Ship Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

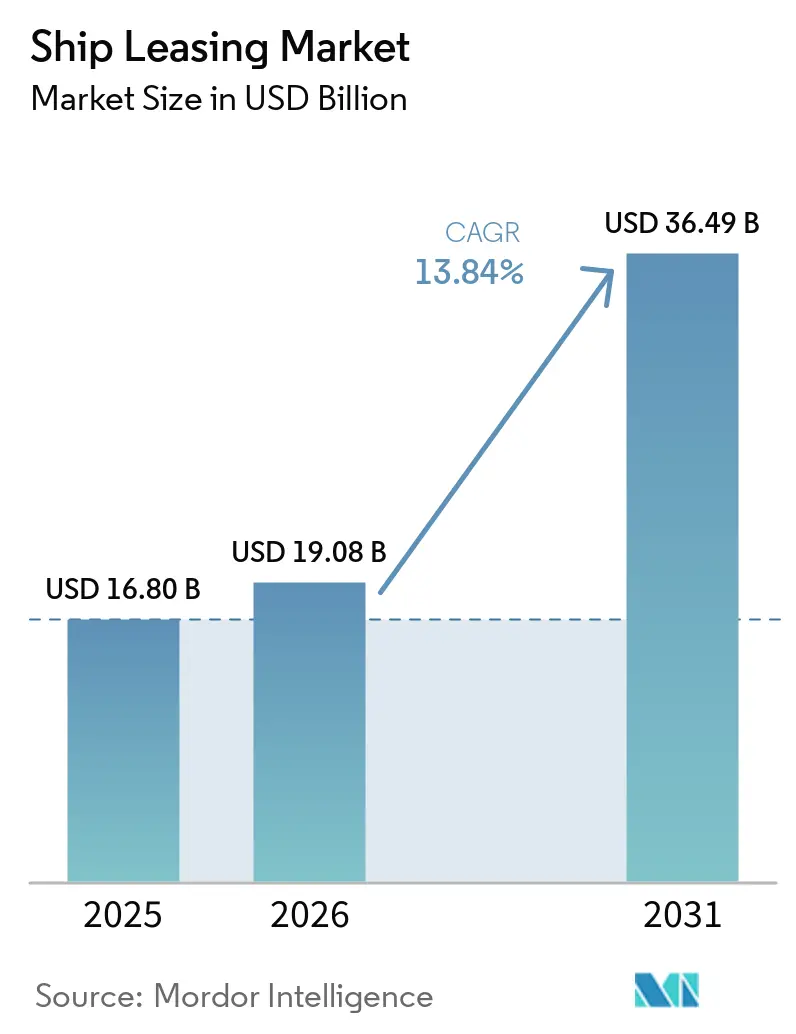

| Market Size (2026) | USD 19.08 Billion |

| Market Size (2031) | USD 36.49 Billion |

| Growth Rate (2026 - 2031) | 13.84% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ship Leasing Market Analysis by Mordor Intelligence

The ship leasing market size was valued at USD 16.80 billion in 2025 and estimated to grow from USD 19.08 billion in 2026 to reach USD 36.49 billion by 2031, at a CAGR of 13.84% over 2026-2031. Three structural shifts underpin this rapid expansion. First, the International Maritime Organization’s (IMO) Carbon Intensity Indicator (CII) reduction schedule is compressing vessel economic lives, compelling owners to retire older tonnage and seek alternative financing. Second, Basel IV capital rules are prompting European and Japanese lenders to pare ship-finance exposure, widening rate spreads and opening room for non-bank lessors. Third, geopolitical volatility, from Red Sea reroutings to potential Suez Canal normalization, has amplified demand for long-term leases that insulate liners from spot-market swings. Lessors that can embed carbon-indexed rent adjustments, provide real-time CII monitoring, and diversify across vessel classes are positioned to capture outsized value creation opportunities over the next five years.

Key Report Takeaways

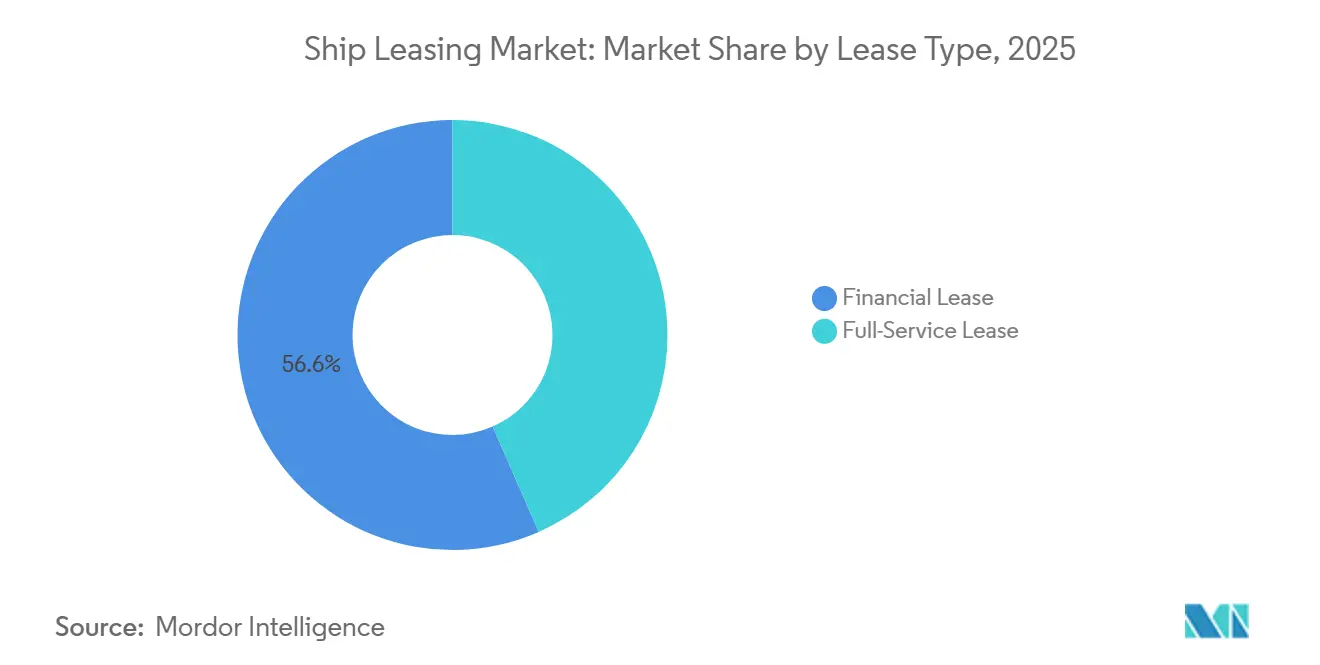

- By lease type, financial lease led with 56.57% of the ship leasing market share in 2025; full-service lease is projected to expand at a 13.89% CAGR through 2031.

- By application, container ships commanded a 57.98% share of the ship leasing market size in 2025; bulk carriers are registering a 14.01% CAGR to 2031.

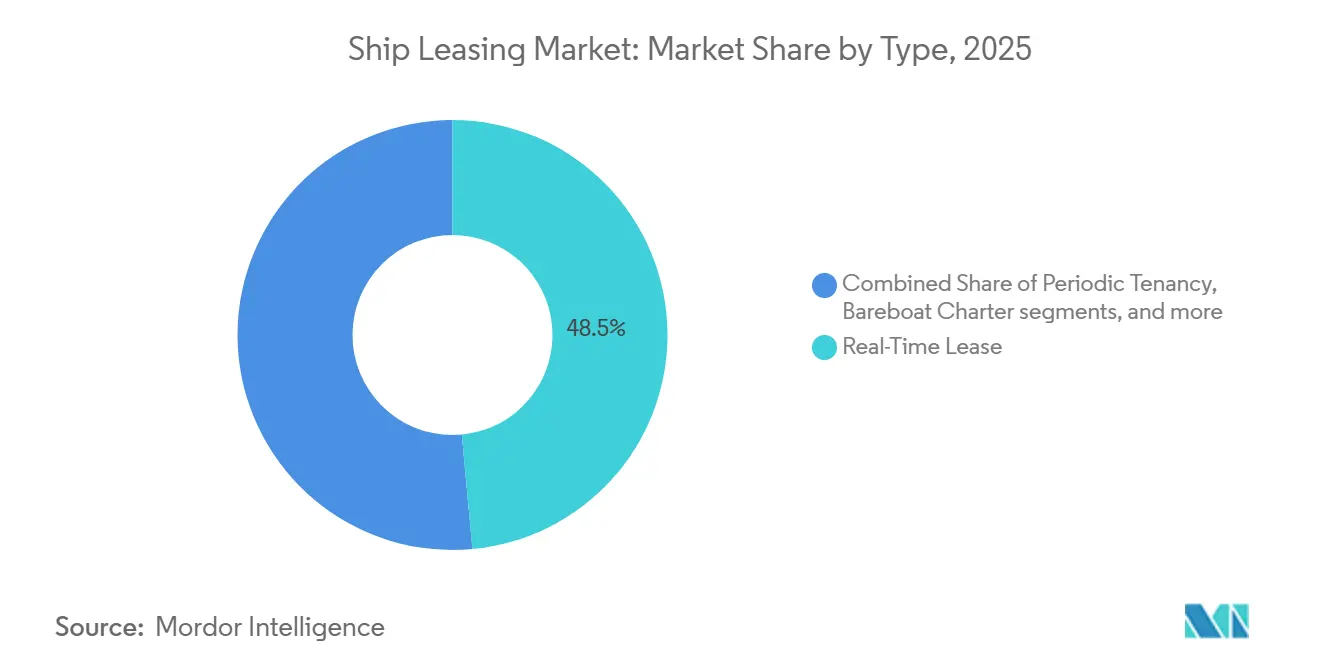

- By type, real-time lease accounted for 48.52% of revenue in 2025; bareboat charter is advancing at a 14.28% CAGR through 2031.

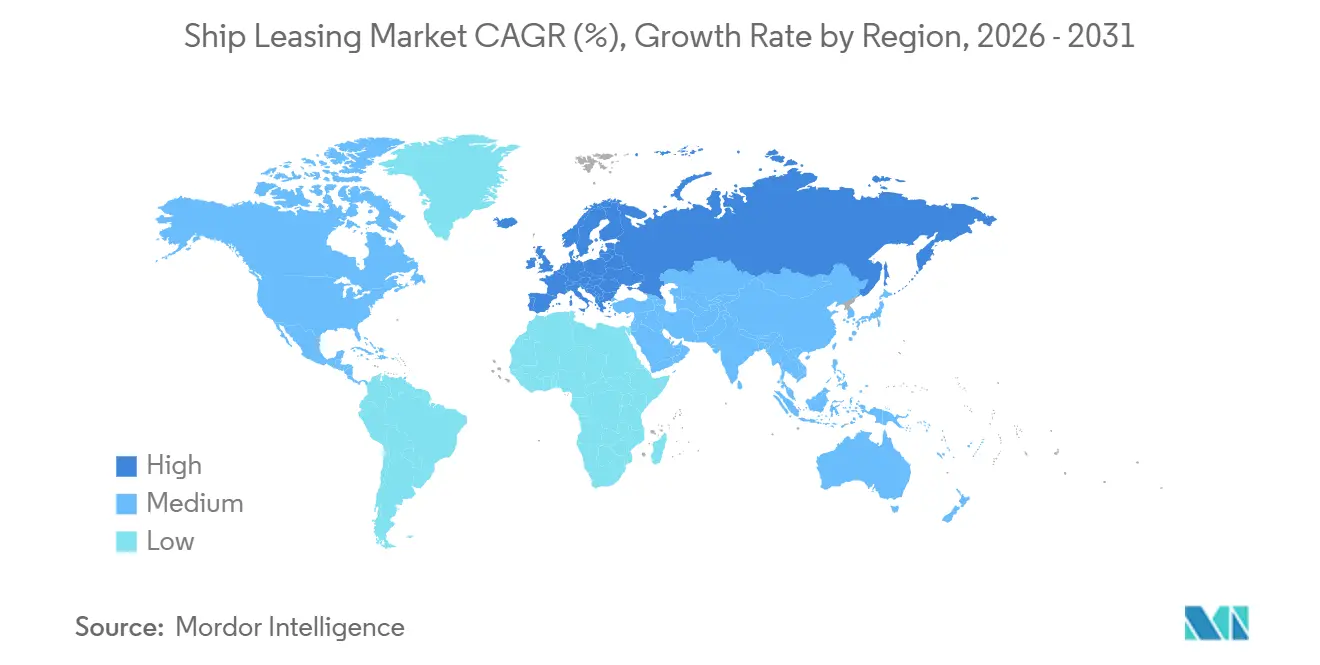

- By geography, North America held a 42.55% share in 2025; Europe is forecasted to record a 14.32% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ship Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid fleet renewal driven by IMO decarbonization rules | +3.2% | Global, with acute pressure in EU ETS zones and North-East Atlantic ECA | Medium term (2-4 years) |

| Attractive interest-rate spreads amid retreat of traditional maritime lenders | +2.8% | North America and Europe core, Asia-Pacific secondary | Short term (≤ 2 years) |

| Chinese policy banks' push for lease-based export financing | +2.5% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Rising demand for long-term charter cover by e-commerce-driven liner alliances | +2.1% | Global, concentrated in trans-Pacific and Asia-Europe trades | Medium term (2-4 years) |

| Emergence of carbon-indexed lease structures with performance-based rent | +1.6% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Tokenization of vessel assets enabling fractional digital leases | +0.9% | Singapore, UAE, select European jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Fleet Renewal Driven by IMO Decarbonization Rules

The IMO is set to review and likely increase the stringency of CII reduction factors. Between 2027 and 2030, ships will be required to achieve progressively lower carbon intensity levels, with specific targets to be finalized by 2026. Ships will need to implement advanced technologies, optimize routes, and enhance energy efficiency to remain compliant.[1]International Maritime Organization, “IMO Regulations on Energy Efficiency and Carbon Intensity,” International Maritime Organization, imo.org Non-compliance may lead to commercial disadvantages, such as increased port fees or restricted access to certain ports. As the Energy Efficiency Existing Ship Index (EEXI) and CII frameworks evolve, they are becoming increasingly integrated with regional carbon markets. The European Union Emissions Trading System (EU ETS) currently covers 50% of voyages into and out of Europe, with full coverage expected by 2026. Proactive fleets could potentially reduce operational costs by 10–15% through early compliance and strategic planning. Hamburg Commercial Bank, for instance, provided HOLBORN Europa Raffinerie GmbH with an additional EUR 100 million (USD 113.66 million) in financing for the development of a green diesel production plant.[2]Hamburg Commercial Bank, “Shipping Finance Portfolio,” Hamburg Commercial Bank, hcob-bank.com Hamburg Commercial Bank had been involved in the project since its inception and previously served as Mandated Lead Arranger for a EUR 100 million (USD 113.66 million) financing in 2023. The newest IMO life-cycle GHG guidance is prompting lessors to peg rent to CII performance, keeping lessee and lessor incentives aligned for the long haul.

Attractive Interest-Rate Spreads Amid Retreat of Traditional Maritime Lenders

Basel IV lifts risk weights on shipping and tightens concentration rules, which have led European and Japanese lenders to reduce maritime loan books since 2024 and have widened pricing for non-bank capital in the ship leasing market. The pullback increased spreads and created room for private credit and other non-bank lessors to originate leases at yields that reflect higher risk premiums. Capital from KKR, Apollo, and Oaktree is targeting sale-leasebacks at yields above 8%, compared with sub-6% returns that characterized legacy bank loans in prior cycles. The remaining banks are focusing on investment-grade exposures. Trade policy developments, including US port fees on Chinese-built ships, have also prompted restructurings of cross-border leasing special-purpose vehicles in Asia hubs, which adds to the appeal of flexible leasing formats in the ship leasing market.

Chinese Policy Banks’ Push for Lease-Based Export Financing

China emerged as the largest supplier of ship finance by 2021, with an estimated USD 100 billion in stock, representing more than one quarter of global maritime credit, underscoring Beijing’s strategic push into the ship leasing market. Bank of Communications Financial Leasing manages more than RMB 100 billion (USD 14.58 billion) across 432 vessels and ranks among the top ship lessors by portfolio value. COSCO Shipping Development (Hainan) announced through a stock exchange filing that it has ordered 10 Newcastlemax bulk carriers, each with a capacity of 210,000 dwt. These vessels are designed to be ready for methanol and ammonia. The total value of the contract is approximately USD 730 million. Industrial and Commercial Bank of China and Minsheng continue to expand cross-border leasing through platforms in the Shanghai Free Trade Zone, which offer tax deferrals and streamlined foreign exchange approvals. The model supports shipyard orderbooks and transfers residual-value risk to state-aligned lessors, enabling longer-duration paper in the ship leasing market. Chinese lessors now hold sizable shares in bulker and container leasing across Asia and the Middle East, which shifts competitive dynamics beyond traditional Western syndicates.

Rising Demand for Long-Term Charter Cover by E-Commerce-Driven Liner Alliances

Alliance restructuring in 2025, including Mediterranean Shipping Company's departure from 2M and new vessel-sharing arrangements, consolidated control over more than 850 ships among leading liner groups. This took place while the container orderbook topped 30% of the fleet, with 1.4 million TEU scheduled for delivery in 2026, which has raised the value of predictable lease cover in the ship leasing market. Carriers canceled services and executed more than 70 blank sailings during a short window to stabilize rates, which further increased interest in multi-year charters. Slow steaming has effectively removed 5-7% of nominal capacity and supported lease pricing, even as newbuilds arrive in key trades. A rapid normalization of Suez Canal traffic could prompt sharp rate declines, strengthening the case for lease-backed capacity hedges in the ship leasing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile charter rates tied to geopolitical supply-chain disruptions | -1.80% | Global, acute in Red Sea, Suez Canal, and Black Sea corridors | Short term (≤ 2 years) |

| Stricter Basel IV capital rules curbing bank syndication appetite | -1.40% | Europe and North America core, ripple effects in Asia-Pacific | Medium term (2-4 years) |

| Slow secondary-market liquidity for specialized vessel classes | -1.10% | Global, most pronounced in LNG, chemical tanker, offshore segments | Medium term (2-4 years) |

| ESG-driven investor exclusions limiting financing for older tonnage | -0.70% | Europe and North America leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Charter Rates Tied to Geopolitical Supply-Chain Disruptions

The Baltic Dry Index fluctuated between 700 and 2,500 points in 2024 as weather, conflict, and logistics constraints reshaped trade flows. Detours around the Cape of Good Hope added 10-14 days to Asia-Europe sailings, temporarily lifting spot rates. The Suez Canal Authority projects annual revenue of approximately USD 10 billion by 2026, driven by incentives for certain vessel categories. Some owners are reluctant to lock in above-cycle rates for long periods, which dampens appetite for long-term leases in parts of the ship leasing market. Bulk carrier demand remains tied to Chinese steel dynamics, even after China imported 1.1 billion tons of iron ore in 2024, keeping bulker exposure sensitive to macro policy. Forward-curve depth beyond 12-18 months is limited, and secondary liquidity in specialized classes is thin, increasing residual-value risk for lessors.

Stricter Basel IV Capital Rules Curbing Bank Syndication Appetite

Basel IV phases to 2028 and lifts standardized shipping risk weights to 100-150% based on vessel age and borrower quality, raising capital intensity for banks.[3]Bank for International Settlements, “Basel IV Capital Framework,” Bank for International Settlements, bis.org Large exposure caps at 25% of Tier 1 capital have fragmented syndication pools and raised transaction costs, which favors smaller club deals. Hamburg Commercial Bank’s shipping has shifted to 3-5 participant club deals rather than broader syndications. Japanese lenders have refocused on domestic shipowners and Japan-flagged tonnage, leaving more room for Chinese policy banks and private credit funds to lead leasing structures across the ship leasing market. The capital-charge gap between investment-grade and sub-investment-grade exposures has widened, pushing smaller operators to accept lease rates that sit 200-300 basis points above benchmarks. Secondary markets for LNG, chemicals, and offshore vessels exhibit bid-ask spreads above 15%, which constrain portfolio rebalancing and extend duration risk in lease books.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lease Type: Off-Balance-Sheet Preference Anchors Financial Dominance

Financial lease structures captured 56.57% of the ship leasing market share in 2025, while Full-Service Lease is projected to expand at a 13.89% CAGR through 2031 as operators pursue bundled support under regulatory uncertainty. Chinese lessors play a central role in the financial lease category, with Bank of Communications Financial Leasing managing a portfolio above RMB 100 billion (USD 14.58 billion) across 432 vessels, structured primarily to balance residual risk and tax efficiency. Larger shipowners that maintain technical management teams often prefer financial leases to minimize all-in ownership costs and keep control of operations within the ship leasing market. Mid-tier operators that lack scale benefits lean toward full-service lease packages that combine crewing, technical management, insurance, and compliance support to simplify operations. This split aligns capital efficiency with operating capabilities, enabling lessors to tailor products to distinct owner profiles in the ship leasing market.

Regulatory complexity is lifting demand for full-service offerings. The EU Emissions Trading System’s full inclusion of shipping from 2026, with carbon prices near EUR 80-90 per ton (USD 88-99), is expected to impose annual compliance costs that strain smaller operators that lack in-house carbon accounting tools. Full-service lessors are embedding emissions monitoring, CII optimization advice, and fuel management analytics into lease packages, which monetizes regulatory expertise. Diversified players such as SFL Corporation reported USD 182 million in quarterly revenue in 2024 and USD 113 million in EBITDA from a fleet spanning tankers, bulkers, containers, and car carriers, which illustrates margin potential in bundled models. The trajectory of Full-Service Lease growth will track mid-term IMO greenhouse gas policy milestones, which are expected to be clarified by 2027 and will shape investment plans in the ship leasing market.

By Application: Container Overcapacity Contrasts with Bulk Carrier Resilience

Container ships accounted for a 57.98% share in 2025, while the ship leasing market size for bulk carriers is projected to expand at a 14.01% CAGR through 2031 on the back of commodity trade flows and fleet optimization needs. The Mediterranean Shipping Company’s withdrawal from 2M and subsequent alliance changes reflect carriers’ pivot toward long-term charter coverage, which provides cost visibility in the ship leasing market. Lessors with modern, eco-compliant tonnage continue to secure premium utilization, as evidenced by Global Ship Lease’s 100% utilization and a 3.8-year backlog reported for 2024. The contrast is clear: the orderbook remains elevated as new deliveries enter service, keeping the focus on charter duration and fuel efficiency.

Specialized segments within “others” show diverging dynamics. LNG carrier lease rates surged during 2024-2025 as European utilities secured long-term capacity to replace pipeline gas, which sustained strong demand for long-term leases in the ship leasing market. Car carriers benefited from an export surge in electric vehicles, with China’s EV shipments rising in 2024, supporting new orders for PCTCs with advanced fire-suppression systems. The application mix is steadily shifting toward specialized tonnage that requires technical expertise and robust compliance capabilities, which favors diversified lessors.

By Type: Bareboat Flexibility Gains on Real-Time Liquidity

Real-time lease arrangements held a 48.52% share in 2025, while the ship leasing market size for bareboat charter is projected to expand at a 14.28% CAGR through 2031 as lessees seek flag flexibility and capex-sharing on eco-compliant tonnage. Bareboat charters transfer complete operational control and insurance to the lessee, enabling registry optimization and lower operating costs for owners who prioritize capital efficiency in the ship leasing market. For vessels priced between USD 50 million and USD 80 million in mid-size container classes, the ability to split capital burdens across owners and lessees supports higher fleet renewal and compliance upgrades. COSCO’s October 2025 bareboat financing of 23 methanol-ready bulkers for RMB 7.3 billion (USD 1.06 billion) highlights the structure’s appeal to state-linked enterprises.

Hybrid agreements under “other types,” including synthetic leases and lease-purchase hybrids, are growing as lessors innovate within the constraints of IFRS 16 and ASC 842. Synthetic leases can provide operating lease accounting and financing lease tax treatment, which has proven helpful for Jones Act operators that face stringent build and crew requirements. First Ship Lease Trust’s 2024 divestment of 2 older vessels and redeployment into a 2022-built Ultramax on a 6-year charter shows the portfolio tilt toward modern tonnage with stronger CII profiles in the ship leasing market. As IMO decarbonization mandates increase newbuild costs and limit the economics of older vessels on short tenors, the type mix continues to shift toward longer-duration structures that improve capital productivity for both sides of the lease.

Geography Analysis

North America commanded 42.55% of the ship leasing market share in 2025, supported by Jones Act fleet renewal and a large pool of aging vessels in domestic trades. The Jones Act ecosystem invests over USD 1 billion annually and is contending with an average fleet age above 20 years, which encourages lease-backed renewal strategies. Major US operators such as Crowley, Matson, and TOTE placed LNG-powered orders with domestic yards for deliveries through 2028, which underpin multi-year leasing needs on coastal and domestic routes. The Jones Act’s build, flag, and crew requirements create a captive market with limited foreign competition, which sustains pricing premiums in the ship-leasing market. Canada’s National Shipbuilding Strategy continues to support Arctic-capable vessels and offshore patrol ships, which complement commercial leasing opportunities that form around domestic procurement cycles. Nearshoring and cross-border trade growth are driving feeder and short-sea demand in North American corridors, supporting a steady pipeline of lease originations as logistics networks are rebalanced.

Europe is the fastest-growing region with a projected 14.32% CAGR through 2031 as emissions policy becomes a central driver of fleet decisions in the ship leasing market. The EU Emissions Trading System’s full inclusion of shipping from 2026, with carbon prices near EUR 80-90 per ton (USD 88-99) and estimated annual compliance costs of EUR 10-15 billion (USD 11-16.5 billion), is accelerating demand for scrubber-fitted, LNG-powered, and methanol-ready tonnage. Hamburg Commercial Bank’s EUR 19.4 billion (USD 22.77 billion) ship-finance portfolio, which favors green shipping, signals how European capital is aligning with climate objectives in the ship leasing market. UK Export Finance support is encouraging more domestic deals, while German and French lenders remain core arrangers in syndicated lease transactions. The EU Taxonomy defines criteria for transition-aligned assets, which gives first movers in sustainability-linked leasing an advantage in origination and pricing.

Asia-Pacific remains the volume and liquidity hub for the ship leasing market. China accounts for more than one quarter of global ship finance, a position anchored by policy banks and state-owned lessors such as Bank of Communications Financial Leasing, which manages more than RMB 100 billion (USD 14.58 billion) across 432 vessels. Japan and South Korea continue to dominate high-value construction, including LNG carriers and ammonia-ready designs. They are partnering with global lessors to channel green-propulsion newbuilds into long-term charters. Singapore’s Maritime and Port Authority supports a data infrastructure that enables performance-linked leasing and digital asset innovations across the ship leasing market. India’s Sagarmala program is building coastal and inland waterway capacity, which is opening space for short-sea leasing demand that can scale over the medium term. South America concentrates activity in Brazil, where iron ore and soybean exports support Panamax and Capesize charters, while the Middle East and Africa are emerging as growth frontiers as Gulf sovereign funds explore partnerships with established lessors.

Competitive Landscape

The ship leasing market is moderately fragmented, with the top 10 lessors controlling around a significant portion of global fleet value and a growing share of new originations coming from private credit funds. Chinese policy banks are prioritizing lease-based export financing backed by long-term charters, as illustrated by COSCO Shipping’s RMB 7.3 billion (USD 1.06 billion) bareboat financing for 23 methanol-ready bulkers in October 2025. Western lessors are embedding sustainability-linked KPIs into lease contracts in response to decarbonization alignment frameworks such as the Poseidon Principles, which are now standard among the largest maritime lenders. The result is a market where scale, cost of capital, and climate-aligned structuring capabilities are the primary differentiators.

White-space opportunities are most visible in specialized vessels where traditional bank liquidity is limited and secondary markets are thin. LNG carriers, chemical tankers, and offshore support vessels exhibit bid-ask spreads of 15% or more in secondary markets, offering entry points for technically capable lessors that can price risk and hold assets for more extended periods. Portfolio repositioning at listed leasing vehicles supports the same direction, as shown by First Ship Lease Trust’s 2024 sale of older ships and reinvestment into newer vessels with stronger CII profiles. Regulatory screening under the EU Taxonomy is raising the bar for what counts as transition-aligned capacity, which encourages fleet renewal and capital shifts toward greener tonnage.

Technology and data are emerging competitive levers. Platforms like ShipFinex are expanding the investor base by tokenizing income streams and offering automated distributions, thereby reducing friction for smaller placements in the ship leasing market. The Singapore Maritime Data Hub standardizes performance metrics that enable lessors to monitor CII and fuel consumption in near real time, supporting performance-linked pricing and verification. Association standards for digital documents, such as blockchain bills of lading, shorten administrative cycles and may improve liquidity for short-term lease assignments. Together, these capabilities help leading lessors deliver compliance support, data visibility, and financing innovation in a single package, reinforcing customer stickiness in the ship leasing market.

Ship Leasing Industry Leaders

A.P. Møller – Mærsk A/S

Hamburg Commercial Bank AG

IFCHOR GALBRAITHS Group

FSL Trust Management Pte. Ltd.

Global Ship Lease, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The FY 2027 budget submission allocated USD 1.85 billion in research and development funding to expand the US naval shipbuilding capacity. The funding is earmarked for two studies focused on future foreign frigate and destroyer designs and will also investigate a wide range of procurement options. The goal is to draw more shipbuilding capacity into domestic shipyards and increase the fleet size. This includes examining the capabilities of allied shipbuilding companies to produce ships or their components. Furthermore, this funding will be divided into two distinct efforts: one focusing on the fleet’s future cruiser/destroyer inventory and the other on frigates.

- October 2025: COSCO Shipping Development announced through the Shanghai Stock Exchange that it has contracted two domestic shipyards to construct 23 Kamsarmax bulk carriers and six VLCCs, with a total investment exceeding USD 1.7 billion.

- December 2024: A.P. Moller - Maersk entered into agreements with three shipyards to construct 20 container vessels with dual-fuel engines, totaling 300,000 TEU. These contracts finalize the company's planned owned newbuilding orders as specified in its August 2024 fleet renewal plan update.

Global Ship Leasing Market Report Scope

Ship leasing refers to a contract between a lessor and a lessee for the hire of a ship for a specific period on payment of specified rentals. In the shipping industry, a lessor (legal owner/leasing company) gives a lessee (operator/shipping company), in consideration of regular lease/hire payments, full possession and operational control of the ship for an agreed period.

The ship leasing market is segmented by lease type, application, type, and geography. By lease type, the market has been segmented into financial lease and full-service lease. By application, the market has been segmented into container ships, bulk carriers, and others. By type, the market has been segmented into a real-time lease, periodic tenancy, bareboat charter, and others. The report also covers the market sizes and forecasts for the ship leasing market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Financial Lease |

| Full-Service Lease |

| Container Ships |

| Bulk Carriers |

| Others |

| Real-Time Lease |

| Periodic Tenancy |

| Bareboat Charter |

| Other Types |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Lease Type | Financial Lease | ||

| Full-Service Lease | |||

| By Application | Container Ships | ||

| Bulk Carriers | |||

| Others | |||

| By Type | Real-Time Lease | ||

| Periodic Tenancy | |||

| Bareboat Charter | |||

| Other Types | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the ship leasing market by 2031?

The ship leasing market is forecasted to reach USD 36.49 billion by 2031, expanding at a 13.84% CAGR from 2026.

Which lease type currently dominates revenue?

Financial leases led with 56.57% of 2025 revenue, supported by off-balance-sheet accounting benefits.

Why is Europe the fastest-growing region?

EU ETS carbon costs of EUR 80-90 per ton, effective from 2026, are accelerating demand for eco-tonnage financed through sustainability-linked leases.

How are Chinese policy banks shaping global dynamics?

Policy lenders such as Bank of Communications Financial Leasing control over USD 100 billion in exposure, capturing more than 40% of bulker leasing and anchoring Belt and Road export financing.

What technological innovations are influencing the market?

Tokenization platforms like ShipFinex enable fractional vessel ownership, while real-time CII monitoring through Singapore’s Maritime Data Hub supports carbon-indexed rent structures.

Page last updated on: