Whipping Cream Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

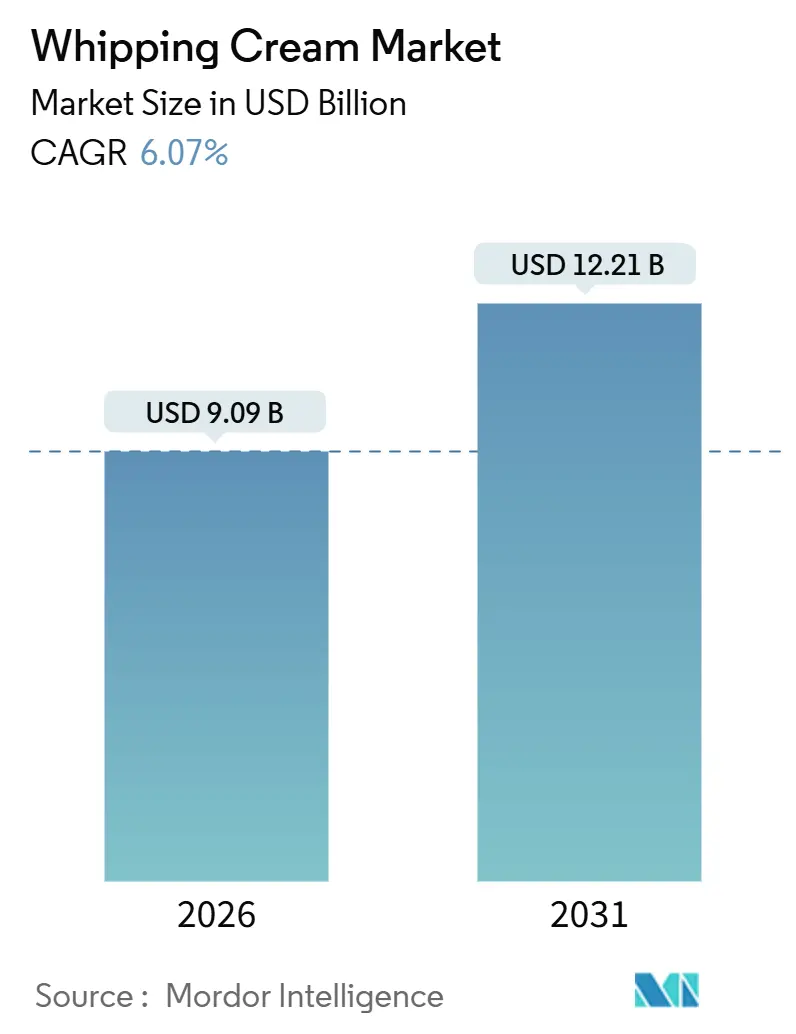

| Market Size (2026) | USD 9.09 Billion |

| Market Size (2031) | USD 12.21 Billion |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Whipping Cream Market Analysis by Mordor Intelligence

The whipping cream market size is estimated at USD 9.09 billion in 2026, and is expected to reach USD 12.21 billion by 2031, at a CAGR of 6.07% during the forecast period (2026-2031). This trajectory reflects structural shifts in how consumers and foodservice operators deploy dairy and plant-based toppings across beverages, desserts, and home-cooking applications. Capacity investments by major dairy cooperatives signal confidence in sustained demand, with Fonterra breaking ground on a USD 88 million UHT cream plant at Edendale in December 2024 that will produce 50 million litres annually by August 2026, doubling to 100 million litres by 2030. These moves underscore a bet that premiumisation in coffee culture, home baking, and on-trade hospitality will outpace health-driven substitution toward non-dairy alternatives. Regulatory clarity on plant-based labeling from the FDA in January 2025 further widens product choice and stimulates competition.

Key Report Takeaways

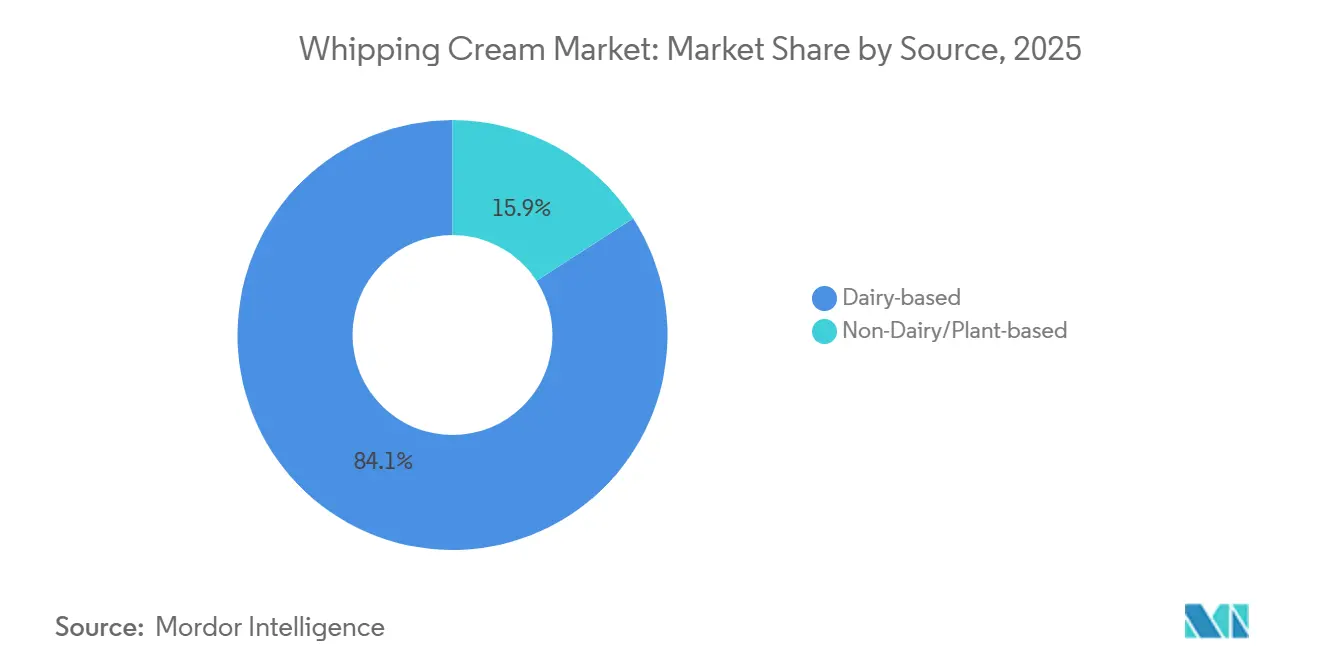

- By source, dairy cream commanded 84.11% of the whipping cream market share in 2025, while non-dairy alternatives are forecast for an 8.05% CAGR through 2031.

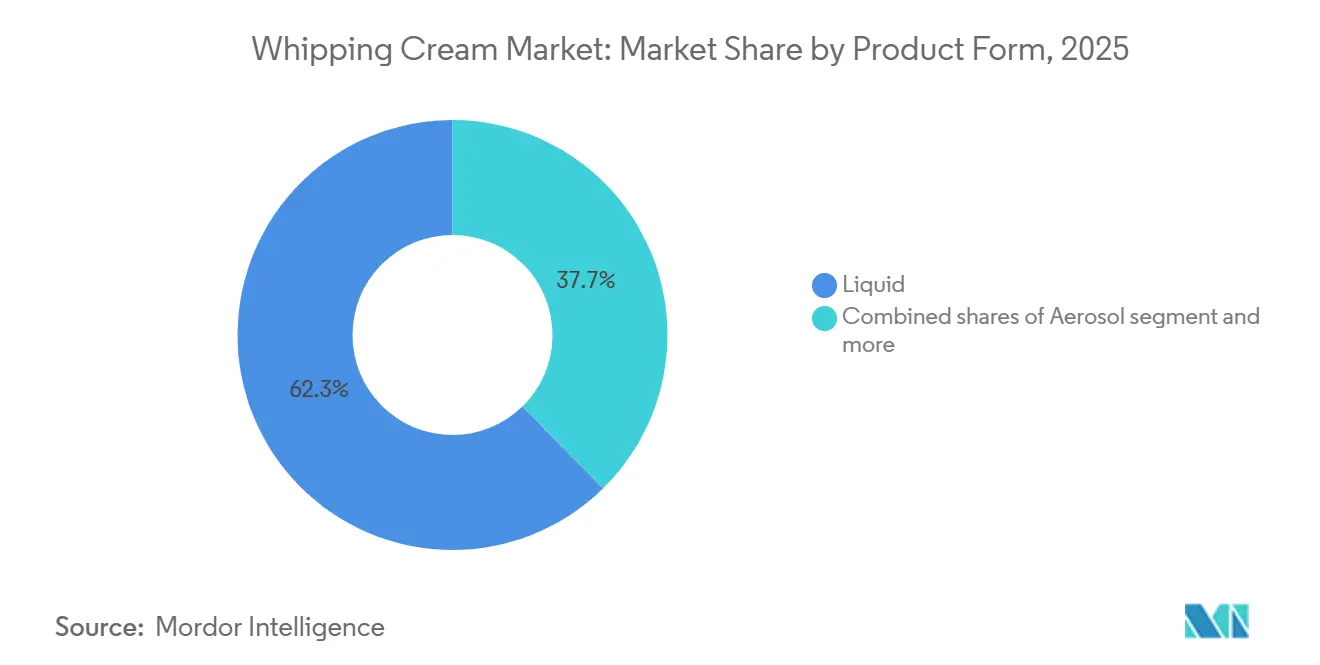

- By product form, liquid cream led with 62.34% of the whipping cream market share in 2025; aerosol formats are projected to advance at an 8.16% CAGR to 2031.

- By distribution channel, off-trade outlets held a 57.65% revenue share in 2025, whereas on-trade sales are poised to climb at a 7.86% CAGR as tourism and café culture rebound.

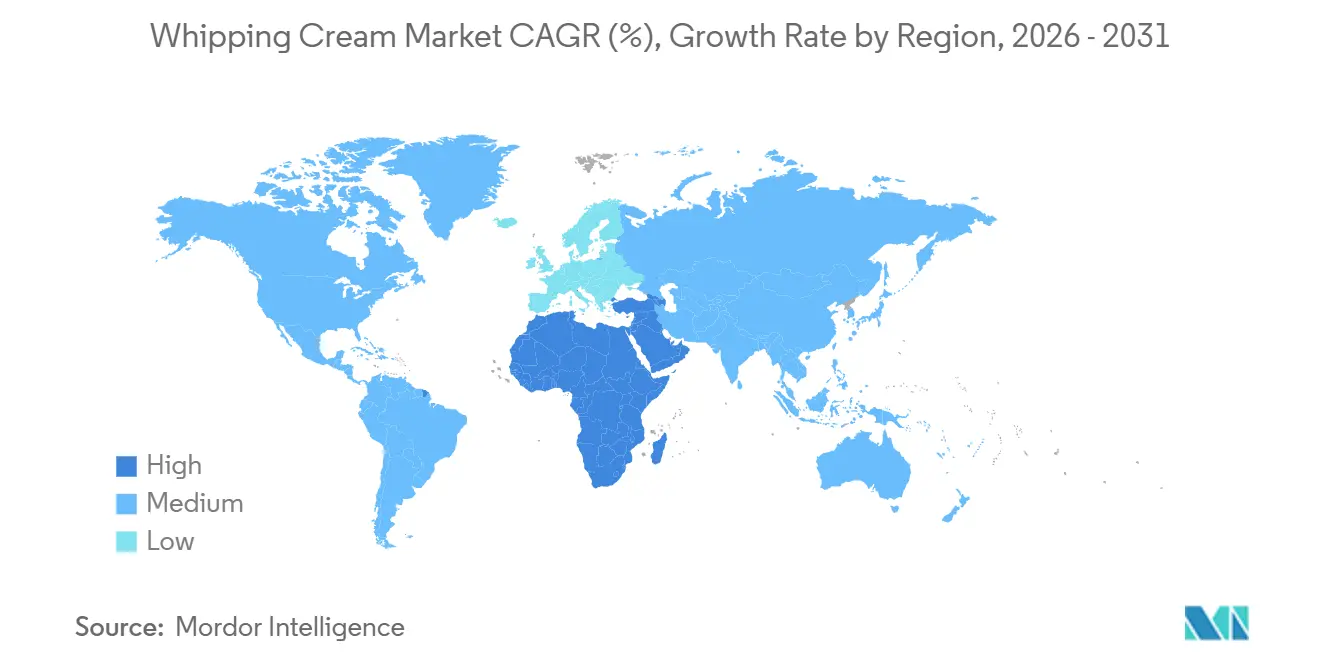

- By geography, Europe accounted for 26.73% of 2025 revenue, and the Middle East & Africa region is set to expand at an 8.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Whipping Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in home baking and cooking trends | +1.5% | Global, with strongest uptake in Europe and North America | Medium term (2-4 years) |

| Expanding foodservice and café culture globally | +2.1% | Global, APAC (Asia-Pacific) and MEA (Middle East and Africa) accelerating | Long term (≥ 4 years) |

| Greater use in beverages and specialty coffees | +1.8% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Rising popularity of plant-based cream alternatives | +1.2% | North America, Europe, APAC coastal cities | Long term (≥ 4 years) |

| Ease of purchase via online retail channels | +1.0% | Global, led by North America and China | Short term (≤ 2 years) |

| Premium dessert demand in tourism hubs | +0.9% | MEA, Europe, select APAC destinations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Home-Baking Culture Drives Retail Demand

Pandemic-era lockdowns catalyzed a durable shift toward home baking, with Arla Foods reporting that 70% of Danes baked at home in 2024, sustaining demand for whipping cream in cakes, pastries, and mousse preparations. This behavior persists even as mobility restrictions are lifted, because consumers discovered cost savings and creative satisfaction in homemade desserts. Retailers responded by expanding shelf space for premium dairy ingredients, including heavy cream with 36% milkfat content that whips to stiffer peaks than standard formulations. The trend is most pronounced in Europe and North America, where baking culture is embedded, yet emerging middle classes in the Asia-Pacific are adopting Western dessert recipes, broadening the addressable market. Ingredient suppliers are launching smaller-format packaging, 250 ml and 500 ml cartons, to reduce waste for occasional bakers, a move that also raises per-unit margins.

Rising Popularity of Plant-Based Cream Alternatives

The plant-based segment in the whipping cream market demonstrates an 8.05% CAGR, attributed to increased consumer awareness regarding health and sustainability factors. According to the Good Food Institute, 59% of United States households purchased plant-based foods in 2024, with nearly 80% demonstrating repeat purchase behavior [1]Source: Good Food Institute, "U.S. Retail Market Insights for the Plant-based Industry", gfi.org. This market trend indicates sustained demand for dairy-free whipping alternatives, particularly plant-based creams derived from coconut, oat, or soy. Technological developments in plant-based formulations have enhanced the stability, texture, and whipping properties of these products to align with conventional dairy standards. The FDA issued draft guidance in January 2025 clarifying that plant-based products may use dairy terms if accompanied by the plant source, reducing regulatory uncertainty. This clarity enables brand investment in marketing and distribution, likely accelerating the 8.05% CAGR for non-dairy whipping cream through 2031. The segment's growth paradoxically benefits incumbent dairy processors, who are acquiring or launching plant-based lines to defend shelf space and capture flexitarian consumers.

Greater Use in Beverages and Specialty Coffees

Specialty coffee sales in the United States grew over two years and reached significant heights in 2024, with Nestlé investing USD 675 million in an Arizona factory to produce Coffee-mate creamers and launching a cold-foam line in January 2025, targeting consumers who crave whipped toppings on iced beverages. The cold-foam format, a lightly whipped cream that floats atop cold brew or iced lattes, has migrated from coffeehouse menus into retail channels, with three-flavor SKUs priced at USD 4.68 to USD 5.49 per 14-fluid-ounce bottle. This innovation extends whipping cream's use case beyond dessert finishing into daily beverage rituals, capturing incremental volume from consumers who previously added only milk or half-and-half. Arla partnered with Baileys to launch a 250 ml squirty whipped cream at Tesco in October 2024 for GBP 2.50 (USD 3.15), blending indulgence with convenience. These product forms lower the barrier to trial and encourage repeat purchase by eliminating the need for manual whipping equipment.

E-commerce Enabling Direct-to-Consumer Cream Brands

E-commerce expansion is driving changes in the whipping cream market as direct-to-consumer (DTC) brands establish distribution channels independent of traditional retail networks. Digital platforms enable companies to distribute specialized products, including organic, plant-based, and artisanal whipping cream variants, frequently packaged with complementary offerings. For instance, Straus Family Creamery in the United States exemplifies this business model by distributing organic whipping cream through its digital platform and premium online grocery retailers. The e-commerce distribution model supports subscription-based revenue streams, enhances inventory management, and provides small-batch manufacturers access to expanded markets. The increasing adoption of online grocery purchasing has positioned DTC as a key distribution channel in the premium and specialty whipping cream segment.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over saturated fat and calorie content | -1.3% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Raw-milk price volatility and supply shortfalls | -1.1% | Global, with regional spikes in Oceania and Europe | Short term (≤ 2 years) |

| Cold-chain infrastructure gaps | -0.8% | APAC emerging markets, MEA, South America | Medium term (2-4 years) |

| Intensifying competition from non-dairy toppings and whipped aerosols | -0.7% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns over Saturated Fat and Calorie Content

Rising consumer awareness about health risks associated with high-fat diets has created significant challenges for traditional whipping cream manufacturers, driving the development of healthier alternatives. Studies on hydrocolloids in whipping cream demonstrate that additives such as pectin and carrageenan enhance foaming properties while reducing lipid digestion rates. The incorporation of these hydrocolloids helps maintain product stability and texture while addressing health concerns. Carrageenan demonstrates superior effectiveness compared to pectin in decreasing lipid digestion, enabling the development of whipped cream products with improved nutritional profiles. These developments address consumer demand for products that combine indulgence with health benefits. Manufacturers are investing in research and development to create innovative formulations that maintain the desired taste and texture while reducing fat content. The market shows increasing acceptance of these modified whipping cream products, particularly among health-conscious consumers who seek alternatives to traditional dairy products.

Raw-milk Price Volatility and Supply Shortfalls

Dairy commodity markets exhibited sharp swings in 2024 and 2025. For instance, USDA data showed Class II butterfat prices in the U.S. Northeast declining from USD 2.85 per pound in January 2025 to USD 2.54 by March 2025, reflecting abundant domestic cream supply. These regional divergences complicate procurement for multinational processors and create margin compression when input costs spike faster than retail prices can adjust. The Big-7 dairy exporters, New Zealand, the European Union, the United States, Australia, Argentina, Uruguay, and Brazil, are forecast to increase milk supply by only 1.6% in 2025 and 0.6% in 2026, constraining the raw-material base for cream production. Smaller processors lacking futures-market hedging or long-term supply contracts face heightened risk of margin erosion or supply interruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Dairy Dominance Faces Plant-Based Disruption

Dairy-based whipping cream captured 84.11% of market revenue in 2025, underpinned by established supply chains, consumer familiarity, and superior whipping performance derived from butterfat's crystallization properties. However, non-dairy and plant-based alternatives are expanding at an 8.05% CAGR through 2031, the fastest rate among source segments, as formulators close the gap on taste and texture. The FDA's January 2025 draft guidance clarifying that plant-based products may use dairy terminology if accompanied by the plant source reduces regulatory friction and enables brand investment.

Dairy processors are responding by acquiring or launching plant-based lines to defend shelf space. Fonterra's USD 88 million UHT cream plant at Edendale, which began production in August 2026 with 50 million litres of annual capacity doubling to 100 million by 2030, signals confidence that dairy demand will persist even as alternatives grow. Non-dairy entrants such as Califia Farms are deploying coconut, oat, and almond bases with hydrocolloids to replicate dairy's mouthfeel, capturing flexitarian consumers who oscillate between dairy and plant-based depending on use occasion. This bifurcation suggests that the 84.11% dairy share in 2025 will erode gradually rather than collapse, as both segments coexist and serve distinct consumer needs.

By Product Form: Aerosol Gains Ground on Convenience

Liquid whipping cream held 62.34% of the market share in 2025, favored by professional bakers and baristas for its versatility and ability to achieve precise textures through manual or mechanical whipping. Yet aerosol formats are growing at 8.16% CAGR through 2031, driven by single-serve convenience and impulse purchases. Whipnotic's flavored aerosol line, featuring a patented nozzle, expanded to over 1,000 retail locations in 2024 and posted 150% quarterly revenue growth by targeting consumers who want dessert finishing without equipment or cleanup. Nestlé launched Coffee-mate Cold Foam in January 2025, offering three flavors in 14-fluid-ounce bottles priced at USD 4.68 to USD 5.49, aimed at the one-in-five coffee drinkers who crave whipped toppings on iced beverages.

The "Others" category, encompassing powdered and frozen formats, serves niche applications such as industrial baking and long-haul foodservice where refrigeration is constrained. Powdered cream offers extended shelf life and reduced freight costs due to lower weight, yet reconstitution adds labor and the final texture rarely matches fresh liquid or aerosol. Frozen whipped cream is used in pre-portioned desserts and institutional catering, where consistency and portion control outweigh the premium mouthfeel of fresh-whipped dairy. Liquid cream's 62.34% share reflects its entrenched position in professional kitchens and home baking, yet aerosol's 8.16% CAGR indicates that convenience-driven formats will capture incremental volume from consumers who prioritize speed and single-serve packaging over artisanal preparation.

By Distribution Channel: On-Trade Growth Outpaces Retail Expansion

The off-trade segment dominates the whipping cream market with a 57.65% share in 2025. This segment includes supermarkets, hypermarkets, convenience stores, and online platforms. Online stores show notable growth, driven by e-commerce expansion and increasing direct-to-consumer sales in the dairy industry. The convenience and accessibility of online shopping, combined with improved cold chain logistics for dairy products, contribute to this growth. Supermarkets and hypermarkets maintain their position as the largest sub-segment through established cold chain infrastructure, diverse product offerings, and the ability to provide competitive pricing through bulk purchasing.

The on-trade segment demonstrates robust growth at a 7.86% CAGR (2026-2031), exceeding overall market growth rates. This expansion stems from the growth of food service chains in emerging markets and the increased inclusion of premium desserts in restaurant menus. The rising consumer preference for dining out, the growth in café culture, and the expansion of bakery chains further drive this segment's growth. For instance, in the United States, 55% of consumers preferred dining at restaurants over ordering takeout or delivery in 2023, according to US Foods Inc [2]Source: US Foods, Inc., "The Diner Dispatch: 2024 American Dining Habits", usfoods.com. The segment presents opportunities for specialized whipping cream products tailored to food service requirements, focusing on stability and performance in commercial settings. These products often feature enhanced heat resistance, longer holding times, and consistent whipping performance. The distinct growth patterns between off-trade and on-trade segments emphasize the need for targeted product development and marketing approaches by manufacturers, including packaging solutions, product formulations, and distribution strategies specific to each channel.

Geography Analysis

Europe commanded 26.73% of whipping cream revenue in 2025, anchored by mature baking traditions, dense coffeehouse networks, and strong per-capita dairy consumption. Germany, France, the United Kingdom, Italy, and Spain represent the largest country markets, where whipping cream is a staple in patisserie, café beverages, and home dessert preparation. Smaller markets such as Poland, Belgium, Sweden, and the Netherlands contribute incremental volume, with Poland benefiting from rising disposable incomes and Belgium from its artisanal chocolate and dessert culture. Europe's established cold-chain infrastructure and stringent food-safety standards under the European Food Safety Authority (EFSA) enable efficient distribution and long shelf life, supporting the region's leadership position.

North America is the second-largest geography, driven by the United States' foodservice sector and Canada's robust dairy industry. U.S. Class II butterfat prices declined from USD 2.85 per pound in January 2025 to USD 2.54 by March 2025 in the Northeast, reflecting abundant domestic cream supply that benefits processors and pressures farmgate prices, according to the USDA AMS. Mexico's growing middle class and expanding café culture add incremental volume, though cold-chain gaps in rural areas constrain penetration. Canada's dairy supply management system stabilizes farmgate prices but limits export competitiveness, focusing processors on domestic and niche premium segments. North America's regulatory environment under the FDA and USDA ensures product safety and labeling clarity, with the FDA's December 2024 finalization of a "healthy" claim rule tightening saturated-fat thresholds effective 2028.

The Middle East and Africa region is expanding at an 8.24% CAGR through 2031, the fastest rate among geographies, propelled by tourism infrastructure in Gulf Cooperation Council states, expatriate demand, and retail modernization. The United Arab Emirates imported USD 1.6 billion of dairy products in 2020, with milk and cream accounting for 43% (USD 669 million), underscoring reliance on imports to meet consumption. Saudi Arabia is the fastest-growing market within MEA, driven by Vision 2030 initiatives that are expanding hospitality capacity and liberalizing the entertainment sectors. High-end hotels and restaurants in Dubai, Riyadh, and Doha stock premium whipping cream for plated desserts and specialty coffees that command USD 10 to USD 15 per item, margins that justify airfreight of chilled dairy from Europe or Oceania when local supply is insufficient. According to the World Tourism Organization (UN Tourism), the UAE and Saudi Arabia recorded the highest international tourist arrivals among Middle Eastern countries, with 28.15 million and 27.4 million visitors respectively in 2023 [3]Source: World Tourism Organization (UN Tourism), "International Tourism Highlights, 2024 Edition", unwto.org.

Competitive Landscape

The whipping cream market demonstrates moderate consolidation, with established dairy companies and regional manufacturers operating in the industry. Companies such as Fonterra Co-operative Group, Arla Foods, Nestlé S.A., Land O’Lakes, and FrieslandCampina hold significant market positions through their extensive distribution networks and diverse product portfolios. These companies prioritize product innovation through the development of new flavors, textures, and functional properties.

Major market players focus on sustainability initiatives that encompass responsible sourcing, reduced packaging waste, and lower carbon emissions. Their market expansion efforts target the Asia-Pacific and Middle East and Africa regions, where rising disposable incomes and changing consumer preferences drive demand. Companies are also investing in research and development to improve product quality, enhance production efficiency, and meet evolving consumer preferences for healthier options.

The market's competitive landscape is transforming as plant-based manufacturers and technology-focused startups challenge traditional dairy producers. New entrants differentiate themselves through alternative ingredients, clean-label formulations, and innovative packaging solutions. Companies are investing in advanced processing technologies to improve product stability, extend shelf life, and enhance environmental sustainability. These technological investments include ultra-high temperature processing, aseptic packaging systems, and automated quality control measures, making technological capabilities an important competitive advantage in the market.

Whipping Cream Industry Leaders

-

Fonterra Co-operative Group

-

Arla Foods AMBA

-

Land O’Lakes

-

FrieslandCampina N.V.

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Anchor Food Professionals released Infiniti whipping cream at FHA-HORECA 2024. The product exhibits a pearl white color and European cream flavor that enhances ingredients and garnishes.

- October 2024: Diageo UK and Arla Foods formed a strategic partnership to introduce Baileys' first whipped cream product in UK retail stores. The Espresso Cream product, which incorporated a new packaging design, became available exclusively at Tesco stores as part of its cream product line.

- August 2024: Whipnotic released two new flavored whipped cream products: peppermint mocha and apple crisp. The products were gluten-free and contained no artificial flavors.

- January 2024: Starco Brands, Inc., introduced a new limited-edition strawberry variant of Whipshots, a vodka-infused whipped cream developed in partnership with Cardi B. The whipped cream product enhances desserts and cocktails.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global whipping cream market as all fluid and aerosol products that contain 30 to 48 percent milk fat and can be aerated into a stable foam for use in desserts, beverages, and savory dishes; plant-based lines such as coconut, oat, or soy creams are included when they are sold specifically for whipping applications.

Scope Exclusion: We omit low-fat table cream below 25 percent fat, shelf-stable cooking cream, and bulk butterfat traded only for industrial re-processing.

Segmentation Overview

-

Source

- Dairy-based

- Non-Dairy/Plant-based

-

Product Form

- Liquid

- Aerosol

- Others

-

Distribution Channel

-

Off-Trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Retailers

- Online Stores

- Other Distribution Channels

- On-Trade

-

Off-Trade

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cream processors, dairy cooperatives, plant-based formulators, and procurement heads at cafés and bakeries across North America, Europe, and Asia-Pacific. Conversations validated yield assumptions, average selling prices, and channel-mix shifts before the model was locked.

Desk Research

Our team first mapped supply and demand through open datasets from the Food and Agriculture Organization, United States Department of Agriculture, Eurostat milk-utilization files, and International Dairy Federation reports. Next, HS-code 0401.40 trade flows were pulled from UN Comtrade, while household expenditure surveys and NielsenIQ public releases clarified retail uptake.

Filings gathered via D&B Hoovers, news scanned in Dow Jones Factiva, and association newsletters then highlighted new plants, packaging shifts, and short-term price swings.

These titles are illustrative; many other public and subscription sources informed cross-checks.

Market-Sizing & Forecasting

We start with a top-down reconstruction: raw-milk volumes, regional fat-recovery ratios, and import-export balances create a potential cream pool that is filtered through household and food-service penetration rates. Selective bottom-up supplier roll-ups of aerosol cans and liquid cartons multiplied by sampled ASPs corroborate totals, giving one clear triangulation. Key drivers fed into the multivariate regression forecast include whole-milk-powder prices, per-capita bakery spending, premium coffee outlet counts, plant-based cream share, and cold-chain warehouse capacity.

Data Validation & Update Cycle

Outputs pass variance checks against historic ratios and external indicators, followed by senior review. The database refreshes annually, with interim updates triggered by tariff shifts or material raw-milk price moves.

Why Mordor's Whipping Cream Baseline Commands Reliability

Published estimates often diverge; some firms report USD 9.15 billion for 2024 or USD 8.40 billion for 2024, while Mordor pegs 2025 at USD 8.65 billion.

Gaps stem from differing fat thresholds, inclusion or exclusion of plant-based lines, and refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.65 B (2025) | Mordor Intelligence | - |

| USD 9.15 B (2024) | Global Consultancy A | Counts table cream and applies uniform price inflation |

| USD 8.40 B (2024) | Industry Association B | Excludes plant-based products |

| USD 9.91 B (2025) | Regional Consultancy C | Relies on capacity announcements without retail sell-through checks |

The comparison shows our estimate sits near the midpoint of credible values, reflecting balanced assumptions. Clients therefore receive a transparent, auditable baseline that flexes with new evidence yet avoids unvetted optimism.

Key Questions Answered in the Report

How large is the global whipping cream market in 2026?

The whipping cream market size reached USD 9.09 billion in 2026 and is set to climb to USD 12.21 billion by 2031.

What is the expected growth rate for whipping cream to 2031?

The market is forecast to post a 6.07% CAGR between 2026 and 2031.

Which product form is growing fastest within whipping cream?

Aerosol whipping cream is projected to expand at an 8.16% CAGR through 2031, outpacing liquid formats.

Which region shows the highest future growth for whipping cream?

The Middle East & Africa region is expected to register an 8.24% CAGR due to tourism-led foodservice demand.

Page last updated on: