Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

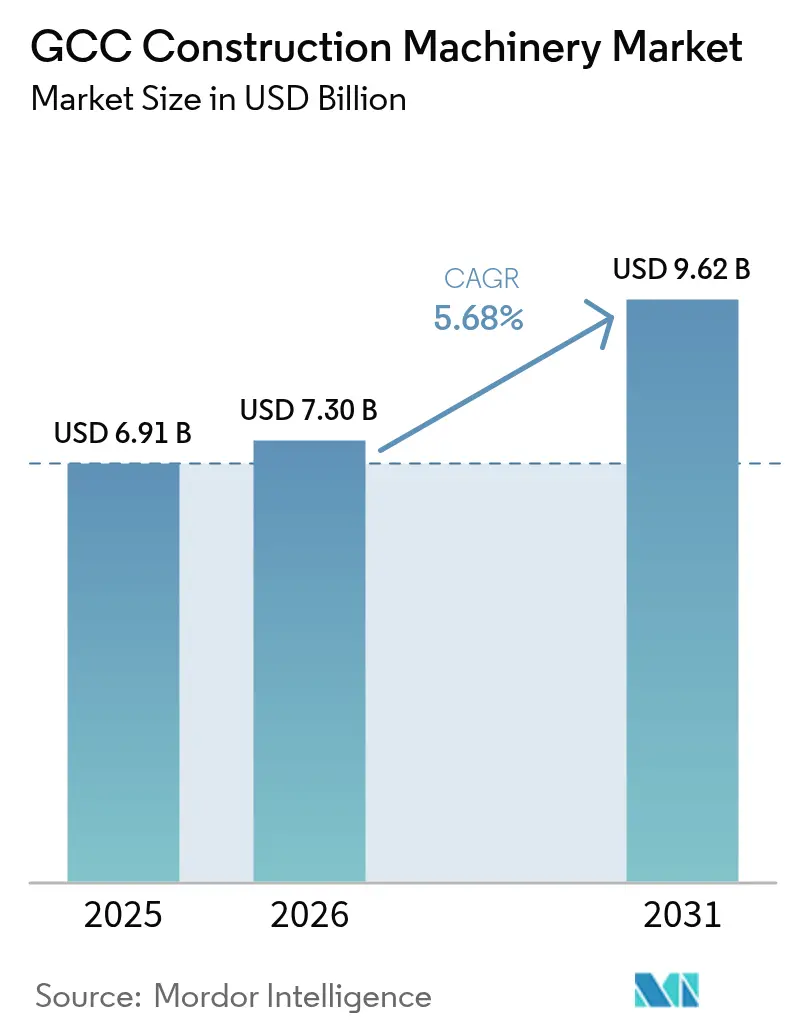

| Base Year Market Size (2025) | USD 6.91 Billion |

| Market Size (2026) | USD 7.3 Billion |

| Market Size (2031) | USD 9.62 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Construction Machinery Market Analysis by Mordor Intelligence

The GCC construction machinery market size is expected to grow from USD 6.91 billion in 2025 to USD 7.3 billion in 2026 and is forecast to reach USD 9.62 billion by 2031 at 5.68% CAGR over 2026-2031. This sustained advance aligns with sovereign wealth fund deployments, rapidly diversifying economies, and an unprecedented pipeline of infrastructure megaprojects that now dominate public–sector capital-expenditure agendas across all six Gulf nations. Sovereign strategies such as Saudi Arabia’s Vision 2030, the UAE’s federal growth program, Qatar National Vision 2030, and Oman Vision 2040 continue to convert hydrocarbon proceeds into long-cycle construction spending, lifting procurement of heavy machinery for urban expansion, industrial corridors, and green-energy installations. Equipment demand remains elastic to demographic growth, with Gulf urban populations climbing 2.1% annually and creating material shortfalls in housing, transit, and utilities. Competitive dynamics are intensifying as Chinese original-equipment manufacturers (OEMs) localize final assembly in Saudi Arabia and the UAE, while incumbents Caterpillar, Komatsu, and Volvo Construction Equipment defend share by scaling digital service platforms and flexible financing. Even with near-term oil-price volatility and a fast-growing rental market tempering fresh unit sales, the long-term trajectory of the GCC construction equipment market is supported by evolving local-content rules, green-hydrogen build-outs, and mandatory digital-engineering standards that collectively necessitate larger, more technologically sophisticated fleets [1]“Kingdom of Saudi Arabia Vision 2030,”, Vision 2030, vision2030.gov.sa [2]“Fiscal Monitor 2025,”, International Monetary Fund, imf.org.

Key Report Takeaways

- By machinery type, excavators led with 54.10% of GCC construction machinery market share in 2025, while motor graders are projected to post the fastest growth at a 7.35% CAGR through 2031.

- By propulsion, internal-combustion equipment commanded 98.05% of the GCC construction machinery market size in 2025, whereas electric alternatives are advancing at a 26.2% CAGR to 2031.

- By application type, earth-moving equipment accounted for 49.05% of the GCC construction machinery market size in 2025 and is expected to grow at a CAGR of 6.55% through 2031.

- By end-user, Infrastructure projects captured 52.20% of the GCC construction machinery market share in 2025, while industrial applications led growth with an 7.9% CAGR through 2031.

- By country, Saudi Arabia held 44.80% of the GCC construction machinery market size in 2025, whereas Oman is forecast to expand at a 7.3% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Construction Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Projects Drive Equipment Demand | +4.2% | Saudi Arabia primary, UAE secondary spillover | Long term (≥ 4 years) |

| Urban Boom Fuels Infra Investment | +3.6% | Global GCC, concentrated in Saudi Arabia and UAE | Medium term (2-4 years) |

| Smart Cities Push Electrification | +3.0% | NEOM, Dubai, Qatar national projects | Medium term (2-4 years) |

| BIM Mandates Spur Smart Equipment Demand | +2.4% | UAE, Saudi Arabia, with Oman early adoption | Short term (≤ 2 years) |

| Local Incentives Drive Assembly Growth | +1.8% | Saudi Arabia IKTVA, UAE ICV programs | Long term (≥ 4 years) |

| Hydrogen Projects Need Heavy-Lift Gear | +1.5% | Saudi Arabia, UAE, Oman coastal developments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision-2030 Megaproject Pipeline Sustains Equipment Demand

Saudi Arabia’s USD 500 billion NEOM initiative alone requires specialized excavators, telematics-enabled bulldozers, and desert-rated cranes for its 170 km linear city and 26,500 km² development zone. Procurement for mega LNG, rail, and tourism clusters extends average fleet-replacement cycles beyond five years, compelling OEMs to embed longer-tenor maintenance contracts and localized parts depots. The geographic concentration of work in the kingdom’s northwest also forces distributors to realign service hubs nearer to project sites [3]“The Line Project Overview,”, NEOM, neom.com.

Rapid Urban Population Growth Intensifies Infrastructure Spend

The rapid urbanization of Gulf cities is creating significant demand for infrastructure development. The annual influx of millions of new residents has resulted in substantial gaps in transport, utilities, and housing infrastructure, leading to increased investment in these sectors. Housing shortages in regions such as Saudi Arabia's Eastern Province and the UAE's Northern Emirates have necessitated large-scale community development projects that require extensive earth-moving and concrete equipment.

The increasing urban density is transforming equipment requirements in the construction sector. The demand for compact excavators and vertical-reach machinery is increasing, especially in confined construction areas. This transition indicates a broader movement toward specialized equipment that can operate efficiently in densely populated urban environments.

Electrification Mandates in Flagship Smart-city Projects

NEOM’s zero-emission construction rules and Dubai’s objective to electrify 30% of public fleets by 2030 catalyze the first significant orders for battery-electric loaders, mini excavators, and mobile compressors. Dubai’s Road & Transport Authority (RTA) commissioned battery-swap stations in 2025, creating an early refueling network blueprint. Initial deployments remain confined to controlled zones, but performance data under high-heat conditions is expected to accelerate broader fleet conversions in the second half of the decade [4]“RTA launches battery-swap stations,”, Road & Transport Authority, rta.ae.

Mandatory BIM Adoption Boosts Demand for Connected Machinery

Dubai now requires building information modeling (BIM) on projects. Similar policies in Saudi Arabia and early adoption in Oman are driving contractor preference for equipment that streams live telemetry into 3D models. Integrated data flows shorten site-meeting preparation fivefold and flag deviations early, improving on-time completion—a premium benefit OEMs monetize through subscription software layers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil Volatility Slows Public Capex | -2.4% | Saudi Arabia, Kuwait, UAE government projects | Short term (≤ 2 years) |

| Rental Surge Hits New Equipment Sales | -1.8% | Global GCC, concentrated in UAE and Qatar | Medium term (2-4 years) |

| Water Rules Raise Operating Costs | -1.2% | UAE, Saudi Arabia arid regions | Long term (≥ 4 years) |

| Operator Shortage Delays Fleet Growth | -0.9% | Global GCC, acute in Oman & Bahrain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility Curbs Public-Sector Capex Cycles

Oil price movements influence fiscal planning and infrastructure development across the Gulf region. Declining crude oil prices reduce government revenues, leading to project rescheduling and delays in equipment procurement. In Saudi Arabia, project awards have decreased as ministries focus on high-priority initiatives instead of optional upgrades.

While large-scale projects maintain dedicated funding, smaller municipal projects face budget constraints. This funding pattern demonstrates a strategic spending approach, where investments target projects delivering measurable economic or social benefits during periods of fiscal uncertainty.

Equipment-Rental Boom Suppresses New-unit Sales

The construction equipment rental market is expanding across the Gulf region, with the United Arab Emirates and Qatar showing significant rental fleet penetration rates. Large construction operators increasingly favor rental arrangements due to bulk pricing advantages and structured equipment replacement cycles, typically occurring every four years. This shift has reduced direct equipment purchases from original equipment manufacturers (OEMs).

The rental equipment experiences more intensive usage, with machines recording approximately double the engine hours compared to privately owned equipment. This increased utilization creates higher demand for maintenance services and replacement components, generating expanded aftermarket revenue streams. While new equipment sales may decrease, the maintenance and service ecosystem supporting rental fleets has emerged as a primary growth segment for equipment suppliers and dealerships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Excavators Remain the Backbone of Infrastructure Build-out

Excavators captured 54.10% of the GCC construction equipment market share in 2025 on foundation, grading, and trenching tasks woven through every megaproject. A pipeline of high-detail earthworks, from NEOM’s trench-based infrastructure spine to dual-carriageway expansions in Abu Dhabi, keeps 30-35-ton models in constant rotation. In the future, motor graders are slated for a 7.35% CAGR through 2031 as Saudi Arabia and Oman push 1,900 km of new highways and smart-city roadway grids that demand precision finish grading.

The increasing digitalization is transforming the machinery composition, with the adoption of telematics in crawler excavators driving market demand, enabling fuel-burn optimization and predictive maintenance routines that cut downtime. Meanwhile, rough-terrain cranes have found a niche in the industrial build-out phase; the single-order purchase of 100 Tadano GR-800EX units by AMHEC illustrates the heightened scale of fleet aggregation on complex job sites. Specialized quarry equipment has experienced an upswing after the Saudi Ministry of Industry shortlisted 30 firms for 22 new quarry licenses, guaranteeing fresh demand for rock breakers and surface-drilling rigs across Tabuk and Eastern Province clusters.

By Propulsion Type: ICE dominance persists but electric fleets emerge in smart-city zones

Internal combustion engines commanded 98.05% of the GCC construction equipment market size in 2025. Reliability in 50 °C ambient temperatures, easy refueling logistics, and proven residual values keep ICE the standard for desert and remote-area projects. However, electric and hybrid equipment is pacing at a 26.2% CAGR through 2031, albeit from a low base. Early adoption focuses on compact excavators, telehandlers, and light towers in enclosed or emissions-sensitive environments such as hospital extensions and subterranean metro stations.

Infrastructure gaps remain the primary brake on wider decarbonization. Even so, Dubai and Riyadh municipal codes now stipulate electric-ready job sites for flagship developments; equipment financiers are responding with operating-lease structures that spread higher capital costs over eight-year terms. Atlas Copco’s launch of containerized 1 MWh energy-storage systems is another sign of ecosystem maturity, providing off-grid fast-charge capabilities for daytime peak operations.

By Application Type: Earth-Moving Stays Dominant Amid Cross-Sector Land Preparation

Earth-moving constituted 49.05% of the GCC construction equipment market size in 2025 and is growing at a CAGR of 6.55% through 2031, owing to persistent land-reclamation, grading, and backfilling requirements across waterfront and desert terrains. Land reclamation alone swallowed 150 million m³ of sand and rock in 2024, necessitating high-capacity dredgers and dozers. Transport and utility corridors further consolidate earth-moving’s primacy through 2031, even as vertical construction accelerates.

Concrete placement and material-handling equipment follow closely as the region pivots to high-rise formats and integrated logistics zones. Vertical tower developments in Dubai and Riyadh drive sling-stage cranes and self-climbing boom pumps deeper into project budgets. At the same time, integrated project delivery models foster packages that bundle earth-moving, material-handling, and finishing equipment, streamlining procurement cycles and compressing build schedules.

By End-User: Infrastructure retains bulk share as industrial investments accelerate

Government-led infrastructure projects controlled 52.20% of the GCC construction equipment market size in 2025 and anchored the largest slice of the market share. Multi-year allocations toward highways, rail, and ports guarantee healthy baseline utilization for graders, pavers, and heavy-lift cranes. Yet industrial applications represent the fastest-growing end-use cohort, clocking an 7.9% CAGR through 2031, as countries push steel, chemicals, and hydrogen clusters to capture downstream value from hydrocarbons.

Manufacturing localization schemes such as Saudi Arabia’s Made in Saudi program and the UAE’s Operation in new fabrication yards, data centers, and logistics hubs, are intensifying calls for precision installation machinery and automated material-handling systems. Residential and commercial segments continue to absorb backhoe loaders and concrete pumps. However, incremental growth skews toward energy-intensive facilities whose construction envelopes require thicker concrete pours, higher clear-heights, and more specialized rigs.

Geography Analysis

Saudi Arabia remains the center of gravity with a 44.80% share of the GCC construction equipment market in 2025. NEOM, the Red Sea tourism corridor, and Riyadh’s metro expansion anchor high-volume orders for crawler cranes, large excavators, and desert-grade articulated dump trucks. In mining, the award of 22 quarry licenses across Eastern Province and Tabuk doubles down on demand for surface-drilling rigs and high-capacity front-end loaders. Local-content rules further reshape supply chains and drive joint-venture assembly plants that compress delivery lead times.

Oman logs the fastest growth at a projected 7.3% CAGR through 2031. The construction tender spanning seven governorates heralds a multiyear stream of earth-moving and concrete-equipment call-offs. Early adoption of unified BIM standards accelerates connected-machinery uptake, enabling small contractors to leapfrog manual fleet-management methods and capture efficiency dividends. Infrastructure upgrades to ports at Duqm and Sohar add marine-rated cranes and dredgers to procurement lists, broadening the equipment mix relative to the country’s historical road-heavy profile.

Dubai’s Palm Jebel Ali revamp and Abu Dhabi’s Etihad Rail extensions are spurring simultaneous demand for pile-driving hammers, ballast regulators, and low-emission loaders. Qatar’s post-World Cup maintenance phases continue to require compact equipment for stadium retrofits, while the planned GCC power-grid interconnector drives orders for transmission-line stringing rigs in Kuwait and Bahrain.

Regulatory Landscape

Across the GCC, construction machinery compliance is shaped by a mix of harmonized Gulf standards and country-specific market-access systems. A key anchor is the GCC Standardization Organization publication of GSO ISO 20474-1:2023, which sets safety requirements for earth-moving machinery and provides a common baseline for OEM design and documentation across member states.

Saudi Arabia applies SASO technical regulations for machinery safety and routes many imported products through the SABER conformity pathway, tightening documentation and conformity-certificate workflows for suppliers and importers. Saudi Arabia also operates a Heavy Equipment Regulatory Center within SASO (established April 2021) focused on inspection, licensing, and safety oversight. In the UAE, federal conformity certificates managed by MoIAT and local emirate-level operating and permitting requirements (for example, Dubai RTA and Abu Dhabi DMT processes) combine to form a multi-layer compliance model for fleets and dealers operating across borders.

Value Chain Analysis

The GCC construction machinery value chain begins with global OEM engineering and component sourcing, then moves into regional importation and, in selected cases, localized final assembly to align with local-content programs (for example, Saudi IKTVA and UAE ICV) referenced in the report context. Execution typically runs through regional dealers and service specialists (such as Kanoo Machinery) and large rental operators, with demand shaped by infrastructure and industrial project owners and EPC contractors across Saudi Arabia, the UAE, and Oman.

Logistics and after-sales capacity matter more in the region due to long transport distances to megaproject sites and high utilization in rental fleets. Port and corridor infrastructure (for example, Jebel Ali in the UAE and King Abdulaziz Port in Saudi Arabia) serves as entry nodes for heavy equipment, while project-driven service hubs, parts depots, and field maintenance networks support lifecycle revenues as machines rack up high engine hours. As connected machinery adoption rises alongside telematics tied to BIM workflows, digital platforms and dealer-led monitoring services gain weight next to traditional parts, consumables, and rebuild activities.

Competitive Landscape

Market concentration in the GCC construction equipment industry remains moderate. Caterpillar sustains its presence via unrivaled parts availability and dealer networks stretching from Jeddah to Muscat. Komatsu leverages semi-autonomous dozer technology to win desert earth-moving contracts, while Volvo Construction Equipment’s electric compact range secures zero-emission pilot sites in Dubai. Chinese entrants XCMG and Sany narrow the technological gap and enjoy cost advantages through regional assembly, meeting local-content mandates, and shaving customs duties.

Digital service ecosystems have become the new battleground. Caterpillar’s VisionLink platform offers predictive service packages that lock in recurring revenue streams. Komatsu’s SmartConstruction cloud integrates drone mapping and machine control, reducing grade-check activities by 80% on Saudi highway jobs. Financing innovation also gains traction; State Street Global Advisors notes a sharp rise in private credit funds underwriting mid-ticket equipment leases, diversifying away from bank syndications and smoothing purchase cycles.

Liebherr holds lattice boom cranes in specialized niches critical for hydrogen electrolyzer lifts, while Manitowoc secures metro tunnel-segment gantry contracts. Local distributors such as Kanoo Machinery and Arabian Jerusalem Truck & Heavy Equipment lead after-sales customization, including locally engineered filtration kits for fine-sand environments. As electric adoption widens, joint ventures between OEMs and Gulf utilities to pilot on-site charging hubs may create future first-mover advantages.

GCC Construction Machinery Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Liebherr International AG

XCMG Construction Machinery Co. Ltd

AB Volvo (Volvo Construction Equipment)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are clustering around technology-enabled roadbuilding, connected fleets, and lifecycle services that fit the region's megaproject execution model. A tangible proof point is the June 2026 deployment of seven intelligent road construction machines by XCMG on Oman's Sultan Said bin Taimur Road dualisation project, which is positioned as an AI-enabled autonomous asphalt paving application. It points to addressable demand for machine control, autonomous compaction/paving packages, operator enablement, and site digitization that OEMs and dealers can productize beyond one-off equipment sales.

Local-content and industrialization programs also provide a route for OEMs and distributors to broaden regional footprints through assembly, parts localization, and remanufacturing capability. Saudi Arabia's National Industrial Development and Logistics Program (NIDLP) target of SAR 1.4 trillion in private-sector investment by 2030, together with the report's stated giga-project pipeline (for example, NEOM), supports demand for localized service hubs, field workshops near remote sites, and structured maintenance contracts aimed at reducing downtime in extreme heat and dust conditions. Electrification pilots in controlled zones (for example, NEOM zero-emission construction rules and Dubai's RTA battery-swap initiative cited in the report context) open a near-term equipment and infrastructure bundle opportunity spanning electric compact machines, energy storage, and jobsite charging solutions, with financing and uptime guarantees as key packaging levers.

Recent Industry Developments

- June 2026: XCMG deployed seven intelligent road construction machines on Oman's Sultan Said bin Taimur Road Dualisation Project, introducing an AI-enabled autonomous asphalt paving application on an active highway program. The deployment raises competitive benchmarks for road construction equipment in the GCC from unit performance to digital workflows and machine-control capability delivered with local contracting partners.

- March 2026: Volvo Construction Equipment highlighted Middle East jobsite results for the new generation of excavators, including a 15% fuel-efficiency improvement and the integration of Volvo Smart View monitoring, supported through the regional dealer network. The update focused on performance and connected monitoring for contractors operating in the region.

- May 2025: Dubai RTA battery-swap initiative expanded to additional depots, supporting electrification pilots for construction equipment and enabling new uptime and charging solutions. The expansion builds out the early refueling network referenced in the report context.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers demand and supply of construction machinery sold for use in building, infrastructure, and related earthworks across GCC countries, expressed in value terms and tied to equipment delivered into active projects and fleet replacements.

Scope exclusions: we exclude equipment rental revenue, aftersales service contracts, operator staffing, and general construction materials from this market sizing.

Segmentation Overview

- By Machinery Type

- Cranes

- Excavators

- Loaders and Backhoes

- Motor Graders

- Telescopic Handlers

- Other Machinery

- By Propulsion Type

- Internal Combustion Engine (ICE)

- Electric / Hybrid

- By Application Type

- Concrete Construction Equipment

- Road Construction Equipment

- Earth-Moving Equipment

- Material Handling Equipment

- By End-User

- Infrastructure

- Commercial

- Residential

- Industrial

- By Country

- Saudi Arabia

- United Arab Emirates

- Kuwait

- Qatar

- Oman

- Bahrain

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the factual base for the model and to keep country-level demand logic grounded in visible construction activity. We referenced public and official sources such as national statistics offices and central banks in GCC countries, ministries that publish infrastructure and housing updates, and customs and trade portals for import trends on machinery categories. Where project pipeline timing was needed, we also used tender portals and public procurement notices, supported by regulator and municipality releases.

To translate construction activity into equipment demand, we reviewed annual reports, investor presentations, and audited filings of relevant ecosystem participants, then cross-checked project awards and timelines using reputable regional business press. Select paid subscriptions were used only where they help normalize company financials and cross-check trade and shipment signals, without relying on single reports. The desk sources listed here are illustrative, and other public references were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives buying cycles in the GCC, including how contractors and project owners time fleet additions and replacements across equipment classes. We spoke with a mix of OEM-facing stakeholders, fleet owners, and large contractor procurement teams across the region, then used follow-up checks to confirm pricing direction, lead times, and the portion of demand that is linked to government-related megaprojects.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | |

| Mid tier: 55% | Functional/Unit leaders: 31% | |

| Smaller Players: 15% | Managers: 55% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where project activity and trade-linked machinery flows are reconstructed for the GCC, then allocated into equipment demand using observed replacement cycles and utilization patterns. This is cross-checked with selective bottom-up approximations, where sampled unit volumes by machinery class are multiplied by typical price bands, and then adjusted based on channel feedback and procurement timing.

Key drivers that materially shape the totals include the pace of infrastructure awards, housing starts and completions, road and rail work intensity, equipment import momentum by country, and fleet replacement behavior for large contractors (including how frequently high-hour machines are rotated). We also track practical pricing drivers such as diesel versus electric adoption for certain use cases, and the shift between earthmoving and material handling when megaproject schedules move from early groundwork into vertical builds.

For forecasting, scenario analysis is used to reflect how sensitive equipment demand is to project execution speed, public capex cycles, and contractor cash flow conditions. Where data gaps appear for smaller countries or niche categories, the model uses proxy relationships from similar GCC markets and then refines them through interview-led checks on penetration and typical fleet composition.

Data Validation & Update Cycle

Validation is done by comparing model outputs against independent signals such as import trends, known project award totals, and directionally consistent equipment pricing movement. When large variances show up, the assumptions are re-checked, outliers are reviewed by a second analyst, and respondents are re-contacted if a swing appears tied to a real market event rather than a modeling artifact.

The report is refreshed annually, and interim updates are made when material events occur, such as sudden changes in public infrastructure spending, major project delays, or noticeable shifts in trade flows. Before delivery, we run a final pass to confirm that the latest macro, project, and pricing indicators have been reflected in the numbers.

Mordor Intelligence's Gcc Construction Machinery Market Size Compared Against Other Published Estimates

Published numbers for the GCC construction machinery market can look far apart because the market boundary is not always identical across studies, even when the titles sound similar. Differences usually come from what is counted as market value, which countries are fully covered, and whether the stated year is a base year, a current year, or a forward estimate.

The benchmark table shows a wide spread that is mainly explained by scope and timing choices. In Mordor Intelligence's model, the value is tied to machinery sales in the GCC (equipment such as excavators, loaders, rollers, bulldozers, cranes, and graders) rather than bundling rental and ongoing service revenue into the same total. In addition, currency timing, whether price progression follows an aggressive versus base case, and how quickly megaproject demand is assumed to convert into deliveries can change the reported market size for the same calendar year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.91 B (2025) | |

| Global Consultancy A | USD 8.50 B (2024) | Uses an earlier base year and may apply a broader price uplift and faster demand conversion assumptions, which can inflate the stated value when project awards are translated into equipment purchases. |

| Industry Publisher B | USD 4.80 B (2024) | Often blends equipment scope differently (for example, mixing heavy and compact categories and service elements) and can undercount large project-linked deliveries if imports and contractor fleet additions are not fully reflected. |

Taken together, the differences are most traceable to what is included in the market boundary, which year is being referenced, and how pricing and delivery timing are handled. Our approach keeps the total linked to observable construction activity and trade signals, then stress-tests it through interviews so the final number remains explainable and repeatable.

Key Questions Answered in the Report

How large is the GCC construction equipment market in 2026?

The market stands at USD 7.3 billion in 2026 and is set to reach USD 9.62 billion by 2031.

What is the forecast CAGR for construction equipment demand across the Gulf?

Aggregate demand is projected to advance at a 5.68% CAGR between 2026 and 2031.

Which machinery category generates the highest revenue?

Excavators contribute the largest share, accounting for 54.10% of 2025 revenue.

Which Gulf country represents the biggest market for construction equipment?

Saudi Arabia commands a 44.80% share of regional sales, driven by Vision 2030 megaprojects.

What impact does equipment rental have on new-unit sales?

Rising rental penetration, particularly in the UAE and Qatar, moderates direct unit purchases but boosts parts and service revenues as rented fleets log higher utilization.

Page last updated on: