Patient Infotainment Terminal Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

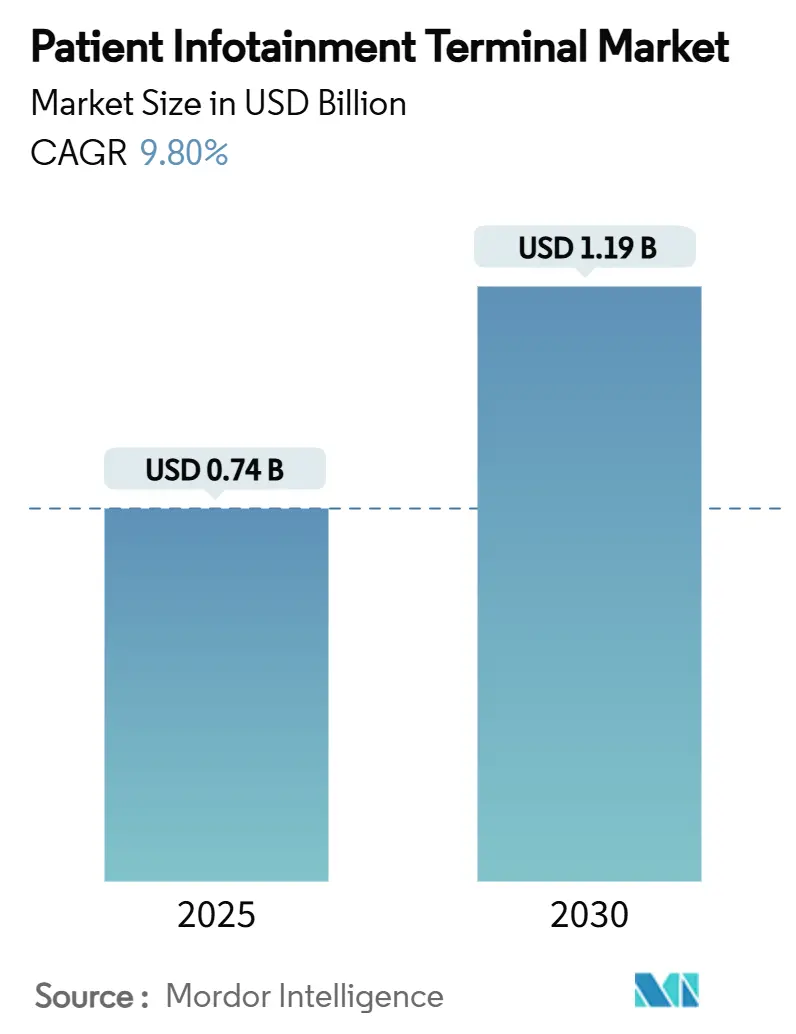

| Market Size (2025) | USD 0.74 Billion |

| Market Size (2030) | USD 1.19 Billion |

| Growth Rate (2025 - 2030) | 9.80% CAGR |

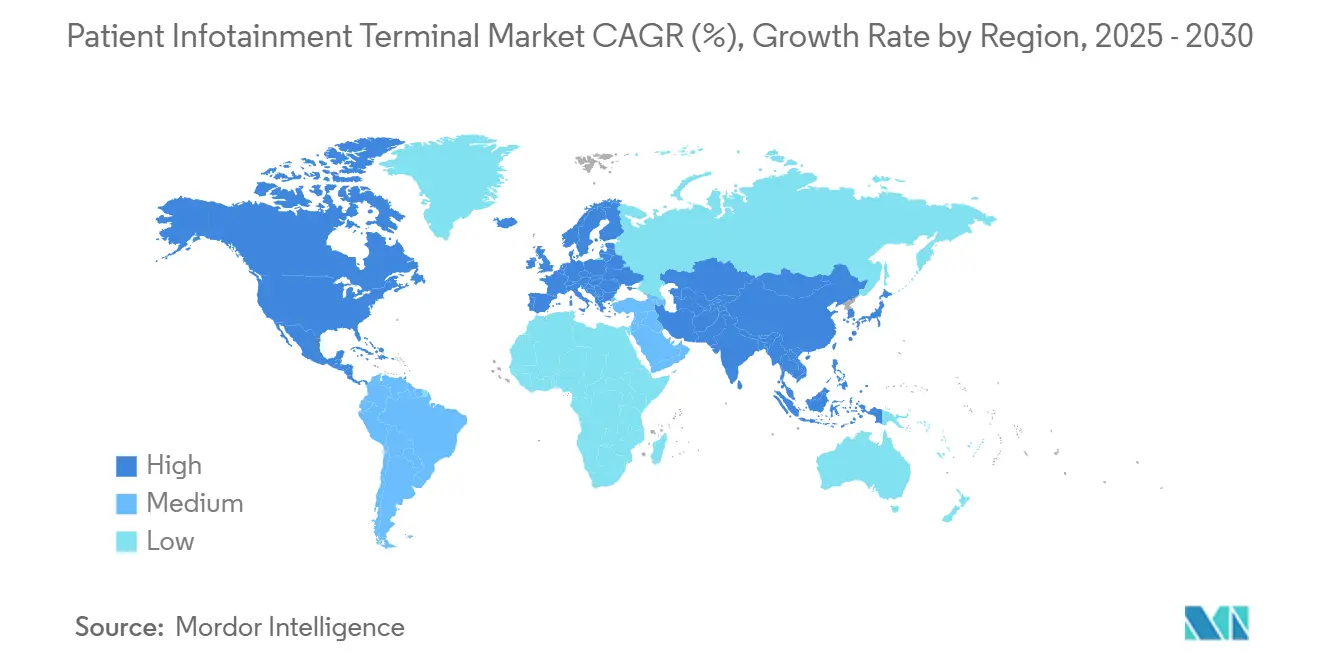

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Infotainment Terminal Market Analysis by Mordor Intelligence

The patient infotainment terminal market size reached USD 0.74 billion in 2025 and is forecast to expand at a 9.8% CAGR, lifting value to USD 1.19 billion by 2030. Smart-hospital programs, HCAHPS-linked reimbursement, and workforce automation jointly power this upward curve for the patient infotainment terminal market. Hospitals now specify integrated engagement platforms that collapse education, entertainment, telehealth, and clinical workflow into a single point of care. Medium displays dominate because they balance cost and functionality, yet large screens are growing fast as aging-care needs reshape display ergonomics. Regulatory incentives, especially the U.S. Hospital Value-Based Purchasing Plan, continue to convert patient-experience technology from a discretionary purchase into an ROI-visible investment that can buffer penalty risk.

Key Report Takeaways

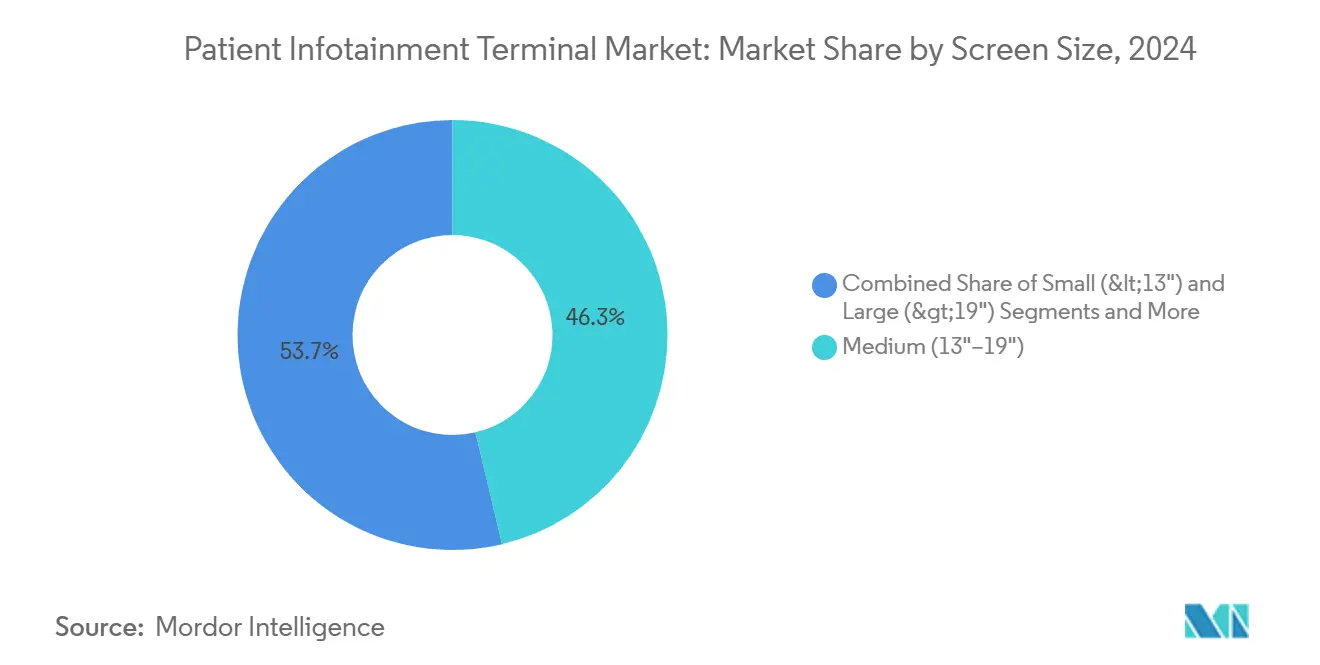

- By screen size, medium displays held 46.3% of patient infotainment terminal market share in 2024.

- By end user, hospitals accounted for 58.1% of the patient infotainment terminal market size in 2024 while home-care and RPM use cases are expanding at 9.8% CAGR to 2030.

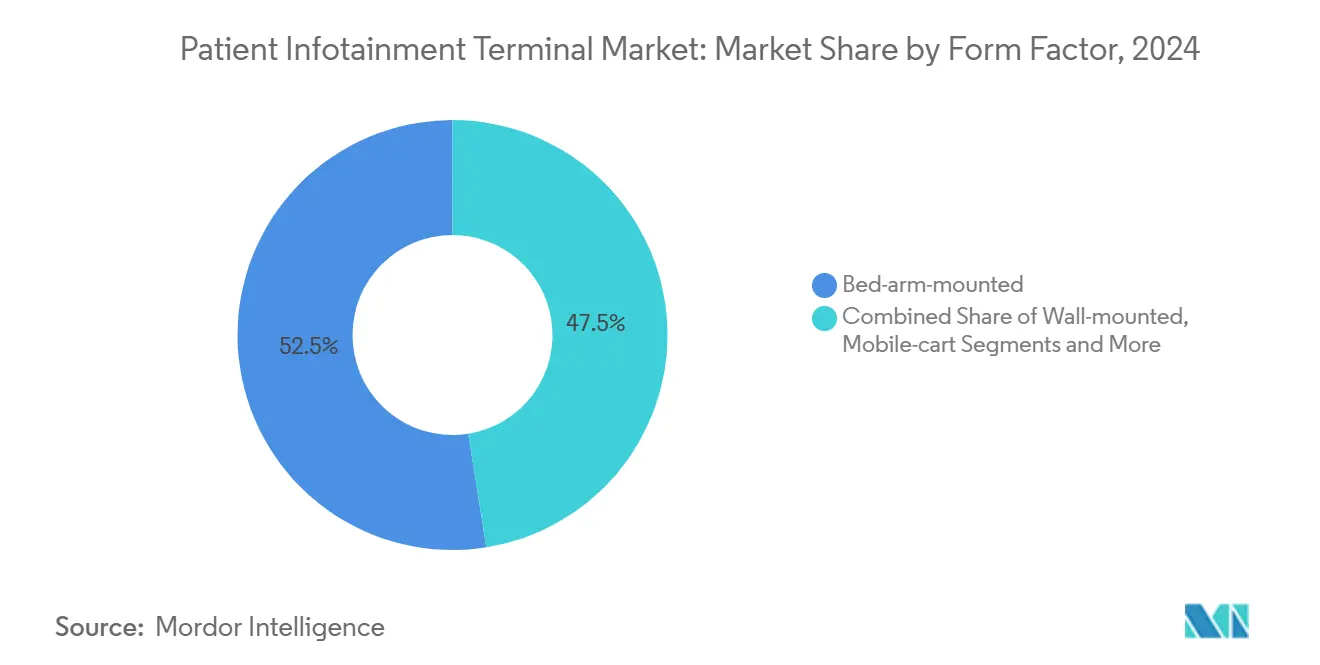

- By form factor, bed-arm-mounted units led with 52.5% share of the patient infotainment terminal market in 2024; handheld and tablet formats are advancing at 9.6% CAGR through 2030.

- By geography, North America commanded 35.4% revenue share in 2024 whereas Asia Pacific is projected to grow at a 10.8% CAGR to 2030.

Global Patient Infotainment Terminal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient-experience-linked reimbursement | +2.10% | North America & EU | Medium term (2-4 years) |

| Smart-hospital digitization & EHR integration | +1.80% | Global | Long term (≥ 4 years) |

| PoE, Wi-Fi 6 & antimicrobial touchscreens | +1.30% | Global | Short term (≤ 2 years) |

| Aging in-patient population | +1.70% | APAC; spill-over to North America & EU | Long term (≥ 4 years) |

| Tele-health reimbursement | +1.40% | North America & EU | Medium term (2-4 years) |

| Staffing shortages & self-service controls | +1.20% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Patient-Experience-Linked Reimbursement Pressure Transforms Hospital Priorities

Hospital payment formulas now tie a larger fraction of revenue to HCAHPS and similar patient-satisfaction indices. The 2025 CMS revision extended survey windows to 49 days, making every inpatient touchpoint measurable.[1]Becker’s Hospital Review Staff, “CMS Extends HCAHPS Collection Window,” beckershospitalreview.com Bedside terminals help collect real-time feedback, deliver on-demand education, and support service recovery workflows that can lift satisfaction scores within a quarter. U.S. systems increasingly treat terminals as cost-avoidance tools because improved HCAHPS metrics shield up to 2% of base DRG payments. European trusts following NHS Friends & Family logic mirror this shift, turning legacy entertainment screens into multi-service engagement hubs that feed quality dashboards.

Rapid Smart-Hospital Digitization Accelerates EHR Integration Demands

Eighty-five percent of health systems plan to embed generative-AI tools by 2025, and patient infotainment terminals form the final display layer for many of those initiatives. Hospitals now specify real-time connectivity with Epic, Cerner, or Meditech along with single sign-on that aligns with nursing badge workflows. Vendors offering middleware that bridges HL7, FHIR, nurse-call, and RTLS gain procurement preference over pure hardware suppliers. The patient infotainment terminal market thus rewards platform breadth and cybersecurity maturity. Integrated devices reduce duplicate logins, lessen alert fatigue, and cut average nurse documentation time by almost 7%, freeing staff capacity amid labor shortages.

PoE and Wi-Fi 6 Infrastructure Advances Reduce Total Cost of Ownership

Hospitals that upgrade access points to Wi-Fi 6 record 30% network-efficiency gains and smoother 4K video streams for inpatient tele-rounds. Coupled with PoE, facilities can hang terminals without separate electrical permits, trimming installation outlays by as much as 40%. Antimicrobial touchscreens lower daily wipe-down frequency yet maintain infection-control compliance, yielding incremental savings on cleaning supplies and staff time. These cost offsets shorten project payback to 18-24 months, convincing CFOs who previously paused capital plans. As procurement teams blend total cost into RFP scoring, the patient infotainment terminal market continues shifting toward PoE-ready, Wi-Fi 6-certified products.

Aging Population Demographics Drive Bedside Engagement Adoption

By 2030, one in six people worldwide will be over 60, and U.S. adults ≥ 65 will reach 81 million.[2]Nordic Global Health, “Global Aging Trends 2025-2030,” nordicglobal.com Longer stays and multimorbidity raise the need for larger fonts, voice interaction, and medication coaching at the bedside. Terminals that surface lab trends and self-service meal ordering improve autonomy, a key driver of satisfaction among geriatric cohorts. In APAC, super-aging societies push governments to subsidize smart wards with engagement tech that eases nurse workloads while maintaining family communication. Vendors that tune UI for diminished dexterity and cognition gain share as the patient infotainment terminal market aligns with senior-friendly design norms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure & uncertain ROI | -1.90% | Global | Short term (≤ 2 years) |

| Stringent data-privacy & cybersecurity regulations | -1.50% | North America & EU | Medium term (2-4 years) |

| Infection-control compliance limits hardware options | -0.80% | Global | Long term (≥ 4 years) |

| BYOD adoption dilutes demand for fixed bedside hardware | -1.10% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure Challenges Hospital Investment Decisions

Unit prices that range from USD 2,000 to USD 8,000, once installation and HL7 integration are counted, stretch capital budgets already strained by inflation. Post-pandemic margin compression leaves smaller hospitals below the 3% operating margin that many boards set as a trigger for discretionary tech. Breach costs averaging USD 9.77 million divert funding to cybersecurity basics, pushing bedside rollouts to later years. ROI typically materializes after three fiscal cycles, yet board mandates often demand a two-year payback. The resulting capex reluctance slows replacement of ten-year-old systems and elongates the refresh window in the patient infotainment terminal market.

Cybersecurity Regulations Impose Significant Compliance Burdens

Proposed 2025 HIPAA updates remove the “addressable” option and insist on multi-factor authentication, encrypted data at rest, and quarterly pen tests. First-year compliance will cost U.S. providers USD 9.3 billion.[3]National Law Review Editors, “Proposed HIPAA Security Rule Update 2025,” natlawreview.com Terminals must now support zero-trust segmentation and tamper-proof firmware, adding roughly 8-10% to the bill of materials. EU hospitals face parallel GDPR device-hardening rules. Procurement teams, therefore, rank NIST-aligned security roadmaps above aesthetic or display-resolution specs. Vendors unable to certify against UL 2900 or IEC 62304 risk exclusion, tightening market entry for new hardware entrants in the patient infotainment terminal market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Screen Size: Medium Displays Balance Functionality and Cost Efficiency

Medium screens delivered 46.3% of 2024 revenue, anchoring their role as default choice across most ward types. This cohort blends 1080p clarity with easy arm-mount ergonomics at a price point CFOs deem sustainable, ensuring steady demand inside the patient infotainment terminal market. OEMs scale volume on this sweet spot, keeping panel costs low even when antimicrobial glass and PoE requirements layer in.

Large panels above 19 inches record 10.2% CAGR to 2030 as geriatric and bariatric wards favor bigger fonts and split-view care dashboards. Small displays drop to niche status outside pediatrics or space-constrained step-down rooms. In parallel, 4K adoption inches upward, driven by tele-stroke and radiology consults that need high pixel density. Vendors able to migrate Android-based UI fluidly across size classes defend share while new entrants target specialty large-display sub-segments within the patient infotainment terminal market.

By End User: Hospitals Drive Core Demand While Home Care Emerges

Hospitals own 58.1% of 2024 unit shipments, reflecting in-house EHR integration and built-in networking budgets. Consolidated IDN buying groups standardize on two to three approved vendors, generating multi-year refresh contracts that stabilize the patient infotainment terminal market size for acute-care sites. The hospital-at-home model, reimbursed in 37 U.S. states, unlocks 9.8% CAGR for home-care deployments through tablet replacements that ship pre-imaged with remote-monitoring apps.

Long-term care and specialty surgery centers fill the remaining volume at modest growth rates. Their adoption hinges on visitor-management integration and resident entertainment packages. As CMS pilots expand hospital-at-home DRGs, DIY installation kits and LTE-backed units accelerate, loosening the acute-care stranglehold on the patient infotainment terminal market.

By Form Factor: Mobility Trends Challenge Fixed Installation Dominance

Bed-arm-mounted terminals retained a 52.5% share in 2024 thanks to proven cable management, ease of cleaning, and stable viewing angles. They remain indispensable in ICUs where line-of-sight to vitals and pumps cannot be compromised. Yet handheld and tablet devices are growing at 9.6% CAGR as infection-control and flexible-seating layouts push care teams toward clean-and-go hardware.

Wall screens persist in surgical prep bays where articulated arms may hinder turnover. Mobile carts resurface when hospitals retrofit older towers without modern cabling. Infection-control policy that mandates daily UV-C disinfection favors sealed mobile tablets that dock wirelessly. The coexistence of fixed and mobile hardware keeps the patient infotainment terminal market diversified, with OEM roadmaps increasingly modular to cross-leverage design spend.

By Functionality: Integration Complexity Drives Platform Consolidation

Platforms combining education, EHR charting, and nurse-call captured 40.6% share in 2024. One API surface eases IT maintenance and reduces training hours, which clinched many of the year’s RFQs. Telehealth-enabled models expand at 8.4% CAGR because virtual ward rounds save physicians travel time and permit on-demand specialty input.

Entertainment-only gear enters sunset as streaming services become expected rather than novel. Next-phase rollouts emphasize ambient voice agents that transcribe conversation or summon environmental controls. Vendors differentiate less on silicon and more on middleware breadth, a pivot that reshapes competitive stakes across the patient infotainment terminal market.

Geography Analysis

North America led with 35.4% share in 2024, leveraging mature reimbursement policies and high EHR saturation to justify premium feature sets in the patient infotainment terminal market. While new HIPAA security clauses raise compliance spend, IDNs still push forward refresh cycles to protect HCAHPS payout. Vendor evaluation now weighs SOC 2 letters and zero-trust blueprints more than bezel color or speaker wattage.

Asia Pacific posts the fastest trajectory at 10.8% CAGR to 2030. Governments in China and India are digitizing tier-2 hospitals through subsidy programs capped at 5% of national GDP, widening the addressable base. Japan and South Korea, wrestling with super-aging curves, underwrite smart-ward pilots that spotlight continuous engagement. Regulatory heterogeneity persists, but local SI alliances unlock deployment at speed, sustaining momentum in this slice of the patient infotainment terminal market.

Europe maintains steady adoption as GDPR sets strict device hardening and audit logging baselines. Nordic health systems rank highest on bedside penetration thanks to nation-wide EPR rollouts, while southern member states catch up via EU-funded resilience grants. Energy-efficiency labels influence procurement, nudging vendors to publish carbon-intensity data for plastics and packaging to remain on supplier rosters.

Competitive Landscape

The patient infotainment terminal market remains moderately fragmented. Barco, Advantech, and Siemens Healthineers leverage bundled imaging and informatics portfolios that ease enterprise agreement sign-off. Advantech’s February 2025 HIT-507 launch adds Intel Celeron horsepower and 10-point touch for sub-USD 2,500 SKUs, courting price-sensitive buyers. Siemens’ Ciartic Move C-arm showcases synergy between surgical imaging and bedside displays for intraoperative patient education.

New entrants advance through software and cloud. Samsung’s July 2025 Xealth buy delivers proprietary app distribution, giving clinicians a controlled ecosystem on consumer-grade Galaxy hardware that can displace legacy arm mounts. Stryker’s care.ai acquisition folds virtual sitter AI into existing beds and stretchers, underscoring a shift from screen resolution wars to algorithm depth.

Partnerships define defense strategies. AvaSure, Oracle, and NVIDIA built an AI concierge that taps hospital LLMs to triage patient requests and translate top-used languages on-device, reducing nurse call frequency. GE HealthCare’s AWS alliance seeds generative AI co-pilots into telemetry dashboards, and Prisma Health’s 1,500 smart bed order aligns Hercules repositioning data with bedside interfaces for falls prevention. Such integrations lock in multi-year revenue streams and raise switching costs inside the patient infotainment terminal market.

Patient Infotainment Terminal Industry Leaders

Barco NV

PDi Communication Systems Inc.

Advantech Co. Ltd.

BEWATEC Kommunikationstechnik GmbH

Siemens Healthineers (HiMed)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Samsung acquired Xealth to accelerate connected-care capabilities, expanding software-centric engagement offerings.

- May 2025: Emory Healthcare opened the first U.S. hospital run entirely on Apple devices integrated with Epic, demonstrating consumer-grade hardware viability in regulated settings.

- April 2025: Transcarent merged with Accolade for USD 621 million, forming a 20-million-member platform that extends patient engagement beyond hospital walls.

- March 2025: AvaSure, Oracle, and NVIDIA launched an AI-powered virtual concierge for inpatient rooms.

Global Patient Infotainment Terminal Market Report Scope

| Small (<13") |

| Medium (13"-19") |

| Large (>19") |

| Hospitals |

| Long-term Care Facilities |

| Specialty Clinics & Day-Surgery Centers |

| Home-care / Remote Patient Monitoring |

| Bed-arm-mounted Terminals |

| Wall-mounted Terminals |

| Mobile-cart Terminals |

| Handheld / Tablet Terminals |

| Entertainment-only |

| Integrated (Edu + EHR access) |

| Tele-health-enabled |

| Multi-modal (room & nurse-call integration) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Screen Size | Small (<13") | |

| Medium (13"-19") | ||

| Large (>19") | ||

| By End User | Hospitals | |

| Long-term Care Facilities | ||

| Specialty Clinics & Day-Surgery Centers | ||

| Home-care / Remote Patient Monitoring | ||

| By Form Factor | Bed-arm-mounted Terminals | |

| Wall-mounted Terminals | ||

| Mobile-cart Terminals | ||

| Handheld / Tablet Terminals | ||

| By Functionality | Entertainment-only | |

| Integrated (Edu + EHR access) | ||

| Tele-health-enabled | ||

| Multi-modal (room & nurse-call integration) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the patient infotainment terminal market in 2025?

The patient infotainment terminal market size stands at USD 0.74 billion in 2025 and is projected to reach USD 1.19 billion by 2030 at a 9.8% CAGR.

Which segment leads by screen size?

Medium displays between 13 and 19 inches held 46.3% of 2024 revenue owing to balanced ergonomics and cost.

What region grows fastest through 2030?

Asia Pacific posts the quickest expansion at a 10.8% CAGR, propelled by government smart-hospital programs and aging demographics.

Which form factor is gaining share?

Handheld and tablet bedside devices are advancing at 9.6% CAGR as infection-control and mobility priorities rise.

Why are hospitals investing despite capital pressures?

HCAHPS-linked reimbursement and smart-hospital roadmaps make patient infotainment terminal a direct lever for patient-experience scores and workforce efficiency gains.

Page last updated on: