Ceiling Tiles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

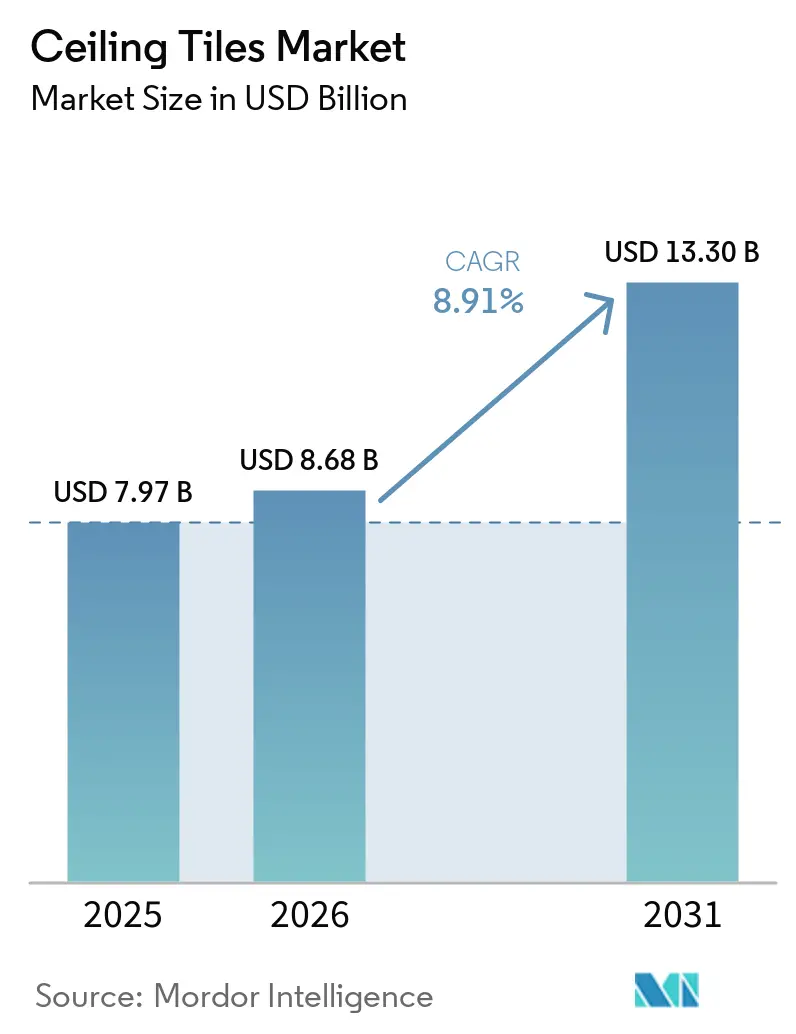

| Market Size (2026) | USD 8.68 Billion |

| Market Size (2031) | USD 13.30 Billion |

| Growth Rate (2026 - 2031) | 8.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ceiling Tiles Market Analysis by Mordor Intelligence

The Ceiling Tiles Market size is expected to increase from USD 7.97 billion in 2025 to USD 8.68 billion in 2026 and reach USD 13.30 billion by 2031, growing at a CAGR of 8.91% over 2026-2031. This ceiling tiles market trajectory is fueled by workplace acoustics mandates, decarbonization pressures on mineral‐fibre substrates, and large‐scale infrastructure investments in Asia that specify non-combustible assemblies. Growth is also tied to bio-based binder breakthroughs that shrink embodied carbon, digital-print platforms that shorten lead times from eight weeks to 10 days, and emerging demand for corrosion-resistant metal panels in humid transit hubs. Competitive intensity remains moderate as the top five suppliers chase regional manufacturing footprints to blunt logistics risk, while smaller Asian manufacturers rely on low-cost gypsum and POP alternatives to win price-sensitive projects. Energy-price volatility, however, continues to inflate mineral-wool production costs in Europe and North America, and substitutes such as mortar-applied acoustic plasters threaten volume growth in low-headroom renovations.

Key Report Takeaways

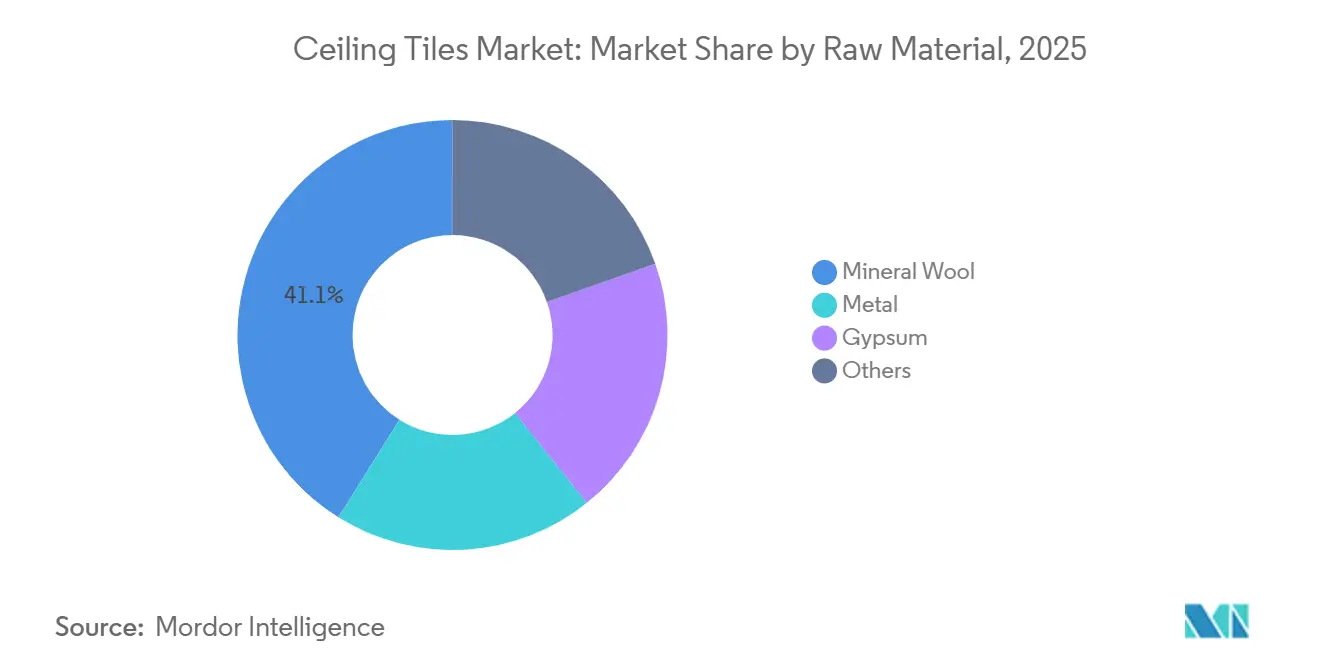

- By raw material, mineral wool captured 41.12% of the ceiling tiles market share in 2025, while metal tiles are advancing at a 9.03% CAGR through 2031.

- By property, acoustic panels led with 65.66% of the ceiling tiles market size in 2025, and non-acoustic multifunctional tiles are expanding at a 9.22% CAGR to 2031.

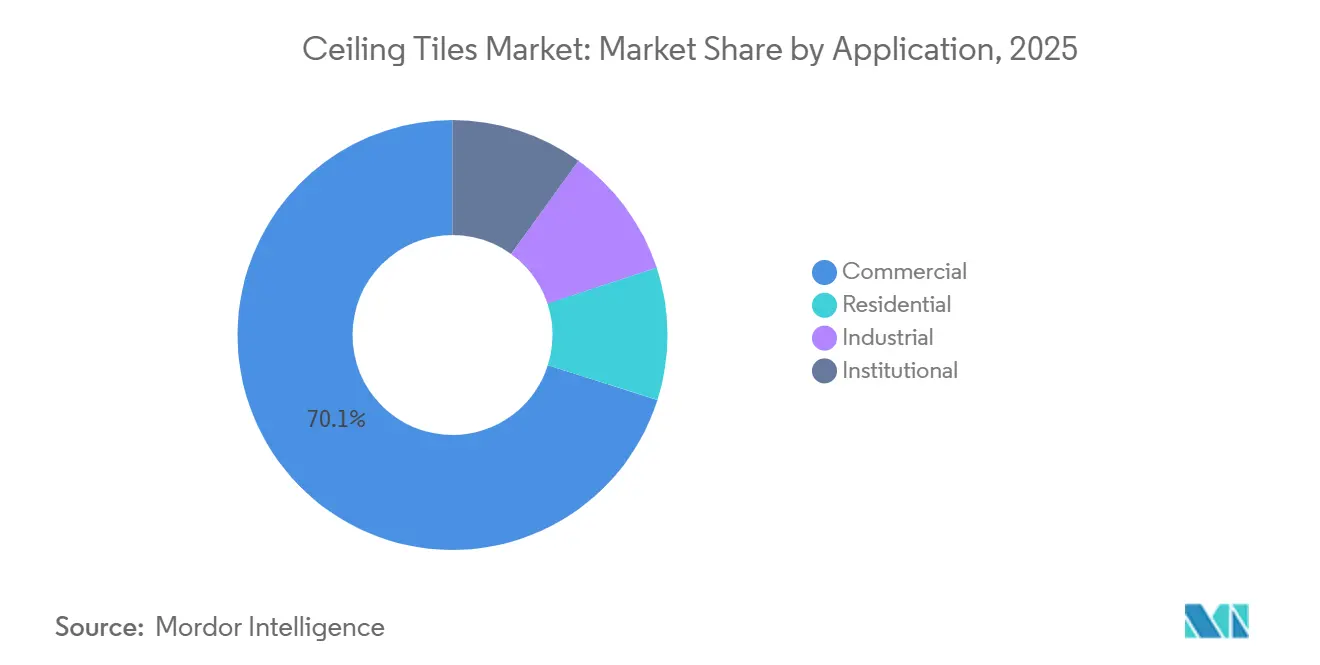

- By application, commercial buildings accounted for 70.12% of demand in 2025; residential installations are growing at a 9.62% CAGR through 2031.

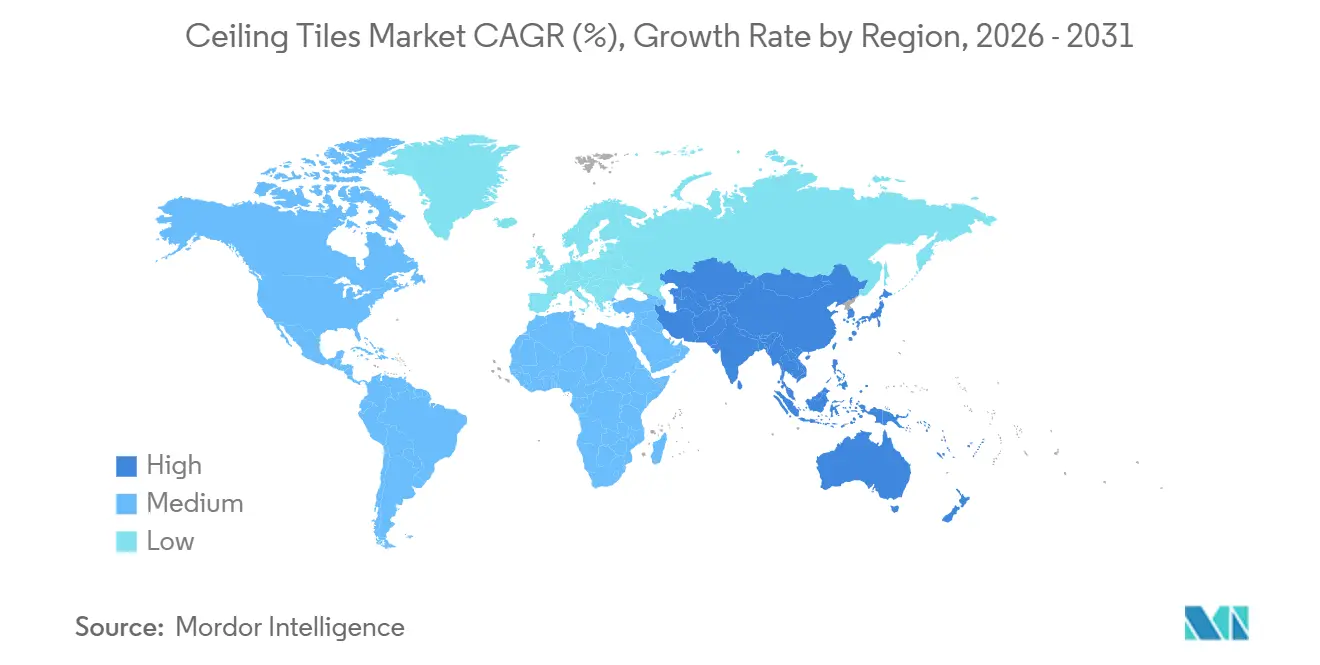

- By geography, North America held 35.34% of 2025 revenue, whereas Asia Pacific is forecast to grow at a 10.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ceiling Tiles Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of acoustic systems in open-plan offices | +1.8% | Global, with concentration in North America, Western Europe, and Asia Pacific urban centers | Medium term (2–4 years) |

| Green-building credits boosting mineral-wool retrofits in Europe | +1.5% | Europe (EU-27, UK, Nordics), spillover to North America | Long term (≥4 years) |

| Metro and airport build-outs mandating non-combustible tiles in Asia | +2.1% | Asia Pacific core (China, India, ASEAN), spillover to Middle East | Short term (≤2 years) |

| Digital-print gypsum tiles enabling premiumization in GCC luxury real estate | +0.9% | Middle East (Saudi Arabia, UAE, Qatar), niche adoption in North America and Europe | Medium term (2–4 years) |

| Bio-based binders cutting embodied carbon of mineral-fiber tiles | +1.3% | Europe, North America, early gains in Australia and Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Acoustic Systems in Open-Plan Offices

As hybrid work models evolve, the demand for quieter collaboration zones intensifies. Rockfon's Sonar dB35 panels, boasting a 0.95 NRC, experienced increased adoption driven by corporate retrofits. Meanwhile, Armstrong's TechZone Ultima system made its mark in the new U.S. Class A office segment. A 2024 study by the Acoustical Society of America revealed a concerning trend: ceiling absorption coefficients dipping below 0.80 are linked to a decline in productivity for floorplates larger than 5,000 sq ft [1]Acoustical Society of America, “Open-Plan Productivity and Ceiling Absorption,” acousticalsociety.org . Knauf's Heradesign wood-wool tiles not only meet the reverberation standards of the WELL Building Standard but also offer the biophilic aesthetics that have gained traction in Europe. These trends highlight the robust demand for acoustic-grade products in the ceiling tiles market.

Green-Building Credits Boosting Mineral-Wool Retrofits in Europe

By 2025, the EU's Building Performance Directive 2024/1275 mandates that governments unveil whole-life carbon benchmarks for public buildings. This move also promotes the use of mineral-wool tiles that come with Environmental Product Declarations. Saint-Gobain's Ecophon Master Rigid, boasting Nordic Swan certification, has gained traction in Germany's retrofit market. Meanwhile, Rockfon's Sonar dB35 line, crafted with recycled content, meets the criteria for BREEAM Excellent credits, bolstering bids for hospitals in the U.K. Given these developments, the European ceiling tiles market is poised for growth, driven by directive-led retrofits.

Metro and Airport Build-Outs Mandating Non-Combustible Tiles in Asia

Asia Pacific’s infrastructure pipeline specifies A1-rated ceilings. Hong Kong International Airport’s Three Runway System used PRANCE aluminum tiles. India added a metro track in 2024, adopting IS 1646:2023 standards that prioritize mineral wool and metal panels over POP. Singapore’s Changi Terminal 5 has pre-qualified Rockfon and USG products that meet ASTM E84 Class A requirements. Such mandates accelerate metal-tile penetration and reinforce regional growth across the ceiling tiles market.

Digital-Print Gypsum Tiles Enabling Premiumization in GCC Luxury Real Estate

High-end developers in the Gulf are purchasing digital-print gypsum panels to differentiate interiors. Armstrong’s CREATE! platform reduces lead time and commands premiums in Saudi and UAE projects. MCI Metalldecken delivered backlit imagery ceilings for Dubai’s Burj Binghatti, achieving a notable price uplift. USG Boral recorded a presence in luxury villas with digital-print gypsum tiles across Riyadh and Abu Dhabi. Customization trends position the ceiling tiles market for higher margin products.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-price volatility inflating mineral-wool costs | -1.2% | Europe, North America, spillover to Asia Pacific manufacturing hubs | Short term (≤2 years) |

| Threat from substitutes such as asphalt and mortar | -0.5% | Global, with concentration in industrial and warehouse applications in North America and Europe | Medium term (2–4 years) |

| Low-cost POP ceilings constraining gypsum-tile uptake in Asia Pacific | -0.7% | Asia Pacific (India, Southeast Asia, Tier 2 and Tier 3 cities), emerging markets in Middle East and Africa | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Energy-Price Volatility Inflating Mineral-Wool Costs

In the first half of 2025, European natural-gas futures increased compared to 2024. This surge in gas prices led to a rise in production costs for both Rockfon and Saint-Gobain. Meanwhile, the U.S. Producer Price Index (PPI) for mineral-wool manufacturing also experienced a year-over-year increase. Additionally, smaller Asian producers, who are importing spot LNG, are experiencing margin compression. This situation is diminishing their competitiveness in the ceiling tiles market.

Threat from Substitutes Such as Asphalt, Mortar, and Low-Cost POP Ceilings

In India, POP false ceilings have undercut gypsum prices, now dominating mid-tier apartments, according to an IGBC 2025 survey[2]Indian Green Building Council, “POP vs Gypsum Survey,” igbc.in . In Southeast Asia, mortar-applied acoustic plasters, favored for eliminating grid requirements, secure a foothold in retrofit projects. Meanwhile, asphalt acoustic panels are making inroads into warehouses, where aesthetics take a backseat, thereby limiting premium growth in the ceiling tiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Mineral Wool Maintains Lead, Metal Gains Momentum

Mineral wool owned 41.12% of the ceiling tiles market share in 2025 as architects valued its thermal and acoustic duality. Metal panels, mainly aluminum, are rising at a 9.03% CAGR because they resist humidity and carry A1 fire ratings required at airports and metros. Gypsum tiles dominate cost-conscious residential builds, though POP competition is squeezing margins in India and Southeast Asia. Composite, PVC, and wood options serve luxury niches seeking organic aesthetics with customized graphics.

Asia Pacific is the backbone of metal's rise, with projects like Hong Kong’s Three Runway System and India’s metro expansion referencing EN 13501-1 and IS 1646:2023 non-combustible standards. In Europe and North America, mineral wool holds sway in retrofits, driven by the importance of environmental product declarations and WELL acoustic scores. Gypsum's cost-effectiveness ensures its continued use, yet its moisture sensitivity poses challenges in bathrooms and humid climates. Highlighting a market trend, bio-based innovations like Armstrong’s Ultima LEC tile signal a move towards lower-carbon raw materials in the ceiling tiles industry.

By Property: Acoustic Dominates, Multifunctional Panels Accelerate

Acoustic solutions controlled 65.66% of the ceiling tiles market size in 2025, underpinned by WELL and ASHRAE 189.1 criteria in offices, schools, and hospitals. Non-acoustic multifunctional tiles, embedding antimicrobial films and moisture barriers, are expanding at a 9.22% CAGR. Armstrong's ACOUSTIBUILT tiles, boasting a 0.90 NRC, seamlessly merge BIOBLOCK protection with HUMIGUARD moisture resistance, showcasing a blend of performance attributes.

As hybrid workforces prioritize speech privacy, corporate retrofits are driving up acoustic demand. In contrast, while residential and light-industrial buildings might settle for a lower NRC, they value design flexibility and antibacterial properties. Shandong Huamei's antimicrobial PVC ceilings, undercutting stone-wool counterparts, have gained traction in China's residential sector. The ongoing integration of features is not only redefining traditional property boundaries but also expanding the revenue potential for the ceiling tiles market.

By Application: Commercial Strength, Residential Velocity

Commercial buildings generated 70.12% of 2025 revenue thanks to stringent ASTM E84 and ISO 9705 fire regulations in headquarters, hospitals, and campuses. Residential volume is stretching at a 9.62% CAGR as North American single-family starts rise and Indian apartment schemes seek quick-install gypsum systems. Industrial users favor metal and PVC tiles for durability under chemical exposure, while institutional projects emphasize both fire safety and acoustics.

North American offices typically refresh ceilings every 12-15 years, ensuring retrofit recurrence. India’s need for affordable urban housing and China’s Tier-2 city growth fuel gypsum and POP installations. Warehousing growth tied to e-commerce drives metal tile usage, and government offices prioritize compliant acoustic assemblies. The ceiling tiles market thus balances mature replacement cycles with emerging residential uptake.

Geography Analysis

North America held 35.34% of 2025 revenue, supported by LEED v4.1 and WELL adoption, plus stable retrofit demand. Asia Pacific is forecast to grow at a 10.56% CAGR, reflecting China’s metro stations, India’s airport upgrades, and ASEAN’s transit hubs, all of which call for non-combustible solutions. Europe’s share stays resilient through mineral-wool retrofits that satisfy the EU Building Performance Directive. Latin America and the Middle East-Africa register mid-single-digit expansion driven by Brazil’s residential starts and GCC luxury developments.

China’s construction output increased in 2024, concentrating mineral wool and metal tile usage in Tier-1 and Tier-2 commercial builds. Japan’s aging stock spurs acoustic retrofits, while Vietnam, Thailand, and Indonesia tighten fire codes, inviting A1-rated products. The ceiling tiles market outlook remains most upbeat in Asia, where rapid urbanization converges with stricter safety standards.

Competitive Landscape

The ceiling tiles market is fragmented. Competition centers on sustainability labels, digital-print speed, and local production. Armstrong’s CREATE! platform shortens customization cycles, trimming project costs by up to 20%. MCI Metalldecken’s backlit metal tiles similarly enhance design flexibility for luxury projects. Regional challengers in China and India compete on cost, relying on domestic gypsum and POP. The influx of bio-based binders and multifunctional surfaces is expected to reshape product hierarchies and intensify differentiation strategies across the ceiling tiles market.

Ceiling Tiles Industry Leaders

AWI Licensing LLC

Knauf Group

Saint-Gobain

ROCKWOOL A/S

Hunter Douglas N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Saint-Gobain India Pvt. Ltd., through its Gyproc business, commissioned India's first near-net-zero gypsum ceiling tiles plant in Visakhapatnam. This marked a significant step toward sustainable construction manufacturing in the country.

- July 2025: Knauf Group inaugurated a new ceiling production facility in Illange, France, specializing in mineral ceilings. This investment aims to enhance sustainability and foster collaboration between Knauf Insulation and Knauf Ceiling Solutions, converting the 2019 rock wool site into a joint production hub.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the ceiling tiles market as factory-made mineral fiber, metal, and gypsum panels that are fitted into exposed-grid or direct-mount systems to form interior ceilings providing acoustic, thermal, and aesthetic functions.

Scope exclusion: Roofing sheets, drywall boards, and structural wall panels lie outside this assessment.

Segmentation Overview

- By Raw Material

- Mineral Wool

- Metal

- Gypsum

- Others (Composite, Plastic and Wood)

- By Property

- Acoustic

- Non-Acoustic

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- By Geography

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle-East and Africa

- Asia Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed installers, distributors, specifiers, and procurement managers across North America, Europe, and three Asia-Pacific growth hubs to validate acoustic adoption rates, refurbishment cycles, and average panel thickness shifts. Follow-up surveys with sustainability officers helped refine assumptions on recycled content premiums.

Desk Research

We started by mapping production, trade, and usage indicators drawn from sources such as UN Comtrade customs codes for mineral fiber boards, U.S. Census Bureau's Construction Put-in-Place tables, Eurostat building permits, and Energy Performance of Buildings directives. Industry specifics were enriched with data from trade bodies like the North American Insulation Manufacturers Association and the European Association for Passive Fire Protection, in addition to company 10-Ks and investor decks that disclose average selling prices. Our paid access to D&B Hoovers and Dow Jones Factiva supplied revenue splits and project news that anchor manufacturer share assumptions. These sources are illustrative, not exhaustive; many others supported data checks and context building.

A second pass gathered regulatory and patent cues (Questel) on low-VOC binders and phase-change inserts that influence pricing trajectories and adoption speed.

Market-Sizing & Forecasting

The market value baseline employs a top-down reconstruction of global non-residential floor-area additions and renovation outlays, adjusted with ceiling-to-floor ratios and penetration rates for suspended systems, which are then priced using region-specific ASPs. Supplier roll-ups and channel checks provide bottom-up spotlights that calibrate totals. Key variables include metro office completions, healthcare bed additions, acoustic regulation intensity scores, mineral wool unit prices, and gypsum board cost inflation. Forecasts apply multivariate regression blended with scenario analysis to link those drivers to demand up to 2030. Data gaps in smaller geographies are bridged by per-capita construction spend proxies benchmarked against peer markets before final adjustment.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst cross-checks, and quarterly re-contacts when price swings exceed five percent. Reports refresh annually, and a live watchlist flags mergers or code changes that can trigger interim updates.

Why Our Ceiling Tiles Baseline Commands Reliability

Published figures often diverge because each firm chooses different material mixes, end-use splits, price bases, and refresh cadences.

Key gap drivers include whether residential retrofit demand is counted, how mineral-fiber import values are converted to installed revenue, and if recycled-content premiums are modeled. Mordor's study reports 2025 installed-value terms, applies blended ASPs vetted with installers, and refreshes every twelve months; other publishers may cite factory-gate 2022 values or extrapolate forward with single-factor growth rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.59 B (2025) | Mordor Intelligence | - |

| USD 8.14 B (2024) | Global Consultancy A | Uses factory-gate pricing; omits retrofit volumes |

| USD 8.40 B (2022) | Industry Data Service B | Older base year and static ASP escalation |

| USD 7.42 B (2023) | Trade Journal C | Excludes mineral-fiber metal hybrids; limited regional splits |

The comparison shows that once scope, pricing point, and refresh cadence are aligned, disparities narrow significantly. This is where Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the ceiling tile market in 2026?

The ceiling tiles market size stands at USD 8.68 billion in 2026, with an 8.91% CAGR projected through 2031, reaching USD 13.30 billion.

Which raw material holds the largest share of global demand?

Mineral-wool panels account for 41.12% of 2025 sales owing to their combined thermal and acoustic performance.

What is the fastest-growing regional opportunity?

Asia Pacific leads with a 10.56% CAGR, driven by non-combustible specifications in metro and airport projects.

Why are digital-print ceilings gaining traction?

Platforms such as Armstrong’s CREATE! cut lead times and enable custom graphics that command higher margins.

How are rising energy prices affecting producers?

European gas price spikes raised mineral-wool manufacturing costs, pressuring margins and prompting renewable-powered production shifts.

Which sustainability trend is most influential?

Bio-based binders, like Armstrong’s biochar and Owens Corning’s maltodextrin systems, are reducing embodied carbon to comply with forthcoming LEED v5 carbon disclosure rules.

Page last updated on: