Dye Sublimation Printing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

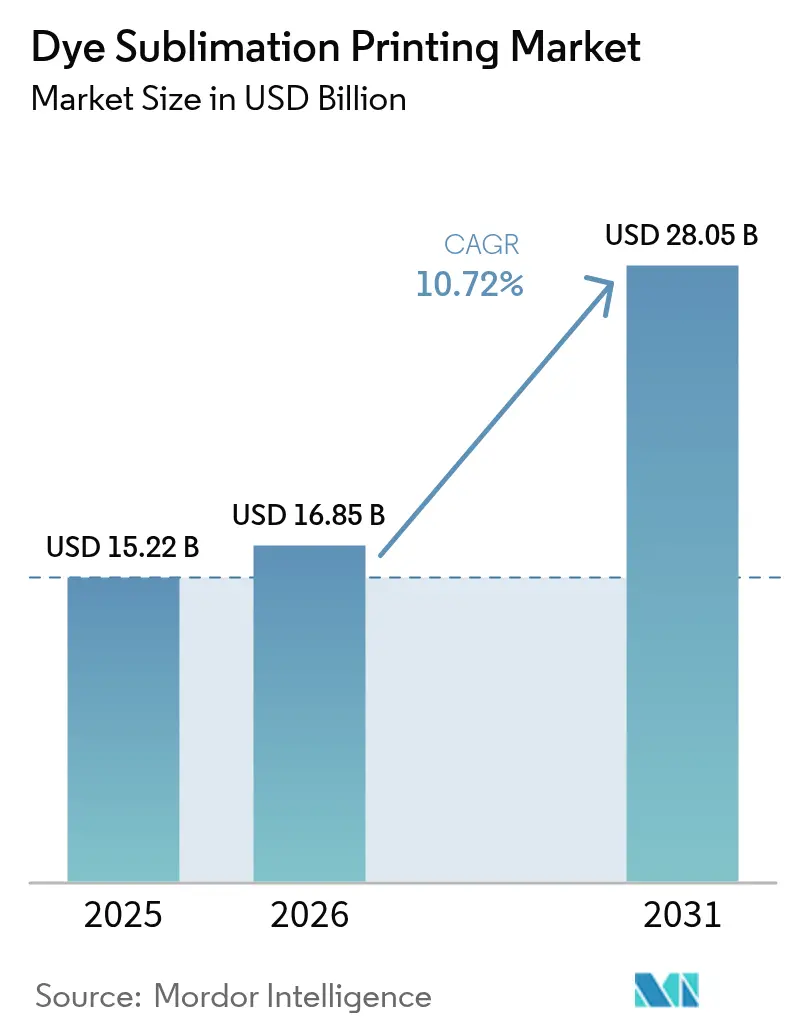

| Market Size (2026) | USD 16.85 Billion |

| Market Size (2031) | USD 28.05 Billion |

| Growth Rate (2026 - 2031) | 10.72% CAGR |

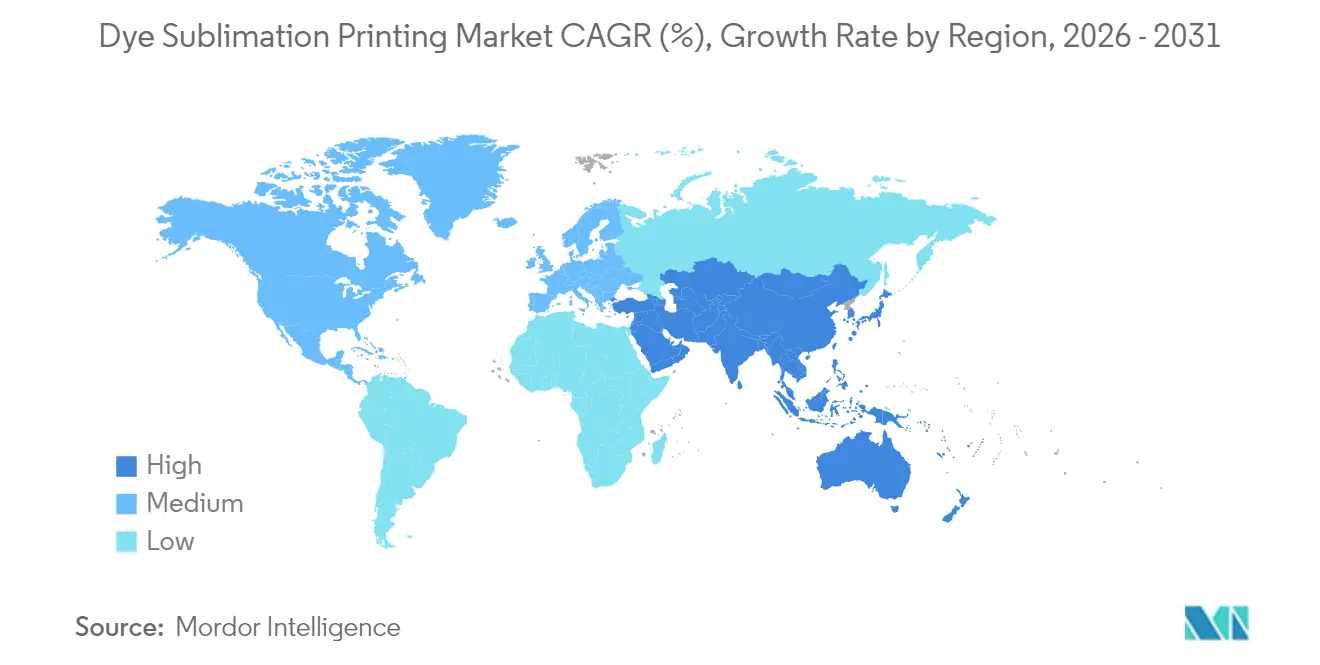

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dye Sublimation Printing Market Analysis by Mordor Intelligence

The dye sublimation printing market size is expected to grow from USD 15.22 billion in 2025 to USD 16.85 billion in 2026 and is forecast to reach USD 28.05 billion by 2031 at 10.72% CAGR over 2026-2031. Demand is intensifying as sports-apparel, automotive interiors, and décor brands seek photo-realistic graphics that can be produced at speed with minimal water use. Manufacturers are countering polyester feedstock inflation by investing in high-speed industrial lines that cut total cost of ownership while maintaining quality and consistency. Strategic capacity additions by printhead and equipment suppliers have also stabilized lead times, allowing converters to accept short-run personalized orders without jeopardizing large-volume contracts. On the sustainability front, tighter global regulations on water and PFAS emissions continue to nudge converters toward water-free sublimation technologies and bio-based polyester substrates, creating a double incentive for equipment upgrades.

Key Report Takeaways

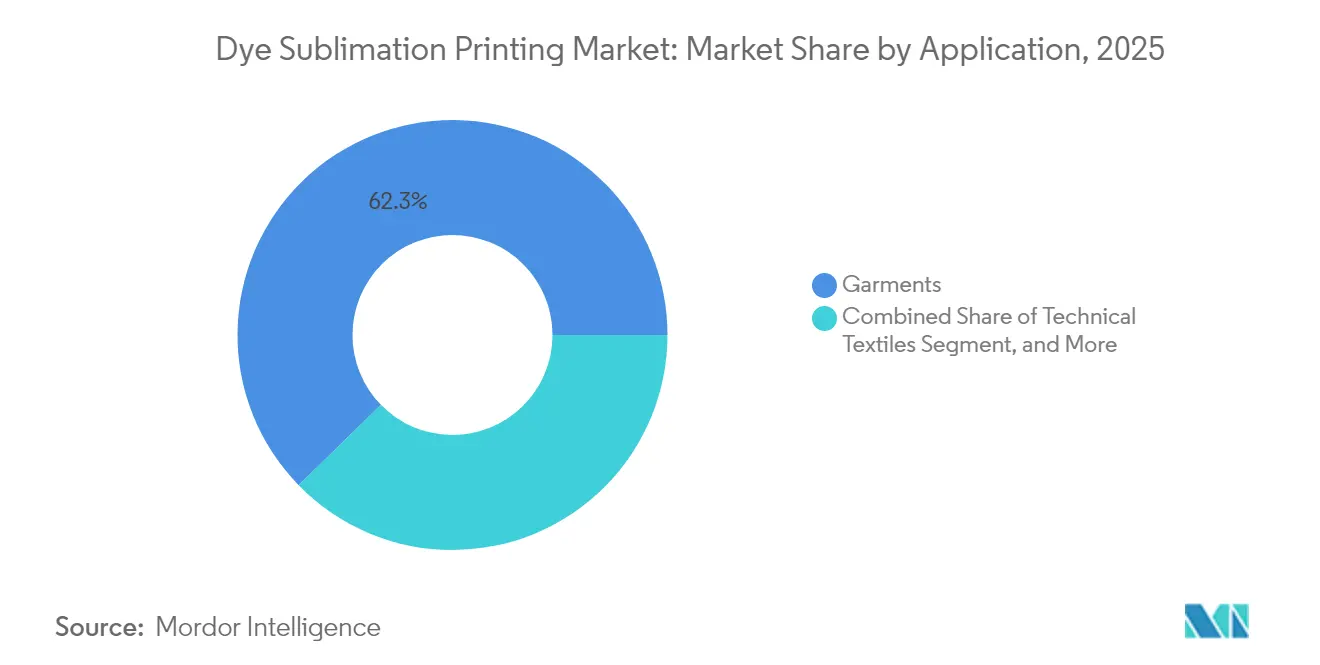

- By application, garments captured 62.31% revenue share in 2025; technical textiles is forecast to expand at an 10.98% CAGR to 2031.

- By printer type, wide-format systems led with 55.74% of the dye sublimation printing market share in 2025, while industrial platforms are projected to grow at 11.76% CAGR through 2031.

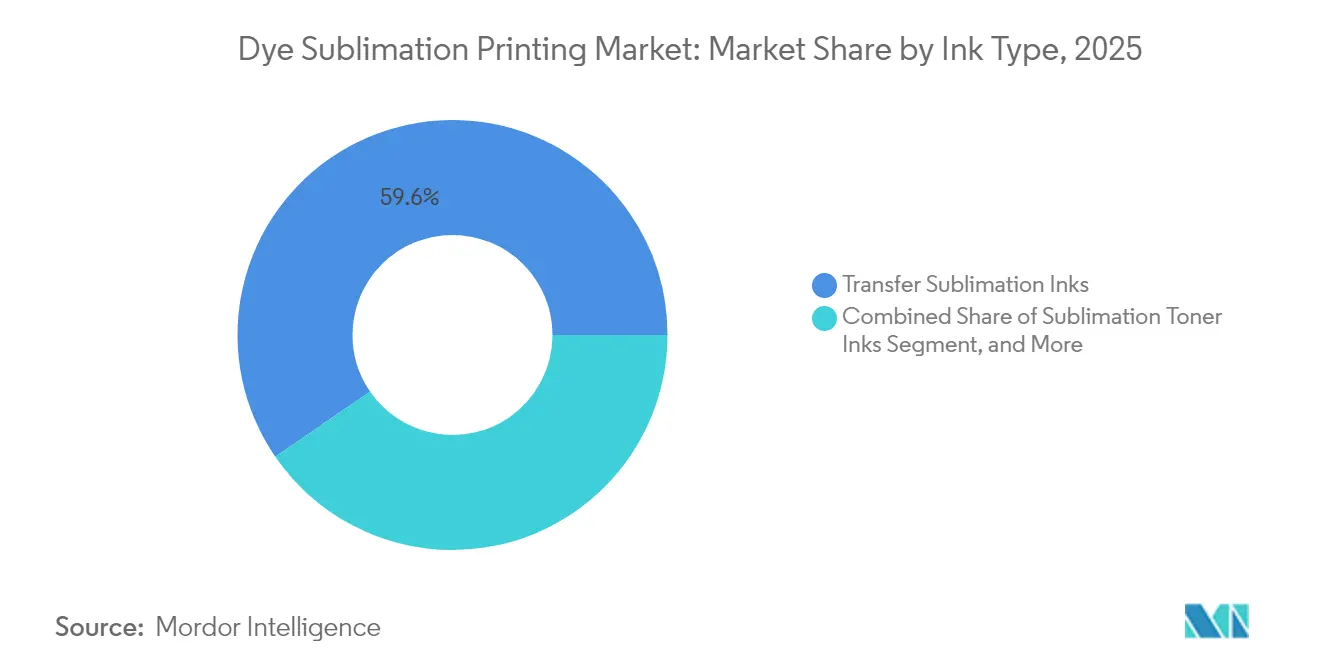

- By ink type, transfer formulations accounted for a 59.58% share of the dye sublimation printing market size in 2025, and direct-to-fabric inks are set to advance at a 12.13% CAGR over the forecast horizon.

- By substrate, polyester fabrics dominated with a 64.71% share in 2025; hybrid technical textiles are expected to rise at a 11.86% CAGR between 2026 and 2031.

- By geography, Asia-Pacific commanded a 40.11% share in 2025 and is projected to register the fastest regional growth at 12.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dye Sublimation Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in customized sports and fashion apparel | +2.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Shift to water-efficient digital textile processes | +2.1% | Global, most pronounced in the EU | Long term (≥ 4 years) |

| High-speed industrial printer launches lowering TCO | +1.9% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| AI-driven design-to-print software adoption | +1.6% | North America and EU, expanding in Asia-Pacific | Medium term (2-4 years) |

| EV interior technical-textile demand surge | +1.4% | China, EU, North America | Long term (≥ 4 years) |

| Bio-based polyester enabling sustainable sublimation | +1.2% | EU and North America, gradual adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Boom in customized sports and fashion apparel

Customization has moved from a nice-to-have to a purchase driver as clubs, collegiate teams, and independent brands commit to on-demand micro-factory models that slash inventory risk. Contract manufacturers that previously relied on screen printing are now adopting digital sublimation lines to handle full-coverage graphics in multiple colorways without incremental setup costs. Cisco Athletic exemplifies the shift by offering unlimited colors and placement options at a flat price, showing buyers that complexity no longer carries a penalty. Teams benefit from two-week lead times, while converters enjoy healthier margins due to lower waste and fewer returns. The same infrastructure is now serving fashion capsules and influencer-led drops, widening the installed base of sublimation equipment. As consumer surveys link brand loyalty to environmental transparency, on-demand production also supports corporate emissions goals by eliminating dead inventory and secondary transport legs.

Shift to water-efficient digital textile processes

Sublimation’s water-free transfer mechanism has become an environmental-compliance shortcut as regulators escalate pressure on wet-processing mills. Operators integrating closed-loop heat recovery report energy savings that compound water reductions, and published case studies show up to 30% throughput gains after layout and energy optimization. Europe’s Sustainable and Circular Textiles Strategy now incentivizes adopters through green-public-procurement scoring, accelerating uptake among large mills that supply global brands. For converters, the ability to secure certifications such as bluesign and OEKO-TEX unlocks premium contracts with retailers that must disclose Scope 3 water footprints. The competitive edge is further reinforced by consumer willingness to pay higher prices for apparel made with certified low-impact printing.

High-speed industrial printer launches, lowering TCO

Equipment makers have narrowed the cost gap with rotary screen printing by boosting productivity and automating calibration. The Epson Monna Lisa ML-64000 hits 740 m²/h at production quality while maintaining dot-placement accuracy through Dynamic Alignment Stabilizer technology, giving large mills the confidence to migrate mainstream job volumes.[1]Epson Monna Lisa, “ML-64000,” epson-monnalisa.eu Asian suppliers such as HPRT follow suit with 1,080 m²/h models that enable full-shift, lights-out operation. Automated maintenance sequences, continuous-ink systems, and printhead redundancy cut downtime, which pushes the break-even point lower for mid-size converters. When setup elimination and waste savings are factored in, analysts note a 15–20% cost advantage over analog methods for runs below 3,000 linear meters.

AI-driven design-to-print software adoption

RIP platforms now integrate neural engines that can auto-generate repeat patterns, predict color shifts on textured fabrics, and optimize nesting to raise material yield. Roland DG’s VersaWorks 7 applies advanced color-management algorithms that lock ICC profiles to fabric batches, ensuring color fidelity across distributed production cells. Plug-ins also tap e-commerce store data to populate names and numbers in batch mode, trimming artwork preparation from hours to minutes. The biggest value emerges in demand forecasting: AI systems analyze sell-through data and trigger automated reprints only when algorithms flag a stock-out risk, preserving the low-inventory promises of on-demand models. Early adopters report 25% faster time-to-market for new designs and a double-digit reduction in art-department labor costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive presses and finishing equipment | -1.8% | Global, especially challenging for SMEs | Short term (≤ 2 years) |

| Polyester-only substrate limitation | -1.2% | Global, with stricter scrutiny in the EU | Medium term (2-4 years) |

| Volatile disperse-dye supply costs | -0.9% | Global, concentrated in Asia-Pacific supply chains | Short term (≤ 2 years) |

| PFAS regulations on transfer papers | -0.7% | North America and EU, expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-intensive presses and finishing equipment

Industrial-grade sublimation lines still command price tags that can top USD 200,000 when heat presses, drying tunnels, and workflow software are included, a hurdle that deters many small producers. High interest rates have pushed monthly leasing costs upward, and nearly half of the surveyed textile firms postponed expansion plans in 2024 due to financing constraints. Facility retrofits add further expense because presses require stable humidity, advanced ventilation systems, and safety controls for high-temperature operations. In response, equipment makers are rolling out click-charge models that bundle hardware, service, and ink into a single cost-per-linear-meter fee, lowering cash outlays for newcomers. Although adoption is growing, the capital barrier continues to suppress the number of new entrants, especially in emerging economies where credit terms remain tight.

PFAS regulations on transfer papers

California’s AB 1817 and the EU’s PFHxA restriction enforce stringent PFAS limits, forcing suppliers to reformulate paper coatings that once relied on fluorinated chemistries for clean release.[2]SGS, “Phasing Out PFAS in the Textile Industry,” sgs.com The transition is complex: new silicone-based alternatives must achieve the same dimensional stability and ink-release performance without compromising line speed. Early reformulations have passed laboratory tests, yet converters note minor yield losses during high-humidity runs. Compliance also demands supply-chain transparency; mills must prove sub-25 ppb PFHxA content and secure third-party certifications, adding cost and administrative load. While the rule encourages innovation and may open the door for biodegradable coatings, near-term disruptions are likely as operators validate replacement papers on press.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Garments Anchor Revenues while Technical Textiles Accelerate

Garments accounted for 62.31% of 2025 revenues, underscoring how teamwear, athleisure, and fast-fashion capsules rely on sublimation to execute vibrant all-over prints without inventory risk. Technical textiles, in contrast, represent a smaller base yet are forecast to grow at 10.98% CAGR as automakers adopt lightweight polyester composites for headliners, door panels, and seat covers. The dye sublimation printing market size for garments is projected to expand steadily because sports leagues continue to shorten replenishment cycles and because direct-to-consumer platforms streamline order aggregation.

Growth in technical textiles is tied to electric-vehicle interior redesigns that replace injection-molded parts with fabric-wrapped components, achieving up to 25% lower carbon footprint. Producers are trialing flame-retardant coatings compatible with sublimation to meet FMVSS 302 standards, opening new revenue streams. Broader automotive mandates that call for 25% recycled content favor polyester-based structures, a substrate sweet spot for sublimation. As regulatory credits incentivize recycled interiors, tier-1 suppliers are negotiating multi-year print contracts, giving converters the volume visibility needed to justify industrial press investments.

By Printer Type: Industrial Platforms Deliver Scale

Wide-format units (<74") retained a 55.74% revenue share in 2025 because they match the width of most roll-to-roll finishing lines and address the mid-volume sweet spot of fashion and décor converters. However, industrial platforms exceeding 74" are expected to log an 11.76% CAGR through 2031, fueled by mills that want single-pass efficiency and full-shift throughput. The dye sublimation printing market benefits as printhead makers quadruple output capacity at new plants, such as Epson’s JPY 5.1 billion (USD 34 million) expansion in Tohoku that targets September 2025 completion.

Industrial lines reduce per-meter ink consumption by leveraging symmetrical nozzle arrays and real-time drop-watch systems that cut overspray. Integration of inline fusing further trims labor because rolls exit completely fixed, ready for inspection and cutting. The combined savings can reduce total operating costs by double digits versus repositionable two-step workflows. For converters in high-labor-cost regions, automation offsets wage inflation and supports reshoring strategies that prioritize quick local delivery.

By Ink Type: Transfer Dominates but Direct-to-Fabric Gains Momentum

Transfer inks delivered a 59.58% share in 2025, sustained by well-established paper supply chains that guarantee color consistency across diverse printer fleets. Direct-to-fabric formulations are forecast to expand at a 12.13% CAGR as mills seek to eliminate paper waste and accelerate job changeovers. Early adopters report a 15% reduction in consumable cost per square meter after switching to paperless workflows, a figure that rises when waste-disposal fees are included.

OEKO-TEX ECO PASSPORT-certified disperse pigments, such as Epson’s Genesta line, satisfy both brand and regulatory requirements while reducing volatile-organic-compound emissions. The dye sublimation printing market size attached to direct-to-fabric is further buoyed by bluesign criteria that mandate PFAS-free inks from January 2025, prompting fashion labels to prefer suppliers already compliant. In parallel, pigment chemists explore bio-sourced colorants that decouple supply costs from crude-oil fluctuations, addressing one of the critical restraints listed above.

By Substrate Category: Polyester Leads, Hybrids Emerge

Polyester maintained a 64.71% revenue share in 2025 because its molecular affinity for sublimation dyes yields unmatched wash-fastness and color vibrancy. Yet, hybrid technical textiles blending recycled polyester with bio-based fibers are slated to grow at a 11.86% CAGR, aligning with automotive and aerospace circularity targets. The dye sublimation printing market benefits as recyclers adopt radiocarbon testing per ASTM D6866 to verify bio-based content, instilling brand confidence in material claims.

Floor carpet makers have introduced mono-material polyester backings that allow full recyclability without compromising abrasion resistance, positioning sublimation as a decorating method that supports end-of-life recovery. In apparel, mills are trialing partially bio-based PET that carries identical dye-uptake characteristics, enabling a seamless transition for existing printers. Converters are therefore expanding substrate portfolios to include knit, woven, and composite structures, diversifying revenue while staying within the polyester chemistry family that sublimation demands.

Geography Analysis

Asia-Pacific generated 40.11% of 2025 revenue, supported by dense manufacturing clusters, integrated feedstock supply, and favorable equipment import tariffs that drop to 0% in markets such as Vietnam. China remains the epicenter with 20.46 billion garment units produced in 2024, representing 4.22% year-over-year growth. Government programs promoting 70% digitalization of textile firms by 2025 are pushing even smaller mills to adopt roll-to-roll sublimation presses, accelerating penetration. Rising labor costs, however, are prompting automation investments that in turn boost demand for high-throughput industrial platforms.

North America retains a sizeable share, driven by collegiate and professional sports teams that require rapid personalization and domestic production for licensing compliance. The region is also early in adopting AI-driven workflow software, resulting in faster design cycles and reduced pre-press labor. Trade-promotion authority agreements continue to shape import duties on blank polyester garments, influencing near-shoring strategies that position Mexico as a substrate supplier to U.S. printers.

Europe’s strict environmental regulations stimulate the adoption of water-free sublimation and PFAS-free coatings, giving the dye sublimation printing market a regulatory tailwind. Horizon Europe has earmarked EUR 10 million for local-for-local digital textile production, a grant line that lowers the capital barrier for micro-factories across the bloc. Brands headquartered in the region are therefore engaging in supplier audits that favor converters holding bluesign, GOTS, and ISO 14001 certifications.

The Middle East and Africa are emergent, led by the UAE’s fashion hub and South Africa’s promotional-product boom. Infrastructure investments in free-trade zones provide duty-free access to both European and Asian markets, making it attractive for global brands to locate finishing operations there. Latin America, while smaller in revenue, shows above-average growth due to soccer merchandising contracts and the rise of domestic sports leagues, adding another vector for regional diversification.

Regulatory Landscape

Regulation affecting dye sublimation printing is increasingly shaped by chemical-content limits, food-contact compliance expectations (where printed packaging is in scope), and wastewater and emissions scrutiny that favors water-free processes. In the EU, the Packaging and Packaging Waste Regulation (PPWR) introduces PFAS limits for food-contact packaging, with Article 5(5) applying from 12 August 2026 and setting thresholds of 25 ppb (targeted PFAS), 250 ppb (sum of targeted PFAS), and 50 ppm (total PFAS, including polymeric). This intersects with ongoing PFAS controls referenced in transfer-paper and coating supply chains and raises the need for documentation and testing across ink and paper inputs.

For printed packaging and other applications where migration or set-off is relevant, EU Good Manufacturing Practice requirements under Regulation (EC) No 2023/2006 continue to govern how printing inks are formulated and applied on non-food-contact sides to prevent unintended transfer. Europe also faces a patchwork compliance environment, since national measures and reference standards remain influential, including Switzerland's Ordinance (SR 817.023.21) for materials and articles in contact with food (revision effective 1 February 2024) and Germany's ink-related transition timeline (extended to 31 December 2026). Industry guidance has tightened as well, including EuPIA's GMP guidance update (5th version, November 2025) and its April 2026 information note on PFAS and printing inks in the context of PPWR, which together push converters toward PFAS-free consumables, stronger supplier declarations, and more formalized process controls.

Value Chain Analysis

The dye sublimation printing value chain starts with upstream petrochemical and recycled feedstocks for polyester-based fabrics and specialty polymer-coated rigid media, alongside disperse dye and ink chemistries, release coatings, and base papers used in transfer workflows. Printhead and printer OEMs provide wide-format and industrial platforms, while heat presses, calendars, dryers, and finishing equipment complete the production cell. Workflow software (RIP, color management, and increasingly cloud monitoring) links prepress to production, with converters, garment decorators, and packaging and visual-communication print service providers producing outputs ranging from short-run personalization to industrial-scale orders for brands, teams, and OEM end users.

Downstream, distribution is increasingly organized around integrated ecosystems that bundle hardware, inks, papers, and service. This reduces downtime risk and simplifies compliance documentation as PFAS and other chemical restrictions expand. Consumables are supported by both large global formulators and integrated specialists that manage coating and logistics in-house, while parts of the broader packaging and printing value chain also incorporate digital inkjet capabilities to address high-mix, low-volume demand and serialized data-to-print requirements. Key operational bottlenecks remain capex-heavy finishing capacity, qualified PFAS-free transfer paper availability, and the stability of disperse dye inputs, which can tighten lead times for converters running both personalization jobs and large-volume contracts.

Competitive Landscape

The dye sublimation printing industry is moderately concentrated, with a handful of vertically integrated vendors combining hardware, consumables, and software into turnkey ecosystems. Epson deepened this integration by acquiring Fiery LLC in September 2024, gaining digital front-end capabilities that enhance workflow continuity from RIP to press. Brother Industries signaled consolidation pressure via a USD 43.34 billion hostile tender for Roland DG, highlighting the strategic value of wide-format portfolios that serve both signage and textile segments.

Competitive advantage increasingly hinges on service models rather than pure hardware specifications. Kornit Digital’s All-Inclusive-Click subscription aligns ink, parts, and maintenance into a pay-per-meter plan, lowering entry barriers for converters wary of capex exposure. Meanwhile, Epson’s Cloud Solution PORT provides real-time fleet analytics, reducing unplanned downtime and helping multi-site operators allocate jobs dynamically. Suppliers with cloud-based diagnostic tools capture recurring revenue and build stickiness by embedding themselves deeper into customer workflows.

New entrants focus on niche opportunities such as direct-to-film and desktop sublimation, but the market’s direction favors scale economics that allow aggressive R&D investment in printhead miniaturization and low-viscosity ink chemistries. Partnerships between press builders and chemical suppliers are tightening, illustrated by joint development agreements that target PFAS-free release coatings. Market positioning therefore revolves around who can offer end-to-end compliance: ISO 9001 quality systems, bluesign approval, and on-site waste-heat recovery solutions now appear on many request-for-quote documents.

Dye Sublimation Printing Industry Leaders

Seiko Epson Corporation

Roland DG Corporation

Fujifilm Holdings Corporation

Canon Inc.

HP Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace is the shift from analog to digital for high-mix, low-volume production where traceability and rapid artwork changes matter, including soft signage, promotional products, and selected packaging print workflows that benefit from variable-data capability. At Interpack 2026, packaging-focused digital printing drew PPWR-driven interest in mono-material structures, which creates room for compatible inks, coatings, and digitally printed functional layers that support recyclability goals without complex laminations. Separately, PFAS limits and brand audit requirements are pushing suppliers to provide clearer declarations and certified input portfolios, which increases opportunities for transfer papers, ink systems, and workflows engineered for documented low-impact production.

Industrial productivity and end-to-end workflow integration are also expanding the addressable base by reducing the operational cost of moving mainstream volumes onto digital lines. Epson's May 2026 introduction of the SureColor SC-F20000, positioned as an industrial dye-sublimation platform with eight PrecisionCore MicroTFP printheads and large, hot-swap ink capacity, illustrates the push toward higher throughput and production stability. Converters that pair such platforms with automation in cutting, inspection, and color-managed RIP workflows are using the same infrastructure for on-demand micro-factory models in sports and fashion, and they are also bidding for more standardized technical-textile programs where repeatability and compliance documentation are part of the request-for-quote.

Recent Industry Developments

- July 2026: Seiko Epson launched the 76-inch SureColor F20030 industrial dye-sublimation printer with an 8-printhead architecture and stated speeds up to 306 m2/h at 600x600 dpi. The launch targets higher-throughput textile production and supports converters that need stable, industrial uptime to run both personalized and repeat orders on the same line.

- May 2026: Seiko Epson introduced the SureColor SC-F20000 industrial dye-sublimation printer, featuring eight PrecisionCore MicroTFP printheads and high-capacity ink handling. This reinforces the market shift toward industrial platforms that narrow the productivity gap with analog processes while keeping digital advantages such as rapid changeovers and color control.

- September 2024: Seiko Epson completed the acquisition of Fiery LLC, adding digital front-end and workflow capabilities to its broader printing portfolio. The acquisition strengthens end-to-end integration from RIP to press, which is increasingly important for multi-site operators that prioritize consistent color, automation, and reduced prepress labor.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from dye sublimation printing, where inks are transferred and fixed onto compatible substrates using heat, mainly for textile and rigid-surface decoration, across global end users and print providers.

Scope exclusions: Exclusions include traditional screen printing, solvent and latex wide-format printing, and direct-to-garment printing that does not use a sublimation transfer or dye fixation step.

Segmentation Overview

- By Application

- Garments

- Technical Textiles

- Household Textiles

- Visual Communication/Soft Signage

- Rigid Substrates

- By Printer Type

- Desktop (<44")

- Wide-Format (44"–74")

- Industrial (>74")

- By Ink Type

- Transfer Sublimation Inks

- Direct-to-Fabric Sublimation Inks

- Sublimation Toner Inks

- By Substrate Category

- Polyester Fabrics

- Polymer-Coated Rigid Media

- Blended/Hybrid Technical Textiles

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the base structure of the model and align it with how the printing and textile ecosystem is tracked publicly. We leaned on public sources such as the US Census Bureau and the US Bureau of Labor Statistics for manufacturing and price signals, and also trade statistics from UN Comtrade for movements of printing equipment and relevant supplies.

To understand materials and process direction, we referred to sources such as the International Organization for Standardization for terminology and process standards, and peer reviewed publications that discuss sublimation inks, polyester interaction, and colorfastness performance. We also reviewed company filings, investor presentations, industry association pages, and reputed press coverage to map adoption drivers by application. Where needed for cross checks, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import export data were used to validate player activity and directional volumes. The sources listed here are illustrative only, and many other public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what is actually being bought and used, and then to test our assumptions around pricing and adoption across textiles, soft signage, and rigid items. We spoke with a mix of equipment and consumables participants, print service providers, and downstream users across APAC, EMEA, and the Americas, so the model reflects differences in polyester penetration, production footprints, and typical print widths.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 17% | APAC: 43% |

| Mid tier: 53% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 18% | Managers: 50% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where the demand pool is reconstructed from printable textile and coated-media usage, and then filtered using realistic penetration for sublimation versus other print methods. After that, results are corroborated through selective bottom-up approximations, where we roll up a sampled set of supplier revenues and validate with channel checks on equipment placements and consumables pull-through.

Key inputs in the model include polyester and polyester-blend usage in target applications, installed base indicators for desktop and wide-format sublimation printers, typical ink consumption per square meter (or per print run) by application, and average selling price ranges for inks, transfer paper, and compatible substrates. We also track adoption signals for soft signage and sportswear, since shifts there quickly change volume requirements and print widths. For the forecast, scenario analysis is used so changes in apparel customization, advertising spend for visual communication, and equipment replacement cycles can be reflected without overfitting limited public datasets. When bottom-up visibility is thin in smaller countries, the gap is handled by applying region-specific adoption and pricing bands that were validated in interviews, and then rechecked against trade and production direction.

Data Validation & Update Cycle

Validation is done by triangulating the final market totals against independent signals, such as trade movement of relevant printing equipment, price trends for inks and paper, and practical capacity and utilization checks shared by interviewees. Outliers are flagged, and assumptions are revisited when a region grows faster than what textile output and signage demand can reasonably support.

Before sign-off, the model goes through multi-step analyst reviews, where calculations, unit conversions, and year-to-year jumps are checked again, followed by selective re-contacts when new information changes a key input. Reports are refreshed annually, and interim updates are made when material events occur, such as major supply expansions, regulatory shifts affecting inks, or sharp pricing changes. Right before delivery, a final pass is completed so clients receive the latest updated view that matches the current market context.

Mordor Intelligence's Dye Sublimation Printing Market Sizing Compared With Other Published Estimates

Published market values for dye sublimation printing can look far apart even when the topic name sounds identical, because the underlying scope and the year used for the starting point often change. Differences also come from how each publisher treats equipment versus consumables, and whether values are captured at factory-gate, distributor level, or end-user spending.

Heat press equipment and blank substrates are a common add-on in some studies, but they sit outside Mordor Intelligence's scope for this market sizing, which keeps the value tied to dye sublimation printing solutions rather than adjacent hardware bundles. Other gaps usually show up in pricing logic, where some estimates extend one blended average price across all applications, even though garments, soft signage, and rigid items consume inks and papers differently. Refresh timing also shifts comparisons, because recent shifts in printer availability and ink pricing can change the current-year total when the model is updated.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.85 B (2026) | |

| Industry Research Publisher A | USD 16.40 B (2025) | Uses a 2025 base year and may blend pricing and penetration assumptions across product types and end users, which can shift the current-year value compared with a 2026 starting point. |

| Global Market Report B | USD 15.18 B (2026) | Often applies factory-gate revenue framing and a broader product-type lens that can mix printers, inks, and related items differently, which can compress the market total depending on what is counted as printing revenue. |

The table shows that the spread is mostly explained by what gets counted as part of printing revenue and how the current year is anchored. By keeping the model tied to clear demand signals (printable area, adoption by application, and realistic ink and paper consumption), the outcome stays traceable and easier to reproduce when inputs change.

Key Questions Answered in the Report

What is the current valuation of the dye sublimation printing market?

The dye sublimation printing market size reached USD 16.85 billion in 2026 and is projected to grow at a 10.72% CAGR to USD 28.05 billion by 2031.

Which application contributes the most revenue?

Garments led in 2025 with 62.31% of total revenue thanks to rising demand for personalized sportswear and fashion items.

Which region is growing fastest?

Asia-Pacific is forecast to expand at a 12.68% CAGR through 2031, supported by concentrated manufacturing capacity and supportive digitalization policies.

Which printer category is set for the highest growth?

Industrial systems wider than 74 inches are expected to grow at 11.76% CAGR as converters invest in high-throughput lines to lower per-unit costs.

How are environmental regulations shaping technology adoption?

Water-free sublimation and PFAS-free transfer papers are gaining traction as regulators in the EU and North America tighten water-usage and chemical-content rules, prompting mills to upgrade equipment and consumables.

What financing options exist for small converters facing high capex?

Subscription models such as pay-per-meter plans bundle hardware, ink, and service into predictable operating costs, easing capital barriers for small and medium producers.

Page last updated on: