Market Overview

| Study Period | 2020 - 2031 |

|---|---|

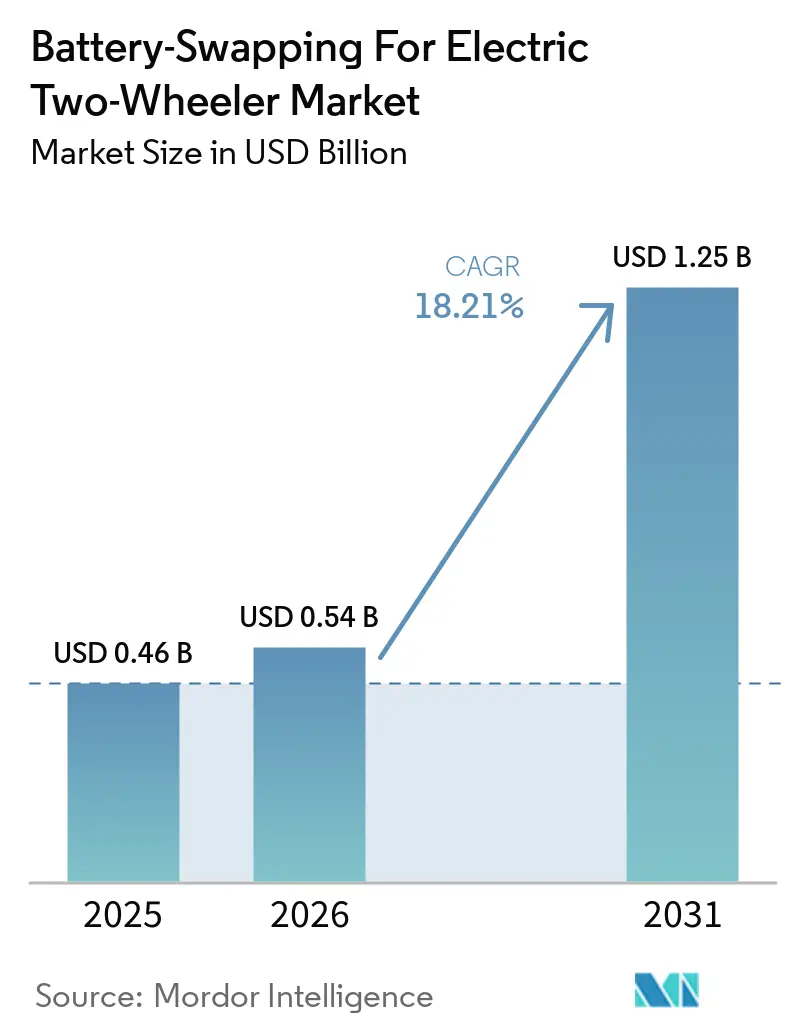

| Market Size (2026) | USD 0.54 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Growth Rate (2026 - 2031) | 18.21% CAGR |

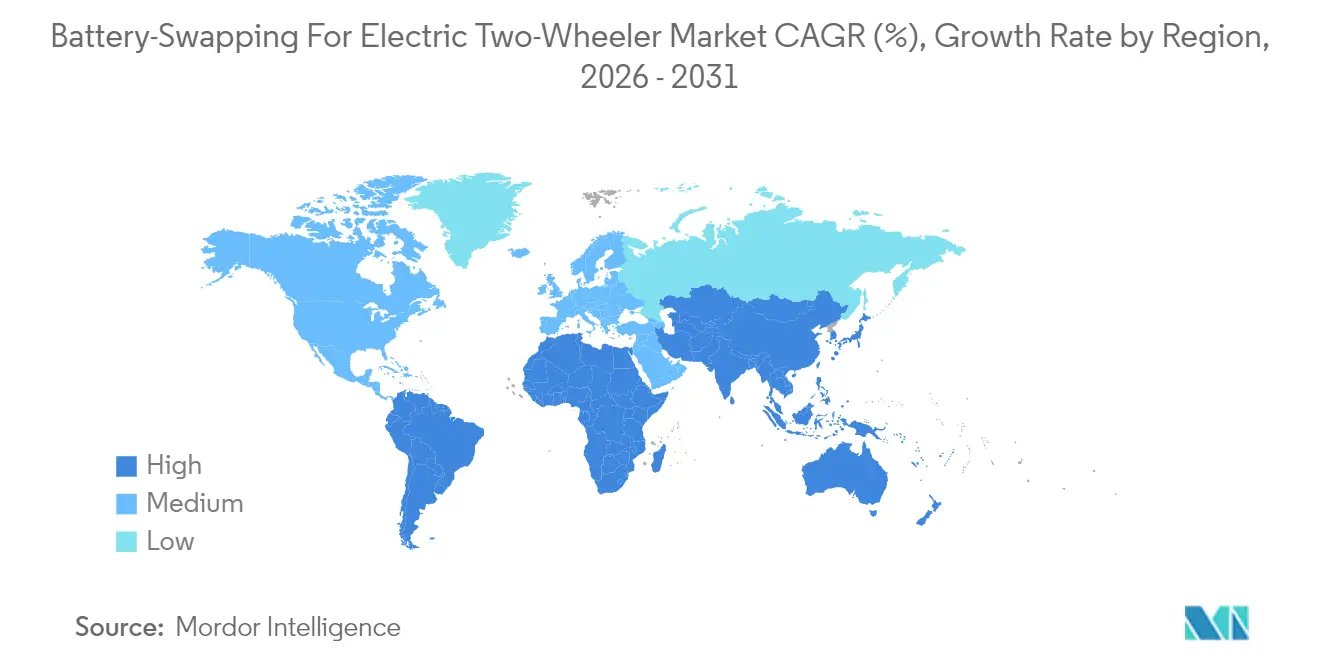

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

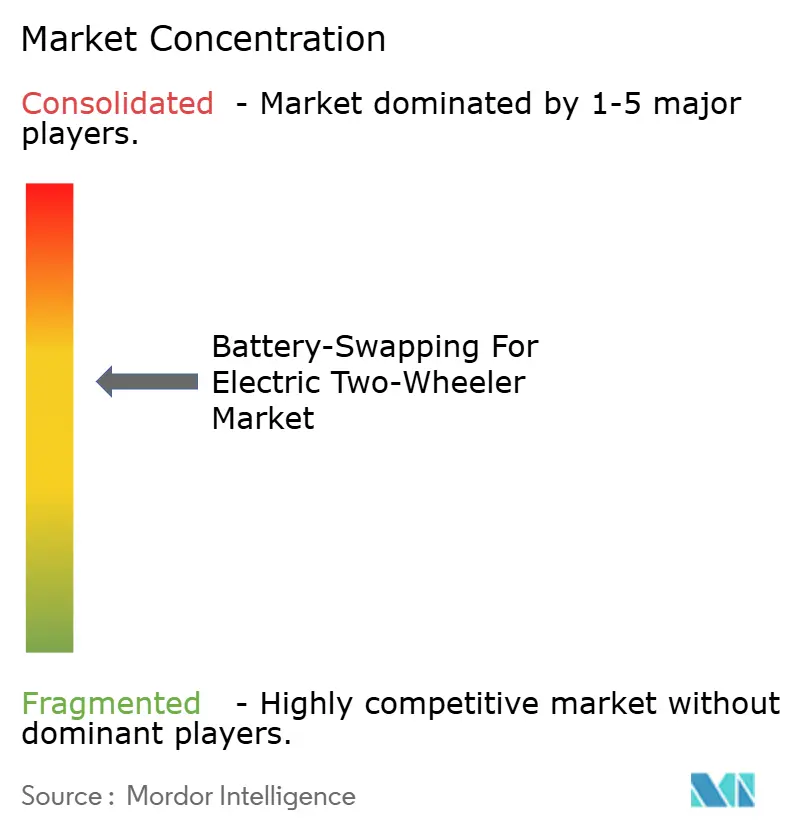

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery-Swapping For Electric Two-Wheeler Market Analysis by Mordor Intelligence

The Battery-Swapping For Electric Two-Wheeler Market size was valued at USD 0.46 billion in 2025 and estimated to grow from USD 0.54 billion in 2026 to reach USD 1.25 billion by 2031, at a CAGR of 18.21% during the forecast period (2026-2031). Reflecting a decisive shift toward service-based battery ownership models that eliminate range anxiety and charging downtime for riders. Demand is accelerating because operators absorb the capital burden of battery inventories while users secure operational flexibility through subscription access. Urban land constraints, government decarbonization mandates, and falling lithium-ion costs converge to reinforce investor confidence in this infrastructure-heavy solution. Competitive intensity is moderate as ecosystem players race to secure first-mover station density. However, proven large-scale deployments in Taiwan and China provide road-tested blueprints for replication in growth regions. Therefore, the battery swapping for the electric two-wheeler market offers multi-vector revenue streams that span subscription fees, second-life grid services, and data-driven fleet optimization.

Key Report Takeaways

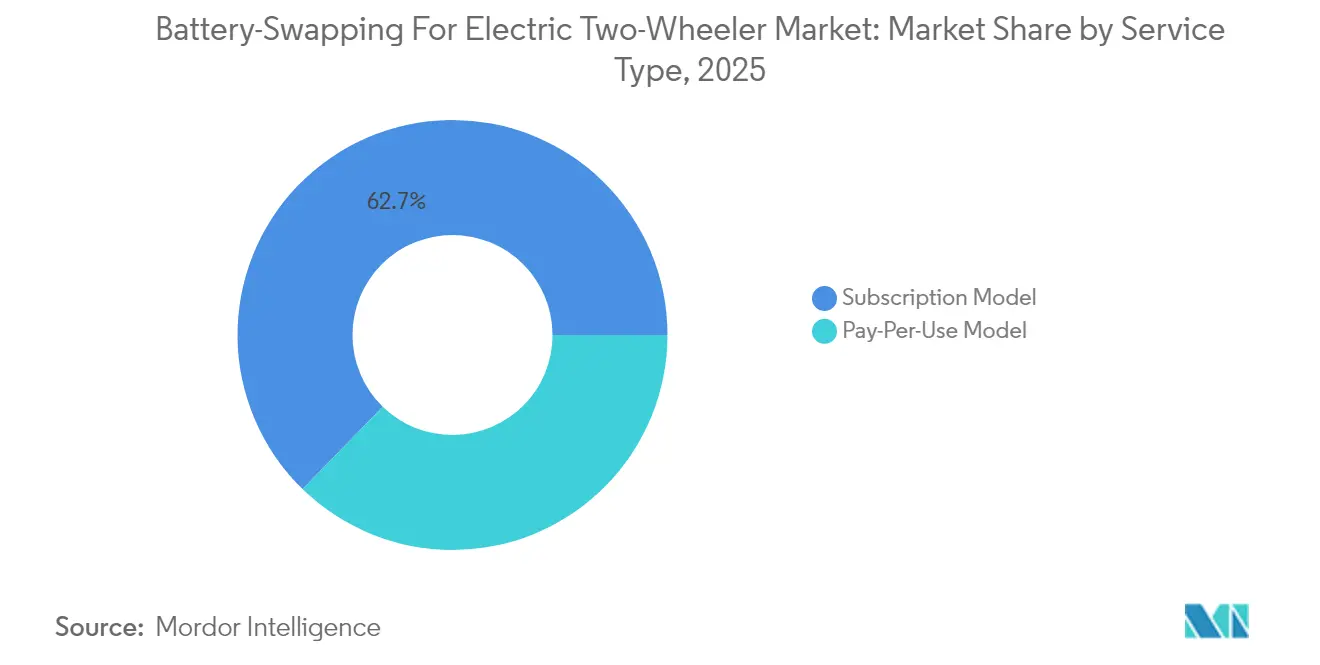

- By service type, subscription plans held 62.72% of the battery swapping for electric two-wheeler market share in 2025, while pay-per-use options are advancing at an 18.62% CAGR through 2031.

- By battery chemistry, lithium-ion packs captured 73.85% of the battery swapping for electric two-wheeler market share in 2025 and are expanding at an 18.55% CAGR to 2031.

- By station design, manual kiosks led with 50.62% of the battery swapping for electric two-wheeler market share in 2025, whereas automated systems are projected to post the highest 18.49% CAGR to 2031.

- By capacity, 1.6–3 kWh modules commanded 45.05% of the battery swapping for electric two-wheeler market share in 2025, and larger-than-3 kWh batteries will see an 18.30% CAGR over the forecast period.

- By two-wheeler type, e-scooters and mopeds accounted for a 66.84% of the battery swapping for electric two-wheeler market share in 2025, and e-motorcycles represent the fastest-growing sub-segment at an 18.44% CAGR.

- By application, commercial fleets held a 58.22% of the battery swapping for electric two-wheeler market share in 2025, while personal mobility use cases exhibit an 18.57% CAGR to 2031.

- By end user, fleet operators captured 48.21% of the battery swapping for electric two-wheeler market share in 2025, and delivery aggregators show the strongest 18.69% CAGR outlook.

- By region, Asia-Pacific dominated with a 45.02% of the battery swapping for electric two-wheeler market share in 2025, and South America is poised for an 18.32% CAGR expansion to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Battery-Swapping For Electric Two-Wheeler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive Decarbonization Mandates | +4.2% | Global, with early gains in China, India, Singapore | Short term (≤ 2 years) |

| Growth Of Delivery Fleets | +3.8% | Asia Pacific core, spill-over to MEA and South America | Medium term (2-4 years) |

| Declining Li-Ion Battery Costs | +3.1% | Global | Long term (≥ 4 years) |

| Proven Large-Scale Swap Ecosystems | +2.9% | Asia Pacific core, with expansion to Europe and North America | Medium term (2-4 years) |

| Urban Land Constraints | +2.4% | Global urban centers, particularly Asia-Pacific | Short term (≤ 2 years) |

| Second-Life & Grid-Service Revenue Streams | +1.8% | Europe and North America, expanding to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive Decarbonization Mandates & Subsidies

Policy momentum is accelerating because governments view battery swapping as a low-grid-impact catalyst for two-wheeler electrification. Singapore introduced the world’s first dedicated technical code for swappable batteries in March 2024, offering a clear interoperability playbook for operators [1]“Swappable Batteries Technical Standard,” lta.gov.sg . China reimburses up to one-third of station capex through provincial funds, fast-tracking installations in tier-2 cities. India’s Electric Mobility Promotion Scheme is earmarked for lithium-ion two- and three-wheelers, with battery swapping models receiving priority incentives [2]“Electric Mobility Promotion Scheme 2024,” heavyindustries.gov.in. Global standard bodies are also active; IEC 63584 and ISO 15118-20 now define authentication and data-exchange layers that unlock cross-brand compatibility. Collectively, these measures reduce investor risk and underpin forecast growth in the battery swapping for the electric two-wheeler market.

Growth of Delivery & Gig-Economy Fleets

High-utilization commercial fleets consider downtime non-negotiable, making battery swapping indispensable for business continuity. Delivery aggregators such as Zomato and Swiggy have embedded swapping into their urban logistics workflows, and Battery Smart now records over 100,000 daily swaps across India, mostly from organized fleets. Municipal agencies echo this trend; Dubai’s Roads and Transport Authority green-lit 36 dedicated swapping sites targeting food-delivery riders. Predictable usage patterns allow operators to optimize battery float levels, elevate station utilization, and secure long-term subscription revenue streams. Consequently, the battery swapping for the electric two-wheeler market is becoming a critical backbone for last-mile commerce.

Declining Li-Ion Battery Costs

Global lithium-ion pack costs fell significantly year on year in 2024, enabling central battery ownership at the station level without eroding profit margins [3]“Cost Trajectory of Lithium-Ion Batteries,” Li et al., nature.com . Energy density gains now surpass 230 Wh/kg, extending scooter range while allowing lighter modules suited to manual handling. Peer-reviewed studies indicate total cost of ownership savings are fair versus private battery ownership because professional charging regimes and depth-of-discharge controls prolong usable life. The trajectory secures lithium-ion's long-run competitiveness and cements its dominance in the battery swapping for the electric two-wheeler market.

Proven Large-Scale Swap Ecosystems

In Taiwan and mainland China, operational proof points have mitigated risks for both investors and regulators. By late 2024, Gogoro achieved significant milestones in cumulative swaps across its extensive network of stations, showcasing high daily throughput per station. Around the same period, NIO reached a major milestone in swaps on its car-centric network, while also demonstrating the adaptability of robotics for two-wheeler applications. These achievements highlight the potential for favorable payback periods with dense deployments and provide data-driven benchmarks for forthcoming projects in India and Indonesia. Consequently, there's a growing interest in replication, solidifying the growth trajectory for battery swapping in the electric two-wheeler sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Station Capex | -2.8% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Interoperability and IP Push-Back From OEMs | -2.1% | Global, with regional variations in standardization | Medium term (2-4 years) |

| Tax Disincentives On Standalone Batteries | -1.5% | Europe and North America, with emerging policy gaps in Asia Pacific | Medium term (2-4 years) |

| Advances In Ultra-Fast Charging | -1.2% | Global, with faster adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Station Capex & Battery Inventory

Operators typically stock several spare battery packs per active vehicle, ensuring availability. Robotic kiosks, priced within a high range (excluding batteries), represent a significant investment. Spiro, having already invested a substantial amount to roll out a large number of bikes and stations across Africa, is eyeing additional funding for the next phase. This capital intensity in deploying networks, especially in markets with limited capital, not only favors established players but also curtails immediate expansion in the battery swapping sector for electric two-wheelers.

Interoperability & IP Push-Back From OEMs

Vehicle makers protect proprietary battery formats, locking riders into single-brand ecosystems and forcing operators to carry multiple SKU inventories. The resulting complexity erodes asset utilization and inflates working capital. Ongoing IEC and ISO standardization efforts face OEM resistance, slowing universal connector adoption and prolonging consumer confusion. Until regulatory mandates or market forces resolve compatibility gaps, this fragmentation will temper growth momentum in the battery swapping for the electric two-wheeler market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Subscriptions Anchor Early-Stage Scale

Subscription contracts commanded 62.72% of the battery swapping for electric two-wheeler market share in 2025, signaling market preference for predictable per-month mobility costs and guaranteed swap access. This leadership translates into stable cash flow financing and accelerated kiosk roll-outs within the battery swapping for electric two-wheeler market. Complementary fleet dashboards allow operators to reallocate batteries dynamically, lifting utilization rates beyond four-fifths. Pay-per-use options record an 18.62% CAGR to 2031 as casual riders value flexibility over commitment, especially in nascent swap geographies. The subscription share is expected to decline slowly yet remain the core monetization pillar because large-scale fleets gravitate toward all-inclusive packages that simplify expense reporting.

Network density fuels a virtuous cycle: more subscribers justify new stations that bring down average trip detour distance, attracting additional users. Differential pricing structures reward high-volume accounts and bulk fleet sign-ups, cementing professional delivery firms as anchor tenants across urban nodes. Policy makers such as India’s Ministry of Heavy Industries channel incentives toward subscription-backed deployments because they generate reliable utilization data for safety oversight. Consequently, the subscription archetype will remain vital to long-term profitability within the battery swapping for electric two-wheeler market.

By Battery Type: Lithium-Ion Solidifies Supremacy

Lithium-ion platforms owned 73.85% of the battery swapping for electric two-wheeler market share in 2025. Also, they registered a robust CAGR of 18.55% till 2031, underpinning the battery swapping for the electric two-wheeler market share advantage through superior 1,000-cycle durability and energy density above 200 Wh/kg. Regulatory updates in China prohibit sub-par lead-acid packs for urban fleets, accelerating the technology shift. The battery swapping for the electric two-wheeler market size for lithium-ion formats is projected to grow exponentially at a robust CAGR. Sodium-ion prototypes attract R&D budgets because they use inexpensive raw materials, yet commercialization remains post-2030.

Additionally, built-in battery management systems comply with IEC 63584 authentication rules, a non-negotiable requirement for automated swap bays. Lead-acid still survives in rural delivery markets owing to low sticker price, but will cede share as recycled lithium capacities expand and subsidy regimes penalize low-energy-density chemistries.

By Station Type: Automation Gains as Labor Costs Climb

Manual kiosks held 50.62% of the battery swapping for electric two-wheeler market share in 2025 because they demand around one-third lower upfront spend versus robotic alternatives, making them suitable for emerging markets. However, automated stations show an 18.49% CAGR to 2031, outpacing manual formats within the battery swapping for electric two-wheeler market as labor rates rise in China, Singapore, and the Gulf. Robotic arms deliver sub-30-second swap cycles and eliminate ergonomic safety risks, satisfying stricter labor codes in Europe and North America.

Capex is falling: tier-one suppliers now offer modular systems priced below USD 65,000 per bay, narrowing the gap with manual booths. Automation also unlocks 24×7 unattended operations, which increases daily transaction counts and shortens payback periods. As cities tighten occupational safety regulations, insurers are beginning to discount premiums for robotic infrastructure, providing yet another tailwind to automated adoption.

By Battery Capacity: Mid-Range Packs Strike Optimal Balance

Modules sized 1.6–3 kWh took 45.05% of the battery swapping for electric two-wheeler market share in 2025, a sweet spot that delivers 80–120 km of real-world range without imposing heavy lifting because packs weigh under 12 kg. Fleet data shows an average daily run-time of 92 km for delivery scooters, matching this capacity edge. The larger-than-3 kWh bracket is expanding at 18.30% CAGR and will cater to e-motorcycles and peri-urban couriers who demand 150 km between swaps. More miniature sub-1.5 kWh packs persist in hyper-price-sensitive markets but face obsolescence as lithium-ion prices shrink.

Thermal management upgrades allow mid-range modules to sustain rapid-charge cycles without degradation, which is critical for high-frequency swap environments. Operators standardize around a limited capacity menu to simplify logistics, enabling economies of scale in pack refurbishment. Battery analytics refine depth-of-discharge thresholds, extending usable life past 1,200 cycles and fortifying cost leadership for mid-tier capacities.

By Two-Wheeler Type: Scooters Dominate Yet Motorcycles Accelerate

Scooters and mopeds covered 66.84% of the battery swapping for electric two-wheeler market share in 2025 because their step-through frames accommodate standardized under-seat packs ideal for swapping. E-motorcycles, constrained by diverse frame geometries, nonetheless post an 18.44% CAGR fueled by performance improvements and OEM launches such as Honda’s Activa e with native swap capability. Sport motorcycles require 3 + kWh modules, urging station operators to expand capacity offerings and rethink cradle designs.

Shared-mobility providers experiment with modular seatpods that accept multiple parallel packs, allowing power scaling without altering vehicle dimensions. Anticipated ISO guidelines on swappable-battery anchoring systems will further unlock motorcycle inclusion by harmonizing latch-point positioning. As such, motorcycles will capture incremental share, but scooters will remain the backbone of the battery swapping for the electric two-wheeler market.

By Application: Commercial Fleets Command Revenue Pools

Commercial fleets generated 58.22% of the battery swapping for electric two-wheeler market share in 2025, underscoring their ability to monetize high daily distances per vehicle. Network planners prioritize depot-adjacent sites that consolidate swap volumes from couriers, ride-hailers, and grocery delivery riders. Personal mobility use cases are catching up via an 18.57% CAGR, boosted by city incentives and rising petrol costs. Long-form subscription bundles appeal to fleet CFOs by converting capex to opex, whereas app-based on-demand swaps resonate with individual riders seeking budget control.

Utilization analytics indicate fleet-focused kiosks achieve break-even in under 24 months, outperforming mixed-use locations by 8 months. Consequently, operators treat fleets as anchor tenants to de-risk rollout before ramping consumer penetration. This dual-track strategy supports the steady expansion of battery swapping for the electric two-wheeler market.

By End User: Organized Fleets Secure Early-Mover Benefits

Fleet operators owned 48.21% of the battery swapping for electric two-wheeler market share in 2025 and will maintain leadership as delivery demand climbs. Organized fleets negotiate bulk energy tariffs and consolidated maintenance, driving lower per-kilometer costs than petrol or plug-in alternatives. Disaggregated consumer riders gradually adopt the network once station density surpasses a convenience threshold of 500 meters average detour distance, which operators expect by 2027 in major APAC metros. Delivery aggregators post the highest 18.69% CAGR as e-commerce migrates to 10-minute quick-commerce models.

Municipal emission caps accelerate B2B electrification, channeling regulatory stickiness toward fleets that must prove zero-tailpipe compliance. Data-sharing memoranda between fleets and city planners support dynamic route zoning, elevating the strategic value of battery swapping for the electric two-wheeler market for urban policy.

Geography Analysis

Asia-Pacific held a 45.02% of the battery swapping for electric two-wheeler market share in 2025, driven by mature battery ecosystems in China, Taiwan, and India, alongside high two-wheeler density. In 2023, China dominated the electric two-wheeler market with significant sales volumes. Meanwhile, India experienced substantial growth, achieving a notable year-on-year increase. Established infrastructure templates in these nations are swiftly being adapted in Vietnam, Thailand, and Indonesia, solidifying their regional leadership.

South America shows the highest 18.32% CAGR owing to initiatives like Brazil’s e-delivery incentive program and Buenos Aires’ electric mobility roadmap that earmarks curbside swap zones. North America and Europe grow from smaller bases but leverage high labor costs to justify automated kiosks that bundle grid-service revenue. The Middle East and Africa trail, but pilot schemes in Dubai and Nairobi confirm the concept’s relevance, where grid access is limited. Collectively, regional dynamics reinforce the diversified nature of opportunity across the battery swapping for the electric two-wheeler market.

North America and Europe pursue niche adoption. Restaurant delivery platforms in New York City and Madrid use swapping to meet noise and emission ordinances. Higher real-estate costs drive kiosks to occupy underused indoor garages or curbside micro-hubs. Stringent worker safety codes push operators toward fully automated bays, aligning regionally with the premium segment of the battery swapping for electric two-wheeler market.

Competitive Landscape

Competition remains moderate in a landscape where ecosystems, not just individual products, set the stage for differentiation. Gogoro solidifies its leadership with an extensive network of stations across Asia and strategic cross-licensing agreements with industry giants like Yamaha, Aeon, and Hero MotoCorp. Meanwhile, CATL capitalizes on its cell-manufacturing scale, allowing it to offer competitive pricing on packs for its domestic partners. Battery Smart and Sun Mobility, adopting asset-light strategies, leverage franchise networks to establish a presence in India's smaller cities swiftly. The trend of strategic alliances is rising: Shell collaborates with Gogoro to co-brand energy pods, and TotalEnergies backs roll-outs in Brazil with financial support.

As ISO authentication protocols level the playing field, the once formidable technology moats are diminishing. Today's competition hinges on user experience, app integration, and swap-time guarantees rather than solely on proprietary hardware. Robotics leaders like ABB and Kuka are enhancing service quality in automated networks by integrating AI-driven fault detection and boosting uptime. In the battery swapping arena for electric two-wheelers, venture capital is increasingly drawn to operators harnessing data analytics to optimize battery health, creating a beneficial cycle of cost efficiency and reliable service.

While capital expenditure and regulatory compliance pose challenges for market entry, software-driven models that lease batteries and delegate station ownership find it easier to navigate. Regional players, bolstered by strong ties to policy-makers, safeguard their territory by advocating for local content regulations. However, the tide of global standardization threatens to unsettle these established defenses. In this evolving landscape, it's clear that adept execution and access to capital hold more weight than mere technological prowess in determining the long-term victors.

Battery-Swapping For Electric Two-Wheeler Industry Leaders

Gogoro Inc.

Immotor Technology

Oyika Pte. Ltd.

Kwang Yang Motor Co., Ltd.

Sun Mobility

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Honda launched the Activa e electric scooter in India with integrated battery-swapping compatibility, marking the first mainstream OEM to embed the feature at mass scale.

- July 2024: Gogoro expanded its Singapore operations to 22 stations with a USD 4 million investment and disclosed a plan to reach 400 sites within two years.

- June 2024: Battery Smart raised USD 65 million in Series B funding to expand its network to 25 Indian cities.

Global Battery-Swapping For Electric Two-Wheeler Market Report Scope

Battery swapping for electric two-wheelers is a technology that allows the replacement of a discharged battery pack with a fully charged pack without the need to wait, as in the case of charging stations. The process of battery swapping is comparatively advantageous for consumers since it is less time-consuming and also attracts a lower price compared to replacing a battery.

The battery-swapping for electric two-wheelers market is segmented by service type, battery type, station type, battery capacity, two-wheeler type, and geography. By service type, the market is segmented into pay-per-use model and subscription model. By battery type, the market is segmented into lithium-ion batteries and lead-acid batteries. By station type, the market is segmented into manual and automated. By battery capacity, the market is segmented into up to 1.5 kWh, 1.6 to 3 kWh, and more than 3 kWh. By two-wheeler type, the market is segmented into e-scooters/mopeds and e-motorcycles. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

The report offers market sizes and forecasts for battery swapping in value (USD) for all the above segments.

By Service Type

| Pay-Per-Use Model |

| Subscription Model |

By Battery Type

| Lithium-ion Battery |

| Lead-acid Battery |

By Station Type

| Manual |

| Automated |

By Battery Capacity

| Up to 1.5 kWh |

| 1.6 – 3 kWh |

| More than 3 kWh |

By Two-Wheeler Type

| E-Scooters / Mopeds |

| E-Motorcycles |

By Application

| Personal Mobility |

| Commercial Fleets |

By End User

| Individual consumers |

| Fleet operators |

| Delivery aggregators |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Service Type | Pay-Per-Use Model | |

| Subscription Model | ||

| By Battery Type | Lithium-ion Battery | |

| Lead-acid Battery | ||

| By Station Type | Manual | |

| Automated | ||

| By Battery Capacity | Up to 1.5 kWh | |

| 1.6 – 3 kWh | ||

| More than 3 kWh | ||

| By Two-Wheeler Type | E-Scooters / Mopeds | |

| E-Motorcycles | ||

| By Application | Personal Mobility | |

| Commercial Fleets | ||

| By End User | Individual consumers | |

| Fleet operators | ||

| Delivery aggregators | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of battery swapping for the electric two-wheeler market by 2031?

The battery swapping for the electric two-wheeler market is forecast to reach USD 1.25 billion by 2031 based on an 18.21% CAGR.

Which service model leads adoption?

Subscription plans hold a 62.72% share because they convert battery ownership into predictable operating expenses for fleets.

Why is Asia-Pacific the largest regional market?

Asia-Pacific combines high two-wheeler density, government subsidies, and proven ecosystem blueprints that lower deployment risk.

How do automated stations compare with manual kiosks?

Automated stations swap batteries in under 30 seconds and post an 18.49% CAGR, but they require higher upfront capital than manual formats.

What role do delivery fleets play?

Delivery and gig-economy fleets generate 58.22% of current demand owing to their need for zero-downtime operations.

Are lithium-ion batteries likely to retain dominance?

Lithium-ion chemistry delivers superior energy density and falling pack prices, securing 73.85% share and an 18.55% CAGR.

Page last updated on: