Scissor Lift Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

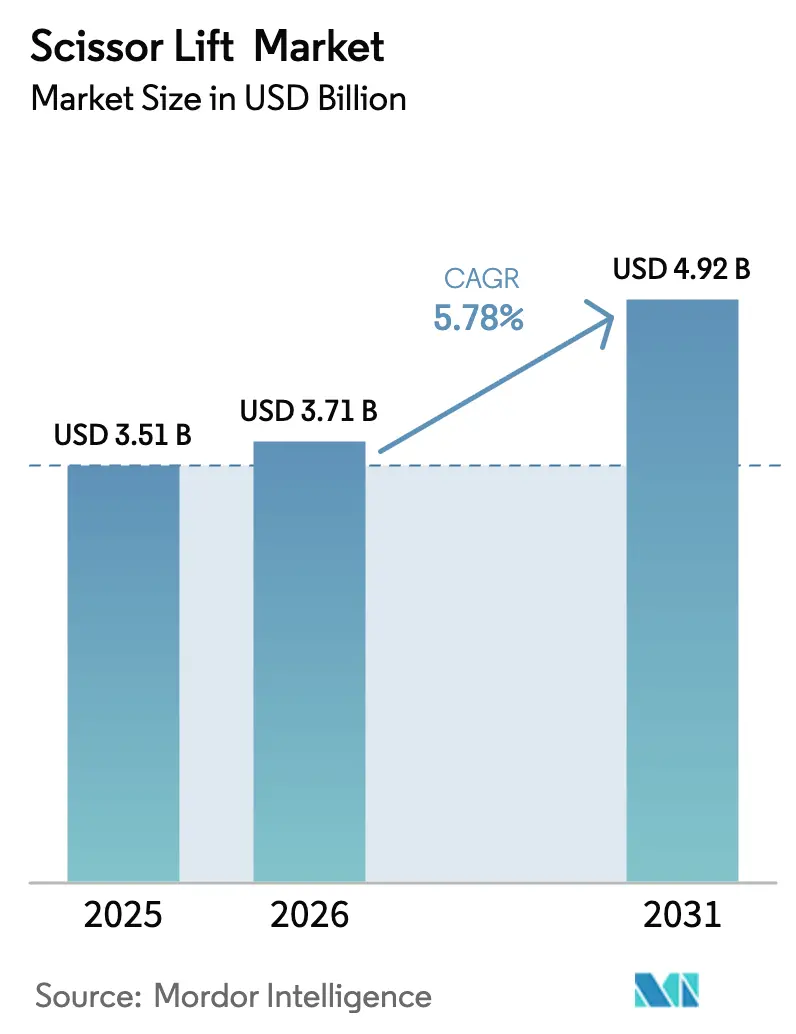

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 4.92 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scissor Lift Market Analysis by Mordor Intelligence

The Scissor Lift market size is expected to grow from USD 3.51 billion in 2025 to USD 3.71 billion in 2026 and is forecast to reach USD 4.92 billion by 2031 at 5.78% CAGR over 2026-2031. Rental fleet owners continue to refresh equipment in response to stricter ANSI and OSHA rules, while contractors increasingly specify quieter, emission-free electric units for indoor jobs. Digital fleet analytics are improving utilization rates and nudging end users toward premium models that offer predictive maintenance and lower life-cycle costs. Risk factors center on operator shortages, raw-material price swings, and the capital intensity of battery replacement cycles.

Key Report Takeaways

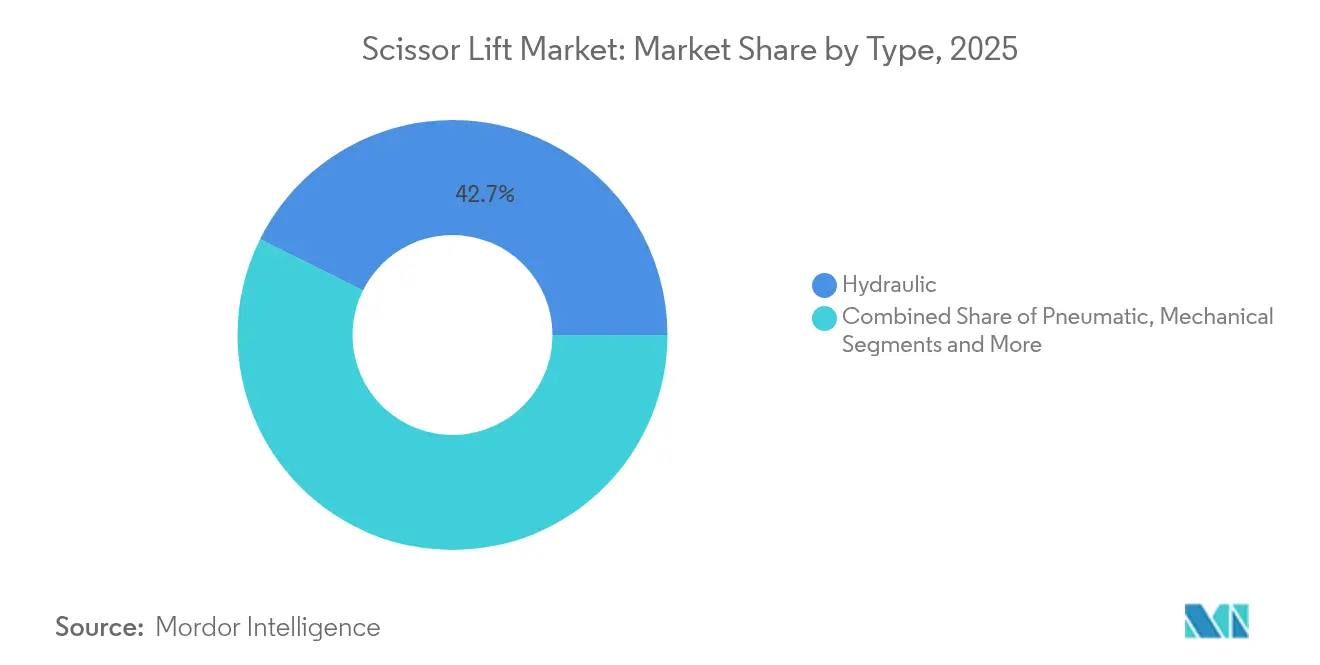

- By type, hydraulic units retained 42.65% of scissor lift market share in 2025, whereas electric platforms are expected to post the highest 6.15% CAGR through 2031.

- By mechanism, self-propelled products led with 60.55% scissor lift market share in 2025, while vehicle-mounted formats are projected to rise at a 5.74% CAGR.

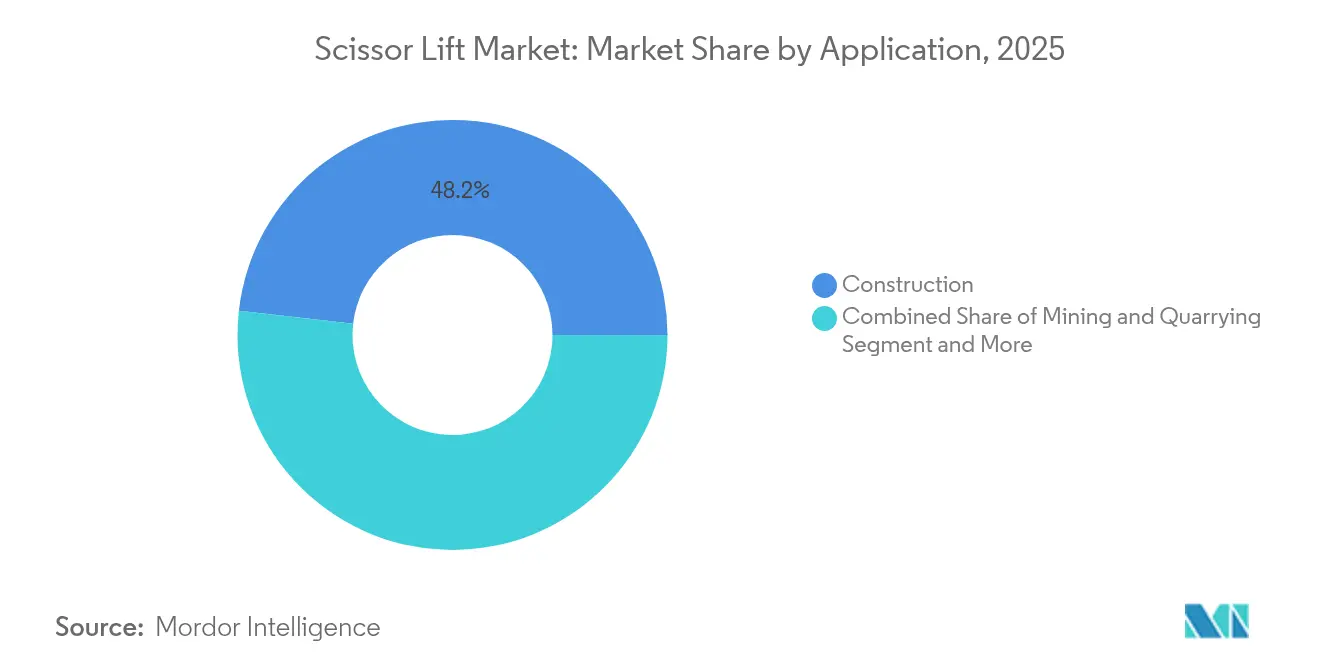

- By application, construction accounted for 48.20% of the scissor lift market size in 2025; logistics and warehousing are forecast to expand at 6.04% CAGR between 2026 and 2031.

- By working height, the 20–30 ft segment commanded 45.10% of the scissor lift market size in 2025, and units below 20 ft are set to grow at a 6.25% CAGR.

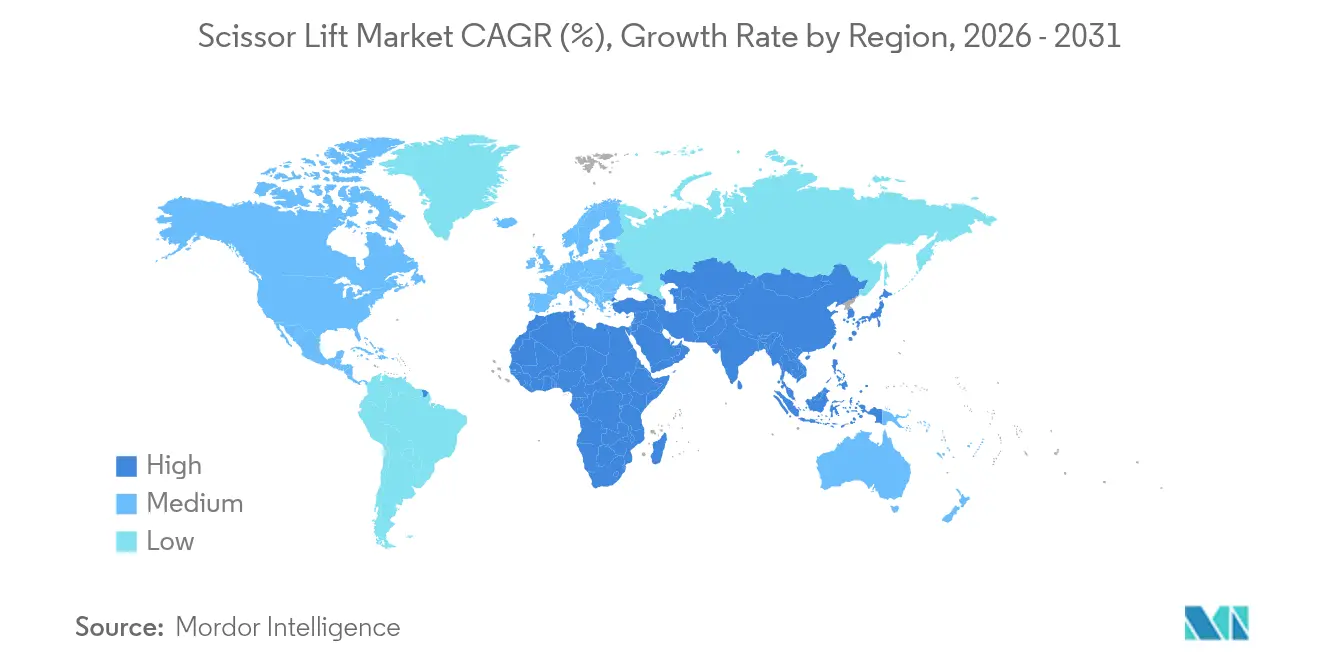

- By geography, North America captured 36.30% revenue in 2025, whereas Asia-Pacific is on track for the fastest 7.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Scissor Lift Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Construction and Infrastructure Pipeline | 1.8% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Warehouse Automation and E-Commerce Expansion | 1.2% | Global, strongest in North America & Europe | Short term (≤ 2 years) |

| Stricter Work-at-Height Safety Regulations | 0.9% | Global, led by developed markets | Long term (≥ 4 years) |

| Shift Toward Battery-Electric MEWPs | 0.7% | Europe & North America early adoption, APAC following | Medium term (2-4 years) |

| IoT-Enabled Fleet Analytics | 0.6% | North America & Europe rental markets | Short term (≤ 2 years) |

| Energy-Efficient Electromechanical Actuators | 0.4% | Global manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Construction & Infrastructure Pipeline

Megaproject activity fuels steady orders for mobile elevating work platforms across highways, bridges, and utility upgrades. United States put-in-place construction spending is set to hit USD 2.24 trillion in 2025 after a 4.1% year-on-year rise, helped by Infrastructure Investment and Jobs Act allocations that span more than 56,000 transport undertakings. Manufacturing construction is particularly robust owing to semiconductor and battery incentives, and power sector outlays are growing 13.1% as grids are strengthened for renewable energy integration. India mirrors this trajectory, lifting federal capital expenditure 11.1% to more than USD 100 billion for FY 2024-25 and relying on a workforce of 51 million to execute metro rail, highway, and housing programs. Such multi-year project pipelines give rental firms confidence to add inventory and keep utilization high, reinforcing healthy demand across the scissor lift market.[1]“Bipartisan Infrastructure Law Dashboard,” White House, whitehouse.gov

Warehouse Automation & E-Commerce Expansion

The number of U.S. warehouse establishments climbed 73% from 2001 to 2023 and continues to rise as omnichannel retailers chase last-mile delivery speed. Developers are shifting toward high-bay facilities that automate storage and retrieval, which drives orders for compact scissor lifts capable of maneuvering in narrow aisles. Industry studies indicate logistics real estate will require an additional 159 million sq ft of space by 2047, with Chinese third-party logistics providers already accounting for one-fifth of new U.S. leasing volume. Automation integrators like Witron prefer electric units because they emit no hydraulic vapor near sensitive robotic gear, further accelerating electrification within the scissor lift market.[2]“Value of Construction Put in Place,” United States Census Bureau, census.gov

Stricter Work-at-Height Safety Regulations

ANSI A92 rules, effective since 2020, classify scissor lifts under Group A equipment and oblige owners to adopt documented Safe Use Plans that encompass pre-shift inspections, gradeability limits, and rescue procedures. OSHA continues to treat scissor lifts as mobile scaffolds, triggering Subpart L compliance and specific fall-arrest measures when guardrails are inadequate. The International Powered Access Federation has launched refreshed training modules to help rental fleets certify operators at scale. Yet, elevated requirements are lengthening learning curves and intensifying replacement cycles for legacy machines that lack tilt sensors or load cells. Safety mandates bolster demand for modern platforms that integrate diagnostics, envelope monitoring, and telematics dashboards.[3]“Aerial Lifts and Scissor Lifts,” Occupational Safety and Health Administration, osha.gov

Shift Toward Battery-Electric MEWPs

Electric drive trains are gaining traction as contractors look to decarbonize job sites and improve indoor air quality. Genie offers lithium-ion packs on its GS E-Drive slab models, promising 10-year life spans and four-hour fast charging. Internal research confirms that electro-hydraulic systems cut energy draw by 10% and recapture power while the platform descends. China supplies roughly 80% of global electric construction equipment and continues to refine battery chemistries that push runtime higher and maintenance lower.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex/Battery-Replacement Cost | -1.1% | Global, strongest impact in emerging markets | Medium term (2-4 years) |

| Shortage of Certified MEWP Operators | -0.9% | North America & Europe acute, spreading globally | Long term (≥ 4 years) |

| Hydraulic Fluid Leaks and Maintenance Downtime | -0.8% | Global, particularly affecting older fleet operators | Short term (≤ 2 years) |

| Lithium-ion Raw-Material Price Volatility | -0.6% | Global supply chain dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hydraulic Fluid Leaks and Maintenance Downtime

Operators of legacy fleets remain vulnerable to unplanned stoppages caused by seal failure, contamination, and weather-induced viscosity swings. The Association of Equipment Management Professionals shows that businesses in the top maintenance quartile log fewer outages yet incur higher service labor hours, underscoring the cost trade-off. Environmental rules governing fluid disposal are tightening, pushing smaller contractors to favor electric alternatives that shed hydraulic circuits altogether. Until replacement cycles fully play out, maintenance burdens will dampen utilization in segments dominated by hydraulic scissor lifts.[4]“2023 Heavy Equipment Comparator,” Association of Equipment Management Professionals, aemp.org

Shortage of Certified MEWP Operators

Contractors report chronic hiring gaps, with 94% of firms unable to secure enough skilled hands. It has been estimated that 41% of today’s equipment operators may retire by 2031, widening the deficit. ANSI updates demand machine-specific training, which raises initial onboarding time. In pilot schemes, simulation programs have cut crane learning curves from six months to seven weeks. However, scaling such curricula industry-wide requires capital and instructor capacity, which many small firms lack. Until supply tightens, rental companies may face under-utilization of advanced models, slowing technology upgrades inside the scissor lift market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electric Uptake Challenges Hydraulic Dominance

Hydraulic units captured 42.65% revenue in 2025, a testament to proven reliability, rugged performance, and familiar maintenance practices. That said, electric variants are on a 6.15% CAGR track through 2031 as total cost of ownership advantages become quantifiable. Fleet trials show lithium-ion packs require no fluid checks and halve routine service hours, appealing to rental houses chasing higher uptime. Pneumatic and mechanical formats serve specialized roles where explosion safety or power independence is mandatory, yet their collective share remains minor.

OEM roadmaps now emphasize electric drivetrains. Genie’s lithium-ion option offers rapid charging and a 10-year warranty, matching project cycles for logistics developers. Research shows electro-hydraulic drives save 10% energy and harvest regenerative descent power. Indoor regulatory constraints encourage this shift, whereas heavy civil works in open terrain continue to rely on hydraulic robustness. The scissor lift market benefits as both technologies coexist, giving buyers a spectrum of price-performance choices.

By Mechanism: Self-Propelled Leadership Meets Vehicle-Mounted Momentum

Self-propelled platforms owned 60.55% of global revenue in 2025 due to their point-of-use mobility and compatibility with dense job sites. Design upgrades such as sealed AC motors and drive-at-full-height capability extend their appeal across installation, fit-out, and maintenance tasks. Vehicle-mounted designs are advancing at 5.74% CAGR because they combine transport and elevation in one asset, which is ideal for municipal utilities that service dispersed assets.

Trailer and unpowered formats fill cost-sensitive niches but face gradual attrition as labor expense rises. Manufacturers are localizing production to align with regional preferences; Genie expanded assembly in Umbertide, Italy, citing European appetite for rough-terrain units with flexible drive layouts. This evolution underscores how the scissor lift market adapts its mechanism choices to emerging mobility economics.

By Application: Construction Leads While Logistics Accelerates

Construction still commands 48.20% revenue, due to federal infrastructure initiatives, renewable power build-outs, and a resurgence in advanced manufacturing plants. Nonresidential megaprojects exceeding USD 1 billion now represent 18% of U.S. spending, ensuring long-cycle demand for mid-height access platforms.

Logistics and warehousing applications will grow 6.04% annually through 2031, driven by omnichannel distribution and automation. Developers prioritize narrow-aisle layouts that need compact units under 20 ft, while retrofits in brownfield properties call for lightweight models that avoid floor reinforcement. Specialized verticals such as mining, aviation, and utilities each require tailored safety features, but their combined volume remains smaller. Reliable, emissions-free operation ensures electric configurations dominate indoor hubs, reinforcing the diverse demand profile inside the scissor lift market.

By Working Height: Mid-Range Dominance and Compact Growth

Units rated 20–30 ft hold 45.10% of 2025 shipments because they satisfy most ceiling maintenance and façade finishing needs without complex stabilization. Their steel frame design balances reach and portability, making them the rental fleet staple. Equipment under 20 ft is on a 6.25% CAGR trajectory, benefiting from warehouse automation and retrofits in hospitals, data centers, and retail interiors where low point-loading is critical.

Manufacturers are launching micro accessories like Skyjack’s XStep to add incremental reach while retaining compact footprints. At the extreme, Dingli’s 37 m model pushes boundaries for stadium roofing and industrial pipe racks. Each height class now offers electric alternatives, ensuring that the scissor lift market serves the full span of elevation requirements with specialized configurations.

Geography Analysis

North America generated 36.30% of 2025 revenue due to a mature rental ecosystem and more than 2.00 trillion USD in total U.S. construction spending projected for 2025. Civil engineering outlays are tracking growth, and power-sector projects are expanding. United Rentals alone operates more than 205,000 aerial units. OSHA and ANSI frameworks accelerate replacement cycles, anchoring premium pricing for compliant models. Canada contributes incremental growth driven by transportation and LNG infrastructure, although commodity price swings introduce volatility.

Asia-Pacific is advancing at 7.09% CAGR through 2031, the quickest worldwide. India’s equipment sales rose as new Stage-V-equivalent emission rules nudged contractors to modernize fleets. Government infrastructure outlays of USD 133 billion for FY 2024-25 underpin sustained demand. China wrestles with property market headwinds, yet supplies 80% of global electric construction machinery, positioning its manufacturers favorably for export growth. Japan invests steadily in disaster-proofing and urban renewal, whereas South Korea’s shipyards drive localized demand for compact electric lifts.

Europe remains a mature yet innovation-oriented arena. Equipment sales slipped in 2024 amid higher borrowing costs, but rebound prospects from 2026 coincide with EU Green Deal retrofits that prioritize low-emission fleets. Germany, France, and the United Kingdom dominate volume, while Eastern Europe offers opportunities tied to rail and energy corridor upgrades. High safety standards and well-capitalized rental groups secure an enduring revenue base for the scissor lift market across the continent.

Competitive Landscape

The scissor lift market shows moderate concentration anchored by JLG Industries, Genie, and Haulotte, firms that bundle diversified portfolios with global service parts networks. JLG broadened its domain by purchasing Hinowa and AUSA, gaining tracked aerial platforms suitable for soft-ground solar farms and tight urban alleys.

Chinese entrants Zhejiang Dingli and Sinoboom leverage cost and battery supply advantages and now target export channels in the Middle East, Eastern Europe, and Latin America. Their latest offerings ship with lithium-ion packs and on-board telematics, narrowing the technology gap with incumbents. Specialty opportunities persist for firms that can engineer explosion-proof, clean-room, or extreme-cold variants.

Digitization is the next battleground. Genie’s most of the parts has commonality across six new models cuts downtime and simplifies inventory, while integrated sensors feed predictive analytics that rental houses use to negotiate uptime guarantees. Incumbents that scale such services are poised to defend their share against low-cost challengers that compete primarily on upfront price. Competitive intensity is a function of innovation cadence, compliance certification, and aftermarket reach.

Scissor Lift Industry Leaders

JLG Industries, Inc.

Genie

Skyjack

Haulotte Group

Zhejiang Dingli Machinery

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Genie launched six new slab scissor lift models (GSTM-1932, GS-2632, GS-3232, GS-2646, GS-3246, GS-4046), featuring a curved linkage design, enhanced chassis rust protection, and 70% parts commonality to cut ownership costs.

- September 2024: Skyjack introduced the micro XStep accessory for its SJ3213 micro and SJ3219 micro lines. This accessory grants an extra 19 inches of working height while maintaining a 250-pound capacity for confined spaces.

- June 2024: Dingli and Hire Safe Solutions unveiled the 3730HRT, the tallest scissor lift worldwide with a 37-meter working height and a 750-kg platform capacity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global scissor lift market as all new self-propelled, vehicle-mounted, trailer-mounted, and push-around platforms that raise a work deck through a crisscross scissor mechanism for tasks in construction, logistics, aviation, utilities, and industrial maintenance. According to Mordor Intelligence analysts, these units generated USD 3.51 billion in revenue during 2025.

Scope Exclusions: Articulated boom lifts, vertical mast lifts, and pure rental service fees not tied to equipment ownership remain outside the scope.

Segmentation Overview

- By Type

- Hydraulic

- Pneumatic

- Mechanical

- Electric

- By Mechanism

- Unpowered

- Self-propelled

- Vehicle-mounted

- Trailer-mounted

- By Application

- Construction

- Mining and Quarrying

- Logistics and Warehousing

- Manufacturing and Industrial

- Government and Utilities

- Aviation and Airports

- Other Applications

- By Working Height

- Less than 20 ft

- 20 to 30 ft

- 30 to 40 ft

- More than 40 ft

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured discussions with rental fleet directors, OEM product managers, and certified MEWP trainers across North America, Europe, China, and the Gulf. These experts validated utilization rates, battery replacement cycles, and regional mark-ups, letting us sharpen assumptions and close gaps left by desk work.

Desk Research

We first mine publicly available evidence. Safety records from OSHA, ANSI A92 rulebooks, International Powered Access Federation fleet censuses, UN Comtrade HS842890 trade data, and construction spending from the US Census Bureau or Eurostat anchor volume, regulatory, and end-use indicators.

Company 10-Ks, investor decks, patent listings accessed through Questel, and global news collected via Dow Jones Factiva refine price curves, battery chemistry shifts, and model launches that influence average selling prices. The sources named are illustrative; many additional public and subscription datasets informed data capture, validation, and clarification.

Market-Sizing & Forecasting

The top-down build starts with regional construction put-in-place, warehouse floor additions, and powered-access rental penetration, which are then converted into height-wise demand pools. Selective bottom-up checks roll sampled OEM shipments with blended ASPs and fleet age profiles to corroborate totals. Key variables include ANSI A92 enforcement timelines, lithium-ion battery cost indices, urban high-rise completions, and average fleet retirement age. A multivariate regression model projects 2025-2030 values, while scenario bands address data uncertainty.

Data Validation & Update Cycle

Outputs pass three rounds of peer review; variance flags trigger re-checks with respondents, and anomalies are reconciled against independent signals before sign-off. Mordor Intelligence refreshes each model annually and issues mid-cycle updates when material events, such as tariff shifts, alter unit economics.

Why Our Scissor Lift Baseline Earns Decision-Maker Trust

Published estimates often diverge because firms adopt different scopes, base years, and pricing ladders. Our disciplined scope selection, yearly refresh, and dual-path modeling keep such gaps minimal.

Key gap drivers observed elsewhere include blending other aerial platforms, relying only on shipment data, or projecting uniform ASP erosion that ignores lithium volatility.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.51 Bn (2025) | Mordor Intelligence | - |

| USD 3.43 Bn (2024) | Global Consultancy A | Combines vertical mast lifts with scissor units and uses shipments only |

| USD 3.54 Bn (2024) | Trade Journal B | Omits rental revenue and applies pre-Covid ASP benchmarks |

The comparison shows that our carefully bounded, frequently refreshed baseline sits between wider definitions and narrow cost views, giving buyers a transparent figure they can map to real procurement and investment decisions.

Key Questions Answered in the Report

What is the current size of the scissor lift market in 2026?

The scissor lift market size is USD 3.71 billion in 2026.

How fast is the scissor lift market expected to grow?

The market is projected to register a 5.78% CAGR and reach USD 4.92 billion by 2031.

Which power system segment is growing the quickest?

Electric scissor lifts are forecast to expand at a 6.15% CAGR through 2031.

Why are electric scissor lifts gaining popularity?

They eliminate hydraulic fluid maintenance, cut energy use by 10%, and comply with emission limits in indoor sites.

Which region will witness the fastest demand growth?

Asia-Pacific is set to grow at a 7.09% CAGR due to rising infrastructure spending in India and technology adoption in China.

What is the main restraint facing the scissor lift market?

The high cost of battery replacement, especially for small and midsize enterprises, is expected to reduce the overall CAGR.

Page last updated on: