Packaging Adhesives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

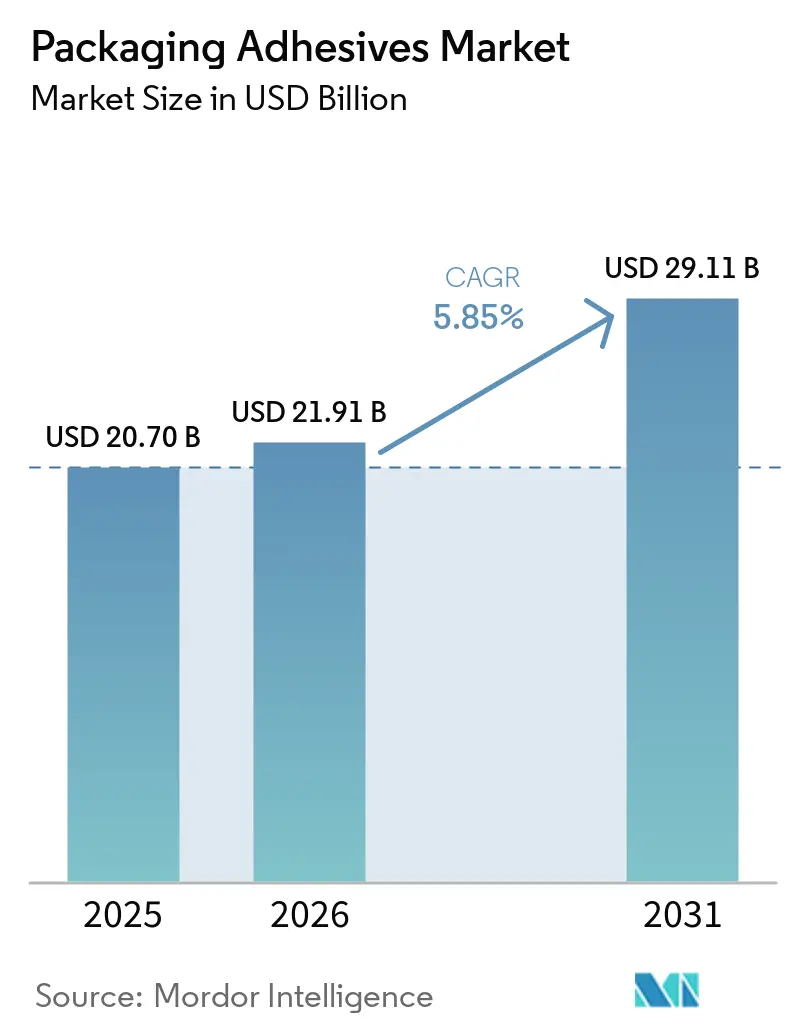

| Market Size (2026) | USD 21.91 Billion |

| Market Size (2031) | USD 29.11 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Adhesives Market Analysis by Mordor Intelligence

The Packaging Adhesives Market size is expected to grow from USD 20.70 billion in 2025 to USD 21.91 billion in 2026 and is forecast to reach USD 29.11 billion by 2031 at 5.85% CAGR over 2026-2031. Rising converter preference for water-based systems, rapid e-commerce fulfillment growth, and tighter food-contact regulations are compressing production cycles and reshaping specification priorities. Brand owners favor mono-material laminates that simplify recycling, which pushes formulators to balance high bond strength with easy delamination. At the same time, AI-enabled dispensing equipment is trimming adhesive consumption and elevating process consistency, rewarding suppliers able to integrate digital support. Feedstock volatility and tougher VOC rules remain profit headwinds, but supplier investment in bio-based chemistries and recyclable adhesives positions the sector for resilient expansion across flexible, rigid, and label applications.

Key Report Takeaways

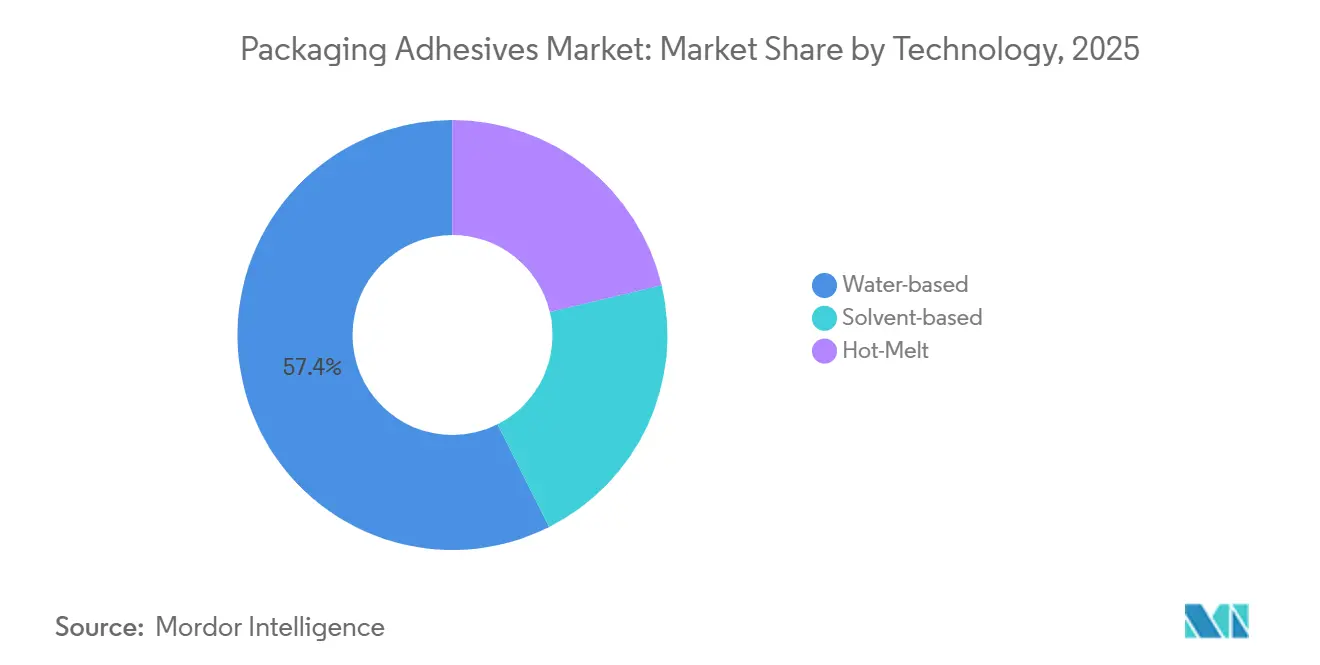

- By technology, water-based adhesives led with 57.42% of 2025 revenue and are set to expand at a 6.19% CAGR through 2031.

- By resin chemistry, ethylene-vinyl acetate captured a 30.61% share in 2025, while bio-based alternatives are advancing at a 6.82% CAGR to 2031.

- By application, flexible packaging accounted for 39.25% of 2025 volume and is growing at a 6.45% CAGR over the forecast period.

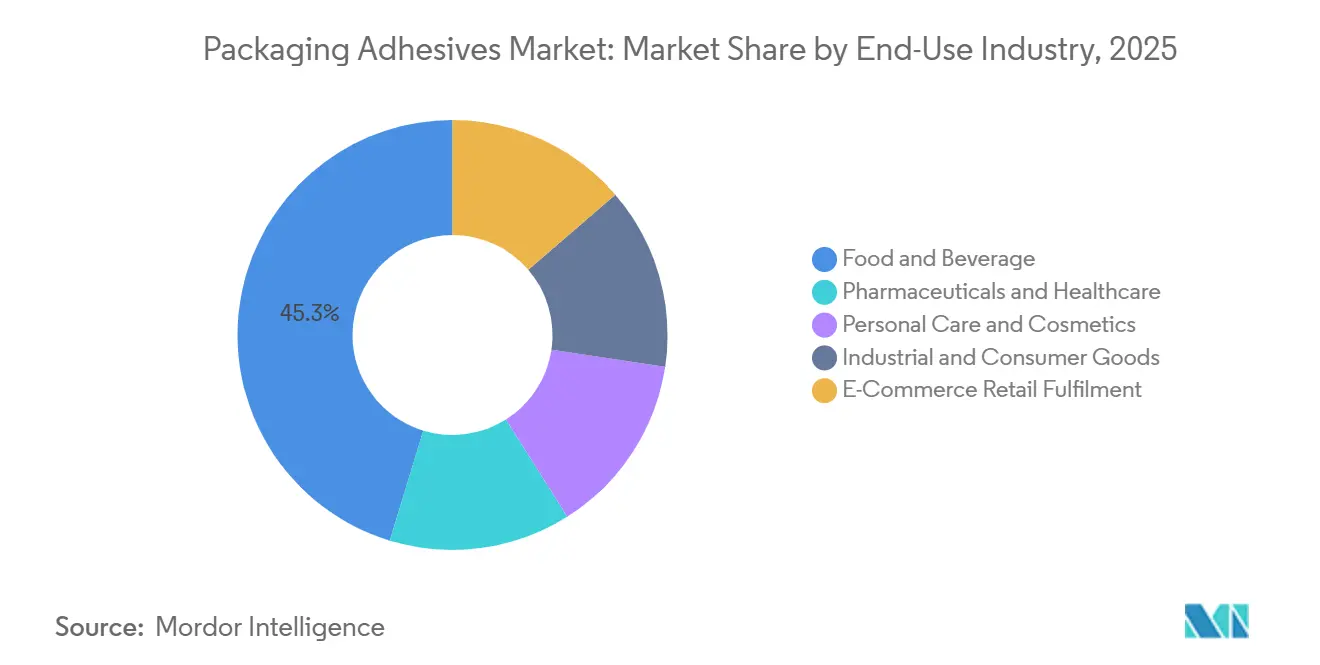

- By end-use industry, food and beverage held 45.29% of demand in 2025, whereas e-commerce retail fulfillment is forecast to record a 7.05% CAGR to 2031.

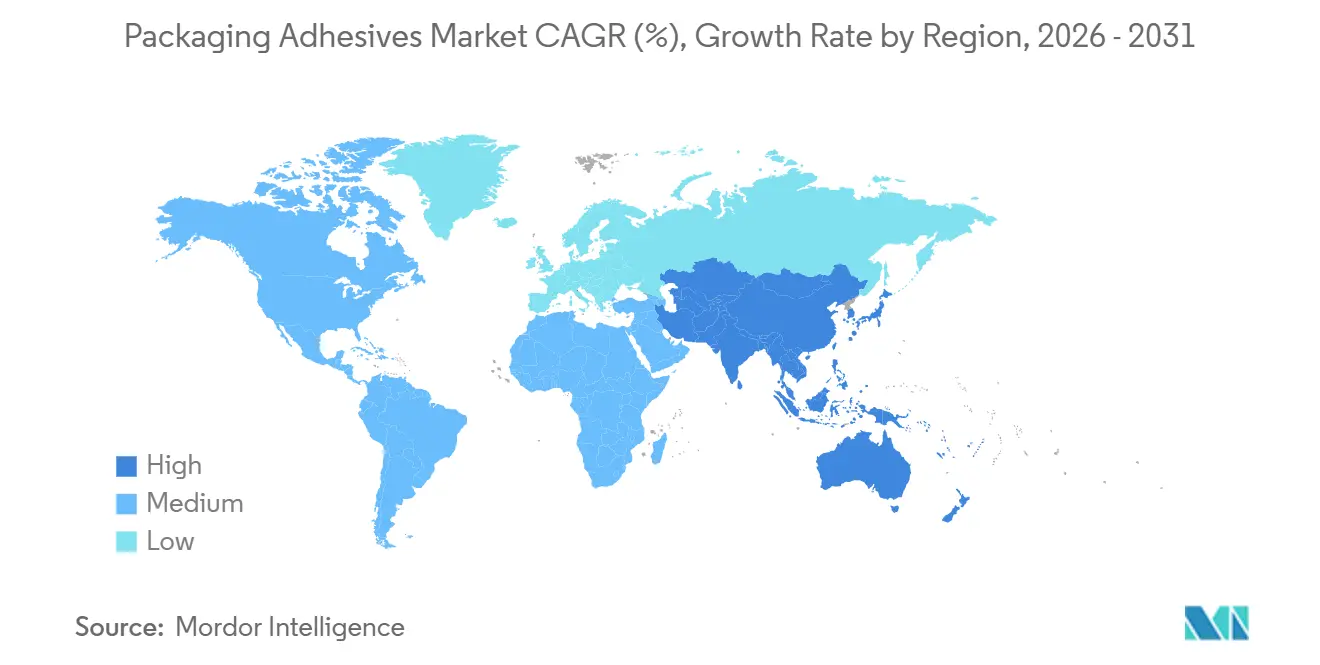

- By geography, Asia-Pacific commanded 40.35% of global consumption in 2025 and is expanding at a 6.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Packaging Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from food and beverage converters | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| E-commerce–driven corrugated and mailer growth | +1.5% | Global, led by North America, Asia-Pacific, Europe | Short term (≤ 2 years) |

| Shift toward sustainable water-based and solvent-free systems | +1.3% | Europe, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| AI-optimised high-speed dispensing lines | +0.9% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Cold-chain direct-to-consumer packaging needs cryogenic-stable bonds | +0.7% | North America, Europe, urban Asia-Pacific hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand From Food and Beverage Converters

In the food and beverage sector, converters are standardizing adhesive portfolios to meet lamination speeds and adhere to zero-migration mandates. Henkel's launch of Aquanence achieved a reduction in curing time and a decrease in oven energy consumption, leading to shorter production lines and diminished emissions. The rise of mono-material polyethylene pouches amplifies the demand for primers that can adhere to corona-treated films but easily wash off in recycling baths. Chemists are fine-tuning the windows of hydroxyl and carboxyl functionalities to ensure shelf-life integrity while facilitating wash-tank release, a skill often dominated by global suppliers with pilot-line capabilities. Additionally, rapid retort sterilization is pushing converters to favor water-based polyurethanes, which achieve full bond strength quickly. These trends are driving a surge in the adoption of high-performance water-based chemistries in the packaging adhesives market.

E-Commerce–Driven Corrugated and Mailer Growth

In 2025, global parcel volumes surged, driving up the demand for corrugated-box adhesives. Fulfillment centers are now utilizing vision-guided dispensing robots, which can adjust bead width in real-time, leading to a reduction in waste. This level of automation not only solidifies partnerships with suppliers offering digital analytics but also creates a competitive edge against commodity players. Hot-melt EVA copolymers are the go-to choice for high-speed lines, thanks to their optimal open time and green strength. As a result, e-commerce is setting new standards, influencing other segments of the packaging adhesives market.

Shift Toward Sustainable Water-Based and Solvent-Free Systems

The EU's Industrial Emissions Directive has set a new limit, capping VOC emissions for coating lines. Water-based acrylic emulsions dominated the label-adhesive volume. However, concerns over hydrolysis in wet environments continue to drive research and development efforts. Dow's RHOXIMAT polyurethane dispersions achieved peel strength on PET, matching solvent benchmarks and eliminating the need for thermal post-curing. Henkel's Technomelt Supra Cool 130, boasting renewable carbon, ensures cryogenic stability, catering to cold-chain demands. With brands committing to renewable content by 2030, the push for bio-based resins intensifies, solidifying sustainable chemistries as a key growth driver in the packaging adhesives sector.

AI-Optimised High-Speed Dispensing Lines

Nordson's BlueFinity system, equipped with inline cameras and machine learning, adjusts pump pressure within a swift timeframe[1]Nordson Corporation, “BlueFinity System White Paper,” Nordson.com . This innovation trims adhesive usage while maintaining seal integrity even with substrate-thickness variations. Meanwhile, Robatech's AX Fusion boasts the capability to forecast nozzle clogging in advance. This foresight translates to a reduction in downtime, benefiting plants across Europe. Furthermore, when converters and suppliers collaborate and share data, they can cut development cycles for next-generation adhesives. However, with significant capital costs per line, only large converters can afford the investment. Yet, the undeniable performance advantage continues to drive demand for these digitally integrated solutions in the packaging adhesives market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in petrochemical feedstock prices | -1.1% | Global, acute in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Stringent VOC and food-contact migration regulations | -0.8% | Europe, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Delamination challenges in mechanical recycling streams | -0.6% | Europe, North America, pilot programs in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Petrochemical Feedstock Prices

Propylene prices are putting pressure on EVA and polyolefin hot-melt margins. Smaller converters, without access to hedging tools, resort to quarterly surcharges to pass on costs, disrupting contract stability. While an ethylene oversupply tempered prices in H1 2024, delays at Middle Eastern crackers negated those gains by late 2025. Dow's in-house ethylene production underscores the protective benefits of vertical integration. This ongoing volatility not only deters investments in additional capacity but also casts a shadow over the packaging adhesives market.

Stringent VOC and Food-Contact Migration Regulations

In 2024, the EPA slashed VOC limits for flexible-packaging adhesives. Meanwhile, in 2025, EFSA introduced guidance that caps non-intentionally added substances[2]European Food Safety Authority, “Non-Intentionally Added Substances Guidance 2025,” Efsa.europa.eu. This move has escalated analytical testing costs per formulation. Companies now face a stretched conformity timeline, a delay that hampers product launches and gives an edge to incumbents with established legacy dossiers. China's GB 9685-2016 has harmonized its aromatic-amine limits with EU standards, amplifying global compliance challenges. Such regulatory pressures are tempering growth in the packaging adhesives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Based Systems Solidify Lead

Water-based products accounted for a 57.42% share of 2025 revenue, and their 6.19% CAGR keeps them the fastest-growing technology tier. Regulatory VOC caps and converter moves to eliminate solvent ovens anchor this trajectory. Adoption is especially strong on new European and North American lamination lines, where cold-curing polyurethanes reduce energy consumption. Solvent-based options persist in aluminum-foil blisters that demand high peel strength, while hot-melt EVA retains dominance in high-speed case sealing thanks to rapid set times. Pressure-sensitive label demand boosts acrylic emulsions that resist plasticizer migration over multiyear life cycles. Hybrid primer-plus-topcoat systems bridge adhesion gaps on corona-treated polypropylene, allowing continuous high-speed throughput. This mix positions water-based chemistries at the center of long-term value creation for the packaging adhesives market.

By Resin Chemistry: EVA Retains Scale, Bio-Based Gains Traction

EVA held 30.61% of 2025 revenue, leveraging formulations designed for open times ideal for automated carton lines. Premium niches in polyurethanes demand retort or steam sterilization resistance, surpassing 121 °C. Acrylic emulsions, favored for pressure-sensitive labels, resist UV exposure and plasticizer bleed, justifying their price premium. Bio-based resins are growing 6.82% annually, fueled by multi-national brand mandates for renewable carbon by 2030. Sustainability and cryogenic stability coexist in advanced solutions. While styrenic block copolymers lose ground, bio-polyolefins, offering similar peel properties and reduced VOCs, gain traction. Natural starch systems find their niche in corrugated applications, where moisture risk remains minimal. Resin suppliers equipped with pilot lines and analytical labs stand out, customizing blends for a competitive edge in the packaging adhesives market.

By Application: Flexible Packaging Extends Dominance

Flexible packaging represented 39.25% of 2025 volume and is forecast to advance at a 6.45% CAGR to 2031. Multi-layer pouches and flow-wraps replace rigid jars, cutting logistic costs. Two-component polyurethanes achieve cure and survive autoclave cycles, meeting converter line-speed and shelf-life targets. Folding cartons leverage dextrin and starch glues optimized for high-speed lines, while labels and tapes grow on momentum in personal care and pharma track-and-trace applications. Sealing usage rises alongside fulfillment-center automation that trims adhesive waste. Specialty segments such as graphics lamination remain steady but price-accretive. The application shift toward high-value flexible pouches lifts the average selling price and margin profile across the packaging adhesives market.

By End-Use Industry: E-Commerce Accelerates Past Traditional Leaders

Food and beverage converters consumed 45.29% of the 2025 volume, yet e-commerce parcels outstripped all peers with a 7.05% CAGR. Hot-melt EVA plays a crucial role in high-speed box lines, ensuring they pass rigorous drop tests. The pharmaceutical sector emphasizes peelable, sterile-barrier adhesives that meet ISO 11607 standards. The personal care industry is driven by the demand for refillable packaging, necessitating labels that can be removed without leaving residue. Both industrial and consumer goods are turning to flexible packaging, moving away from the weight of rigid clamshells. While cold-chain meal kits and biologics may be modest in tonnage, they command a significant price premium due to their cryogenic durability. There's a notable trend of technology transfer across segments, with e-commerce innovations finding their way into food pouches. This shift not only speeds up formulation cycles but also strengthens the value proposition in the packaging adhesives market.

Geography Analysis

Asia-Pacific held a commanding 40.35% share in 2025 and will grow 6.62% annually through 2031. In 2025, China's demand surged as automated lines were rolled out, necessitating digitally integrated hot-melt systems. Driven by rising consumption of packaged foods, India experienced growth, highlighted by the addition of water-based capacity in Gujarat. Japan and South Korea carved out high-performance niches, opting for UV-curable labels that set in under 2 seconds. Meanwhile, ASEAN countries enjoyed growth as brands began diversifying their focus beyond China.

In 2025, North America accounted for a significant portion of the global volume, bolstered by advancements in fulfillment automation and a shift towards recyclable mono-material packaging. Hot-melt demand in the U.S. climbed, spurred by the inauguration of new distribution centers. Specialty label usage in Canada's Ontario and Quebec pharma clusters is on the rise, while Mexico's near-shoring initiatives are driving expansions in Monterrey and Querétaro.

Europe, holding a notable market share, is witnessing growth despite its mature status. Germany is at the forefront of bio-based adoption, with the unveiling of a co-developed starch adhesive boasting renewable content in 2025. The U.K. grapples with post-Brexit dossier duplications, incurring added costs per formulation. Meanwhile, France and Italy are capitalizing on luxury cosmetics exports, which increasingly demand holographic pressure-sensitive labels.

Brazil led South America, driving growth in 2025, as the adoption of flexible packaging helped mitigate distribution costs across the continent's expansive geographies. Argentina's growth was largely attributed to packaging for agricultural exports. The Middle East and Africa, while still representing a modest portion of global demand, are advancing annually. This growth is buoyed by Saudi Arabia's investments in food security and a burgeoning pharmaceutical manufacturing sector in South Africa. Collectively, these regional dynamics are fostering multiple growth nodes, ensuring the continued expansion of the packaging adhesives market.

Competitive Landscape

The packaging adhesives market is moderately fragmented. H.B. Fuller focuses on digital integration, embedding Swift-tak analytics into fulfillment-center robots. 3M mines cryogenic epoxy demand for insulated shippers, while Dow exploits captive ethylene to buffer feedstock swings. Arkema’s 2024 acquisition of Dow’s laminating business positions it closer to food and medical converters. Suppliers offering predictive-maintenance dashboards, therefore, lock in multi-year contracts, reinforcing durable competitive moats inside the packaging adhesives market.

Packaging Adhesives Industry Leaders

Henkel AG & Co. KGaA

H.B. Fuller Company

3M

Arkema

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BASF introduced water-based Epotal adhesives, developed to facilitate material separation in PET-based packaging. The company also launched label adhesives (acResin) that could be removed without leaving harmful residues.

- August 2025: Sonoco Products Company announced that it is investing USD 30 million to boost its packaging adhesives production capacity in the U.S. This investment will enhance current production lines and introduce new ones.

Global Packaging Adhesives Market Report Scope

Packaging adhesives are mainly used for advanced bonding to meet demanding applications in a wide variety of end-use market products such as boxes and cartons. They can be of different types, such as water-based, which are developed using a combination of water, polymers, and additives.

The packaging adhesives market is segmented on the basis of technology, resin chemistry, application, end-user industry, and geography. By Technology, the market is segmented into water-based, solvent-based, and hot-melt. By Resin Chemistry, the market is segmented into acrylics, polyurethanes, ethylene-vinyl acetate (EVA), styrenic block copolymers, and natural/bio-based. By Application, the market is segmented into flexible packaging, folding cartons and boxes, labels and tapes, sealing, and other applications (tissue and towel over-wrap, graphics and specialty). By End-Use Industry, the market is segmented into food and beverage, pharmaceuticals and healthcare, personal care and cosmetics, industrial and consumer goods, and e-commerce retail fulfillment. The report also covers the market size and forecasts for the packaging adhesive market in 16 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Water-based |

| Solvent-based |

| Hot-Melt |

| Acrylics |

| Polyurethanes |

| Ethylene-Vinyl Acetate (EVA) |

| Styrenic Block Copolymers |

| Natural/Bio-based |

| Flexible Packaging |

| Folding Cartons and Boxes |

| Labels and Tapes |

| Sealing |

| Other Applications (Tissue and Towel Over-wrap, Graphics and Specialty) |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| Industrial and Consumer Goods |

| E-Commerce Retail Fulfilment |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Technology | Water-based | |

| Solvent-based | ||

| Hot-Melt | ||

| By Resin Chemistry | Acrylics | |

| Polyurethanes | ||

| Ethylene-Vinyl Acetate (EVA) | ||

| Styrenic Block Copolymers | ||

| Natural/Bio-based | ||

| By Application | Flexible Packaging | |

| Folding Cartons and Boxes | ||

| Labels and Tapes | ||

| Sealing | ||

| Other Applications (Tissue and Towel Over-wrap, Graphics and Specialty) | ||

| By End-Use Industry | Food and Beverage | |

| Pharmaceuticals and Healthcare | ||

| Personal Care and Cosmetics | ||

| Industrial and Consumer Goods | ||

| E-Commerce Retail Fulfilment | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the packaging adhesives market?

The packaging adhesives market size was USD 21.91 billion in 2026 and is projected to reach USD 29.11 billion by 2031, registering a CAGR of 5.85%.

Which technology holds the largest share?

Water-based systems led with 57.42% of revenue in 2025, driven by stricter VOC rules and energy-saving benefits.

Which end-use segment is growing fastest?

E-commerce retail fulfillment is advancing at a 7.05% CAGR thanks to surging parcel volumes and automated distribution centers.

Why are bio-based adhesives gaining traction?

Brands' pledge to increase renewable content by 2030 is pushing formulators toward bio-based resins, which are growing at 6.82% annually.

Which region offers the most growth potential?

Asia-Pacific accounts for 40.35% of demand and is expanding at a 6.62% CAGR, led by China and India.

Page last updated on: