Guatemala Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

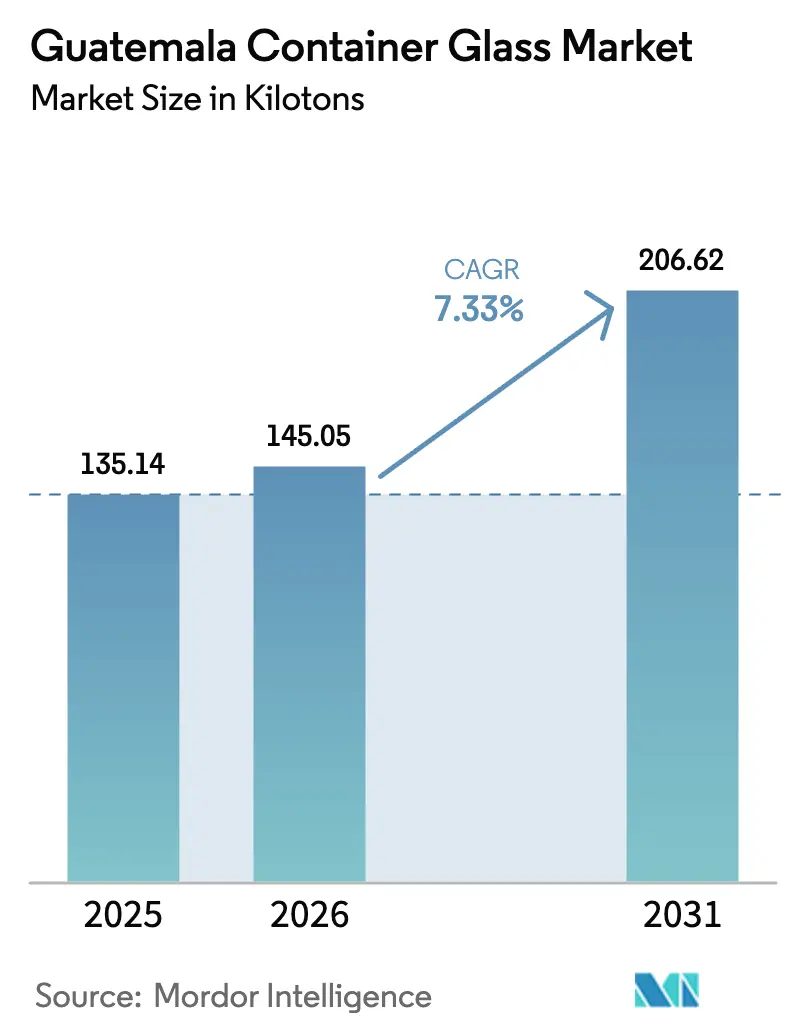

| Base Year Market Size (2025) | 135.14 kilotons |

| Market Volume (2026) | 145.05 kilotons |

| Market Volume (2031) | 206.62 kilotons |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

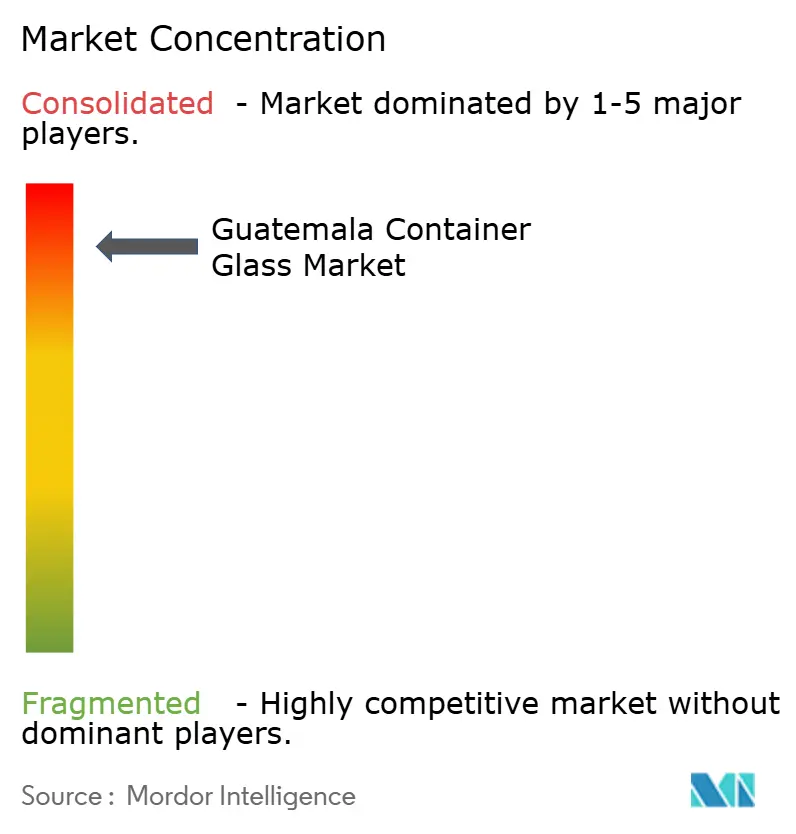

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Guatemala Container Glass Market Analysis by Mordor Intelligence

Guatemala container glass market size in 2026 is estimated at 145.05 kilotons, growing from 2025 value of 135.14 kilotons with 2031 projections showing 206.62 kilotons, growing at 7.33% CAGR over 2026-2031. Regulatory mandates on waste segregation, premiumization in beverages, and near-shoring of supply chains continue to underpin this expansion. Beverage brands are switching from PET and aluminum to glass for export-quality presentation, with Licores de Guatemala already shifting 30% of its output to glass bottles aimed at overseas buyers. Rising renewable-energy capacity adds a sustainability narrative; however, electricity prices remain elevated compared to those in Mexico and Costa Rica, creating cost pressures on furnace operations.[1]Christopher Hernandez-Roy, Andrea Casique, and Natalia Hidalgo, “Assessing Guatemala as a Nearshoring Destination,” Center for Strategic and International Studies, csis.org Persistent port congestion and a 63% on-time delivery failure rate are encouraging beverage producers to source containers domestically.

Key Report Takeaways

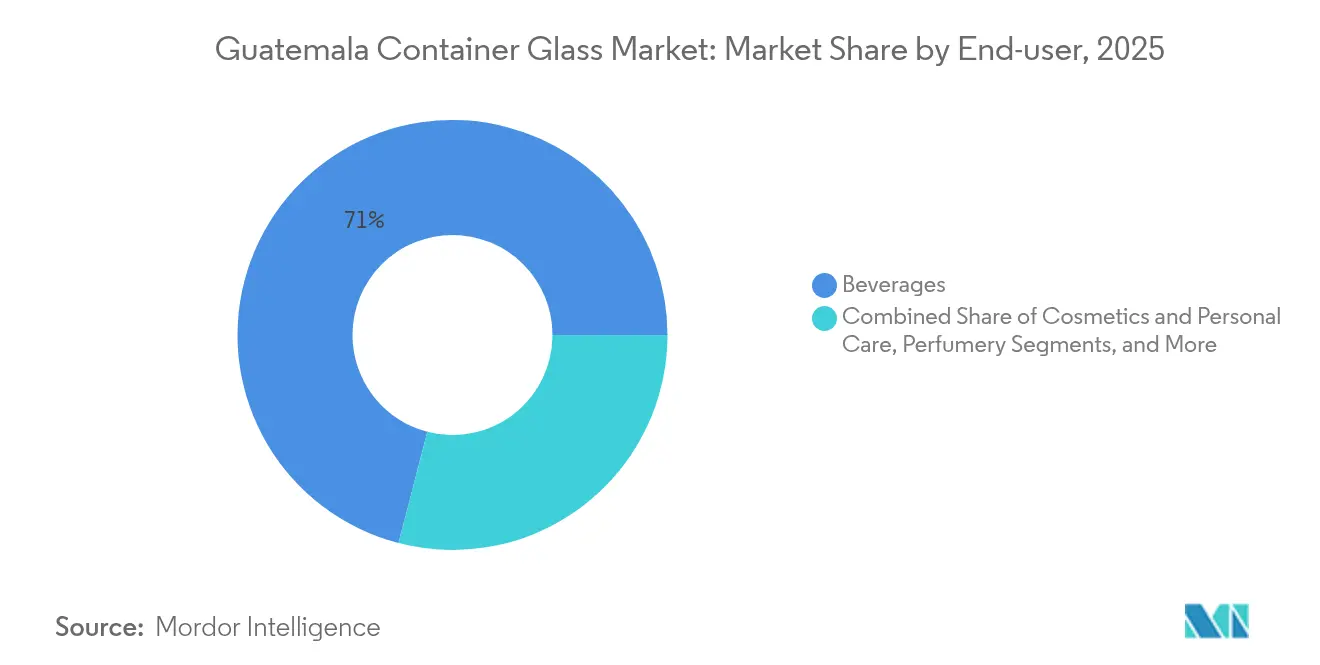

- By end-user, beverages captured 70.96% of the Guatemala container glass market share in 2025.

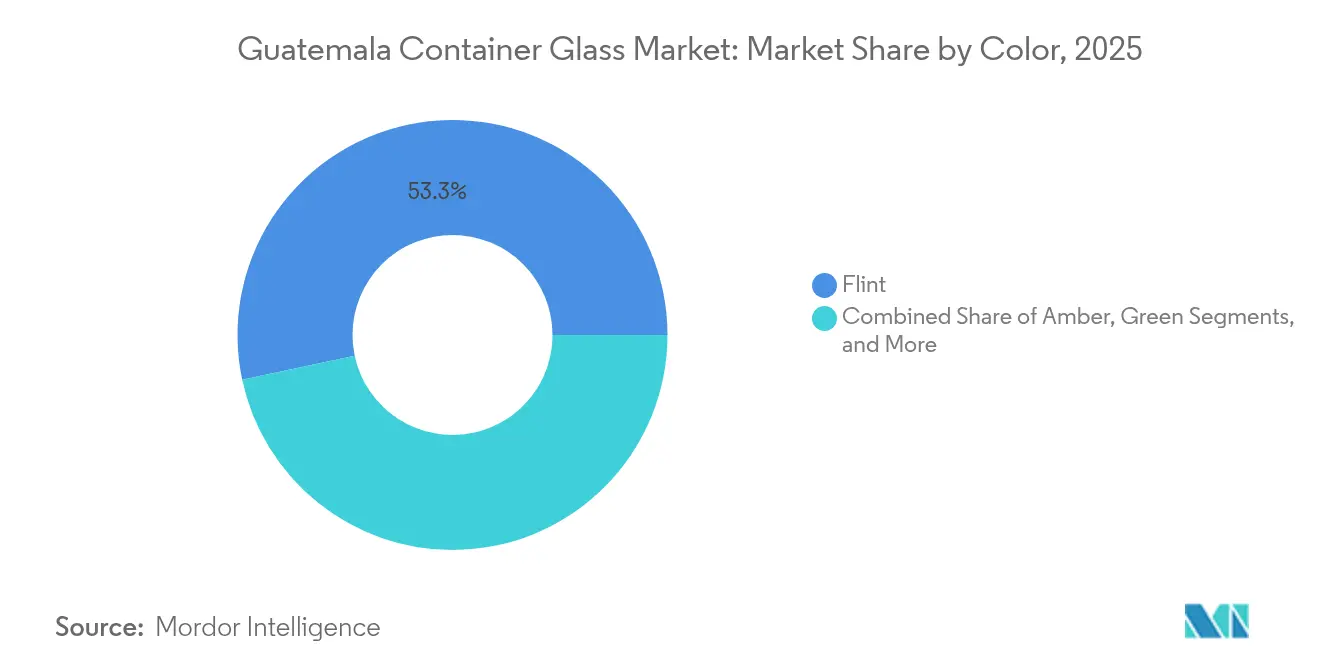

- By color, the Guatemala container glass market for amber glass is projected to grow at a 9.05% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Guatemala Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from beverage industry | +2.1% | National hubs, export corridors | Medium term (2-4 years) |

| Mandatory waste-sorting law boosts cullet supply | +1.8% | National rollout, phased municipal adoption | Long term (≥ 4 years) |

| Premium spirits and craft beers drive flint demand | +1.4% | Domestic production, international export markets | Medium term (2-4 years) |

| Port congestion makes local sourcing attractive | +0.9% | All import-dependent regions | Short term (≤ 2 years) |

| Light-weighting and returnable programs | +0.7% | Nationwide, led by large bottlers | Long term (≥ 4 years) |

| Regional FDI in glass capacity | +0.6% | Free-trade zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Beverage Industry

Guatemala’s beverage sector logged 192.8 million unit cases at Coca-Cola FEMSA in 2024, up 10.7% year-over-year, and retained a 35% share for returnable bottles.[2]Coca-Cola FEMSA, “20-F 2024,” coca-colafemsa.com Bottled-water volumes jumped 29.8%, signaling diversification into premium hydration lines that prefer glass to underscore purity. With beverages contributing USD 5.63 billion and generating 440,000 direct jobs, producers possess both the capital and motivation to upgrade their packaging. The sector’s export reach, facilitated by DR-CAFTA, keeps the Guatemala container glass market embedded in regional value chains. Domestic suppliers thus gain a steady pipeline of high-volume orders, anchoring furnace utilization rates above 85% across major plants.

Mandatory Waste-Sorting Law Boosts Cullet Supply

Acuerdo Gubernativo 164-2021 obligates households and businesses to segregate glass as a category of recyclables, effective as of February 2025. Municipal solid-waste generation of 0.519 kg per capita per day, collected at a rate of 71.3% by private firms, creates a ready feedstock for cullet processors. The measure lowers raw material costs by 12% for compliant manufacturers and incentivizes furnace operators to increase the recycled-glass content to 45% by 2027. Formalized collection contracts benefit larger recyclers, potentially consolidating the supply chain while meeting corporate ESG targets of beverage multinationals.

Premium Spirits and Craft Beers Driving Flint Demand

Ron Zacapa, Botran, and a growing craft-beer scene push demand for premium flint bottles that showcase clarity and color. Licores de Guatemala abandoned PET entirely for its export lines after a 2023 glass shortage, aligning its packaging with global luxury expectations and ESG goals. Exports represent 30% of corporate volume and enjoy tariff-free entry into the United States under DR-CAFTA, thereby sustaining long-term demand for flint consumption. Regional furnace expansions, such as Vitro’s USD 70 million upgrade in Toluca, create spillover supply for Guatemalan spirits bottlers.

Port Congestion Makes Local Sourcing More Attractive

Puerto Quetzal operates at 121% capacity and reports vessel waits of four hours, while Santo Tomás de Castilla faces similar gridlock, citing limited gate slots and chassis shortages, which push on-time delivery rates to just 37%. Beverage lines that run on just-in-time inventories are vulnerable to imported-container delays; therefore, redirecting orders to Vidriera Guatemalteca S.A. and Empresas Comegua S.A. Local sourcing trims lead times by three weeks and reduces demurrage costs by up to USD 210 per forty-foot equivalent unit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy prices for furnace operations | -1.6% | Nationwide | Medium term (2-4 years) |

| Growing PET and aluminum substitution | -1.2% | High-volume beverage categories | Long term (≥ 4 years) |

| Fragmented cullet-collection infrastructure | -0.8% | Rural areas | Long term (≥ 4 years) |

| Limited domestic market scale for specialties | -0.5% | Niche segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy Prices for Furnace Operations

Although renewables account for 71% of Guatemala’s electricity mix, industrial tariffs average USD 0.145 per kWh, roughly 18% higher than Mexico’s rates. Glass melting demands uninterrupted high-temperature processes, making energy around 30% of the cost of goods. Planned hydropower additions of 3,700 MW through 2040 promise future relief, but community opposition and long permitting cycles delay commissioning. Manufacturers thus hedge their risks with long-term power purchase agreements and invest in oxy-fuel furnaces that reduce gas consumption by 12%, yet require a steep upfront capital investment.

Growing PET and Aluminum Substitution

Ball Corporation’s joint venture with Envases Universales maintains a robust can-making footprint in Guatemala, producing lighter, resealable options that compete directly with glass. Coca-Cola FEMSA operates its PET lines at 96.4% utilization, reflecting capacity tightness that could influence further investment in plastics. For mass-market sodas retailing below USD 0.60 per liter, PET bottles reduce logistics costs by 28% compared to glass, challenging volume growth in price-sensitive segments. Nonetheless, ESG mandates and premium branding offset some substitution risk by reaffirming glass’s recyclability and perceived quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Volume Growth

The beverages segment represented 70.96% of the Guatemala container glass market share in 2025. It captured momentum from sparkling-soft drink volumes, which rose 10.7% year over year, and from premium spirits that are migrating their packaging from PET to flint. Coca-Cola FEMSA’s reliance on returnable bottles stabilizes baseline demand because every glass cycle extends the container's lifespan by an estimated 35 turns, preserving value for both the filler and the producer. Food packaging ranks second, driven by export-oriented sauces and processed fruits that utilize glass for both shelf appeal and regulatory compliance in North America.

The fastest-growing segment is cosmetics and personal care at a 9.48% CAGR through 2031. Rising disposable incomes and social-media influence drive premium skincare launches that favor small-format flint bottles with droppers or atomizers. Pharmaceuticals and perfumery follow a steady trajectory, leveraging amber vials for UV-sensitive formulations. Environmental approvals from the Ministry of Environment and Natural Resources (MARN) guarantee compliance for medical-grade containers, boosting domestic credibility among multinational healthcare clients. Collectively, these niches diversify the revenue base and reduce dependence on beverage cycles for the Guatemala container glass market.

By Color: Flint Dominance with Amber Growth

Flint glass secured 53.33% of demand in 2025, mirroring the prominence of premium spirits and clear-label soft drinks that rely on translucence to communicate purity. The Guatemala container glass market size for flint bottles reached 72.07 kilotons in 2025 and is projected to expand at a 6.66% CAGR through 2031, driven by export compliance and brand storytelling. Local furnaces calibrate silica content to achieve iron levels of less than 1.5 ppm, meeting U.S. and EU transparency thresholds.

Amber glass is the fastest-growing color segment, with a 9.05% CAGR, driven by pharmaceutical adoption and the craft-beer renaissance's demand for UV protection. Industry players blend amber cullet at 25% ratios, benefiting from the waste-sorting regulation that prevents color contamination. Green and specialty colors remain stable, supporting wine, olive oil, and high-end cosmetics niches. Vitro’s newly commissioned 230 tonnes-per-day furnace designates one production line exclusively for cosmetics, amber, and flint, aligning regional capacity with evolving color mixes.

Geography Analysis

Guatemala anchors the Central American packaging corridor, aided by 3-day sail times to Miami and dual-coast access. The Guatemala container glass market size in the domestic geography is forecast to grow at a 7.31% CAGR, supported by USD 1.55 billion in manufacturing FDI realized in 2023, of which 15.7% targeted industrial projects. Free-trade zones grant 10-year income-tax holidays and duty-exempt machinery imports, incentivizing furnace upgrades and batch-house automation.

The customs union spanning Guatemala, Honduras, and El Salvador creates a 34.8 million-person consumer base, simplifying regional distribution for container producers. However, alcoholic beverages fall outside simplified transit rules, requiring separate customs declarations that elongate lead times by up to 72 hours. Ongoing CA-9 corridor improvements financed by a USD 175 million IDB loan promise to shave 18% off inland trucking costs once operational.

Infrastructure constraints remain material. Puerto Quetzal’s USD 1 billion master plan aims to attract private partners to expand capacity beyond 340,000 TEU, yet progress is incremental. In the meantime, manufacturers hedge risk with inventory buffers equivalent to 35 days of finished goods supply. Renewable-energy projects clustered near the western highlands aim to lower power costs, though grid bottlenecks limit immediate impact. These dynamics collectively shape freight, energy, and compliance inputs in the Guatemala container glass market.

Competitive Landscape

The market shows moderate concentration. Vidriera Guatemalteca S.A. operates the main domestic furnace, while O-I holds almost 50% ownership of Empresas Comegua S.A., channeling global technical know-how into local operations. Combined, the top five suppliers account for roughly 68% of the output, indicating room for niche entrants but providing incumbents with scale advantages in energy procurement and cullet contracts. Recent bankable deals include IDB Invest’s USD 50 million financing to packaging distributor Laki, which bolsters regional supply chains, highlighting lender confidence in the sector.

Strategic moves center on furnace modernization, returnable-bottle pools, and light-weighting. Vidriera Guatemalteca piloted a narrow-neck press-and-blow line, cutting container weight by 15% without compromising strength, thereby lowering per-unit gas consumption. Meanwhile, Ball-Envases Universales escalates aluminum-can production, upping negotiation pressure on glass makers to retain beverage contracts. Regulatory oversight is tightening: the new Competition Superintendency created in 2024 will enforce antitrust rules from 2027, potentially curbing exclusive supply agreements that limit smaller firms’ access to cullet streams.

Emerging white spaces exist in the cosmetics, pharmaceutical vials, and specialty food sectors, where domestic output is limited. Firms exploring these niches weigh smaller batch sizes against higher margins and may leverage ZDEEP incentives for pilot plants. Access to low-interest development financing and technology transfers from Mexico’s glass hub positions Guatemala as a feasible micro-regional cluster for specialty production.

Guatemala Container Glass Industry Leaders

Vidriera Guatemalteca, S.A.

Feemio Group Co., Ltd.

Changsha Kotto Glass Industrial Co Ltd

New High Glass Guatemala S.A.

LSS Africa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IDB Invest approved up to USD 50 million financing for Laki to strengthen packaging supply chains across Guatemala, El Salvador, and Honduras.

- February 2025: Vitro commissioned its USD 70 million Furnace in Toluca, adding 230 tonnes per day of capacity, targeting spirits and cosmetics customers.

- February 2025: Mandatory secondary waste classification, as outlined in Acuerdo Gubernativo 164-2021, took effect, requiring the nationwide separation of glass sources.

- January 2025: Guatemala attracted USD 1.69 billion in FDI for 2024, with 15.7% funneled into manufacturing, bolstering packaging-sector prospects.

Guatemala Container Glass Market Report Scope

Glass containers are vessels made from glass used to store and protect products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. Available in diverse shapes and sizes, such as bottles, jars, and vials, these containers provide airtight seals and protect contents from external contaminants. Glass packaging is valued for its non-reactive nature, preservation of product quality, and high recyclability. These attributes make glass containers a preferred choice for packaging across multiple industries.

Guatemala container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the 2026 market size and growth outlook for Guatemala container glass?

The Guatemala container glass market size is 145.05 kilotons in 2026 and is projected to grow 7.33% CAGR to 206.62 kilotons by 2031.

Which end-user segment consumes the most glass containers in Guatemala?

Beverages account for 70.96% of demand, driven by soft-drink volumes and premium spirits.

How does the waste-sorting law affect glass-container producers?

High industrial electricity tariffs and substitution pressure from PET bottles and aluminum cans constrain competitiveness.

Why are beverage companies favoring local sourcing of glass?

Chronic port congestion and 63% on-time failure rates for imports make local supply more reliable and cost effective.

Which color segment is growing fastest through 2031?

Amber glass leads growth with a 9.05% CAGR, supported by pharmaceuticals and craft beer applications.

Page last updated on: