Electric Two-Wheeler Battery Management System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.24 Billion |

| Market Size (2030) | USD 3.70 Billion |

| Growth Rate (2025 - 2030) | 10.58% CAGR |

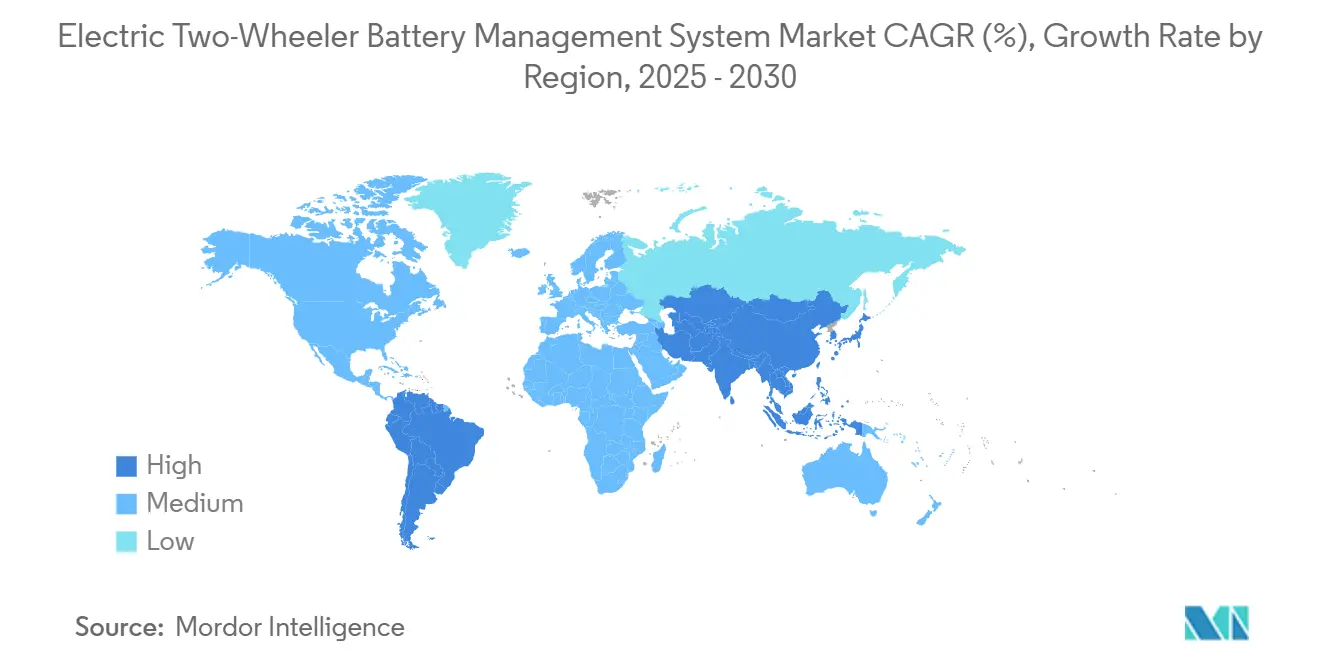

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Two-Wheeler Battery Management System Market Analysis by Mordor Intelligence

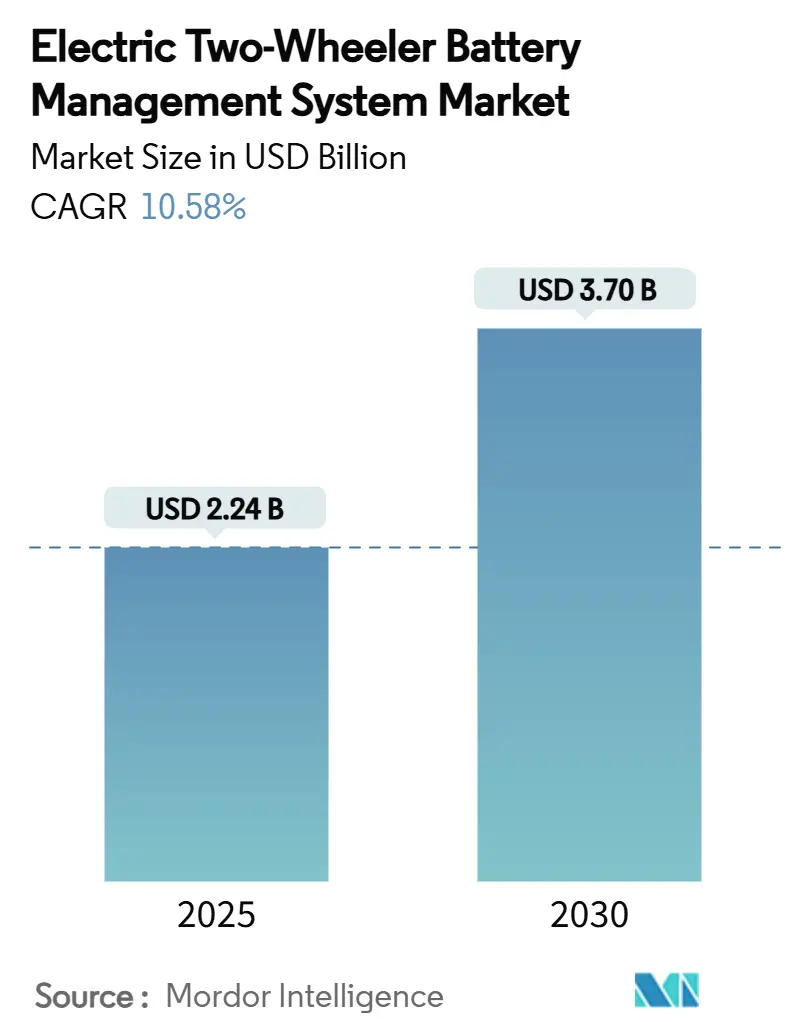

The Electric Two-Wheeler Battery Management System market size stands at USD 2.24 billion in 2025 and is projected to reach USD 3.70 billion by 2030, translating into a 10.58% CAGR over the forecast period. A confluence of declining lithium-ion cell prices, tougher safety regulations, and fiscal incentives is accelerating adoption, turning sophisticated BMS electronics from optional extras into mandatory fitments for almost every new electric scooter, moped, e-motorcycle, and e-bicycle. Technology convergence around wireless connectivity, predictive analytics, and cloud-based diagnostics is widening the functional scope of BMS units, while powertrain voltage is steadily moving beyond the traditional 48 V plateau to satisfy fast-charging and performance expectations. Competitive pressure is rising as cell makers such as CATL and Samsung SDI bundle in-house BMS with their packs, forcing independent suppliers to differentiate through software, AI, and over-the-air upgrade capabilities. At the same time, government-backed rebate schemes in Asia-Pacific and digital-battery-passport rules in Europe are reshaping cost curves, compliance workloads, and channel strategies.

Key Report Takeaways

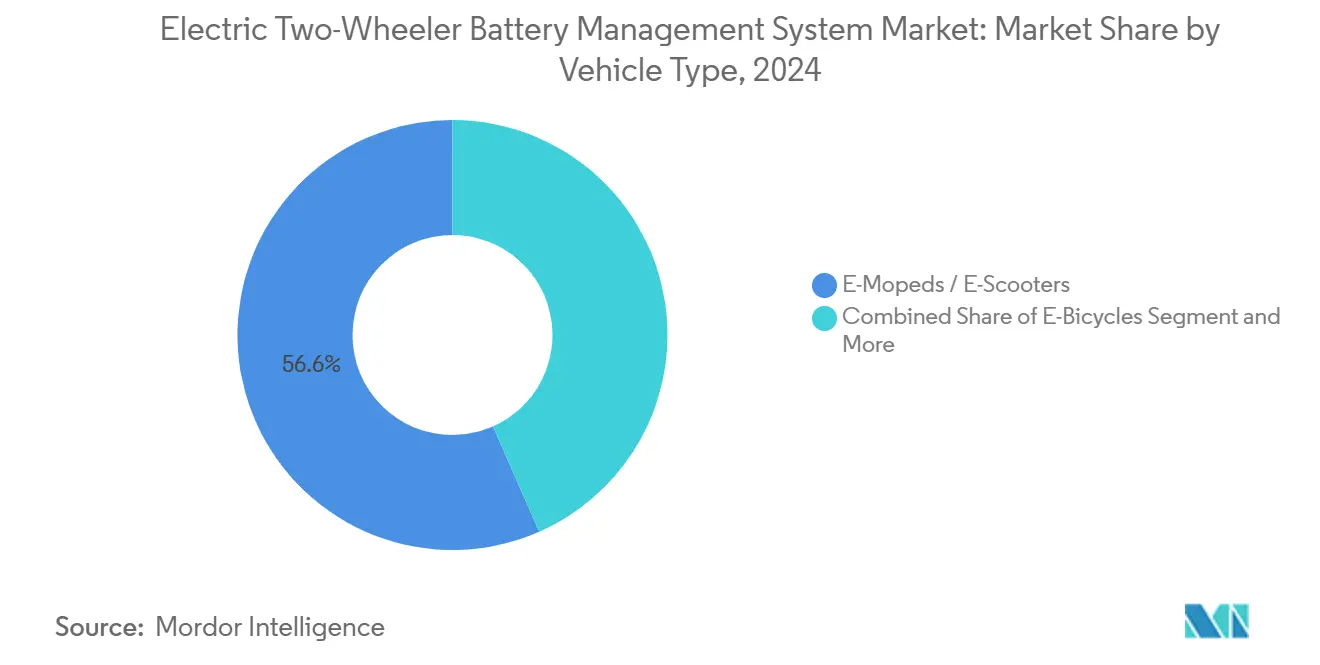

- By vehicle category, e-mopeds and e-scooters led with 56.62% revenue share in 2024; e-motorcycles are forecast to expand at a 19.26% CAGR through 2030.

- By battery chemistry, NMC/NCM commanded 62.39% of the Electric Two-Wheeler Battery Management System market share in 2024, while solid-state batteries are projected to grow at a 17.89% CAGR to 2030.

- By pack voltage, 48 V architectures held 44.19% share of the Electric Two-Wheeler Battery Management System market size in 2024; systems above 96 V are advancing at an 18.27% CAGR over the same period.

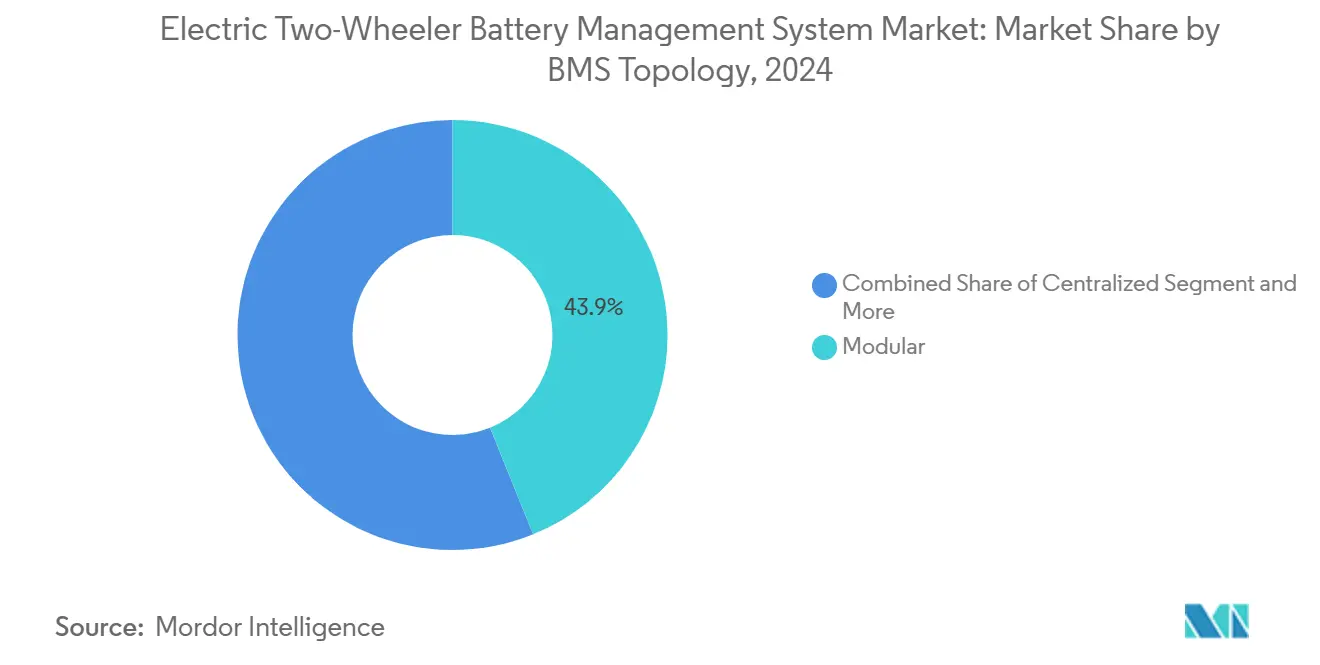

- By BMS topology, modular solutions accounted for 43.87% share in 2024, whereas distributed architectures post the highest forecast CAGR of 17.63% to 2030.

- By cooling method, air-cooled passive packs secured 67.28% share in 2024; liquid-cooled designs are poised for a 16.29% CAGR through 2030.

- By sales channel, factory-fitted units dominated with 81.29% share in 2024, yet Battery-as-a-Service systems are registering an 18.72% CAGR to 2030.

- By end-use pattern, personal ownership represented 74.38% of 2024 demand; commercial delivery fleets are tracking a 16.35% CAGR during the forecast period.

- By geography, Asia-Pacific captured 76.65% of 2024 global revenue and remains the fastest-growing region at a 14.48% CAGR.

Global Electric Two-Wheeler Battery Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium-ion Shift in Two-Wheelers | +2.8% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) |

| Incentive-led Safety Mandates | +2.1% | India, China, EU core markets | Short term (≤ 2 years) |

| Cheaper Low-Voltage BMS ICs | +1.9% | Global manufacturing hubs | Medium term (2-4 years) |

| AI Digital-Twin SoH/SOC Boost | +1.5% | North America, Europe, premium Asia-Pacific markets | Long term (≥ 4 years) |

| Wireless/Cloud BMS for Fleets | +1.4% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Analytics-Centric Swap Stations | +1.2% | Asia-Pacific core, spill-over to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Lithium-Ion Batteries in Electric Two-Wheelers

Substituting lead-acid packs with higher-density lithium-ion modules multiplies the complexity, functionality, and bill-of-materials value of every Electric Two-Wheeler Battery Management System market installation. National rules such as China’s GB 17761-2024 require unique coding and advanced monitoring, forcing smaller OEMs to upgrade or exit. Higher-energy NMC cells heighten thermal-runaway risk, so cell balancing, impedance tracking, and rapid fault isolation have become indispensable. Data generated by these smarter controllers underpins predictive maintenance contracts and mobility subscription models that create recurring revenue beyond hardware.

Government Incentives and Evolving Battery-Safety Standards

Purchase rebates, tax breaks, and targeted subventions—such as India’s Electric Mobility Promotion Scheme 2024—directly subsidize two-wheeler electrification and indirectly subsidize premium BMS electronics. Parallel safety mandates, including the EU Battery Regulation 2023/1542’s digital-passport clause, oblige BMS units to log real-time performance and cycle history accessible through QR codes[1]“Regulation (EU) 2023/1542 on Batteries,”, European Parliament & Council, europarl.europa.eu. Compliance-ready suppliers gain speed-to-market advantages, whereas laggards must absorb extra testing, certification, and redesign costs.

Falling Prices of Low-Voltage BMS ICs and Reference Designs

Component suppliers have bundled multi-channel voltage sensing, current shunts, and built-in coulomb counting into single ASICs, slashing cost and board area for 36 V – 60 V packs. Readily available reference designs compress engineering lead times, enabling smaller OEMs to integrate features such as passive balancing, cell undervoltage lockout, and ISO 26262-ready diagnostics without incurring heavy R&D budgets. Consequently, differentiation pivots from basic safety functions to software extensibility, connectivity, and cloud analytics.

AI-Driven Predictive Analytics and Digital-Twin BMS

Advances in on-board processing and edge-to-cloud architectures enable BMS algorithms to forecast state-of-health, remaining useful life, and thermal hotspots under dynamic load profiles. Fleet operators gain the ability to schedule maintenance precisely, extend pack life, and optimize energy costs. Over-the-air firmware updates further lengthen product lifecycles and lower warranty risk, strengthening customer lock-in for data-centric suppliers

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Costly Functional-Safety Compliance | -1.8% | Global, with stricter enforcement in EU and India | Short term (≤ 2 years) |

| Thermal-Runaway Scrutiny | -1.3% | China, India core markets with global implications | Medium term (2-4 years) |

| Fragmented, Non-interoperable Supply Base | -1.1% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Proprietary Algorithm Lock-ins | -0.9% | North America, Europe, premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Functional-Safety Certification Costs (ISO 26262, AIS-156)

From design FMEA through hardware-in-the-loop stress testing, full compliance can cost more than a new BMS platform. Large Tier-1s absorb the workload with in-house labs; start-ups must outsource, which increases cash burn and delays launches. As rules tighten and market entry points narrow, consolidation around incumbents with existing certificates is promoted.

Thermal-Runaway Incidents Triggering Regulatory Scrutiny

A spate of battery fires in major Asian cities has pushed authorities to demand two-hour thermal-soak resilience and early-warning diagnostics. Meeting those thresholds necessitates extra sensors, higher-bandwidth controllers, and sometimes a shift to liquid cooling—raising unit cost and design complexity. Insurers also raise premiums for non-certified packs, indirectly discouraging low-spec BMS adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle – Consumer Scooters Dominate as Performance Motorcycles Accelerate

E-mopeds and e-scooters accounted for 56.62% of 2024 installations, underscoring their role as the everyday urban workhorses for the Electric Two-Wheeler Battery Management System market. Their popularity stems from lower upfront pricing, subsidy alignment, and the suitability of 48 V packs containing power-electronics costs. High unit volumes translate into scale advantages for BMS suppliers that can standardise designs across multiple scooter models.

The momentum, however, is shifting toward e-motorcycles, which are projected to log a 19.26% CAGR between 2025 and 2030—the fastest of all vehicle categories. These premium machines demand higher-voltage architectures, faster CAN bus sampling, and more sophisticated thermal management, lifting BMS value per unit. Brands that master quick-charge compatibility and OTA performance tuning stand to capture the segment’s margin upside.

By Battery Chemistry – Nickel-Cobalt Rules, Solid-State Emerges

Nickel-cobalt chemistries dominated 2024 with a 62.39% share, benefiting from mature supply chains, high specific energy, and robust OEM design experience. The chemistry’s thermal sensitivity, though, drives stringent cell-balancing and fault-isolation requirements, ensuring stable demand for advanced BMS feature sets.

Solid-state cells are the headline growth story, forecast to expand at a 17.89% CAGR through 2030. Their intrinsically safer solid electrolyte reduces fire risk, yet also necessitates fresh impedance-tracking algorithms and mechanical pressure monitoring inside the BMS. Early-moving suppliers that launch chemistry-agnostic firmware will be best positioned as pilot lines scale to mass production.

By Pack Voltage – 48 V Remains the Workhorse, above 96 V Surges

Traditional 48 V packs retained 44.19% share in 2024, balancing cost, safety certification effort, and compatibility with widely available 2 kW–4 kW motors. Their ubiquity encourages BMS hardware reuse across price tiers and simplifies aftermarket servicing.

Packs above 96 V are the fastest climbers, advancing at an 18.27% CAGR. Higher voltage slashes charge times and enables highway-legal acceleration, but it also multiplies series cell counts, sparking demand for distributed sensing boards and reinforced isolation. BMS platforms that can scale seamlessly from 72 V to 120 V will capture future-ready OEM design slots.

By BMS Technology – Modular Leads, Distributed Gains Ground

Modular systems commanded 43.87% of 2024 shipments by delivering a pragmatic balance between cost and scalability; stackable slave boards let OEMs cover multiple pack sizes without a ground-up redesign. The approach also eases serviceability because failed modules can be swapped in minutes.

Distributed architectures are growing quickest at 17.63% CAGR thanks to their precision measurement and wiring-harness weight savings—key advantages in high-cell-count, high-voltage packs. Embedding A/D converters at the cell board level improves noise immunity, while daisy-chain communication simplifies future feature additions such as wireless telemetry.

By Cooling & Packaging – Passive Air Dominates, Liquid Cooling Accelerates

Air-cooled passive designs held a commanding 67.28% share in 2024, favored for their simplicity, low BOM, and ease of integration into under-seat battery bays. Most urban scooters running sub-4 kW motors can keep cell temperatures within safe limits using only finned housings and airflow from vehicle motion.

Liquid-cooled systems, however, are set to rise at a brisk 16.29% CAGR as power outputs, fast-charge currents, and continuous-duty fleet cycles intensify thermal load. Integrated pumps and cold plates allow packs to stay below critical 45 °C thresholds even under 5C charge rates, pushing BMS suppliers to incorporate coolant-flow monitoring and leak diagnostics.

By Sales Channel – Factory-Fitted Prevails, Battery-as-a-Service Takes Off

OEM-integrated, factory-fitted BMS units made up 81.29% of 2024 volume. Tight packaging, homologation efficiency, and VIN-level traceability make in-house integration the default choice for most brands.

Battery-as-a-Service solutions represent the breakout channel, expected to register an 18.72% CAGR through 2030. Swappable packs necessitate instant state-of-health verification, unique ID encryption, and kiosk-to-cloud synchronisation—drive-up requirements that position software-centric BMS vendors for recurring subscription revenues.

By End-Use Pattern – Personal Riders Lead, Commercial Fleets Propel Growth

Personal ownership remained the largest usage mode at 74.38% in 2024, anchored by the consumer scooter boom in Asia’s megacities and rising recreational e-bike adoption in Europe. The segment values intuitive state-of-charge displays and theft-deterrent features in its BMS wish-list.

Commercial delivery fleets are the fastest-expanding cohort, clocking a 16.35% CAGR to 2030. Their duty cycles expose packs to deep daily discharge and aggressive charging, elevating the importance of predictive maintenance, cycle-life analytics, and warranty-backed uptime guarantees. Fleet contracts therefore skew toward BMS suppliers offering cloud dashboards, API integration, and remote firmware updates.

Geography Analysis

Asia-Pacific retains an overwhelming scale, accounting for 76.65% of 2024 revenue and advancing at a 14.48% CAGR amid supportive subsidies, dense supplier bases, and high urban two-wheeler dependence. National standards such as China’s GB 17761-2024 make advanced BMS a prerequisite for market entry, effectively lifting the average selling price[2]“GB 17761-2024 Electric Bicycle Safety Specification,”, National Standardisation Administration of China, sac.gov.cn. ASEAN markets are layering purchase rebates and local-content rules, encouraging domestic pack makers to co-develop BMS locally, although supply chains remain vulnerable to trade friction.

Europe positions itself as the premium compliance hub. The digital-battery-passport obligation from 2027 propels demand for data-rich BMS able to secure chain-of-custody proofs and real-time durability metrics. Fleet electrification in courier and micromobility services adds volume, while stringent functional-safety norms restrict low-spec imports.

North America shows moderate adoption; state incentives and corporate fleet mandates sustain steady growth, but domestic cell production lags. OEMs therefore negotiate long-term agreements with Asian suppliers, raising exposure to geopolitical risk. South America and Middle East & Africa remain emerging prospects: limited charging infrastructure curtails volumes today, yet localised assembly coupled with low-cost LFP chemistries could unlock upside mid-term.

Competitive Landscape

Competition blends battery giants, automotive electronics specialists, and nimble software start-ups. CATL leverages its EV cell share to attach proprietary BMS[3]“Annual Report 2024,”, CATL, catl.com, bundling pack warranties, and lifecycle analytics to lock in OEMs. Bosch eBike Systems exploits its ISO 26262 pedigree to capture premium e-bicycle niches through update-enabled features such as AI-based range estimation. Samsung SDI, LG Energy Solution, and BYD pursue vertical integration, co-designing cell chemistries, modules, and controllers to shave cost and accelerate time-to-market.

Meanwhile, predictive-software vendors like Eatron secure strategic investments from incumbent vehicle makers seeking AI capability. Wireless-mesh innovators adapt ultra-reliable protocols to cut harness weight and simplify module packaging. Patent filings centred on cloud-connected diagnostics, adaptive charging, and digital-twin modelling signal a shift of competitive battleground from hardware BOM to algorithm IP.

Supplier relationships increasingly hinge on compliance readiness: those offering pre-certified designs for ISO 26262 and EU battery passports gain fast-track approvals. Barriers to entry rise for newcomers lacking the capital to fund certification, pushing the industry toward moderate concentration even as niche disrupters carve out IP-rich territories.

Electric Two-Wheeler Battery Management System Industry Leaders

Bosch eBike Systems

Shimano (STEPS)

Bafang Electric

Yamaha Motor

LG Energy Solution

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: India's Ministry of Power released comprehensive guidelines for battery swapping and charging stations, mandating smart BMS with IoT capabilities for remote monitoring and promoting Battery-as-a-Service models. The guidelines allow operators to use existing electricity connections and deploy liquid-cooled swappable batteries for larger vehicles, creating new infrastructure opportunities for BMS providers.

- January 2025: Bosch eBike Systems introduced digital theft protection for eBike batteries at CES 2025, enabling users to digitally deactivate batteries via smartphone or display. The company also launched Range Control AI-powered route planning and Eco+ mode optimization features through the eBike Flow app, demonstrating the evolution toward software-defined BMS capabilities.

- April 2024: CATL and Beijing Hyundai signed a strategic agreement to enhance Hyundai's electric vehicle lineup with advanced CATL batteries, planning to launch over 10 new global models featuring innovative battery technologies including CTP (Cell to Pack) and NP (Nickel Manganese Cobalt-free) systems.

Global Electric Two-Wheeler Battery Management System Market Report Scope

Electric Two-Wheeler Battery Management System Report is Segmented by Vehicle (E-Bicycles and More), Battery Chemistry (Lithium-Iron-Phosphate and More), Pack Voltage (Below 36V and More), BMS Topology (Centralized and More), Cooling & Packaging (Liquid-Cooled and More), Sales Channel (Factory-Fitted and More), End-Use (Personal Ownership and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| E-Bicycles |

| E-Mopeds / E-Scooters |

| E-Motorcycles |

| Lithium-Iron-Phosphate (LFP) |

| Nickel-Manganese-Cobalt (NMC/NCM) |

| Others (LCO, LTO, etc.) |

| Below 36 V |

| 48 V |

| 60 V |

| 72 V |

| Above 96 V |

| Centralized |

| Distributed |

| Modular |

| Liquid-Cooled |

| Air-Cooled Passive |

| Forced-Air Active |

| Factory-Fitted (OEM integrated) |

| Aftermarket Retrofit / Replacement |

| Battery-as-a-Service / Swap-Station Packs |

| Personal Ownership |

| Shared Mobility Fleets |

| Commercial Delivery Fleets |

| Institutional / Governmental Fleets |

| North America | United States | ||

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Corporation Council | Saudi Arabia |

| United Arab Emirates | |||

| Rest of Gulf Corporation Council | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

| By Vehicle | E-Bicycles | |||

| E-Mopeds / E-Scooters | ||||

| E-Motorcycles | ||||

| By Battery Chemistry | Lithium-Iron-Phosphate (LFP) | |||

| Nickel-Manganese-Cobalt (NMC/NCM) | ||||

| Others (LCO, LTO, etc.) | ||||

| By Pack Voltage | Below 36 V | |||

| 48 V | ||||

| 60 V | ||||

| 72 V | ||||

| Above 96 V | ||||

| By BMS Topology | Centralized | |||

| Distributed | ||||

| Modular | ||||

| By Cooling & Packaging | Liquid-Cooled | |||

| Air-Cooled Passive | ||||

| Forced-Air Active | ||||

| By Sales Channel | Factory-Fitted (OEM integrated) | |||

| Aftermarket Retrofit / Replacement | ||||

| Battery-as-a-Service / Swap-Station Packs | ||||

| By End-Use Pattern | Personal Ownership | |||

| Shared Mobility Fleets | ||||

| Commercial Delivery Fleets | ||||

| Institutional / Governmental Fleets | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Rest of North America | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Gulf Corporation Council | Saudi Arabia | |

| United Arab Emirates | ||||

| Rest of Gulf Corporation Council | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Kenya | ||||

| Rest of Africa | ||||

Key Questions Answered in the Report

What is the forecast CAGR for global BMS demand in electric two-wheelers to 2030?

The market is expected to post a 10.58% CAGR, rising from USD 2.24 billion in 2025 to USD 3.70 billion in 2030.

Which vehicle class is growing fastest for BMS adoption?

E-motorcycles lead growth with a 19.26% CAGR thanks to higher-voltage powertrains and fast-charge requirements.

Why are distributed BMS topologies gaining traction?

They scale efficiently to high cell counts, improve measurement accuracy, and simplify maintenance for fleet operators.

How will EU battery passports influence BMS design?

Controllers must log and transmit real-time performance, traceability, and durability data to comply with Regulation 2023/1542.

What cooling method is emerging for high-power two-wheelers?

Liquid cooling is expanding at a 16.29% CAGR because it keeps pack temperatures below 45 °C during rapid charging.

Page last updated on: