Dual Screen Laptops Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

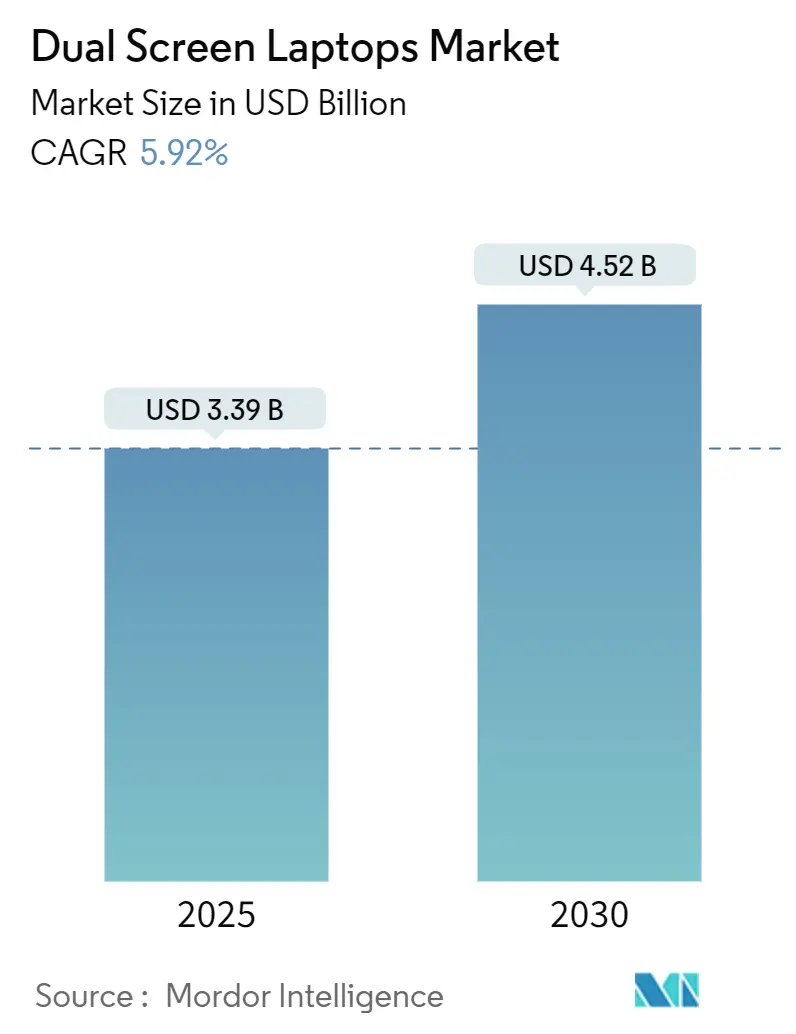

| Market Size (2025) | USD 3.39 Billion |

| Market Size (2030) | USD 4.52 Billion |

| Growth Rate (2025 - 2030) | 5.92% CAGR |

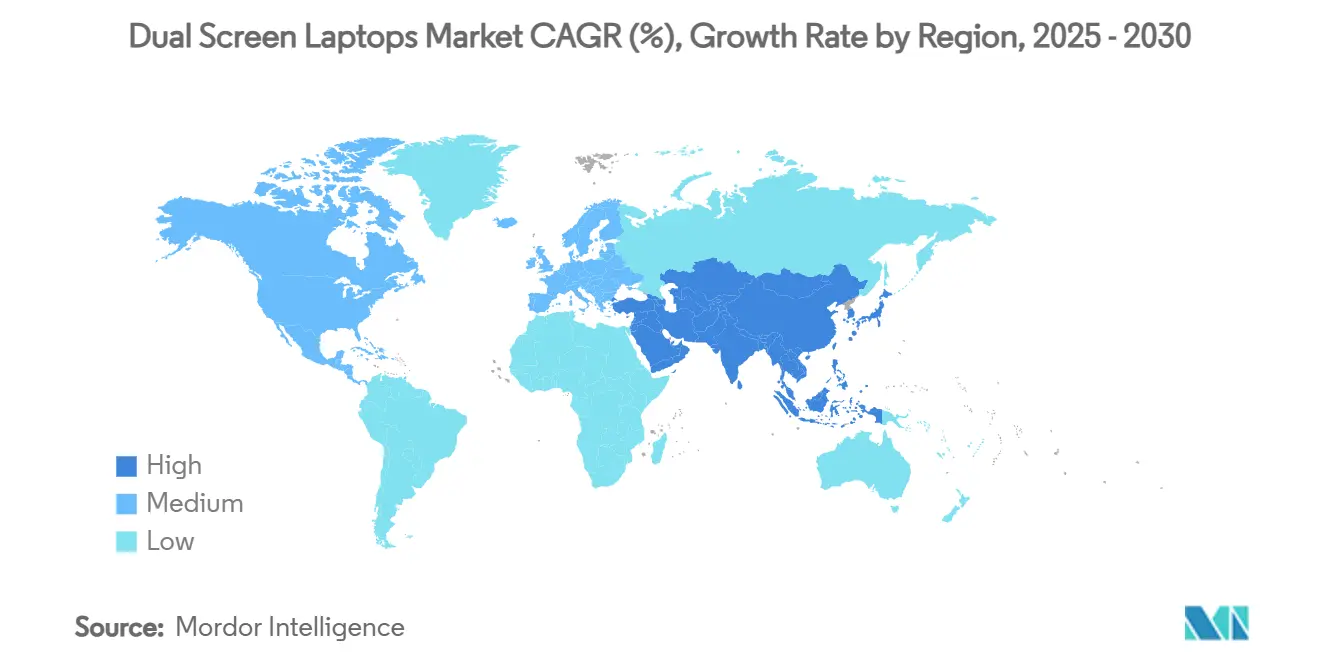

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

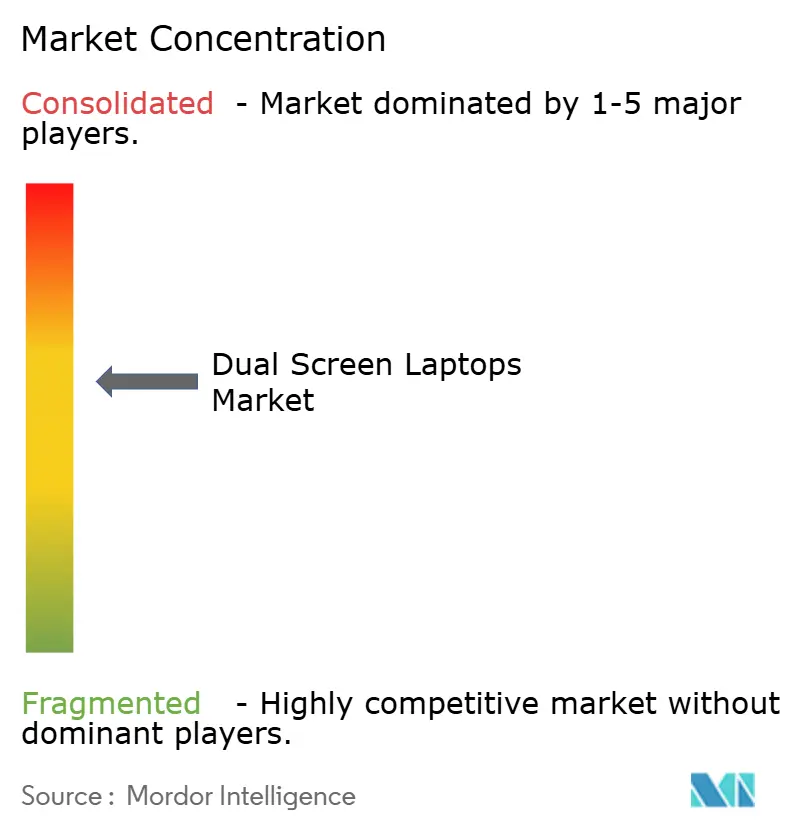

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dual Screen Laptops Market Analysis by Mordor Intelligence

The dual screen laptops market size stood at USD 3.39 billion in 2025 and is forecast to reach USD 4.52 billion by 2030, expanding at a 5.92% CAGR. Growth rests on premium device demand, OLED cost declines, and edge-AI enhancements that let manufacturers defend higher average selling prices. Dual-hinge clamshell formats retained user familiarity, while detachable designs unlocked tablet flexibility. OLED supply-chain scale in South Korea and China aligned with rising creative-economy device budgets, helping OEMs widen margins despite soft traditional notebook volumes. Edge-AI chipsets such as Qualcomm’s Snapdragon X Elite brought fanless, thin-and-light designs to the dual-screen laptops market, further supporting ASP expansion. North America led early adoption on the back of hybrid-work norms, but education pilots across Asia-Pacific signaled the next wave of shipment growth.

Key Report Takeaways

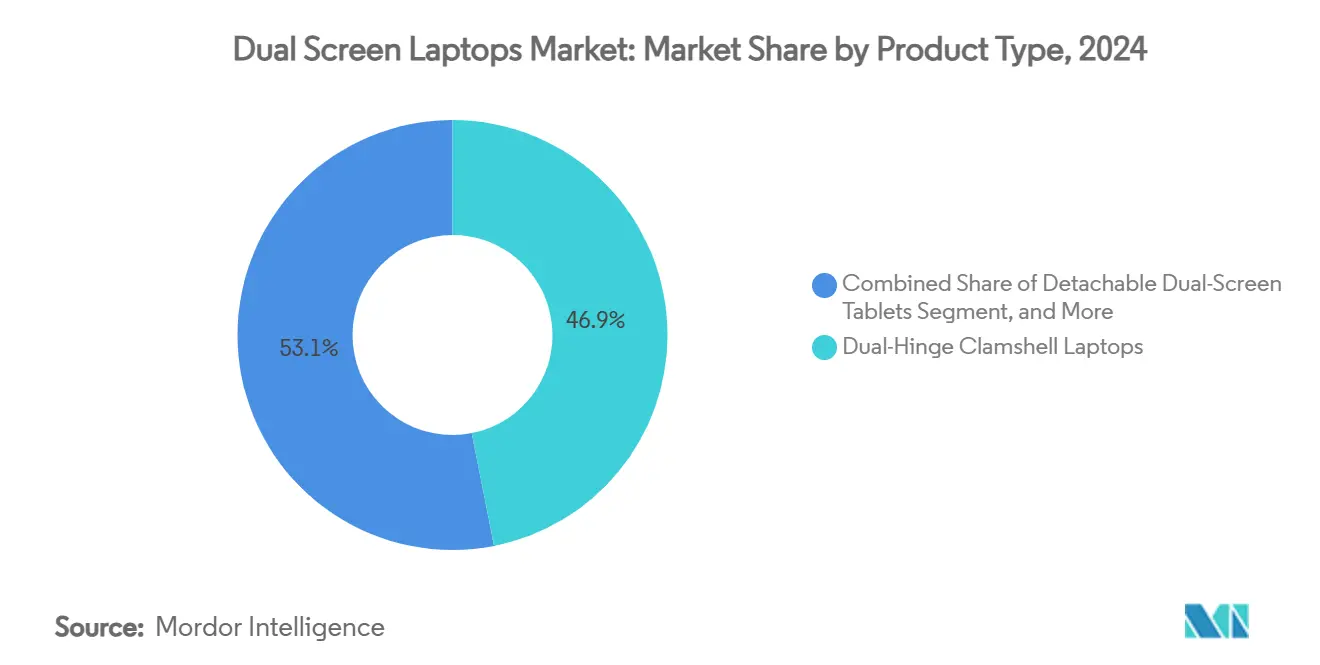

- By product type, dual-hinge clamshells led with 46.90% of the dual-screen laptops market share in 2024, while detachable dual-screen tablets are projected to post a 7.15% CAGR through 2030.

- By screen size, the 15–16.9-inch category captured 52.70% share of the dual-screen laptops market size in 2024, and the < 13-inch class is advancing at a 7.01% CAGR through 2030.

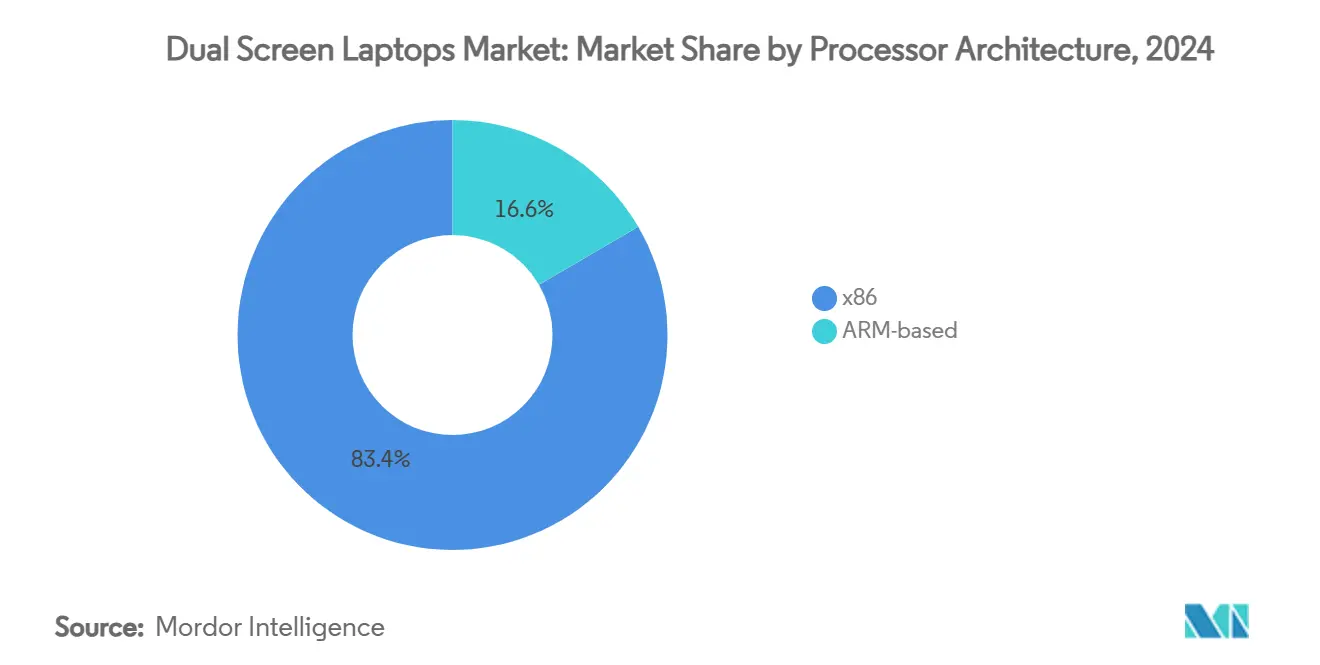

- By processor architecture, x86 accounted for 83.40% of the dual-screen laptops market size in 2024, but ARM-based chipsets recorded a 7.35% CAGR to 2030.

- By target user, creative professionals commanded a 41.60% share of the dual-screen laptops market size in 2024; the education segment is forecast to expand at an 8.75% CAGR to 2030.

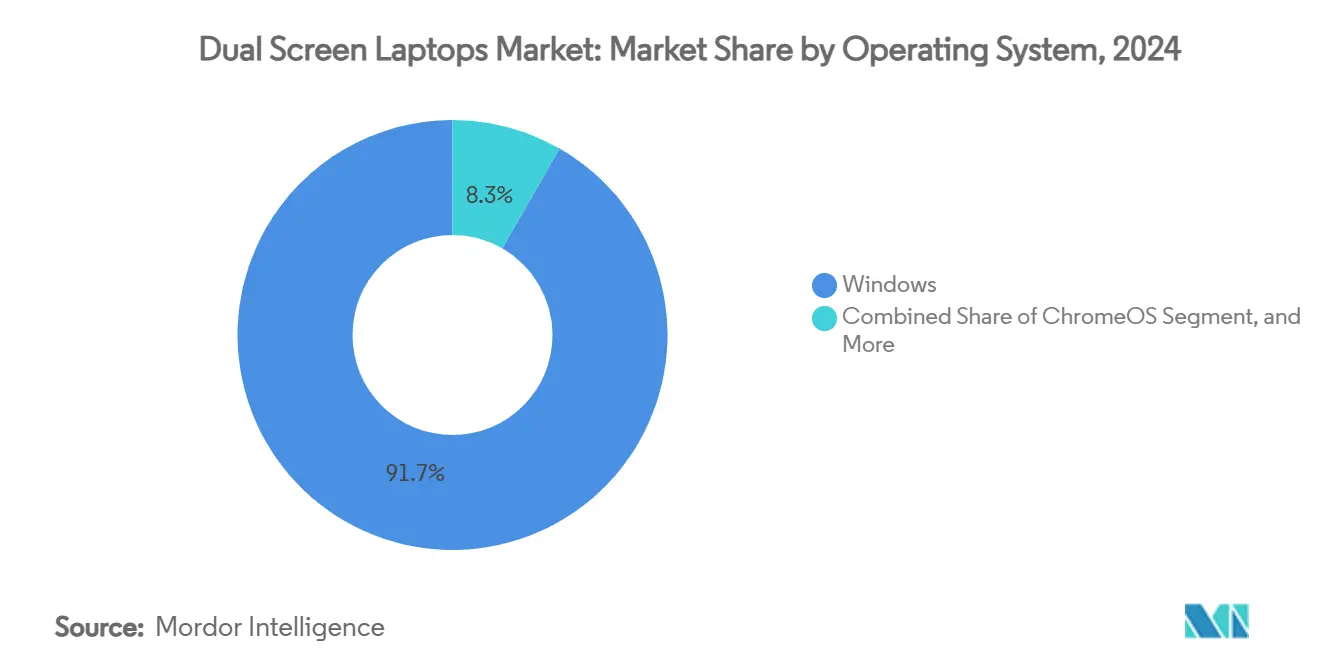

- By operating system, Windows held 91.70% dual screen laptops market share in 2024, whereas ChromeOS is set to grow at an 8.36% CAGR through 2030.

- By distribution channel, online direct-to-consumer sales represented 44.90% of the dual-screen laptops market size in 2024 and are rising at a 7.95% CAGR to 2030.

- By geography, North America secured 38.60% dual screen laptops market share in 2024; Asia-Pacific is projected to grow at a 9.14% CAGR between 2025-2030.

Market Trends and Insights

Drivers Impact Analysis of Dual Screen Laptops Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for multitasking productivity devices | +1.20% | Global (North America, Europe focus) | Medium term (2–4 years) |

| Growing popularity of mobile creative professionals | +0.90% | North America, EU; accelerating in APAC | Short term (≤ 2 years) |

| OEM pursuit of ASP expansion in premium PC segment | +1.10% | Global | Medium term (2–4 years) |

| Edge-AI-optimized dual-display form-factor innovations | +0.80% | APAC core, scaling to North America | Long term (≥ 4 years) |

| Foldable OLED cost curve crossover by 2027 | +1.00% | Global, led by Asian fabs | Long term (≥ 4 years) |

| EU Right-to-Repair regulations favouring modular dual screens | +0.30% | Europe with global spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Multitasking Productivity Devices

Hybrid work drove professionals to replicate desktop multi-monitor setups on the move. ASUS’s 2025 Zenbook DUO delivers dual 14-inch OLED panels that expand to 19.8 inches of cumulative workspace without topping 3.64 lb, illustrating how OEMs translate that need into hardware[1]ASUS. “ASUS Launches Zenbook DUO.” ASUS newsroom, January 31, 2024, asus.com. Native Windows 11 window-spanning and gesture controls lower the adoption curve, while early field pilots inside finance and consulting firms validate time-saving gains for spreadsheet, coding, and design tasks. Productivity-centric software developers now ship dual-pane presets, turning a hardware novelty into an ecosystem norm that sustains premium pricing.

Growing Popularity of Mobile Creative Professionals

Social-media monetization and remote agency workflows enlarge the addressable base of creators ready to pay for high-spec portable studios. Lenovo’s Yoga Book 9i frames the narrative by branding itself a “portable creative studio” equipped with two 14-inch OLEDs that let editors preview and produce simultaneously. Adobe’s dual-screen UI presets plus touch shortcuts enhance clip trimming and color grading efficiency, cementing the dual screen laptops market as an indispensable creator toolkit. Regional uptake aligns with disposable-income clusters in the United States, Germany, and Japan, but Southeast Asian influencer communities are closing the gap as broadband and sponsorship revenues rise.

OEM Pursuit of ASP Expansion in Premium PC Segment

Facing plateauing unit volumes, vendors refocus on value-add hardware differentiation. The ASUS Zenbook DUO debuted at USD 1,699 versus USD 800-1,200 for similar single-screen ultrabooks, proving buyers will reward form-factor novelty with higher spend [2]ASUS. “ASUS Launches Zenbook DUO.” ASUS newsroom, January 31, 2024, asus.com. HP’s OmniBook X couples Snapdragon X Elite silicon with dual panels to blend exceptional battery life and AI smarts, providing clear justification for price premiums in executive fleets. The resulting margin buffer partially shields OEMs from panel and logistics inflation.

Edge-AI-Optimized Dual-Display Form-Factor Innovations

On-device AI accelerators now manage content flow between panels, predict user intent, and modulate power budgets. Qualcomm’s Snapdragon X Elite delivers 45 TOPS NPU throughput that dynamically allocates apps to the primary or secondary screen while maintaining fanless thermals [3]Greg Freedman. “Qualcomm Snapdragon X Elite and X Plus.” Tom’s Hardware, April 24, 2024, tomshardware.com. Asian notebook ODMs exploit in-house AI firmware teams, accelerating feature rollouts such as real-time transcription on one screen while video plays on the other. This intelligence helps mask software-ecosystem gaps and elevates user experience, broadening the dual screen laptops market beyond early adopters.

Restraints Impact Analysis of Dual Screen Laptops Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BOM costs versus single-screen ultraportables | -1.80% | Global | Short term (≤ 2 years) |

| Limited software ecosystem optimisation for dual displays | -1.10% | Global | Medium term (2–4 years) |

| Thermal-management challenges in slim dual-hinge chassis | -0.90% | Global | Medium term (2–4 years) |

| User adoption inertia outside creator & gaming niches | -0.70% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High BOM Costs Versus Single-Screen Ultraportables

Dual OLED panels add USD 400–600 to build costs, forcing retail prices beyond mainstream acceptance. The GPD Duo crowdfunding tag of USD 1,860 for top specs exemplifies the stretch. While tandem OLED lines promise cost relief, near-term elasticity caps unit upside, especially in emerging markets.

Limited Software Ecosystem Optimisation for Dual Displays

Microsoft’s API toolkits exist, yet most third-party apps default to single-window behavior, leaving users to juggle manual placements. ASUS compensates via proprietary ScreenXpert overlays, but such vendor-specific fixes fragment UX and deter ISV investment. Until user bases cross a critical mass, developers remain hesitant.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Dual Screen Laptops Market Segment Analysis

By Product Type:

Clamshell Familiarity Sustains LeadershipDual-hinge clamshells generated 46.90% of 2024 revenue, anchoring the dual screen laptops market thanks to unchanged typing posture and proven hinge life cycles. The ASUS Zenbook DUO pairs a detachable Bluetooth keyboard with stacked screens, letting users shift instantly between laptop and portable monitor modes. Detachable dual-screen tablets, though only a fraction of shipments today, post a 7.15% CAGR as stylus-based art and classroom scenarios accelerate. Convertible 360° designs entice road warriors seeking versatility, yet hinge complexity and weight temper mass interest. Gaming-specific models like the ROG Zephyrus Duo 16 carve profitable niches by dedicating the lower display to stream chat and telemetry.

A widening component ecosystem aids each format. ODMs now offer reference boards sized for dual panels, and panel makers supply narrow-bezel 16:10 OLEDs that align cleanly when stacked. These advances decrease engineering burdens, paving the way for hybrid concepts such as Compal’s DualFlip, which morphs from tablet to side-by-side desktop orientation within seconds. As BOM spreads shrink, the dual screen laptops market stands poised for product-mix diversification beyond today’s clamshell skew.

By Screen Size:

15-16.9 Inch Class Balances Workspace and PortabilityThe 15-16.9 inch tier delivered 52.70% of 2024 shipments, underlining user appetite for desktop-replacement real estate without exceeding carry-on weight limits. Lenovo’s 14-inch-per-panel Yoga Book 9i shows vendors gravitating toward larger canvases that still fit airline trays. Sub-13-inch entrants, while niche, log a 7.01% CAGR by targeting students and commuters prioritizing bag footprint over screen acreage.

Display-supply innovation shapes future size trends. Samsung Display prototypes 18.1-inch foldable OLEDs that split into two 13-inch panes, hinting at a convergence of large-panel economics and dual-use versatility. Conversely, ultralight magnesium chassis and low-power tandem OLEDs keep smaller formats relevant by boosting battery endurance past eight hours with dual panels active. Consequently, the dual screen laptops market keeps a two-track strategy: bigger for desk-centric creators and gamers, smaller for on-the-go presenters and students.

By Processor Architecture:

ARM Momentum Gathers Amid x86 Strengthx86 still underpins 83.40% of shipments on the back of decades-old Windows compatibility and core-count advantages vital for heavy Adobe or CAD workloads. Intel’s Arrow Lake improvements in integrated graphics and AI offload specifically target dual-display energy budgets, extending unplugged uptime in ASUS’s 2025 Zenbook DUO by nearly two hours versus its predecessor. Yet ARM designs move rapidly, posting a 7.35% CAGR, as Qualcomm couples fanless ceilings with robust NPUs that enhance edge-AI features valued in education and field-service deployments.

Ecosystem shifts favor heterogeneity. Microsoft’s Prism emulation layer narrows compatibility gaps, and Adobe now issues simultaneous ARM/x86 updates for Creative Cloud. For OEMs, ARM’s smaller dies and lower thermals unlock chassis freedom, crucial where dual panels already constrain airflow. While x86 keeps performance leadership, dual screen laptop buyers increasingly weigh battery, noise, and AI functions when choosing silicon.

By Target User:

Education Segment AscendsCreative professionals held a 41.60% share in 2024, cementing their status as technology trendsetters willing to pilot novel workflows for editing, rendering, and scoring. The dual screen laptops market size for education, though smaller today, is growing fastest at 8.75% CAGR as ministries equip digital classrooms with ChromeOS-based dual-panel devices that support simultaneous lesson content and interactive quizzes.

Enterprise executives constitute a stable mid-single-digit growth pool, using secondary screens for live dashboards during video calls. Gamers and streamers value real-time chat monitoring, but budget constraints cap volumes. Over 2025-2030, the education push broadens geographic reach and introduces younger cohorts to dual-panel ergonomics, potentially translating into higher consumption when those students move into professional roles.

By Operating System:

ChromeOS Erodes Windows LeadDespite Windows shipping on 91.70% of dual screen laptops in 2024, ChromeOS’s 8.36% CAGR underlines appetite for low-maintenance, cloud-centric environments. Google’s OS automates window pairing across displays, an advantage when IT departments must train thousands of teachers quickly. Linux forks linger in R&D centers, requiring hardened security but lacking commercial volume.

Microsoft counters with deeper Teams and Copilot integration that exploits dual-panel layouts for concurrent note-taking and meeting content. The resulting OS contest drives faster UX innovation, benefiting end users regardless of platform choice and sustaining overall dual screen laptops market growth.

By Distribution Channel:

Direct-to-Consumer Deepens OEM MarginsOnline brand storefronts owned 44.90% of 2024 revenue and will outpace all other routes at 7.95% CAGR. High-ticket dual screen models need rich demos, configuration options, and post-sale onboarding—services best delivered on vendor sites. ASUS leverages online live chats and 360° product viewers to shrink hesitation for USD 1,699+ notebooks.

E-commerce marketplaces extend reach yet squeeze margin via commission fees, while big-box retail struggles to illustrate multi-screen benefits on crowded shelves. Corporate VARs remain vital for enterprise rollouts needing imaging, asset-tagging, and financing bundles. As average screen counts per PC rise, OEMs pivot to customer-education-heavy channels that maximize conversion and keep the dual screen laptops market profitable.

Geography Analysis

North America Dual Screen Laptops Market

North America contributed 38.60% of 2024 revenue, benefiting from mature hybrid-work cultures and a dense creator economy that values time-saving hardware. Silicon Valley influencers catalyze early adoption, and enterprise IT budgets swallow premium ASPs when ROI is demonstrated. Vendor marketing often launches in the region first, creating a trickle-down halo internationally.

Europe Dual Screen Laptops Market

Europe follows as a technology-sophisticated yet regulation-minded arena where Right-to-Repair rules influence product design. German SMBs use dual screens to reduce external-monitor spend, while French studios embrace mobile post-production on location. However, high energy costs and eco-labels compel OEMs to push tandem OLED power savings and repairable module narratives to secure public-sector deals.

APAC Dual Screen Laptops Market

Asia-Pacific, although holding a smaller current base, is the dual screen laptops market growth engine at 9.14% CAGR. Chinese OEMs benefit from local OLED capacity and government ed-tech subsidies. Japanese corps adopt the format to sustain productivity in space-constrained apartments, whereas Indian IT outsourcers deploy dual screens within managed-device schemes to elevate coding throughput. Competitive BOM efficiencies stemming from proximity to panel fabs amplify the region’s shipment acceleration.

Competitive Landscape

The market remains moderately concentrated. ASUS drives category definition via Zenbook DUO for productivity and ROG Zephyrus Duo for gaming, pairing hardware with ScreenXpert utilities for out-of-the-box multiscreen mastery. Lenovo leverages enterprise account reach and the Yoga Book 9i’s premium build to court corporate creatives. Dell enters with Pro Max Premium dual-OLED workstations co-engineered with NVIDIA to secure CAD and visualization workloads.

Challengers such as ACEMAGIC explore horizontal folding designs, offering differentiated ergonomics that may circumvent certain hinge patents[4]Scharon Harding. “ACEMAGIC’s X1 Approach.” Ars Technica, August 23, 2024, arstechnica.com. Framework Computer’s modular ethos intersects nicely with European repair laws, suggesting a potential asymmetric threat if it scales supply. Display vendors-Samsung Display, LG Display, BOE-wield strategic leverage through exclusive panel tech and yield advantages, influencing OEM launch calendars.

Strategic moves revolve around display innovation partnerships, AI-silicon tie-ups, and channel diversification. Patent race intensity in hinge reliability and cooling underscores barriers to entry, whereas open-source software kits lower hurdles for smaller brands to deliver acceptable UX. Over the forecast horizon, leadership will hinge on merging hardware novelty with seamless software, not on screen count alone.

Dual Screen Laptops Industry Leaders

ASUS Tek Computer Inc.

Lenovo Group Limited

HP Inc.

Dell Technologies Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Dual Screen Laptops Market Companies Covered in this Report

- ASUS Tek Computer Inc.

- Lenovo Group Limited

- HP Inc.

- Dell Technologies Inc.

- Microsoft Corporation

- Acer Inc.

- Apple Inc. (future ARM dual-screen patents)

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- Dynabook Inc.

- MSI - Micro-Star International Co., Ltd.

- Razer Inc.

- Gigabyte Technology Co., Ltd.

- VAIO Corporation

- LG Electronics Inc.

- Chuwi Innovation and Technology (Shenzhen) Co., Ltd.

- Eve Devices Oy

- XOLOT PC Technology Co., Ltd.

- Tongfang Co., Ltd. (Clevo ODM)

- Compal Electronics, Inc. (ODM)

Recent Industry Developments in Dual Screen Laptops Market

- March 2025: Samsung Display unveiled 240 Hz laptop OLEDs and a 27-inch 500 Hz QD-OLED monitor, signaling next-level responsiveness that can migrate into dual panels.

- March 2025: Dell introduced Pro Max Premium dual-OLED laptops with tandem technology and RTX Pro graphics at GTC 2025.

- February 2025: ASUS shipped the Zenbook DUO 2025 running Intel Arrow Lake H, adding battery-savvy AI scheduling.

- January 2025: Lenovo unveiled Yoga Book 9i Gen 10 with brighter 14-inch tandem OLEDs and Arrow Lake processors.

Global Dual Screen Laptops Market Report Scope

Segmentation Overview

| Detachable Dual-Screen Tablets |

| Dual-Hinge Clamshell Laptops |

| Convertible 360° Dual-Screen 2-in-1s |

| Gaming-Focused Dual-Screen Laptops |

| Less than 13-inch |

| 13-14.9 inch |

| 15-16.9 inch |

| More Than and Equal to 17-inch |

| x86 (Intel, AMD) |

| ARM-based (Qualcomm, Apple Silicon licensing) |

| Creative Professionals |

| Enterprise Executives |

| Gamers & Streamers |

| Education Segment |

| Windows |

| ChromeOS |

| Other Operating Systems (Linux distributions, proprietary) |

| Online Direct-to-Consumer |

| E-commerce Marketplaces |

| Brick-and-Mortar Retail |

| Enterprise Value-Added Resellers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Detachable Dual-Screen Tablets | ||

| Dual-Hinge Clamshell Laptops | |||

| Convertible 360° Dual-Screen 2-in-1s | |||

| Gaming-Focused Dual-Screen Laptops | |||

| By Screen Size | Less than 13-inch | ||

| 13-14.9 inch | |||

| 15-16.9 inch | |||

| More Than and Equal to 17-inch | |||

| By Processor Architecture | x86 (Intel, AMD) | ||

| ARM-based (Qualcomm, Apple Silicon licensing) | |||

| By Target User | Creative Professionals | ||

| Enterprise Executives | |||

| Gamers & Streamers | |||

| Education Segment | |||

| By Operating System | Windows | ||

| ChromeOS | |||

| Other Operating Systems (Linux distributions, proprietary) | |||

| By Distribution Channel | Online Direct-to-Consumer | ||

| E-commerce Marketplaces | |||

| Brick-and-Mortar Retail | |||

| Enterprise Value-Added Resellers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the dual screen laptops market in 2025?

The dual screen laptops market size reached USD 3.39 billion in 2025 and is projected to hit USD 4.52 billion by 2030.

Which form factor leads shipments today?

Dual-hinge clamshells held 46.90% of 2024 shipments, thanks to familiar ergonomics and robust hinge reliability.

Which region will grow fastest through 2030?

Asia-Pacific is forecast to post a 9.14% CAGR as education deployments and local OLED manufacturing scale up.

Why are ARM processors gaining traction?

ARM-based chipsets like Snapdragon X Elite deliver fanless thermals and integrated AI engines, fuelling a 7.35% CAGR within the segment.

What is the biggest barrier to mass adoption?

High bill-of-materials costs, adding USD 400-600 per unit, keep average selling prices high and restrict mainstream uptake.

Page last updated on: