Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

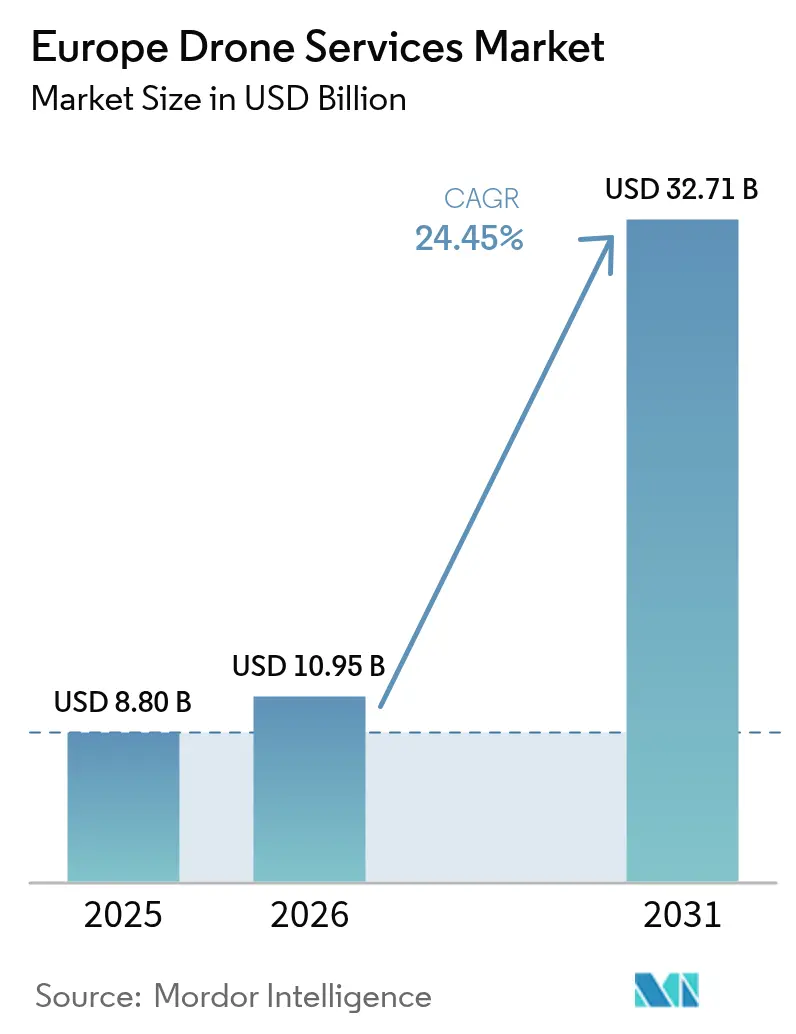

| Base Year Market Size (2025) | USD 8.80 Billion |

| Market Size (2026) | USD 10.95 Billion |

| Market Size (2031) | USD 32.71 Billion |

| Growth Rate (2026 - 2031) | 24.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Drone Services Market Analysis by Mordor Intelligence

Europe drone services market size in 2026 is estimated at USD 10.95 billion, growing from 2025 value of USD 8.80 billion with 2031 projections showing USD 32.71 billion, growing at 24.45% CAGR over 2026-2031. Growth has three pillars: EU-level regulatory harmonization, rapid progress in beyond-visual-line-of-sight (BVLOS) automation, and enterprise demand for faster, safer, and cheaper inspection workflows. The European Union Aviation Safety Agency (EASA) now lets operators file a single declaration to fly the same mission profile in any member state, eliminating duplicate paperwork and encouraging providers to scale across borders.[1]Source: European Union Aviation Safety Agency, “Civil Drones,” easa.europa.eu Construction and infrastructure owners have already cut bridge-inspection costs by as much as 40% when replacing rope crews with drones. Utilities lower power-line survey expenses by up to 80% versus helicopter patrols while saving 258 tons of CO₂ annually. Together, these efficiencies expand the Europe drone services market by attracting asset-intensive industries that once relied on traditional methods.

Key Report Takeaways

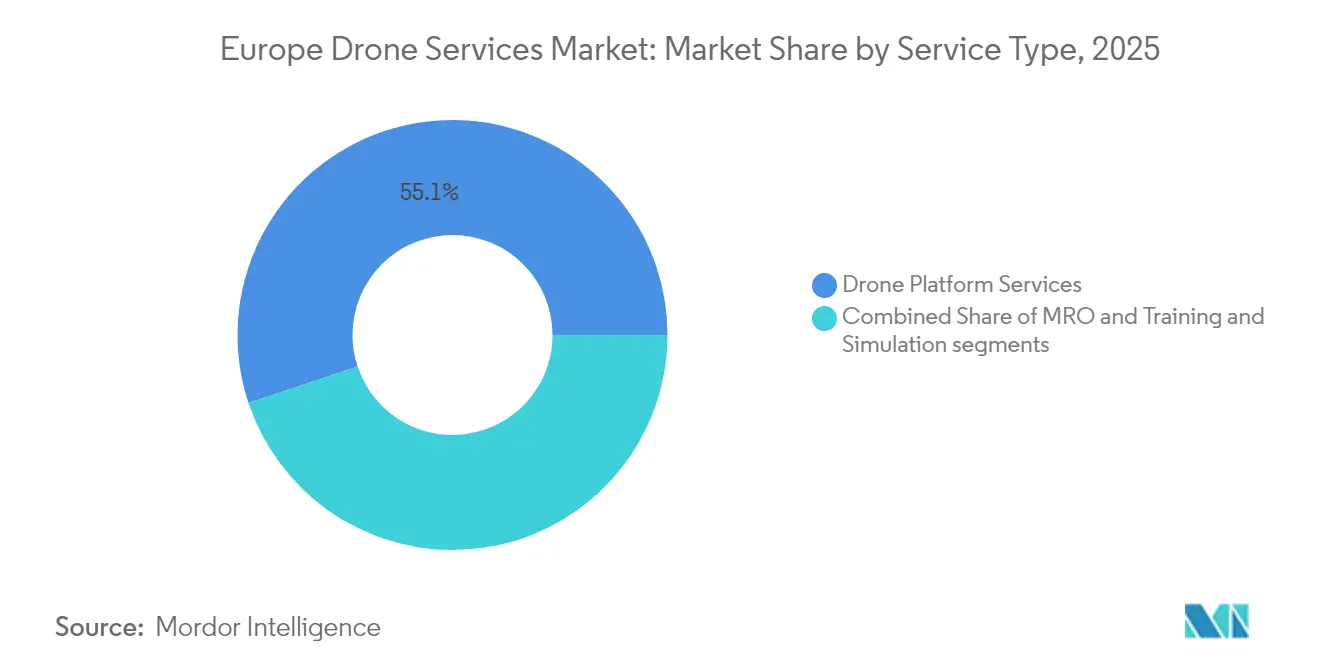

- By service type, platform services led with 55.12% of the Europe drone services market share in 2025, while training and simulation recorded the highest CAGR at 29.74% through 2031.

- By end-user industry, construction and infrastructure commanded 32.30% revenue share in 2025; medical and parcel delivery are forecasted to expand at a 29.35% CAGR to 2031.

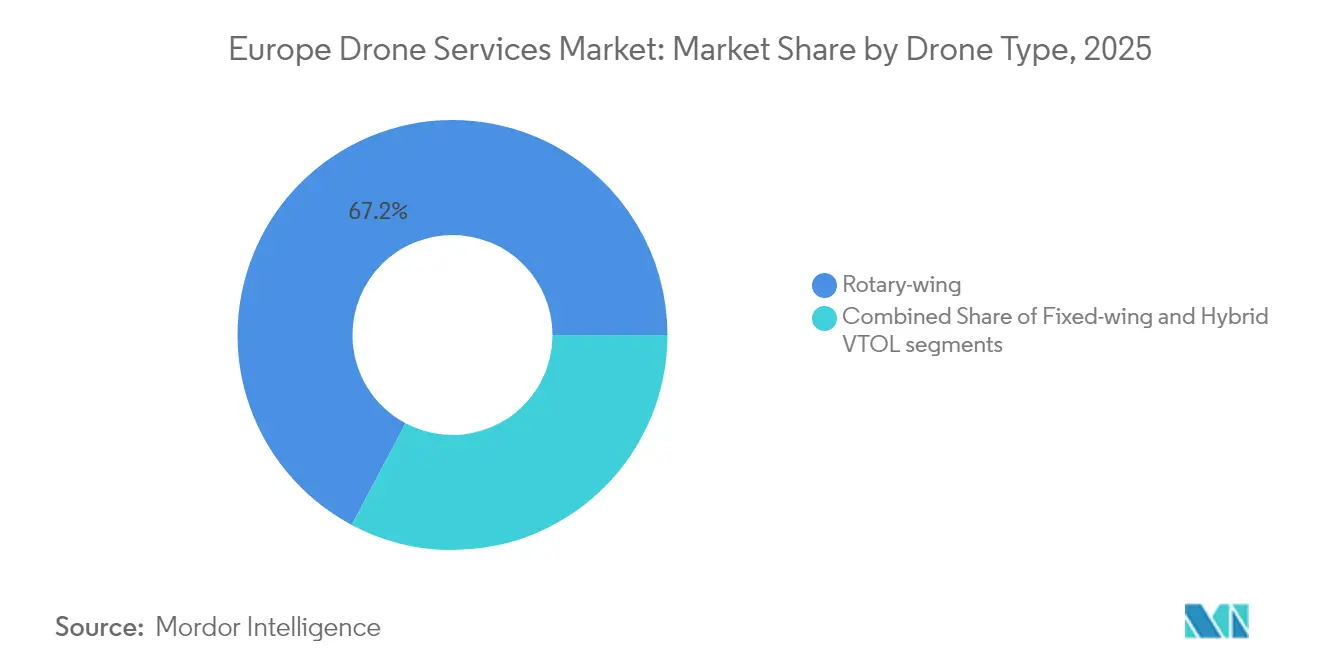

- By drone type, rotary-wing systems held 67.23% of the Europe drone services market size in 2025, and hybrid VTOL is progressing at a 29.96% CAGR to 2031.

- By operating range, visual-line-of-sight (VLOS) flights represented 76.20% of the European drone services market in 2025, whereas BVLOS services are growing at 30.31% CAGR.

- By geography, the United Kingdom accounted for 28.70% of the Europe drone services market share in 2025, while Spain is projected to register the highest growth at 29.31% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Drone Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU regulatory harmonization accelerates BVLOS approvals | 6.2% | EU-wide, strongest in UK, Germany, France | Medium term (2-4 years) |

| Rising demand for asset inspection and monitoring | 5.8% | Global, concentrated in UK, Germany, Netherlands | Short term (≤ 2 years) |

| Logistics and e-commerce pilots scaling drone delivery | 4.9% | Urban centers across EU, led by UK, Spain | Medium term (2-4 years) |

| Cost advantage vs. helicopters for energy inspections | 3.7% | Northern Europe, offshore wind regions | Short term (≤ 2 years) |

| Subsidies for pesticide-reduction via ag-spraying drones | 2.4% | Agricultural regions, France, Spain, Italy | Long term (≥ 4 years) |

| Defense-sector pilot training spill-over to civil market | 2.3% | NATO countries, concentrated in UK, Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Regulatory Harmonization Accelerates BVLOS Approvals

The Europe drone services market benefits from a single rulebook that supersedes legacy national laws. EASA’s Standard Scenarios, effective January 2024, replace lengthy authorizations with self-declarations for routine BVLOS work. Providers redeploy aircraft and pilots across borders without extra licensing, enabling pan-European contracts that were impossible two years ago. Pilot-certificate reciprocity further unifies labor pools, though some states still apply stricter interpretations that delay approvals. Full alignment will likely be by 2026, unlocking another tier of BVLOS demand and sharpening competition as larger firms consolidate regional specialists to gain scale.

Rising Demand for Asset Inspection and Monitoring

Asset-heavy sectors choose drones to reduce cost, downtime, and safety risks. Bridge owners finish inspections 75% faster while collecting higher-resolution imagery that feeds predictive-maintenance analytics.[2]Source: Flyability SA, “Bridge Inspections With Elios Drones,” flyability.com Wind turbine surveys cost USD 300–769 per unit compared to rope access costs of more than USD 2,000. Nordic utilities favor drones because harsh winter conditions limit climber days, but rarely use ground uncrewed aircraft equipped with de-icing systems. Therefore, the Europe drone services market deepens its presence in energy, transport, and industrial facilities as owners shift budgets from manual methods to digital twins maintained by autonomous fleets.

Logistics and E-commerce Pilots Scaling Drone Delivery

Urban healthcare networks now prove that BVLOS logistics works at the city scale. A London blood-sample route cut transport times from 30 minutes by car to 2 minutes by drone and reduced emissions by 99%. Similar pilots appear in Germany and the Netherlands as hospitals seek on-demand pathology and pharmacy runs. E-commerce platforms test lightweight parcels in congestion zones where vans face low-emission penalties. Growth hinges on airspace management and community acceptance, yet every successful trial expands the addressable segment for European drone services market providers with last-mile ambitions.

Cost Advantage Versus Helicopters for Energy Inspections

European grid operators transition from helicopter patrols to electric drones that consume a fraction of the fuel and operate safely near live wires. Sweden’s Vattenfall saved 258 tons of CO₂ annually by migrating 22,000 km of line surveys to unmanned aircraft. Offshore wind-farm owners record similar gains, scheduling more frequent checks without vessel mobilization or crew-transfer risk. These economics protect margins and support EU decarbonization targets, reinforcing long-term adoption trends that propel the Europe drone services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict BVLOS certification hurdles | -4.1% | EU-wide, particularly restrictive in Germany, France | Medium term (2-4 years) |

| Shortage of skilled drone pilots/operators | -3.6% | Global, acute in Nordic countries, Netherlands | Short term (≤ 2 years) |

| Public privacy and noise-nuisance concerns | -2.8% | Urban centers, particularly Germany, Netherlands | Long term (≥ 4 years) |

| Limited drone-specific insurance underwriting capacity | -2.1% | EU-wide, most restrictive in smaller markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict BVLOS Certification Hurdles

Even after harmonization, BVLOS operators submit detailed Specific Operations Risk Assessments that can exceed 300 pages and take up to 12 months to clear.[3]Source: FlytBase Inc., “EU Drone Regulations for BVLOS Operations,” flytbase.com Smaller firms struggle with legal fees and insurance premiums, discouraging market entry and slowing the shift from visual operations. Standard Scenarios cover only routine missions, so complex flights—such as over dense urban areas or near airports—continue to demand bespoke approvals. Uneven enforcement across national authorities adds uncertainty that restrains the European drone services market during the transition phase.

Shortage of Skilled Drone Pilots/Operators

EASA lists more than 1.6 million registered operators, yet the pool of BVLOS-qualified pilots remains thin. Demand for complex inspection and emergency-response missions outpaces training throughput, especially in Nordic markets where severe weather requires additional skill sets. As a result, training and simulation revenues grow 30.41% per year, but labor gaps still inflate project lead times. Defense-sector graduates offer partial relief, yet overall capacity lags market need, tempering near-term expansion for the Europe drone services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integrated Platforms Extend Lead

Drone platform services entered 2025 with 55.12% of Europe drone services market share, reflecting an enterprise shift toward turnkey offerings that wrap flight operations, cloud analytics, and compliance reporting into one contract. Buyers avoid the capital cost of in-house fleets and tap providers such as Cyberhawk, whose iHawk platform merges drone imagery with satellite and IoT feeds to power asset-health dashboards. Centralized data pipelines let clients benchmark sites across several countries while meeting harmonized EU record-keeping rules, a capability that attracts multinational utilities and construction majors. Because providers invoice on a per-asset or subscription basis, the revenue model delivers predictable cash flow that helps finance the continual software upgrades now expected by customers.

Training and simulation services, although a smaller slice today, are expanding at a 29.74% CAGR as insurers and regulators tighten pilot-qualification standards. High-fidelity virtual environments replicate BVLOS scenarios so crews can log competency hours without risking hardware or breaching airspace limits. Airlines and emergency-response agencies now mandate simulator credentials before pilots fly live sorties, pushing demand for accredited courseware across the Europe drone services market. This surge strengthens the overall European drone services market size by easing the pilot bottleneck, lowering accident rates, reducing insurance premiums, and broadening customer adoption.

By End-User Industry: Construction Holds the Top Position

Construction and infrastructure owners commanded 32.30% revenue share in 2025 because governments require more frequent inspections of bridges, roads, and tunnels. Drones cut lane-closure times, slash labor exposure at height, and capture richer data, enabling project managers to detect defects before they escalate. With most large contractors now embedding as-built drone scans into Building Information Modeling workflows, service providers secure multi-year framework agreements that stabilize income. Public-private partnerships drive further uptake as concessionaires must prove asset integrity to lenders and regulators, reinforcing drones as a standard line item in maintenance budgets.

Healthcare and parcel delivery, while smaller today, are racing ahead at a 29.35% CAGR and will diversify the Europe drone services market size through 2031. Wing’s NHS blood-sample corridor in London validated two-minute urban flights, prompting hospitals in Germany and the Netherlands to budget similar services for pathology, pharmacy, and organ transport. E-commerce platforms pursue same-day delivery in congestion zones where diesel vans incur rising low-emission penalties, turning lightweight BVLOS drones into an economic necessity. This dual momentum across health and retail buffers providers against cyclical slowdowns in construction activity and supports recurring-revenue business models.

By Drone Type: Rotary-Wing Prevalence and VTOL Surge

Rotary-wing craft accounted for 67.23% of the Europe drone services market size in 2025 because their hovering ability lets inspectors linger centimetres from blades, girders, and cables. Payload flexibility permits rapid swaps between RGB, thermal, and LiDAR sensors, enabling one aircraft to service multiple job types daily. Utilities favor rotors for tight right-of-way corridors where fixed-wing glide paths are infeasible, while public-safety agencies value the stable platform during casualty winch or loudspeaker missions. Mature supply chains and falling battery prices keep operating costs predictable, reinforcing rotary systems as the workhorse of the sector.

Hybrid VTOL aircraft post the fastest 29.96% CAGR as firms demand vertical lift and 100-km range in a single frame. Quantum-Systems’ Vector family and Avy’s autonomous box solution lift off in car-park footprints, transition to wing-borne cruise, and land back on the same pad, doubling daily coverage without runway infrastructure. These aircraft unlock BVLOS corridor inspections, offshore wind scouting, and inter-island medical supply routes that rotary fleets cannot serve economically. As sensor miniaturization continues, VTOL payload capacity rises, allowing providers to retire certain fixed-wing models and streamline maintenance inventories.

By Operating Range: BVLOS Uptake Gains Pace

Visual line-of-sight (VLOS) missions retained 76.20% share because they avoid complex Specific Operations Risk Assessments and carry lower insurance deductibles. Small-to-medium enterprises book VLOS flights for real-estate marketing, roof surveys, and event security, where pilots stay within 500 m of the drone. Quick mobilization appeals to price-sensitive clients, and national regulators process VLOS notifications in hours rather than weeks, keeping barriers to entry modest for new operators. These attributes ensure VLOS activity will continue to underpin baseline volumes across the Europe drone services market.

BVLOS sorties, though smaller in count, expand 30.31% per year as infrastructure, logistics, and emergency-response agencies need corridor-length coverage. EASA’s Standard Scenarios now let crews file a one-page declaration for predefined low-risk profiles, trimming approval cycles and driving fresh investment in detect-and-avoid avionics. Providers that hold multi-country BVLOS certificates command premium day rates because few rivals can match their compliance footing. As underwriters collect more flight-safety data, insurance premiums are trending down, which will widen the pool of BVLOS-qualified operators and lift the Europe drone services market share for extended-range missions.

Geography Analysis

The United Kingdom led regional revenue with a 28.70% share in 2025. The Civil Aviation Authority’s sandbox program grants time-bound BVLOS approvals that attract global payload integrators, creating a dense supplier ecosystem. Hospitals, energy majors, and transport agencies now embed drones in daily workflows rather than pilots. The UK also hosts advanced detect-and-avoid trials that feed EU-wide standards, strengthening its influence in the Europe drone services market.

Spain records the fastest 29.31% CAGR through 2031, propelled by public funding for urban-air-mobility corridors and agriculture modernization. Government tenders subsidize pesticide-reduction spraying, offering guaranteed hours to service operators and derisking hardware purchases. High tourist inflows spur authorities to monitor coastlines and heritage sites with unmanned patrols, further enlarging local demand. These programs amplify Spain’s contribution to the Europe drone services market and encourage foreign providers to establish Iberian hubs.

Germany and France remain sizeable markets supported by automotive, chemical, and energy industrial inspection. German turbine owners schedule drone checks during short weather windows, valuing consistent imagery that improves blade-repair planning. France tightens data-security rules, lengthening approval cycles but rewarding operators with cybersecurity credentials. Nordic nations embrace unmanned flights in sub-zero climates and defense scenarios, while the Netherlands pioneers automated depots for last-mile parcels. Collectively, these geographies diversify the Europe drone services market and mitigate single-country risk for pan-European providers.

Competitive Landscape

Competition remains moderate-to-high, with dozens of niche specialists balanced by a handful of scale platforms. Cyberhawk, Sky-Futures, and Terra Drone anchor the upper tier through integrated software and cross-border operating certificates. Their platforms ingest visual, thermal, and LiDAR feeds and export actionable insights into asset-management suites. Mid-tier players focus on vertical niches, such as Mainblades’ aircraft-skin inspection service, which cuts turnaround time for airlines.

Strategic partnerships accelerate market entry without heavy capital outlays. Kier Group’s alliance with DroneDeploy layers automated mapping on top of construction schedules, demonstrating a template that other contractors now copy. Software differentiation centers on AI-powered defect recognition, which lowers analytic labor and widens margins. SkyeBrowse trimmed 3D-model processing times by 40%, letting responders capture situational awareness within minutes.

Firms with robust safety logs negotiate better rates, pricing out smaller rivals. Investors favor businesses with proprietary data sets and can transition to recurring-revenue analytics. Over the forecast period, the Europe drone services market will likely see mergers that blend hardware OEMs with service operations, mirroring trends in manned aviation maintenance.

Europe Drone Services Industry Leaders

Cyberhawk Innovations Limited

Sky Futures Partners Limited

DroneDeploy, Inc.

Terra Drone Corporation

Aerodyne Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The UK Civil Aviation Authority (CAA) has approved the first beyond visual line of sight (BVLOS) drone flights over Critical National Infrastructure, with Drone Major conducting initial inspections. The CAA plans to enable routine drone inspections by 2027, targeting sectors like energy, utilities, defense, and border management to enhance efficiency and reduce costs.

- June 2025: Skymantics, a leader in geospatial AI and multimodal logistics, will showcase its advanced drone logistics software at IAM Madrid – Expodrónica 2025. Developed under the WINGWAY II project, supported by Spain’s Ministry of Industry, the platform enhances operational planning, regulatory compliance, and risk management by integrating Unmanned Aerial Systems (UAS) into logistics workflows.

- April 2024: Skyports secured USD 110 million Series C funding to expand drone ports across Europe.

Europe Drone Services Market Report Scope

The European drone services market encompasses the market for drone-based services in various commercial and civilian applications in the European region. The market offers an overview of the developments in the drone services industry in the region. The European drone services market is segmented by application into construction, agriculture, energy, law enforcement, medical and parcel delivery, and other applications. The other applications segment includes the usage of drone services for applications such as entertainment, insurance, and mining. The report also offers the market size of and forecasts for the drone services market in major countries in the European region. For each segment, the market size and forecasts are represented in value (USD billion).

By Service Type

| Drone Platform Services | Piloting and Operations |

| Data Analytics | |

| Data Processing | |

| Maintenance, Repair and Overhaul (MRO) | |

| Training and Simulation |

By End User Industry

| Construction and Infrastructure |

| Agriculture and Forestry |

| Energy and Utilities |

| Law Enforcement and Public Safety |

| Medical and Parcel Delivery |

| Others (Mining, Real-estate, Media) |

By Drone Type

| Rotary-wing |

| Fixed-wing |

| Hybrid VTOL |

By Operating Range

| Visual Line-of-Sight (VLOS) |

| Beyond Visual Line-of-Sight (BVLOS) |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Netherlands |

| Nordic Countries |

| Rest of Europe |

| By Service Type | Drone Platform Services | Piloting and Operations |

| Data Analytics | ||

| Data Processing | ||

| Maintenance, Repair and Overhaul (MRO) | ||

| Training and Simulation | ||

| By End User Industry | Construction and Infrastructure | |

| Agriculture and Forestry | ||

| Energy and Utilities | ||

| Law Enforcement and Public Safety | ||

| Medical and Parcel Delivery | ||

| Others (Mining, Real-estate, Media) | ||

| By Drone Type | Rotary-wing | |

| Fixed-wing | ||

| Hybrid VTOL | ||

| By Operating Range | Visual Line-of-Sight (VLOS) | |

| Beyond Visual Line-of-Sight (BVLOS) | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Nordic Countries | ||

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe drone services market?

The market is valued at USD 10.95 billion in 2026 and is set to reach USD 32.71 billion by 2031, recording a 24.45% CAGR.

Which end-user industry generates the most demand?

Construction and infrastructure accounts for 32.30% of 2025 revenue because drones cut inspection time and improve safety.

How fast is BVLOS activity growing?

BVLOS services are expanding at a 30.31% CAGR thanks to EASA Standard Scenarios that streamline approvals.

Why are hybrid VTOL drones gaining popularity?

Hybrid VTOL platforms offer both hover precision and long-range cruise, driving a 29.96% CAGR in their segment.

Which country leads the region?

The United Kingdom holds 28.70% market share due to early regulatory sandboxes and strong healthcare and energy demand.

What limits market expansion in the near term?

Complex BVLOS certification and a shortage of qualified pilots remain the primary bottlenecks despite notable training-sector growth.

Page last updated on: