Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

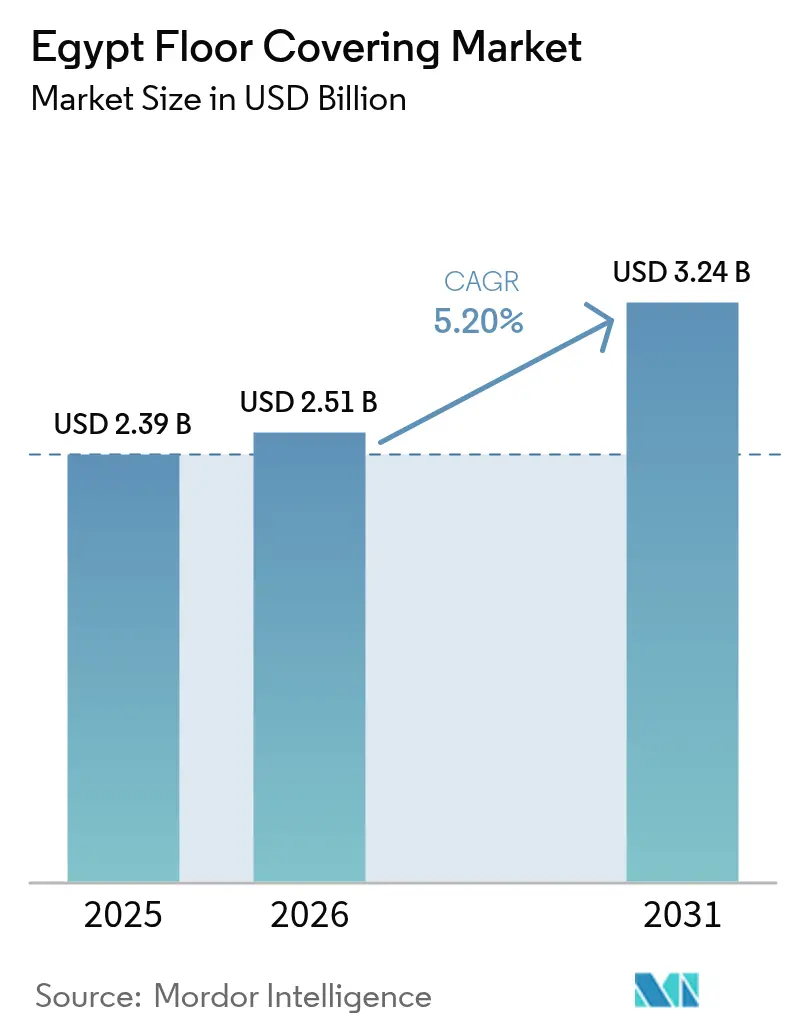

| Base Year Market Size (2025) | USD 2.39 Billion |

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 3.24 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

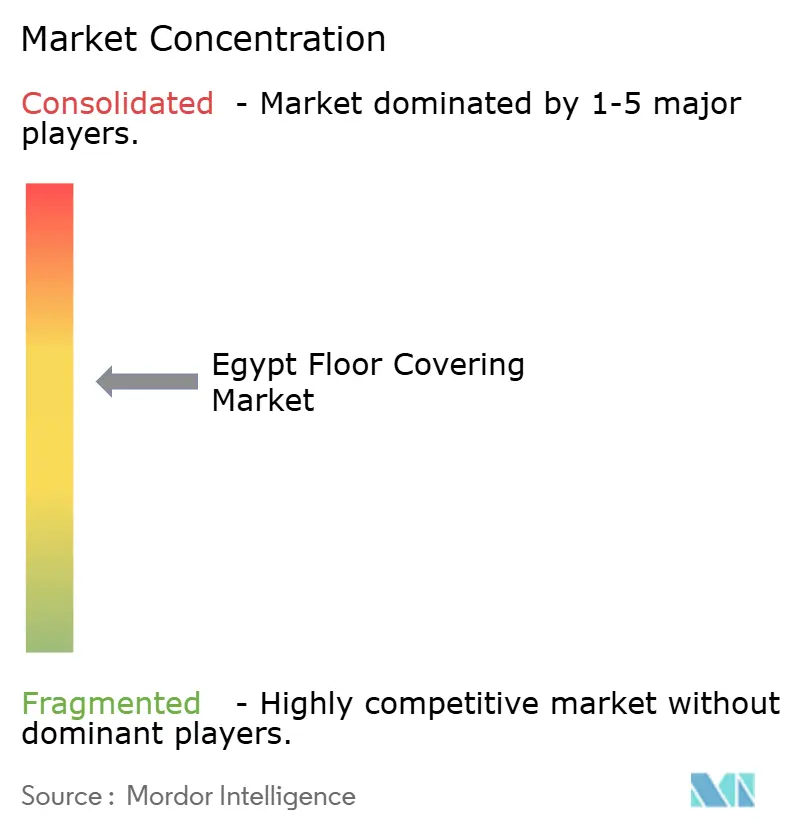

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Floor Covering Market Analysis by Mordor Intelligence

Egypt Floor Covering Market size in 2026 is estimated at USD 2.51 billion, growing from 2025 value of USD 2.39 billion with 2031 projections showing USD 3.24 billion, growing at 5.20% CAGR over 2026-2031.

Robust government housing programs, the tourism boom along the Red Sea, and accelerated commercial real-estate investments are anchoring demand across product categories. The Egypt floor covering market also benefits from the country’s status as Africa’s largest ceramic-tile producer, giving local manufacturers a structural cost advantage that shields them from most import-related price shocks[1]Source: Housing and Building National Research Center, “Assessment of Some Locally Produced Egyptian Ceramic Wall Tiles,” tandfonline.com. . According to the JLL Egypt Construction Market Intelligence Report (Q1 2024), Construction activity recorded an 8.00% CAGR in 2024 -2025, underpinned by roughly USD 515 billion in unawarded regional projects that are progressively moving to contract award and breaking ground. Parallel growth in hospitality, exemplified by IHG’s pipeline of 21 hotels and Hilton’s plan to more than triple its Egyptian footprint, continues to pull premium specifications into the procurement mix. Finally, Egypt’s strategic location and regional free-trade agreements keep the Egypt floor covering market competitive in exports, with carpets and textile floor coverings reaching USD 28 million in 2023, primarily to African neighbors.

Key Report Takeaways

- By product type, carpet and rugs held 41.12% of the Egypt floor covering market share in 2025, while resilient floor covering is forecast to advance at an 8.09% CAGR through 2031.

- By construction type, renovation and replacement captured 64.02% of the Egypt floor covering market size in 2025; new construction is set to expand at a 7.06% CAGR to 2031.

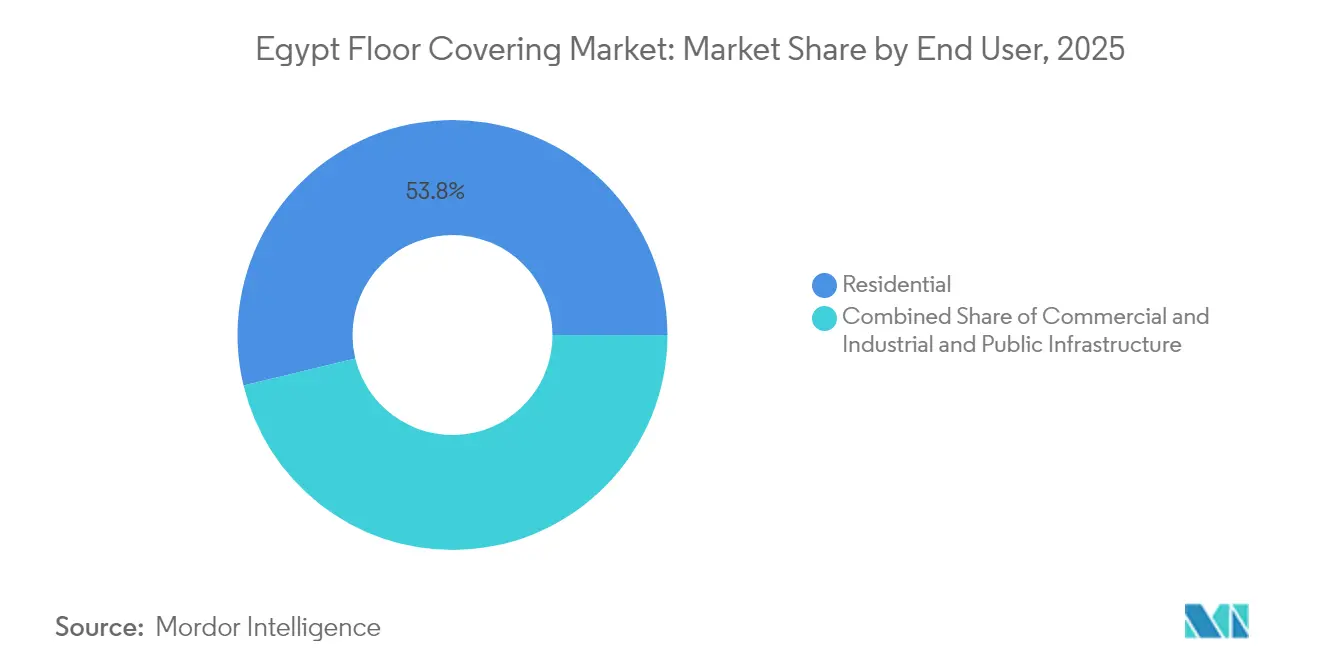

- By end user, residential maintained a 53.78% share in 2025, whereas commercial applications are progressing at a 6.55% CAGR through 2031.

- By distribution channel, B2C retail dominated with 69.34% value share in 2025, yet B2B contractors and dealers are forecast to post an 8.22% CAGR up to 2031.

- By geography, Greater Cairo & Giza led with 39.86% revenue share in 2025, while the Red Sea Governorates are poised for the fastest 8.63% CAGR through 2031

- Leading players such as Oriental Weaver, Cleopatra Ceramics, Tarkett S.A., Mohawk Industries, and RAK Ceramics hold major market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of government-backed housing megaprojects | +1.8% | New Administrative Capital, new cities | Medium term (2-4 years) |

| Tourism-led hotel & resort refurbishments along the Red Sea | +1.2% | Red Sea coast, North Coast, Cairo metro | Short term (≤2 years) |

| Retail and mall expansion in tier-2 cities creating new flooring demand | +0.9% | Alexandria, Giza, Suez Corridor | Medium term (2-4 years) |

| Climate-resilient, heat-tolerant materials gaining preference | +0.7% | Upper Egypt, desert regions | Long term (≥4 years) |

| Massive infrastructure and transport-hub build-outs | +1.1% | National corridors, logistics zones | Medium term (2-4 years) |

| Growth in educational construction and renovation | +1.3% | Greater Cairo, Delta region, Assiut | Short to Medium (1–3 yrs) |

| Source: Mordor Intelligence | |||

Expansion of Government-Backed Housing Megaprojects

The New Administrative Capital alone embodies a USD 45 billion commitment that will require more than 1.5 million m² of flooring across government buildings, residential compounds, and mixed-use districts. Similar urban centers underway in Alamein, Mansoura, and 6th of October City embed flooring specifications into public tenders, effectively guaranteeing volume orders for established tile and resilient-flooring suppliers. Large lot purchases allow domestic producers to amortize energy costs and upgrade kiln technology, thereby cementing a cost-per-square-meter advantage that smaller regional competitors struggle to match. The Egypt floor covering market thus capitalizes on scale economics, while public procurement rules emphasize local content and fast delivery schedules that raise barriers to importers. Contractors operating in these megaprojects increasingly select climate-appropriate ceramic grades and luxury vinyl tile (LVT) that tolerates thermal cycling.

Tourism-Led Hotel & Resort Refurbishments Along the Red Sea

Hospitality chains continue to set higher aesthetic and durability benchmarks. IHG and Hilton collectively target more than 40 new hotels by 2030, translating into roughly 750,000 m² of premium flooring demand in the short term. Project owners require anti-slip, salt-air-resistant surfaces that can be installed with minimal downtime, prompting a shift toward modular LVT, porcelain slabs, and engineered-stone composites. The Egypt floor covering market benefits because domestic tile plants have added high-definition digital printing and rectification lines, enabling them to supply luxury specifications at sub-import prices. Suppliers able to certify products to LEED or EDGE environmental standards secure preferred-vendor status on resort developments, further reinforcing market share.

Retail and Mall Expansion in Tier-2 Cities Creating New Flooring Demand

Modern retail footprints in Alexandria, Giza, and Suez Canal governorates now cluster around mall projects ranging from 50,000 to 100,000 m². Each development typically allocates 25% of gross built-up area to common zones that call for high-traffic porcelain, terrazzo, or rigid-core vinyl. Developers also earmark feature zones for polished-concrete or micro-topping systems that deliver contemporary aesthetics at lower lifecycle cost. As these investors diversify beyond Cairo, the Egypt floor covering market spreads geographically and creates sales pipelines for distributors with multi-city logistics coverage. In parallel, omnichannel retail formats integrate in-store pickup areas whose repeated pallet movement necessitates heavy-duty resilient flooring.

Climate-Resilient and Heat-Tolerant Materials Gaining Preference

Egypt's extreme climate conditions are accelerating the adoption of advanced flooring materials designed to withstand temperature fluctuations, UV exposure, and thermal expansion challenges. The growing preference for climate-resilient materials reflects lessons learned from traditional flooring failures in Egypt's harsh environment, where summer temperatures exceed 40°C and thermal cycling causes material degradation. Luxury vinyl tile (LVT) and stone plastic composite (SPC) products are gaining traction due to their dimensional stability and resistance to thermal expansion, particularly in commercial applications where air conditioning costs make temperature control expensive.[2]Source: Floor Daily, “Rigid LVT Continues to Evolve,” floordaily.net. The UAE's commitment to a 31% carbon emission reduction by 2030 is influencing regional building standards, with Dubai's leadership in LEED-certified projects creating spillover effects in Egyptian construction practices. This trend is driving innovation in locally-sourced materials, including date palm-based flooring solutions showcased at Index Dubai 2024, which offer natural heat resistance and sustainability credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency-driven volatility in imported wood costs | –1.4% | National premium segments | Short term (≤2 years) |

| Price competition from low-cost ceramic tiles | –0.8% | Budget residential, mass retail | Medium term (2-4 years) |

| Limited local manufacturing capacity restricting large-scale export opportunities | –0.6% | National | Long term (≥4 years) |

| Shortage of skilled installers outside metro areas | –0.5% | Rural and tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency-Driven Volatility in Imported Wood Costs

The Egyptian pound's devaluation against major currencies is creating unprecedented cost pressures for flooring manufacturers and distributors relying on imported raw materials. Research indicates that currency depreciation leads to inflation exceeding 37%, with wood flooring and laminate products experiencing disproportionate price increases due to their import dependency. The purchasing power parity method suggests a fair exchange rate of EGP 38.5 per USD, significantly different from current market rates, creating ongoing uncertainty for project planning and pricing strategies. This volatility is forcing manufacturers to explore alternative supply chains and accelerate domestic raw material sourcing, though Egypt's limited forestry resources constrain local wood availability. The currency challenge is particularly acute for premium residential projects where imported hardwood and engineered wood products command higher margins but face increasing price sensitivity from developers and end consumers.

Price Competition from Low-Cost Ceramic Tiles

Egypt's position as Africa's largest ceramic tile producer has created intense price competition that pressures profit margins across the flooring value chain. Domestic ceramic manufacturers benefit from abundant low-cost raw materials and established production infrastructure, enabling aggressive pricing strategies that challenge imported alternatives and premium domestic products. The availability of high plastic clays as alternatives to imported bentonite clay is further reducing production costs and enhancing price competitiveness in the ceramic segment. This pricing pressure is forcing non-ceramic flooring manufacturers to emphasize value-added features such as installation ease, durability, and design flexibility to justify premium pricing. The competitive intensity is particularly challenging for resilient flooring products that must compete against ceramic tiles in cost-sensitive residential and commercial applications where aesthetic preferences may favor traditional ceramic solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Resilient Innovation Challenges Traditional Dominance

Carpet and rugs retained 41.12% of the Egypt floor covering market share in 2025, driven by cultural affinity and Oriental Weavers’ scale advantages that produced EGP 2.54 billion net profit in 2024. However, resilient flooring is projected to post an 8.09% CAGR, positioning it as the prime disruptor of the Egypt floor covering market through 2031. Luxury Vinyl Tile and SPC gain acceptance in healthcare, education, and hospitality, where rapid installation and moisture resistance outweigh higher ticket prices. Locally manufactured ceramic, meanwhile, leverages cost leadership, broad style pallets, and nationwide distribution networks, defending its share in mass-market housing.

Currency shocks sideline imported hardwood and engineered wood, shrinking assortments and elevating ceramic and SPC substitution. Laminate remains a mid-price compromise, though concerns over moisture swelling restrict its penetration in coastal sites. Niche cork and rubber solutions serve high-performance zones such as gyms and labs, yet limited local output and specialist installation keep volumes modest. Overall, category transitions reflect a balance of cultural preference and pragmatic adaptation to Egypt’s climate and macro-economy within the Egypt floor covering market.

By Construction Type: Renovation Dominance Shifts Toward New Development

Renovation and replacement accounted for 64.02% of the Egypt floor covering market size in 2025, reflecting cyclical refurbishment of a vast existing building stock. New construction, fueled by megaprojects and housing programs, is forecast for a 7.06% CAGR, gradually eroding the historical skew toward renovation. Replacement cycles typically favor click-fit resilient tiles and thin-set ceramic that minimize downtime, whereas green-field developments adopt integrated acoustic underlays, raised floors, and long-life coatings.

Tourism megaprojects blend the two dynamics: hotel operators refurbish existing assets even as sizable new builds break ground. Government tender frameworks now bundle supply and installation packages, shifting risk to contractors and stimulating B2B channel growth. The net result is a more balanced opportunity mix, with renovation still larger but new construction increasingly influential across the Egypt floor covering market.

By End User: Commercial Growth Outpaces Residential Base

Residential maintained 53.78% of 2025 revenue, sustained by mortgage subsidies and demographic momentum. Commercial space, however, should register a 6.55% CAGR to 2031, outstripping residential growth as office and retail inventories surge across the New Administrative Capital and satellite cities. Hospitality corridors along the Red Sea require high-durability specifications that favor porcelain planks, LVT, and patterned carpets engineered for frequent cleaning.

Industrial and public infrastructure users adopt anti-static vinyl, heavy-duty rubber, and epoxy systems designed for forklift traffic and high chemical exposure. Growing attention to indoor-air quality in schools and hospitals fosters adoption of low-VOC SPC and antimicrobial carpets, reshaping product development roadmaps within the Egypt floor covering market.

By Distribution Channel: B2B Growth Challenges Retail Dominance

B2C / Retail Channels captured 69.34% of sales in 2025 due to Egypt’s network of neighbourhood dealers and large furniture showrooms. Yet B2B specialist contractors and project dealers will post an 8.22% CAGR as megaproject complexity pushes procurement toward turnkey solutions. Developers in the New Administrative Capital increasingly sign framework agreements covering supply, installation, and after-sales support, favouring entities that hold inventory close to job sites.

Home centres still influence consumer choices for apartment renovations, while e-commerce gains traction among digitally savvy millennials. Hybrid models emerge in mixed-use districts, where residents select floors at retail design studios that feed consolidated contractor orders, tightening supply-chain coordination across the Egypt floor covering market.

Geography Analysis

Greater Cairo dominates value demand as the New Administrative Capital channels state-backed budgets into multi-tower precincts requiring 75,000 m² of floor finishes per governmental complex. Developers here approximate premium grade-A office rents in USD terms, justifying imports of Italian porcelain for marquee lobbies. Along the Red Sea, Hurghada and Sharm El-Sheikh accelerate hospitality refurbishments on the back of 14.6 million tourist arrivals anticipated for 2025, translating into continuous cycles of corridor-carpet replacement and pool-deck tiling.

Alexandria and Egypt’s North Coast ride the Ras El Hekma masterplan, where a USD 35 billion UAE-backed injection triggers a wave of residential and retail starts scheduled to deliver 25,000 units by 2030. Suez Canal cities expand warehouse and logistics footprints, each averaging 40,000 m² of epoxy-coated concrete annually once Egypt inaugurates its “dry-port” strategy. Upper Egypt remains price-sensitive, pulling from local ceramic producers based in Minya whose distribution radius sits within 300 km to minimize freight. Export-oriented manufacturing clusters in Tenth of Ramadan City and Sadat City serve African markets under the COMESA tariff preference, providing the Egypt floor covering market with foreign-exchange buffers when domestic demand softens.

Value Chain Analysis

The Egypt floor covering value chain starts with raw-material inputs and intermediate processing, then moves through manufacturing, distribution, installation, and after-sales service. Key inputs include clays and minerals for ceramics and stone, polymers and additives for vinyl/SPC, and yarns for carpets and rugs. Large domestic players reduce supply risk through integration. For example, Oriental Weavers supports nylon carpet output via its in-house King Tut yarn facility (120 tons/day), while major carpet producers such as MAC Carpet operate multiple manufacturing sites in Tenth of Ramadan City, including free-zone-linked capacity that supports export logistics and FX management.

Downstream, product flows split between B2C retail (neighborhood dealers, home centers, specialty stores, and online) and B2B channels (contractors, project dealers, and framework procurement for megaprojects). Industrial zones and logistics corridors shape competitiveness, and SPC production presence in specialized parks such as Unispec at the Teda Industrial Park in Suez improves access to port infrastructure and project customers. Bottlenecks concentrate around imported raw materials for wood and some chemical inputs, where foreign-currency availability and port clearance timing can affect landed cost and lead time. A second constraint is installer availability outside major metros, which can limit adoption of more specification-sensitive systems such as LVT/SPC and advanced subfloor preparations.

Competitive Landscape

The Egypt floor covering market is moderately concentrated, with a few leading players controlling a significant portion of the market. Oriental Weavers dominate the stems from cradle-to-gate integration, global franchising channels, and annual output surpassing 109 million m². Cleopatra Ceramics capitalizes on proximity to Sinai clay quarries to supply value tiles across MENA, while Tarkett leverages regional LVT demand through its strategic alliance with Elissa Plastics. Technology differentiation centres on digital glazing, inkjet aesthetics, and in-line quality control using AI-enabled defect detection.

Sustainability upgrades remain a strategic battleground. Cleopatra Ceramics trailed hydrogen co-firing in biscuit kilns, targeting a 15% CO₂ intensity reduction by 2027. Tarkett deployed post-consumer PVC take-back lines, while Marble & Granite City introduced water-reclamation loops that recycle 95% of process slurry. M&A prospects swirl around mid-tier terrazzo mosaics producers looking for capital infusion to modernize rotary polishing lines. Meanwhile, European brands court Egyptian OEMs for private-label estimates, widening product range without building greenfield plants.

Egypt Floor Covering Industry Leaders

Oriental Weaver

Cleopatra Ceramics

Tarkett S.A

Mohawk Industries

RAK Ceramics

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Specification-led demand in mixed-use and infrastructure-linked developments is creating whitespace for flooring systems positioned on lifecycle performance, installation speed, and maintenance efficiency, especially in hospitality, education, healthcare, and transport-adjacent commercial spaces. The operating and fit-out momentum around Greater Cairo transport upgrades (East Nile Monorail operational in early 2026, continued work on West Nile Monorail and Metro Line 4) supports opportunities for heavy-traffic finishes and modular resilient systems. It also creates a fit for adhesive/underlayment ecosystems that contractors can deploy at scale across phased handovers in the New Administrative Capital and surrounding districts.

On the supply side, industrial policy actions in 2026 around steel safeguards and evolving export compliance create two practical opportunity areas for floor covering participants. First, local sourcing and fabrication of metal-based finishing components (profiles, trims, stair nosings, access-floor elements) can become more competitive as definitive safeguard measures on certain imported steel flat products move into enforcement from April 2026. Second, export-oriented manufacturers and suppliers can differentiate by building environmental documentation capabilities aligned with GOEIC requirements introduced under Resolution No. 33 of 2026, strengthening access to international buyers that request emissions and compliance evidence as part of procurement.

Recent Industry Developments

- May 2026: Oriental Weavers launched a unified digital platform to expand e-commerce across the group and improve customer personalization. The initiative strengthens direct-to-consumer reach alongside traditional dealers, and it can help stabilize sell-through by improving product discovery and order capture during renovation cycles.

- February 2025: Prime Minister Moustafa Madbouly inaugurated Ceramica Cleopatra Group's factory Phase II in the Ain Sokhna industrial zone, covering 500,000 square meters and backed by EGP 5 billion in investment. The added industrial footprint supports higher local availability of ceramic and porcelain products used in housing and hospitality projects, reinforcing domestic supply depth versus imports.

- December 2024: Hilton announced plans to triple its hotel count in Egypt by adding 25 properties. This pipeline raises near-term procurement activity for premium, high-durability floor finishes in guest rooms and public areas, supporting demand for porcelain, modular resilient flooring, and specified carpet solutions across key tourist corridors.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this work, the Egypt floor covering market is the value of products used to cover floors that are sold and installed within Egypt across residential, commercial, and builder-led demand.

Scope exclusions: We exclude furniture, floor care chemicals, adhesives sold as standalone products, and broader interior decor items that are not used as floor coverings.

Segmentation Overview

- By Product Type

- Carpet and Rugs

- Resilient Floor Covering

- Vinyl Sheets & VCT

- Luxury Vinyl Tiles (LVT)

- Linoleum

- Rubber Flooring

- Cork Flooring

- Non-Resilient Floor Covering

- Ceramic & Porcelain Tile

- Natural Stone

- Hardwood

- Engineered Wood

- Laminate

- Resilient Floor Covering

- By Construction Type

- New Construction

- Renovation & Replacement

- By End User

- Residential

- Commercial

- Industrial & Public Infrastructure

- By Distribution Channel

- B2C/Retail Channels

- Home Centers

- Specialty Stores

- Online

- Other Distribution Channels

- B2B/Contractors/Dealers

- B2C/Retail Channels

- By Geography

- Greater Cairo & Giza

- Alexandria & Mediterranean Coast

- Nile Delta

- Upper Egypt

- Suez Canal & Sinai

- Red Sea Governorates

- Carpet and Rugs

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set clear market boundaries and to anchor the model to real Egypt construction and trade signals before assumptions were taken to the field. We referred to public sources such as CAPMAS releases, the Central Bank of Egypt publications, UN Comtrade trade statistics, World Bank macro indicators, and industry standards and papers from sources like ISO and peer reviewed journals.

To translate these signals into a usable sizing structure, we also reviewed company filings and investor presentations, importers and distributor catalogs, and reported updates from reputed press and association websites covering building materials and housing activity. For pricing and company financial consistency checks, we selectively used paid subscriptions for company financials and news, and for shipment level import-export views where it helped validate product availability and value ranges. This source list is illustrative, and many other references were used to collect data points, cross check gaps, and clarify unclear splits.

Primary Interviews and Surveys

Primary work was done to confirm what is actually counted as floor covering in Egypt, and to pressure test shares across product types, end users, and channels. We spoke with manufacturers, importers, distributors, installers, and large buyers, so assumptions like mix shifts, average selling prices, and renovation versus new build demand could be corrected when desk signals were not enough. Because this is a country market, inputs were validated across major demand centers and project types rather than being split into global regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | |

| Mid tier: 52% | Functional/Unit leaders: 43% | |

| Smaller Players: 20% | Managers: 45% |

Market-Sizing & Forecasting

The core model starts from a top down build where construction activity and renovation demand are translated into a flooring demand pool for Egypt, which is then converted into market value using category level price bands. Where possible, we corroborated the total with selective bottom up checks, such as supplier and importer roll ups from a sampled set, and a simple volume times average selling price build for key products to adjust the overall number.

Inputs used in the model include building completion and permitting trends, residential versus commercial project intensity, renovation and replacement frequency, import dependence by product type, and average price movement by resilient and non resilient categories. Because currency and inflation can distort value series, we tracked exchange rate periods used for conversion and aligned them with pricing feedback captured in the interviews.

For forecasting, we used scenario analysis supported by a light multivariate view, where the construction pipeline, housing formation signals, and refurbishment activity were treated as the main drivers and then reweighted based on what installers and distributors expect for mix changes. If a bottom up check was missing for a niche category, the gap was handled through share based allocation from validated mixes, followed by a reasonableness check against trade and channel indicators.

Data Validation & Update Cycle

Validation is done through repeated cross checks, where model totals are compared against independent signals like import value trends, construction activity direction, and observed price ranges. When a large variance shows up, the driver is isolated, the assumption is revisited, and a quick re contact is triggered with the relevant respondent group before sign off.

A second analyst review is done to spot inconsistencies across segments and years, and then the full workbook is checked for arithmetic and unit logic before publication. Reports are refreshed annually, and interim updates are made when material events occur that can shift pricing, trade flows, or construction momentum. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Egypt Floor Covering Market Size Measured Against Other Published Estimates

Published market values for Egypt floor covering can look far apart because the scope is not always identical, and because pricing and currency timing assumptions can shift the value even when volume is similar. Differences also come from how firms treat renovation demand, channel markups, and whether the number reflects products only or also bundles in installation services.

The benchmark table shows a meaningful spread across current year values, and in Mordor Intelligence's model the figure is tied to floor covering product revenue within Egypt, with product categories and end user demand validated through interviews and then aligned to trade and construction signals for that same year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.39 B (2025) | |

| Global Consultancy A | USD 2.64 B (2026) | Uses a later base year and may apply a faster price step up, which can lift value even if underlying demand growth stays similar. |

| Industry Portal B | USD 2.27 B (2024) | Often relies on older-year snapshots and may undercount renovation and replacement purchases, which reduces the value in years with active refurbishments. |

When the year, currency timing, and what is included are lined up, much of the difference becomes explainable and repeatable. Our approach keeps the total traceable to clear demand drivers like construction activity, renovation share, and category pricing, which makes the final number easier to reconcile and update.

Key Questions Answered in the Report

How large is the Egypt floor covering market in 2026?

The market is valued at USD 2.51 billion in 2026 and is expected to reach USD 3.24 billion by 2031.

Which product category is growing fastest?

Resilient flooring, led by SPC and LVT, is forecast for an 8.09% CAGR through 2031.

What drives flooring demand along the Red Sea?

USD 125 billion of hospitality projects such as Ras El Hekma and Ras Ghamila require durable, salt-resistant commercial flooring.

How does currency volatility impact wood flooring?

Pound depreciation has raised landed wood costs by more than 50%, shifting demand toward locally produced ceramic and SPC.

Who leads the domestic competitive landscape?

Oriental Weavers holds 34% share in machine-made carpets, while Cleopatra Ceramics controls 11.50% of ceramic tile sales.

What is the outlook for B2B distribution?

B2B contractor channels are projected to grow at an 8.22% CAGR as megaproject developers favor turnkey supply-and-install agreements.

Page last updated on: