China E Scooter Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

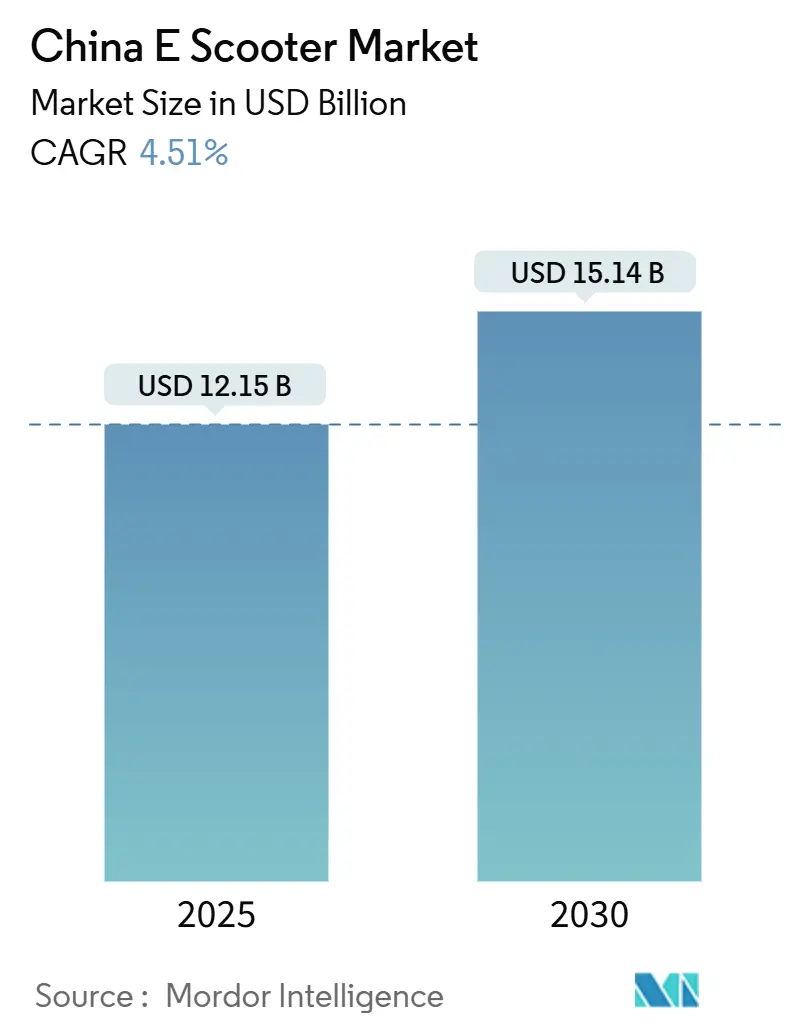

| Market Size (2025) | USD 12.15 Billion |

| Market Size (2030) | USD 15.14 Billion |

| Growth Rate (2025 - 2030) | 4.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China E Scooter Market Analysis by Mordor Intelligence

The China E Scooter Market size is estimated at USD 12.15 billion in 2025, and is expected to reach USD 15.14 billion by 2030, at a CAGR of 4.51% during the forecast period (2025-2030). A shift from volume-oriented competition to value-driven differentiation is underway as large players streamline supply chains, improve safety features, and roll out lithium-based battery offerings that meet tightening regulatory standards. The battery-swap franchising, sodium-ion pilot programs, and corporate “green logistics” pledges are accelerating fleet electrification among logistics firms, supermarkets, and parcel operators. Rising working-capital constraints, a supply-glut of low-end models, and fire-safety compliance costs, however, compress margins for smaller original equipment manufacturers (OEMs) and may slow penetration in lower-income rural prefectures.

Key Report Takeaways

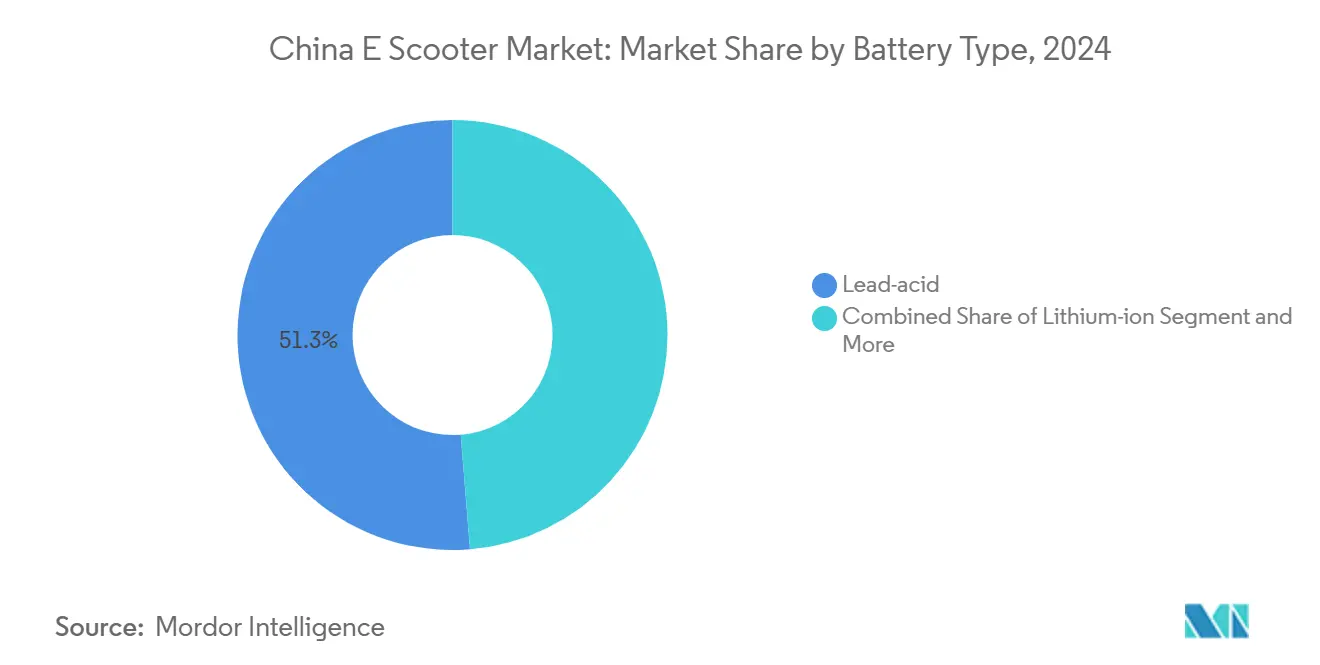

- By battery type, lead-acid captured 51.27% of China electric scooter market share in 2024, while sodium-ion chemistries are forecast to grow at a 6.53% CAGR to 2030.

- By power output, sub-3.6 kW units led with 61.25% revenue share in 2024; the 7.2–10 kW range is set to expand at a 6.61% CAGR through 2030.

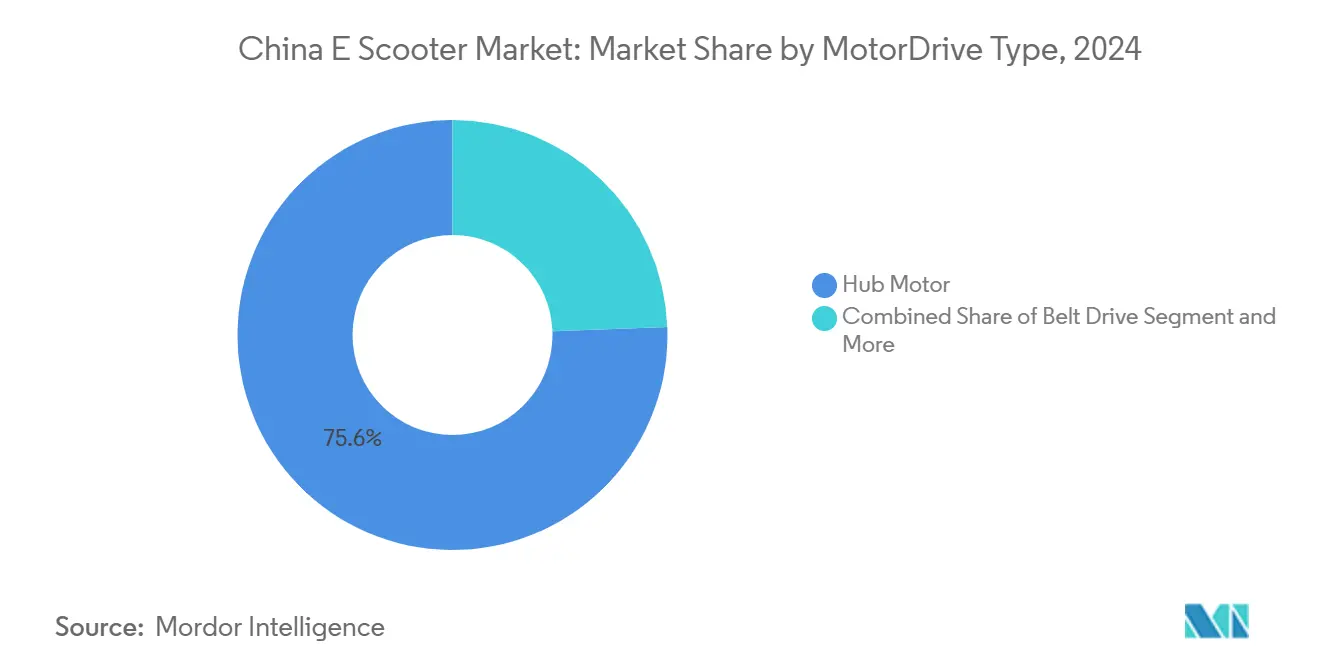

- By motor configuration, hub motors dominated with 75.64% share in 2024, yet mid-drive adoption is expected to log a 6.58% CAGR to 2030.

- By end-use, personal ownership accounted for 71.28% of market revenue in 2024, whereas micromobility service providers are projected to post the highest 6.63% CAGR over the same horizon.

China E Scooter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Lithium-Ion Pack Price Declines | +1.8% | Global, concentrated in tier-1 Chinese cities | Medium term (2-4 years) |

| Expansion Of Last-Mile Delivery Demand | +1.5% | Urban China, spillover to tier-2 cities | Short term (≤ 2 years) |

| National Phase-Out Of Lead-Acid Incentives | +1.2% | National, with early gains in Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| Green Logistics Corporate Pledges | +0.9% | Major Chinese metropolitan areas | Long term (≥ 4 years) |

| Sodium-Ion Pilot Subsidies | +0.7% | Pilot regions, expanding nationally | Long term (≥ 4 years) |

| Rise Of Battery-Swap Franchising Models | +0.4% | Dense urban areas, commercial fleet hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Lithium-Ion Pack Price Declines

Lithium-ion battery pack costs in China fell to USD 94 per kWh in 2024, undercutting the global average and reflecting the country’s command of roughly three-fourths of worldwide pack output capacity[1]“Next-Generation Sodium-Ion Batteries Debut,” CATL, catl.com. The stabilization of lithium carbonate prices, combined with the rapid adoption of lithium iron phosphate cells and increased vertical integration in cathode production, has empowered OEMs to offer more affordable entry-level electric scooters without compromising on range. This trend is expected to drive significant growth in the electric scooter market, as cost reductions make these vehicles more accessible to a broader consumer base. Additionally, advancements in battery technology and streamlined production processes are likely to further enhance the performance and affordability of electric scooters during the forecast period.

Expansion Of Last-Mile Delivery Demand

In late 2024, China's express parcel sector reached a significant milestone, driven by surging e-commerce demand, technological innovation, and a vast logistics infrastructure. This growth underscores its critical role in supporting domestic consumption and economic activity, such as Cainiao's scaled Level 4 autonomous delivery pilots, which handle 1,500 packages per vehicle daily[2]“Autonomous Delivery Vehicle Milestones,” Cainiao, cainiao.com. Logistics operators augment these unmanned fleets with high-durability 7.2–10 kW electric scooters to cover overflow peaks, reduce labor turnover, and comply with citywide decarbonization targets. The order cycle of these commercial units spurs demand for telematics-enabled dashboards, reinforced chassis, and extended-range battery packs.

National Phase-Out Of Lead-Acid Incentives

The 2025 trade-in scheme grants higher financial support to riders who scrap lithium-ion scooters for new lead-acid models, aiming to mitigate battery-fire risks during the transition to higher-density packs[3]“Circular on 2025 Consumer Trade-in Program,” Ministry of Commerce, mofcom.gov.cn. Parallel enforcement of GB 42295-2022 electrical safety rules and GB 43854-2024 pack standards forces OEM redesigns of controllers, chargers, and battery casings, increasing compliance investments yet catalyzing a systemic move toward safer chemistries.

Sodium-Ion Pilot Subsidies

Central ministries have rolled out targeted incentives to promote the adoption of sodium-ion two-wheelers in specific regions to localize supply chains and lessen reliance on unpredictable metal markets. These initiatives align with the broader objective of fostering sustainable transportation solutions and enhancing domestic manufacturing capabilities. Meanwhile, major battery manufacturers are making notable advancements: one has introduced a high-energy-density sodium-ion cell, and another has commenced building a large-scale production facility, setting the stage for economical mass deployment in the near future.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Glut Driven Margin Compression | -1.4% | National, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Rural Charging-Infrastructure Deficit | -1.2% | Rural and tier-3/4 cities, limited tier-2 spillover | Long term (≥ 4 years) |

| OEM Working-Capital Crunch | -1.1% | National, concentrated in Jiangsu, Zhejiang manufacturing clusters | Short term (≤ 2 years) |

| Fire-Safety Regulatory Tightening | -0.8% | National, stricter enforcement in tier-1 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Glut Driven Margin Compression

After the pandemic, demand rebounded unevenly, resulting in surplus inventory, diminished export activities, and manufacturing capacities that weren't fully tapped. Key materials, especially steel and aluminum, saw rising input costs, intensifying the pressure. Meanwhile, domestic OEMs faced prolonged payment cycles, hinting at a squeeze in liquidity and mounting operational stress throughout the value chain. Platforms like BYD’s DiChain securitize supplier receivables yet extract discounted service fees, eroding margins for sub-scale scooter assemblers. Consolidation is expected as smaller brands confront liquidity gaps, negative working capital, and rising retailer rebates.

Fire-Safety Regulatory Tightening

An uptick in more than 21,000 scooter-related fires in 2023 prompted the State Administration for Market Regulation and other agencies to intensify factory audits and implement thermal-runaway stress testing protocols under GB 42295-2022. Mandatory QR code tracing of every battery pack obligates manufacturers to deploy enterprise resource planning and manufacturing execution systems, raising compliance costs that disproportionately burden workshops producing fewer than 10,000 units annually. Tier-1 city fire departments now require residential complexes to install isolated charging rooms, limiting home-balcony charging and potentially slowing uptake among apartment dwellers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Sodium-ion momentum reshapes the chemistry mix

Lead-acid batteries retained 51.27% revenue share in 2024, a reflection of entrenched price leadership, robust recycling networks, and the perceived safety of low-energy packs. Yet sodium-ion and allied chemistries are forecast to log a 4.53% CAGR through 2030, markedly higher than the overall China electric scooter market. CATL’s first-generation sodium-ion cell and BYD’s announced 30 GWh facility testify to strategic bets on abundant sodium resources, which offer de-risked raw material supply and lower winter-temperature performance losses. Early sales of Yadea’s sodium-ion e-bicycle in January 2025 suggest commercial readiness in urban commuter segments that require moderate range at lower cost. Lithium-ion polymer variants will likely retain loyal followings in premium performance scooters, particularly those targeting on-demand personal mobility in high-income districts where ultra-fast charging and lightweight frames command a price premium.

In the mid-term, national subsidies that reward upgrades from older lithium-ion packs to safer lead-acid replacements illustrate policy caution, balancing fire-risk mitigation with longer-term cues favoring high-energy chemistries. Manufacturers with vertically integrated cathode, anode, and pack assembly lines enjoy input-cost hedging advantages, while firms stuck in contract manufacturing face commodity price swings. Foreign battery suppliers eye joint ventures to gain a foothold in this accelerated technology race, yet local players’ dominance of over 80% of global lithium conversion capacity ensures competitive barriers remain substantial. The chemistry mix will therefore pivot on a blend of policy directives, raw-material price trajectories, and end-user safety perceptions, ultimately reinforcing multi-chemistry portfolios among top-tier brands.

By Power Output: Mid-range power climbs as delivery fleets demand torque

The sub-3.6 kW category accounted for 61.25% of revenue in 2024, thanks to national speed caps that limit many commuter models to 25 km/h and thus favor smaller motors. That mass-market dominance coexists with meaningful growth in the 7.2–10 kW band, where a 4.61% CAGR is predicted through 2030, outperforming the China electric scooter market. Delivery firms in hilly Chongqing, Kunming, and Xiamen purchase higher-powered models to sustain tight parcel schedules without overheating or capacity loss on steep grades. While the 3.6–7.2 kW tranche remains an attractive compromise for peri-urban commuters who need extra acceleration for mixed-traffic arterials, many OEMs are updating controller software, duty cycles, and regenerative braking logic to square regulatory compliance with consumer expectations for quicker take-offs and extended hill climbs.

Scooters over 10 kW remain a niche, primarily because licensing shifts such vehicles into a light-motorcycle classification that mandates insurance, motorcycle plates, and specialized helmets. The impending rollout of a unified national power-rating code may further narrow the high-power window. Nonetheless, specialty players market 11 kW models to recreational users seeking weekend leisure rides and to corporate fleets requiring heavy cargo boxes for point-to-point cold-chain delivery. The power-output matrix therefore shows segmentation along both regulatory lines and user-case heterogeneity, reinforcing the importance of targeted model portfolios.

By Motor/Drive Type: Mid-drive traction gains on performance grounds

Hub motors dominated 75.64% of sales in 2024, benefitting from low tooling costs, straightforward assembly, and simplified maintenance regimes. Yet mid-drive units are on a faster 4.58% CAGR trajectory that outpaces the China electric scooter market, driven by torque advantages, superior weight distribution, and better energy efficiency in stop-and-go inner-city scenarios. Tier-1 OEMs advertise mid-drive configurations paired with belt drive and proprietary controllers to deliver higher climbing angles and quieter operation, catering to premium riders and commercial couriers who value performance parity with 50 cc gasoline mopeds.

Belt drive and chain systems remain relevant in specialized performance niches, such as food-delivery scooters equipped with insulated cargo boxes or aftermarket-tuning segments promoted by lifestyle brands. Extensive investments in motor-controller co-design are producing compact integrated drive units that cut assembly time, reduce wiring complexity, and improve reliability. Hardware advances are being complemented by vector control algorithms that optimize efficiency at various load points. Consequently, OEMs capable of supplying bundled powertrains and in-house software achieve margin protection against commodity motor suppliers.

By End-Use: Micromobility services accelerate amid shared-fleet expansion

Personal ownership dominated with 71.28% revenue share in 2024, underpinned by the China electric scooter market’s decade-long consumer adoption curve. Micromobility operators, however, are forecast to expand unit demand at a 4.63% CAGR through 2030, as venture-backed platforms deploy dockless scooters near subway exits, tourist attractions, and campus corridors. These fleets require ruggedized frames, modular battery bays, and telematics for real-time fleet optimization. Commercial parcel carriers also seek differentiated scooter variants featuring tablet mounts, anti-theft geofencing, and quick-swap battery interfaces that sustain 18-hour duty cycles.

Corporate purchasing departments increasingly include two-wheelers in ESG-aligned commuting benefits programs, providing staff with employer-subsidized vehicles that reduce parking constraints and shorten last-mile transit times from metro stations. Operational leasing firms bundle hardware, maintenance, and insurance, creating predictable residual value models that appeal to finance teams. Together, these shifts widen the addressable end-use spectrum beyond retail consumers toward institutional and municipal customers.

Geography Analysis

Tier-1 cities such as Beijing, Shanghai, and Shenzhen constitute the densest demand clusters for the China electric scooter market. Residents benefit from local regulations that exempt compliant scooter models from license-plate lotteries, tilting commuter decisions toward electrified two-wheelers. Battery-swap stations are becoming common at office parks, shopping centers, and multi-family housing garages, shortening range anxiety and amplifying convenience.

Tier-2 urban regions, including Chengdu, Xi’an, and Ningbo, display brisk scooter uptake yet differ in regulatory leniency, sometimes allowing marginally higher speed limits or heavier cargo racks. Local development zones actively court scooter assemblers with tax breaks and plant-construction support, seeking to replicate the supply-chain ecosystems of Jiangsu and Zhejiang. Still, uneven enforcement of national standards can create patchwork compliance demands that challenge OEM rollouts. Geographically, roughly three-fifth of commuters in cities below tier-3 continue to rely on two-wheelers for trips under 10 km, a statistic that underscores the resilience of low-cost transportation in regions with limited subway coverage.

Rural townships present latent demand but face gaps in high-amperage grid connections, relying on informal wall-socket charging or coin-operated outlets near convenience stores. Government pilot funds target county-level charging micro-grids and agricultural-electricity pricing reforms, yet project timelines remain uncertain. Meanwhile, manufacturing clusters in Jiangmen, Wuxi, and Taizhou consolidate production and supply-chain bases, ensuring export-ready scooters funnel efficiently through coastal ports. Regional synergy between battery cell plants in Anhui and motor suppliers in Guangdong underscores the agglomeration advantages unique to eastern seaboard provinces.

Competitive Landscape

Market concentration remains moderate as leading brands Yadea, Aima, Tailg, and Niu Technologies capitalize on scale, multi-chemistry battery sourcing, and dealership footprints that surpass 20,000 combined outlets nationwide. Yadea retained the revenue crown in 2024, leveraging an R&D pipeline of more than 1,900 patents and unveiling a sodium-ion powered model ahead of rivals. Aima strengthened premium pricing power by integrating 5G-enabled dashboards and anti-theft geofencing. Tailg forged a battery-supply alliance with BYD in December 2024 to embed automotive-grade safety protocols and pack traceability into its commuter line-up.

Niu Technologies, the first China-listed smart-scooter specialist on the NASDAQ, pivoted to mid-drive powertrains and subscription-priced connectivity services to boost recurring revenue. High entry barriers now stem less from mass manufacturing prowess than from proprietary software, after-sales service, and captive battery ecosystems that lock in customer lifetime value. Industry consolidation will likely accelerate as smaller assemblers fold or merge, unable to amortize rising compliance costs.

The shift toward solution-centric competition incentivizes OEMs to pair scooter hardware with fleet-management dashboards, telematics analytics, and pay-by-swap battery subscriptions. This integrated value proposition empowers logistic and sharing-fleet clients to measure carbon savings and optimize asset utilization, reinforcing long-term vendor relationships. In essence, competitive dynamics gravitate toward ecosystem control rather than transactional unit sales.

China E Scooter Industry Leaders

Yadea Technology Group

Aima Technology Group

Tailg Group

Niu Technologies

Luyuan Electric Vehicle

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: China’s Ministry of Commerce released RMB 1 billion in e-bike trade-in subsidies covering 1.65 million consumers and triggering 1.66 million new scooter purchases.

- January 2025: Yadea introduced the world’s first mass-produced sodium-ion battery e-bicycle, signaling commercial readiness of alternative chemistries.

- December 2024: Tailg and BYD announced a strategic pact on battery supply and joint safety-system development to integrate automotive-grade packs into commuter scooters.

China E Scooter Market Report Scope

| Lead-acid |

| Lithium-ion |

| Lithium-ion Polymer |

| Sodium-ion & Emerging Chemistries |

| Less than 3.6 kW |

| 3.6 – 7.2 kW |

| 7.2 – 10 kW |

| More than 10 kW |

| Hub Motor |

| Belt Drive |

| Chain Drive |

| Mid-drive Motor |

| Personal / Individual |

| Commercial & Corporate Fleets |

| Micromobility Service Providers |

| Delivery & Logistics |

| By Battery Type | Lead-acid |

| Lithium-ion | |

| Lithium-ion Polymer | |

| Sodium-ion & Emerging Chemistries | |

| By Power Output | Less than 3.6 kW |

| 3.6 – 7.2 kW | |

| 7.2 – 10 kW | |

| More than 10 kW | |

| By Motor / Drive Type | Hub Motor |

| Belt Drive | |

| Chain Drive | |

| Mid-drive Motor | |

| By End-Use | Personal / Individual |

| Commercial & Corporate Fleets | |

| Micromobility Service Providers | |

| Delivery & Logistics |

Key Questions Answered in the Report

What is the current size of the China electric scooter market?

The China electric scooter market size stood at USD 12.15 billion in 2025 and is expected to reach USD 15.14 billion by 2030.

Which battery chemistry is growing the fastest in Chinese electric scooters?

Sodium-ion batteries are projected to grow at a 4.53% CAGR through 2030, outpacing lithium-ion and lead-acid alternatives.

How are delivery companies influencing electric-scooter demand?

Logistics operators boost demand by adopting 7.2–10 kW models for last-mile and overflow delivery tasks, helping the power segment grow at a 4.61% CAGR.

Why are mid-drive motors gaining popularity?

Mid-drive motors offer better torque, improved weight balance, and higher energy efficiency, leading to a projected 4.58% CAGR for this drive type.

Which cities account for the highest electric-scooter penetration in China?

Beijing, Shanghai, and Shenzhen lead adoption due to robust charging infrastructure and supportive regulations.

Page last updated on: