Electric Vehicle Battery Swapping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

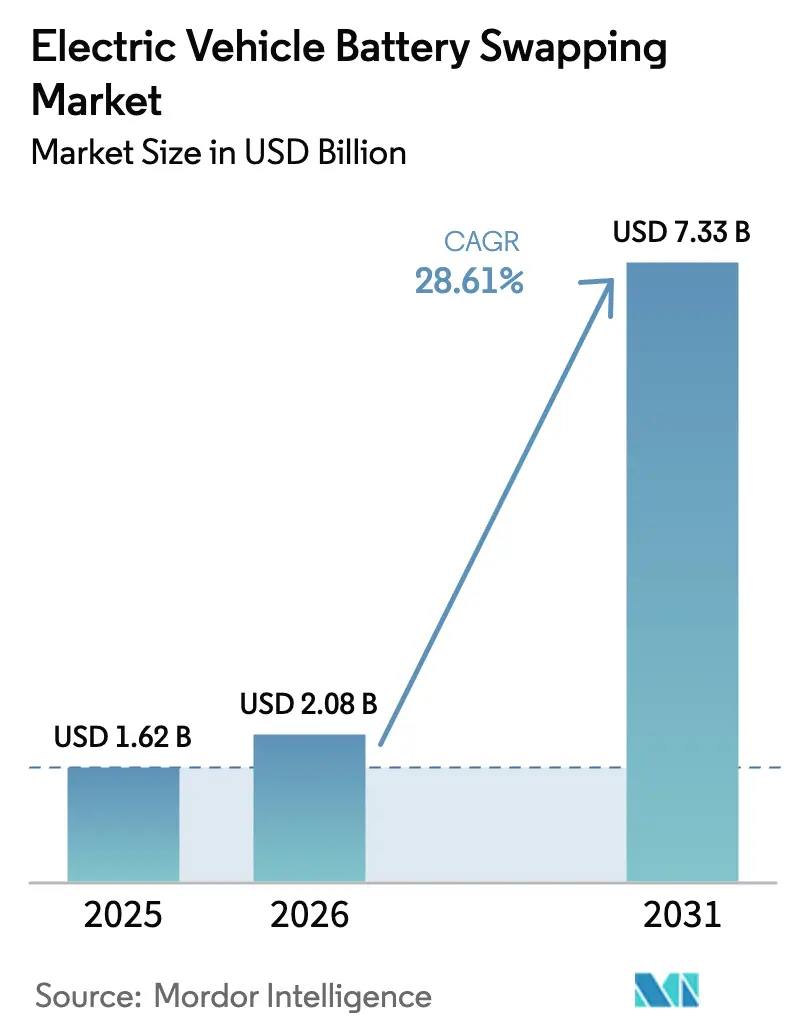

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 7.33 Billion |

| Growth Rate (2026 - 2031) | 28.61% CAGR |

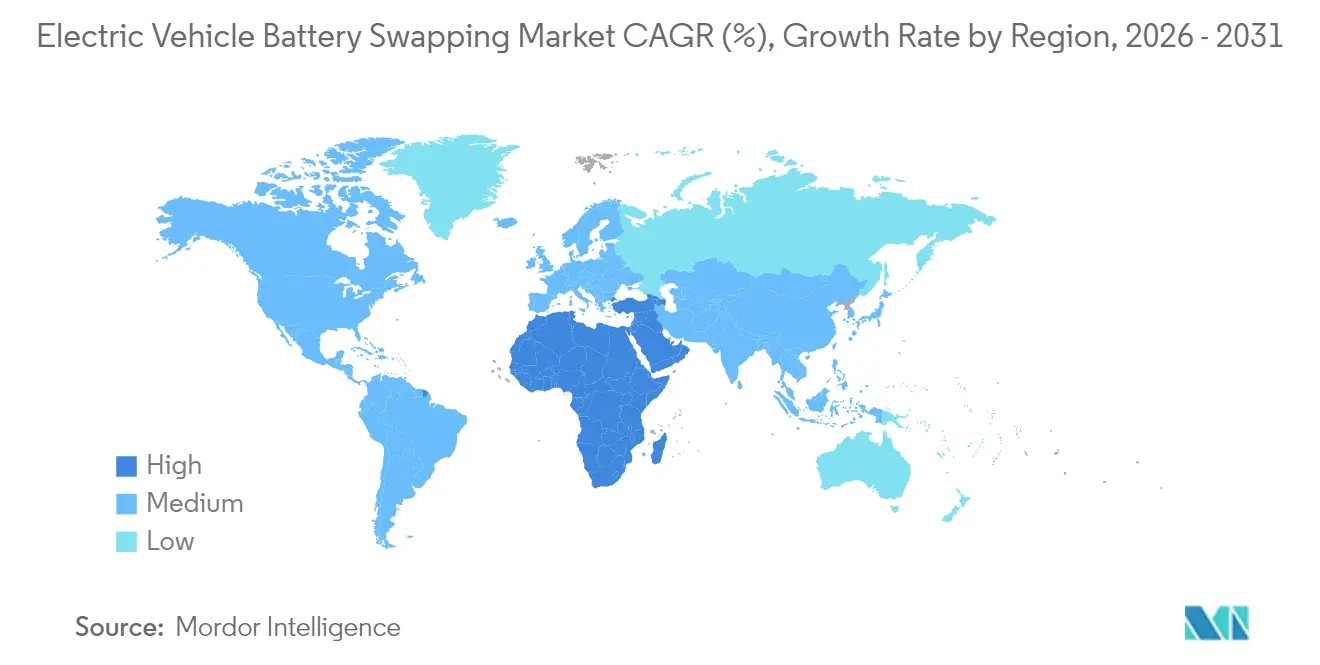

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

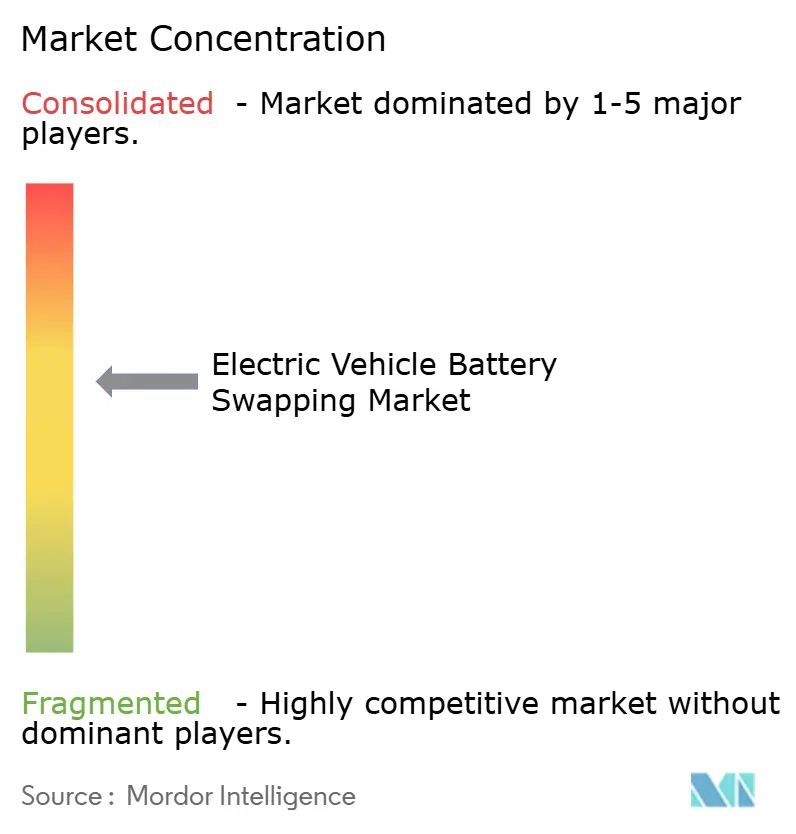

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Vehicle Battery Swapping Market Analysis by Mordor Intelligence

The Electric Vehicle Battery Swapping Market size was valued at USD 1.62 billion in 2025 and estimated to grow from USD 2.08 billion in 2026 to reach USD 7.33 billion by 2031, at a CAGR of 28.61% during the forecast period (2026-2031). Growth stems from surging EV penetration, mounting pressure to curb transport-sector emissions, and the operational advantages of instant battery exchange over plug-in charging. China’s move toward unified battery formats, highlighted by CATL’s Choco-SEB packs that enable 100-second swaps, is creating a template that other regions are now studying. Government fleet-electrification mandates have opened predictable revenue streams for station operators, while second-life battery programs are emerging as an additional profit lever through grid-storage reuse. Subscription pricing dominates revenue because it converts large battery costs into manageable operating expenses, a structure that resonates with ride-sharing, logistics, and last-mile delivery businesses.

Key Report Takeaways

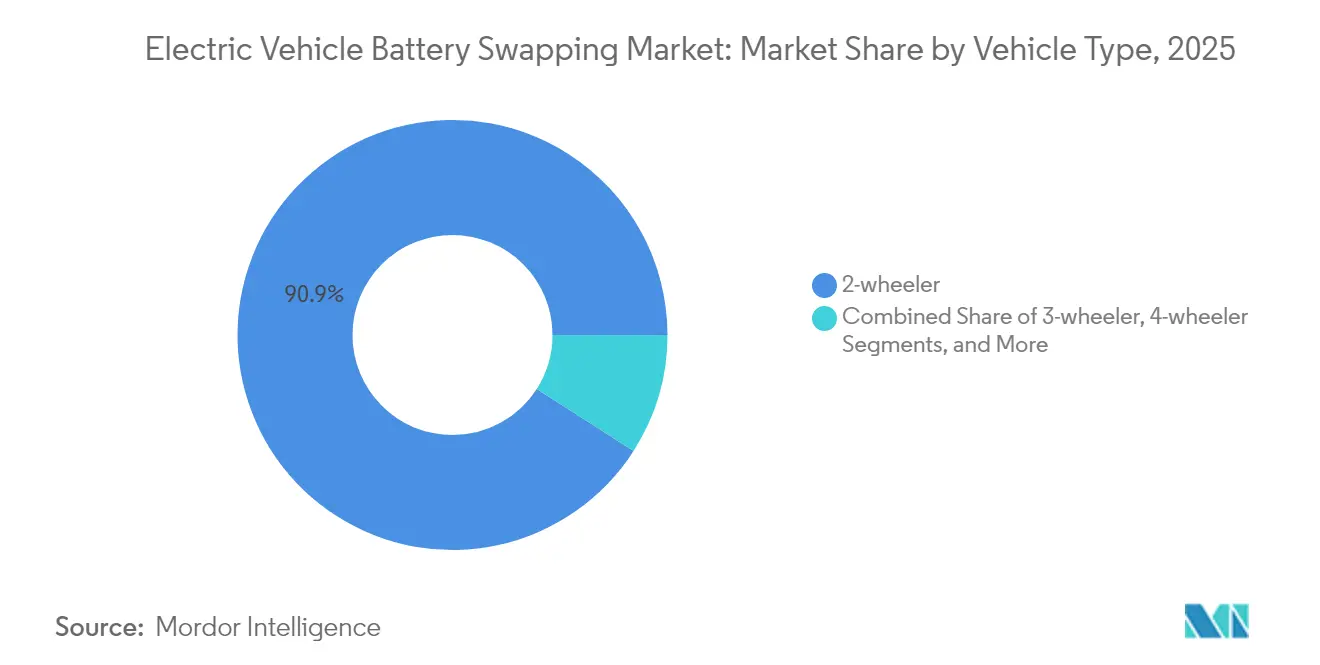

- By vehicle type, two-wheelers led with 90.94% of the EV battery swapping market share in 2025, whereas three-wheelers are projected to grow at 43.20% CAGR through 2031.

- By services, subscriptions captured 62.18% revenue in 2025; on-demand transactions are expected to advance at a 30.37% CAGR to 2031.

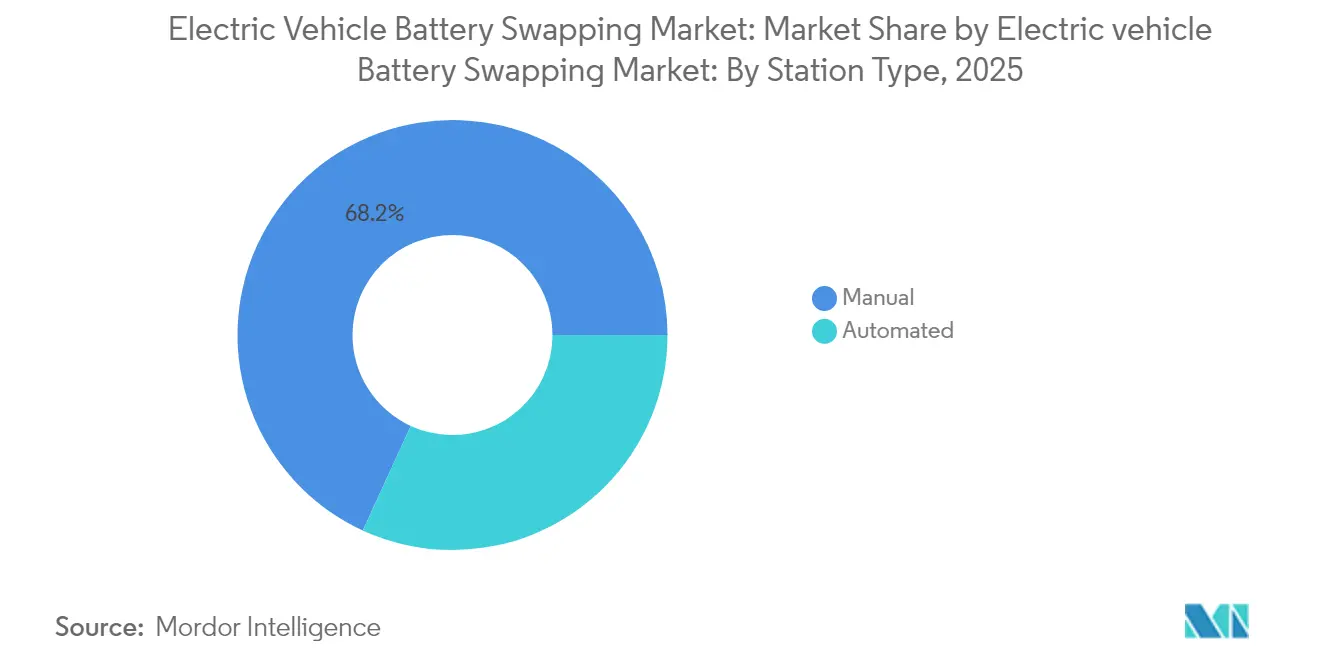

- By station type, manual installations controlled 68.15% of the electric vehicle battery swapping market size in 2025, while automated sites are expected to scale at a 28.92% CAGR.

- By battery chemistry, lithium-ion packs accounted for a 95.12% share of the electric vehicle battery swapping market in 2025 and are expected to remain the fastest-growing subsegment, with a 28.67% CAGR.

- By geography, Asia-Pacific held 52.82% of the electric vehicle battery swapping market in 2025; the Middle East and Africa region is expected to be the fastest climber, with a 39.28% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Electric Vehicle Battery Swapping Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased adoption of electric vehicles | +8.2% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Government initiatives to reduce carbon emissions | +6.8% | China, Europe, California | Medium term (2-4 years) |

| Rise in investment in battery-swapping infrastructure | +5.4% | China, India, Middle East | Short term (≤ 2 years) |

| Urban fleet-electrification mandates | +4.7% | Global Tier-1 cities | Short term (≤ 2 years) |

| AI-powered predictive analytics optimize station inventory | +3.1% | North America | Medium term (2-4 years) |

| Second-life battery valuation models | +2.3% | China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Adoption of Electric Vehicles

Critical mass in the electric two- and three-wheeler segments underpins the electric vehicle battery swapping market. Honda began large-scale swap services for the Activa e: scooter in February 2025, validating the architecture for mainstream OEMs. Battery Smart achieved 50 million cumulative swaps across 1,000 locations, demonstrating that predictable urban routes translate into repeatable, high-volume energy transactions. Meanwhile, CATL has contracted 100,000 standardized packs with 31 automakers, embedding swap capability at the design stage rather than as an aftermarket retrofit. As urban density grows, curb-side charging becomes harder to deploy, reinforcing demand for centralized facilities that can handle dozens of vehicles per hour in a footprint smaller than a retail parking bay.

Government Initiatives to Reduce Carbon Emissions

Targeted regulations are accelerating battery-swap roll-outs. India’s January 2025 guidelines formally recognized Battery-as-a-Service and mandated state utilities to supply power connections within predefined timelines, cutting through a major permitting hurdle. California’s Advanced Clean Fleets rule imposes zero-emission commercial vehicles from 2036 onward, nudging high-utilization operators toward swap-based refueling that can restore range in under three minutes[1]"California Resources Board", ZEV Forward, ww2.arb.ca.gov.. China has already certified more than 100 models for swap compatibility under CAAM standards, giving domestic players a first-mover advantage. Europe’s Battery Regulation 2023/1542 places carbon-footprint and recyclate-content disclosure obligations on pack makers, a framework that supports multi-life battery management intrinsic to swapping. Collectively, these policies pivot incentives away from generalized EV subsidies toward infrastructure-specific support that lowers operating costs for fleet operators.

Rise in Investment in Battery-Swapping Infrastructure

Institutional capital is treating swap stations as energy infrastructure rather than speculative tech. Battery Smart’s USD 65 million Series B and a USD 25 million credit line from responsibility will fund 2,500 new stations by 2027. CATL earmarked USD 345.6 million for 1,000 Chocolate swap stations in 2025, with partner funding to push the figure to 10,000 sites[2]"CATL Launches Battery Swap Ecosystem", Contemporary Amperex Technology Co., Limited, www.catl.com.. Panasonic’s minority stake in Upgrid aligns the cell manufacturer with a downstream revenue pool spanning energy-arbitrage and grid-balancing services. These deals reflect an investment thesis built on diversified cash flows, subscription fees, energy sales, battery leasing, and second-life repurposing, absent from conventional fast-charging networks.

Urban Fleet-Electrification Mandates for Last-Mile Delivery

Zero-emission zones in Shanghai, Delhi, London, and Los Angeles now restrict internal-combustion delivery vehicles during peak hours. Swap-enabled 3-wheelers avoid idle time and reclaim revenue-generating hours otherwise lost to charging. CATL’s commercial-vehicle-sized Choco modules provide 200 km range per swap, enough for two full delivery loops before a second exchange. Predictable duty cycles allow subscription pricing that locks energy costs, a compelling proposition for fleet managers.

Restraints Impact Analysis of Electric Vehicle Battery Swapping Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of battery-form-factor standardization | -4.20% | North America, Europe | Medium term (2-4 years) |

| High upfront capex for swap-station networks | -3.80% | Capital-scarce emerging markets | Short term (≤ 2 years) |

| Urban grid-capacity constraints | -2.10% | Dense legacy cities | Medium term (2-4 years) |

| Cyber-security vulnerabilities in battery-ID protocols | -1.50% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Battery-Form-Factor Standardization

OEM-specific pack shapes force operators to stock multiple SKUs, inflating inventory costs and complicating automated handling. China’s industry-government alliance achieved basic alignment, but Western automakers still pursue proprietary formats for competitive differentiation. DIN committees are working with NIO on a Europe-wide geometry standard, yet final ratification is unlikely before 2027. Ford’s modular cartridge patent hints at interoperability through adapter trays, a hardware workaround that still adds cost and complexity.

High Upfront Capex for Swap-Station Networks

Even the smallest semi-automated kiosk can exceed USD 500,000 once battery inventory is included. This strains operators in markets where interest rates sit above 9% and tenure for infrastructure loans is short. Although financial institutions are starting to classify stations as utility-grade assets, underwriting remains conservative without long-term take-or-pay contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Electric Vehicle Battery Swapping Market Segment Analysis

By Vehicle Type:

Commercial Fleets Drive AdoptionIn 2025, the two-wheeler category controlled 90.94% of the EV battery swapping market share, underscoring the influence of scooter-centric urban mobility in Asia-Pacific. Commercial three-wheelers, though smaller in absolute volume, will post the fastest 43.20% CAGR between 2026 and 2031 as delivery platforms pursue uptime gains unavailable with plug-in charging. Subscription-enabled fleets such as Battery Smart’s pool demonstrate how predictable daily swap cycles translate into stable station utilization.

The four-wheeler slice remains embryonic but is gaining visibility in ride-hailing and express-parcel fleets. NIO’s decision to extend its Battery-as-a-Service model to the Firefly mass segment will broaden consumer exposure to swap-ready sedans and crossovers. Specialized categories, airport service buggies, autonomous last-mile pods, and municipal micro-trucks occupy the emerging “Others” column and provide test beds for low-volume but high-utilization form factors.

By Services:

Subscription Models Dominate RevenueSubscriptions supplied 62.18% of 2025 revenue, affirming customer appetite for predictable monthly energy costs that decouple the battery from vehicle asset value. Gogoro’s 608,000 active subscribers paid an average of 369 TWD (USD 11.35) per month, generating USD 137.9 million in 2024 service revenue.

On-demand swaps cater to casual or seasonal riders and will expand at 30.37% CAGR as urban populations seek flexible mobility budgeting. Operators treat pay-per-swap volumes as a funnel that eventually upgrades high-frequency users into subscription tiers. Revenue mix will likely equilibrate near 50-50 once city networks achieve saturation, balancing stable base income with variable upside from tourism and part-time gig drivers.

By Station Type:

Automation Gains TractionManual kiosks still managed 68.15% of the electric vehicle battery swapping market size in 2025 thanks to low start-up cost and relaxed permitting. These sites are common in dense Southeast-Asian alleyways where robotic clearances are hard to maintain. Yet automated stations are accelerating because they cut labor, improve safety and raise throughput from 40 to 100 swaps per day. NIO’s third-generation Power Swap 3.0 bay changes a pack in 135 seconds and handles 408 daily swaps in stress tests.

As utilization passes 200 swaps per day, the cost advantage tilts toward automation. Operators are therefore pursuing a hub-and-spoke topology: flagship automated hubs on main corridors feed smaller satellite manual booths in side streets. Ford’s patent suggests mainstream automakers may incorporate alignment rails and docking logic that work across brands, potentially accelerating automation uptake once multi-OEM compatibility is proven.

By Battery Type:

Lithium-Ion Dominance ContinuesLithium-ion chemistry maintained a 95.12% stake in 2025 and still headlines growth at 28.67% CAGR, proving that incremental density gains, cost deflation and recycling ecosystems outweigh the allure of nascent chemistries. Gogoro’s solid-state lithium-ceramic prototype pushes energy density 140% higher while retaining mechanical interchangeability, implying that step-change performance is achievable without abandoning existing swap formats.

Lead-acid remains confined to low-price two-wheelers in markets with minimal range demands. Alternative chemistries such as sodium-ion or zinc-air are under laboratory study but face volumetric constraints incompatible with today’s scooter battery bays. Hence, innovation focus is squarely on lithium-ion refinement: silicon-enhanced anodes, high-nickel cathodes and advanced thermal interfaces that together lift duty cycles above 4,000 swaps before capacity dips under 80%.

Geography Analysis

APAC Electric Vehicle Battery Swapping Market

Asia-Pacific captured 52.82% of the electric vehicle battery swapping market size in 2025 on the back of a tightly aligned industrial policy and indigenous battery supply chains. China counted more than 2,300 active swap stations by December 2024, dwarfing all other regions combined, and continues to subsidize standardized packs through local grants. India’s two- and three-wheeler fleets are migrating rapidly as state energy regulators fast-track low-tariff connections for swap depots.

MEA Electric Vehicle Battery Swapping Market

The Middle East and Africa bloc shows the highest 39.28% CAGR to 2031. Sovereign funds in the United Arab Emirates have earmarked USD 1.8 billion for sustainable mobility, with NIO’s Abu Dhabi station symbolizing early-stage ecosystem anchoring. African capitals where grid reliability is uneven are exploring containerized solar + swap micro-hubs, leapfrogging expensive public charging corridors.

North America and Europe Electric Vehicle Battery Swapping Market

North America and Europe trail adoption but hold latent potential. California’s rulebook offers visibility for investors to underwrite long-life infrastructure, while the EU’s recycled-content mandate dovetails with swap-centric circular-economy propositions. CATL confirmed memoranda with fleet operators in Germany and France for pilot hubs by 2026. Permitting regimes remain the critical path item; nonetheless, once two or three standardized formats emerge, operators expect replication curves similar to Asia’s first wave.

Competitive Landscape

Competitive intensity is moderate; top players expand geographically rather than undercut on price. CATL and NIO are vertically integrating cell manufacture, vehicle partnerships, and station hardware to keep margin across the chain. Their 2025 agreement assigns CATL a minority stake in NIO and commits both to co-develop Firefly-brand swap-ready mass vehicles, reinforcing the network-effect moat around their shared battery spec.

Gogoro remains dominant in Taiwan and is exporting its franchise model through joint ventures in Tel Aviv, Jakarta, and Seoul. Battery Smart commands a significant share of organized swap activity in India’s National Capital Region, focusing on ultra-dense 2-wheeler corridors and franchised micro-stations. Panasonic’s Upgrid investment signals a play for B2B energy-as-a-service revenues, while Ford’s patent disclosures hint at an eventual OEM-run network in North America.

The technology race centers on automation throughput and digital optimization. Operators with AI-driven fleet-level state-of-health dashboards can allocate batteries dynamically and flag anomalies before catastrophic failure, reducing warranty costs. Collaboration, not head-to-head rivalry, is therefore the emerging norm as firms see greater value in shared standards that expand the total addressable EV battery swapping market.

Electric Vehicle Battery Swapping Industry Leaders

-

Gogoro

-

NIO

-

Ample

-

Battery Smart

-

Sun Mobility

- *Disclaimer: Major Players sorted in no particular order

Electric Vehicle Battery Swapping Market Companies Covered in this Report

- Amara Raja Group

- Ample

- Aulton New Energy Automotive Technology Co. Ltd

- Battery Smart

- Bounce Infinity

- Esmito Solutions Pvt Ltd

- Gogoro

- IMMOTOR

- Kwang Yang Motor Co. Ltd (KYMCO)

- Lithion Power Private Limited

- NIO

- Numocity

- Oyika Pte. Ltd

- SUN Mobility

- Swobbee

- VoltUp

- RACE Energy

- MO Batteries

- EVeez

Recent Industry Developments in Electric Vehicle Battery Swapping Market

- March 2025: CATL pledged USD 345.6 million for 1,000 new Chocolate swap stations and invested in NIO to standardize cross-brand packs.

- November 2024: Honda introduced Activa e: swap service in India, marking the first mass-volume OEM deployment outside China.

- March 2024: Ola Electric patented a new swappable battery technology designed specifically for its upcoming B2B electric scooters and rickshaws. These batteries feature a boxy design with a top handle, facilitating easy installation & removal.

Global Electric Vehicle Battery Swapping Market Report Scope

Segmentation Overview

| 2-Wheeler |

| 3-Wheeler |

| 4-Wheeler |

| Others |

| Subscription |

| On-demand |

| Manual |

| Automated |

| Lithium-ion |

| Lead-acid |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Mexico | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | 2-Wheeler | |

| 3-Wheeler | ||

| 4-Wheeler | ||

| Others | ||

| By Services | Subscription | |

| On-demand | ||

| By Station Type | Manual | |

| Automated | ||

| By Battery Type | Lithium-ion | |

| Lead-acid | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Electric Vehicle Battery Swapping Market in 2026?

The Electric Vehicle Battery Swapping Market size is valued at USD 2.08 billion as of 2026 and is on track for a 28.61% CAGR toward 2031.

Which vehicle segment adopts battery swapping the most?

Two-wheelers dominate, holding 90.94% market share in 2025 thanks to dense scooter fleets in Asia-Pacific.

What drives the rapid growth of swap stations in the Middle East?

Sovereign wealth funds are financing sustainable transport projects, and relaxed permitting plus plentiful real estate support fast station roll-outs.

Why do operators prefer subscription models?

Subscriptions convert high battery ownership costs into predictable monthly operating expenses, improving cash flow and facilitating network expansion.

Will lithium-ion remain the chemistry of choice?

Yes, lithium-ion keeps a 95.12% share and continues to improve in energy density, making it the backbone of swap-ready designs well into the next decade.

Page last updated on: