Mexico Commercial Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.14 Billion |

| Market Size (2026) | USD 4.24 Billion |

| Market Size (2031) | USD 4.72 Billion |

| Growth Rate (2026 - 2031) | 2.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Commercial Printing Market Analysis by Mordor Intelligence

The Mexico Commercial Printing Market size is projected to expand from USD 4.14 billion in 2025 and USD 4.24 billion in 2026 to USD 4.72 billion by 2031, registering a CAGR of 2.18% between 2026 to 2031.

Driven by near-shoring, the Mexico commercial printing market is experiencing brisk demand for short-run packaging, compliance labeling and point-of-sale (POS) collateral that legacy offset plants struggle to supply profitably. Brand owners relocating production into Querétaro, Monterrey and the northern border states now ask for variable-data jobs with 48-hour turnarounds, pushing converters toward hybrid digital-flexo presses. At the same time, food and beverage manufacturers are expanding recyclable-substrate initiatives under the January 2026 Circular Economy Law, spurring investment in water-based flexography and ultraviolet (UV) curing systems. Electricity tariffs rose 6-8% in 2024, prompting small and medium enterprises (SMEs) to tap FIDE’s subsidized loans for photovoltaic arrays and LED curing, while stricter volatile-organic-compound (VOC) norms from SEMARNAT accelerate the migration away from solvent inks. Despite chronic operator shortages, the Mexico commercial printing market continues to attract capital as equipment suppliers open local service hubs and offer peso-denominated financing.

Key Report Takeaways

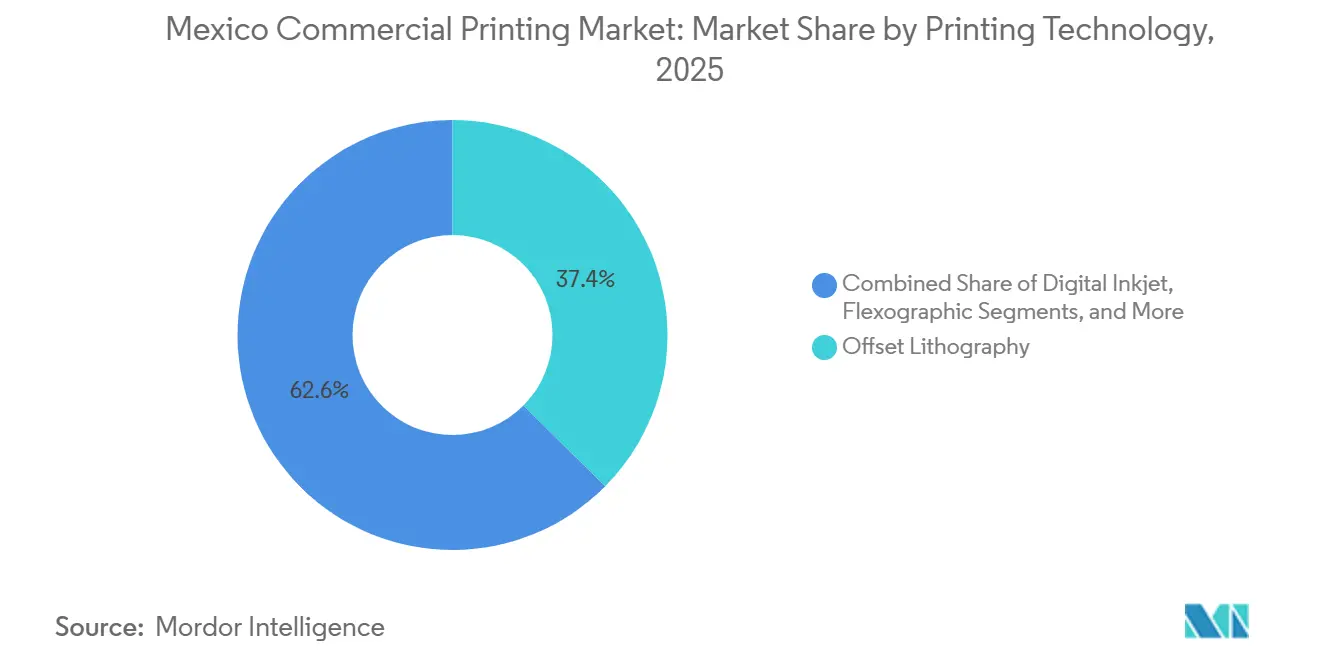

- By printing technology, offset lithography led with 37.43% of Mexico commercial printing market share in 2025, while digital inkjet is projected to expand at a 3.37% CAGR through 2031.

- By application, packaging accounted for 53.48% of the Mexico commercial printing market size in 2025 and is advancing at a 3.23% CAGR to 2031.

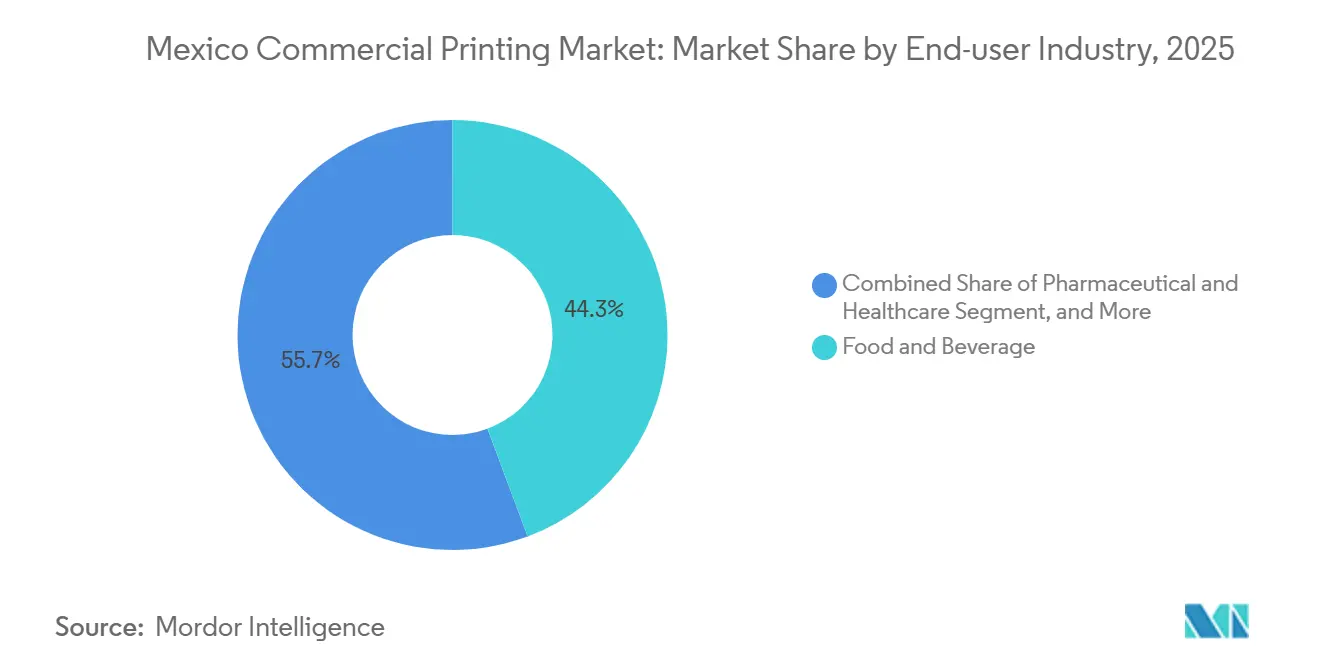

- By end-user industry, food and beverage contributed 44.31% revenue share in 2025, whereas retail and e-commerce is forecast to record the fastest 3.16% CAGR through 2031.

- By substrate type, paper and paperboard dominated with 58.23% share in 2025, but plastic films and labels are poised to grow at a 2.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Commercial Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand Growth in Packaging and Labels | +0.8% | National, high in Querétaro, Estado de México, Jalisco | Medium term (2-4 years) |

| Expansion of Mexico’s Retail POS and OOH Advertising | +0.3% | National, early gains in Mexico City, Monterrey, Guadalajara | Short term (≤ 2 years) |

| Rapid Adoption of High-Speed Digital Inkjet Presses | +0.5% | National, first movers in Mexico City metro, Querétaro | Medium term (2-4 years) |

| Brand Owner Push for Sustainable Substrates and Inks | +0.4% | National, spill-over to Central America corridors | Long term (≥ 4 years) |

| Near-shoring Boosts Short-Run Print Demand for US Trade | +0.6% | Northern border states and Bajío | Short term (≤ 2 years) |

| Government Energy-Efficiency Financing for SME Print Shops | +0.2% | National, higher uptake in Estado de México, Puebla | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand Growth in Packaging and Labels

Packaging and labels accounted for 53.48% of 2025 revenue and will outpace all other uses at a 3.23% CAGR as Coca-Cola FEMSA, Grupo Bimbo, and other beverage and bakery giants add capacity while meeting the front-of-package warning-label rules tightened in 2024. The two leading bottlers processed more than 31.5 thousand tons of recycled PET and cut virgin plastic by over 2,100 tons, forcing converters to certify ink migration on food-grade recycled resin [1]Coca-Cola FEMSA, “Form 20-F 2024,” coca-colafemsa.com. SIG’s USD 35 million Querétaro expansion, scheduled to go online in 2H 2026, will lift aseptic-carton output by 50%, opening new volume for UV-cured flexo coatings. Draft waste-management amendments targeting 20% recycled content by 2025 and 30% by 2030 further lock in substrate innovation.

Expansion of Mexico’s Retail POS and OOH Advertising

Retail media spend is moving from USD 1.99 billion in 2024 toward USD 3.2 billion by 2030, led by OXXO’s roll-out of 8,000+ in-store digital screens. Rapid campaign refresh cycles lift weekly demand for shelf-talkers and window clings produced on digital inkjet presses, while static billboard volumes slip as LED displays take share. Labelexpo Mexico 2025 showcased hybrid workflows that marry digital personalization with flexographic economics, giving converters the flexibility needed for omnichannel retailers.

Rapid Adoption of High-Speed Digital Inkjet Presses

Digital inkjet is the fastest-growing technology segment at 3.37% CAGR to 2031 as HP Indigo 6K, Domino and Durst platforms cut makeready time by up to 30% compared with legacy flexo lines. Flexopolis’ second BOBST Master M5 press, installed December 2024, combines inline cameras with PrintTutor register control to slash waste during changeovers, illustrating how modular presses boost capacity without enlarging footprints. Local service expansions by HP, Netstal and Koenig and Bauer reduce downtime and encourage SME adoption.

Brand Owner Push for Sustainable Substrates and Inks

The January 2026 Circular Economy Law formalized extended producer responsibility and recyclability thresholds, accelerating the shift to water-based and UV-ink systems compatible with polyethylene and mono-material film structures. Grupo Bimbo already counts 94% of global packaging as recyclable and diverted 4,861 tons of waste in 2024, setting a procurement precedent that ripples across supply chains.[2]Grupo Bimbo, “Annual Report 2024,” grupobimbo.comNew IFRS S1/S2 disclosures beginning with 2026 filings oblige listed firms to audit Scope 3 emissions from packaging, so printers supplying multinational brands must document substrate origin and ink chemistry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digitisation and Media Substitution | -0.5% | National, acute in urban centers | Long term (≥ 4 years) |

| Feedstock (Paper/Pulp) Price Volatility | -0.4% | National, tied to global commodity swings | Short term (≤ 2 years) |

| Stricter VOC and Solvent-Based Ink Regulations | -0.2% | Major metros, especially Monterrey and Mexico City | Medium term (2-4 years) |

| Shortage of Skilled Press Operators | -0.3% | Border maquiladoras and Bajío industrial corridor | Medium term (2-4 years) |

| Escalating Electricity Tariffs | -0.3% | SMEs lacking solar in most regions | Short term (≤ 2 years) |

| Consolidation Compresses SME Margins | -0.2% | Mexico City metro and Querétaro clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Digitisation and Media Substitution

Banks, utilities and government agencies accelerated e-statement rollout, shrinking transactional volumes by double digits annually. Banco de México’s polymer note program extended 20-peso note durability from 8.3 months to 28.8 months, reducing annual replacements 42% and trimming security-printing runs [3]Banco de México, “Counterfeit Note Statistics,” banxico.org.mx. Advertising continues its digital pivot, and new permits restrict packaging characters for high-sugar foods, lowering print complexity and revenue per job.

Feedstock (Paper/Pulp) Price Volatility

Containerboard prices dropped from USD 725 per ton in January 2024 to USD 650 by Q4 2024. However, fluctuations in pulp prices, recycled PET, and foreign-exchange rates continue to impact margins. This is particularly challenging for small and medium-sized enterprises (SMEs) that lack hedging programs [4]Banco de México, “Counterfeit Note Statistics,” banxico.org.mx. Additionally, with recycled polymer premiums sitting at 10-20% above virgin resin prices, costs are further inflated. This comes at a time when legislation mandates a 20% recycled content by 2025. While larger converters are securing multi-year contracts, smaller offset houses frequently opt for spot purchases, leaving them vulnerable to market volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Digital Inkjet Captures Growth Momentum

Offset lithography retained a 37.43% share of the Mexico commercial printing market in 2025, yet its expansion prospects are muted amid buyers' demand for variable data and SKU agility. Digital inkjet, though smaller, is set to capture the bulk of the incremental Mexico commercial printing market size thanks to a 3.37% CAGR that underscores its appeal for runs under 5,000 sheets. Flexographic presses remain staples for labels and flexible packaging, but hybrid configurations combining UV-inkjet heads with servo-driven flexo stations blur traditional boundaries and offer converters a pathway to faster setup and lower waste.

HP Indigo’s 6K installations, Domino’s N610i modules, and Durst’s Tau platform provide converters with inline varnish, die-cutting, and embellishment without halt, elevating margins in premium shrink-sleeve and pressure-sensitive label work. Meanwhile, BOBST Master M5 lines at Flexopolis demonstrate how automated registration delivers 30% higher throughput versus older gear. Gravure persists in high-volume snack laminates yet faces solvent-regulation headwinds, while screen and pad printing consolidate into niche tactile and industrial marking. The upshot is a technology slate where digital inkjet leads growth and offset cedes share, locking in a multi-speed future for the Mexico commercial printing market.

By Application: Packaging Extends Its Lead Amid Publishing Decline

Packaging accounted for 53.48% of 2025 revenue and will continue to gain share as the Mexico commercial printing market size expands to USD 4.72 billion by 2031. Demand stems from Coca-Cola FEMSA’s 2.124 billion unit cases and Grupo Bimbo’s nationwide bakery network, both of which require pressure-sensitive labels, shrink sleeves, and carton blanks that comply with tighter recyclability rules.

Publishing, catalog, and magazine work keeps shrinking as consumers gravitate online, while advertising morphs from large static billboards to short-cycle POS materials refreshed weekly in convenience chains. Security printing volumes drop because polymer banknotes last longer, yet complexity rises with RFID and QR anti-counterfeiting layers. Industrial manuals and compliance labels tied to near-shoring give a counterweight, but the revenue gravity remains firmly with packaging inside the Mexico commercial printing market.

By End-User Industry: Retail and E-Commerce Picks Up Speed

Food and beverage accounted for 44.31% of 2025 spending in the Mexico commercial printing market, reflecting beverage bottlers' and bakery giants’ reliance on wraparound labels and flexible packs. Retail and e-commerce, however, is the standout growth engine, clocking a 3.16% CAGR as online merchandise sales head for USD 66.3 billion by 2028.

Digital shelf-edge labels, QR-encoded promotion flyers, and branded corrugated mailers are cascading through OXXO’s 8,000-screen network and nationwide fulfillment centers. Pharmaceutical, healthcare, and automotive users collectively add demand for tamper-evident labels and multilingual manuals, though tight regulatory cycles often shift print to compliant specialists. Overall, retail acceleration ensures diverse touchpoints continue to flow into the Mexico commercial printing industry, even as entrenched food clients maintain scale.

By Substrate Type: Plastic Films and Labels Gain Ground

Paper and paperboard accounted for 58.23% of 2025 usage, yet stringent recycled-content targets are driving brand owners toward lightweight polyethylene, BOPP, and PET films. Plastic films and labels are therefore projected to outpace board at a 2.94% CAGR, contributing meaningfully to incremental growth in Mexico's commercial printing market share through 2031.

Coca-Cola FEMSA’s recycled-PET target already sits at 30%, and Grupo Bimbo fashions corner boards from recovered bread wrappers, moves that raise ink-migration and adhesion hurdles for converters. Metalized foils remain relevant in premium coffee and confectionery niches, but high material costs cap volumes. Netstal’s new Querétaro unit quickens the shift to label-less bottle formats requiring in-mold decoration. Substrate choice is thus becoming a strategic lever for cost, circularity and brand-story alignment across the Mexico commercial printing market.

Geography Analysis

Near-shoring has concentrated fresh capital along Mexico’s northern border and the Bajío corridor, funneling high-mix, low-volume label orders into Nuevo León, Chihuahua, and Querétaro. Monterrey printers routinely shuttle compliance labels across the Texas border within 48 hours, leveraging duty-free USMCA lanes, whereas wage inflation and operator churn have driven up automation adoption. Mexico City and Estado de México remain the largest clusters by establishment count, anchored by publishing, advertising, and consumer goods packaging, but rising industrial tariffs have sped up solar-panel adoption under FIDE’s Eco-Crédito Empresarial.

Querétaro’s manufacturing tax incentives helped lure SIG’s aseptic carton expansion, creating spillover demand for UV-cured flexo and plate-making capacity. Guanajuato and Aguascalientes, integral to the automotive chain, require multi-language technical literature and under-hood label stocks resistant to heat and fluids, widening the specialty print footprint. Central America, served by Chiapas and Tabasco, offers growth headroom but still trails Mexico’s robust infrastructure.

Regional disparities in water availability and electricity reliability complicate investment calculus. SEMARNAT’s forthcoming water-rights revision could cap withdrawals in drought-prone states, while electricity tariffs vary by up to 15% across time-of-use bands. SMEs that cannot deploy rooftop solar or water-recycling loops may relocate or exit, further clustering capacity in power-stable industrial parks. Even with these constraints, the Mexico commercial printing market continues to benefit from its geographic proximity to United States customers.

Competitive Landscape

Mexico’s printing scene is notably fragmented, with Quad/Graphics de México, Grupo Litoprint and Litho Formas commanding only a modest slice of the Mexico commercial printing market. Scale leaders differentiate through investments in high-speed inkjet presses, automated registration controls, and enterprise resource planning integration that streamline prepress-to-ship. For instance, Litho Formas retains ISO 14298 central bank certification for secure print, giving it a moat around ballots and brand-protection items.

Consolidation pressures mount as multinational packaging groups pursue bolt-on acquisitions to lock in regional capacity. ProMach’s 2024 purchase of Etiflex illustrates how foreign acquirers view Mexican label shops as strategic footholds. Equipment vendors bolster the transition, with HP financing peso-denominated leases and BOBST bundling service agreements that minimize downtime. These dynamics elevate technology access as the decisive factor separating growth converters from commodity offset houses.

SMEs still dominate by number, yet battle rising input costs and talent shortages. Electricity hikes slice margins for shops running metal-halide curing lamps, and experienced press operators often migrate to better-paying automotive plants. Government credit lines partly ease the burden, but many family-run firms lack the collateral or financial sophistication to qualify. As a result, competitive intensity is shifting toward mid-tier players able to blend localized service with digitized workflows.

Mexico Commercial Printing Industry Leaders

Ink Throwers DE Mexico SA

Dataprint Mexico

Central Print Mexico

Imprime TUS Ideas

Grupo Formex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SIG committed USD 35 million to expand its Querétaro aseptic-carton plant, targeting a 50% capacity lift and six new carton formats, go-live slated for 2H 2026.

- April 2025: Labelexpo Mexico 2025 hosted 450+ exhibitors, unveiling HP Indigo 6K presses, Flexivel’s 12-color flexo machine and multiple hybrid lines, underscoring supplier faith in Mexico

- February 2025: SIG opened a Reliability and Performance Center in Querétaro to deliver remote asset support for North American filling-line customers.

- January 2025: Netstal established Netstal Máquinas in Santiago de Querétaro, enhancing local sales and service for closure and preform injection systems.

Mexico Commercial Printing Market Report Scope

The Mexico Commercial Printing Market Report is Segmented by Printing Technology (Offset Lithography, Digital Inkjet, Flexographic, Gravure, Screen, Other Printing Technologies), Application (Packaging, Advertising, Publishing, Security and Transactional Printing, Other Applications), End-User Industry (Food and Beverage, Retail and E-Commerce, Pharmaceutical and Healthcare, Industrial and Automotive, Other End-User Industry), Substrate Type (Paper and Paperboard, Plastic Films and Labels, Metal/Foil, Other Substrates), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Offset Lithography |

| Digital Inkjet |

| Flexographic |

| Gravure |

| Screen |

| Other Printing Technologies |

| Packaging |

| Advertising |

| Publishing |

| Security and Transactional Printing |

| Other Applications |

| Food and Beverage |

| Retail and E-Commerce |

| Pharmaceutical and Healthcare |

| Industrial and Automotive |

| Other End-User Industry |

| Paper and Paperboard |

| Plastic Films and Labels |

| Metal/Foil |

| Other Substrates |

| By Printing Technology | Offset Lithography |

| Digital Inkjet | |

| Flexographic | |

| Gravure | |

| Screen | |

| Other Printing Technologies | |

| By Application | Packaging |

| Advertising | |

| Publishing | |

| Security and Transactional Printing | |

| Other Applications | |

| By End-User Industry | Food and Beverage |

| Retail and E-Commerce | |

| Pharmaceutical and Healthcare | |

| Industrial and Automotive | |

| Other End-User Industry | |

| By Substrate Type | Paper and Paperboard |

| Plastic Films and Labels | |

| Metal/Foil | |

| Other Substrates |

Key Questions Answered in the Report

How large will the Mexico commercial printing market be by 2031?

The market is forecast to reach USD 4.72 billion by 2031, expanding at a 2.18% CAGR from 2026-2031.

Which application segment is growing the fastest?

Packaging is advancing at a 3.23% CAGR through 2031 as food and beverage and e-commerce demand recyclable, short-run packs.

Why is digital inkjet adoption accelerating?

Brand owners require variable data, rapid changeovers and substrate flexibility, making high-speed inkjet presses the most economical choice for runs under 5,000 impressions.

How are sustainability regulations affecting printers?

The 2026 Circular Economy Law mandates recycled-content thresholds, driving a shift to water-based and UV-curable inks and increasing certification requirements for converters.

What financing options exist for SMEs upgrading equipment?

FIDE’s Eco-Crédito Empresarial offers subsidized loans repaid via monthly electricity bills, enabling SMEs to install solar panels and energy-efficient curing systems.

Which regions in Mexico see the most near-shoring-driven print demand?

Nuevo León, Chihuahua and the Bajío corridor receive heavy foreign investment, generating fast-turnaround orders for compliance labels and packaging.

Page last updated on: