Die Casting Machinery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.06 Billion |

| Market Size (2031) | USD 5.46 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

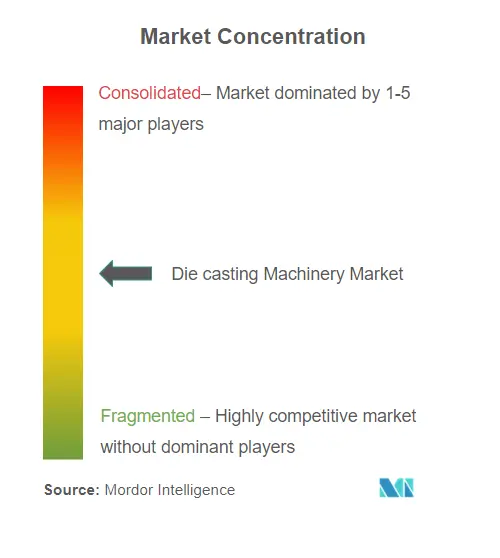

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Die Casting Machinery Market Analysis by Mordor Intelligence

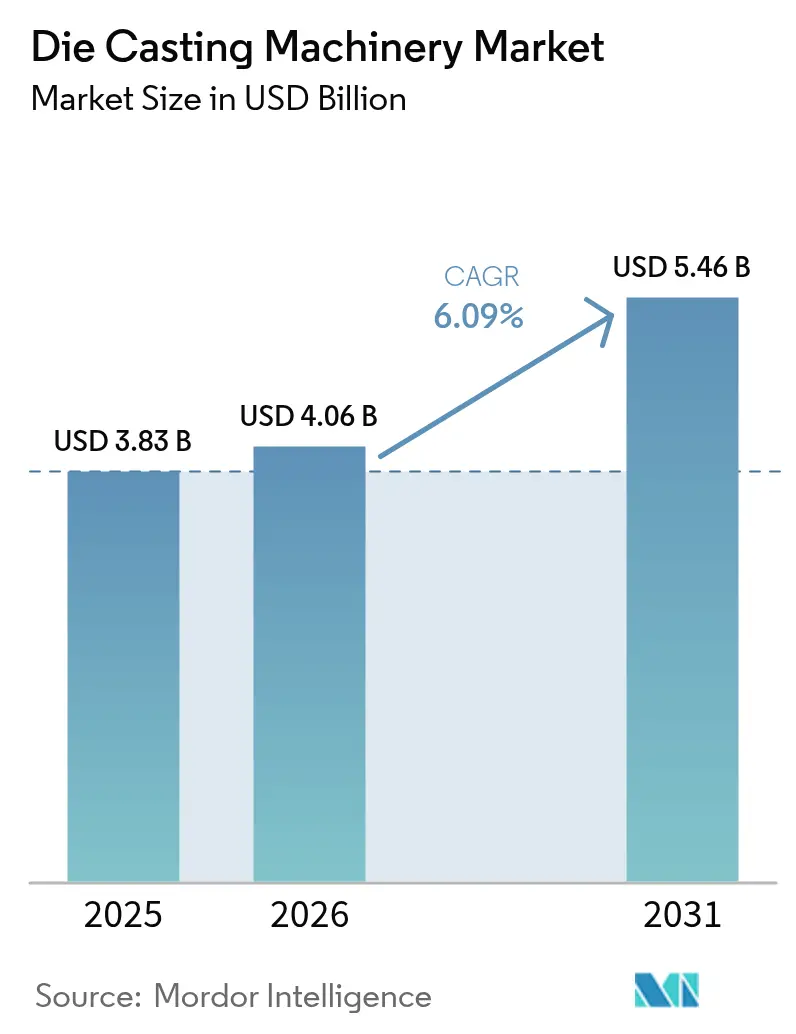

The die casting machinery market size is expected to grow from USD 3.83 billion in 2025 to USD 4.06 billion in 2026 and is forecast to reach USD 5.46 billion by 2031 at 6.09% CAGR over 2026-2031. Intense equipment replacement cycles, electric-vehicle (EV) platform redesigns, and electronics miniaturization are steering procurement budgets toward high-tonnage presses, hot-chamber machines, and fully automated cells. Structural giga-casting emerged as a game-changer in manufacturing, creating a premium segment. By leveraging large-scale presses, this innovation minimizes the reliance on welding, speeding up final assembly and bolstering structural integrity. Such enhancements are desirable for high-performance applications. Simultaneously, as semiconductor packaging evolves and 5G infrastructure expands, there's a surging demand for compact, high-precision casting cells. Typically employing zinc and magnesium, these systems are meticulously designed to uphold tight tolerances, catering to the sophisticated needs of contemporary electronics. Smart factory upgrades are becoming increasingly prevalent in the die-casting industry. These enhancements not only facilitate predictive defect detection but also bolster energy efficiency, underscoring a significant digital transformation on the foundry floor. As a result, manufacturers are leveraging these technologies to enhance quality control and promote operational sustainability. While the Asia-Pacific region remains the cornerstone of global production, the Middle East and Africa are witnessing a meteoric rise. With diversification efforts in full swing, these regions are not only developing new manufacturing capacities but are also establishing a notable presence in the global die casting arena.

Key Report Takeaways

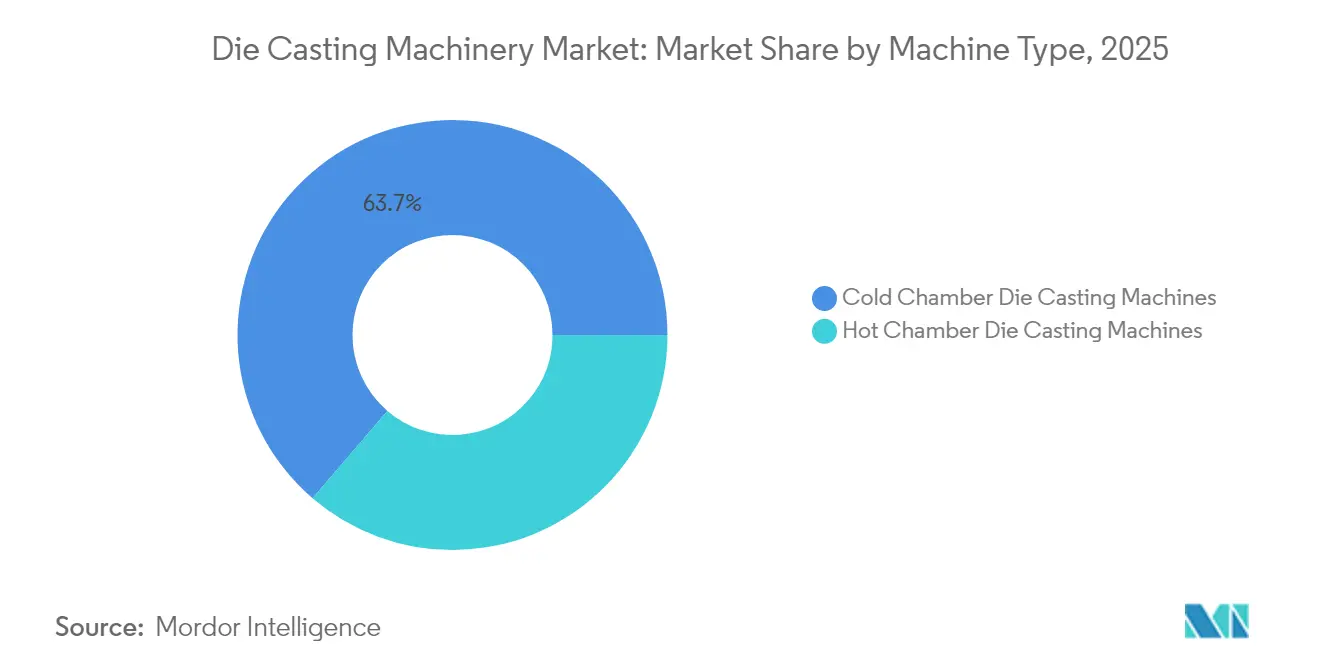

- By machine type, cold-chamber equipment held 63.72% of the die casting machinery market share in 2025, while hot-chamber units are projected to register a 6.58% CAGR to 2031.

- By material, aluminum accounted for 72.75% of the die casting machinery market size in 2025, with magnesium poised to advance at a 7.42% CAGR through 2031.

- By end-user, automotive applications led with a 53.65% share in 2025; the aerospace sector is forecast to grow at a 7.11% CAGR between 2026 and 2031.

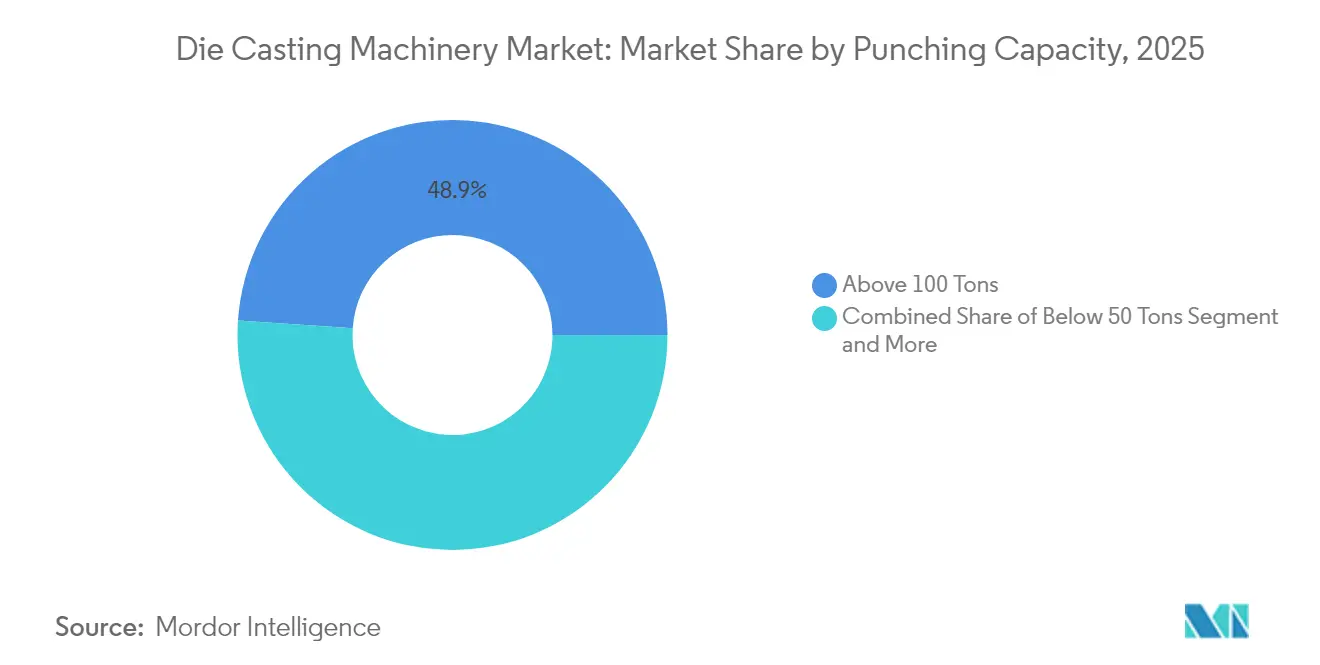

- By punching capacity, presses above 100 tons captured a 48.93% share in 2025, whereas sub-50-ton machines are expected to log a 7.63% CAGR to 2031.

- By automation level, semi-automated cells represented a 45.05% share in 2025, and fully automated lines are expected to grow at an 8.02% CAGR through 2031.

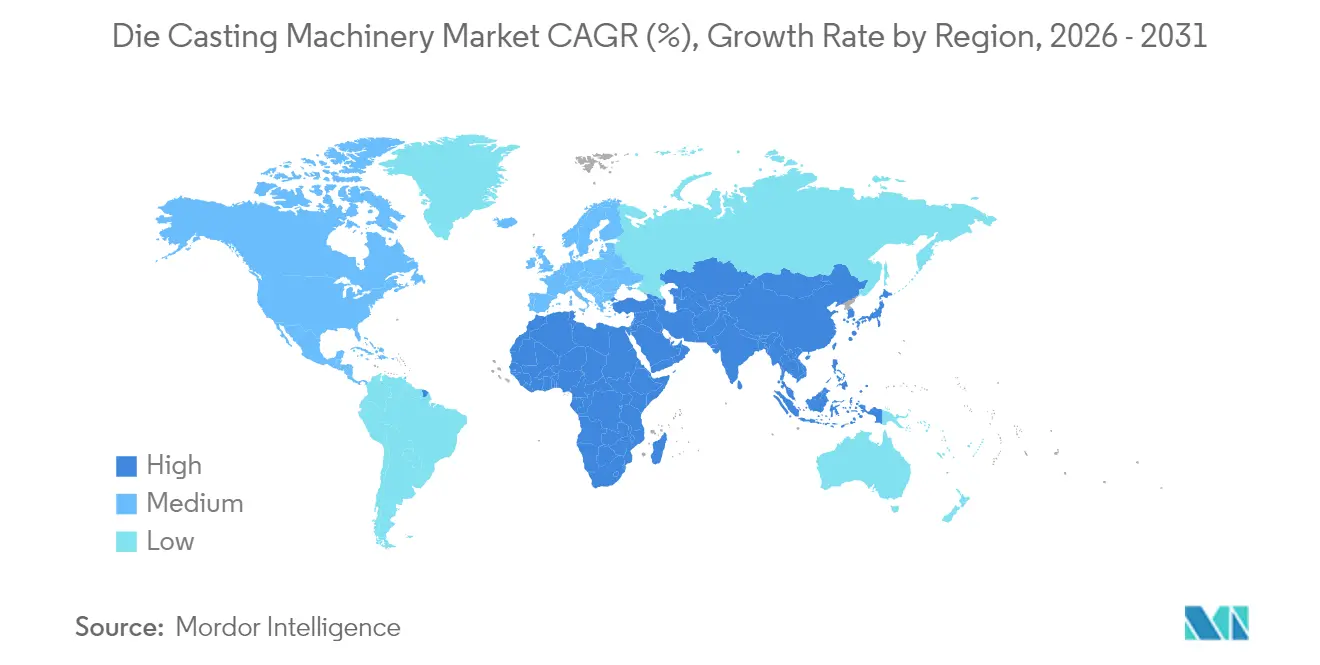

- By geography, Asia-Pacific commanded 46.55% of the die casting machinery market share in 2025, while the Middle East and Africa region is projected to grow at a 7.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Die Casting Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Mega/Giga-Casting Surge | +2.1% | Global, strongest in China, Europe, North America | Medium term (2-4 years) |

| Hot-Chamber Demand from Miniaturization | +1.3% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Industry 4.0 Press Retrofits | +0.9% | Europe, North America, advanced Asia-Pacific markets | Long term (≥ 4 years) |

| EU BAT-2024 Energy Upgrades | +0.7% | Europe, regulatory influence spreading globally | Medium term (2-4 years) |

| Rheocasting Retrofit Kits | +0.6% | Global, concentrated in automotive hubs | Long term (≥ 4 years) |

| 3D-Printed Conformal Dies | +0.5% | North America, Europe, advanced manufacturing hubs | Long te |

| Source: Mordor Intelligence | |||

EV-Led Mega-/Giga-Casting Demand Surge

High-tonnage presses produce single-piece rear underbody castings, replacing multiple components and streamlining production. Tesla’s program success encouraged Ford, Volvo, and GM to commit to structural architectures that depend on giga-press supplies throughout the vehicle lifecycle. Chinese OEMs such as Wanfeng Aowe are expanding magnesium mega-cast trials, aiming to capitalize on chassis-integrated battery packs. As competition intensifies, the die casting machinery market is bifurcating into two distinct segments: conventional mid-tonnage lines and high-investment giga-press setups, which are tailored for significant structural components. Demand visibility extends beyond 2030 as battery-to-chassis integration becomes a design standard, ensuring multi-plant investment waves across three continents[1]“Tesla Giga-Press Supply Chain Insights,”, SMM News Center, smm.cn.

Electronics Miniaturization Boosting Hot-Chamber Demand

As semiconductor packaging evolves, the demand for precise die casting solutions surges. With bump pitches tightening, there's a heightened demand for casings and heat-spreaders that boast tight machining tolerances. To meet these exacting standards, fast-cycle hot-chamber systems, particularly those utilizing zinc and magnesium, are gaining traction. Foundries supporting major players like TSMC and Intel are adopting multi-slide casting cells, which offer superior melt temperature control and rapid cycle times to meet the needs of modern electronics manufacturing. In 5G infrastructure, large-scale magnesium casting lines are supplying lightweight components, such as antenna housings, which reinforces the case for hot-chamber casting technologies. Emerging applications in diamond semiconductors and quantum computing are expected to demand advanced thermal management, further solidifying the relevance of hot-chamber systems. Their quick adaptability to various product types makes them ideal for high-mix production environments that require flexibility and precision.

Industry 4.0 Retrofits Replacing Legacy Presses

AI and innovative technologies are transforming the die casting sector. AI-supervised furnaces and advanced shot monitoring systems improve defect prediction, enhancing quality assurance. In Japan, retrofitting cold-chamber lines with IoT sensors and predictive tools has boosted energy efficiency and reliability. Germany’s ReGAIN initiative utilizes multi-pressure monitoring and edge analytics to enhance throughput and minimize material waste in gravity, sand, and die casting processes. Blockchain-ready quality records simplify compliance, enable real-time traceability, and ease audits. These systems handle high-volume operations while maintaining performance. Collectively, these innovations shift the industry from a hardware-focused to a data-driven approach, enabling more intelligent decisions, increased production agility, and enhanced sustainability globally.

EU BAT-2024 Compliance Driving Energy-Efficient Upgrades

Directive 2024/1244 obliges European foundries to disclose their metal emissions and energy use, starting with the 2027 reporting season[2]“Regulation 2024/1244 Industrial Emissions Portal,”, European Commission, europa.eu. To enhance sustainability and ensure compliance, facilities with high emissions must adopt advanced filtration systems, implement closed-loop cooling, and align their energy management frameworks with ISO 50001 standards. Public benchmarking spurs peer pressure, accelerating orders for presses with regenerative heating and real-time metering. New EU regulations, set to enforce substantial CO₂ reductions for heavy vehicles in the coming decade, are indirectly driving up the demand for magnesium and aluminum structural castings. Manufacturers are turning to these lighter components as they strive to meet compliance targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum/Magnesium Price Volatility | -1.4% | Global, especially emerging markets | Short term (≤ 2 years) |

| EUR 10m + Giga-Press CAPEX Barrier | -0.8% | Global, strongest impact on SME foundries | Medium term (2-4 years) |

| Grid Amperage Shortages | -0.6% | Africa, parts of Asia | Long term (≥ 4 years) |

| Premium Steel Supply Constraints | -0.4% | Global supply-chain risk | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aluminum and Magnesium Price Volatility

LME aluminum prices fluctuated between USD 2,100 and USD 2,400 per metric ton during 2024, while magnesium prices gyrated even more sharply due to heavy Chinese supply concentration[3]“Aluminum and Magnesium Price Volatility Report,”, SMM News Center, smm.cn. Raw materials, a significant cost component for finished components, are pressuring casting margins. Foundries are adopting hedging strategies to manage volatility. Despite higher production volumes, some manufacturers face revenue declines due to fluctuating input costs. Energy costs, particularly electricity for melt furnaces, have a significant impact on profitability. Price spikes lead to immediate financial strain. Foundries are using short-term measures, such as dual sourcing and alloy substitution, but these offer only temporary relief. Persistent cost instability is dampening investment in the die casting machinery market, with stakeholders adopting cautious approaches despite ongoing technological advancements.

Grid Amperage Deficits in Emerging Markets

High-tonnage presses draw significant peak loads, yet many African and South-Asian grids lack stable high-amp feeders. Brownouts risk scrap, tooling damage, and missed contractual delivery windows. Foundries fund private substations or gas-fired generators, inflating operating costs and adding carbon intensity. Policy programs are slowly reinforcing grids, but until upgrades arrive, large-press uptake in these regions remains limited, tempering die casting machinery market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Cold Chamber Dominance Drives Aluminum Processing

Cold-chamber units accounted for 63.72% of the die casting machinery market share in 2025, reflecting their suitability for high-temperature aluminum alloys. Hot-chamber machines, while smaller in installed base, are tracking a 6.58% CAGR as electronics contracts escalate. The die casting machinery market size attached to giga-press cold-chamber lines is growing as OEMs transition to single-piece EV body castings, driving the average tonnage upward. Integrated servo shot systems and closed-loop cooling now appear on both machine classes, signaling feature convergence.

In hot-chamber niches, zinc multi-slide platforms meet 30-second takt-time mandates for 5G radio casings, whereas magnesium systems win where weight trimming outranks corrosion concerns. Industry 4.0 modules retrofit across both types, collecting melt and plunger data for cloud analytics. Heat-recovery options and hybrid drive hydraulics cut power draw, improving total cost of ownership. As quality tolerance windows shrink, both machine types embrace inline X-ray and ultrasonic inspection to verify near-net geometry at the press exit. Dual-supplier sourcing strategies by OEMs sustain demand diversity across the die casting machinery market.

By Material Type: Aluminum Leadership Faces Magnesium Acceleration

Aluminum held a commanding 72.75% share of the 2025 die casting machinery market size due to its favorable strength-to-weight ratio for EV platforms. Magnesium, which is 35% lighter, is on track for a 7.42% CAGR through 2031 as telecom gear and laptop frames pursue weight savings. Automotive giga-casting still relies on aluminum for crash energy absorption, but interior brackets and steering wheels are increasingly being made from magnesium.

Zinc remains vital for intricately detailed hardware and MEMS housings, as it is favored for its dimensional stability at low cycle times. New alloy families, such as aluminum-scandium, improve weldability in battery enclosures, broadening the application scope. Volatility in base-metal pricing prompts users to blend alloys based on forward contracts, but performance needs increasingly trump cost factors for mission-critical parts. Continuous melt-quality monitoring facilitates switching between alloys without contaminating holding furnaces, a practice gaining traction across the die-casting machinery market.

By End-User Industry: Automotive Scale Meets Aerospace Momentum

The automotive sector accounts for a 53.65% share of the die casting machine 2025, underscoring its capacity for high-volume capital deployment. Battery packs, motor housings, and integrated chassis components anchor aluminum giga-casting orders. Aerospace is scaling at a 7.11% CAGR as carriers restore fleet expansion and OEMs chase fuel-burn savings with magnesium-lithium structures.

Electronics manufacturers are turning to ultra-fine components for devices ranging from smartphones and VR headsets to advanced cooling systems in quantum computing. Concurrently, buyers of industrial machinery are seeking large, sturdy castings for hydraulic bodies and wind-turbine hubs. Meanwhile, defense programs are delving into specialized heat sinks tailored for high-energy platforms. Cross-vertical technology transfer, such as automotive-derived giga-casting for aerospace wing ribs, is broadening the customer pool and cushioning cyclicality in the die casting machinery market.

By Punching Capacity: Large Capacity Prevalence Versus Small Capacity Growth

Presses exceeding 100 tons accounted for 48.93% of shipments in 2025, primarily serving the high-value automotive and industrial sectors. Sub-50-ton models, although smaller in revenue, are expected to achieve a 7.63% CAGR by 2031, driven by applications such as watch casings, medical implants, and MEMS housings that require micron-level repeatability.

Ultra-high-tonnage platforms are leading the shift towards single-piece vehicle structures. Meanwhile, compact modular die-casting rigs are becoming popular for prototyping and producing low-volume aerospace components. Supporting both ends of this spectrum, servo-electric shot systems offer precise speed control and lessen the dependence on hydraulic fluids. Additionally, lifecycle audits that monitor energy consumption per casting cycle are steering investment choices towards right-sizing, rather than a blanket trend of upsizing in the die-casting machinery market.

By Automation Level: Semi-Automated Present State Versus Full Automation Future

Semi-automated cells accounted for 45.05% of 2025 installations, striking a balance between operator oversight and robotic spraying and extraction. Fully automated lines are expected to deliver an 8.02% CAGR through 2031, as labor costs and uptime expectations continue to rise. AI vision now tags defects in-flight, instantly routing borderline parts to re-work.

Collaborative robots streamline die lube application, while automatic ladles sync with real-time melt-level data. Cybersecurity hardening becomes mandatory as plants integrate MES, ERP, and cloud analytics. Skill shortages press owners to retrain machinists into data technicians, a trend amplified by national upskilling grants. Manual stations persist in niche jewelry and artistic foundries but face gradual obsolescence within the die casting machinery market.

Geography Analysis

Asia-Pacific secured 46.55% of 2025 revenue, lifted by China’s cost-efficient supply chain and India’s ascending EV assembly footprint. Japanese firms sustain premium machine exports and diamond semiconductor research and development, undergirding regional innovation. South Korea’s packaging giants are reinforcing demand for hot-chamber equipment, while ASEAN nations are incubating contract manufacturing hubs for mid-capacity lines.

Europe’s growth rests on compliance-driven replacement as BAT-2024 forces energy-wasteful presses off the floor. Germany’s ReGAIN consortium serves as a pilot, merging AI assistants with low-carbon electricity contracts. Italy’s Lombardy cluster adopts conformal-cooling tooling at scale, while Nordic foundries push closed-loop water systems to align with strict emissions caps.

The Middle East and Africa, although still in its early stages in terms of absolute volume, is expected to record a 7.74% CAGR as economic diversification blueprints finance aluminum smelters, grid upgrades, and skill academies. Saudi Arabia’s Vision 2030 triggers local automotive component programs, and Egypt courts electronics assemblers seeking tariff-free access to the EU. Grid limitations still hinder giga-press rollouts, but modular micro-grids and solar cogeneration projects aim to unlock large-scale press opportunities in the coming decade. North America trails Asia in tonnage additions but benefits from EV tax incentives that favor domestic structural casting capacity. Reshoring campaigns and Buy American clauses further bolster the regional share of the die casting machinery market.

Competitive Landscape

Bühler Group, IDRA (part of L.K. Technology), and Shibaura Machine headline the global tier, each bundling presses with end-to-end digital twins that predict die life and energy use. Chinese challengers Yizumi and Haitian leverage cost advantages and rapid customization to penetrate price-sensitive orders, especially in Southeast Asia. Medium-sized European players focus on retrofit AI platforms, offering pay-per-shot service contracts that monetize uptime improvements.

Emerging software vendors sell cloud-agnostic predictive maintenance tools compatible with any press brand, enabling older lines to achieve near-parity OEE with new machines. Additive-tooling specialists collaborate with machine OEMs to certify conformal-cooling die inserts, locking in cross-sales. Overall, differentiation shifts from raw tonnage to data-rich ecosystems that reduce defects, energy consumption, and downtime in the die casting machinery market.

Die Casting Machinery Industry Leaders

Buhler AG

L.K. Technology Holdings Limited

Haitian Die Casting

Shibaura Machine

Yizumi Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UBE Machinery Corporation, Ltd., the flagship of the UBE Group's machinery division, has significantly expanded its range of die casting machines. These machines utilize 'giga casting' technology, adeptly molding body structure components for battery electric vehicles (BEVs) and more, all from aluminum alloy.

- September 2024: YIZUMI is unveiling the NEXT² Series, a 2-Platen Die Casting Machine, backed by a fresh development strategy and an advanced technical roadmap. This new series aims to enhance operational efficiency, improve precision, and cater to the evolving demands of the die casting industry, showcasing YIZUMI's commitment to innovation and technological advancement.

Global Die Casting Machinery Market Report Scope

The die casting machinery market report is segmented by machine type (hot chamber die casting machines and cold chamber die casting machines), material type (aluminum, and more), end-user industry (automotive, electrical and electronics, and more), punching capacity (below 50 tons, and more), automation level (manual, semi-automated, and fully automated), and geography. The market forecasts are provided in terms of value (USD).

| Hot Chamber Die Casting Machines |

| Cold Chamber Die Casting Machines |

| Aluminum |

| Zinc |

| Magnesium |

| Others |

| Automotive |

| Electrical and Electronics |

| Aerospace |

| Industrial Manufacturing |

| Others |

| Below 50 Tons |

| 50 - 100 Tons |

| Above 100 Tons |

| Manual |

| Semi-Automated |

| Fully Automated |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Machine Type | Hot Chamber Die Casting Machines | |

| Cold Chamber Die Casting Machines | ||

| By Material Type | Aluminum | |

| Zinc | ||

| Magnesium | ||

| Others | ||

| By End-User Industry | Automotive | |

| Electrical and Electronics | ||

| Aerospace | ||

| Industrial Manufacturing | ||

| Others | ||

| By Punching Capacity | Below 50 Tons | |

| 50 - 100 Tons | ||

| Above 100 Tons | ||

| By Automation Level | Manual | |

| Semi-Automated | ||

| Fully Automated | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What current spending outlook underpins new die casting capacity?

Global equipment outlays are expanding on a 6.09% CAGR through 2031, lifting the die casting machines market size to USD 5.46 billion.

How are giga-presses changing automotive body production?

6,000- to 9,000-ton presses enable single-piece underbodies that remove 79 parts and slash assembly time by 40%.

Which region is gaining share fastest?

The Middle East and Africa are registering a 7.74% CAGR thanks to industrial diversification and infrastructure upgrades.

Why is hot-chamber demand rising in electronics?

Semiconductor packaging now needs sub-50-micron tolerances that hot-chamber zinc and magnesium machines can deliver in <30-second cycles.

What digital tools are foundries adopting first?

IoT furnace sensors and AI defect-prediction models that reach 96.9% accuracy deliver immediate scrap and energy savings

Page last updated on: