Wearable And Body-worn Cameras Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

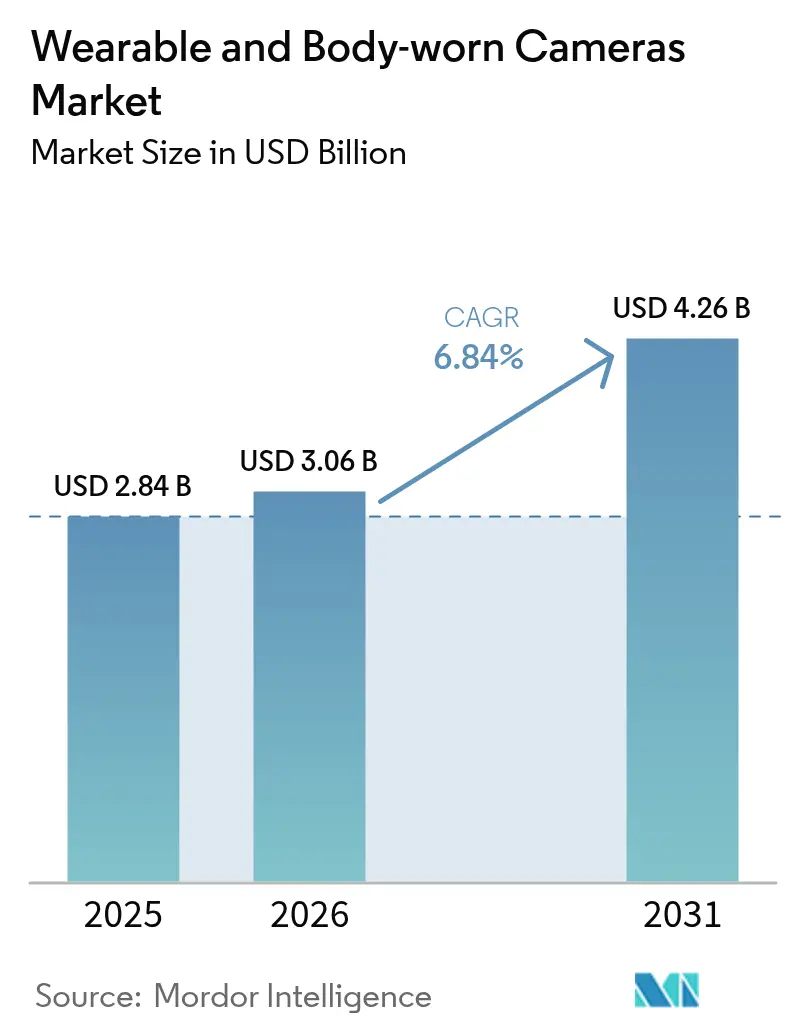

| Market Size (2026) | USD 3.06 Billion |

| Market Size (2031) | USD 4.26 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wearable And Body-worn Cameras Market Analysis by Mordor Intelligence

The wearable and body-worn cameras market size was valued at USD 2.84 billion in 2025 and estimated to grow from USD 3.06 billion in 2026 to reach USD 4.26 billion by 2031, at a CAGR of 6.84% during the forecast period. Accelerating statutory mandates, a shift toward subscription-based evidence-management ecosystems, and falling component prices are moving the wearable and body-worn cameras market from discretionary to must-have spending for public-sector agencies. State-level grants in the United States, large-scale police modernization budgets in India, and a surge in industrial safety deployments collectively expand total addressable demand, while edge AI accelerators embedded in next-generation devices unlock new use cases such as real-time redaction. Form-factor innovation is broadening adoption beyond patrol officers, as lightweight eyewear and clip-on models attract healthcare and manufacturing users. However, privacy frameworks such as GDPR and California’s Consumer Privacy Act inject region-specific compliance costs that slow uptake in Europe and parts of North America.

Key Report Takeaways

- By product type, body-worn cameras accounted for 62.31% of wearable and body-worn cameras market share in 2025, whereas eyewear cameras are projected to expand at a 7.01% CAGR through 2031.

- By resolution, Full HD devices led shipments with 47.82% share in 2025; 4K and above units represent the fastest-growing tier, advancing at 9.21% CAGR over 2026-2031.

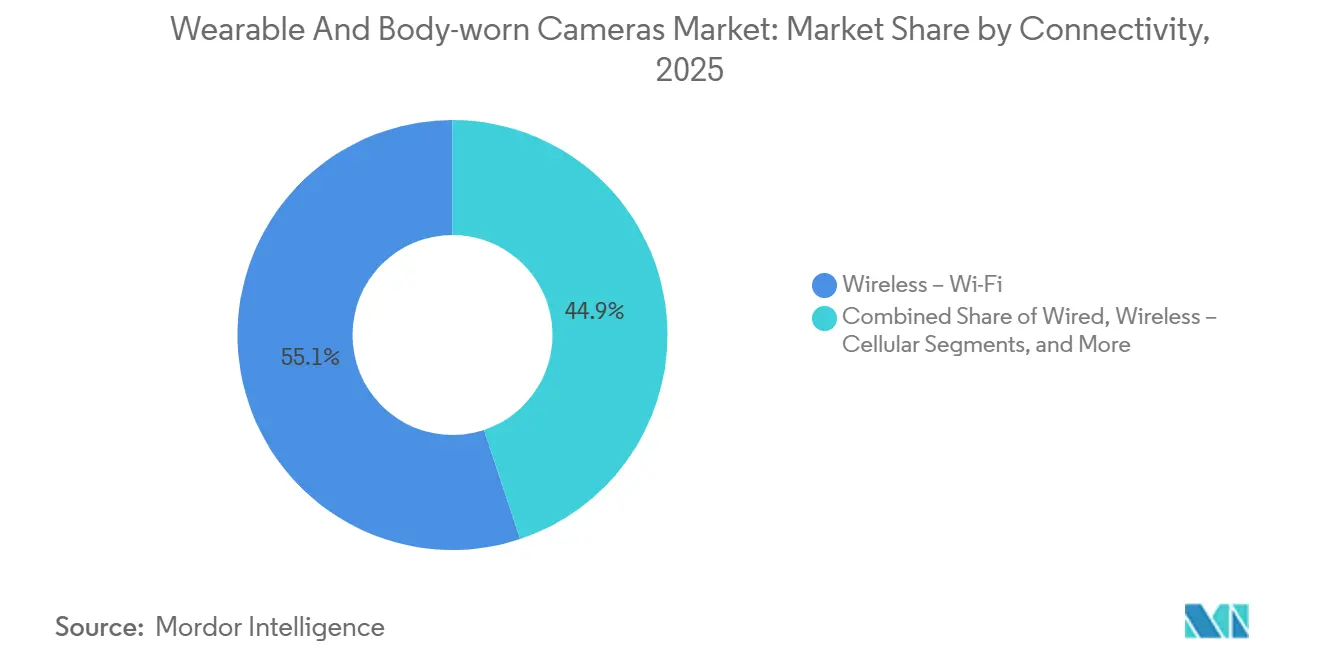

- By connectivity, Wi-Fi dominated with 55.11% share in 2025, while 5G cellular streaming is forecast to post an 8.34% CAGR through 2031.

- By end user, law-enforcement and public safety commanded 68.54% of demand in 2025; healthcare and telemedicine applications are poised for the quickest expansion at 6.96% CAGR to 2031.

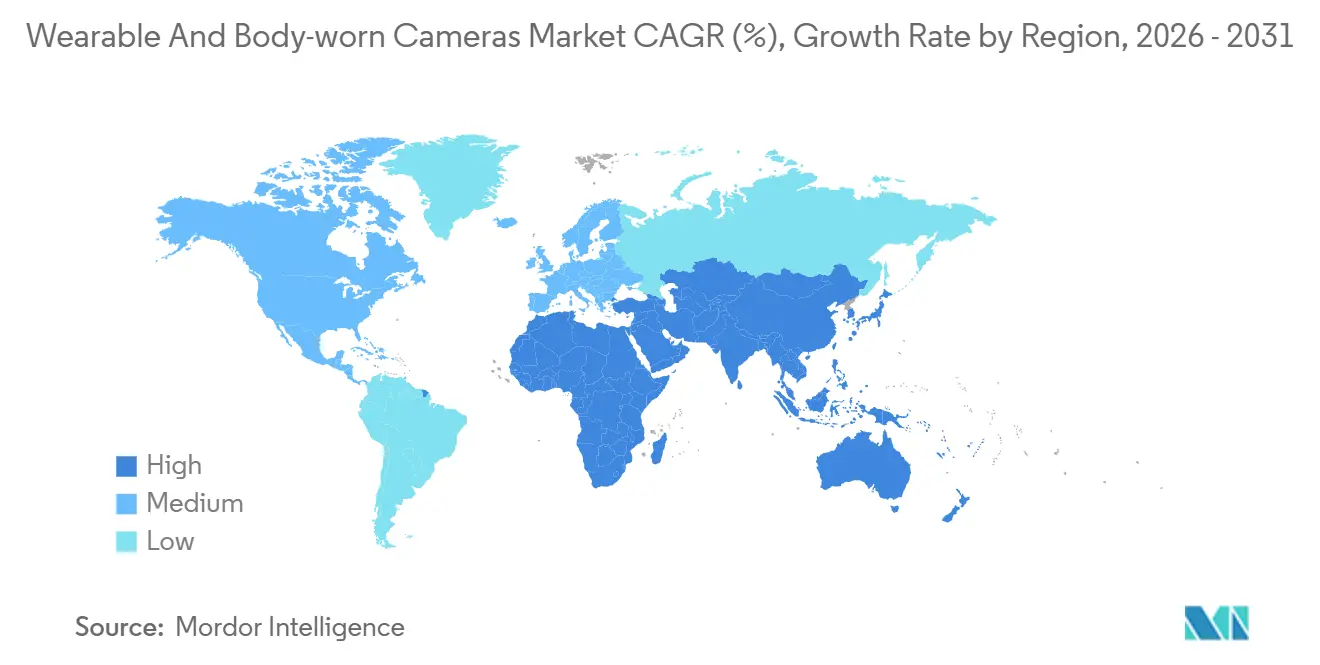

- By geography, North America contributed 38.24% of the 2025 revenue base, yet Asia-Pacific is set to grow the fastest at a 9.93% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wearable And Body-worn Cameras Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated Adoption by Law-Enforcement Agencies | +2.1% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Rising Demand for Accountability and Transparency | +1.8% | Global | Short term (≤ 2 years) |

| Decreasing Hardware and Cloud-Storage Costs | +1.3% | Global | Long term (≥ 4 years) |

| Industrial Safety and Worker-Training Adoption | +0.9% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Edge-AI Co-Processors Enabling On-Device Redaction | +0.7% | GDPR compliance zones | Long term (≥ 4 years) |

| Integration With Digital Evidence-Management Ecosystems | +0.6% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Mandated Adoption by Law-Enforcement Agencies

Legislative mandates are recasting body-worn cameras as compulsory capital equipment, guaranteeing multi-year refresh cycles and predictable revenue streams. Illinois earmarked USD 56 million in 2025 for agencies that pair cameras with compliant evidence-management software, and comparable grant pools in Ohio, Virginia, and Texas replicate this linkage of hardware to cloud ecosystems.[1]Illinois Criminal Justice Information Authority, “Body-Worn Camera Grant Program Announced,” icjia.illinois.gov India’s Ministry of Home Affairs likewise instructed state forces to prioritize procurement, accelerating deployments of more than 12,000 units in 2025 alone. Replacement periods of three to five years embed recurring opportunities for vendors that bundle cameras with annual service contracts.

Rising Demand for Accountability and Transparency

Public scrutiny is turning cameras into symbols of procedural justice, spurring adoption even where statutes lag. A 2025 Police Executive Research Forum study reported 23% fewer use-of-force complaints in departments with full-fleet coverage.[2]Police Executive Research Forum, “Ten Years of Body-Worn Camera Deployment Review,” policeforum.org Oversight boards now audit activation compliance, and civil-rights litigation routinely cites video evidence as proof of transparency, accelerating decision cycles for hesitant municipalities. Healthcare institutions have mirrored this logic; peer-reviewed work showed a 47% drop in emergency-department violence after camera rollouts, validating use outside policing.

Decreasing Hardware and Cloud-Storage Costs

Smartphone-driven sensor commoditization and hyperscale cloud competition have lowered entry prices to USD 400–600 per unit under subscription models, compared with USD 800–1,200 for legacy one-time purchases. Service contracts that bundle storage and AI redaction spread costs over five years, expanding affordability for smaller agencies and for industrial buyers who lack public-sector grants. Open-source evidence platforms gaining traction in Asia-Pacific further squeeze total cost of ownership, though they often omit advanced analytics demanded by larger forces.

Industrial Safety and Worker-Training Adoption

Manufacturing, construction, and utilities are embracing cameras to audit procedures, confirm training, and reconstruct incidents, creating a parallel channel disconnected from law-enforcement cycles. Motorola’s intrinsically safe VB400 and Axon’s lightweight Body Workforce Mini cater to ergonomics and hazardous-area certifications, while insurers now discount premiums 5–10% for companies with comprehensive video programs. With an estimated 12 million frontline workers in North America alone, the industrial safety segment represents a sizeable expansion vector for the wearable and body-worn cameras market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and Data-Protection Regulations | -1.4% | Europe, North America | Short term (≤ 2 years) |

| High Bandwidth and Storage Requirements | -0.9% | Global | Medium term (2–4 years) |

| Fragmented Regional Certification Standards | -0.5% | Asia-Pacific, Middle East | Long term (≥ 4 years) |

| Lithium-Polymer Swell Limiting Multi-Shift Deployment | -0.4% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Privacy and Data-Protection Regulations

GDPR, CCPA, and emerging state laws impose divergent retention and disclosure rules that push agencies to adopt selective-recording protocols, increase administrative paperwork, and invest in costly redaction workflows. Continuous recording was deemed disproportionate by the European Court of Justice in 2025, obligating departments to prove necessity for each activation scenario. California’s 2026 amendments also grant individuals deletion rights, forcing manual review processes that heighten operational overhead.[3]California Attorney General, “Consumer Privacy Act Amendments,” oag.ca.gov

High Bandwidth and Storage Requirements

Each 4K camera produces 12 GB per shift, driving annual per-device storage to 4.4 TB and straining cloud budgets with egress fees of USD 0.09–0.12 per GB. Rural agencies lack 5G coverage, negating live-streaming benefits and relegating uploads to end-of-shift Wi-Fi, while compression trade-offs erode image quality vital for AI analytics. Developing regions with average download speeds below 20 Mbps confront even starker hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Dominance With Eyewear Momentum

The wearable and body-worn cameras market size for body-worn units reached USD 1.77 billion in 2025, translating to 62.31% of segment revenue, whereas eyewear offerings are projected to post the quickest 7.01% CAGR through 2031. Established mounting standards, ruggedness, and broad grant eligibility keep torso-mounted devices entrenched. Eyewear appeals to nurses, factory assemblers, and field technicians seeking hands-free line-of-sight capture. Hybrid models such as Motorola’s SVX, which merges camera and speaker-mic, point to a converging form-factor landscape that balances ergonomics with evidentiary chain-of-custody features.

Clip-on and accessory cameras widen access for cash-strapped departments because they retrofit existing uniforms, deferring wholesale kit replacement. Helmet-mounted variants stay niche in tactical and extreme-sports circles owing to weight distribution challenges. Continued miniaturization and consumer-electronics aesthetics will help eyewear rise, yet body-worn cameras will likely hold the majority of wearable and body-worn cameras market share until at least 2028 given entrenched procurement cycles.

By Resolution: AI Push Forces 4K Uptick

Full HD captured 47.82% of 2025 unit shipments, but agencies are fast pivoting toward 4K to satisfy AI facial-recognition thresholds that demand 120–150 pixels across a face, boosting operating distance to 40 feet.[4]National Institute of Standards and Technology, “Facial Recognition Performance Standards,” nist.gov The wearable and body-worn cameras market size for 4K devices is forecast to triple by 2031 as H.265 compression and falling NAND-flash prices temper storage inflation. Hytera’s SC880 showcases 10-hour battery endurance at 4K/5G settings, mitigating power-drain objections that dogged earlier UHD prototypes.

Legacy 720p fleets are approaching obsolescence, prompting refreshes that default to 1080p or 4K. Courts increasingly dispute sub-HD footage for evidentiary clarity, compelling agencies to future-proof with higher pixel densities. Vendors offering seamless down-sampling for archival storage without losing courtroom admissibility will secure a competitive advantage.

By Connectivity: Wi-Fi Foundations, 5G Futures

Wi-Fi dominated with a 55.11% share, accounting for more than half of shipments in 2025, thanks to zero-cost LAN uploads and institutional familiarity. While 5G cellular streaming is forecast to post an 8.34% CAGR through 2031. Still, 5G stands to redefine situational awareness as latency drops below 200 milliseconds, enabling command centers to intervene during unfolding events. The wearable and body-worn cameras market size for cellular-enabled models is projected to reach USD 1.48 billion by 2031, spurred by flat-rate law-enforcement data plans priced at USD 25–35 per line. Dual-mode radios that shift among 5G, 4G, and Wi-Fi offer continuity in patchy coverage zones.

For correctional or high-security installations, wired docks persist to isolate sensitive video from external networks. Bluetooth remains auxiliary for configuration rather than bulk transfer. Vendors are packaging SIM-agnostic eSIM modules to curb carrier lock-in, an appealing feature for agencies combining urban 5G with remote Wi-Fi backhauls.

By End User: Public Safety Core, Healthcare Upswing

Law-enforcement’s 68.54% revenue contribution underscores its anchor role, yet healthcare’s 6.96% forecast CAGR signals diversification momentum. Hospitals view cameras as de-escalation and litigation-defense tools BMC Emergency Medicine documented a 47% violence reduction after deployment. Industrial safety initiatives, buoyed by insurer incentives, now account for a growing tranche of the wearable and body-worn cameras industry, while consumer adventure filming remains an enthusiasm segment served mainly by action-camera incumbents.

Military programs prioritize secure encryption and tamper detection for battlefield after-action review but face budget competition from drones and cyber-defense assets. Sports officiating and coaching represent emergent micro-niches where ultra-wide-angle optics support performance analytics, though gross revenue impact is modest relative to policing and healthcare.

Geography Analysis

North America underpinned 38.24% of global revenue in 2025 as mature replacement cycles intersected with new 5G streaming pilot programs spanning federal to county levels. Agencies benefit from grant pipelines that transition cameras from discretionary capital to fixed budget lines. The wearable and body-worn cameras market size for Asia-Pacific is set to rise fastest, advancing at 9.93% CAGR as India’s INR 500 crore modernization fund catalyzes multi-state procurements and China fuses AI recognition layers onto hardware showcased at 2025 security forums.

Europe’s trajectory is moderated by stringent GDPR compliance demands that favor premium models with on-device redaction, sustaining higher average selling prices but slowing unit volumes. Selective-activation mandates stemming from the 2025 European Court ruling compel workflow overhauls that temporarily defer purchases until policies mature. Secondary sales of refurbished units from U.S. agencies increasingly feed Latin American and African demand where budgets constrain new-equipment buys.

Asia-Pacific’s fragmented supplier base sees local makers such as Hytera capturing municipal contracts through 30-40% lower pricing compared with Western brands, while NDAA clauses steer U.S. federal procurement toward Korean and Japanese vendors. In Australia and New Zealand, officer-assault concerns are building political momentum for nationwide camera strategies, albeit from a low installed base. Middle-East projects concentrate in high-density urban corridors where smart-city funding umbrellas body-worn rollout under broader public-safety initiatives.

Competitive Landscape

The wearable and body-worn cameras industry displays moderate concentration. Axon Enterprise and Motorola Solutions jointly hold major share of U.S. law-enforcement procurement, yet their grip loosens in Asia-Pacific and verticals such as industrial safety where local compliance knowledge trumps ecosystem lock-in. Axon’s USD 213 million cloud-and-services quarter in 2024 underscores the stickiness of subscription models that levy USD 15–25 monthly per device and finance ongoing R&D.

Motorola’s strategy links cameras with radios and command-center analytics, evidenced by the 2025 SVX launch blending video capture and speaker-mic into one intrinsically safe unit. Panasonic i-PRO differentiates on 12-hour field-swappable batteries and GDPR-oriented workflows that appeal to European constabularies. New entrants focus on edge AI; Getac-Veritone’s 15-minute automated redaction tackles a pressing compliance choke point, while smaller vendors attack price-sensitive industrial niches with ruggedized, minimal-feature cameras at sub-USD 300 price tags.

GoPro is repurposing its consumer heritage for enterprise training and sports officiating, augmenting its Hero line with magnetic mounts and HDR capture suitable for motion analysis. Certification regimes such as NDAA continue to reshape sourcing, excluding Chinese-origin components from U.S. federal bids and rewarding alternative Asian supply chains. Battery chemistry and life cycle endure as differentiation arenas, with Motorola touting 18-hour performance from a 2,925 mAh pack, while Panasonic offers quick-swap modules that sustain triple-shift coverage without mid-tour recharge.

Wearable And Body-worn Cameras Industry Leaders

Axon Enterprise Inc.

Motorola Solutions Inc. (WatchGuard)

Digital Ally Inc.

Panasonic i-PRO Sensing Solutions Co., Ltd.

GoPro Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Axon and Microsoft Azure integrated generative-AI evidence summarization into Evidence.com, trimming report-writing time by 30%.

- January 2026: The U.K. Home Office allocated GBP 15 million to extend body-worn cameras across 20 rural forces, bundling five-year cloud storage into the grants.

- December 2025: Motorola Solutions secured a USD 28 million contract to supply 7,000 VB400 5G cameras to the Los Angeles Police Department with seven-year evidence-library services.

- November 2025: Panasonic i-PRO unveiled its Unified Evidence Platform in Europe, enabling synchronized multi-angle case files with automated GDPR redaction.

Global Wearable And Body-worn Cameras Market Report Scope

The wearable and body-worn cameras market has witnessed significant growth in recent years, driven by increasing demand across various end-user industries such as law enforcement, healthcare, and sports. These devices are gaining traction due to their ability to provide real-time data, enhance operational efficiency, and improve safety and accountability. The market is expected to continue its upward trajectory over the forecast period, supported by technological advancements and growing adoption in emerging regions.

The Wearable and Body-Worn Cameras Market Report is Segmented by Product Type (Body-worn, Head/Helmet-mounted, Eyewear, Clip-on), Resolution (HD, Full HD, 4K and Above), Connectivity (Wired, Wi-Fi, Cellular, Bluetooth), End User (Law-enforcement, Military, Sports, Healthcare, Industrial, Consumer), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Body-worn Cameras |

| Head/Helmet-mounted Cameras |

| Eyewear Cameras |

| Clip-on and Accessory Cameras |

| HD (720p) |

| Full HD (1080p) |

| 4K and Above |

| Wired |

| Wireless - Wi-Fi |

| Wireless - Cellular |

| Wireless - Bluetooth |

| Law-enforcement and Public Safety |

| Military and Defense |

| Sports and Adventure |

| Healthcare and Tele-medicine |

| Industrial and Commercial Workforce |

| Consumer / Personal |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Product Type | Body-worn Cameras | |

| Head/Helmet-mounted Cameras | ||

| Eyewear Cameras | ||

| Clip-on and Accessory Cameras | ||

| By Resolution | HD (720p) | |

| Full HD (1080p) | ||

| 4K and Above | ||

| By Connectivity | Wired | |

| Wireless - Wi-Fi | ||

| Wireless - Cellular | ||

| Wireless - Bluetooth | ||

| By End User | Law-enforcement and Public Safety | |

| Military and Defense | ||

| Sports and Adventure | ||

| Healthcare and Tele-medicine | ||

| Industrial and Commercial Workforce | ||

| Consumer / Personal | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the estimated size of the wearable and body-worn cameras market in 2026 and its expected value by 2031?

It is valued at USD 3.06 billion in 2026 and projected to climb to USD 4.26 billion by 2031, reflecting a 6.84% CAGR.

Which geographic region is forecast to deliver the quickest revenue growth through 2031?

Asia-Pacific is set to advance at a 9.93% CAGR, outpacing all other regions.

What core factors are driving large-scale adoption among police agencies?

Statutory mandates that tie grant funding to camera deployment and evidence-management integration, coupled with public demand for accountability and transparency.

How are hospitals and clinics benefiting from body-worn cameras?

Facilities use the devices to de-escalate confrontations and document care, with peer-reviewed research showing a 47% drop in emergency-department violence after rollout.

Which technology trend is helping agencies cut privacy-compliance workloads?

Cameras equipped with edge-based AI now perform real-time face and license-plate redaction, trimming processing time from hours to minutes.

Who currently leads North American procurement for professional body-worn cameras?

Axon Enterprise and Motorola Solutions together account for roughly 60% of law-enforcement purchases in the region.

Page last updated on: