Electric Kick Scooter Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

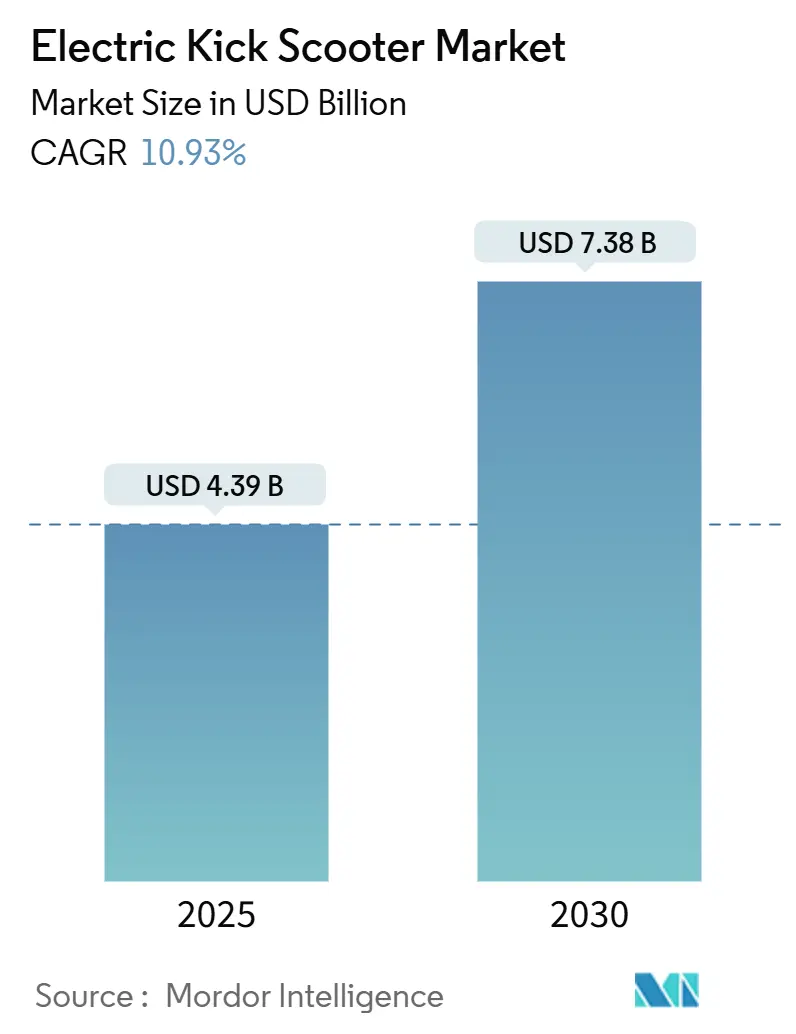

| Market Size (2025) | USD 4.39 Billion |

| Market Size (2030) | USD 7.38 Billion |

| Growth Rate (2025 - 2030) | 10.93% CAGR |

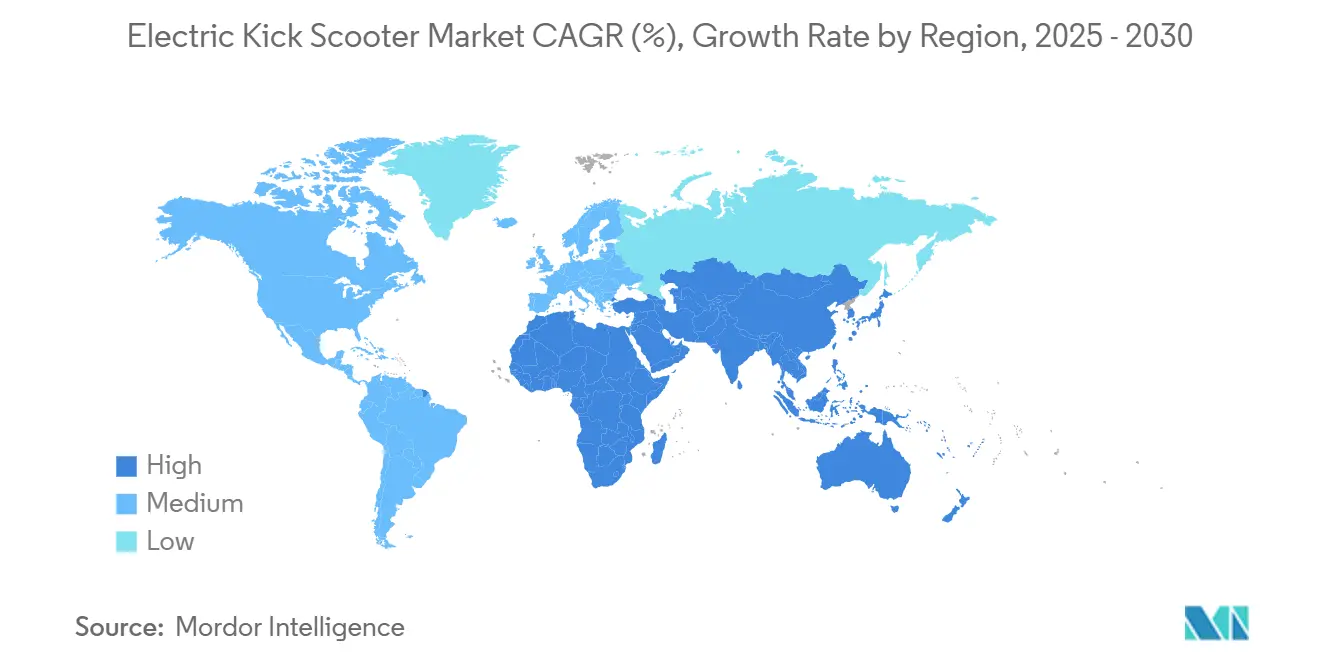

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

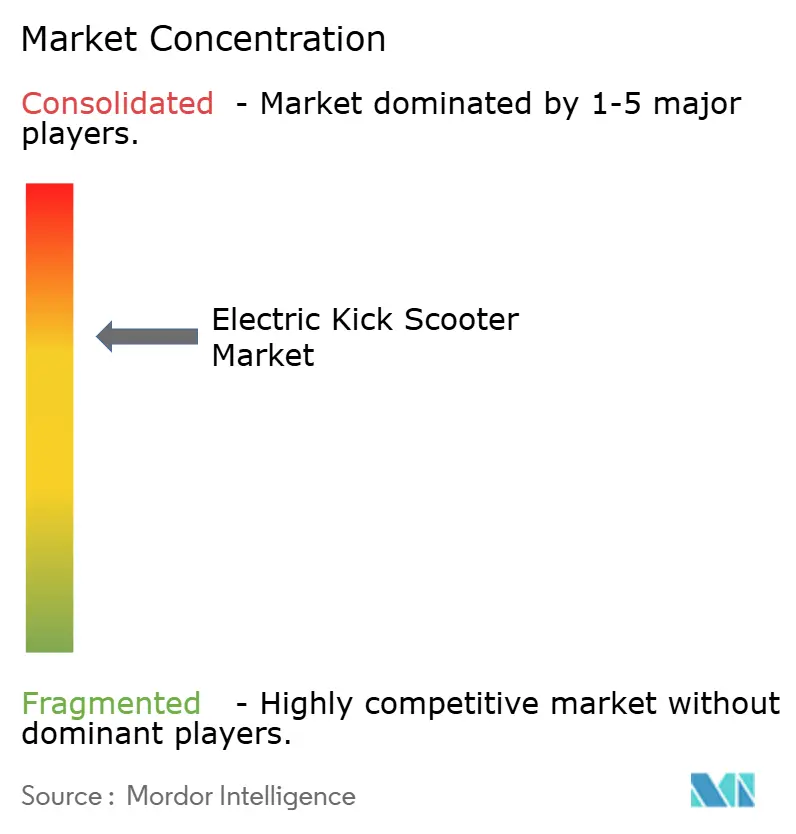

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Kick Scooter Market Analysis by Mordor Intelligence

The Electric Kick Scooter Market size is estimated at USD 4.39 billion in 2025, and is expected to reach USD 7.38 billion by 2030, at a CAGR of 10.93% during the forecast period (2025-2030). Intensifying urban congestion and supportive regulatory incentives underpin steady demand, while advances in battery chemistry, hub-motor efficiency, and data-driven fleet management sharpen the value proposition for commuters and fleet operators. Shared micro-mobility platforms now record positive free cash flow, demonstrating profitable unit economics at scale. Simultaneously, trade policy pressures accelerate near-shoring, prompting leading Chinese brands to open Indonesian and Vietnamese plants that mitigate tariff exposure. Supply-side consolidation in Europe and a proliferation of sodium-ion alternatives point to a maturing yet innovative, competitive arena.

Key Report Takeaways

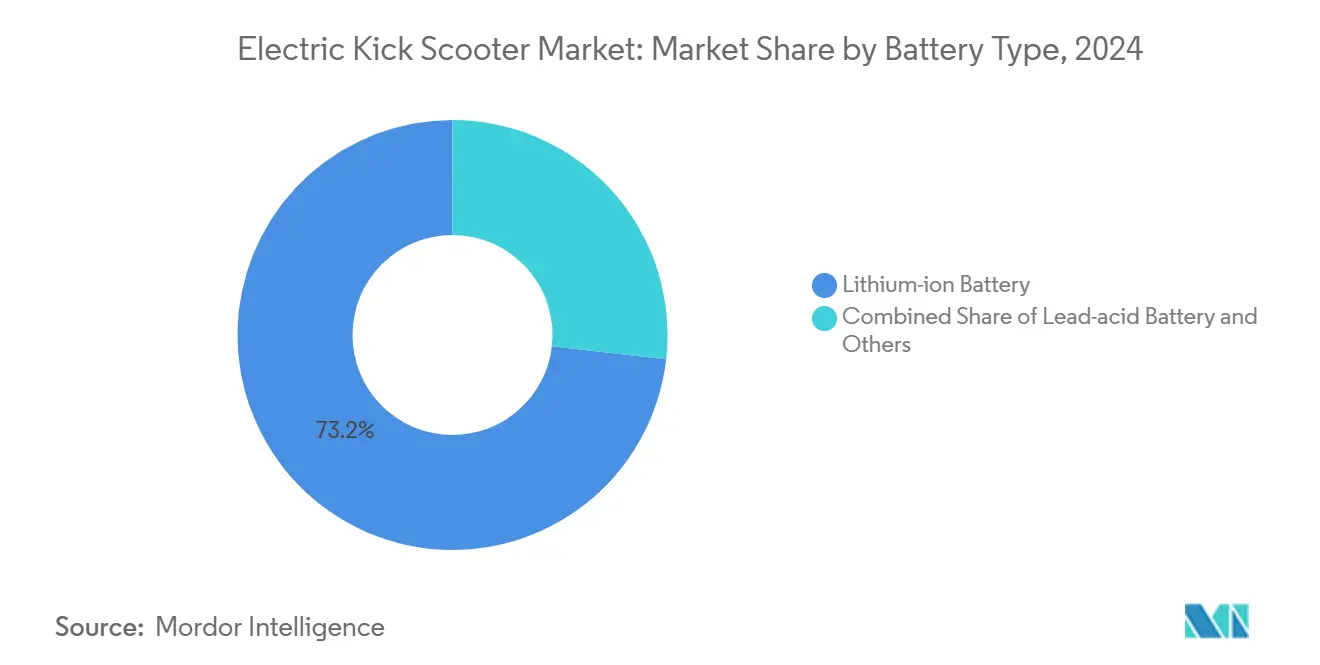

- By battery type, lithium-ion held 73.18% of the electric kick scooter market share in 2024, and sodium-ion systems in the “Others” category are projected to expand at a 10.95% CAGR through 2030.

- By drive type, hub motors commanded 65.68% of the electric kick scooter market share in 2024. and posted the fastest CAGR at 11.03% to 2030.

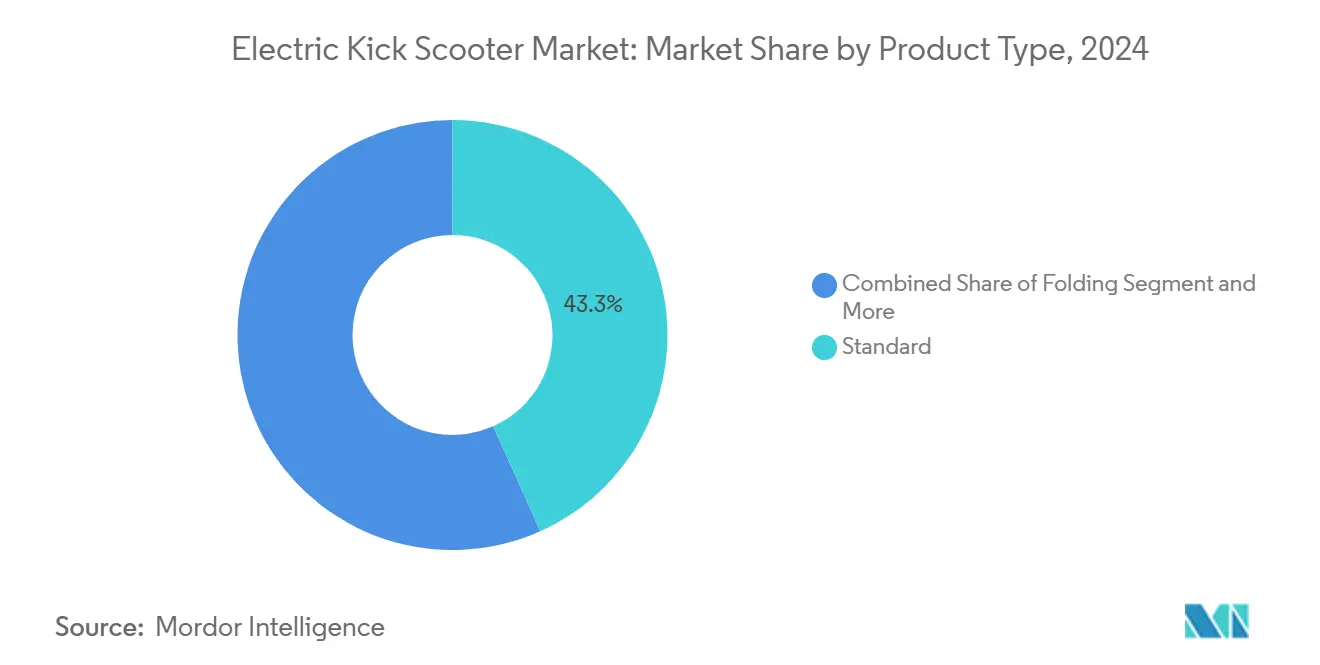

- By product type, the standard held 43.27% of the electric kick scooter market share in 2024, and folding models registered an 11.05% CAGR, outpacing standard units.

- By end use, personal held 68.71% of the electric kick scooter market share in 2024, whereas commercial fleets will grow at a 10.97% CAGR from 2025-2030.

- By geography, Europe commanded 37.88% of the electric kick scooter market share in 2024, while the Middle East and Africa are forecast to advance at a 10.98% CAGR through 2030.

Global Electric Kick Scooter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Shared Micro-Mobility Services | +2.8% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Urban Congestion | +2.3% | Global metropolitan areas | Short term (≤ 2 years) |

| Supportive E-Mobility Incentives | +2.1% | Europe, Asia-Pacific, selective North America | Long term (≥ 4 years) |

| Advances In Lithium-Ion Battery Density | +1.9% | Global manufacturing, Asia Pacific production centers | Medium term (2-4 years) |

| Swappable Sodium-Ion Battery Packs Emerge | +1.2% | China, expanding to Southeast Asia | Long term (≥ 4 years) |

| Tariff-Driven Regional Assembly | +0.8% | North America, Europe, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Shared Micro-Mobility Services

Lime logged 200 million rides in 2024 and generated USD 810 million in gross bookings, confirming the viability of scale-built fleet economics [1]“Lime Achieves Second Year of Free Cash Flow,” Lime, li.me . Gen4 vehicles with swappable batteries lowered downtime and operating costs, turning Lime’s cash flow positive for a second straight year. VOI likewise reported full-year Adjusted EBIT profitability and expanded its fleet by two-fifths by adding three sturdier models that consume three-fifths less power [2]“VOI Reports Profitability and New Fleet Rollout,” VOI Technology, voi.com . Consolidation peaked with the TIER-Dott merger, shrinking Europe’s field to three dominant operators enjoying economies of scale in procurement, regulatory compliance, and data analytics. These achievements support last-mile trips under 5 kilometers, where scooters outperform taxis and private cars in both time and cost metrics.

Urban Congestion Boosting Last-Mile Demand

Peak-hour trips under 8 kilometers illustrate a measurable time advantage for electric scooters versus ride-hailing or private cars. Commercial delivery services such as Zypp Electric in India and Zoomo in the UK deploy purpose-built cargo scooters to slash delivery windows and service costs. Multimodal commuters in London registered many scooter-linked rides in 2024, marking a significant jump year over year. Municipal support follows: London’s new parking bays and a three-fifths expansion in operational staff highlight infrastructure alignment. Three-wheel platforms and cargo variants further broaden use-case scenarios without sacrificing compact maneuverability.

Supportive E-Mobility Incentives & Regulations

Municipal policy increasingly favors micro-mobility, from Dubai’s structured permits to Oslo’s two-year tenders awarding multiple vehicles to only three firms. London installed more than two thousand parking spaces under Lime’s massive Action Plan, a concrete sign of government-industry collaboration. Even so, regulatory complexity persists: Bloomington, Indiana, canceled Lime’s contract for missing a one-third e-bike ratio, underscoring evolving compliance demands. Mandated UL 2272 certification has become a de facto entry requirement that rewards incumbents with certified portfolios while deterring new entrants that lack safety infrastructure.

Advances in Lithium-Ion Battery Density & Cost

Segway’s GT3 Pro reaches a 138-kilometer theoretical range on dual 2,160 Wh packs, illustrating how chemistry and power-management upgrades extend service intervals. Indian replacement prices of INR 55,000-100,000 (USD 660-1,200) for lithium-ion packs validate ownership economics. Sodium-ion prototypes by CATL deliver lower cost and better thermal stability, albeit at lower energy density, positioning them for high-temperature markets. Sophisticated battery-management systems now schedule charging and track cycles and integrate predictive diagnostics, lengthening pack life while lowering fleet OPEX. Lime’s recycling partnership with Redwood Materials recovers up to four-fifths of critical metals, cutting future battery procurement cost curves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Injury Rates Trigger City Restrictions | -1.8% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| High Manufacturing and Maintenance Costs | -1.4% | Global manufacturing, operational markets | Medium term (2-4 years) |

| Import Tariffs On China-Made Units | -1.1% | North America, Europe import markets | Medium term (2-4 years) |

| Battery-Fire Certification Delays | -0.9% | North America, Europe regulatory markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Injury Rates Trigger City Restrictions

Accident spikes have forced Paris, Madrid, and Vienna to impose stricter speed caps and geofenced slow zones, throttling fleet utilization and revenue. Operators respond with technological fixes: Honda’s gyroscope-based auto-balance prototypes, slated for 2026-2028, promise enhanced stability that could placate regulators by reducing fall incidents. Until then, every crash statistic risks new curbs that disrupt market momentum.

High Manufacturing & Maintenance Costs

Onshoring a U.S. factory requires huge capital outlays and battles the one-fourth tariff still levied on Chinese e-bikes. Tariffs raise retail prices and cause sticker shock. Lifecycle costs remain elevated when vandalism limits shared-fleet vehicles to less than 1,000 kilometers. VOI’s Voiager 8 mitigates this through modular, easily swappable components and reduced power draw, extending service life and improving ROI.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Lithium-Ion Dominance Faces Sodium-Ion Disruption

Lithium-ion packs captured 73.18% of the electric kick scooter market in 2024, underpinning mass-production scale, superior energy density, and a mature recycling ecosystem. Swappable architectures and Redwood-backed recycling loops reclaim up to four-fifths of critical materials, shrinking replacement cost curves. Sodium-ion technology, the primary constituent of the “Others” category, stands out with a 10.95% CAGR to 2030 as CATL and local producers commercialize its lower cost structure and improved thermal stability, making it attractive for tropical climates and safety-centric regulators.

Cost advantages and thermal resilience make sodium-ion a compelling alternative for shared micro-mobility fleets that prioritize total cost of ownership over maximum range. Lead-acid remains relegated to price-sensitive niches and continues to forfeit share. Intelligent battery-management systems embedded in Segway’s BMS 2.0 provide cycle tracking and predictive diagnostics that lengthen service life and lower maintenance overhead.

By Drive Type: Hub Motors Achieve Technical Maturation

Hub motors secured 65.68% of the electric kick scooter market share in 2024 and are advancing at an 11.03% CAGR through 2030. Brushless DC hubs offer favorable torque-to-weight ratios and near-zero maintenance, explaining their dominance over SRM alternatives that trade efficiency for cost. Chain drives persist in heavy-payload cargo models where torque peaks matter more than efficiency, while belt drives serve premium enthusiasts who prioritize quiet operation.

Donut Lab’s latest in-wheel developments increase power density without adding unsprung mass, making hub motors more attractive for future cargo variants. With simplified wiring and fewer moving parts, hub architecture reduces assembly complexity and parts inventories, further reinforcing its leadership.

By Product Type: Folding Innovation Drives Segment Growth

Standard non-folding scooters held 43.27% of the electric kick scooter market share in 2024, maintaining a foothold in shared fleets where durability outweighs portability. The folding sub-segment, however, posts the fastest expansion at 11.05% CAGR as dense urban living spaces value compact storage. Ultralight carbon-fiber frames in NIU’s KQi Air cut carry weight yet maintain structural integrity for daily commuting.

Self-balancing prototypes embed gyroscopes for autostability to reduce fall incidents and enable future autonomous re-positioning. While solar-charging decks remain experimental, folding designs benefit from real-estate constraints in apartments and offices, cementing their appeal among individual owners and increasingly among corporate fleets prioritizing convenient indoor storage.

By End Use: Commercial Applications Accelerate Growth

Personal ownership dominated with 68.71% of the electric kick scooter market share in 2024 but faces an incremental shift as commercial fleets log a 10.97% CAGR. Last-mile logistics providers like Zypp Electric and Zoomo equip cargo variants with large-capacity racks and embedded telematics to boost utilization and enforce predictive maintenance cycles.

High daily usage and centralized servicing give fleet operators superior unit economics relative to consumer owners. Dedicated software dashboards optimize routing and battery swaps, driving higher revenue per asset and quicker payback periods. Consequently, commercial adoption expands from food delivery into pharma, postal, and convenience retail segments.

Geography Analysis

Europe led with a 37.88% of the electric kick scooter market share in 2024, buoyed by mature shared-mobility ecosystems and supportive municipal tenders. Oslo’s multiple-unit program and London’s massive parking initiative reinforce structural demand. However, safety concerns in Paris, Madrid, and Vienna produce new speed caps and fleet caps that complicate volume growth. Supplier consolidation into three dominant operators, post the TIER-Dott deal, supplies the scale needed to navigate Europe’s fragmented regulatory framework.

The Middle East and Africa represent the fastest-growing territory at a 10.98% CAGR through 2030. Dubai’s clear rule-making and Saudi Arabia’s electrification roadmaps create fertile ground for pilots that can scale quickly in purpose-built smart cities like NEOM. Sub-Saharan Africa shows latent potential as two-wheelers leapfrog legacy transport, aided by donor-backed infrastructure and low-cost Chinese imports.

Asia-Pacific remains the manufacturing nucleus: In 2024, China exported a significant number of units at a competitive average FOB price, accounting for more than half of global output. By 2027, India's domestic penetration is set to rise substantially, driven by capacity expansions from Ola Electric, TVS, and Bajaj. North America's tariff pressures now effectively several on complete units are prompting near-shoring. This is underscored by Yadea's establishment of a substantial plant in Indonesia and TAILG's facility in Vietnam, both strategically sidestepping U.S. and EU tax barriers.

Competitive Landscape

Europe’s operator field compressed to three majors after the TIER-Dott merger. The merger delivered a huge investment in combined revenue and trimmed duplicative overhead. Lime invests in proprietary battery architecture to cut maintenance costs, achieving positive free cash flow for two consecutive years. VOI’s Voiager 8 and Segway-Ninebot’s GT3 Pro embody hardware differentiation through enhanced suspension, rugged frames, and integrated navigation [3]“GT3 Pro Launch Press Kit,” Segway-Ninebot, segway.com.

Production concentration remains Chinese, with Segway-Ninebot, Xiaomi, NIU, and Yadea wielding economies of scale. Yet, tariff-induced regional capacity like Yadea Indonesia signals a pivot toward diversified footprints that lessen geopolitical risk. Sodium-ion and swappable-battery startups attract venture capital as they promise safer chemistry and lower cost per watt-hour, challenging lithium-ion incumbency in the long run.

White-space persists in cargo and three-wheel variants tuned for delivery fleets and safety-conscious municipal requirements. Startups focusing on battery analytics, recycling, and stability software enter through these niches, intensifying innovation even as market leaders consolidate volume.

Electric Kick Scooter Industry Leaders

Segway-Ninebot

Xiaomi

YADEA

Razor USA

Niu Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lime partnered with Redwood Materials to recycle lithium-ion packs across the U.S., Germany, and the Netherlands, enabling up to 98% material recovery and advancing Lime’s 2030 net-zero roadmap.

- April 2025: Lime introduced the LimeBike and LimeGlider lines, deploying 10,000 modular vehicles with swappable batteries in Europe and North America.

- March 2025: VOI Technology enlarged its fleet 40% with the Voiager 8 e-scooter and two new e-bikes, lowering power consumption by 54% and extending product durability to bolster its first full-year EBIT-positive performance.

Global Electric Kick Scooter Market Report Scope

| Lead-acid Battery |

| Lithium-ion Battery |

| Others |

| Belt Drive |

| Chain Drive |

| Hub Motors |

| Standard |

| Folding |

| Self-balancing |

| Others |

| Personal |

| Commercial |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Battery Type | Lead-acid Battery | |

| Lithium-ion Battery | ||

| Others | ||

| By Drive Type | Belt Drive | |

| Chain Drive | ||

| Hub Motors | ||

| By Product Type | Standard | |

| Folding | ||

| Self-balancing | ||

| Others | ||

| By End Use | Personal | |

| Commercial | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the electric kick scooter market?

The market stands at USD 4.39 billion in 2025 and is forecast to reach USD 7.38 billion by 2030.

Which battery technology leads today?

Lithium-ion batteries hold 73.18% share, although sodium-ion packs are the fastest-growing alternative.

Which region is expanding fastest?

The Middle East and Africa post the highest projected CAGR at 10.98% through 2030.

How concentrated is the competitive landscape?

Top operators and manufacturers jointly yield a concentration score of 7 out of 10.

What drives commercial fleet adoption?

Predictable usage patterns, centralized maintenance, and cargo-specific scooter models cut the total cost of ownership and spur a 10.97% CAGR in commercial deployment.

Page last updated on: