Dominican Republic Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

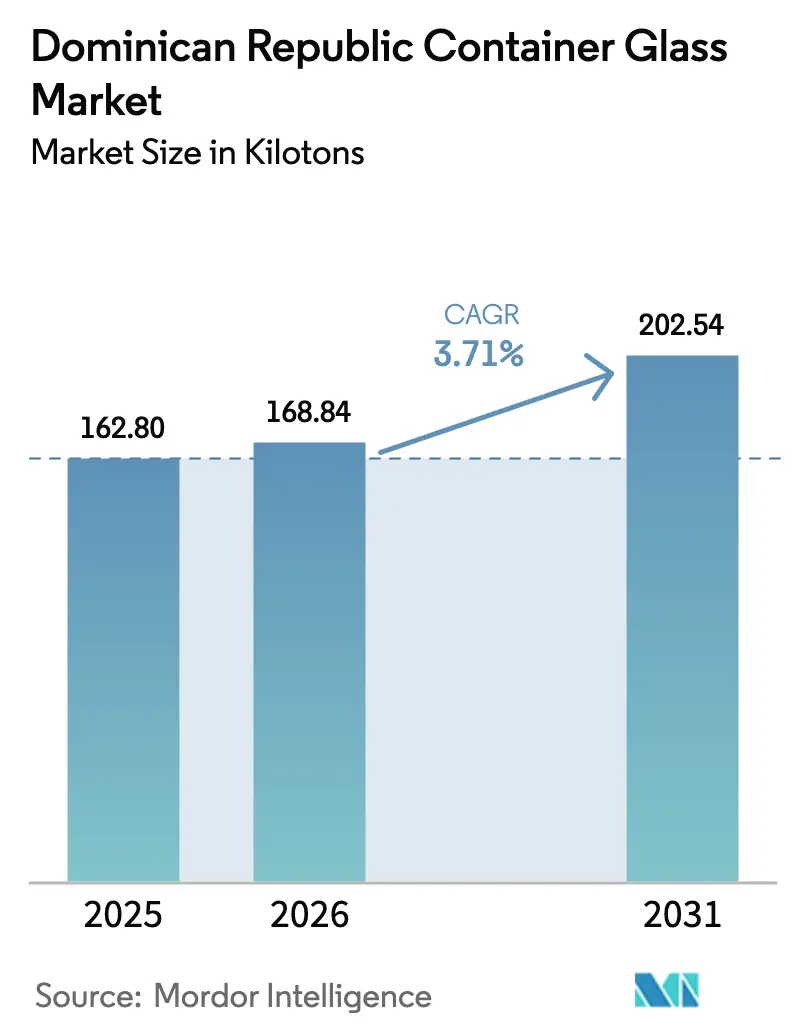

| Base Year Market Size (2025) | 162.8 kilotons |

| Market Volume (2026) | 168.84 kilotons |

| Market Volume (2031) | 202.54 kilotons |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

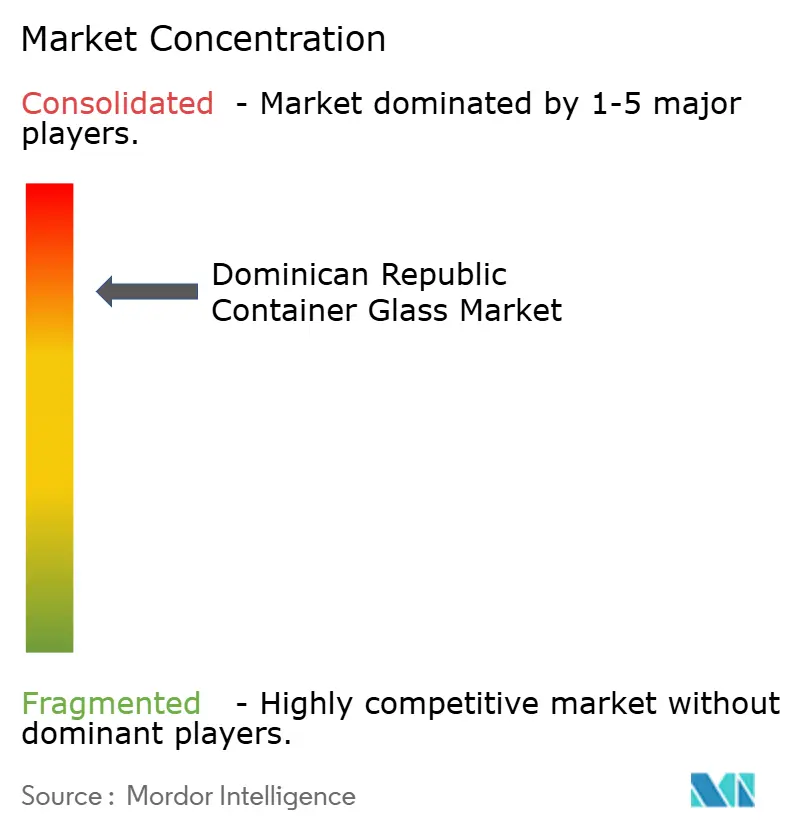

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dominican Republic Container Glass Market Analysis by Mordor Intelligence

Dominican Republic container glass market size in 2026 is estimated at 168.84 kilotons, growing from 2025 value of 162.8 kilotons with 2031 projections showing 202.54 kilotons, growing at 3.71% CAGR over 2026-2031. Accelerating demand is driven by converging sustainability mandates, beverage premiumization, and a resilient tourism sector that attracts more than 10 million international arrivals annually. Investing in returnable bottle logistics enhances cullet availability, reducing furnace energy intensity and promoting cost competitiveness. Meanwhile, premium rum, craft beer, and export-oriented cosmetics lines increasingly specify high-quality glass to signal provenance and product safety. Electricity sector reforms, trade-zone industrial expansion, and near-shoring of agri-processing collectively underpin long-term growth fundamentals, even as energy price volatility, currency swings, and skilled-labor shortages pose near-term headwinds to furnaces operating at full utilization.

Key Report Takeaways

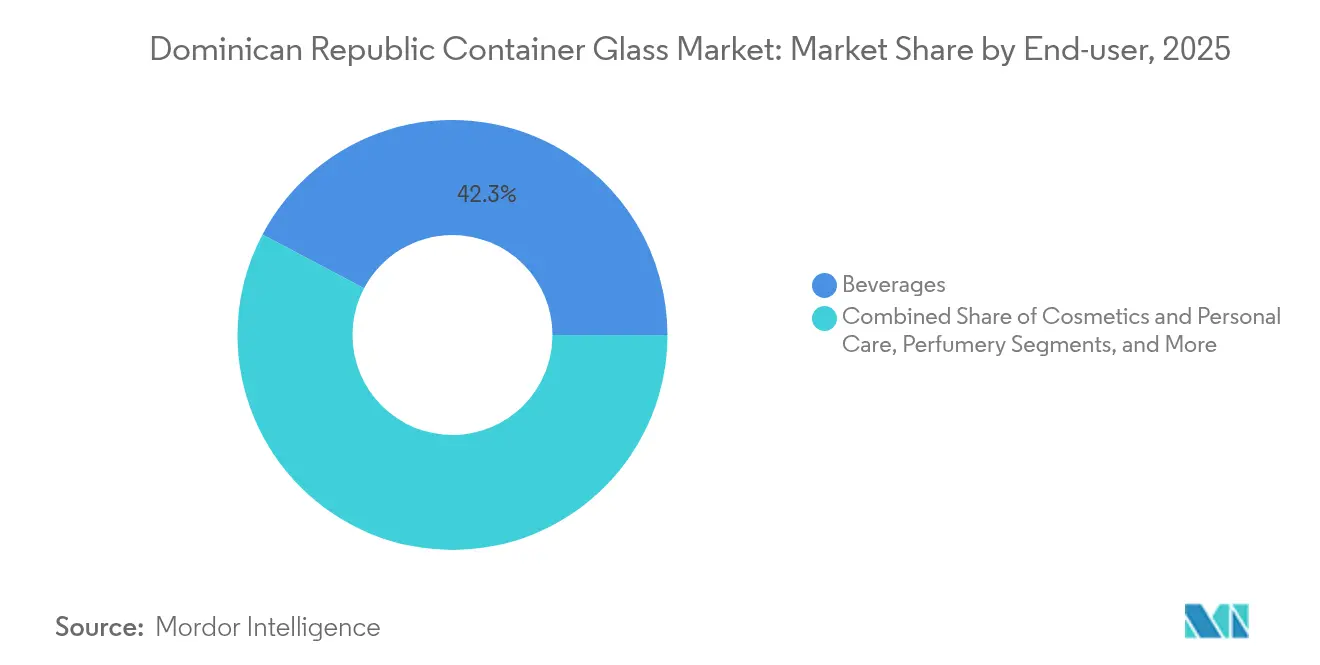

- By end-user, beverages captured 42.25% of the Dominican Republic container glass market share in 2025.

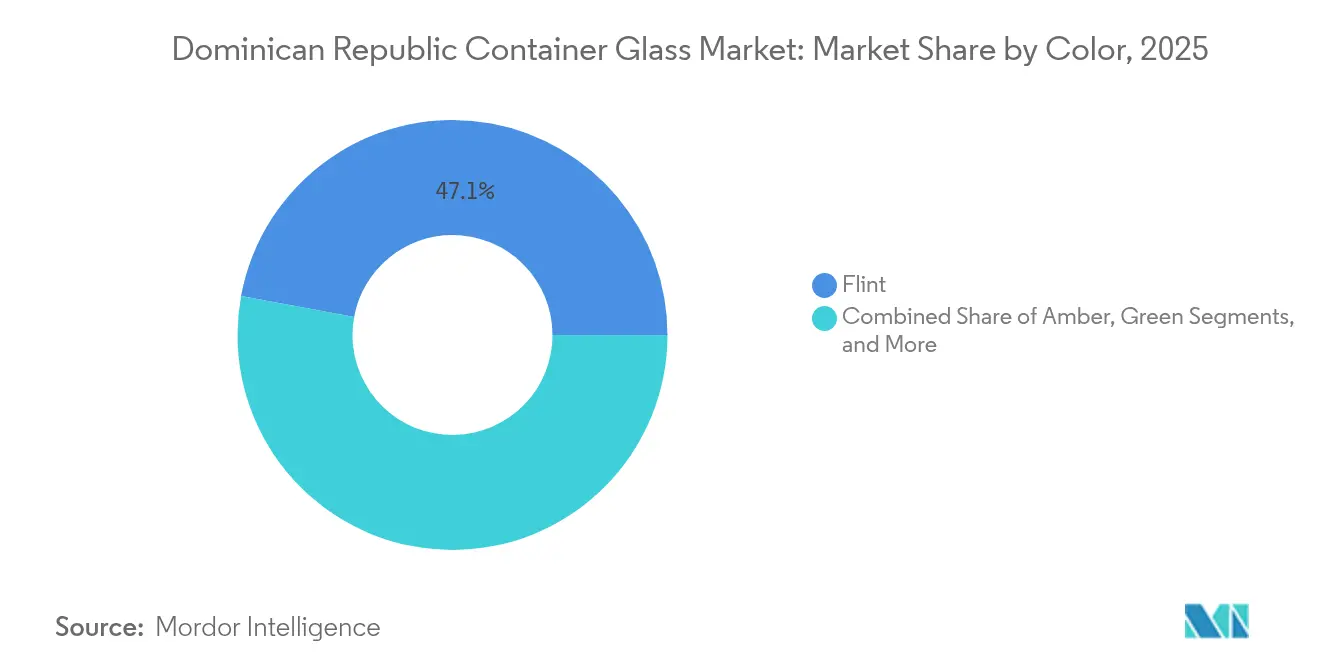

- By color, the Dominican Republic container glass market for amber glass is projected to grow at a 5.86% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Dominican Republic Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of sustainable packaging | +1.2% | Global, with early gains in Santo Domingo and Santiago | Medium term (2-4 years) |

| Food and beverage premiumization wave | +0.8% | North America and Caribbean export markets | Short term (≤ 2 years) |

| Return-bottle logistics cost advantage | +0.6% | Dominican Republic domestic market | Long term (≥ 4 years) |

| Government push for circular economy | +0.4% | National, guided by Ministry of Environment policy | Medium term (2-4 years) |

| Beer export-hub strategy of AB InBev | +0.5% | Caribbean and Americas export corridors | Medium term (2-4 years) |

| Tourism-led demand for craft spirits | +0.3% | Tourist zones: Punta Cana, Puerto Plata, Santo Domingo | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising popularity of sustainable packaging

Glass enjoys a favorable environmental perception, with 92% of United States consumers rating it positively for sustainability. Tourists arriving in Punta Cana and Santo Domingo bring similar expectations, prompting resort operators to favor returnable or high-recycled-content bottles on menus. AB InBev’s pledge to reach 100% returnable or majority-recycled packaging by 2025 directly influences Cervecería Nacional Dominicana's procurement policies and cultivates steady cullet demand. Local recyclers over 300 “Botelleros” operating nationwide recover 90% of bottles, trimming virgin raw-material needs and furnace energy loads by about 40% when cullet is substituted. Financing support from multilateral lenders adds momentum to closed-loop infrastructure build-out, making sustainability both a brand differentiator and a cost lever.

Food and beverage premiumisation wave

Rum, craft beer, and flavored malt beverages now position packaging as an extension of brand storytelling. Brugal’s Colección Visionaria rum, for example, features an amber bottle with a matte gradient and gold screen-print, conveying heritage and exclusivity.[1]Appartement 103, “Brugal Colección Visionaria – Packaging of the World,” packagingoftheworld.com In parallel, Dominican hair-care exports expanded by 66% between 2014-2020, and premium glass jars and flacons help manufacturers comply with stringent U.S. shelf-appeal and recyclability benchmarks. Higher-margin SKUs enable bottlers to absorb the fuel surcharge embedded in domestic electricity tariffs, thereby sustaining production volumes despite elevated input costs. The premium trade-down risk remains limited thanks to tourism-driven spending and an expanding middle class that values aspirational brands.

Return-bottle logistics cost advantage

Cervecería Nacional Dominicana’s closed-loop system recovers 90% of bottles through its nationwide network, proving the economic viability of circular glass in an island context. Reusing bottles up to 25 cycles reduces the per-unit container cost and lowers the total landed cost compared to single-use glass or plastic. Energy savings achieved through cullet melt offset roughly 15% of furnace gas demand at peak production. IDB Invest has begun replicating the model regionally, suggesting future cross-border cullet flows that could raise furnace utilization while reducing the carbon footprint. Scale economies arising from standardized bottle designs further compress logistics costs for route-to-market partners.

Government push for circular economy

Law 225-20 promotes extended producer responsibility and targets a 25% reduction in greenhouse-gas emissions by 2030, directly incentivizing glass recycling and recovery programs. The Ministry of Environment coordinates with municipal waste operators on segregated glass collection, while a USD 750 million green-bond program launched in 2024 earmarks funds for new cullet processing lines. Public-private task forces analyze tax incentives to stimulate furnace upgrades toward oxy-fuel and electric melter hybrids that dovetail with solar-intensive grids. As regulatory clarity improves, bottlers gain the policy certainty needed for long-dated capital commitments, solidifying investment pipelines and strengthening supply security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy and fuel costs | -1.8% | National, with acute impact in industrial zones | Short term (≤ 2 years) |

| Currency volatility and imported inputs | -1.2% | National, affecting import-dependent firms | Medium term (2-4 years) |

| Plastics tax-credit uncertainty | -0.6% | National regulatory environment | Medium term (2-4 years) |

| Shortage of skilled furnace operators | -0.4% | Industrial manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High energy and fuel costs

Industrial electricity averages USD 0.16 per kWh, ranking among the highest in the Caribbean and eroding margins for energy-intensive melts. Natural-gas import prices fluctuated between USD 4.80 and USD 33.52 per 1,000 cubic feet in 2024, making fuel budgeting unpredictable. Electricity distribution losses exceeding 36% compel utilities to pass inefficiencies on to heavy users, and tariff hikes tied to sector reform could precede service-quality improvements. Combined, these factors push manufacturers to adopt variable-speed drives, oxy-fuel burners, and batch pre-heaters to pare kWh per melted ton. Some operators hedge by installing rooftop solar arrays that cover up to 20% of their daytime load, yet base-furnace fire remains gas-reliant until proven hybrid models are scaled.

Currency volatility and imported inputs

The Dominican peso’s swings against the U.S. dollar heighten raw-material cost uncertainty, notably for soda ash, specialty coatings, and refractory bricks, which are priced in foreign currency. Freight rates out of China escalated from USD 1,500 to almost USD 13,000 per container at their 2024 peak, inflating inbound costs for molds and inspection equipment. Manufacturers with limited forward-currency cover absorb translation losses that compress working-capital buffers. Export-led bottlers pass some variance through pricing in U.S. dollars, but domestic-focused firms face a thinner margin cushion, amplifying supply-chain risk whenever the peso depreciates rapidly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: beverages dominate while cosmetics accelerate growth

Beverages retained 42.25% of the Dominican Republic container glass market share in 2025, reflecting strong beer and rum consumption anchored by Cervecería Nacional Dominicana’s multi-brew portfolio and AB InBev’s export logistics. Within the alcohol industry, returnable flint bottles are reused 25 times, optimizing glass throughput and reducing tonnage. Non-alcoholic drinks, such as juices, low-sugar sodas, and functional beverages, also utilize tap formats to align with wellness positioning in resort hospitality outlets.

Cosmetics and personal care, although smaller in absolute terms, post the fastest 5.59% CAGR to 2031, driven by export-oriented hair-care and skin-care brands that emphasize premium glass jars for enhanced shelf appeal. Producers leverage the Dominican Republic's container glass market size, advantages, short lead times, bilingual regulatory compliance, and favorable CAFTA-DR tariffs to ship to more than 40 destinations, primarily on the U.S. eastern seaboard. The food, pharmaceutical, and niche perfumery segments round out the demand stack, each benefiting from the traceability and tamper-evident properties associated with glass.

By Color: flint holds scale leadership while amber wins on premium cues

Flint glass accounted for 47.10% of the Dominican Republic's container glass market size in 2025, driven by high-volume beer and soft-drink bottlings that prioritize product visibility, standardization, and low unit costs. Flint’s compatibility with returnable pool circulation ensures efficient cleaning-station turnarounds and a low risk of contamination.

Amber glass grows at a 5.86% CAGR, lifted by premium rum producers seeking ultraviolet protection and distinctive brand aesthetics. Finishing techniques such as gradient coatings, embossing, and applied ceramic labeling command higher margins that offset the extra costs of colorants. Green glass services wine and artisanal spirit niches, while cobalt and specialty colors address limited-edition launches where brand differentiation justifies shorter production runs.

Geography Analysis

The Dominican Republic's container glass market benefits from its position as the largest economy in the Caribbean, with a USD 121.4 billion GDP and a 14.9% manufacturing share in 2023. Growth in tourism receipts fuels demand for packaging in resort corridors, where import-substituting beverages and cosmetics anchor local supply chains. Free-trade zones accounted for USD 7.8 billion in exports during 2022, and each new assembly plant adds incremental volumes of bottles and jars for products sold to Central America and the United States.

Regional trade dynamics connect domestic furnaces with Trinidad’s Carib Glass and Costa Rica’s VICESA, shaping a networked supply base that balances seasonal demand surges. CAFTA-DR grants duty-free access to U.S. ports, allowing Dominican producers to backfill short runs for stateside craft brands that cannot meet minimum domestic batch sizes. Meanwhile, port modernization under the “Release in 24 Hours” customs program cuts dwell time, a crucial factor when heavy containers accrue demurrage costs at twice the rate of palletized freight.

Near-shoring of agri-processing, medical devices, and specialty foods is projected to add up to 8.3 million ft² of industrial real estate, creating downstream packaging demand estimated at USD 100 million. Electricity-sector reform targets 400 MW of rooftop solar potential at industrial parks, an initiative that, if realized, would reduce the cost of glass melting energy over the forecast horizon.

Competitive Landscape

Domestic manufacturing is moderately concentrated around Caribbean Glass Industry S.A., whose Pedro Brand facility can produce 500 million bottles annually under six-year offtake agreements that secure roughly 70% of Cervecería Nacional Dominicana orders. The supply-side set-up locks in furnace utilization rates while allowing incremental export cargoes to Puerto Rico and Haiti during the off-season.

AB InBev’s 97% control of CND, finalized in January 2024 for USD 0.3 billion, consolidates procurement power and orients bottle specifications toward global returnability standards. Regional capacity additions by Carib Glass in Trinidad and VICESA in Costa Rica maintain competitive tension, especially for lightweight single-trip bottles required by boutique condiment and nutraceutical clients. Technology differentiation centers on circular platforms, such as ecoSPIRITS, whose San Pedro de Macorís ecoPLANT refills bulk vessels for the hospitality channel, thereby reducing single-use glass demand in bars that stock premium liquors.[3]ecoSPIRITS, “Pernod Ricard and ecoSPIRITS deepen partnership for circularity in spirits,” ecospirits.global

Despite a USD 13.3 million IDB Invest credit line, the ZZ Glass start-up has yet to break ground, highlighting barriers posed by capital intensity, feedstock security, and skilled labor shortages. As a result, incumbent players retain bargaining leverage; however, policy incentives for solar-powered electric melting could lower entry thresholds and attract new investors over the long term.

Dominican Republic Container Glass Industry Leaders

Caribbean Glass Industry S.A.

Feemio Group Co., Ltd.

Almacenes Carballo

ALPLA Caribe, Inc.

Saverglass SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: IFC’s Country Private Sector Diagnostic outlined USD 100 million in agri-logistics packaging opportunities tied to near-shoring.

- September 2024: IMF Article IV report underscored electricity-sector reform urgency, affecting cost competitiveness of energy-intensive glass furnaces.

- August 2024: Dominican government enacted a Fiscal Responsibility Law that preserves green-bond funding for circular-economy infrastructure, including cullet processing lines.

- June 2024: Central Bank data confirmed construction sector growth of 12.2%, buoying architectural and container glass prospects.

Dominican Republic Container Glass Market Report Scope

Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. It is often chosen for products where purity, safety, and environmental sustainability are paramount concerns.

Dominican Republic container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large will the Dominican Republic container glass market be by 2031?

It is projected to reach 202.54 kilotons by 2031, expanding at a 3.71% CAGR.

Which segment is growing fastest in volume terms?

Cosmetics and personal care containers post the highest 5.59% CAGR through 2031, buoyed by export sales to over 40 countries.

What driver most benefits producers today?

The rise of sustainable packaging, backed by 90% bottle-return rates and new cullet plants, lowers raw-material use and boosts furnace efficiency.

Why are energy costs a concern for glass makers?

Industrial electricity averages USD 0.16 per kWh and gas imports swing widely, affecting an energy-intensive melting process that represents up to 90% of plant emissions.

Which color segment shows the strongest growth?

Amber glass leads, growing at a 5.86% CAGR thanks to premium rum and craft spirits demanding light-protective bottles with upscale finishes.

How concentrated is industry ownership?

The top five firms hold about 70% of capacity, giving the market a moderate concentration score of 7.

Page last updated on: