Healthcare Automation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 44.75 Billion |

| Market Size (2030) | USD 69.06 Billion |

| Growth Rate (2025 - 2030) | 9.07% CAGR |

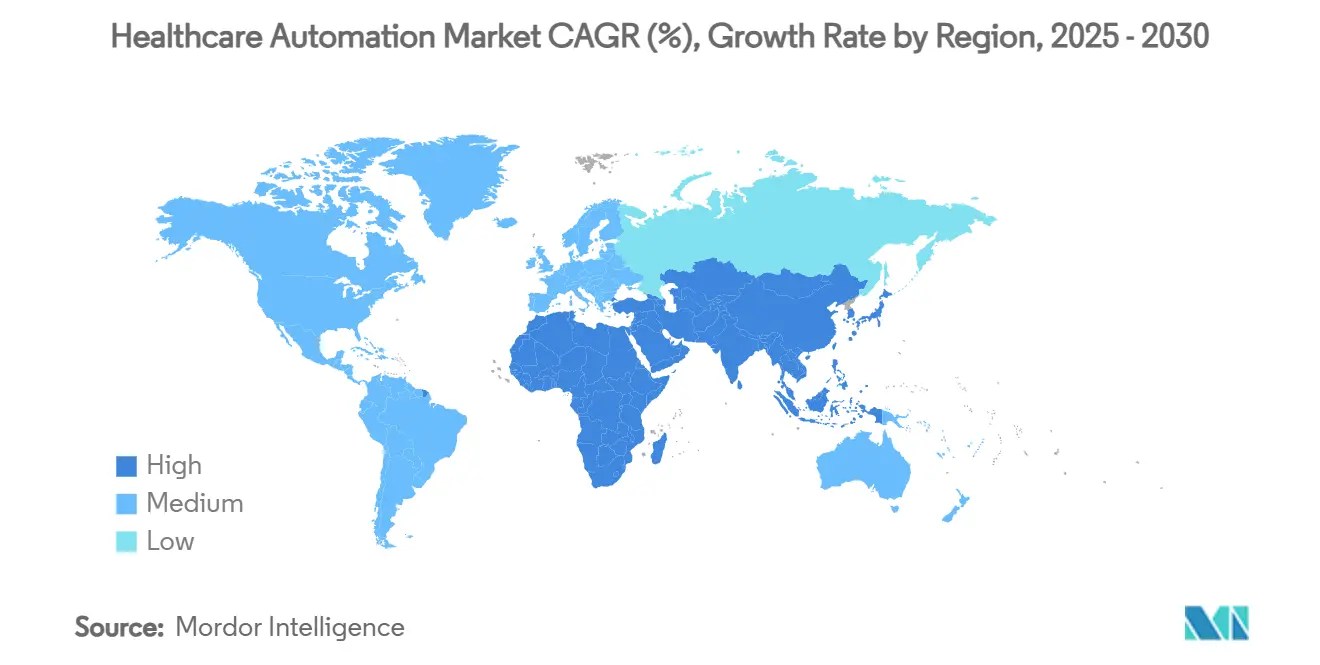

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Automation Market Analysis by Mordor Intelligence

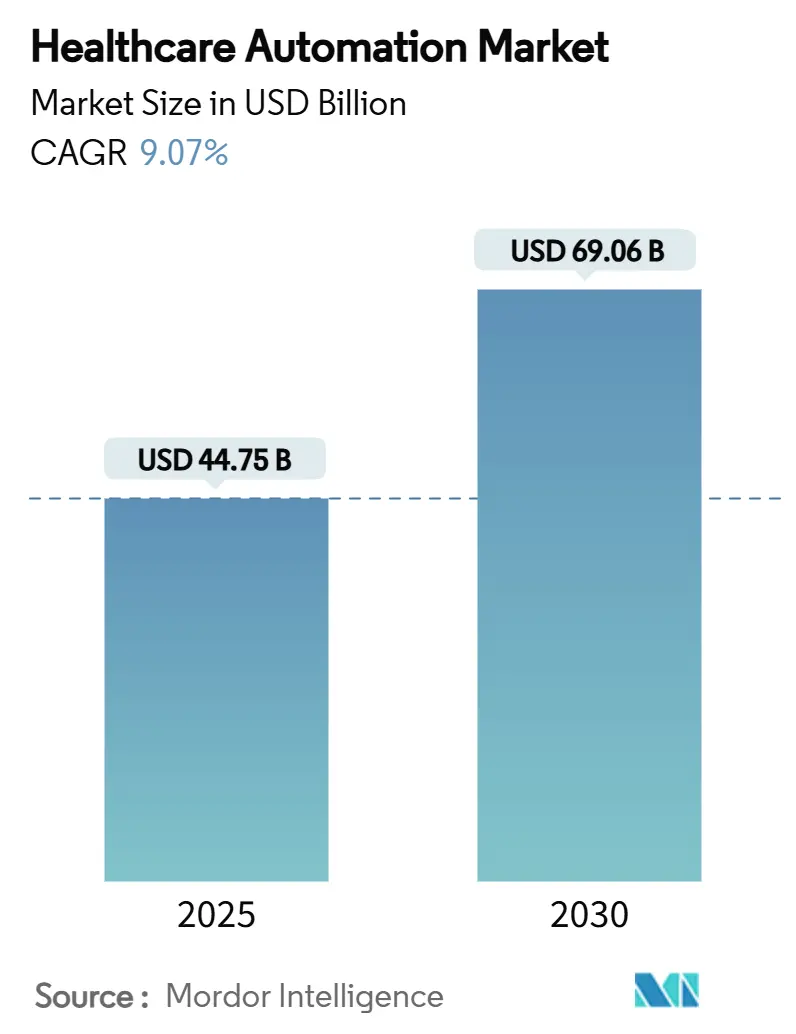

The healthcare automation market size stands at USD 44.75 billion in 2025 and is projected to reach USD 69.06 billion by 2030, advancing at a 9.07% CAGR over the forecast period. Continued investment stems from the need to counter clinician shortages, control labor expenses, and achieve consistent quality across care settings. Standardized automated workflows reduce medication errors, accelerate diagnostics, and free staff for direct patient engagement. Hardware remains the largest revenue contributor, yet managed services display the fastest expansion as providers favor turnkey deployments that lower internal IT burden. In regional terms, North America provides the largest installed base, while Asia-Pacific records the quickest uptake thanks to rapid infrastructure build-out and favorable government digitization policies. Consolidation among device manufacturers, AI specialists, and EHR vendors is reshaping competitive dynamics, signaling a shift toward integrated platforms rather than isolated tools.[1]U.S. Food and Drug Administration, “Artificial Intelligence and Machine Learning (AI/ML)-Enabled Medical Devices,” fda.gov

Key Report Takeaways

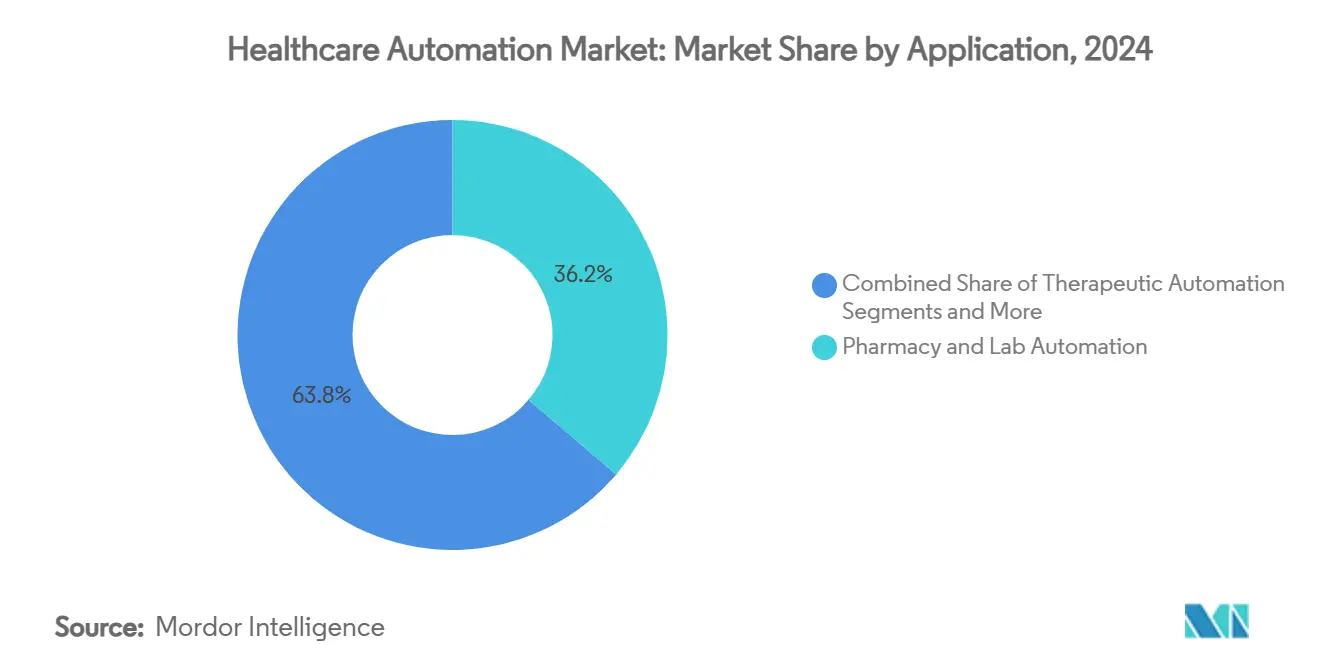

- By application, pharmacy and laboratory automation led with a 36.23% share in 2024, whereas telehealth and remote patient management is forecast to expand at a 13.55% CAGR to 2030.

- By component, hardware accounted for 51.24% of the healthcare automation market share in 2024, while services are set to grow fastest at 12.49% through 2030.

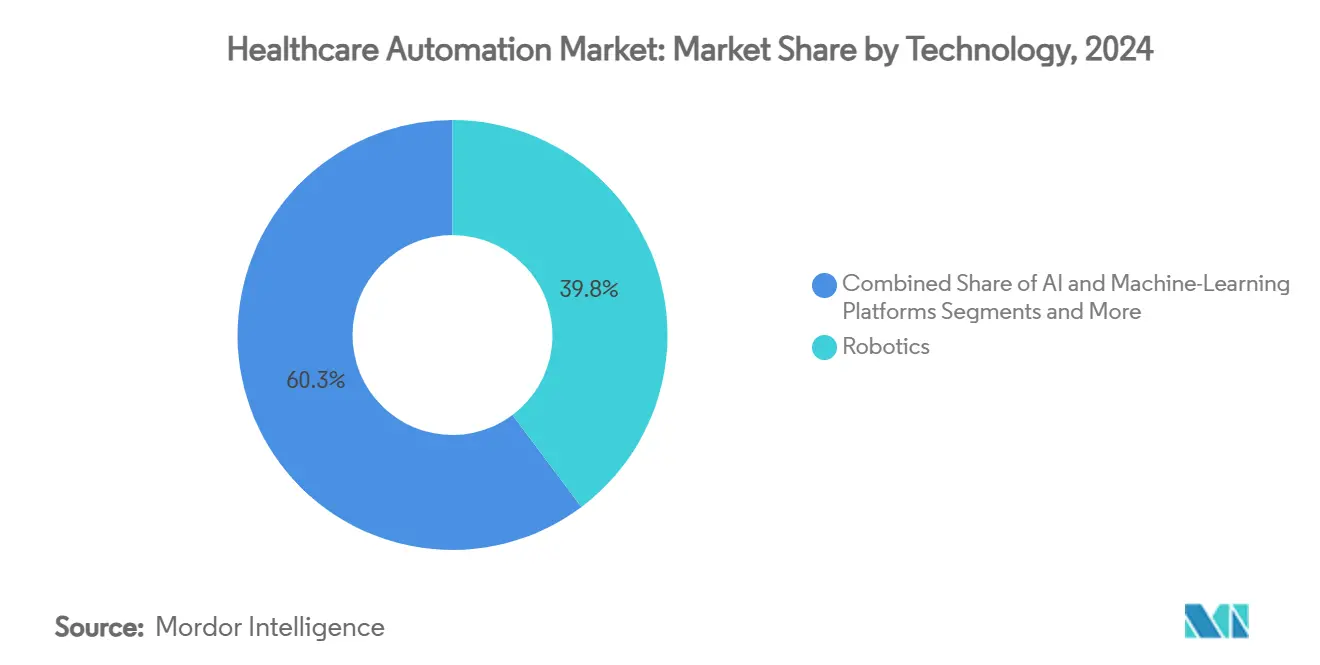

- By technology, robotics held 39.75% of the healthcare automation market size in 2024; AI and machine-learning platforms are poised for a 13.77% CAGR between 2025 and 2030.

- By end user, hospitals and surgical centers captured 45.67% of demand in 2024, although home healthcare and assisted-living facilities are on track to record the highest 12.73% CAGR by 2030.

- By geography, North America commanded 36.24% revenue in 2024, yet Asia-Pacific is projected to lead growth with an 11.35% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Healthcare Automation Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labor Costs & Clinician Shortages | + 1.8% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Need To Reduce Medication-Related Errors | + 1.2% | Global, priority in developed markets | Short term (≤ 2 years) |

| Rapid Adoption Of AI-Driven Surgical & Diagnostic Robots | + 1.5% | North America, Europe, expanding to APAC | Long term (≥ 4 years) |

| Regulatory Push For EHR Interoperability & Automation | + 0.9% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Decentralized "Micro-Hospital" Models Needing Compact Automation | + 0.7% | North America, pilot programs in Europe | Long term (≥ 4 years) |

| Value-Based Care Rewarding Automated Quality-Metric Capture | + 0.6% | North America, early adoption in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Labor Costs and Clinician Shortages

Global health systems face a workforce gap that automation helps close by reallocating staff to complex care duties. Nursing vacancies alone have driven annual supplemental labor costs near USD 90 billion in the United States, incentivizing investment in technologies that automate routine documentation, dispensing, and logistics tasks. Japan illustrates the fiscal upside as government programs subsidize robotic caregivers that support its aging population. As wage growth outpaces overall inflation, the return on automation capital remains compelling, especially for North American and European providers under acute staffing pressure. Strategic deployment of smart robots, AI scheduling, and automated pharmacy lines collectively increases throughput without proportional labor additions, enhancing the mid-term growth outlook of the healthcare automation market.

Need to Reduce Medication-Related Errors

An estimated 1.5 million Americans experience preventable medication harm each year, costing hospitals more than USD 3.5 billion. Automated dispensing cabinets, barcode medication administration, and AI-verified prescription platforms lower error rates by up to 85%, while delivering real-time inventory control that curtails waste. Facilities that integrated closed-loop pharmacy robotics report faster fulfillment and tighter regulatory compliance. Strong safety outcomes accelerate purchasing decisions, positioning medication automation as an early-stage priority worldwide.

Rapid Adoption of AI-Driven Surgical and Diagnostic Robots

The U.S. FDA had cleared more than 520 AI medical algorithms by mid-2024, and surgical robotics represents a rapidly growing portion of these approvals. Modern systems blend mechanical precision with machine-learning feedback that guides instrument movement and predicts complications. Hospitals adopting these technologies achieve shorter stays, reduced readmission risk, and higher surgeon efficiency. AI-enhanced diagnostic robots that automate blood morphology or pathology slide evaluation further amplify laboratory capacity. Long validation cycles lengthen the revenue ramp, yet the clear clinical upside supports sustained spending and lifts the long-term trajectory of the healthcare automation market.

Regulatory Push for EHR Interoperability and Automation

Mandates such as the U.S. 21st Century Cures Act require interoperable electronic records that share structured data. Harmonized data flows allow automated clinical decision support, RPA-enabled prior authorization, and seamless quality reporting. Vendors like Epic and Oracle align architectures with HL7 FHIR standards, opening pathways for tightly integrated automation across inpatient and outpatient settings. Regulatory clarity boosts purchaser confidence and strengthens mid-term adoption in North America and Europe.

Restraints Impact Analysis of Healthcare Automation Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX & Maintenance | -1.1% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Cyber-Security & Data-Privacy Vulnerabilities | -0.8% | Global, priority in developed markets | Medium term (2-4 years) |

| Algorithmic Bias & Medico-Legal Liability Of AI Systems | -0.7% | North America & Europe primarily | Long term (≥ 4 years) |

| Fragmented Device Standards Hindering Interoperability | -0.5% | Global, varying by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Maintenance

Comprehensive automation suites can exceed USD 1 million for a midsize hospital, including hardware, integration, and annual service contracts amounting to 15-20% of purchase price. Smaller providers and those in emerging markets struggle with such capital intensity, delaying adoption or limiting scope. Cloud-hosted solutions and subscription financing mitigate some burden yet cannot fully offset the steep initial outlay, tempering near-term expansion of the healthcare automation market.

Cyber-Security and Data-Privacy Vulnerabilities

Healthcare organizations suffer 25% more cyber incidents than other industries, and every new automated endpoint widens the attack surface. A breach can halt robotic pharmacies or compromise AI triage algorithms, creating direct patient-safety risk. Compliance frameworks such as HIPAA and GDPR demand encryption, segmentation, and continuous monitoring, pushing up total cost of ownership. Persistent threat evolution sustains this medium-term restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Healthcare Automation Market Segment Analysis

By Application:

Pharmacy Automation Drives Medication Safety RevolutionPharmacy and laboratory automation captured 36.23% of the healthcare automation market share in 2024, underlining the urgent global drive to prevent medication errors and accelerate specimen throughput. Automated dispensing, inventory analytics, and robotic sample processors tighten control and unlock rapid ROI, especially in high-volume hospitals. The segment’s mature evidence base and straightforward regulatory path sustain steady capital inflow.

Telehealth and remote patient management is the fastest-growing application at a 13.55% CAGR through 2030, energized by reimbursement parity for virtual visits and patient preference for home-based chronic-care monitoring. Connected devices feed AI triage engines that alert clinicians to deterioration, reducing avoidable admissions and nurturing cross-sell opportunities for platform vendors. Administrative workflow automation, diagnostic robotics, and medical logistics collectively broaden addressable revenue, ensuring the healthcare automation market continues its upward march.

By Component:

Service-Centric Models Accelerate AdoptionHardware preserved 51.24% of 2024 revenue, reflecting the sizeable ticket price of robots, imaging systems, and automated cabinets. Yet services record a 12.49% CAGR, revealing a clear shift toward managed deployments that guarantee uptime and relieve strained hospital IT teams. Subscription models covering installation, clinical training, and lifecycle upgrades transform CAPEX into predictable OPEX, especially attractive for community hospitals.

Software platforms deliver expanding value by orchestrating disparate devices, managing AI workflows, and generating compliance reports. Cloud-native architectures further reduce onsite footprint and allow rapid feature releases. This pivot to services and software elevates ecosystem thinking, encouraging providers to source from vendors able to bundle comprehensive offerings across the healthcare automation market.

By Technology:

AI Platforms Outpace Traditional MechanicsRobotics booked 39.75% of the healthcare automation market size in 2024, anchored by mature surgical systems and pharmacy robots. However, AI and machine-learning platforms surge ahead at a 13.77% CAGR, furnishing predictive analytics, autonomous navigation, and natural-language documentation. Facilities adopt AI layers that sit atop existing robots, extending utility without wholesale replacement.[2]Benjamin I. Rapoport, “Levels of Autonomy in FDA-Cleared Surgical Robots: A Systematic Review,” npj Digital Medicine, nature.com

Robotic process automation acts as an accessible on-ramp, automating claims and scheduling with minimal integration complexity. Automated imaging, diagnostic algorithms, and sensor-enabled IoT devices round out growth, collectively forming data-rich feedback loops that increase system intelligence. Vendor competitiveness now rests on the depth of AI toolsets rather than mechanical prowess alone.

By End User:

Home Healthcare Gains Strategic PriorityHospitals and surgical centers generated 45.67% of 2024 demand, owing to their scale and wide procedural mix. Most tertiary centers have already automated core pharmacy and OR functions, so incremental spend targets advanced AI modules and interoperable dashboards. Diagnostic laboratories keep expanding automation to handle swelling test volumes, addressing chronic technologist shortages.[3]Roche Diagnostics, “Top Lab Trends for 2025,” roche.com

Home healthcare and assisted-living facilities post the fastest 12.73% CAGR, supported by aging demographics and payer preference for lower-cost care settings. Remote-monitoring hubs, automated pill dispensers, and AI chatbots together build a virtual safety net that enables seniors to remain at home longer. Ambulatory clinics and payers also escalate adoption, proving that the healthcare automation market extends well beyond hospital walls.

Geography Analysis

North America Healthcare Automation Market

North America delivered 36.24% of global revenue in 2024 due to robust infrastructure, generous reimbursement, and clear regulatory pathways for AI-enabled devices. U.S. health systems leverage value-based payment schemes to justify rapid deployment, while Canada emphasizes nationwide access and continuity across its single-payer environment. Capital intensity remains manageable because scale allows multi-site rollouts that optimize asset utilization.

Europe Healthcare Automation Market

Europe maintains steady uptake driven by workforce scarcity, strict medication-safety mandates, and EU-wide digital strategies. Germany leads spending on integrated laboratory robotics, whereas the United Kingdom’s NHS funds AI scheduling and imaging tools to clear procedural backlogs. Southern European countries show rising interest, though budget allocation proceeds in phased tenders aligned with national e-health roadmaps.

APAC Healthcare Automation Market

Asia-Pacific records the highest 11.35% CAGR owing to large population bases, government digitization subsidies, and private investment into future-proof hospitals. China’s 14th Five-Year Plan earmarks funds for smart infrastructure, accelerating automated pharmacy and imaging installations. Japan focuses on elder-care robotics to offset workforce contraction, and Australia pioneers interoperable cloud diagnostics across rural regions. These dynamics collectively ensure that the healthcare automation market continues to diversify geographically.

Competitive Landscape

Market structure is moderately fragmented, with legacy device manufacturers vying against focused automation specialists and cloud-native AI entrants. Siemens Healthineers, GE HealthCare, and Medtronic expand portfolio breadth by integrating analytics layers and service contracts. Omnicell and Swisslog Healthcare maintain deep pharmacy expertise, while Epic and Oracle embed robotic process connectors within EHR suites to deepen client lock-in.

Consolidation intensifies as vendors seek platform completeness. Commure’s USD 139 million purchase of AI documentation firm Augmedix in 2024 demonstrated appetite for data-generation assets that enrich downstream automation modules. GE HealthCare partnered with Amazon Web Services to develop foundation models that underpin cloud diagnostic applications, whereas BD joined forces with Biosero to integrate robotic flow cytometry for drug discovery.

Strategic differentiation hinges on open APIs, cybersecurity stewardship, and outcomes-based contracting rather than hardware specs alone. Suppliers that guarantee seamless scaling from flagship hospitals to satellite clinics are best positioned to capture lifetime value across the expanding healthcare automation market.

Healthcare Automation Industry Leaders

Siemens Healthineers

GE HealthCare

BD

Intuitive Surgical

Koninklijke Philips N.V

- *Disclaimer: Major Players sorted in no particular order

Healthcare Automation Market Companies Covered in this Report

- Siemens Healthineers

- GE Healthcare

- Koninklijke Philips

- Medtronic

- Intuitive Surgical

- Stryker

- Beckton Dickinson

- Omnicell

- Mckesson

- Oracle

- Baxter

- Swisslog Healthcare

- IBM

- UiPath

- Optum

- Epic Systems

- Canon

- Johnson & Johnson

- Zebra Technologies

- Yuyama Co.

- Terumo

Recent Industry Developments in Healthcare Automation Market

- July 2025: Scopio Labs unveiled an AI system that automates blood-morphology analysis, removing manual microscope review and improving diagnostic turnaround.

- July 2025: Sheba Medical Center joined with Hippocratic AI to deploy generative agents that streamline patient navigation and documentation.

- March 2025: VisiQuate acquired Rotera to enlarge its AI-based revenue-cycle automation portfolio.

- March 2025: Talkdesk released purpose-built AI agents that automate healthcare contact-center workflows.

Global Healthcare Automation Market Report Scope

Segmentation Overview

| Diagnostics & Monitoring Automation |

| Therapeutic Automation |

| Pharmacy & Laboratory Automation |

| Medical Logistics & Training Automation |

| Administrative & Workflow Automation |

| Tele-health & Remote Patient Management Automation |

| Hardware (Robots, Devices, ADCs) |

| Software (AI, RPA, Middleware) |

| Services (Implementation, Managed, Training) |

| Robotics |

| AI & Machine-Learning Platforms |

| Robotic Process Automation (RPA) & Software Bots |

| Automated Medication Dispensing & Storage Systems |

| Automated Imaging & Diagnostics Platforms |

| Wearable Sensor & IoT Automation |

| Hospitals & Surgical Centers |

| Diagnostic Laboratories |

| Retail & Hospital Pharmacies |

| Ambulatory & Specialty Clinics |

| Home Healthcare & Assisted-Living Facilities |

| Payers & Health Insurance Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Diagnostics & Monitoring Automation | |

| Therapeutic Automation | ||

| Pharmacy & Laboratory Automation | ||

| Medical Logistics & Training Automation | ||

| Administrative & Workflow Automation | ||

| Tele-health & Remote Patient Management Automation | ||

| By Component | Hardware (Robots, Devices, ADCs) | |

| Software (AI, RPA, Middleware) | ||

| Services (Implementation, Managed, Training) | ||

| By Technology / Automation Type | Robotics | |

| AI & Machine-Learning Platforms | ||

| Robotic Process Automation (RPA) & Software Bots | ||

| Automated Medication Dispensing & Storage Systems | ||

| Automated Imaging & Diagnostics Platforms | ||

| Wearable Sensor & IoT Automation | ||

| By End User | Hospitals & Surgical Centers | |

| Diagnostic Laboratories | ||

| Retail & Hospital Pharmacies | ||

| Ambulatory & Specialty Clinics | ||

| Home Healthcare & Assisted-Living Facilities | ||

| Payers & Health Insurance Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the healthcare automation market in 2025?

It is valued at USD 44.75 billion and is projected to reach USD 69.06 billion by 2030.

Which application segment leads spending?

Pharmacy and laboratory solutions hold 36.23% of 2024 revenue, driven by urgent medication-safety and lab-throughput needs.

What region will grow fastest through 2030?

Asia-Pacific is forecast to post an 11.35% CAGR as governments fund smart hospitals and aging-care robotics.

Why are services expanding faster than hardware?

Providers opt for managed, subscription models that shift capital purchases into predictable operating expenses, propelling a 12.49% CAGR for services.

What is the main restraint to wider adoption?

High upfront capital and maintenance costs remain the strongest brake, especially for small hospitals and emerging-market facilities.

How is AI changing surgical automation?

FDA-cleared robots now pair mechanical precision with learning algorithms that guide instrument paths and predict complications, improving outcomes and utilization.

Page last updated on: