Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

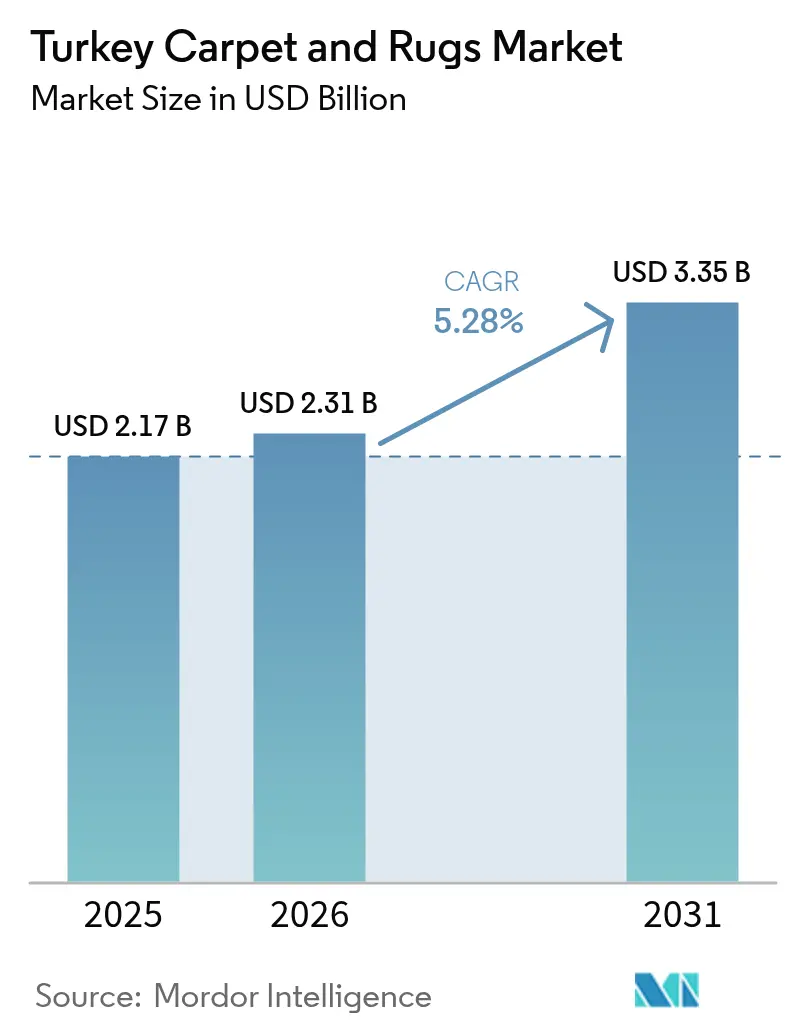

| Base Year Market Size (2025) | USD 2.17 Billion |

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Carpets and Rugs Market Analysis by Mordor Intelligence

The Turkey Carpets and Rugs Market size is expected to increase from USD 2.17 billion in 2025 to USD 2.31 billion in 2026 and reach USD 3.35 billion by 2031, growing at a CAGR of 5.28% over 2026-2031.

Driving forces behind the steady trajectory include a weakened lira that improves export competitiveness, government-funded urban renewal initiatives that expand domestic replacement cycles, and ongoing premiumization that lifts average selling prices. Robust export sales, especially to the United States and the Gulf Cooperation Council, reinforce the industry’s dual-engine growth model by buffering local slowdowns. Gaziantep’s well-established machine-made cluster keeps production costs low and helps meet quick-turn foreign orders, while Istanbul’s logistics advantages enable faster multimodal shipments to Europe. Meanwhile, investment in closed-loop recycling and solution-dyed synthetics positions suppliers to align with increasingly stringent sustainability requirements in key destination markets. Although competition from hard-surface flooring continues to pressure share in new builds, Turkish manufacturers mitigate the threat with differentiated texture, acoustic, and customization features.

Key Report Takeaways

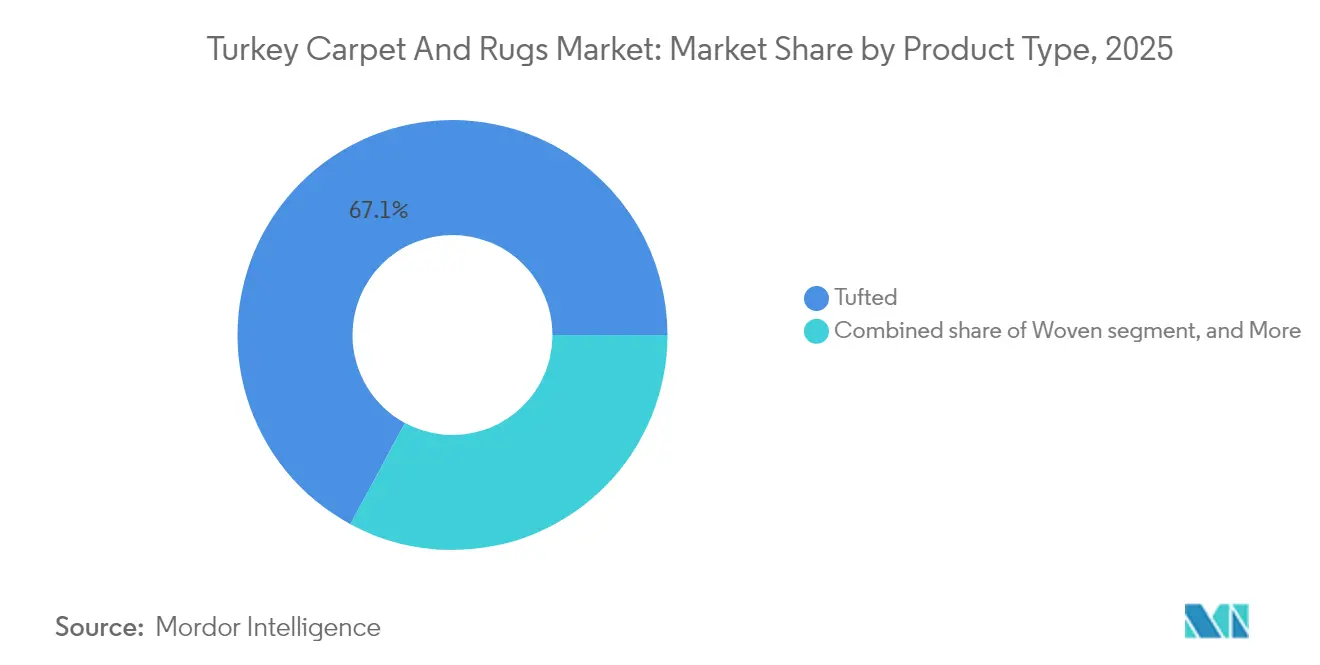

- By product type, tufted captured 67.12% of Turkey Carpets and Rugs Market share in 2025, while knotted/hand-knotted is projected to advance at an 8.35% CAGR through 2031.

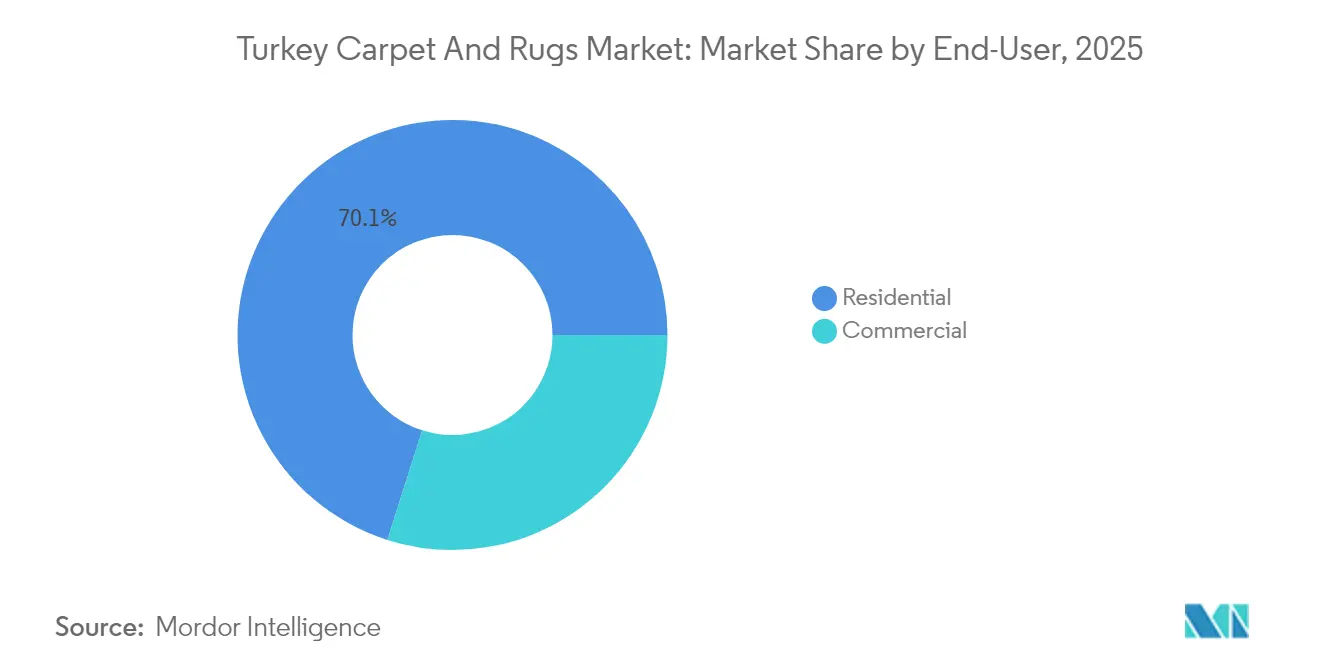

- By end-user, residential generated 70.10% of 2025 revenue, whereas healthcare & educational facilities will expand at a 6.45% CAGR between 2026 and 2031.

- By distribution channel, B2C/retail maintained 60.20% contribution in 2025, while online platforms are advancing at a 7.15% CAGR during the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Carpets and Rugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential renovation & urban-rejuvenation projects | +1.2% | Marmara, Southeastern Anatolia, Central Anatolia | Medium term (2-4 years) |

| Surge in exports to high-value GCC & US buyers | +0.9% | Southeastern Anatolia, Aegean, Marmara | Short term (≤ 2 years) |

| Shift toward polypropylene & solution-dyed PET for cost efficiency | +0.8% | Southeastern Anatolia, Marmara, Central Anatolia | Long term (≥ 4 years) |

| Government incentives for Gaziantep’s machine-made carpet cluster | +0.6% | Southeastern Anatolia | Medium term (2-4 years) |

| Growing e-commerce penetration in home-décor | +0.5% | Marmara, Aegean, Central Anatolia | Short term (≤ 2 years) |

| Niche demand for hand-knotted Anatolian heritage pieces among Gen-Z collectors | +0.3% | Aegean, Central Anatolia, Southeastern Anatolia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Residential Renovation & Urban-Rejuvenation Projects

Publicly funded seismic-risk programs accelerate full-unit reconstruction schedules, thereby compressing traditional renovation cycles and generating bulk carpet tenders that exceed ordinary retail demand. Municipal coordination with contractors allows established manufacturers to secure multi-building orders, leveraging scale and flexible credit terms. The projects often specify complete interior packages, creating opportunities for higher-margin premium flooring in new up-market apartments. Neighborhood-wide rebuilding concentrates order volumes geographically, enabling cost-effective distribution and installation logistics. Moreover, compliance with updated safety codes enhances perceptions of quality, which supports upselling into stain-resistant or antimicrobial ranges. Because the initiatives span multiple provinces, they lessen regional sales volatility by staggering project timelines.

Surge in Exports to High-Value GCC & US Buyers

Currency depreciation sharpened price competitiveness, but exporters increasingly succeed through design agility rather than simple cost advantages. Turkish suppliers blend European aesthetics with Middle Eastern motifs to cater to both Gulf luxury consumers and U.S. trend seekers, capturing USD 784 million from American buyers in 2024 [1]International Finance Corporation release (via Karabük Haber), “Bakan Kacır’dan Karabük’e destek sözü,” karabukhaber.com.tr.. Brand-name U.S. producers such as Karastan outsourced area-rug lines to Turkish factories, evidencing trust in local quality and reliability. Repeat orders from GCC retailers validate the region’s appetite for premium, culturally aligned designs. Exporters also benefit from preferential trade frameworks linked to Turkey’s customs-union relationship with the European Union, which lends regulatory familiarity valued by North American partners. Higher per-unit pricing in these markets cushions margin pressures arising from raw-material volatility. Consequently, the Turkey carpets market continues to diversify revenue streams beyond continental Europe.

Shift Toward Polypropylene & Solution-Dyed PET for Cost Efficiency

Manufacturers increasingly favor polypropylene because it pairs low input prices with robust performance attributes, reinforcing the material’s above 25.0% share in 2024. Solution-dyed PET further reduces warranty claims by embedding color during extrusion, improving fade resistance and shortening production cycles. Integration of recycled PET helps firms comply with green-procurement criteria in destinations such as the European Union, while also mitigating reliance on crude-derived virgin feedstocks. The International Finance Corporation’s USD 50 million backing for a closed-loop recycling plant expands local access to post-consumer fiber, aligning supply security with environmental mandates [2]International Finance Corporation release (via Karabük Haber), “Bakan Kacır’dan Karabük’e destek sözü,” karabukhaber.com.tr.. Collectively, these innovations strengthen Turkey carpets market competitiveness against hard-surface categories.

Government Incentives for Gaziantep’s Machine-Made Carpet Cluster

The Ministry of Trade broadened its “prestigious fair” program in April 2025, raising the reimbursement ceiling to TRY 1 million (USD 36,000) per firm and allowing domestic exhibitions to qualify [3]Bursa 5n1k, “Yurt içi fuarlara ‘prestijli fuar’ desteği,” bursa5n1k.com.. Such support defrays international marketing costs for small and mid-sized enterprises, fostering cluster-wide export momentum. Organized industrial zones in Gaziantep already provide shared logistics and raw-material purchasing, magnifying the benefit of new promotional funds. Planned upgrades under Turkey’s 2030 Industrial Strategy promise tax incentives for automation and advanced finishing lines, which can elevate regional manufacturers into premium segments. The cluster’s concentration of skilled technicians improves knowledge diffusion, accelerating technology adoption. Over time, competitive advantages could widen relative to dispersed rivals, reinforcing Southeastern Anatolia’s role within the Turkey carpets market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-linked fiber prices (PP, nylon) pressuring margins | -0.7% | Southeastern Anatolia, Marmara, Central Anatolia | Short term (≤ 2 years) |

| Competition from hard-surface flooring (LVT, laminate, ceramics) | -0.5% | Marmara, Aegean, Central Anatolia | Medium term (2-4 years) |

| Rising labor costs affecting manufacturing competitiveness | -0.4% | Southeastern Anatolia, Central Anatolia | Medium term (2-4 years) |

| Environmental regulations limiting synthetic fibre usage | -0.3% | Nationwide (esp. Marmara, Aegean) | Long term (4+ years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Linked Fiber Prices Pressuring Margins

Polypropylene and nylon costs fluctuate with global oil benchmarks, complicating quotes denominated in foreign currency while inputs are sourced in lira. Larger producers negotiate annual supply contracts or deploy financial hedges, but smaller firms lack the scale to absorb sudden spikes, forcing opportunistic inventory builds that strain working capital. Exporters face an additional layer of risk because extended shipping times lock prices for weeks before raw-material purchases settle. Recycling gains only partially offset volatility because secondary feedstock volumes remain limited relative to total demand. In response, stakeholders lobby for state-backed hedging facilities and greater transparency in domestic petrochemical pricing. Persistent commodity swings could suppress the headline 4.39% CAGR if mitigation measures fall short.

Competition from Hard-Surface Flooring Alternatives

Laminate and luxury-vinyl tile manufacturers have capitalized on perceptions of easier maintenance and modern aesthetics, diverting share from carpet in urban condos. Marketers highlight allergy reduction and quick cleaning to target health-conscious consumers, particularly amid post-pandemic hygiene awareness. Turkish carpet mills counter with antimicrobial treatments, enhanced stain blocking, and modular tile systems that speed partial replacement. Kastamonu Entegre’s upgraded laminate collections heighten domestic rivalry by promoting click-lock ease of installation. Developers sometimes specify mixed flooring, allocating hard surfaces to kitchens while retaining carpet in bedrooms, which limits full displacement but trims total square-meter demand. Over the mid-term, successful differentiation will hinge on demonstrating acoustic benefits, personalized design, and superior tactile comfort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tufted Dominance Faces Artisanal Renaissance

Tufted offerings commanded 67.12% of Turkey carpets market share in 2025 because rapid needle-punch loops enable cost-efficient mass production and reliable quality for large residential projects. Economies of scale within Gaziantep’s cluster drive unit costs lower than imported alternatives, reinforcing domestic preference. Woven constructions retain niche appeal in mid-range hospitality, as their dimensional stability supports high-traffic corridors, while needle-punched variants serve technical sectors like automotive trunk liners. Yet knotted and hand-knotted rugs are forecast to grow at an 8.35% CAGR, fueled by revived consumer interest in authenticity, storytelling, and long-term value retention. Digital channels allow artisans to reach affluent diaspora buyers, sustaining community livelihoods and preserving cultural motifs. Consequently, suppliers balance high-volume tufted lines with small-batch handcrafted collections to capture both ends of the price spectrum.

Knotted production remains labor-intensive, with lead times stretching several months, yet premium gross margins justify artisan training programs subsidized by local chambers of commerce. Middle-income homeowners increasingly mix statement handmade pieces with machine-made runners, expanding addressable demand beyond elite circles. Manufacturers experiment with semi-mechanized looms to speed weaving while preserving irregular texture sought by collectors. Flat-weave kilims evolve into wall art and upholstery fabric, broadening applications outside conventional floor covering. Retailers curate limited editions, fostering urgency and higher turn rates per square meter. Such hybrid product portfolios improve resilience against macro shocks, ensuring the Turkey carpets market maintains both volume stability and premium upside.

By End-User: Residential Stability Contrasts Institutional Growth

Residential buyers generated 70.10% of 2025 turnover, underpinned by routine replacement cycles, do-it-yourself renovation surges, and lifestyle shifts toward home personalization. Remote-work adoption encourages acoustic insulation and comfort upgrades, sustaining baseline demand even during housing-starts slowdowns. Developers bundle carpets with turnkey apartment packages to accelerate sales velocity, while mortgage campaigns by state banks support middle-class purchasing power. Contrasting with steady residential momentum, healthcare and educational facilities showcase the fastest CAGR at 6.45% through 2031 because administrators seek antimicrobial, low-VOC floor coverings compliant with updated hygiene codes. Government-backed hospital modernization funnels large contracts to suppliers offering tailored sterilization treatments and seam-welded installation systems. Consequently, vendors calibrate product lines to meet divergent performance specifications across residential coziness and institutional sterility.

Commercial offices display moderate rebound as hybrid schedules limit full-floor occupancy but corporate renovation budgets prioritize modular carpet tiles for flexible reconfiguration. Retail chains choose budget tufted rolls for cost control yet explore digitally printed area rugs to refresh visual merchandising quickly. Hospitality projects, buoyed by tourism recovery, select custom-color wool-blend axminster for lobbies and corridors, commanding premium margins. Public-private partnership universities invest in stain-proof nylon tiles to lower lifecycle maintenance costs. Meanwhile, leisure facilities such as cinemas adopt plush polypropylene for acoustic dampening. Such varied end-user needs compel Turkey carpets industry players to expand design studios and technical advisory teams.

By Distribution Channel: Digital Transformation Accelerates Traditional Retail

B2C and specialty retail formats contributed 60.20% to 2025 revenue, reflecting consumer desire to touch fibers and compare dye lots before purchase; staff provide vital guidance on pile height, underlay options, and room acoustics. Big-box home-improvement chains run in-store kiosks that let shoppers visualize floor plans, marrying physical sample handling with digital preview. Nonetheless, online sales will grow at 7.15% CAGR, propelled by high-resolution product configurators, free swatch deliveries, and transparent return policies. Manufacturers host virtual showrooms with 360-degree views, capturing leads for authorized installers. Direct-to-consumer micro-brands compete on curated aesthetics and eco-friendly credentials, cutting overheads tied to physical outlets. Omnichannel strategies synchronizing inventory, pricing, and loyalty programs therefore become central to retaining share in the Turkey carpets market.

Trade contractors and interior designers continue to source via B2B portals that consolidate technical datasheets and bid pricing; these platforms streamline procurement for commercial builds. Some mills pilot subscription models in which offices receive scheduled tile replacements financed as operating expenditure. Furniture stores cross-sell accent rugs bundled with sofa sets, leveraging higher footfall. Social-commerce live streams feature real-time auction formats that stimulate impulse buys among younger viewers. Freight consolidators optimize less-than-truckload shipments of rolled goods, shortening delivery windows and reducing damage rates. As a result, distribution ecosystems evolve to satisfy rising expectations for speed, transparency, and personalization.

Competitive Landscape

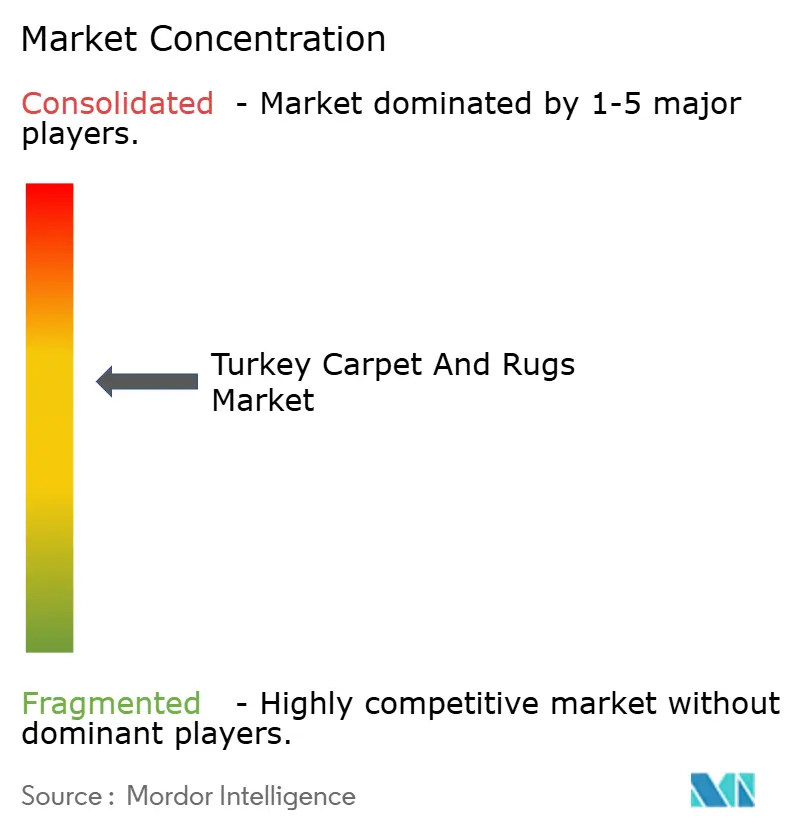

The Turkey Carpets market shows a moderate level of concentration, with the top five players holding a significant portion of the market, suggesting that opportunities for consolidation still exist while competition remains relatively manageable. Strategic trends in the industry highlight vertical integration and geographic specialization. Leading companies such as Merinos and Dinarsu benefit from the support of their parent companies and rely on well-established distribution networks to strengthen their market positions. The sector's fragmented structure enables niche players to capture specialized segments through heritage branding, custom design capabilities, or technical textile applications. White-space opportunities emerge in circular economy solutions, smart textile integration, and direct-to-consumer digital platforms that bypass traditional distribution channels.

Technology adoption accelerates competitive differentiation, with companies investing in digital carpet printing, automated weaving systems, and enterprise resource planning solutions to improve efficiency and customization capabilities. Royal Halı's implementation of Nebim V3 ERP systems exemplifies how mid-tier manufacturers pursue operational excellence through technology integration. The International Finance Corporation's USD 50 million investment in textile recycling infrastructure signals institutional recognition of sustainability-driven competitive advantages [4]Textilegence, “Carpet manufacturer YD Dokuma declares bankruptcy,” textilegence.com]. . Market disruption potential exists in IoT-enabled smart carpets for elder-care monitoring and retail analytics, representing convergence opportunities between traditional manufacturing and emerging technology applications.

Turkey Carpets and Rugs Industry Leaders

Merinos (Erciyes Holding)

Dinarsu (Zorlu)

Royal Halı

Royal Halı

Kaşmir Halı

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Turkish Ministry of Trade expanded its “prestigious fair” support program to domestic exhibitions, raising the funding ceiling to TRY 1 million (USD 36,000) per firm.

- March 2025: Zenova Carpet Tekstil reported a 17.86% increase in net sales revenue and a 64.52% rise in operating profit for 2023.

- January 2025: Karastan halted U.S. area-rug production and shifted manufacturing to Turkish partners, modifying looms to produce existing bestsellers while developing new collections in Turkey and India.

Turkey Carpets and Rugs Market Report Scope

Carpets and rugs are floor coverings used to improve the aesthetics of the house/office spaces and provide comfort and warmth. The Turkish carpet and rugs market is segmented by type into tufted, woven, needle-punched, knotted, and other types, application into residential and commercial, and distribution channels into offline (contractors and retail), online, and other distribution channels. The report offers market size and forecasts for the Turkish carpets and rugs market, which are provided in terms of revenue (USD) for all the above segments.

By Product Type

| Tufted |

| Woven |

| Needle-Punched |

| Knotted / Hand-Knotted |

| Others (Flat-weave, Hooked, Braided) |

By End-User

| Residential | |

| Commercial | Hospitality & Leisure |

| Corporate Offices | |

| Retail | |

| Healthcare & Educational Institutions | |

| Other Commercial Facilities |

By Distribution Channel

| B2B / Direct from Manufacturers | |

| B2C / Retail | Home-Improvement & DIY Stores |

| Specialty Flooring Stores (incl. exclusive brand outlets) | |

| Furniture & Furnishing Stores | |

| Online | |

| Other Distribution Channels |

| By Product Type | Tufted | |

| Woven | ||

| Needle-Punched | ||

| Knotted / Hand-Knotted | ||

| Others (Flat-weave, Hooked, Braided) | ||

| By End-User | Residential | |

| Commercial | Hospitality & Leisure | |

| Corporate Offices | ||

| Retail | ||

| Healthcare & Educational Institutions | ||

| Other Commercial Facilities | ||

| By Distribution Channel | B2B / Direct from Manufacturers | |

| B2C / Retail | Home-Improvement & DIY Stores | |

| Specialty Flooring Stores (incl. exclusive brand outlets) | ||

| Furniture & Furnishing Stores | ||

| Online | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the expected growth rate for Turkish carpet exports?

Exports are supported by a 4.18% industry CAGR and reached USD 2.8 billion in 2024, with high-value GCC and U.S. demand driving future gains.

Which product segment is growing fastest?

Hand-knotted rugs are forecast to grow at an 8.35% CAGR, reflecting rising demand for premium, heritage-rich designs.

Which material shows the highest growth momentum?

Recycled and bio-based fibers are advancing at a 11.6% CAGR, buoyed by sustainability mandates and IFC-backed recycling investments.

Which distribution channel is expanding most rapidly?

Online platforms are growing at a 7.15% CAGR as augmented-reality tools and direct-to-consumer models gain traction.

Page last updated on: