Thrust Vector Control Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

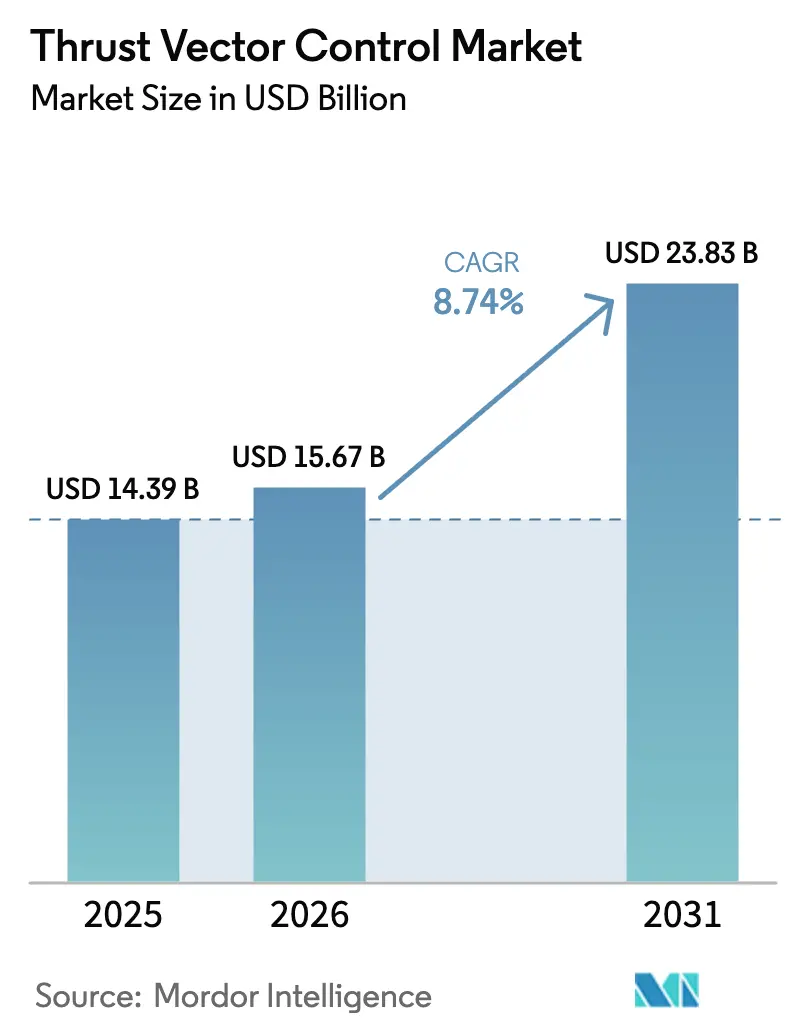

| Market Size (2026) | USD 15.67 Billion |

| Market Size (2031) | USD 23.83 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thrust Vector Control Market Analysis by Mordor Intelligence

The thrust vector control market size is expected to grow from USD 14.39 billion in 2025 to USD 15.67 billion in 2026 and is forecasted to reach USD 23.83 billion by 2031 at an 8.74% CAGR over 2026-2031. Growing launch cadence in the commercial space segment and the scale-up of reusable architectures are expanding demand for high-reliability actuators that can tolerate repeated thermal and mechanical cycles. The surge in US orbital activity, led by SpaceX, and the parallel push by Chinese commercial firms to field reusable methane-fueled vehicles, are reinforcing a multi-year order pipeline for thrust vector control hardware, software, and services. Reusable economics are compressing launch costs and raising fleet utilization, thereby increasing inspection, repair, and overhaul events for thrust vectoring subsystems across first- and upper-stage vehicles. Defense modernization is equally influential, as missile stockpile replenishment and next-generation programs fuel new production runs and upgrades for fin actuation, divert and attitude control, and nozzle vectoring solutions across tactical and strategic systems. The technology mix is shifting from hydraulic to all-electric designs to cut weight and simplify maintenance while enabling tighter digital control loops and improved efficiency, as seen in Starship’s planned electric TVC implementation for upper-stage Raptor engines.

Key Report Takeaways

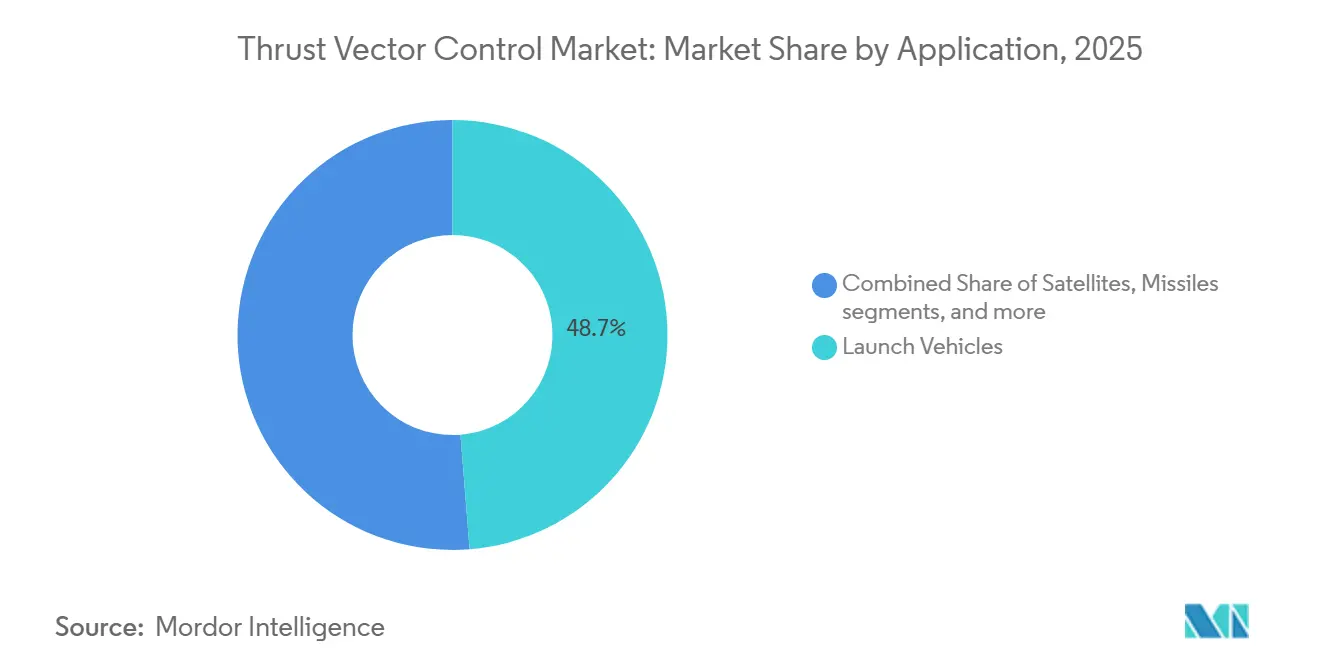

- By application, launch vehicles led with 48.73% revenue share in 2025, while satellites are forecasted to expand at a 10.68% CAGR through 2031.

- By end user, defense held 66.82% of the market in 2025, while space agencies are poised to grow at a 10.37% CAGR through 2031.

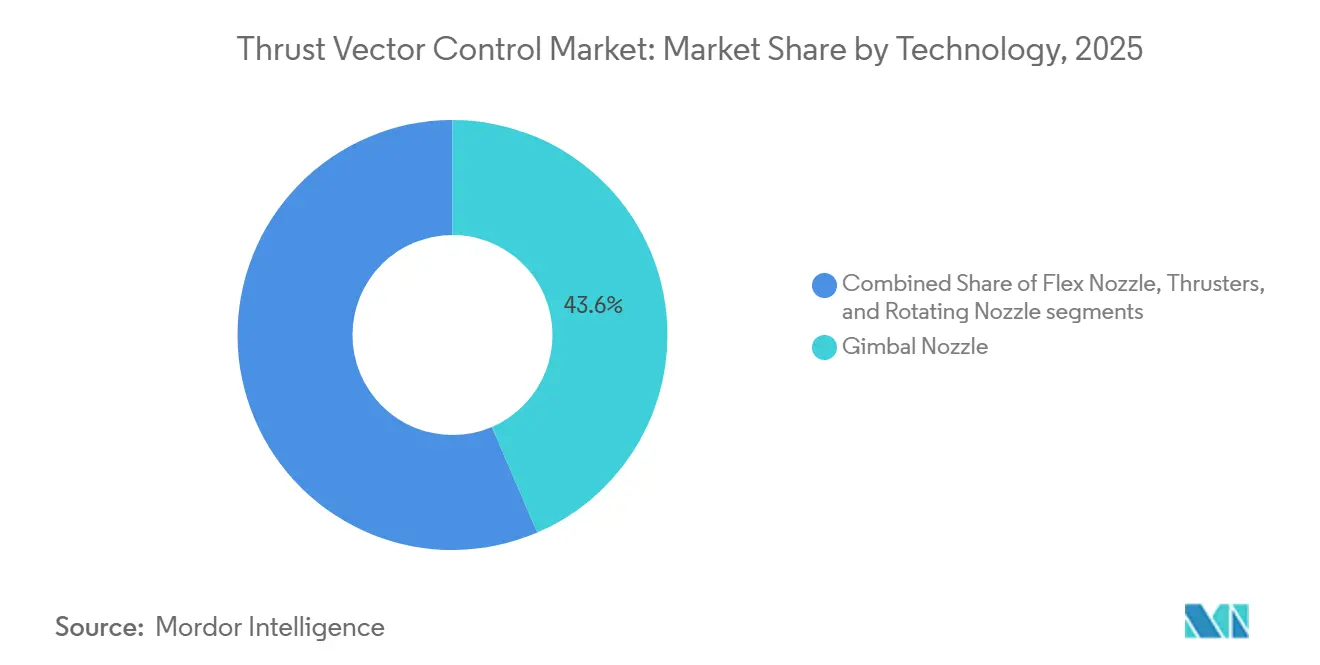

- By technology, gimbal nozzles accounted for a 43.55% share in 2025, while rotating nozzles are projected to post the fastest growth at an 11.51% CAGR through 2031.

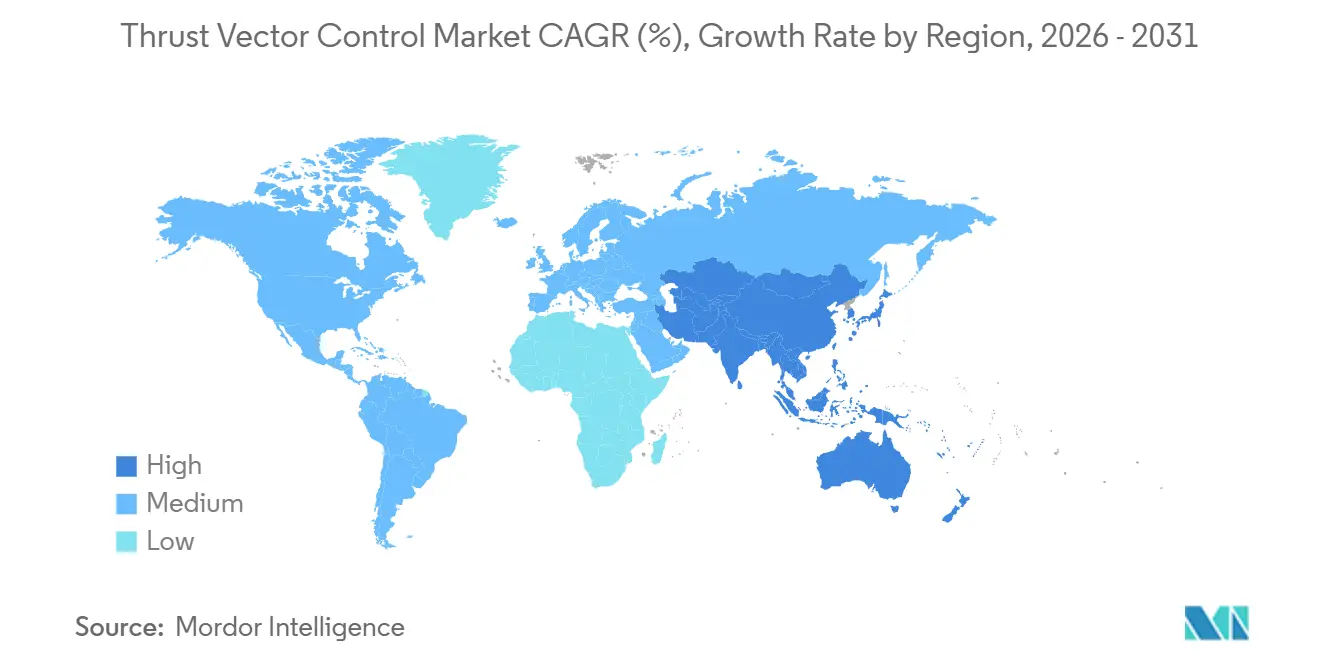

- By geography, North America retained a 46.38% share in 2025, while Asia-Pacific is set to register the fastest growth at a 9.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thrust Vector Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising launch-vehicle cadence and small-sat demand | +2.1% | Global, with concentrations in North America, Asia-Pacific (China, India), and Europe | Medium term (2-4 years) |

| Missile fleet modernization in major defense budgets | +2.4% | Global, strongest in North America, Asia-Pacific, Middle East | Long term (≥ 4 years) |

| Reusable rockets amplifying TVC maintenance cycles | +1.6% | North America, Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Hypersonic weapons race among the US, China, and Russia | +1.3% | National, with early gains in US (Huntsville, Tucson), China, Russia | Long term (≥ 4 years) |

| Commercial space-tourism and private crewed-mission boom | +0.7% | North America & EU | Short term (≤ 2 years) |

| Transition from hydraulic to all-electric actuators | +0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Launch-Vehicle Cadence and Small-Sat Demand

Global launch operations scaled to record levels in 2024 and then accelerated through 2025, with SpaceX conducting 165 orbital missions that accounted for the bulk of US activity and driving steady demand for thrust vector control systems and spares across first- and second-stage systems. Chinese commercial launch firms advanced reusable methane-fueled vehicles, and program milestones set in 2025 and 2026 signaled a region-wide shift toward reusable platforms that intensify actuator duty cycles and ground turnaround work. Reusability has increased post-flight inspections and component refurbishment, which increases the lifetime value for thrust vector control providers as launch frequency rises and fleets age. Large constellation programs such as Project Kuiper have booked launch capacity across multiple providers, which underpins long-range demand for vectoring hardware on both heavy-lift and medium-lift vehicles used to seed orbit planes at pace. This scale introduces more exacting requirements for actuator responsiveness and thermal resilience, especially for rapid relight and precision landing maneuvers in reusable operations. The thrust vector control market benefits from this cadence-driven expansion because higher flight rates and reflight targets increase the installed base, the maintenance loop, and the need for digital control upgrades over time.

Missile Fleet Modernization in Major Defense Budgets

Munitions and missile defense recapitalization programs are scaling through multi-year procurements and capacity expansions, creating stable demand for guidance, control, and thrust vectoring subsystems across air defense, cruise missiles, and interceptors. Global military expenditure rose meaningfully in 2024, and public budgets in 2025 and 2026 have prioritized standoff strike, integrated air and missile defense, and long-range fires, which pull through actuation hardware and control electronics. Japan approved its largest defense budget to date for fiscal 2026, allocating significant funds to standoff missile capability, including domestic Type-12 surface-to-ship missiles, which sustains demand for vectoring, fin actuation, and control units across production lots.[1]Mari Yamaguchi, “Japanese Cabinet Approves Record Defense Spending,” AP News, apnews.com Prime contractors have formalized framework agreements to accelerate output of critical munitions, with production targets reaching into the thousands per year across multiple lines, supporting supplier tooling, workforce expansion, and long-lead material contracts for thrust vector control components. This procurement tempo underscores the value of modularity and common interfaces for actuators and control cards, enabling adaptation across families of missiles with minimal redesign, thereby shortening qualification cycles and reducing unit cost over time. As these modernization waves continue, the thrust vector control market captures growth from both new starts and retrofit programs that upgrade legacy inventories to meet new range, maneuverability, and survivability requirements.

Reusable Rockets Amplifying TVC Maintenance Cycles

SpaceX extended its first-stage reuse records and tallied a high volume of booster landings in 2025, highlighting the wear profile that actuators and gimbal mechanisms endure across multiple cycles of ascent, entry, and landing. Lower cost per kilogram from partial and planned full reusability is changing mission economics, increasing flight rates, and expanding demand for life-limited elements within vectoring systems that require replacement or overhaul after defined cycles. Chinese firms executed vertical takeoff and landing demonstrations and scheduled orbital test flights of reusable, methane-fueled vehicles into 2026, indicating a widening customer base for ruggedized electromechanical actuators and control electronics that can withstand thermal gradients and dynamic loads unique to return and landing. The cadence targets set by next-generation heavy-lift concepts place significant emphasis on rapid inspection and swap-friendly architecture for thrust vector control subsystems to support quick turnarounds. Operators and insurers have identified thrust vectoring as a key enabler of safe landings and precision control, which influences design choices for materials, cooling, drive systems, and software redundancy. This reuse-driven operating model lifts recurring service revenue and deepens long-term customer relationships for vendors in the thrust vector control market.

Commercial Space-Tourism and Private Crewed-Mission Boom

Suborbital and orbital crewed missions set elevated safety and reliability thresholds for propulsion vectoring components, which lengthen qualification timelines and increase content value per flight article. Blue Origin completed its 37th New Shepard mission in December 2025. Then it reallocated resources in early 2026 to accelerate human lunar capability development, reflecting a roadmap that still requires robust, flight-proven actuation and control subsystems as systems evolve.[2]Blue Origin Communications, “New Shepard Completes 37th Mission,” Blue Origin, blueorigin.com Sierra Space advanced the Dream Chaser program toward its first orbital cargo mission by completing key pre-flight milestones at the Kennedy Space Center in late 2025, signaling readiness steps that set interface and reliability expectations for suppliers of thrust vector control components on related propulsion modules and docking maneuver thrusters. Private crewed flights under commercial frameworks have also demonstrated rigorous test and certification paths that translate into stringent configuration control and documentation for all critical systems. These missions drive continuous improvements in actuator health monitoring, redundancy, and digital command architectures to support fault tolerance and crew safety across ascent and reentry segments. As commercial human spaceflight expands, the thrust vector control market captures premium opportunities tied to higher assurance levels and extended verification regimes that differentiate crewed from uncrewed programs. Vendors that can demonstrate reliability in crewed environments are well-positioned to win new contracts across both public and private programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High qualification and certification cost | -0.9% | Global, with regulatory influence from NASA, FAA, ESA, ISRO | Long term (≥ 4 years) |

| Stringent reliability/safety thresholds in human–rated flight | -0.6% | National, with early gains in US (Cape Canaveral), Europe, Japan | Long term (≥ 4 years) |

| Supply bottlenecks in high-temperature composite nozzles | -0.5% | Global, with acute challenges in North America, Asia-Pacific | Medium term (2-4 years) |

| Tightening export-control regimes on dual-use propulsion tech | -0.7% | National, with gains in US, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Qualification and Certification Cost

Human spaceflight and national security programs impose rigorous standards, driving extensive verification and validation test campaigns for propulsion vectoring systems that add time and expense to development. NASA’s Aerospace Safety Advisory Panel highlighted structural and process challenges in developmental programs, reinforcing the need for strong systems engineering oversight and safety assurance, which can increase cost and delay certification for complex actuation and control elements. Commercial cargo and crew programs impose strict requirements on hardware and software integration, telemetry, and fault management, resulting in detailed documentation and qualification artifacts for thrust vector control components. FAA oversight in commercial human spaceflight adds another layer of safety processes, mishap review requirements, and return-to-flight conditions that affect propulsion vectoring systems and associated command software. These combined demands can stress smaller suppliers that lack large compliance teams, prompting them to partner with primes that already maintain mature quality systems and certification pathways. As a result, incumbents have an advantage in capturing high-assurance programs, while challengers must fund significant non-recurring engineering and qualification work before entering serial production. This cost intensity acts as a structural headwind for broad-based entry in the thrust vector control market.

Stringent Reliability/Safety Thresholds in Human-Rated Flight

NASA’s safety panel underscored the importance of clear roles and responsibilities, along with technical insight, in developmental spacecraft, noting that contracting structures can complicate risk management and slow issue resolution for crewed platforms. These observations translate into deeper scrutiny of propulsion vectoring hardware and software interfaces, redundancy, and failure modes, which lengthen test timelines and increase supplier obligations. FAA oversight also influences commercial crew activities, as mishap investigations can pause operations while corrective actions are validated, potentially cascading into supply plans for vectoring components. Human-rated vehicles require integrated system performance under maximum dynamic pressure, stage separation events, and reentry loads, imposing stringent design requirements on actuators, seals, bearings, and electronics. Vendors that can demonstrate proven reliability and provide comprehensive telemetry for condition monitoring are better placed to meet these thresholds. Even with that capability, the time and cost required to achieve approvals can slow the pace of new product introductions in the thrust vector control market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Launch Vehicles Drive Volume While Satellites Accelerate Fastest

Launch vehicles accounted for 48.73% of the thrust vector control market share in 2025, driven by reusable booster fleets and high-cadence constellation deployments. Reusability has increased lifecycle demand for actuators and vectoring hardware by enabling more maintenance cycles per vehicle. High launch rates in the US in 2025 highlighted the need for actuator reliability across repeated landings and rapid relights. Parallel developments in China with recoverable methane vehicles indicate a multi-regional opportunity for ruggedized TVC actuation and control electronics. These trends enhance the installed base, supporting predictive maintenance solutions and deeper integration of telemetry for health monitoring across thrust vector control subsystems.

Satellites are the fastest-growing application, with the thrust vector control market size for satellites projected to grow at a 10.68% CAGR from 2026 to 2031. Orbit-raising, station-keeping, and collision avoidance drive unit demand for control thrusters and precise actuation. The increasing number of active spacecraft boosts the need for reaction control systems and small thrusters. Human spaceflight logistics and cargo vehicles also influence vectoring content tied to rendezvous and docking maneuvers. As satellite volumes grow, standardization and modularity in vectoring components support common spares and lower total cost of ownership, strengthening the value proposition for operators renewing or expanding fleets.

By End User: Defense Dominates Supply While Space Agencies Pursue Sovereign Capability

Defense accounted for 66.82% of the market in 2025, driven by investments in missile defense, long-range strike, and inventory replenishment. Global military spending prioritized integrated air and missile defense and standoff weapons, leading to extended production runs and capacity expansions. Multi-year framework agreements scaled output across munitions lines, illustrating the demand for actuation and control suppliers. Export orders for air and missile defense systems reinforced the global footprint of thrust vector control content. Upgrades and new starts favored modular, ruggedized electromechanical solutions, strengthening suppliers' installed base and aftermarket potential.

Space agencies are forecasted to grow at a 10.37% CAGR through 2031 as nations invest in lunar logistics, Mars-return preparations, and new multi-mission landers and orbiters that require precise vectoring. Agency programs selecting new engines for lunar landers highlight the demand for throttleable propulsion and integrated engine controllers. Government cargo and resupply contracts for space stations and cislunar missions ensure a predictable cadence of missions where vectoring performance is critical. Programs blending civil and national security objectives expand the customer base for thrust vector control technology. Sovereign capability drives emphasize domestic supply chains and portfolio breadth, rewarding suppliers with proven heritage and documentation.

By Technology: Gimbal Nozzles Anchor Market as Rotating Nozzles Capitalize on Innovation

Gimbal nozzles captured a 43.55% share in 2025, maintaining a leadership position due to their versatility and proven performance across various applications, including small satellites, upper stages, and heavy-lift cores. These systems redirect thrust by tilting the engine or nozzle, supported by advanced actuator technology with a strong record of successful missions. Suppliers are expanding manufacturing capacity to support upcoming launch vehicle programs and hypersonic testbeds. This established heritage and associated ecosystem reinforce the gimbal segment’s ease of integration for new vehicles adopting proven architectures.

Rotating nozzles are projected to achieve the fastest growth, with an 11.51% CAGR through 2031, driven by advancements in compact directional control solutions for advanced missile systems and maneuver-critical platforms. These designs focus on high response rates, weight reduction, and digital control, aligning with the industry shift from hydraulic to electromechanical actuation. Thruster-based vectoring for spacecraft and satellites is also scaling with the deployment of constellations, increasing production volumes of small, precise control units. The technology base is advancing toward tighter software integration and standardized control electronics, streamlining qualification and reducing time-to-flight. As these systems gain flight heritage, the thrust vector control market benefits from upgrades and integration services that enhance responsiveness and maintainability.

Geography Analysis

North America retained 46.38% of the thrust vector control market share in 2025, supported by a large defense industrial base, high research and procurement outlays, and the world’s highest orbital cadence led by commercial providers. SpaceX executed 165 orbital launches in 2025 and widened the installed base of reusable first stages, which require rigorous actuator maintenance and frequent inspections, thereby supporting recurring demand for electromechanical subsystems and gimbal units.[3]Mike Wall, “SpaceX Shatters Its Rocket Launch Record Yet Again,” Space.com, space.com The US defense procurement in 2026 focuses on missile defense, standoff strike, and hypersonic development, sustaining orders for fin actuation and nozzle vectoring. NASA programs and commercial cargo initiatives continue to anchor supplier roadmaps, as Dream Chaser’s pre-flight milestones in late 2025 signaled progress toward first orbital operations, which require reliable vectoring for orbital maneuvering and reentry stability.

Asia-Pacific is projected to register the fastest growth, with the thrust vector control market in the region expanding at a 9.77% CAGR through 2031. National programs focus on reusable launch vehicles, military inventories, and sovereign satellite constellations. Chinese commercial firms reported progress on vertical recovery and planned orbital test flights through 2026, signaling demand for ruggedized vectoring systems. Japan’s record defense budget for fiscal 2026 emphasizes standoff missile capability and domestic production, elevating the need for fin actuation and nozzle vectoring content.

Europe continues to invest in space resilience and dual-use capabilities, creating opportunities for thrust vector control suppliers across launch, satellites, and defense applications. The European Space Agency advanced navigation and resilience efforts, while manufacturers delivered hardware for reusable-launcher landing legs and vectoring systems to support test campaigns. In the Middle East and Africa, defense spending growth and ambitions in space contribute to a rising addressable base for vectoring and control solutions, supported by regional procurement programs and new satellite initiatives.

Competitive Landscape

Industry leaders are consolidating capabilities in actuation, control electronics, and integration services to capture growth across launch and defense applications. Woodward expanded its portfolio by acquiring Safran’s North American electromechanical actuation business in 2025 and secured selection to supply spoiler actuation systems for the Airbus A350, broadening its exposure in primary flight control and aftermarket services. Safran enhanced its capabilities by purchasing flight control and actuation activities from Collins Aerospace in 2025, adding scale across commercial and military applications, including missiles.

Program momentum remains critical as suppliers demonstrate flight heritage and production readiness across major platforms. Moog expanded its space actuation and avionics manufacturing capacity in 2025 to support priority development programs, underscoring sustained demand for precision thrust vector control and fin-steering solutions. Spaceplane and cargo vehicle integrators advanced toward first flights, with supplier ecosystems in place for propulsion and control subsystems, reinforcing the importance of qualification and integrated test campaigns for thrust-vectoring components.

On the munitions side, framework agreements were formalized in 2026 to expand production of critical missile systems, requiring scaled deliveries of actuation hardware and control electronics that meet strict standards. In launch, operators disclosed plans to test fully electric thrust vector control on heavy-lift vehicles, underscoring interest in advanced electromechanical solutions and integrated engine controllers. European suppliers delivered structural and vectoring systems for reusable launchers, demonstrating regional capabilities in composite structures and landing and control mechanisms.

Thrust Vector Control Industry Leaders

Honeywell International Inc.

Moog Inc.

RTX Corporation

Woodward, Inc.

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sierra Space completed the initial nine satellite structures for the Space Development Agency’s Tranche 2 Tracking Layer ahead of schedule as part of a USD 740 million contract for missile warning and tracking satellites.

- June 2025: SpaceX secured a USD 81.6 million contract to launch the US military’s WSF-M2 weather-monitoring satellite in 2027, under the NSSL Phase 3 Lane 1 program. The mission, USSF-178, includes BLAZE-2 as a secondary payload and features trust vector control technology.

Global Thrust Vector Control Market Report Scope

Thrust vector control (TVC), also known as thrust vectoring, is the ability of a fighter aircraft, rocket, or other launch vehicle to manipulate the direction of the thrust from its engine or motors to control the attitude or angular velocity of the vehicle.

The thrust vector control market is segmented based on application, end user, technology, and geography. By application, the market is segmented into launch vehicles, satellites, missiles, and combat aircraft. By end user, the market is divided into space agencies and defense bodies. By technology, the market is classified into gimbal nozzles, flex nozzles, thrusters, and rotating nozzles. The report also covers the market sizes and forecasts for the thrust vector control market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Launch Vehicles |

| Satellites |

| Missiles |

| Combat Aircraft |

| Defense |

| Space Agencies |

| Gimbal Nozzle |

| Flex Nozzle |

| Thrusters |

| Rotating Nozzle |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Launch Vehicles | ||

| Satellites | |||

| Missiles | |||

| Combat Aircraft | |||

| By End User | Defense | ||

| Space Agencies | |||

| By Technology | Gimbal Nozzle | ||

| Flex Nozzle | |||

| Thrusters | |||

| Rotating Nozzle | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the thrust vector control market through 2031?

The thrust vector control market size is USD 15.67 billion in 2026 and is projected to reach USD 23.83 billion by 2031 at a CAGR of 8.74%.

Which application leads and which grows fastest in the thrust vector control market?

Launch vehicles led with 48.73% share in 2025, while satellites are forecasted to grow at a 10.68% CAGR from 2026 to 2031.

How are reusability trends shaping demand for thrust vector control systems?

Reusable boosters boost actuator duty cycles and maintenance events due to repeated ascent and landing, strengthening aftermarket and upgrade demand.

Which regions are most important for near-term growth in the thrust vector control market?

North America held 46.38% share in 2025, while Asia-Pacific is set to record the fastest growth with a 9.77% CAGR through 2031.

What technology shifts are most impactful in the thrust vector control industry?

The transition from hydraulic to fully electric actuation is improving efficiency and maintainability, with major operators planning flight tests on heavy-lift vehicles.

How do export controls and certification impact suppliers in this space?

Tightened export rules and rigorous NASA and FAA oversight add time and cost to qualification, which favors suppliers with strong compliance and flight heritage.

Page last updated on: