Mini-LED Display Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

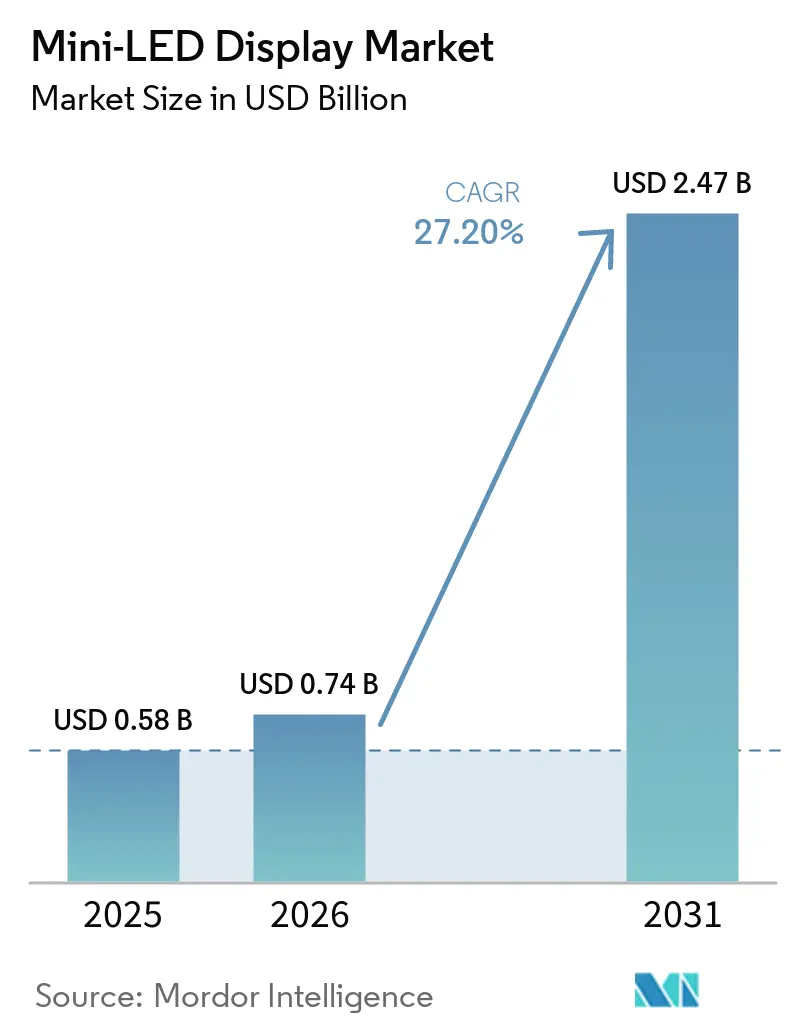

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 27.20% CAGR |

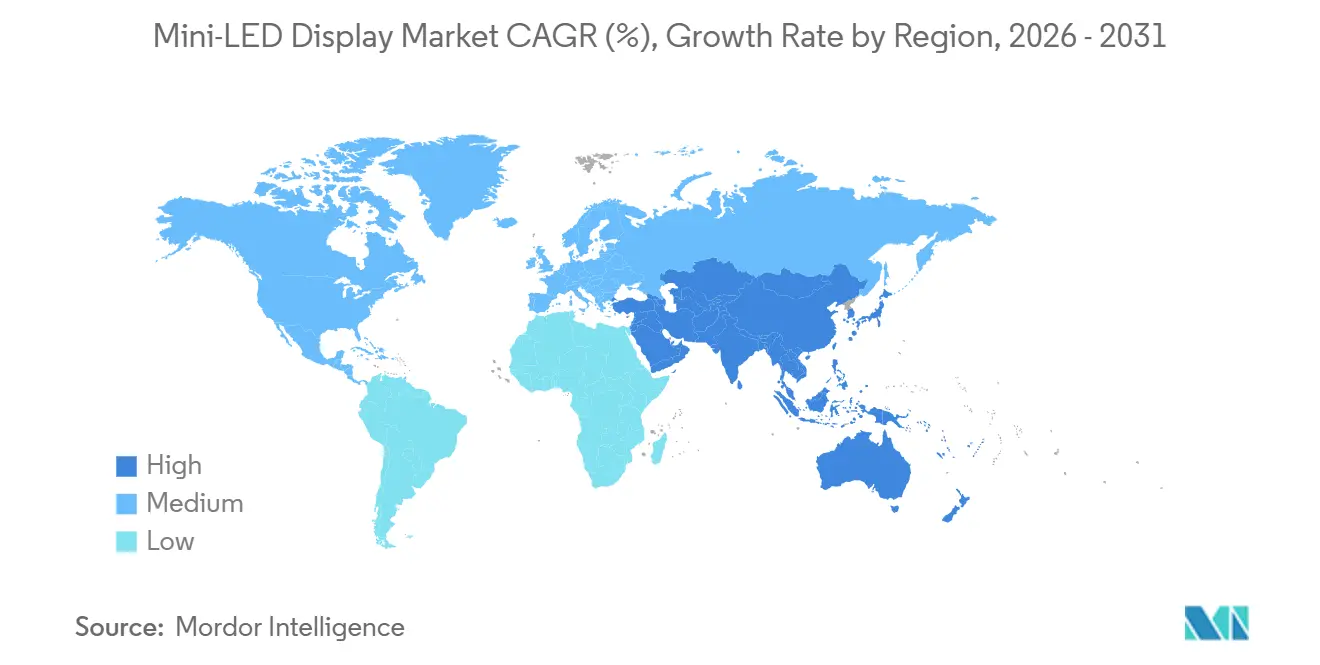

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mini-LED Display Market Analysis by Mordor Intelligence

The Mini-LED Display market size is projected to expand from USD 0.58 billion in 2025 and USD 0.74 billion in 2026 to USD 2.47 billion by 2031, registering a CAGR of 27.20% between 2026 and 2031. The market is witnessing significant growth driven by several factors, including the shift in television manufacturing capacity away from OLED, the rapid decline in costs of quantum-dot on-chip processes, and the increasing demand for automotive cockpit displays that require brightness levels exceeding 2,000 nits. In 2025, Asia-Pacific manufacturers capitalized on government policy subsidies to drive Mini-LED television penetration to approximately 10% of the domestic market. Additionally, the expiration of quantum-dot patents in 2026 is expected to reduce bill-of-materials costs, making mid-tier products more affordable. Competitive dynamics in the market intensified after Samsung Electronics and LG Electronics introduced RGB Mini-LED televisions at CES 2026, aiming to counter the growing dominance of Chinese manufacturers, who led global Mini-LED TV shipments in 2025. Despite advancements in Micro-LED technology, yield bottlenecks continue to hinder its widespread adoption, thereby extending the commercial viability of Mini-LED solutions throughout the forecast period.

Key Report Takeaways

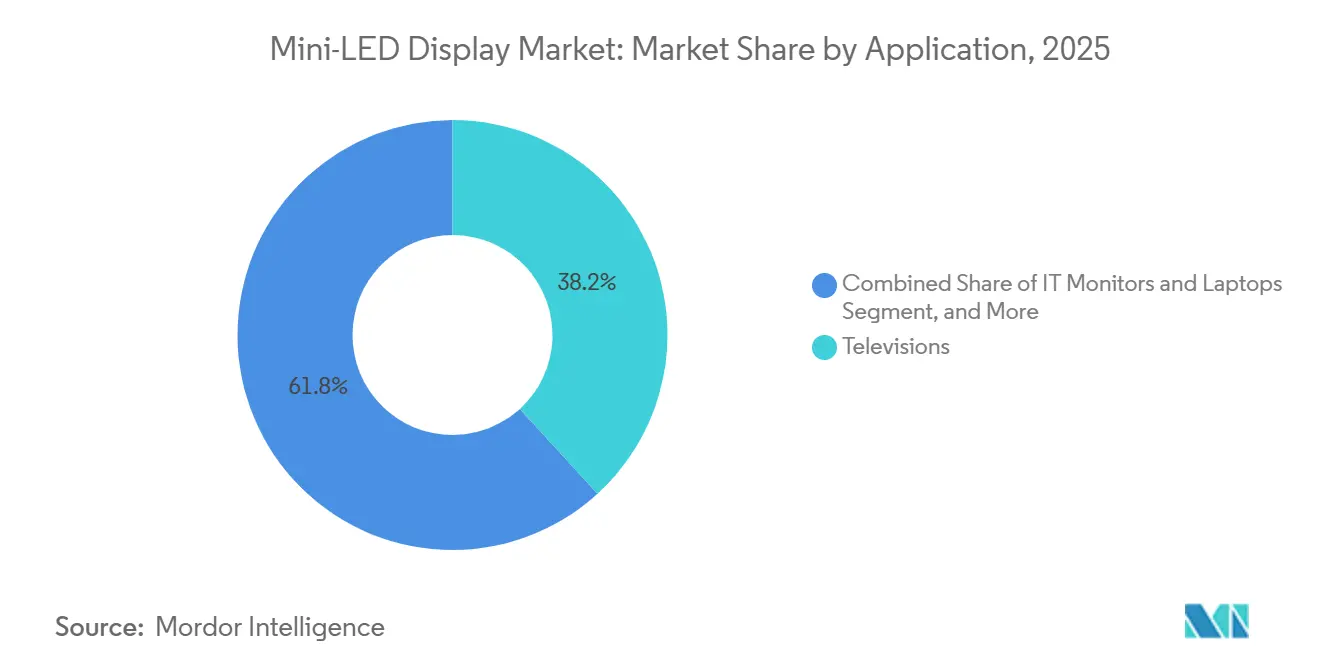

- By application, televisions led with 38.23% of the Mini-LED Display market share in 2025, while the automotive displays are forecast to advance at a 27.55% CAGR through 2031.

- By technology, Mini-LED BLU held 72.48% of the market share in 2025, while Direct-Emissive Mini-LEDs are forecast to advance at a 27.78% CAGR through 2031.

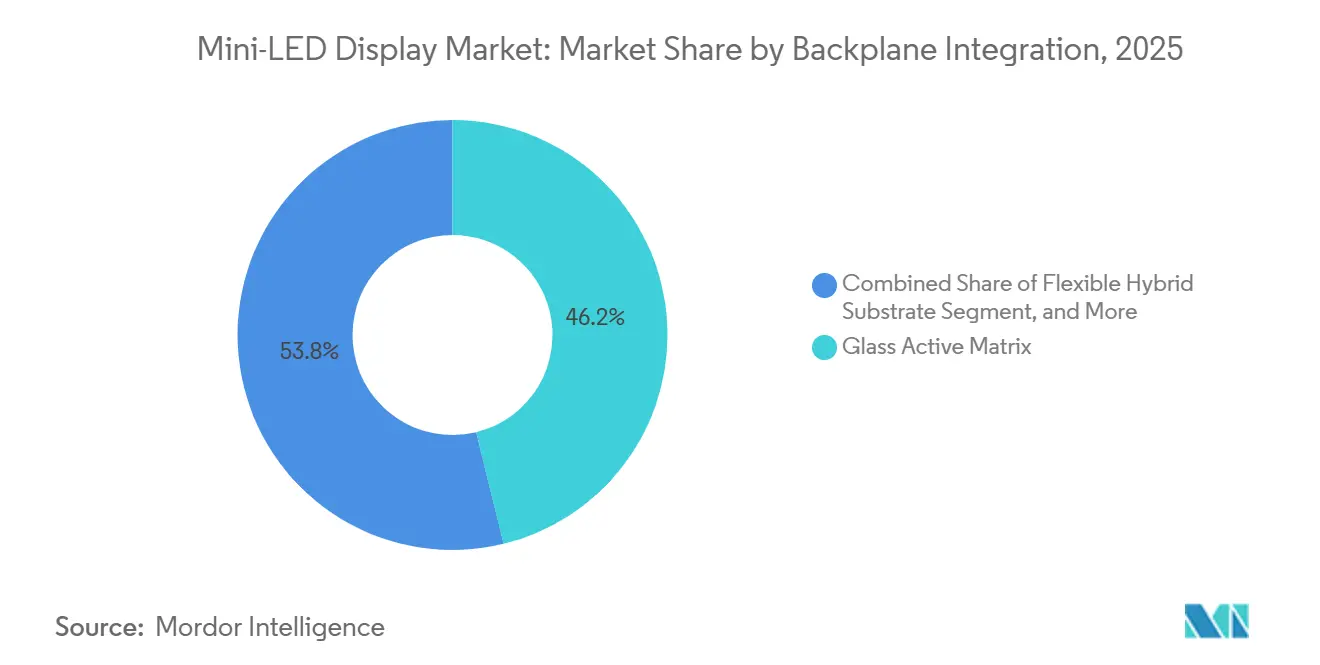

- By backplane integration, Glass Active Matrix led the Mini-Light Emitting Diode (LED) Display market with 46.19% market share in 2025, while Flexible Hybrid Substrate is forecast to grow at a 27.97% CAGR through 2031.

- By geography, Asia-Pacific led with 54.74% of the Mini-LED Display market share in 2025, while the Middle East is forecast to advance at a 27.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mini-LED Display Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling Mini-LED Back-Plane Costs | 6.5% | Global | Long term (≥ 4 years) |

| TV Makers Capacity Switches From OLED in 2H 2025 | 5.8% | Global, led by Asia-Pacific | Short term (≤ 2 years) |

| Automotive Cockpits Shift to ≥ 2,000-Nit Displays | 4.2% | Global premium vehicles | Medium term (2-4 years) |

| Micro-LED Yield Issues Prolonging Mini-LED Window | 3.5% | Global | Medium term (2-4 years) |

| Quantum-Dot On-Chip Patents Expiring 2026 | 2.8% | Global | Short term (≤ 2 years) |

| In-Flight Entertainment Retrofits 2025-2027 | 1.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Falling Mini-LED Back-Plane Costs Drive Market Expansion

Back-plane manufacturing efficiencies drove a 15-20% year-over-year cost decline in 2025, closing the price gap with OLED in 55-65 inch televisions. Shared LCD infrastructure allowed glass thin-film transistor back-planes to amortize capital expenditures and enabled TCL to lift Mini-LED TV shipments by 176% in H1 2025, underscoring the elasticity between cost and demand. Shift from metal bumps to conductive photoresist bumps further simplified the mass-transfer workflow, boosting yields and positioning the technology for continued cost compression through 2031.

TV Makers Capacity Switches From OLED in 2H 2025

Samsung Electronics and LG Electronics reallocated production lines from OLED to RGB Mini-LED technology in late 2025 to address the growing competition from Chinese brands, which dominated the Mini-LED TV market in terms of volume. This strategic shift allowed the companies to reduce lead times, broaden their product offerings, and introduce new models through premium tiers showcased at CES 2026. The move highlighted their confidence in leveraging refined LCD back-lighting technology as a competitive advantage, ensuring they remain relevant and competitive in the evolving display technology landscape.

Automotive Cockpits Shift to ≥ 2,000-Nit Displays

Original equipment manufacturers mandated ≥ 2,000-nit peak brightness for cockpit displays beginning in 2025 to ensure sunlight readability and support advanced driver assistance overlays. This requirement aims to enhance visibility and functionality, particularly under challenging lighting conditions, thereby improving safety and user experience. Mini-LED back-lighting met these targets with lower burn-in risk than OLED and better efficiency than conventional LCD. These advantages have positioned Mini-LED technology as a preferred choice for automotive applications. In response to this growing demand, Samsung Display announced plans to start mass production of Mini-LED automotive panels in Q4 2025, signaling a significant shift in the automotive display market.[1]Samsung Display, “Automotive Mini-LED Mass Production,” samsungdisplay.com

Micro-LED Yield Issues Prolonging Mini-LED Window

Micro-LED technology continues to face significant challenges in achieving the 99.999% defect-free threshold required for large displays, hindering its commercial viability. Apple’s decision to cancel its Micro-LED program in March 2024 further underscored the challenges of scaling this technology. Despite ongoing efforts, the substantial capital investments made by companies such as Ams Osram and Sanan highlight the immense technical and financial barriers that remain. As a result, Mini-LED has emerged as the preferred high-brightness solution for the medium term, offering a more practical and cost-effective alternative while the industry works to overcome Micro-LED's limitations.[2]Sixteen-Nine, “Micro-LED Manufacturing Challenges,” sixteen-nine.net

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bill of Materials Premium Over OLED Below 55 Inch | -3.2% | Global mass market | Medium term (2-4 years) |

| HDR Halo Complaints in Gaming Monitors | -2.1% | Global gaming segment | Long term (≥ 4 years) |

| EU Ecodesign Ban on > 5 W Back-Lights 2028 | -1.8% | Europe | Medium term (2-4 years) |

| Rare-Earth Phosphor Price Volatility | -1.4% | Global, China-weighted supply | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bill of Materials Premium Over OLED Below 55 Inch

In 2025, Mini-LED panels below 55 inches remained costlier than OLED panels due to the higher LED-array density and the need for additional driver ICs. This cost disparity limited the penetration of Mini-LED technology in price-sensitive market segments, where affordability is a key factor. However, advancements in QD on-chip integration have started to reduce phosphor-related expenses, gradually narrowing the cost gap between Mini-LED and OLED. Despite these improvements, the adoption of Mini-LED in mid-size displays is expected to remain limited until after 2028. Manufacturers are focusing on optimizing production processes to make Mini-LED technology more competitive in the coming years.

HDR Halo Complaints in Gaming Monitors

Blooming artifacts around bright objects in dark scenes remained a significant issue on mid-range Mini-LED gaming monitors, which typically feature only 200-500 dimming zones. These artifacts, often referred to as HDR halo effects, negatively affected the viewing experience and led to unfavorable user reviews. The resulting erosion in perceived value compared to OLED displays forced manufacturers to increase the number of dimming zones and enhance algorithmic complexity to address the issue. However, these improvements came at the cost of higher production expenses and increased power consumption. As a result, the growth of Mini-LED technology in the highly competitive gaming monitor segment has been tempered, with brands striving to balance performance enhancements and cost efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Televisions Anchor Volume, Automotive Accelerates

Televisions accounted for 38.23% of the Mini-LED Display market in 2025, supported by premium models that offered higher brightness than OLED at lower prices.[3]Sixteen-Nine, “Micro-LED Manufacturing Challenges,” sixteen-nine.net The segment benefited from rapid capacity shifts and subsidies in China. Automotive displays are projected to grow at a 27.55% CAGR through 2031 as electric vehicles increasingly adopt cockpit screens larger than 10 inches. These larger screens require superior sunlight readability to enhance driver visibility and support advanced functionalities. The demand for high-performance displays is further driven by the integration of advanced driver assistance systems (ADAS) and infotainment features. Additionally, the push for energy-efficient, durable display technologies is expected to drive growth in this segment over the forecast period.

Adoption of Mini-LED in professional monitors and laptops has strengthened since it met HDR certifications exceeding 1,000 nits and 100% DCI-P3, making it highly attractive to content creators. These certifications ensure superior color accuracy and brightness, critical for professional applications such as video editing and graphic design. Smartphones and tablets saw limited adoption, particularly with Apple’s iPad Pro, which used Mini-LED for enhanced display performance. However, wearables remained a niche application due to thermal constraints and the high cost of Mini-LED technology. Despite these challenges, advancements in Mini-LED technology are expected to gradually expand its adoption across various device categories.

By Technology: Back-Light Units Dominate, Direct-Emissive Gains Traction

Back-light unit configurations accounted for 72.48% of sales in 2025, primarily due to their compatibility with existing LCD manufacturing lines. This compatibility allowed manufacturers to integrate Mini-LED technology without significant changes to production processes, making it a cost-effective solution. Additionally, the demand for high-performance displays across automotive and consumer electronics applications further drove the adoption of back-light units. The technology's ability to enhance brightness and contrast while maintaining energy efficiency contributed to its widespread use. As a result, back-light units remained a dominant segment in the mini-light-emitting diode (LED) display market during this period.

Direct-emissive Mini-LED technology is projected to grow at a compound annual growth rate (CAGR) of 27.78% from 2025 to 2031, driven by advancements in display technology and increasing demand for innovative applications. Samsung’s 130-inch Micro RGB showcase and the rising interest in transparent displays have significantly contributed to this growth trajectory. Unlike traditional back-light units, direct-emissive Mini-LED eliminates the need for liquid crystals, enabling pixel-level control and improved transparency. However, the technology requires 10-20 times as many LEDs, leading to higher production costs and greater thermal management challenges. Consequently, its adoption is expected to remain focused on large-format signage and specialized installations, where its unique benefits outweigh the associated costs.

By Backplane Integration: Glass Active Matrix Leads, Flexible Substrates Accelerate

Glass active-matrix backplanes commanded 46.19% of 2025 revenue, offering precise dimming across thousands of zones. These back-planes benefit significantly from shared infrastructure with LCD and OLED technologies, making them a cost-effective and efficient choice. Their ability to deliver high performance in terms of brightness and contrast has made them a preferred option in the market. Flexible hybrid substrates are projected to grow at a 27.97% CAGR during the 2026-2031 period. This growth is driven by increasing demand for curved dashboards in automotive applications and for foldable consumer devices, both of which require advanced display technologies.

PCB passive matrix options cater to entry-level displays, offering a more affordable solution but with limited zone counts due to voltage drops, such as AUO and Innolux in flexible capacity, underscoring the growing importance of bendable backplane constraints. These options are primarily used in applications where cost efficiency is a priority over advanced features. Investments by key players such as AUO and Innolux in flexible capacity underscore the growing importance of bendable backplanes. These innovations are particularly critical for automotive displays and next-generation laptops, where flexibility and durability are essential for meeting evolving consumer and industry demands.

Geography Analysis

Asia-Pacific captured 54.74% market share in 2025, driven by China’s vertically integrated ecosystem, where BOE, TCL, CSOT, and Tianma aligned LED chip and panel production for speed and cost savings. Subsidies lifted Mini-LED television share toward 10% domestically, while South Korea’s Samsung Display and LG Display redirected capacity from OLED to Mini-LED to defend their market share. Additionally, the region benefited from a strong supply chain and government support, which further accelerated adoption. The increasing demand for high-performance displays in consumer electronics and automotive applications also contributed to the region's dominance. Asia-Pacific remains a key hub for innovation and production in the mini-LED display market.

North America and Europe favored premium televisions and gaming monitors, with automakers in both regions specifying Mini-LED cockpits for electric vehicles to enhance display quality and functionality. The European Union’s Ecodesign rules, effective in 2028, place efficiency pressure on back-light power, inadvertently encouraging the adoption of high-zone Mini-LED designs that improve luminance per watt.[4]European Commission, “Ecodesign Regulation 2019/2021,” ec.europa.euThese regions also witnessed growing investments in display technologies to meet e increasing demand for energy-efficient, high-resolution displays. The focus on sustainability and innovation has positioned North America and Europe as significant contributors to the Mini-LED market. Furthermore, the rising popularity of gaming and home entertainment systems has driven demand for premium display solutions.

The Middle East is projected to record the fastest regional CAGR at 27.81% through 2031, propelled by large-format digital signage in commercial real estate and transportation hubs. The region's focus on modernizing infrastructure and adopting advanced technologies has fueled the demand for Mini-LED displays. Additionally, government initiatives to develop smart cities and enhance public spaces have further boosted the market. South America and Africa remain smaller contributors but are starting to deploy Mini-LED video walls in high-visibility urban projects. These regions are gradually embracing Mini-LED technology for applications in advertising, entertainment, and public information systems, showcasing their potential for future growth.

Competitive Landscape

The market is moderately fragmented. Samsung Electronics, LG Display, BOE Technology Group, AU Optronics, and TCL CSOT lead panel shipments, while Nichia, Epistar, and Seoul Semiconductor dominate LED chips. Vertical integration accelerated in 2026 after TCL CSOT purchased a 80% stake in Prima for CNY 490 million (USD 70 million) to secure chip supply for its Suzhou video wall line. This acquisition enabled TCL CSOT to streamline its supply chain and reduce its reliance on external suppliers, thereby enhancing production efficiency. The move also positioned the company to better compete in the global market by ensuring a steady supply of critical components.

Chinese disruptors such as Nationstar and Sanan leveraged lower costs to pressure Japanese and Taiwanese suppliers, fostering price erosion that broadened mid-tier adoption. These companies capitalized on their cost advantages to expand their market presence, particularly in emerging economies. Differentiation now centers on zone density, AI back-light algorithms, and integrated quantum-dot layers, which are becoming key competitive factors. Samsung’s NQ4 AI Gen2 processor exemplifies this trend, leveraging real-time scene analysis to enhance contrast and reduce power consumption. Such innovations are driving the adoption of Mini-LED technology across a range of applications, including televisions and automotive displays.

Micro-LED advances remain on industry roadmaps, but yield challenges mean Mini-LED will capture premium and mid-tier share through at least 2031. The high production costs and technical complexities of Micro-LEDs have delayed their widespread adoption, keeping Mini-LEDs as the preferred choice for many manufacturers. Suppliers capable of ramping flexible substrates and automotive-grade reliability will command premium margins as cockpit digitization expands. This trend is particularly evident in the automotive sector, where demand for advanced display technologies continues to grow. As a result, Mini-LED technology is expected to maintain its dominance in the market for the foreseeable future.

Mini-LED Display Industry Leaders

Samsung Electronics Co., Ltd.

LG Display Co., Ltd.

BOE Technology Group Co., Ltd.

AU Optronics Corp.

TCL China Star Optoelectronics Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Xiaomi launched its new Mini-LED TV S series in India, featuring enhanced brightness, contrast, and color accuracy using advanced Mini-LED backlighting technology.

- January 2026: Samsung Electronics and LG Electronics showcased RGB Mini-LED TVs at CES 2026; Samsung also revealed a 130-inch Micro RGB television.

- January 2026: Samsung Electronics introduced its 2026 Neo QLED 4K and new Mini-LED series spanning 43 inches to 100 inches, powered by NQ4 AI Gen2 processors.

- January 2026: TCL CSOT acquired 80% of Prima for CNY 490 million (USD 70 million) to vertically integrate LED chip manufacturing.

Global Mini-LED Display Market Report Scope

The Mini-LED Display Market refers to the segment of the display industry focused on screens that use thousands of microscopic light-emitting diodes (typically 100-200 microns in size) as a backlight or as a direct display technology to enhance brightness, contrast, and color accuracy. Mini-LED technology is primarily used in LCD panels to enable advanced local dimming, delivering performance closer to OLED while maintaining higher brightness and longer lifespan.

The Mini-LED Display Market Report is Segmented by Application (Televisions, IT Monitors and Laptops, Smartphones and Tablets, Automotive Displays, and Wearables and AR/VR), Technology (Mini-LED Backlight Unit, and Direct-Emissive Mini-LED), Backplane Integration (PCB Passive Matrix, Glass Active Matrix, and Flexible Hybrid Substrate), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| TVs |

| IT Monitors and Laptops |

| Smartphones and Tablets |

| Automotive Displays |

| Wearables and AR/VR |

| Mini-LED Backlight Unit (BLU) |

| Direct-Emissive Mini-LED |

| PCB Passive Matrix |

| Glass Active Matrix |

| Flexible Hybrid Substrate |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application | TVs | ||

| IT Monitors and Laptops | |||

| Smartphones and Tablets | |||

| Automotive Displays | |||

| Wearables and AR/VR | |||

| By Technology | Mini-LED Backlight Unit (BLU) | ||

| Direct-Emissive Mini-LED | |||

| By Backplane Integration | PCB Passive Matrix | ||

| Glass Active Matrix | |||

| Flexible Hybrid Substrate | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the mini-LED display market by 2031?

The mini-LED display market size is forecast to reach USD 2.47 billion by 2031 at an 27.20% CAGR.

How fast is Mini-LED TV adoption growing in China?

Government subsidies drove Mini-LED television penetration to nearly 10% of domestic shipments in 2025, with projected volume of 20 million units in 2026.

Why do automakers prefer Mini-LED over OLED for cockpits?

Mini-LED exceeds 2,000 nits brightness, avoids burn-in, and meets the thermal stability required for automotive qualification.

What keeps Micro-LED from replacing Mini-LED quickly?

Mass transfer yields remain below the 99.999% threshold, making Micro-LED too costly for mainstream consumer products before 2031.

Which back-plane type leads Mini-LED integration?

Glass active matrix back-planes held 46.19% share in 2025 because they leverage existing LCD infrastructure for precise dimming control.

What is the outlook for flexible Mini-LED substrates?

Flexible hybrid back-planes are forecast to post a 27.97% CAGR through 2031 as curved dashboards and foldable devices gain traction.

Page last updated on: