape

The aerospace 3D printing market shows moderate concentration. Strategic partnerships dominate: Boeing extended its Stratasys agreement to cabin interiors, and Airbus embeds EOS multi-laser machines directly into A350 lines. Equipment vendors pursue vertical integration; Desktop Metal controls its own powder supply through partnerships, while Velo3D offers design-for-additive software to lock in customers.

M&A spikes underline the maturing ecosystem. Nikon-SLM combines optical-metrology know-how with quad-laser powder beds to chase engine cases, while GE Additive incubates binder-jet technology for cost-sensitive brackets. Software pure-plays such as Materialise land AS9100D certification, integrating print planning into OEM product-lifecycle systems. Emerging outsiders focus on specialization: Relativity Space prints entire rocket airframes; Norsk Titanium uses rapid plasma deposition exclusively for large titanium near-net shapes. The result is a layered competitive field where IP portfolios, qualification data, and service-bureau capacity matter as much as machine throughput, shaping the trajectory of the aerospace 3D printing market.

3D Printing In Aerospace And Defense Industry Leaders

3D Systems Corporation

Ultimaker B.V.

Stratasys Ltd.

Norsk Titanium AS

EOS GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Qualification acceleration and digital-thread adoption stand out as a clear whitespace area, since certification burden continues to limit broader serial production of flight parts. NASA published its Computational Materials for Qualification and Certification (CM4QC) strategy in March 2026 to reduce the cost and time of qualification and certification for process-intensive materials, explicitly targeting metal additive manufacturing in aviation. That positioning reinforces the broader move toward computational evidence and data-driven process control. Standards and guidance adoption also supports more repeatable, auditable production flows that can be scaled across suppliers rather than requalified part-by-part, including ISO/ASTM 52920 qualification principles and SAE ARP7043 for design and repair of aircraft components, alongside FAA AC 33.15-3 for powder bed fusion in engines.

Defense and hypersonics are also creating demand for high-temperature alloys, ruggedized production, and faster iteration where additive manufacturing supports program pull. In March 2026, the US Defense Innovation Unit reported completion of a suborbital hypersonic test platform featuring the first fully 3D-printed airframe for a hypersonic platform using high-temperature alloys, illustrating a use case where additive manufacturing enables geometries and materials combinations that are difficult to industrialize with conventional methods. A second opportunity area is point-of-need manufacturing and sustainment, where distributed networks (including those demonstrated during RIMPAC 2026) highlight secure data transfer, qualified part release processes, and interoperable certification approaches across allied supply chains. This expands demand for production-grade machines, inspection capacity, and qualification services beyond centralized facilities.

Recent Industry Developments

- June 2026: Norsk Titanium formalized a multi-year Cooperation and Research Agreement with Airbus to advance the industrialization of Rapid Plasma Deposition for structural titanium parts. The agreement builds on prior certification work tied to Airbus platforms and reinforces the shift from proof-of-concept to repeatable production pathways for fatigue-critical airframe structures.

- March 2026: Stratasys Direct was selected for the U.S. Department of War Joint Additive Manufacturing Acceptability (JAMA) IV Pilot Parts Program to accelerate qualification and deployment of 3D-printed parts. The award strengthens Stratasys Directs position in defense qualification workflows where documentation, traceability, and repeatability govern scale-up from prototype lots to operational parts.

- April 2024: Relativity Space signed a USD 8.7 million agreement with the U.S. Air Force Research Laboratory to advance real-time flaw detection in additive manufacturing over a two-year period. The work targets in-process quality assurance for large-scale metal printing, supporting faster acceptance of flight-relevant parts by reducing scrap risk and increasing confidence in production monitoring.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from 3D printing (additive manufacturing) used to make aerospace and defense parts, prototypes, and tooling, across aircraft, UAV, and spacecraft programs.

Scope exclusions: 3D printing tied mainly to land vehicles and naval platforms is excluded from this market sizing.

Segmentation Overview

- By Application

- Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Spacecraft and Launch Vehicles

- By Material

- Metal Alloys (Ti, Ni, Al)

- Specialty and Refractory Metals

- High-performance Polymers and Composites

- By Printer Technology

- Powder Bed Fusion

- Directed Energy Deposition

- Material Extrusion

- Others

- By End Product

- Engine Components

- Structural Components

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- Israel

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build the initial demand map, and pull time series that can be checked year to year. We referenced public sources such as FAA airworthiness and aircraft data, NASA technical reports and program releases, US Department of Defense budget and procurement documents, and US International Trade Commission trade statistics to validate the direction of equipment and material flows.

To keep assumptions practical, we also reviewed SEC filings (such as 10-Ks), investor presentations, and product documentation published by industry participants, plus aerospace and defense association websites and reputable press coverage of qualification milestones. Patent databases were used selectively to understand where activity is moving by process and material class. We also used an import and export shipment-level database where it helped validate directional movement in powders and specialized inputs. These examples are not exhaustive, and many other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on confirming which aerospace and defense use cases are moving from prototyping into repeat production, and how qualification timelines affect near-term volumes. We spoke with a mix of equipment and material suppliers, service providers, and end users across major regions, so pricing steps, adoption rates, and country-level assumptions could be corrected when desk signals were thin.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | APAC: 49% |

| Mid tier: 49% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 19% | Managers: 55% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started with a top-down build where aerospace production and defense aviation activity are translated into an addressable additive manufacturing spend pool, and then allocated using adoption and qualification indicators. Since demand is linked to long program cycles, we tracked inputs such as aircraft and engine production rates, defense aviation procurement and sustainment intensity, the share of metal versus polymer printing in flight-critical versus noncritical uses, and typical powder and feedstock price movements.

The totals were then corroborated with selective bottom-up approximations, including sampled supplier revenue exposure to aerospace and defense, channel checks on equipment installations, and a volume-times-ASP cross-check for major material categories. When a bottom-up cut was missing for a country or a niche use case, the gap was handled by applying validated penetration rates to the closest comparable program base, followed by a sanity check against observed qualification progress.

Forecasts were built using scenario analysis anchored to production outlooks and expert views on certification pace, and then refined with light smoothing where year-to-year ordering was lumpy. Before finalizing, results were checked for alignment with program ramp-ups, material mix shifts, and expected utilization improvements at qualified sites.

Data Validation & Update Cycle

Outputs were checked against independent signals such as aerospace build rates, defense budget direction, and the pace of additive part qualification announcements, which helped flag values that moved too fast or too slow. Variances were reviewed step by step, starting with analyst model checks, followed by a second review of assumptions and formulas before sign-off. Targeted re-contacts were then triggered when a major input (such as production guidance or material pricing) shifted.

The report is refreshed annually, and interim updates are made when material events occur, such as large program awards, policy changes, or sharp shifts in aerospace production schedules. Before delivery, a final pass is completed so clients receive the latest updated view based on the most recent public information and confirmed interview feedback.

Mordor Intelligence's Aerospace and Defense 3d Printing Market Size Compared With Other Published Estimates

Published market sizes for this space can look far apart because the scope line is drawn differently, and because assumptions around qualification timing and production adoption are not always made explicit. Differences also show up when one estimate focuses only on aerospace, while another blends in wider defense manufacturing.

The key gap drivers are usually whether revenues are counted for equipment only versus equipment plus materials and services, whether aerospace is combined with broader defense platforms, and how average selling prices are moved over time as utilization rises. Currency conversion timing and how frequently the underlying aircraft production and defense aviation outlook is refreshed can also shift the stated base-year value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.02 B (2026) | |

| Industry Consultancy A | USD 4.80 B (2023) | Uses an earlier base year and a wider additive manufacturing definition that can include defense categories beyond aerospace platforms, which changes the demand pool before forecasting assumptions are applied. |

| Global Research Desk B | USD 3.13 B (2023) | Tracks aerospace 3D printing without the full aerospace and defense boundary, which can undercount production and sustainment uses tied to defense aviation programs. |

The table shows a clear spread mainly because the included end uses and the base year are not the same across sources. In the Mordor Intelligence model, aerospace programs plus defense aviation uses across aircraft, UAVs, and spacecraft are counted, while land and naval platforms sit outside scope, which shifts the total versus broader or narrower definitions. With stated variables, repeatable checks, and interview-backed adoption pacing, the number stays traceable to program activity instead of relying on a single headline growth rate.

Key Questions Answered in the Report

How fast is global demand for 3D Printing In Aerospace And Defense Market expected to grow through 2031?

The value pool is projected to expand from USD 5.02 billion in 2026 to USD 12.41 billion by 2031, equal to a 19.83% CAGR.

Which application currently generates the highest additive manufacturing revenue in aerospace?

Aircraft parts lead with 64.95% of 2025 revenue, thanks to widespread use in brackets, ducts, and engine hardware.

What region is likely to post the quickest growth?

Asia-Pacific is projected to record a 25.95% CAGR through 2031, fueled by Chinese, Indian, and Japanese aerospace programs.

Which printing technology holds the largest installed base?

Powder-bed fusion accounts for 55.35% of certified aerospace builds, driven by its fine resolution and mature qualification data.

Why are titanium powders critical to additive manufacturing for aerospace?

Titanium offers the best strength-to-weight ratio for high-temperature zones, but its supply chain remains exposed to geopolitical disruptions and price swings.

Page last updated on: