GCC Forklift Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

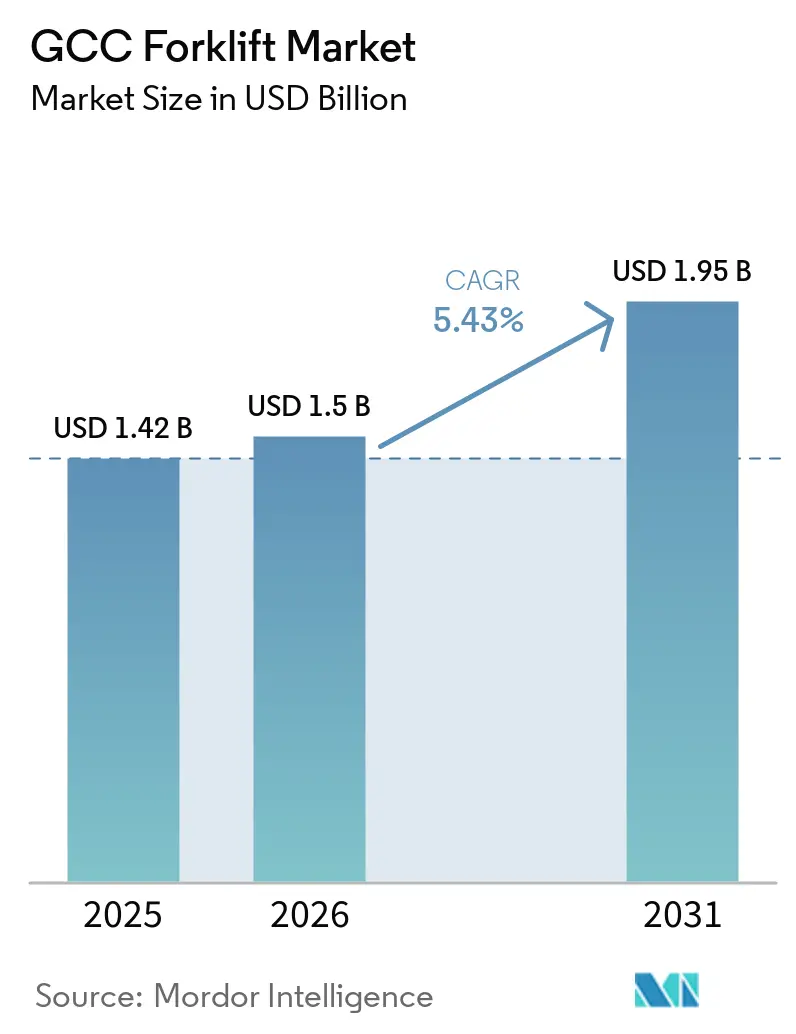

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 1.95 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Forklift Market Analysis by Mordor Intelligence

The GCC forklift market size is expected to increase from USD 1.42 billion in 2025 to USD 1.50 billion in 2026 and reach USD 1.95 billion by 2031, growing at a CAGR of 5.43% over 2026-2031. Fleet renewal is shifting toward infrastructure-led demand as sovereign programs decouple equipment orders from crude-price cycles, with Saudi Arabia’s Vision 2030 projects pulling deliveries forward and shortening replacement windows. Lithium-ion total-cost-of-ownership economics now undercut lead-acid, reinforcing an electric-first mindset that is embedded in incentive schemes such as the Kingdom’s 20% capital-cost rebate and the UAE Clean Energy Strategy 2050. E-commerce fulfillment density is reshaping warehouse design, driving the uptake of narrow-aisle electric riders and order-pickers that improve cubic utilization in high-rent urban hubs. Moderate competitive intensity prevails: global original-equipment manufacturers (OEMs) defend premium share through service contracts and rapid-parts logistics, while Chinese challengers win cost-sensitive customers by localizing assembly hubs and warranty support.

Key Report Takeaways

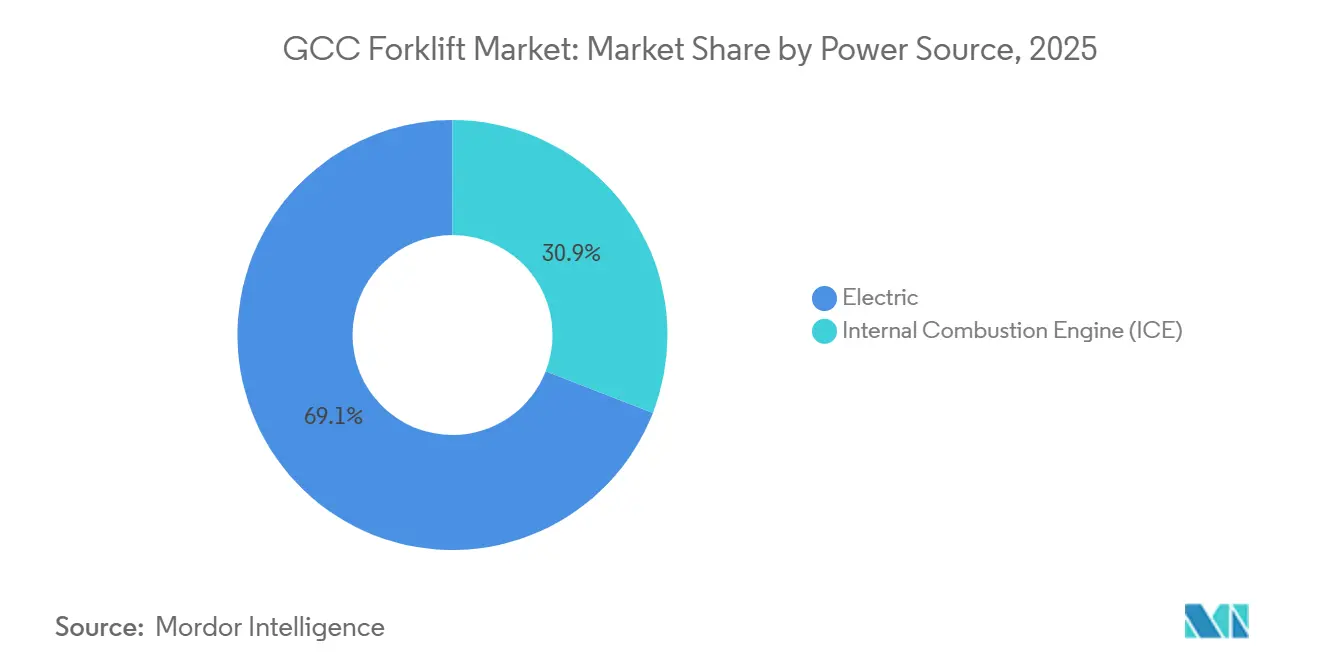

- By power source, electric forklifts accounted for 69.13% share of the GCC forklift market size in 2025 and are advancing at a 7.34% CAGR through 2031.

- By forklift class, Class 4/5 accounted for 43.55% share in 2025, while Class 1 electric rider trucks are set to expand with 8.04% CAGR between 2026 and 2031.

- By tonnage capacity, the 5-10 ton band commanded 60.03% of GCC forklift market share in 2025, while the above 10 ton category is set to grow at a 5.94% CAGR.

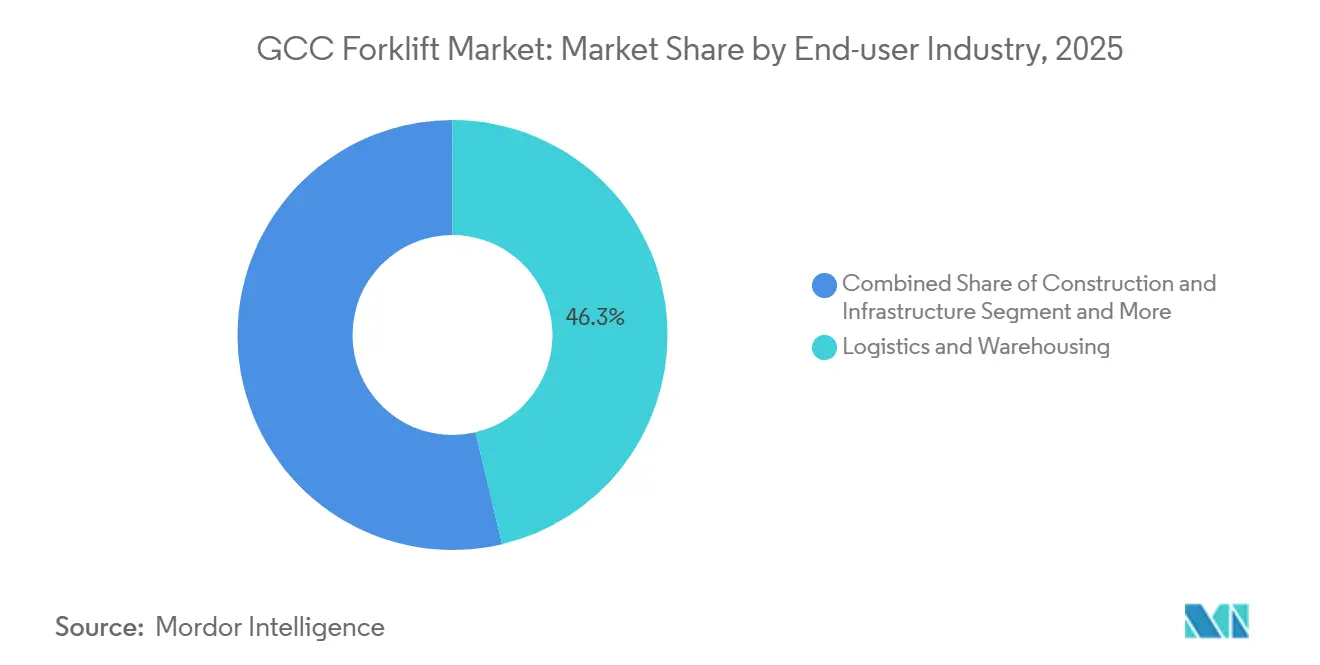

- By end-user industry, logistics and warehousing represented 46.31% of the GCC forklift market size in 2025 and is projected to grow at 6.21% through 2031.

- By product type, counterbalanced models held 68.15% share in 2025, while the warehouse trucks are advancing at a 7.61% CAGR over 2026-2031.

- By geography, Saudi Arabia led with 38.06% of the GCC forklift market share in 2025, and will grow at a 6.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Forklift Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega GCC Infrastructure Projects | +1.8% | Saudi Arabia, United Arab Emirates, Qatar | Medium term (2-4 years) |

| E-commerce-led Warehouse Boom | +1.5% | Saudi Arabia, United Arab Emirates | Short term (≤ 2 years) |

| Electric and Li-ion Forklift Shift | +1.3% | GCC-wide | Long term (≥ 4 years) |

| 3PL and Cold-chain Expansion | +0.9% | United Arab Emirates, Saudi Arabia | Medium term (2-4 years) |

| Free-zone Port Corridors | +0.7% | United Arab Emirates, Saudi Arabia, Oman | Medium term (2-4 years) |

| Autonomous Fulfillment Centers | +0.6% | Saudi Arabia, United Arab Emirates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mega GCC Infrastructure Projects (Vision 2030 et al.)

Saudi Arabia's NEOM Port, backed by a significant investment, is set to revolutionize its operations. Phase 1 will see the installation of automated ship-to-shore cranes, complemented by numerous support forklifts. In a significant shift, the port is compressing the typical multi-year equipment replacement cycle into a much shorter purchasing window. Meanwhile, logistics for the Red Sea Project and the construction of the Qiddiya entertainment city are securing multi-year leases with local distributors. This strategy not only ensures uptime commitments but also skews procurement towards original equipment manufacturers (OEMs) that boast in-country service hubs. Furthermore, global brands, with their promise of expedited parts delivery, are seizing this heightened urgency, successfully capturing orders that sidestep the conventional spot purchasing methods historically linked to oil revenue.

E-commerce-led Warehouse Boom

Amazon operates a large fulfillment center in Riyadh, while KEZAD manages an expansive logistics park, both secured under long-term contracts spanning a decade[1]“Riyadh Fulfillment Center Goes Live,” LOGISTICS MIDDLE EAST, logisticsmiddleeast.com. These contracts shield equipment demand from the volatility of oil prices. With the rising expectations for same-day deliveries, forklift density has significantly increased, making lithium-ion models, especially those with opportunity-charging capabilities, the top choice. As urban land costs climb, there's a pronounced push towards vertical storage. This trend has subsequently boosted the volumes of reach-trucks and order-pickers in the GCC forklift market.

Shift Toward Electric and Li-ion Forklifts

Saudi Arabia's rebate is accelerating the adoption of electric vehicles, and the long cycle life of lithium-ion batteries is justifying their higher initial costs. DP World has placed a tender for electric reach stackers, specifically choosing lithium-iron-phosphate batteries that can operate in high-temperature conditions. However, a significant portion of warehouses still require panel upgrades, which can extend lead times considerably. For fleet managers who aren't well-versed in electrical codes, turnkey electrification packages that combine equipment, chargers, and grid permits make the procurement process much more straightforward.

3PL and Cold-chain Expansion

At its Jeddah site, RSA Cold Chain mandates heated-cab forklifts, certified under HACCP and ISO 22000 standards. This specialized niche is predominantly held by industry leaders Crown and Jungheinrich. Meanwhile, NewCold's foray into the United Arab Emirates and Qatar showcases a blend of automation, integrating robotic pallet shuttles alongside human-operated forklifts. In a significant move, Agility's regional consolidation has rolled out electric forklift replacements across multiple nations, underscoring their emphasis on uptime—a priority that justifies price premiums over standard economy models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price CAPEX Cyclicality | -0.8% | Saudi Arabia, United Arab Emirates, Kuwait | Short term (≤ 2 years) |

| Forklift-operator Skills Shortage | -0.6% | GCC-wide | Medium term (2-4 years) |

| Desert Climate Accelerates TCO | -0.5% | Saudi Arabia, United Arab Emirates, Qatar | Long term (≥ 4 years) |

| Fragmented Battery-recycling Rules | -0.3% | GCC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oil-price CAPEX Cyclicality

Saudi Aramco's decision to reduce its capital budget for 2026 signals a trend: petrochemical and oil-field contractors tend to postpone upgrades whenever Brent prices decline. This shift has extended their replacement cycles to a decade. Meanwhile, OEMs are turning to operating leases tied to crude indices, aiming to bring stability to the GCC forklift market.

Forklift-operator Skills Shortage

In 2025, job postings increasingly highlighted the requirement for certified candidates, which led to a rise in wage expectations across the industry. The fragmentation of cross-border licenses further exacerbated workforce turnover, creating challenges for employers in retaining skilled operators. To address these issues, companies began adopting semi-automated driver assistance technologies and implementing bundled training contracts to attract and retain talent while ensuring operational efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Electrification Outpaces Diesel Economics

Electric forklifts held 69.13% share in 2025 and grew at 7.34% through 2031, underscoring the GCC forklift market shift toward lithium-ion economics. At Duqm Port, grid limitations led to the specification of diesel forklifts in 2025, underscoring the continued importance of internal-combustion units in outdoor settings. Battery-swap clauses, which transfer degradation costs to OEMs, help mitigate residual-value risks. Meanwhile, hydrogen fuel-cell trials at KAUST suggest a potential third pathway for the future.

Fleet operators are balancing the penalties of desert heat against capital rebates, favoring suppliers with local battery-refurbishment programs that complete the lifecycle loop. In the GCC forklift market, Chinese brands are gaining a competitive advantage by partnering with Dubatt, effectively reducing midlife replacement costs.

By Forklift Class: Narrow-aisle Electric Riders Gain Share

Class 4/5 cushion and pneumatic units retained 43.55% share in 2025, but Class 1 electric riders posted the fastest 8.04% CAGR. Amazon’s Riyadh hub deployed several narrow-aisle units to double storage density, underscoring how warehouse layouts influence class selection. Class 3 pallet trucks also rise as labor regulators tighten ergonomic standards, converting manual jacks into powered models.

In port yards, Diesel Class 4/5 units are still essential. NEOM's gravel surfaces and the weights of containers necessitate the use of rough-terrain forklifts. With emission regulations on the horizon in 2027, diesel prices are expected to increase. This potential change is likely to hasten the shift towards electric forklifts in the GCC market.

By Tonnage Capacity: Heavy-lift Demand Tracks Port Expansions

The 5-10-ton segment captured 60.03% share in 2025, fueled by container-yard moves at Jebel Ali and Hamad Port. Above-10-ton forklifts grow 5.94% as automated cranes still need landside support for oversize cargo. Sub-5-ton models dominate retail and light industry, where indoor air quality dictates electric operation.

Construction contractors remain faithful to 7-10-ton diesel units, while petrochemical turnarounds demand 18-25-ton explosion-proof models. This specialization funnels heavy-lift spending toward premium OEMs with engineering depth, consolidating high-tonnage share within the GCC forklift market.

By End-user Industry: Logistics Dominates, Manufacturing Lags

Logistics and warehousing accounted for 46.31% share in 2025 and will lead at 6.21% CAGR, driven by 3PL consolidation and e-commerce SLAs. Construction faces tender delays that shorten buying windows, while manufacturing remains stable but stagnant as automation replaces manual tasks.

Retailers are transitioning to electric fleets to adhere to indoor emission regulations. Meanwhile, petrochemical giants set the ATEX Zone 1 standards, a benchmark that mid-tier brands find challenging to meet. As airports modernize, they spur a rising demand for electric fleets, broadening the GCC forklift market's reach into unconventional sectors.

By Product Type: Warehouse Trucks Gain on Fulfillment Density

Counterbalanced forklifts retained 68.15% share in 2025, yet warehouse trucks logged 7.61% CAGR as land-scarce e-commerce hubs adopt vertical racking. Reach trucks lift to 14 meters in 2.7-meter aisles, a configuration that halves real-estate cost per pallet. Counterbalanced models anchor port fleets where outdoor durability and high tonnage remain critical.

In the GCC forklift market, warehouse trucks are leading the shift toward electrification, while counterbalanced trucks are progressing at a slower pace. OEMs with extensive warehouse portfolios are experiencing significant growth, compelling generalists to innovate with financing solutions and multi-year service bundles.

Geography Analysis

Saudi Arabia secured 38.06% share in 2025 and posted the region’s fastest 6.58% CAGR to 2031 on the back of Vision 2030 megaprojects. NEOM and Red Sea timelines compress fleet turnover, while an electric rebate speeds lithium-ion uptake. Summer peaks above 45 °C trim battery range by 23%, prompting costly climate-controlled charging rooms and steering operators toward automated guidance that reduces driver skill dependency.

Jebel Ali's ramp-up and KEZAD's long-term 3PL leases, which shield orders from oil fluctuations, anchor the United Arab Emirates in second place. The United Arab Emirates's recycling infrastructure offers operators a cost advantage on closed-loop batteries compared to their export-reliant neighbors. Chinese OEMs establishing service hubs in Dubai have reduced parts lead times, diminishing the premium gap with established players and broadening the GCC's forklift market presence.

Qatar, Kuwait, Oman, and Bahrain account for the rest. Qatar's North Field LNG and Hamad Port expansion fuel a demand for forklifts. Meanwhile, Kuwait holds off on tenders due to budget constraints. Oman's Duqm Port is acquiring diesel forklifts, awaiting its power substation's completion in 2027. Bahrain's new logistics park in Hidd is transitioning to electric fleets, aligning with regional sustainability mandates. While SASO's 2026 technical regulation streamlines safety standards, it imposes a compliance cost per unit, easing cross-border transactions within the GCC forklift market [2]“SASO Issues Lifting-Equipment Regulation,” SASO, saso.gov.sa .

Competitive Landscape

Global OEMs, such as Toyota, KION, Jungheinrich, Crown, and Hyster-Yale, maintain a stronghold in the market through premium positioning and reliable service guarantees. Chinese manufacturers, including Hangcha, HELI, BYD, and EP Equipment, are steadily expanding their presence by offering competitive pricing and establishing localized hubs, such as Hangcha’s center in Jebel Ali. Other players, like Mitsubishi Logisnext, Doosan, Manitou, and CAT Lift Trucks, focus on specialized applications and flexible financing solutions to cater to niche demands.

Electrification and service bundling are shaping the strategies of key market participants. Kanoo Machinery’s Combilift, for example, offers leasing models that integrate equipment, maintenance, and training over multi-year periods, helping buyers manage costs effectively. BYD uses closed-loop recycling to cut lifecycle expense, evidenced by SANY’s 40-unit electric deal in Qatar—the region’s largest single order [3]“Largest Electric Forklift Order in the Gulf,” SANY, sanyglobal.com.

Automation is also influencing purchasing decisions, with API-enabled telematics becoming a critical factor. OEMs that adopt open software protocols are better positioned to address the evolving needs of the market and ensure long-term relevance. These advancements are expected to play a pivotal role in shaping the future of the GCC forklift market.

GCC Forklift Industry Leaders

Toyota Industries Corporation (Toyota Material Handling)

KION Group AG

Jungheinrich AG

Crown Equipment Corporation

Hyster-Yale Materials Handling, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Qatar’s Jaidah Group introduced the Baoli KBD160S diesel forklift with 16-ton capacity to serve heavy industrial clients.

- December 2025: HULKMAN delivered two FD70 diesel forklifts to a Saudi customer, emphasizing design commonality for easy maintenance.

- September 2025: SANY shipped 40 electric forklifts to a Qatari logistics operator, the Middle East’s largest single electric-forklift contract.

- May 2025: Dayim Equipment Rental received the first batch of Hangcha forklifts from a USD 15 million order to expand multi-country rental fleets.

GCC Forklift Market Report Scope

The scope includes segmentation by power source (internal combustion engine and electric), forklift class (class 1 - electric rider, class 2 - electric narrow-aisle, class 3 - electric hand/rider, and class 4/5 - ICE cushion and pneumatic), tonnage capacity (below 5 ton, 5-10 ton, and above 10 ton), end-user industry (logistics and warehousing, construction and infrastructure, manufacturing (discrete and process), retail and wholesale, oil and gas/petrochemicals, and others (food-cold chain, airports)), and product type (counterbalanced forklifts, and warehouse trucks (reach, order-picker, pallet)). The analysis also covers country-level segmentation, including Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain. Market size and growth forecasts are presented by value in USD and by volume in units.

| Internal Combustion Engine (ICE) |

| Electric |

| Class 1 - Electric Rider |

| Class 2 - Electric Narrow-aisle |

| Class 3 - Electric Hand/Rider |

| Class 4/5 - ICE Cushion and Pneumatic |

| Below 5 Ton |

| 5 - 10 Ton |

| Above 10 Ton |

| Logistics and Warehousing |

| Construction and Infrastructure |

| Manufacturing (Discrete and Process) |

| Retail and Wholesale |

| Oil and Gas/Petrochemicals |

| Others (Food-cold Chain, Airports) |

| Counterbalanced Forklifts |

| Warehouse Trucks (Reach, Order-picker, Pallet) |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Power Source | Internal Combustion Engine (ICE) |

| Electric | |

| By Forklift Class | Class 1 - Electric Rider |

| Class 2 - Electric Narrow-aisle | |

| Class 3 - Electric Hand/Rider | |

| Class 4/5 - ICE Cushion and Pneumatic | |

| By Tonnage Capacity | Below 5 Ton |

| 5 - 10 Ton | |

| Above 10 Ton | |

| By End-user Industry | Logistics and Warehousing |

| Construction and Infrastructure | |

| Manufacturing (Discrete and Process) | |

| Retail and Wholesale | |

| Oil and Gas/Petrochemicals | |

| Others (Food-cold Chain, Airports) | |

| By Product Type | Counterbalanced Forklifts |

| Warehouse Trucks (Reach, Order-picker, Pallet) | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

How large will the GCC forklift market be by 2031?

It is forecast to reach USD 1.95 billion by 2031, expanding at a 5.43% CAGR from 2026 to 2031.

Which segment is growing fastest in the GCC forklift market?

Class 1 electric rider trucks post the highest growth at an 8.04% CAGR between 2026 and 2031.

Why are electric forklifts gaining share in Gulf countries?

Lithium-ion economics now beat lead-acid on five-year total cost, and Saudi Arabia’s 20% rebate plus UAE clean-energy policies accelerate adoption.

What drives forklift demand in Saudi Arabia?

Vision 2030 infrastructure projects, such as NEOM Port and rapid e-commerce warehouse expansion, compress replacement cycles and boost orders.

Page last updated on: