Digital Photo Frame Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

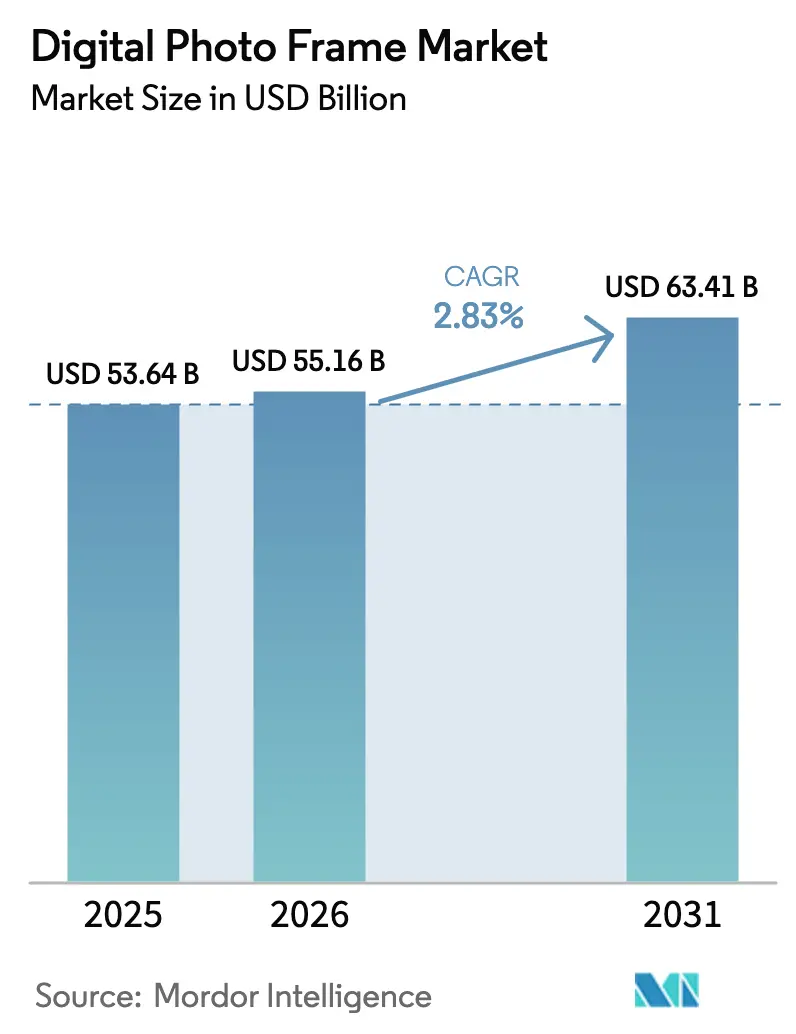

| Market Size (2026) | USD 55.16 Billion |

| Market Size (2031) | USD 63.41 Billion |

| Growth Rate (2026 - 2031) | 2.83% CAGR |

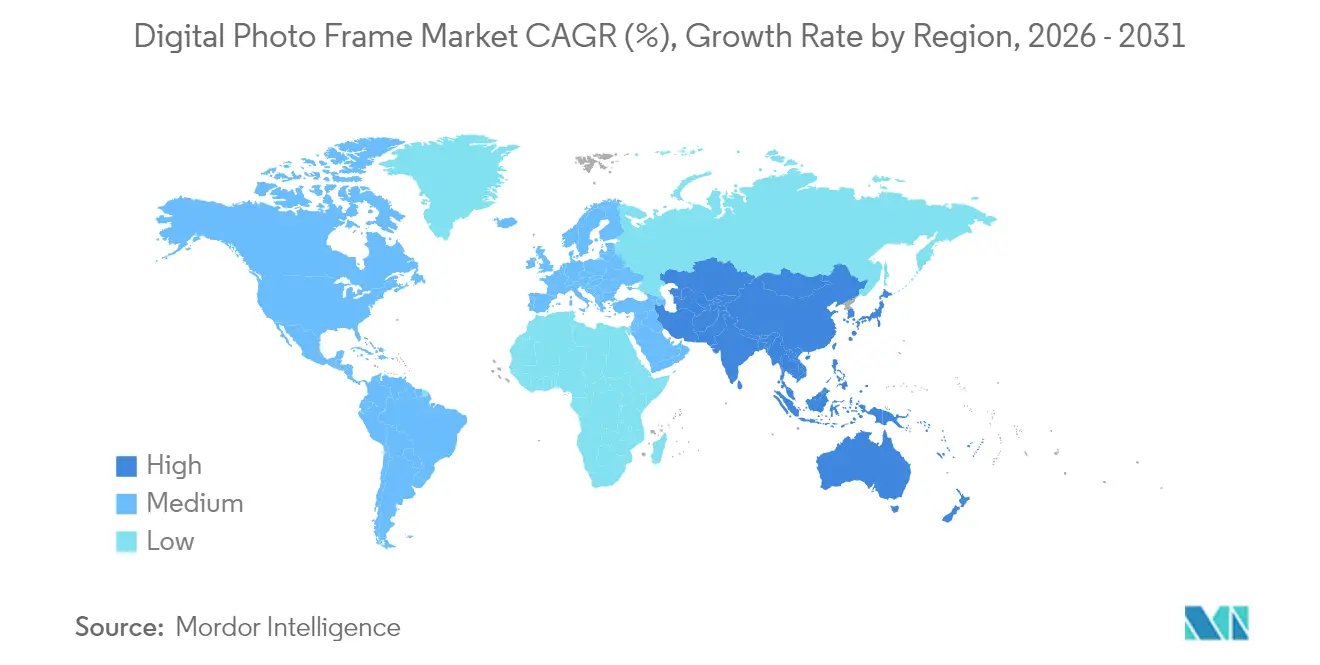

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Photo Frame Market Analysis by Mordor Intelligence

The digital photo frame market size is expected to grow from USD 53.64 billion in 2025 to USD 55.16 billion in 2026 and is forecast to reach USD 63.41 billion by 2031 at 2.83% CAGR over 2026-2031. Rising smart-home penetration, expanding Wi-Fi ecosystems and premium design upgrades continue to offset competitive pressure from smartphones and multi-purpose smart displays. Residential demand remains the primary volume driver, while healthcare and commercial deployments add incremental growth by turning frames into engagement, memory-care and branding tools. Manufacturers concentrate on connectivity, cloud services and artificial-intelligence curation to maintain differentiation as hardware margins narrow. Regionally, North America retains clear value leadership, yet Asia-Pacific (APAC) delivers the fastest unit and revenue expansion on the back of rising middle-class incomes and local manufacturing scale. Channel dynamics favor online marketplaces that help shoppers compare specifications, secure promotional pricing and integrate optional subscription services, accelerating direct-to-customer fulfillment.

Key Report Takeaways

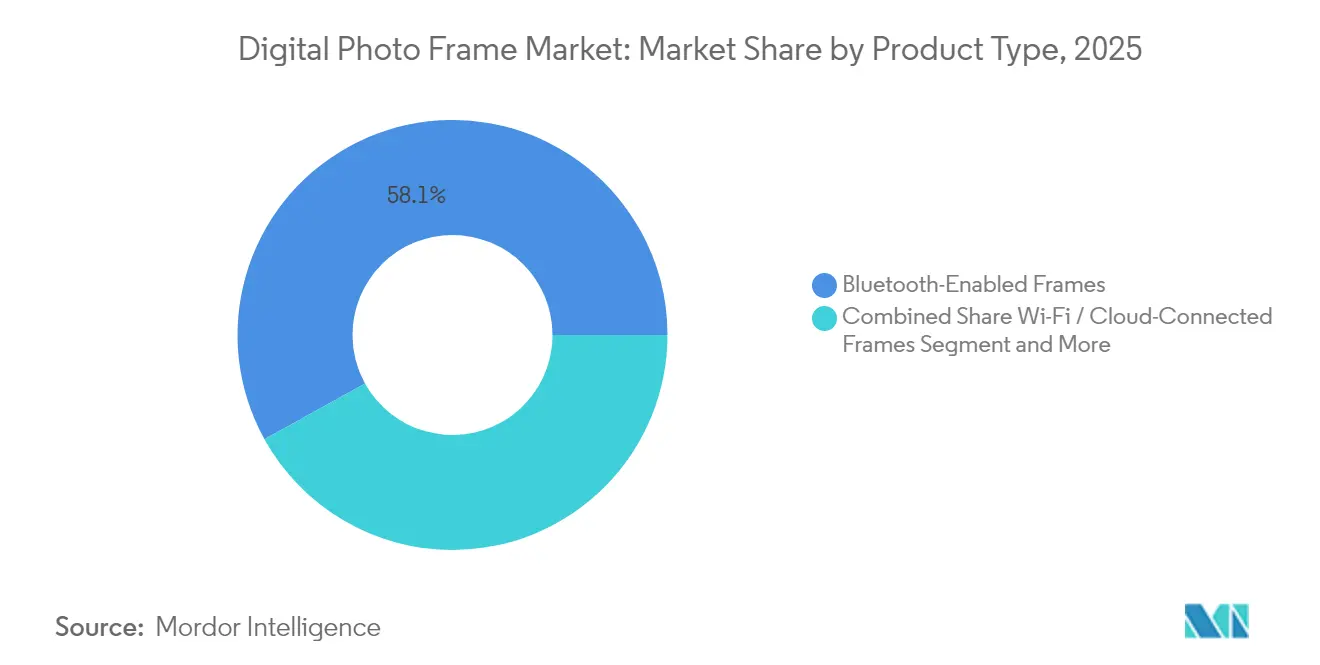

- By product type, Bluetooth-enabled units led with 58.05% of the digital photo frame market share in 2025, whereas Wi-Fi/cloud-connected models are projected to grow fastest at a 5.55% CAGR to 2031.

- By screen size, 7-inch–10-inch frames held 55.05% revenue share in 2025; up-to-7-inch formats are set to expand at a 4.05% CAGR through 2031.

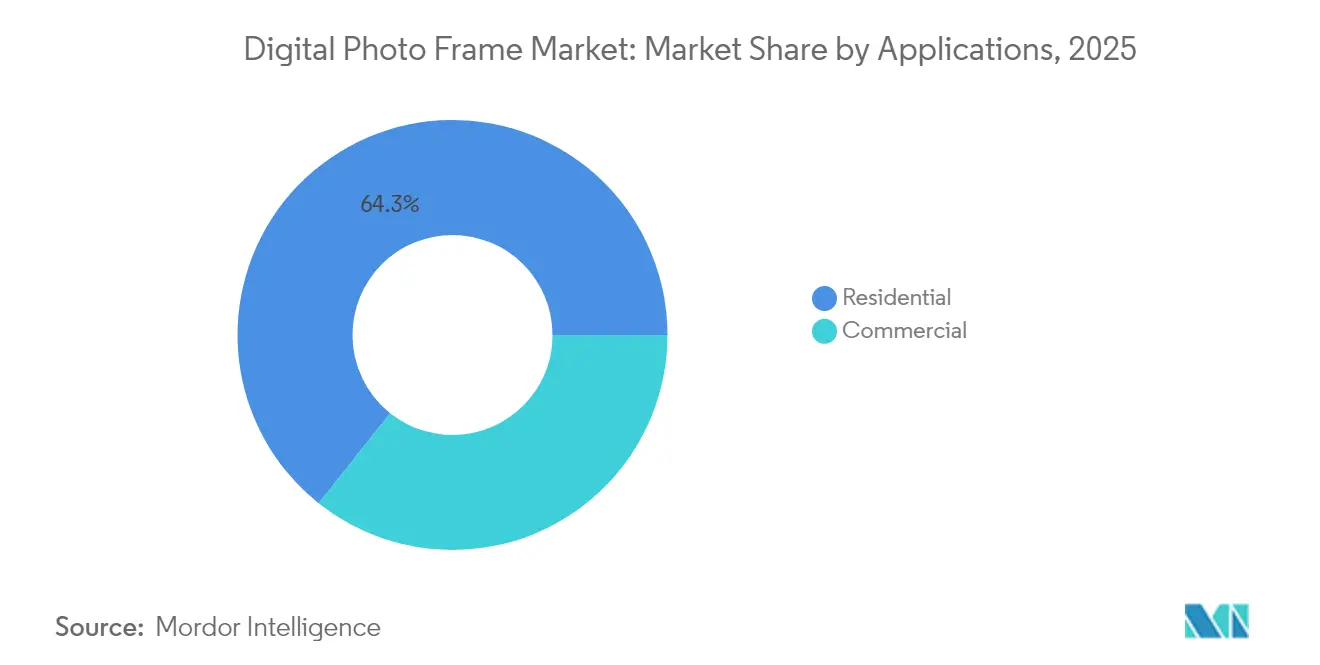

- By application, residential use captured 64.30% of the digital photo frame market size in 2025, while healthcare facilities are advancing at a 4.22% CAGR between 2026-2031.

- By distribution channel, online sales commanded 59.10% share of the digital photo frame market in 2025 and are forecast to grow at 4.92% CAGR.

- By geography, North America led with 34.45% digital photo frame market share in 2025; Asia-Pacific is expected to post a 5.28% CAGR and remain the fastest-growing region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Photo Frame Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing smart-home device penetration | +0.8% | Global; strongest in North America and the EU | Medium term (2-4 years) |

| Expansion of Wi-Fi/cloud ecosystems | +0.6% | Global; Asia-Pacific core with spill-over to MEA | Long term (≥ 4 years) |

| Demand for personalised digital wall-art and décor | +0.4% | Primarily North America and the EU | Short term (≤ 2 years) |

| Senior-care memory-support use cases | +0.3% | Global; early gains in North America and Japan | Medium term (2-4 years) |

| NFT and digital-art monetisation | +0.2% | North America and EU; selective Asia-Pacific markets | Long term (≥ 4 years) |

| Battery-powered e-ink technology advancements | +0.2% | Global; initial traction in premium EU and US households | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Smart-Home Device Penetration

Smart-home adoption transforms frames from single-purpose objects to connected nodes in household ecosystems. Samsung’s 2025 Vision AI platform integrates content curation, voice and gesture control, positioning frames as intelligent companions rather than passive displays.[1]Samsung Electronics, “The Frame Art Store Adds 2,000 Masterpieces,” samsung.com Voice assistants such as Amazon Alexa and Google Assistant enable hands-free operation, while occupancy sensors manage power use to improve energy efficiency. These capabilities raise switching costs for consumers already invested in broader smart-home setups, reinforcing demand within the digital photo frame market.

Expansion of Wi-Fi/Cloud Ecosystems Around Photo Storage and Sharing

Cloud connectivity reshapes purchase criteria as users prioritize effortless syncing across Google Photos, Apple iCloud and social platforms. Aura maintains subscription-free auto-sync to differentiate on total cost of ownership, whereas Nixplay’s transition toward paid tiers illustrates revenue diversification pressures. As families spread geographically, remote upload capabilities become a core expectation, elevating the importance of robust backend infrastructure and data privacy assurances within the digital photo frame market.[2]Aura Frames, “How Aura Syncs with Google Photos,” auraframes.com

Demand for Personalised, Digital Wall-Art and Décor

Frames increasingly double as rotating art canvases. Samsung’s Art Store gives owners access to curated galleries, enabling the device to blend into interior design schemes. Anti-glare coatings, swappable bezels and flush-mount kits address aesthetic requirements, while e-ink prototypes deliver battery life measured in years, freeing placement from power-outlet constraints. Premium styling encourages higher ASPs that support manufacturer margins despite component cost pressure.

Senior-Care Memory-Support Use Cases

Healthcare facilities deploy connected frames to assist dementia and Alzheimer’s patients, using loops of family photos and familiar scenery to trigger recognition and emotional comfort. MindCare Store reports rising bulk-order enquiries from senior-living operators seeking central management dashboards for simultaneous content updates.[3]MindCare Store, “Digital Frames for Memory Care Facilities,” mindcarestore.com Simplified touch interfaces and large text overlays cater to declining vision and dexterity, broadening the addressable base for the digital photo frame market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from smartphones and tablets | −0.5% | Global | Short term (≤ 2 years) |

| Rapid price erosion and margin squeeze | −0.4% | Global; Asia-Pacific manufacturing pressure | Medium term (2-4 years) |

| Tightening e-waste/circular-economy regulation | −0.2% | EU primarily; expanding globally | Long term (≥ 4 years) |

| Privacy compliance hurdles for cloud-linked frames | −0.1% | EU; spill-over to worldwide standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Smartphones and Tablets

Feature-rich phones and tablets provide high-resolution screens, cloud sync and broad app ecosystems, reducing incremental value for dedicated frames. Multi-function devices appeal to space-constrained households, leading many first-time buyers to forgo frame purchases entirely. Vendors counter by highlighting always-on display modes, hassle-free photo rotation and elderly-friendly controls that mobile hardware cannot fully replicate.

Rapid Price Erosion and Margin Squeeze

Chinese OEMs offer 8-inch Wi-Fi models at factory prices as low as USD 25, pressuring branded vendors to differentiate through software, design and support. Ongoing LCD panel tightness compounds cost volatility, while aggressive online discounting compresses retail margins further. Premium players such as Aura defend price points via build quality and ad-free cloud services but face an expanding value gap compared with budget alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Connectivity Drives Differentiation

Wi-Fi/cloud models command premium pricing but only 41.95% volume in 2025, yet they are set to post a 5.55% CAGR, the fastest within the digital photo frame market. Bluetooth-only versions remain volume leaders because their lower BOM supports entry-level price tags, sustaining a 58.05% share in 2025. Consumers gradually migrate to seamless auto-sync, face recognition and remote sharing, prompting vendors to bundle lifetime cloud storage to secure recurring engagement. As a result, manufacturers expect the Wi-Fi cohort to contribute more than half of the digital photo frame market size by 2031.

Hardware-plus-software bundling is central to long-term profitability. Aura’s 2024 revenue of USD 21.3 million reflects traction from a subscription-free model, while Nixplay’s paywall controversy shows the risk of altering terms post-purchase. Successful entrants court developers via open APIs that let third-party apps push images, calendars and ambient data, creating stickiness that restricts substitution by multifunction displays.

By Screen Size: Mid-Range Dominance with Premium Growth

The 7-inch–10-inch bracket delivered 55.05% of 2025 revenue and remains the workhorse for mainstream households thanks to balanced visibility, footprint and price. Compact sub-7-inch frames are forecast to grow at 4.05% CAGR, supported by gifting occasions, desk placements and dorm use. Meanwhile, the above-10-inch group attracts décor enthusiasts and commercial buyers who value statement pieces; these units increasingly use matte-finish quantum-dot or e-ink panels that mimic paper texture.

Retail data illustrate consumers’ evolving willingness to invest in larger canvases once basic needs are met. Samsung’s Frame Pro line, available in 43-inch and 55-inch variants, signals a high-margin niche that pairs with curated art subscriptions. Given premium elasticity, large-format models are projected to account for USD 17.55 billion of the digital photo frame market size by 2031.

By Application: Healthcare Emerges as Growth Driver

Residential installations continue to dominate with 64.30% share, underscoring frames’ emotional role in family storytelling. Yet senior-care and hospital deployments will record the fastest 4.22% CAGR, encouraged by clinical studies linking visual reminiscence therapy to reduced agitation among dementia patients. Operators value centralized content control and medical-grade wipe-clean enclosures, attributes now standard on commercial SKU roadmaps.

Retail and hospitality segments use frames for low-cost dynamic signage, menu boards and brand storytelling. Corporate offices display employee spotlights and KPI dashboards, turning idle walls into real-time communication assets. Education trials show promise for digital honor-roll boards and art showcases that replace paper posters, broadening the opportunity set for the digital photo frame market.

By Distribution Channel: Online Supremacy Accelerates

E-commerce captured 59.10% share in 2025, propelled by easy specification comparison, aggressive flash sales and integrated warranty registration. Marketplace algorithms reward high-velocity SKUs, compelling brands to optimize keywords, bundle accessories and finance sponsored listings. The shift also simplifies alignment between hardware sales and cloud-service upgrades, letting vendors upsell storage tiers at checkout.

Brick-and-mortar remains useful for product-in-hand evaluation, especially during Q4 gifting peaks, but showroom floors increasingly serve demonstration rather than inventory purposes. Retailers mitigate risk by partnering with drop-ship programs that pass fulfillment to brand warehouses. This hybrid strategy keeps frames visible to casual shoppers while acknowledging that final purchases—and subscription sign-ups—primarily occur online, reinforcing channel concentration within the digital photo frame market.

Geography Analysis

North America held 34.45% share in 2025 as early smart-home adopters embraced cloud features. Continued replacement cycles hinge on incremental benefits such as AI auto-tagging, wider aspect ratios and sustainable materials. Privacy-minded consumers spur interest in on-device processing and domestic-region data hosting, shaping future SKU positioning.

Asia-Pacific 5.28% CAGR stems from rapid urban expansion and strong gifting cultures. Competitive local manufacturing slashes time-to-market for feature updates, letting regional brands undercut global rivals on price yet match connectivity. China’s export scale further influences component pricing worldwide, indirectly benefiting Asia-Pacific demand.

Europe confronts stricter data, repairability and recyclability obligations under Regulation 2024/1781, raising compliance investments. Manufacturers respond with modular boards and user-replaceable batteries to extend service life, aligning with circular-economy policy goals while maintaining premium aesthetics cherished in markets such as Germany, France and the UK.

Competitive Landscape

The market is moderately fragmented. Pure-play specialists such as Nixplay and Aura vie with diversified electronics giants like Samsung and Amazon that leverage cross-category ecosystems to bundle frame functionality with smart displays. Amazon’s November 2024 launch of the 21-inch Echo Show underscores convergence: one device spans photo display, streaming, videoconferencing and voice assistance, challenging single-function frames for living-room real estate.

Samsung counters with the Frame Pro line, adding Neo QLED panels, customizable bezels and Vision AI algorithms to curate both personal photos and licensed art. The company pairs hardware sales with Art Store subscriptions, creating annuity streams that mitigate hardware margin compression within the digital photo frame industry.

On the cost-focused end, dozens of Shenzhen OEMs iterate rapidly, introducing Wi-Fi 6, touch UI and matte coatings within months of concept. Their ability to supply private-label SKUs for global retailers intensifies price erosion. European boutique vendors differentiate via FSC-certified wood frames, EU-based cloud hosts and GDPR-aligned data policies, carving premium niches among privacy-conscious customers

Digital Photo Frame Industry Leaders

Nixplay

Aura Home Inc.

Skylight

Netgear Inc. (Meural)

Lenovo Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Aura introduced the Aspen frame, a 12-inch antiglare model priced at USD 229 that adds caption support and people search.

- March 2025: Nixplay faced a class-action lawsuit alleging unfair alteration of previously unlimited cloud storage commitments (court filing reference: US District Court, N.D. California, 3:25-cv-00428).

- January 2025: Samsung unveiled the Frame Pro at CES 2025, incorporating Neo QLED technology and Vision AI-powered content recommendations.

- November 2024: Amazon released the Echo Show 21, its largest smart display with a dedicated photo frame mode triggered by voice commands.

Global Digital Photo Frame Market Report Scope

A digital photo frame is an electronic device that showcases digital images in a frame-like format, akin to traditional photo frames. However, unlike their conventional counterparts that hold printed photographs, digital photo frames utilize an LCD or LED screen to present a sequence of digital images, frequently in a slideshow format. These frames support various digital photo formats, including JPEG, PNG, and GIF. Moreover, they can be updated through USB drives, memory cards, or wireless connections like Wi-Fi and Bluetooth.

The study tracks the revenue accrued through the sale of digital photo frame by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The digital photo frame market is segmented by application (residential, and commercial), distribution channel (online and offline), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Wi-Fi / Cloud-Connected Frames |

| Bluetooth-Enabled Frames |

| Non-Connected (USB / SD) Frames |

| Up to 7-inch |

| 7-inch - 10-inch |

| 10-inch - 15-inch |

| Above 15-inch |

| Residential | |

| Commercial | Retail and Hospitality |

| Corporate Offices | |

| Healthcare Facilities | |

| Education |

| Online |

| Offline |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Wi-Fi / Cloud-Connected Frames | ||

| Bluetooth-Enabled Frames | |||

| Non-Connected (USB / SD) Frames | |||

| By Screen Size | Up to 7-inch | ||

| 7-inch - 10-inch | |||

| 10-inch - 15-inch | |||

| Above 15-inch | |||

| By Application | Residential | ||

| Commercial | Retail and Hospitality | ||

| Corporate Offices | |||

| Healthcare Facilities | |||

| Education | |||

| By Distribution Channel | Online | ||

| Offline | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the digital photo frame market?

The digital photo frame market is valued at USD 55.16 billion in 2026 and is projected to reach USD 63.41 billion by 2031, growing at a 2.83% CAGR.

Which region is expanding fastest?

APAC exhibits the highest growth, with a forecast 5.28% CAGR through 2031 due to urbanization, rising incomes and competitive local manufacturing.

How large is the mid-size 7-inch–10-inch segment?

This size category captured 55.05% of digital photo frame market share in 2025, reflecting its balance of display area and affordability.

Why are Wi-Fi frames growing quickly?

Wi-Fi/cloud connectivity eliminates manual photo transfers, enables remote family sharing and supports AI-based curation, resulting in a 5.55% projected CAGR for these models.

Page last updated on: