Defense Gyroscope Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

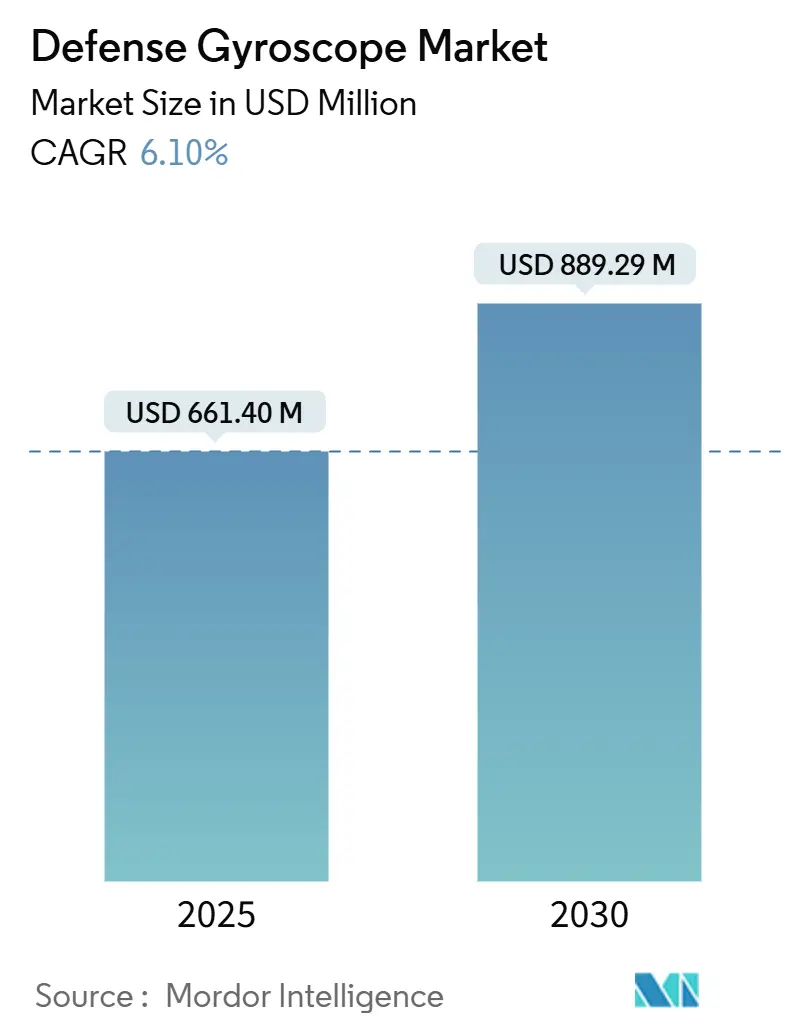

| Market Size (2025) | USD 661.40 Million |

| Market Size (2030) | USD 889.29 Million |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Defense Gyroscope Market Analysis by Mordor Intelligence

The defense gyroscope market size is USD 661.4 million in 2025 and is forecasted to reach USD 889.29 million by 2030, advancing at a 6.10% CAGR. Demand is anchored in defense-modernization programs, unmanned-platform proliferation, and continued migration from mechanical to micro-electromechanical systems (MEMS), fiber-optic, and nascent quantum technologies. Procurement agencies prioritize solutions that combine tactical- to navigation-grade accuracy with improved size, weight, power, and cost (SWaP-C) metrics, creating sustained momentum for MEMS and photonic designs. North America, backed by the world’s largest defense budget, currently leads the defense gyroscope market, while Asia-Pacific delivers the fastest expansion as regional powers fund indigenous capability development. Competitive strategies revolve around vertical integration, quantum research partnerships, and supply-chain resilience initiatives to secure critical polarization-maintaining fibers and other specialty inputs.

Key Report Takeaways

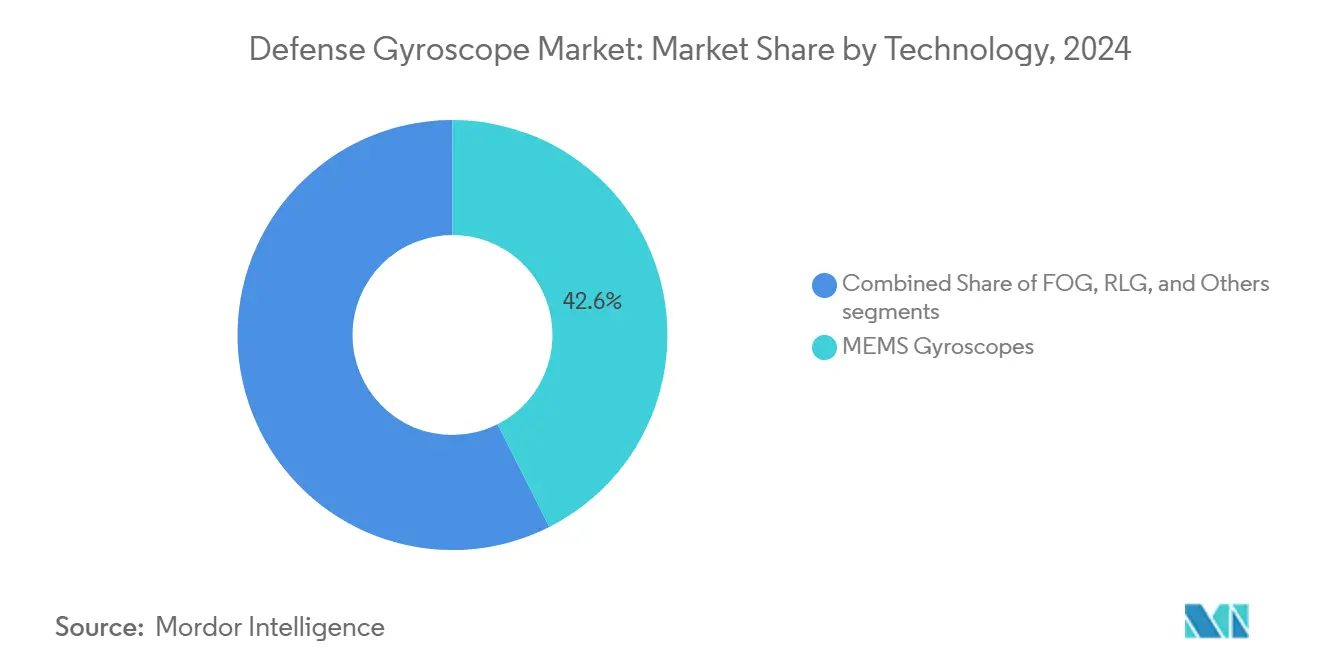

- By technology, MEMS gyroscopes led with 42.56% revenue share of the defense gyroscope market in 2024; the segment is projected to expand at a 7.32% CAGR to 2030.

- By platform, airborne systems held 36.22% of the defense gyroscope market share in 2024, while unmanned systems recorded the highest projected CAGR at 7.89% through 2030.

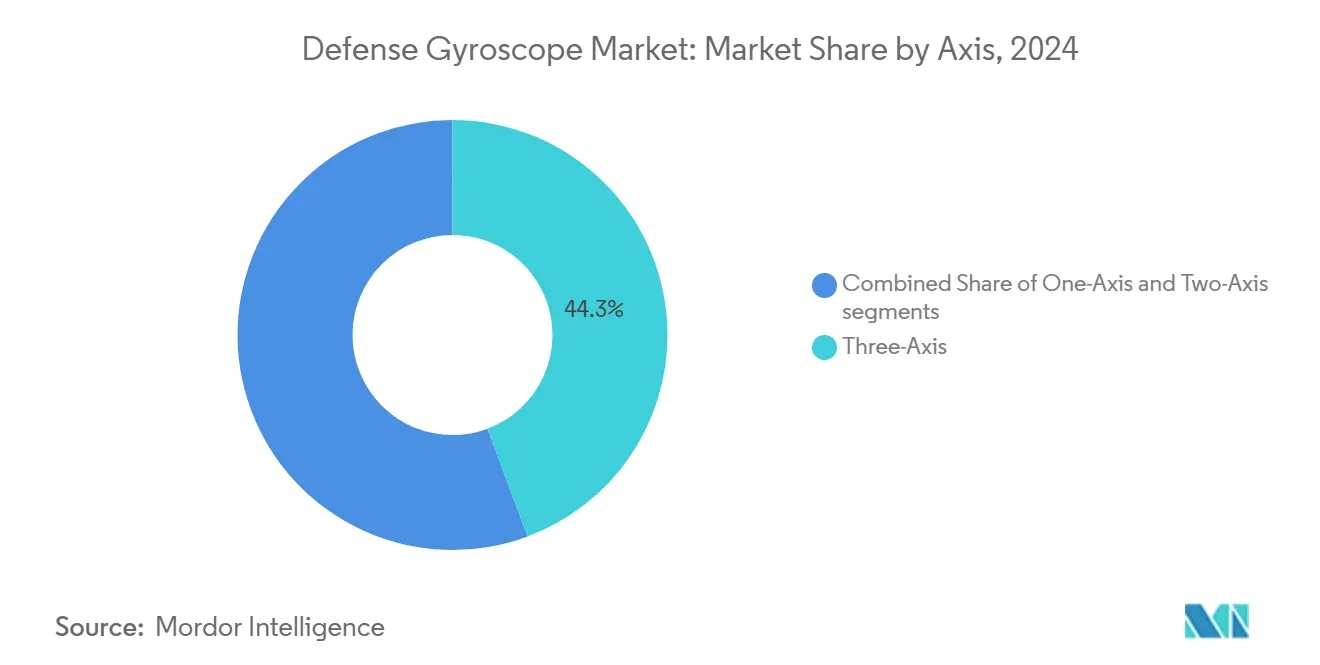

- By axis configuration, three-axis units accounted for 44.32% of the defense gyroscope market size in 2024 and are advancing at a 7.34% CAGR to 2030.

- By application, navigation and positioning captured 52.62% of the defense gyroscope market in 2024; robotics and autonomy show the fastest growth at 7.55% through 2030.

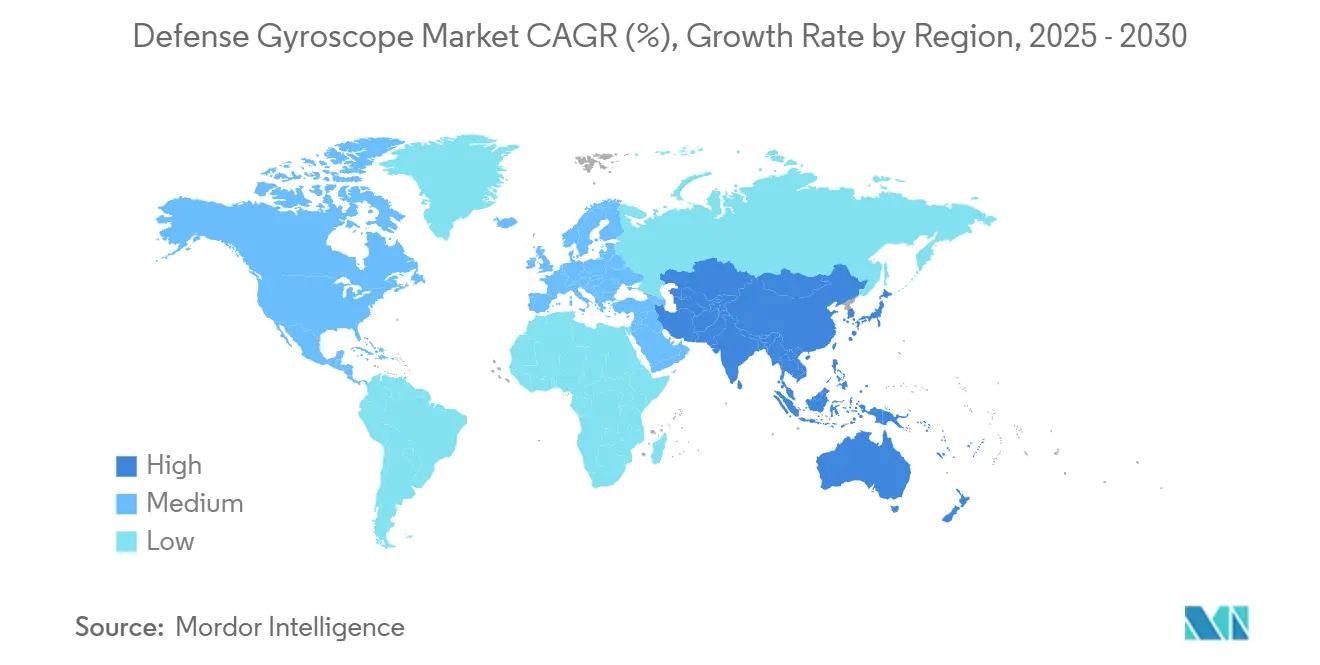

- By geography, North America retained a 34.22% share in 2024, whereas the Asia-Pacific is poised for an 8.01% CAGR during the forecast horizon.

Global Defense Gyroscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global defense modernization budgets | +1.8% | Global (North America, Europe, Asia-Pacific) | Medium term (2-4 years) |

| Rising deployment of unmanned and autonomous defense platforms | +1.5% | Global (North America, Asia-Pacific) | Medium term (2-4 years) |

| Advancements in MEMS and photonic miniaturization reducing SWaP-C | +1.2% | Global (North America, Europe) | Long term (≥ 4 years) |

| Modernization of naval and submarine inertial navigation systems | +0.9% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Integration of AI-enabled self-calibrating gyroscopes to reduce life-cycle costs | +0.7% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Growing investments in quantum and silicon photonics R&D for GPS-denied environments | +0.6% | North America, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Defense Modernization Budgets

Defense appropriations reached historic highs in 2025, with Japan dedicating JPY 8.54 trillion (USD 57.2 billion) and India allocating INR 681,210 crore (USD 81.7 billion). This surge accelerates procurement of precision navigation suites spanning air, land, and naval domains. Multi-domain operation doctrines require interoperable inertial units that sustain accuracy across contested environments. Prime contractors concentrate on domestic production to lower foreign-sourcing exposure, opening market space for local gyroscope suppliers. The US production diplomacy policy further supports trusted-network manufacturing, magnifying demand for North American and allied offerings.

Rising Deployment of Unmanned and Autonomous Defense Platforms

The US Army’s GEARS project retrofitted 41 Palletized Load System trucks with autonomous navigation kits, underscoring accelerating field adoption. Beyond ground assets, 411 commercial satellite constellation projects—39% in the CubeSat class—illustrate scaling needs for compact inertial sensors in space architectures. Battlefield lessons from electronic warfare theaters underline the necessity of GPS-denied navigation, prompting drone programs to embed inertial redundancy. AI-enabled swarming demands precise relative positioning, favoring high-volume MEMS production that meets fleet-level cost targets.

Advancements in MEMS and Photonic Miniaturization Reducing SWaP-C

Technical evaluations show state-of-the-art MEMS gyroscopes achieving 0.03°/h bias instability and 0.004°/√h angle random walk, cutting the traditional gap with fiber-optic models while preserving SWaP-C benefits.[1]Silicon Sensing, “MEMS vs FOG: Which one should you choose?” siliconsensing.com Research in air-core fiber-optic gyroscopes has reached 0.0017°/h bias instability, a tenfold precision jump tied to thermal-drift mitigation. US Army SBIR solicitations for multilayer waveguide optical gyroscopes reveal government intent to fund photonic integration that may redefine tactical-grade navigation.[2]Army SBIR|STTR, “Multilayer Waveguide Optical Gyroscope,” armysbir.army.mil Chip-scale optical devices employing multi-mode co-detection now demonstrate 1°/h bias instability, paving the way for insertion into space-constrained platforms.

Modernization of Naval and Submarine Inertial Navigation Systems

Fleet upgrades require devices capable of months-long submerged operation without GPS. Thales recorded EUR 14.70 billion (USD 17.29 billion) in 2024 orders, including submarine and frigate navigation packages. Royal Navy trials of quantum navigation sensors foreshadow the adoption of atomic-scale precision that eliminates drift during extended missions. Airbus’s Astrix 200 fiber-optic gyroscope secures bias stability below 0.0005°/h over 15-year lifetimes, confirming stringent naval performance baselines. AI-driven self-calibration reduces maintenance between deployments, underscoring a shift toward navigation-grade FOG and quantum solutions despite higher upfront prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of fiber optic gyroscopes (FOG) and ring laser gyroscopes (RLG) compared to MEMS | -0.8% | Global (emerging markets most affected) | Short term (≤ 2 years) |

| Stringent export control and ITAR regulations limiting technology transfer | -0.6% | Global (US-origin technologies) | Medium term (2-4 years) |

| Emergence of alternative navigation techniques challenging gyroscope adoption | -0.4% | Global, with concentration in autonomous vehicle and robotics sectors | Medium term (2-4 years) |

| Supply chain bottlenecks in polarization-maintaining (PM) fibers for photonic gyroscopes | -0.3% | Global, with primary impact on FOG manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Fiber-Optic Gyroscopes and Ring-Laser Gyroscopes Compared to MEMS

Navigation-grade FOG and RLG units are often priced 10–20 times tactical-grade MEMS alternatives. The tight supply of polarization-maintaining fiber exacerbates cost premiums and throttles production scaling, especially for emerging-market buyers. Although life-cycle value propositions can offset initial expenditures, procurement budgets in cost-sensitive programs frequently default to MEMS. Chinese entrants, notably ERICCO and AVIC, inject price competition, pressuring incumbents while raising security vetting demands from Western customers.

Stringent Export Control and ITAR Regulations Limiting Technology Transfer

US Munitions List categories XI, XII, and XV impose licensing on gyroscopes meeting control-moment or bias-stability thresholds, adding 30–60 days to export timelines and raising administrative overhead. The September 2024 AUKUS exemption offers relief for Australia and the UK but leaves broader markets subject to legacy restrictions. Dual-product strategies—one for domestic, one for export—erode economies of scale, prompting allied partners to accelerate indigenous development to hedge against long-term supply constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: MEMS Dominance Accelerates

MEMS devices claimed 42.56% of the defense gyroscope market in 2024 and are forecasted to grow at a 7.32% CAGR to 2030. Due to satellite constellation rollouts and autonomous vehicle fleet procurements that reward unit-cost efficiency, the defense gyroscope market size attached to MEMS is projected to widen. Fiber-optic gyroscopes, such as submarine navigation, retain leadership in applications demanding bias instability below 0.01°/h. RLG solutions witness share attrition as MEMS units approach comparable tactical accuracy at one-tenth the acquisition and maintenance outlay.

Photonic integration—chip-scale optical gyroscopes demonstrating 1°/h performance—blurs traditional boundaries between MEMS and FOG categories, opening a new competitive lane for suppliers that master wafer-level waveguide fabrication. Others, including quantum and hemispherical resonator technologies, occupy early-stage niches but attract strategic investment from primes preparing for post-2030 technology refresh cycles.

By Platform: Unmanned Systems Drive Growth

Airborne programs held 36.22% of the defense gyroscope market share in 2024, sustained by fighter upgrades, rotorcraft digital backbones, and transport-aircraft retrofit projects. Unmanned systems, however, post the highest 7.89% CAGR as militaries field drone swarms, optionally manned ground vehicles, and autonomous maritime vessels. The defense gyroscope market benefits from doctrine shifts toward attritable platforms, driving large-volume MEMS procurement.

Naval demand centers on fiber-optic and quantum devices capable of maintaining sub-0.01°/h stability during multi-month submerged patrols. Land-vehicle modernization introduces digital situational-awareness nodes needing inertial referencing, while satellite manufacturers specify radiation-hardened sensors for both CubeSat and GEO assets.

By Axis: Three-Axis Systems Dominate

Three-axis configurations comprised 44.32% of the defense gyroscope market size in 2024 and register a 7.34% CAGR through 2030 as integrated inertial-measurement units (IMUs) replace multi-sensor assemblies. Consolidated packaging lowers wiring complexity and improves mean-time-between-failure metrics. Two-axis and single-axis arrangements persist in cost-optimized stabilization rings and directed-energy pointing units but relinquish share to fully integrated solutions that sustain six-degree-of-freedom awareness.

Thales’s TopAxyz IMU, coupling ring-laser gyrometers with MEMS accelerometers, exemplifies the preferred architecture: a sealed module embedding three-axis gyroscopes, accelerometers, and processing, providing system designers with plug-and-play navigation inputs.

By Application: Navigation Leads, Robotics Accelerates

Navigation and positioning retained 52.62% of the defense gyroscope market in 2024 as every airframe, ship, and land vehicle mandates inertial fallback capacity in GPS-contested scenarios. Robotics and autonomy, projected at a 7.55% CAGR, rise in parallel with AI-guided reconnaissance drones and logistics convoys. Guidance and control remain steady, tied to precision-guided munition demand; however, budget reallocation toward persistent platforms tempers growth.

Platform-stabilization users adopt compact MEMS units that offer line-of-sight pointing accuracy within tactical tolerances, while quantum gyroscopes surface in research payloads like the QYRO CubeSat, hinting at future disruption in surveillance-grade precision.

Geography Analysis

North America controlled 34.22% of the defense gyroscope market share in 2024, leveraging the largest global defense budget and a mature industrial ecosystem. Honeywell’s EUR 200 million (USD 235.22 million) acquisition of Civitanavi Systems in Q3 2024 bolstered regional fiber-optic capacity, while its planned aerospace divisional spin-off earmarks a USD 15 billion revenue focus with 40% dedicated to defense and space. Friend-shoring initiatives embedded in the National Defense Industrial Strategy aim to repatriate critical component production, shielding supply chains from geopolitical friction. The AUKUS exemption, effective September 2024, streamlines technology flow among the United States, Australia, and the United Kingdom, likely accelerating joint-project fielding.

Asia-Pacific exhibits the strongest momentum at an 8.01% CAGR toward 2030. Japan’s USD 57.2 billion 2025 allocation and India’s USD 81.7 billion defense budget underscore a multi-billion-dollar procurement pipeline. China cultivates domestic suppliers—ERICCO and AVIC—challenging Western price points and stimulating indigenous R&D across the region. South Korea’s expanding defense-industrial footprint and Australia’s participation in AUKUS propel additional demand. Widespread investment in unmanned maritime surveillance and aerial platforms supports high-volume MEMS and mid-grade FOG uptake.

Europe maintains balanced growth, fueled by collaborative defense frameworks and corporate consolidation. Safran targets a doubling of defense-electronics revenue by 2028–2030 and gained EU antitrust clearance for its USD 1.8 billion acquisition of Collins Aerospace’s flight-control division, strengthening inertial-navigation capabilities.[3]GuruFocus, “Safran’s $1.8 Billion Acquisition Approved,” gurufocus.com Thales, holding an order backlog worth EUR 39.2 billion (USD 46.10 billion), integrates quantum research with established ring-laser lines to secure long-term relevance. European Defence Fund financing encourages cross-border R&D, yet divergent national export-control regimes continue to add administrative layers to intra-bloc technology transfer.

Competitive Landscape

Market concentration is moderate; Honeywell International Inc., Northrop Grumman Corporation, and Safran headline the three-tier structure, combining MEMS, FOG, and RLG portfolios within vertically integrated supply chains. Honeywell’s Civitanavi acquisition extends European presence and deepens FOG expertise, while the forthcoming corporate separation intends to sharpen focus on aerospace and defense navigation solutions. Northrop Grumman Corporation leverages LITEF subsidiary competencies in ring-laser technology, merging them with research into silicon-photonics pathways for next-generation IMUs.

Safran’s acquisition of Collins Aerospace’s flight-control business expands integration playbooks across avionics and inertial guidance, positioning the firm to bundle gyroscope hardware with flight-control surfaces in turnkey offerings. Vector Atomic and Lockheed Martin’s QuINS demonstration introduces quantum-class contenders; such entrants often partner with primes to overcome production-rate and certification hurdles.

Supply-chain resilience emerges as a pivotal competitive differentiator. Polarization-maintaining fiber shortages during pandemic disruptions spurred near-shoring moves by several North American and European producers. ITAR compliance infrastructure advantages incumbents, although September 2024 AUKUS revisions grant smaller allied suppliers a route into restricted markets. Pressure from Chinese value competitors motivates Western firms to highlight trusted-supplier provenance in procurement competitions.

Defense Gyroscope Industry Leaders

Honeywell International Inc.

Northrop Grumman Corporation

Exail Technologies

EMCORE Corporation

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Curtiss-Wright Corporation secured contracts from Rheinmetall to provide turret drive stabilization systems (TDSS) for Germany's Boxer Heavy Weapon Carrier and Hungary's Lynx Infantry Fighting Vehicle (IFV). The TDSS incorporates gyroscope technology that maintains accurate turret stabilization during vehicle movement.

- July 2024: The US Navy awarded The Charles Stark Draper Laboratory Inc. in Cambridge, Massachusetts, a USD 111 million contract to manufacture interferometric fiber optic gyros (IFOGs) for Trident II (D5) submarine-launched nuclear missiles.

Global Defense Gyroscope Market Report Scope

| MEMS Gyroscopes |

| Fiber-Optic Gyroscopes (FOG) |

| Ring Laser Gyroscopes (RLG) |

| Others |

| Airborne Platforms |

| Naval and Sub-Surface Platforms |

| Land Vehicles |

| Spacecraft and Satellites |

| Missiles and Precision-Guided Munitions |

| Unmanned Systems |

| One-Axis |

| Two-Axis |

| Three-Axis |

| Navigation and Positioning |

| Guidance and Control |

| Platform Stabilization and Pointing |

| Robotics and Autonomy |

| Surveillance and ISR Payloads |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middile East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Technology | MEMS Gyroscopes | ||

| Fiber-Optic Gyroscopes (FOG) | |||

| Ring Laser Gyroscopes (RLG) | |||

| Others | |||

| By Platform | Airborne Platforms | ||

| Naval and Sub-Surface Platforms | |||

| Land Vehicles | |||

| Spacecraft and Satellites | |||

| Missiles and Precision-Guided Munitions | |||

| Unmanned Systems | |||

| By Axis | One-Axis | ||

| Two-Axis | |||

| Three-Axis | |||

| By Application | Navigation and Positioning | ||

| Guidance and Control | |||

| Platform Stabilization and Pointing | |||

| Robotics and Autonomy | |||

| Surveillance and ISR Payloads | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middile East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the defense gyroscope market in 2025?

The defense gyroscope market size is valued at USD 661.4 million in 2025.

What is the expected CAGR for defense gyroscopes through 2030?

The market is projected to each USD 889.29 million by 2030, advancing at a 6.10% CAGR.

Which region shows the fastest demand growth for defense gyroscopes?

Asia-Pacific leads with an 8.01% CAGR, driven by rising defense budgets in Japan, India, China, and South Korea

Which technology segment dominates current deployments?

MEMS gyroscopes hold a 42.56% market share and are expanding at a 7.32% CAGR thanks to SWaP-C efficiencies.

What platform category records the highest growth rate?

Unmanned systems post the fastest platform CAGR at 7.89% as militaries scale autonomous fleets.

Which application area contributes the most revenue today?

Navigation and positioning applications account for 52.62% of market revenue due to GPS-denied operational requirements.

Page last updated on: