Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.92 Billion |

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

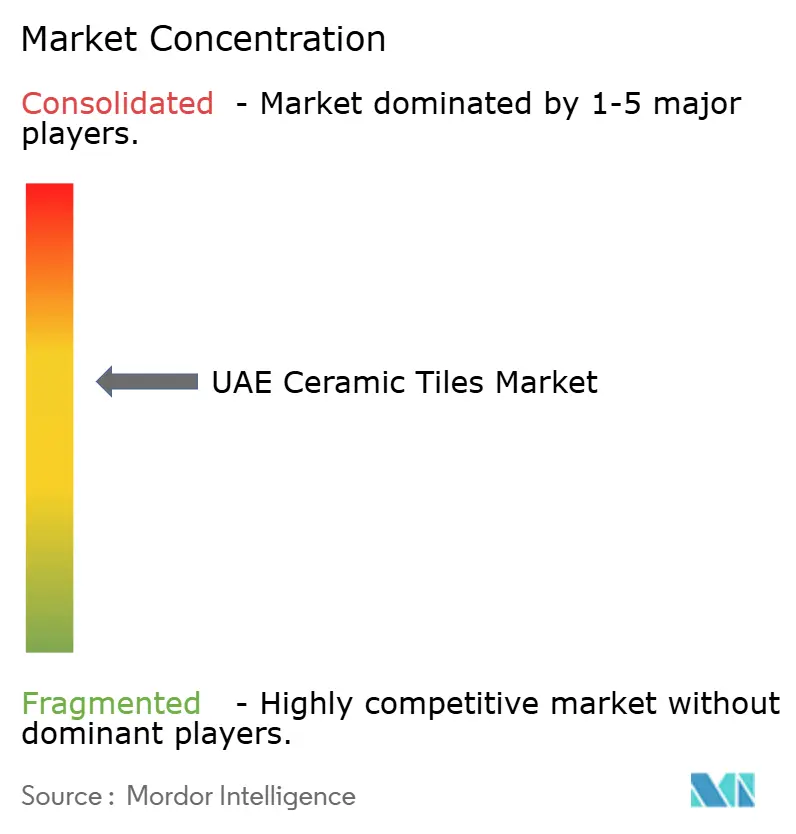

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Ceramic Tiles Market Analysis by Mordor Intelligence

The UAE ceramic tiles market size in 2026 is estimated at USD 0.97 billion, growing from 2025 value of USD 0.92 billion with 2031 projections showing USD 1.26 billion, growing at 5.31% CAGR over 2026-2031. Infrastructure spending, tourism-driven commercial projects, and population growth are jointly lifting demand across floor, wall, and specialty applications. Dubai approved more than 30,000 building permit requests in 1H 2025, underscoring a construction surge that raises tile consumption[1]Dubai Municipality, “Building Permit Statistics H1 2025,” dubaimunicipality.ae.. International visitors rebounded by 15.5% to 29.2 million in 2024, spurring hotel and leisure developments that specify premium porcelain and mosaic finishes. The federal net-zero 2050 agenda is accelerating the uptake of eco-friendly surfaces as developers pursue green-building credits. Digital retail uptake, backed by 99% internet penetration, is reshaping purchase pathways for both contractors and homeowners[2]Telecommunications and Digital Government Regulatory Authority, “UAE ICT Indicators 2024,” tra.gov.ae..

Key Report Takeaways

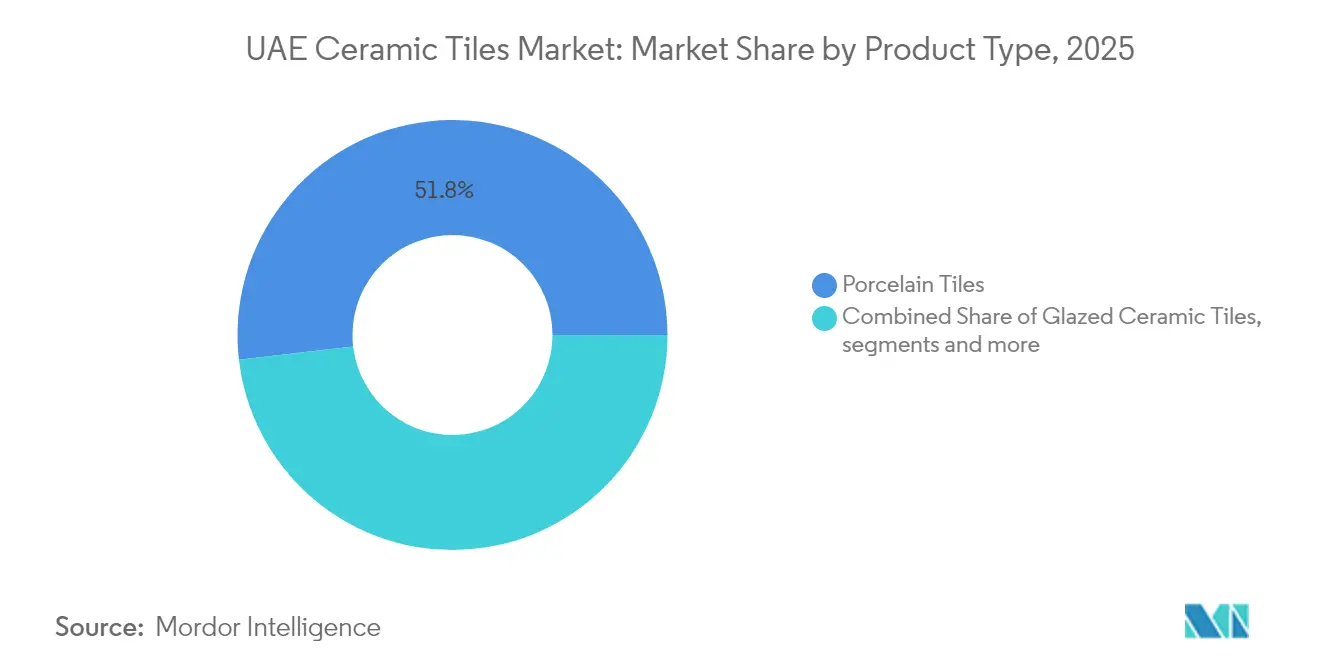

- By product type, porcelain captured 51.83% of the UAE tiles market share in 2025; mosaic is projected to advance at a 6.18% CAGR through 2031.

- By application, floor coverings represented 60.62% of the UAE tiles market size in 2025, while wall installations are projected to grow at a 5.47% CAGR to 2031.

- By end-user, the residential segment accounted for 47.55% of revenue in 2025 and is projected to grow at a 5.88% CAGR through 2031.

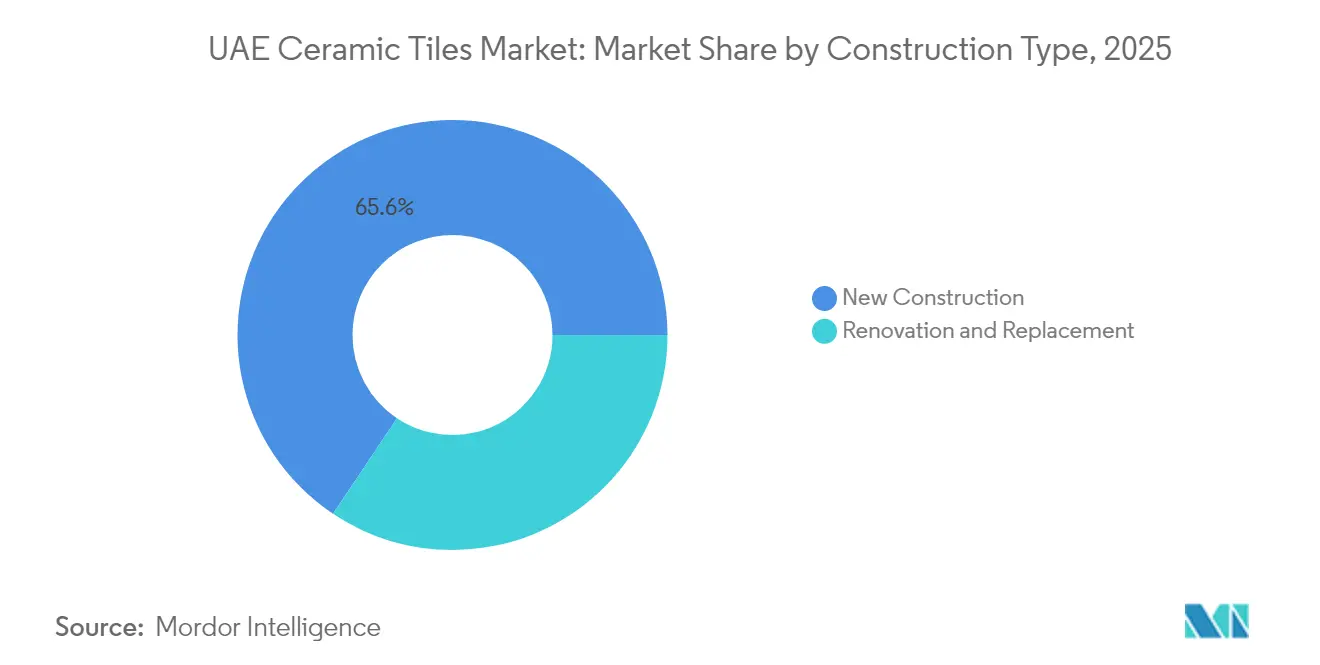

- By construction type, new-build activity accounted for 65.62% of total demand in 2025; renovation work is rising at a 5.71% CAGR on asset-upgrade cycles.

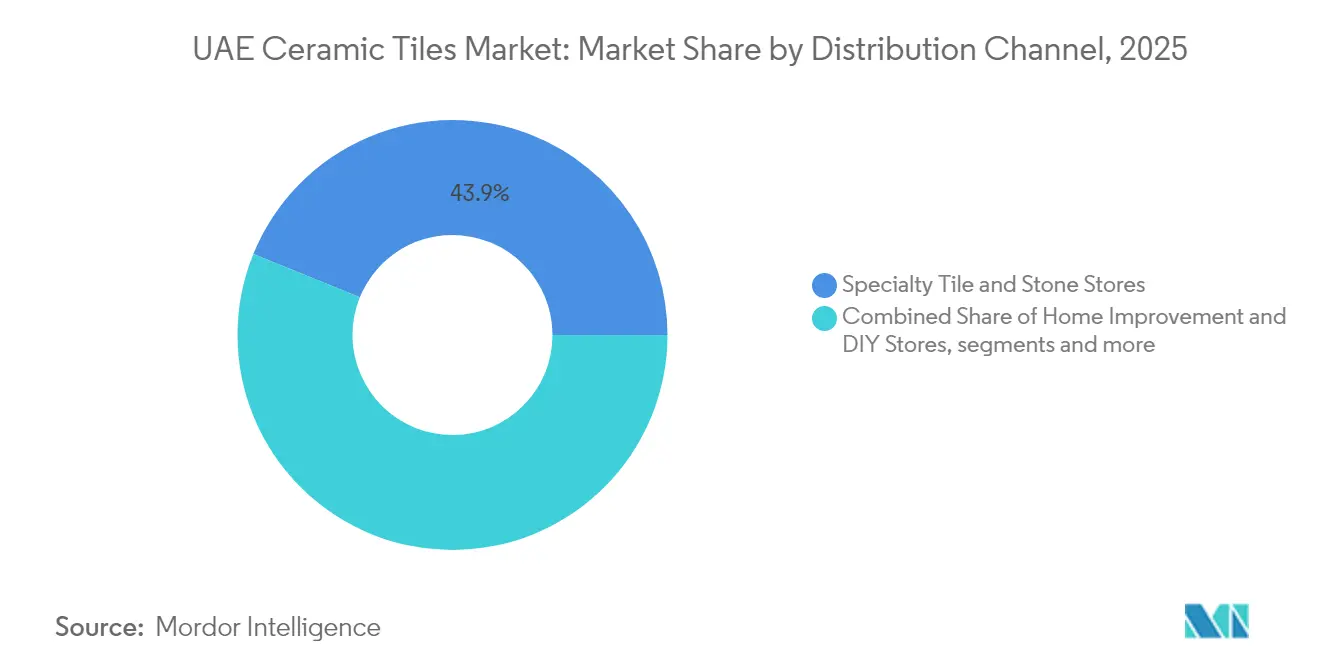

- By distribution channel, specialty stores dominated with a 43.85% share in 2025, yet online platforms are expanding fastest at a 6.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization & infrastructure drives | +1.8% | Dubai, Abu Dhabi core, spillover to Northern Emirates | Medium term (2-4 years) |

| Tourism-led commercial build-out (post-Expo) | +1.2% | Dubai primary, Abu Dhabi secondary | Short term (≤ 2 years) |

| Residential boom from expatriate inflow | +1.5% | Dubai, Abu Dhabi, Sharjah urban corridors | Medium term (2-4 years) |

| Premium porcelain preference | +0.8% | UAE-wide, concentrated in luxury segments | Long term (≥ 4 years) |

| Green-building regulations spur eco-tiles | +0.7% | National, early adoption in Dubai, Abu Dhabi | Long term (≥ 4 years) |

| Antimicrobial healthcare tile demand | +0.4% | National, healthcare facility concentrations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization & Infrastructure Drives

Dubai logged 20% construction growth in 1H 2025, producing over 5.5 million m² of licensed space. Multi-storey commercial projects claimed 45% of permits, while villa plots accounted for 40%, broadening tile requirements across surface types. Federal outlays on Etihad Rail and a planned hyperloop corridor knit new urban zones needing durable floor and wall solutions[3] Source: International Trade Administration, “UAE Infrastructure Opportunities,” trade.gov.. Dubai’s one-window “Build in Dubai” portal now cuts approval times, pulling tile orders forward in schedules. Vision 2031’s goal of doubling GDP ensures a multi-year project pipeline that sustains the UAE tiles market. Government infrastructure investments, including the USD 11 billion Etihad rail project and USD 5.9 billion hyperloop initiative, are establishing new urban corridors that require extensive tile installations across transportation hubs and supporting facilities.

Tourism-Led Commercial Build-Out (Post-Expo)

Hotel keys in Dubai reached 154,000 in 2024, with several global brands announcing additional towers for handover before 2028. International arrivals climbed 15.5% year on year, underpinning fresh demand for premium lobby and guest-room finishes. The AED 10 billion Dubai Exhibition Centre, at 180,000 m², sets a regional benchmark for large-format porcelain specified for heavy foot traffic. Gaming-ready entertainment complexes slated for Ras Al Khaimah add new leisure sub-segments requiring specialty anti-slip tiles. Branded residences, offering higher yields than standard apartments, are standardizing marble-effect porcelain across kitchens and baths. The hospitality sector's focus on branded residences, which yield higher returns than traditional developments, is driving premium tile specifications across mixed-use projects. Legacy Expo infrastructure continues generating derivative commercial projects, with the site's transformation into a permanent business and innovation hub requiring ongoing tile installations across office, retail, and event spaces.

Residential Boom from Expatriate Inflow

Expats represent 88.5% of the UAE’s 11.35 million population, lifting housing completions and tile uptake. Dubai alone is on track to deliver 90,000 homes by 2027, translating to roughly 72 million m² of new floor and wall surfaces. Abu Dhabi’s 38,700-unit pipeline through 2028 similarly boosts ceramic and porcelain volumes[4]Source: Cavendish Maxwell, “Abu Dhabi Residential Market Q4 2024,” cavendishmaxwell.com.. Mortgage registrations surged 34% in 2024 as lower interest rates spurred buyer activity, accelerating fit-out schedules. Average apartment prices rose 8% in Dubai and 11.5% in Abu Dhabi, prompting developers to specify higher-grade tiles to justify list prices. The UAE's GDP per capita of USD 38,000 in 2024, coupled with strong employment growth in the services sector, is supporting premium residential demand that favors higher-value tile categories. Ready property demand surged nearly 50% year-on-year, with 75% of transactions being apartments, indicating strong tile volume requirements across multi-unit residential developments.

Premium Porcelain Preference

Porcelain secured a 52.2% share of the UAE tiles market in 2024 thanks to its low porosity, colorfast glazes, and 75-year life claims. Italian ceramic exports to the UAE grew 2.1% in 1H 2024 to nearly EUR 40 million, reflecting sustained demand for luxury finishes. RAK Ceramics invested AED 50 million to add a high-capacity porcelain line designed for GCC heat cycles. Buildings consume 90% of national electricity for cooling, so thermally stable porcelain mitigates delamination risk. Growth in million-dollar home sales—from 6.3% in 2020 to 18.1% in 2024—supports wider porcelain adoption across living areas and outdoor terraces. Porcelain's non-porous, fully vitrified properties align with the UAE's emphasis on hygiene and maintenance efficiency in both residential and commercial applications. The segment's technical advantages, including stain resistance and ease of cleaning, make it particularly suitable for the UAE's dusty environment and high-traffic commercial spaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material & energy cost volatility | -1.1% | National, manufacturing-concentrated areas | Short term (≤ 2 years) |

| Low-cost Asian import pressure | -0.8% | UAE-wide, price-sensitive segments | Medium term (2-4 years) |

| Water-scarcity limits on wet processes | -0.3% | Manufacturing zones, Northern Emirates | Long term (≥ 4 years) |

| Weak tile-recycling infrastructure | -0.2% | National, construction waste management | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material & Energy Cost Volatility

Arabian Ceramics’ latest environmental product declaration shows that kiln firing dominates energy inputs, exposing profit lines to fuel swings. The UAE aims to lift renewable and low-carbon capacity to 156.6 GW by 2050, a shift that will reset industrial tariffs. Local cement plants have operated below 30% capacity since 2023, owing to cost spikes, signaling similar margin risk for tile kilns. Gas-indexed glaze frits saw double-digit price inflation in 2024, squeezing small batch producers lacking hedges. Exchange-rate movements on imported clay from India and feldspar from Turkey add another volatile layer to landed costs. The UAE's strategic location offers some protection through diversified sourcing options, but manufacturers must navigate complex logistics and currency fluctuations. Rising electricity costs, with the UAE consuming significant energy for cooling and industrial processes, directly impact manufacturing competitiveness and pricing strategies across the tiles sector.

Low-Cost Asian Import Pressure

China and India have expanded combined tile capacity beyond 15 billion m², funneling surplus into the Middle East at aggressive price points. Kajaria Ceramics alone ships over 86 million m² annually and is boosting UAE channel partners to reach contractors faster. Europe’s antidumping cases illustrate how low-priced imports can erode domestic share, a risk mirrored in the UAE tiles market. Premium segments still lean on European design leadership, giving local distributors margin insulation against purely cost-driven offers. Local firms exploit proximity to promise 48-hour delivery and custom cuts, services hard for offshore producers to match at scale. The UAE's emphasis on luxury and branded developments creates market segmentation opportunities where premium positioning can command higher margins despite import pressure. Local manufacturers benefit from proximity advantages, including faster delivery times, customization capabilities, and direct customer relationships that imports cannot easily replicate. The challenge intensifies in price-sensitive segments like basic ceramic tiles for mass residential projects, where import alternatives offer significant cost advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Drives Premium Positioning

Porcelain commanded 51.83% of the UAE ceramic tiles market share in 2025, thanks to its longevity and low maintenance profile. Mosaic, though smaller, is posting the fastest 6.18% CAGR as hotels and high-end apartments pursue differentiated aesthetics. Glazed ceramic sustains mid-tier housing due to favorable price-to-quality ratios, while unglazed clay targets utility zones where slip resistance outweighs gloss. Decorative sub-categories, including hand-cut zellige, cater to boutique dining and spa interiors seeking artisanal narratives. Italian export data showing rising unit values underlines buyers’ willingness to pay premiums for design-rich porcelain, a trend that should lift the UAE tiles market size for upscale grades through 2031.

Porcelain production investments—such as RAK Ceramics’ new large-format slab line—signal confidence in sustained luxury demand. Mosaic uptake tracks hospitality refurbishment cycles, evidenced by 2024 capex programs at Atlantis The Royal and Jumeirah Group properties. Glazed ceramic faces price erosion from Asian imports but still dominate quick-turn villa projects. Unglazed and technical stoneware is winning data-center tenders where electrostatic discharge control matters. Decorative tiles benefit from Dubai Design District showrooms that showcase limited-edition collections to architects and owners.

By Application: Floor Applications Lead While Wall Segments Accelerate

Flooring absorbed 60.62% of the UAE tiles market size in 2025 as residential blocks and malls prioritized hard-wearing surfaces. Wall installations are gaining at a 5.47% CAGR as open-lobby concepts demand statement cladding and large-format panels. Roof-specific tiles occupy a niche for solar-reflective or ventilated systems needed under desert heat loads. Transport hubs, including the USD 11 billion Etihad Rail stations, specify anti-slip porcelain for concourses, adding significant floor volumes. Mega venues such as the Dubai Exhibition Centre apply 120 × 120 cm tiles to reduce grout lines and maintenance bills.

Wall-centric demand stems from the hospitality sector’s push for immersive interiors, where feature walls integrate LED backlighting or 3D relief surfaces. Retailers like Dubai Mall are phasing textured wall clads to elevate experiential shopping. Residential buyers personalize kitchens with marble-look vertical slabs, driving higher-margin SKUs for suppliers. Roof applications remain governed by green-building mandates that reward solar albedo; light-colored ceramic coverings thus find favor in villa clusters. Overall, spending is shifting toward wall and roof treatments, diversifying revenue streams within the UAE tiles market.

By End-User: Residential Sector Maintains Leadership Through Population Growth

Residential projects took 47.55 of % UAE tiles market share in 2025 as soaring expatriate inflows lifted housing completions. Commercial accounts—including hotels, offices, retail, and healthcare—made up the balance, but hospitality alone is trending at double-digit growth in tile volume. Public-sector investments in clinics and schools stimulate demand for antimicrobial and easy-clean surfaces. Logistics and data-center builds, classified here under “Other commercial,” prefer heavy-duty porcelain raised floors for cabling flexibility. A pipeline of 128 government schools scheduled for retrofit by 2028 will further widen educational demand.

Higher mortgage approvals and rising per-capita income underpin mid- to high-end apartment launches in Dubai South and Abu Dhabi’s Yas Island. The hospitality boom, buoyed by 29.2 million tourists in 2024, ensures room-refurbishment cycles remain tight, refreshing wall and floor finishes every five to seven years. Retail landlords renovate promenades to maintain footfall, specifying slip-resistant tiles near F&B clusters. Hospital operators adopt large-format porcelain with silver-ion glazes to meet infection-control norms. Consequently, both residential and diversified commercial segments contribute resilient growth to the UAE ceramic tiles market.

By Construction Type: New Construction Dominates Amid Infrastructure Boom

New-build captured 65.62% of the UAE ceramic tiles market share in 2025, reflecting USD 100 billion worth of active infrastructure and real-estate projects. Renovation demand is still strong, charting a 5.71% CAGR as first-generation towers from the 2000s hit lifecycle refurbishment windows. Dubai Municipality’s 30,000 permit issuances illustrate persistent ground-breaking activity. Expo City’s conversion into a mixed-use innovation hub injects new build-outs plus adaptive reuse, keeping tile orders steady. Transport mega-projects, including the Dubai-Sharjah tramway, anchor additional residential clusters, boosting fresh tile uptake.

Renovation accelerates in hospitality, where brand audits impose strict upgrade cycles; Jumeirah Group alone budgets AED 1.5 billion for room overhauls through 2027. Apartment owners undertake kitchen and bathroom makeovers to capture resale premiums, sustaining DIY-store throughput. Government retrofits targeting energy performance create niches for reflective roof tiles and ventilated façades. Rising renter-to-owner transitions among expats spur internal flat renovations timed with handovers. Collectively, fresh groundbreaks plus cyclical upgrades fortify long-range visibility for the UAE tiles market.

By Distribution Channel: Traditional Retail Leads While Digital Channels Disrupt

Specialty retailers controlled a 43.85% share in 2025 because architects favor showrooms that curate large-format samples. Online sites, though smaller, posted a 6.55% CAGR on the back of easy price comparisons and 48-hour delivery guarantees. DIY chains service villa upgraders who opt for weekend installations aided by click-and-collect. Direct contractor sales thrive where developers bulk-order containers straight from factories, cutting mediator margins. AFAQ, the GCC instant-payment rail, trims cross-border settlement costs, helping distributors widen inventory across all emirates.

Omnichannel strategies emerge as legacy showrooms invest in AR visualization apps that replay virtual rooms over smartphones. E-commerce portals integrate with third-party installers, closing the value loop. DIY stores diversify into waterproofing ancillaries to raise basket size. Contractors embrace supplier web portals for just-in-time pallet drops to site cranes. The competitive race now revolves around speed, sample visualization, and end-to-end project logistics inside the UAE tiles market.

Geography Analysis

Dubai accounted for 45.12 of % UAE tiles market share in 2025, propelled by a 20% construction spike and a population tracking 4 million by 2026. Hotel room stock hit 154,000, and the AED 10 billion exhibition-center extension alone consumed nearly 200,000 m² of porcelain. Luxury-home transactions over USD 1 million climbed to 18.1% of total sales, raising spend on high-spec tiles. Smart-city pilots such as District 2020 encourage digital building envelopes that integrate sensor-embedded ceramic façades. The emirate's strategic positioning as a regional business hub attracts international companies requiring new office facilities, while its role as a luxury shopping destination drives retail space expansion that benefits tile demand. Dubai's advanced digital infrastructure and smart city initiatives create opportunities for innovative tile applications in technology-integrated buildings and public spaces.

Abu Dhabi ranks second by value as sovereign funds funnel capital into mixed-use waterfronts on Saadiyat and Al Maryah Islands. A 38,700-unit housing pipeline, plus a 34% jump in mortgages, accelerates ceramic demand. Apartment values rose 11.5% in 2024, pushing developers toward premium tile lines for differentiation. Cultural builds—Louvre Abu Dhabi extensions and Guggenheim foundations—order bespoke stoneware for galleries and walkways. The emirate's energy sector transformation, including renewable energy initiatives and the Barakah nuclear power plant, drives infrastructure development that benefits construction materials demand. Abu Dhabi's cultural and tourism initiatives, including major museum and entertainment projects, create opportunities for distinctive tile applications in high-profile public facilities. The emirate's strategic investments in technology and innovation, including AI and data center development, generate demand for specialized commercial tile applications in modern facility categories.

Sharjah and the Northern Emirates register the fastest 5.49% CAGR as manufacturers shift plants to lower-cost zones near Ras Al Khaimah. RAK’s economic plan caps sector dominance at 30% of GDP, opening ceramic clusters with tax incentives. Solar mandates push Fujairah villa roofs toward reflective clay formats. Affordable housing in Ajman and Umm Al-Quwain draws mid-range glazed imports. New free-trade zones at Khorfakkan Port simplify raw-material inflows, underpinning local tile production scalability across the UAE tiles market. The region's population growth, driven by affordable housing options and employment opportunities in manufacturing and logistics sectors, generates sustained residential tile demand. Others category, including Ajman, Umm Al-Quwain, Ras Al-Khaimah, and Fujairah, collectively represent emerging opportunities where development costs and government incentives attract both residential and commercial projects that require tile installations. The geographical distribution reflects the UAE's balanced development approach, with each emirate contributing unique strengths that collectively drive national tile market growth across diverse application categories and price segments.

Competitive Landscape

Competition is moderate, with the top five suppliers holding major market share in 2024 in the UAE ceramic tiles market. RAK Ceramics leverages four plants and 10,000 m² daily slab capacity to serve GCC turnkey contracts. Porcelanosa and Marazzi supply high-design collections through flagship Dubai Design District showrooms, targeting branded residences. Kajaria and Somany route Indian-made volumes via Jebel Ali re-export hubs, undercutting price points yet widening style portfolios. Atlas Concorde partners with local distributor Khalid Marwan to fast-track Italian stock for hotel refurbishments. Digital printing, large-slab presses, and eco-kilns feature heavily in CAPEX plans as firms vie for lead times and sustainability marks. Technology adoption is becoming a critical differentiator, with manufacturers investing in digital design capabilities, sustainable production processes, and supply chain optimization to compete effectively.

Supply-chain resilience counts; Gulf freight lanes benefit from the new AFAQ real-time payments network, smoothing multination invoicing. White-space niches include antimicrobial surfaces for hospitals and AI-designed mosaics customizable via app. Circular-economy entrants, such as TerraTile’s 100% recycled platform under ADQ backing, could steal share once institutional buyers pivot to green procurement. ISO 14001 stewardship certificates now appear in 80% of tender pre-qualifications, nudging laggards to retrofit plants. Small players may consolidate under private-equity roll-ups to gain volume rebates and digital commerce capabilities. he competitive landscape is influenced by regulatory compliance requirements, including ISO 9001 and ISO 14001 standards for quality and environmental management, as demonstrated by Arabian Ceramics' certification adherence. Market consolidation opportunities exist as smaller players seek scale advantages, while international expansion strategies focus on capturing the UAE's position as a gateway to broader Middle Eastern and African markets.

UAE Ceramic Tiles Industry Leaders

RAK Ceramics

Porcellan Co. LLC

Al Khaleej Ceramics

Marazzi Group

Kajaria Ceramics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: At INDEX Dubai, Aximer unveiled new porcelain stoneware series from Ceramiche Supergres, Famarella, and Saime.

- December 2024: Danube Home launched the Milano tile range, featuring Italian-inspired ceramic, wood-look, and porcelain lines.

- June 2024: SCS Global Services issued an Environmental Product Declaration for Arabian Ceramics porcelain tiles, validating a 75-year service life and 70% recyclability.

- April 2024: ADNEC Group partnered with Terrax to create TerraTile, a fully recycled modular flooring system backed by an AED 100 million R&D fund.

UAE Ceramic Tiles Market Report Scope

Ceramic tiles are made up of clay, water, and inorganic materials at high temperatures in a kiln. Ceramic tiles are highly durable and cost less than natural stone.

The UAE ceramic tiles market is segmented into product type, application, construction, and end users. The market is segmented by product type into glazed, porcelain, and scratch-free. By application, the market is segmented into floor tiles and wall tiles. The market is segmented by construction type into new construction, replacement, and renovation. By end user, the market is segmented into residential and commercial. The report offers market size and forecasts for the UAE ceramic tiles market in value (USD billion) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Abu Dhabi |

| Dubai |

| Sharjah & Northern Emirates |

| Others (Ajman, Umm Al-Quwain, Ras Al-Khaimah, Fujairah) |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Abu Dhabi | |

| Dubai | ||

| Sharjah & Northern Emirates | ||

| Others (Ajman, Umm Al-Quwain, Ras Al-Khaimah, Fujairah) | ||

Key Questions Answered in the Report

What is the current value of the UAE tiles market?

The UAE tiles market size is USD 0.97 billion in 2026 and is projected to reach USD 1.26 billion by 2031.

Which product category leads sales in the UAE?

Porcelain tiles dominate with 51.83% market share owing to their durability, low porosity, and premium aesthetics.

How fast are online tile sales growing in the UAE?

Online channels are expanding at a 6.55% CAGR as buyers embrace digital catalogs and rapid delivery options.

Why is renovation demand rising across the country?

A wave of buildings from the early 2000s is hitting refurbishment age, while hotels operate shorter upgrade cycles to stay competitive.

Which emirate shows the highest growth momentum?

Sharjah and the Northern Emirates post the fastest 5.49% CAGR, driven by industrial diversification and affordable housing projects.

Page last updated on: