Dermatophytic Onychomycosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 3.14 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dermatophytic Onychomycosis Treatment Market Analysis by Mordor Intelligence

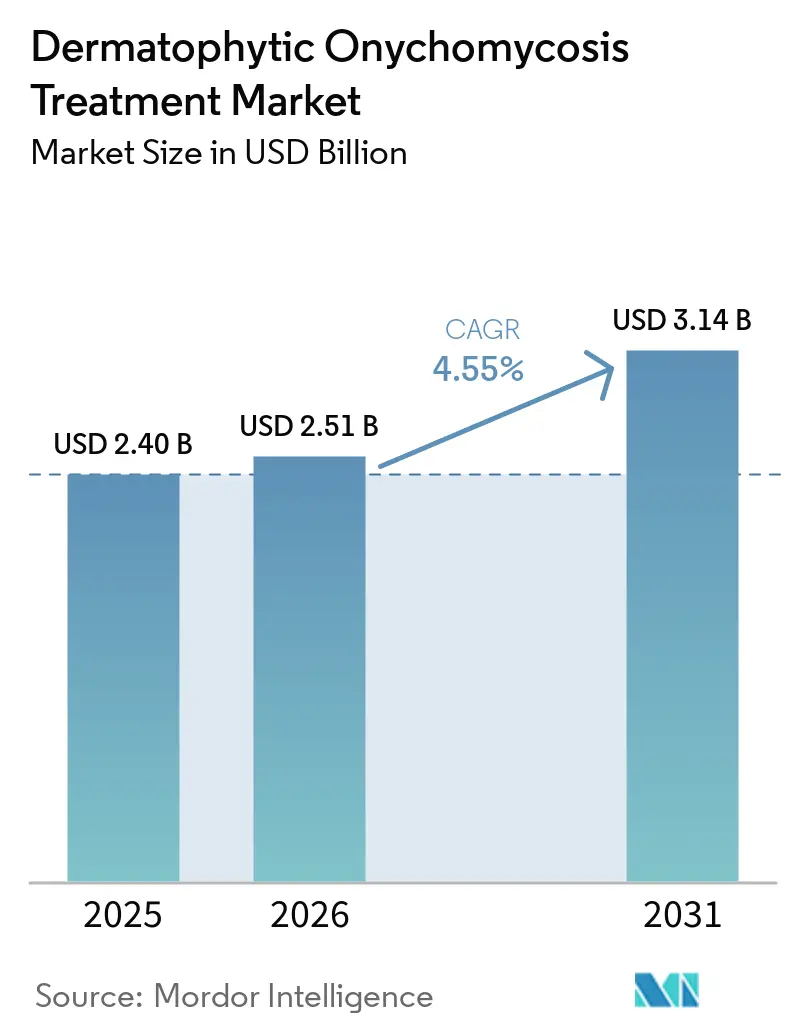

The Dermatophytic Onychomycosis Treatment Market size is expected to grow from USD 2.40 billion in 2025 to USD 2.51 billion in 2026 and is forecast to reach USD 3.14 billion by 2031 at 4.55% CAGR over 2026-2031.

The market is being supported by a broad patient pool that is expanding in parallel with diabetes and population aging, both of which raise infection risk and also make treatment more clinically important. Demand is also being lifted by a large untreated population, because laboratory confirmation remains limited and many diagnosed patients still do not receive antifungal therapy, which leaves room for future treatment conversion as diagnostic workflows improve. Product access is broadening through a mix of branded innovation, generic depth, OTC reclassification in selected European markets, and online pharmacy adoption, which is changing how patients enter treatment and refill therapy. At the same time, the dermatophytic onychomycosis treatment market is being reshaped by better topical delivery systems, which are improving nail penetration and narrowing the historical performance gap with oral therapy in mild-to-moderate cases. Competitive strategy is therefore moving in 2 directions, with low-cost generics defending volume while companies with differentiated delivery platforms and regional launch partnerships target premium niches and faster-growth access channels.

Key Report Takeaways

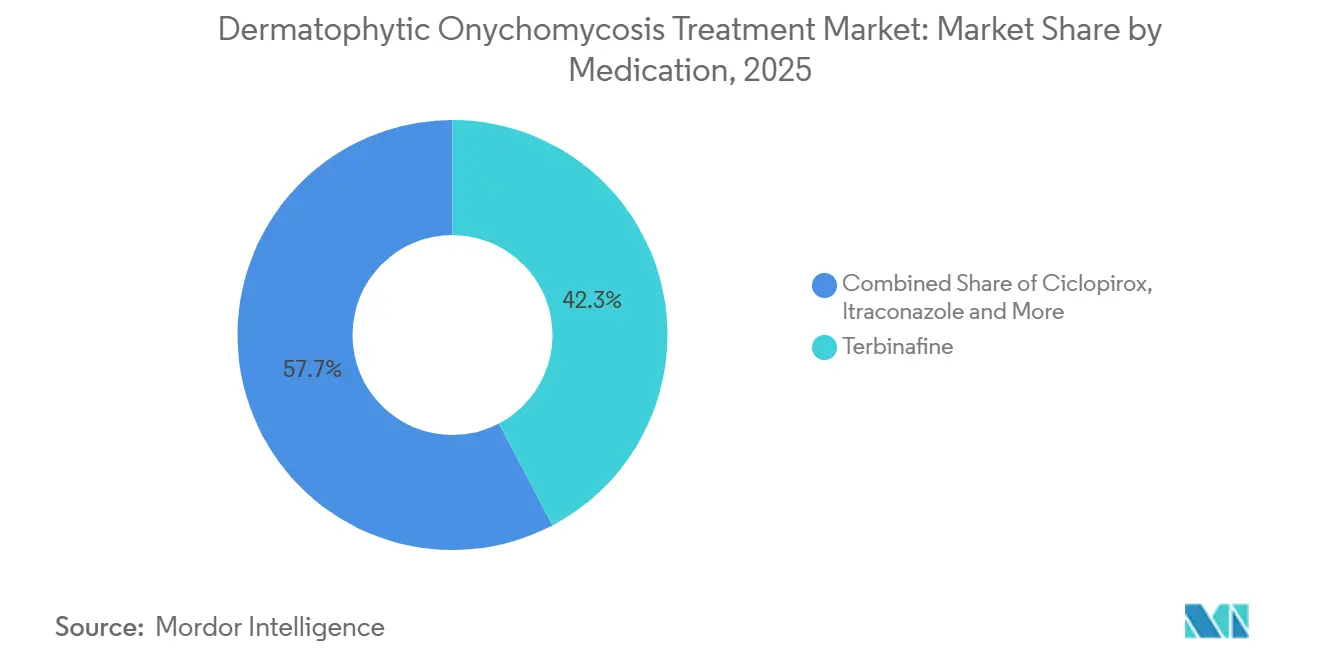

- By medication, terbinafine held 42.31% of the dermatophytic onychomycosis treatment market share in 2025, while ciclopirox is projected to expand at a 6.38% CAGR through 2031.

- By product type, tablets accounted for 57.24% of the dermatophytic onychomycosis treatment market size in 2025, while nail paints are forecast to grow at a 5.52% CAGR through 2031.

- By treatment route, oral therapy captured 59.52% share in 2025, while topical therapy is projected to advance at a 5.25% CAGR through 2031.

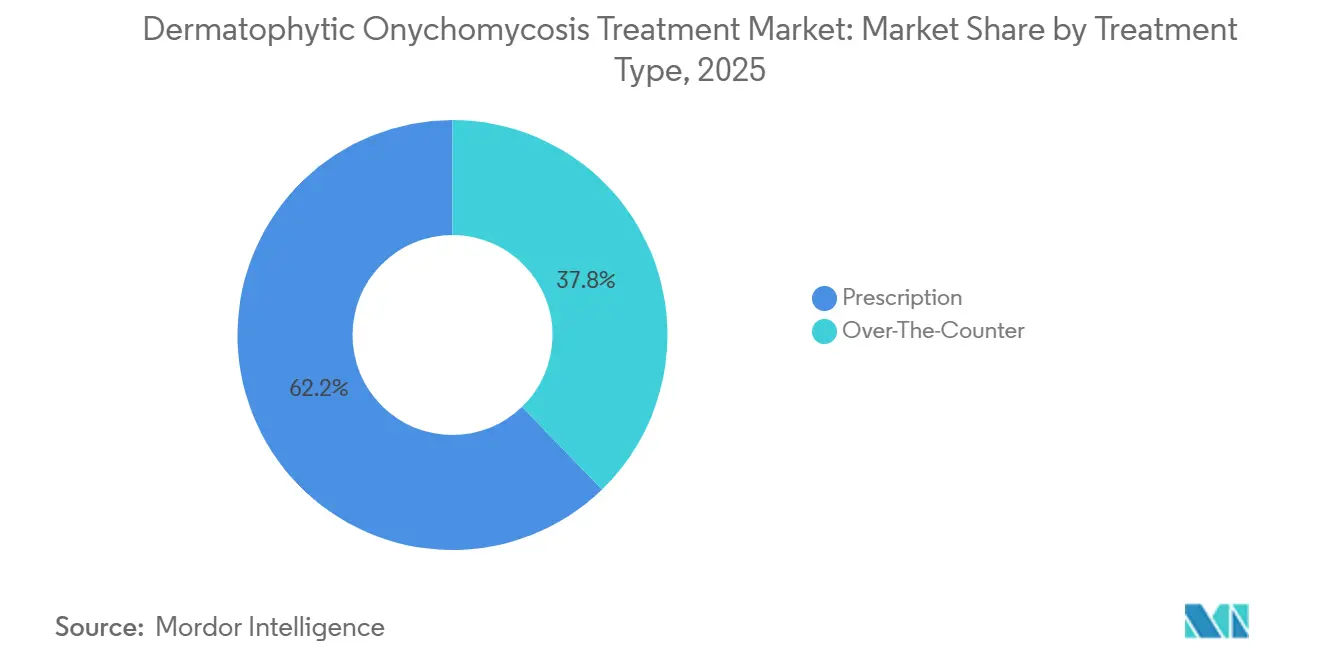

- By treatment type, prescription products held 62.24% share in 2025, while OTC products are expected to have a 6.52% CAGR through 2031.

- By distribution channel, retail pharmacies led with 42.56% share in 2025, while online pharmacies are expected to grow at a 6.85% CAGR through 2031.

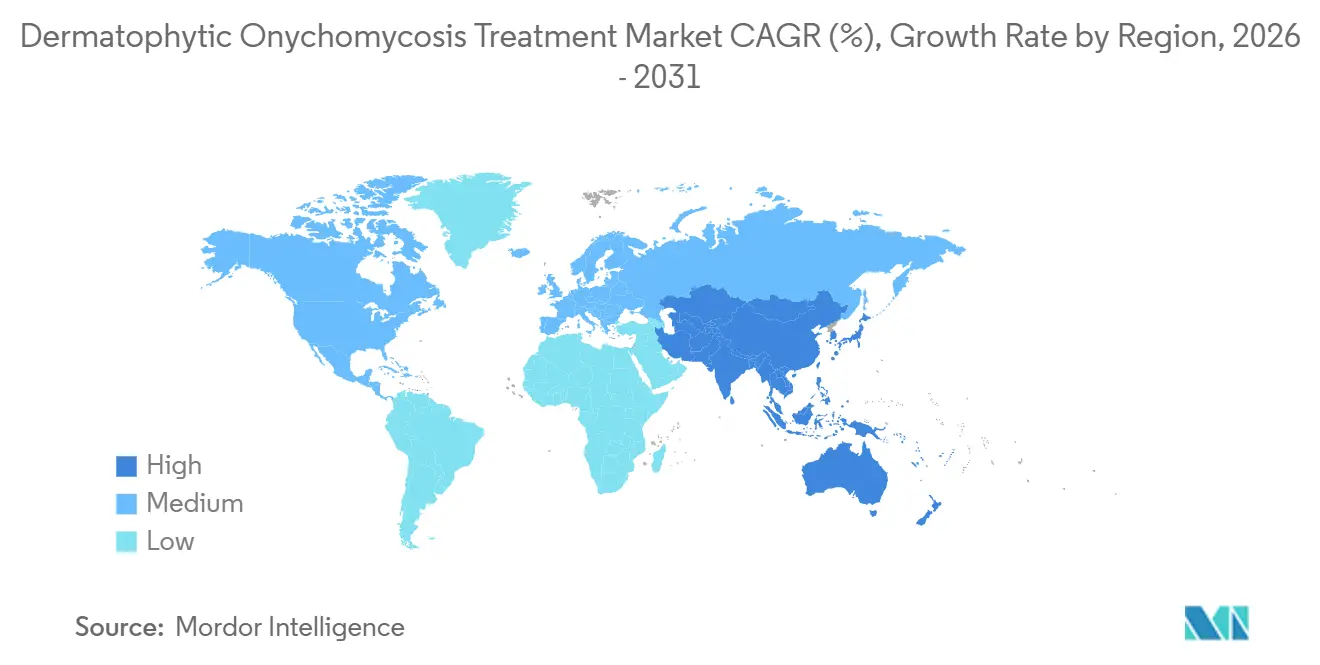

- By geography, North America held 38.22% share in 2025, while Asia-Pacific is projected to expand at a 6.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dermatophytic Onychomycosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Dermatophyte Burden in Aging and Diabetic Populations | +1.2% | Global, with amplified effect in APAC and North America | Long term (≥ 4 years) |

| Preference Shift Toward Topical Therapies With Better Cosmetic Acceptance | +0.6% | North America & EU | Medium term (2-4 years) |

| Expanding Access To Specialist Dermatology and Retail Pharmacy Channels | +0.4% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Growing Use of Advanced Nail Penetration Technologies | +0.7% | North America & Europe | Medium term (2-4 years) |

| Underdiagnosis Creating Latent Treatment Conversion Opportunity | +0.3% | Global, with early conversion in North America | Short term (≤ 2 years) |

| Recurrence Management Driving Repeat Prescriptions and Combination Therapy Uptake | +0.5% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Dermatophyte Burden in Aging and Diabetic Populations

The dermatophytic onychomycosis treatment market is most firmly supported by diabetes-linked demand, because diabetes affected 589 million people worldwide in 2024 and many of these patients face conditions that raise fungal nail infection risk and complicate treatment. The same evidence base shows that diabetic individuals face up to 2.8 times greater odds of developing onychomycosis than non-diabetic individuals, which keeps this patient pool central to long-run therapy demand. Aging adds a second structural layer, because geriatric patients face 4.7 times greater onychomycosis risk than the general population as nail growth slows and cumulative dermatophyte exposure rises over time. The effect on the dermatophytic onychomycosis treatment market is broader than simple case growth, because these patients often need longer treatment, closer follow-up, and more careful management when neuropathy, immune dysfunction, or poor nail perfusion are present. Clinical burden also matters beyond dermatology, because diabetic nail infection can feed into wound-care and podiatry management pathways, which expands the practical prescriber base for therapy. This makes the dermatophytic onychomycosis treatment market less dependent on cosmetic demand alone and more connected to chronic disease management in older and higher-risk populations.

Growing Use of Advanced Nail Penetration Technologies

The dermatophytic onychomycosis treatment market is also being lifted by better topical delivery, because poor penetration through the keratin nail plate had long limited topical efficacy and kept oral therapy in a stronger position. In a 2024 randomized clinical trial, ciclopirox 8% with hydroxypropyl chitosan showed 3.25-fold higher permeability than older reference lacquer formulations, which directly supports the newer growth profile for premium topical formats. Separate laboratory work showed that microporation combined with optimized gel vehicles further improved drug flux across the nail plate, which strengthens the case for technology-led differentiation in this category. The commercial proof point became clearer in 2025, when Moberg Pharma stated that Terclara, a water-soluble terbinafine nail lacquer using HPCH technology, achieved 76% mycological cure in Phase III trials and quickly became the market leader in Norway after launch. These gains matter for the dermatophytic onychomycosis treatment market because they improve the value proposition of topical treatment in mild-to-moderate disease and support OTC positioning in selected European markets. They also shift competitive advantage toward companies that own delivery intellectual property rather than toward companies competing only on generic price[1]Moberg Pharma AB, “Terclara Launch in Norway,” Moberg Pharma Press Release, mobergpharma.com.

Underdiagnosis Creating Latent Treatment Conversion Opportunity

The dermatophytic onychomycosis treatment market still has meaningful room to expand within diagnosed care settings, because treatment conversion remains low relative to the number of patients seen in practice. Lipner and colleagues reported that fewer than 25% of U.S. outpatient visits with an onychomycosis diagnosis involved confirmatory mycological testing and that antifungal treatment was prescribed in only 20% to 25% of such visits. The same treatment gap is tied to diagnostic uncertainty, because clinical diagnosis without laboratory confirmation is accurate in only about 50% of cases, which makes prescribers more cautious when systemic treatment requires monitoring and counseling. This leaves the dermatophytic onychomycosis treatment market with a practical growth path that depends less on finding new patients and more on confirming existing cases with better workflow tools. Walker and colleagues also showed that Black patients were 25% more likely to be diagnosed with onychomycosis but 42% less likely to receive efinaconazole prescriptions than White patients, which points to a second conversion gap linked to access and prescribing differences. As PCR and high-volume dermatology testing workflows improve, the dermatophytic onychomycosis treatment market can gain from higher confirmed-positive rates and a stronger chance that each confirmed case proceeds to therapy.

Recurrence Management Driving Repeat Prescriptions and Combination Therapy Uptake

The dermatophytic onychomycosis treatment market benefits from the fact that treatment does not always end with a single course, because recurrence risk keeps patients in follow-up and often extends therapy use beyond the initial regimen. In U.S. practice data, combination oral-plus-topical therapy was documented in 32.4% of treated patients and treatment switching occurred in another 30.7%, which shows that clinical management already goes beyond simple one-product use. This pattern raises product utilization per patient and supports steady refill behavior across both prescription and maintenance-oriented topical formats. The dermatophytic onychomycosis treatment market is also supported by newer maintenance evidence, because a 2025 publication by Gupta and Cooper reported no relapse over a 48-month maintenance study with efinaconazole 10% applied 2 to 3 times weekly. That evidence shifts clinician behavior toward planned maintenance instead of waiting for visible recurrence, especially in patients with prior treatment failure or comorbid risk factors. The result is a more durable revenue profile for the dermatophytic onychomycosis treatment market, because repeat prescriptions and combination therapy become part of routine care rather than exceptional use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Treatment Duration Depresses Adherence and Persistence | -0.7% | Global | Long term (≥ 4 years) |

| Oral Antifungal Safety Concerns Limit High-Value Prescribing | -0.5% | North America & Europe | Medium term (2-4 years) |

| Limited Reimbursement and High Out-Of-Pocket Cost in Several Markets | -0.4% | North America & MEA | Medium term (2-4 years) |

| Therapeutic Resistance and Biofilm Persistence Reduce Cure Confidence | -0.6% | Global, with early emergence in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long Treatment Duration Depresses Adherence and Persistence

The dermatophytic onychomycosis treatment market still faces a basic adherence problem, because visible nail improvement arrives slowly even when fungal control is achieved earlier in the course of therapy. The user input showed that oral terbinafine regimens commonly run for 3 to 6 months in toenails, while topical monotherapy can extend to 9 to 12 months for a single affected toenail, which makes persistence difficult in routine care. This weighs on the dermatophytic onychomycosis treatment market because many patients judge progress by cosmetic clearing rather than by mycological response, and that delay weakens motivation to continue treatment. The burden is especially relevant in elderly and diabetic populations, where longer treatment windows overlap with polypharmacy, mobility limits, and lower tolerance for repeated follow-up. Digital reminders and teledermatology follow-up can help, but the dermatophytic onychomycosis treatment market does not yet benefit fully from these tools because adoption remains uneven across the highest-risk patient groups. Until treatment timelines become easier to manage or easier to explain, adherence drag will continue to limit realized outcomes and branded product persistence in daily practice.

Therapeutic Resistance and Biofilm Persistence Reduce Cure Confidence

The dermatophytic onychomycosis treatment market is also facing a more serious clinical constraint from antifungal resistance, especially as resistant dermatophyte strains move beyond their earlier geographic base. The CDC reported that Trichophyton indotineae accounted for 38% of all dermatophyte isolates referred to the UK National Mycology Reference Laboratory in 2024, which signals a meaningful challenge to confidence in first-line terbinafine use[2]CDC, “Spread of Antifungal-Resistant Trichophyton indotineae, United Kingdom, 2017–2024,” Emerging Infectious Diseases, cdc.gov. The problem is amplified by biofilm behavior, because 2024 evidence linked strong biofilm-producing dermatophyte isolates with higher antifungal MICs and a 2 to 3 times greater association with prior oral antifungal treatment failure. This pushes the dermatophytic onychomycosis treatment market toward new mechanisms and more selective treatment choice, rather than depending only on broader use of existing oral agents. Vanda Pharmaceuticals is already testing VTR-297, a topical HDAC inhibitor with a distinct fungal mechanism, in Phase II clinical development, which shows how resistance is shaping pipeline direction. As stewardship measures and susceptibility awareness expand, the dermatophytic onychomycosis treatment market may gain from innovation, but near-term prescribing confidence in standard therapy remains under pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Medication: Terbinafine’s Lead Intact but Resistance Narrows the Gap

Terbinafine held 42.31% of segment revenue in 2025, which kept it as the largest medication in the dermatophytic onychomycosis treatment market because it remains the standard first-line systemic option for dermatophyte-led infection. Its lead reflects 3 reinforcing factors, guideline familiarity, broad generic supply, and strong clinical acceptance in moderate-to-severe disease where deeper fungal involvement limits what topical therapy can do. In cost-sensitive settings this leadership is still durable, because generic oral therapy fits the reimbursement and pricing logic that shapes a large share of established prescribing pathways. Even so, the medication mix inside the dermatophytic onychomycosis treatment market is starting to change because reliance on a single first-line oral agent also creates exposure to resistance concerns and safety-related prescribing hesitation. That shift does not remove terbinafine from its leading position, but it does reduce the ease with which it can extend share from here, especially where resistant strains are entering routine clinical awareness.

Ciclopirox is the fastest-growing medication at a 6.38% CAGR through 2031, and that pace shows how formulation improvement is changing what older molecules can deliver in the dermatophytic onychomycosis industry. HPCH delivery technology has improved nail penetration, while clinical practice evidence in 2025 showed that combination ciclopirox-terbinafine therapy outperformed oral monotherapy in real-world records analyzed with artificial intelligence. That combination role matters, because it supports ciclopirox both as a standalone topical option in milder disease and as an adjunct in higher-risk or recurrent cases. Itraconazole continues to hold a defensive place for patients who cannot use terbinafine or who need an alternative oral path when resistance concerns are stronger. Fluconazole remains relevant in practice because of low cost and physician familiarity, even though its dermatophyte-specific profile is less compelling than terbinafine. Amorolfine keeps a useful weekly-application topical niche across Europe and Asia, which gives the dermatophytic onychomycosis treatment market a broader range of adherence-oriented options outside the U.S.

By Product Type: Tablet Durability Tested by Nail Paint Innovation

Tablets accounted for 57.24% of the dermatophytic onychomycosis treatment market size in 2025, reflecting the continuing need for oral systemic treatment in cases where disease depth and nail involvement reduce the expected effect of surface therapy. The tablet format also benefits from established physician habit, mature generic availability, and straightforward dosing that fits existing care pathways in dermatology, podiatry, and primary care. For many clinicians, tablets still define the core treatment backbone of the dermatophytic onychomycosis treatment market when disease is moderate or severe and rapid fungal suppression matters more than cosmetic preferences. That keeps the category durable, even while some patients and physicians prefer to avoid monitoring demands associated with systemic therapy. The leading position of tablets therefore remains grounded in clinical necessity rather than in format preference alone.

Nail paints are forecast to grow at a 5.52% CAGR through 2031, which makes them the most dynamic product format as improved delivery systems raise efficacy expectations in milder disease. The clearest validation came from Moberg Pharma, which reported 76% mycological cure for Terclara in Phase III trials compared with up to 42% for prior comparators. Those data matter because they turn nail paints from a lower-efficacy legacy format into a more credible treatment choice within the dermatophytic onychomycosis treatment market. Better cosmetic acceptance also supports this shift, since many patients are more willing to stay on a visible and non-systemic format when the performance tradeoff becomes less severe. The growth of nail paints therefore reflects both science and behavior, not just packaging format. As a result, the dermatophytic onychomycosis treatment market is likely to see a more balanced split between oral and advanced topical product forms over the forecast period.

By Treatment Route: Oral Holds Share While Topical Disrupts the Prescribing Calculus

Oral therapy held 59.52% of route revenue in 2025 and retained the largest share of the dermatophytic onychomycosis treatment market because oral drugs still reach deeply embedded fungal elements more reliably in advanced disease. This route remains especially important where nail thickening, multi-nail involvement, or higher-risk diabetic status makes clinicians prioritize systemic clearance. Oral therapy also fits long-standing treatment algorithms, so physician familiarity keeps it central to established practice in large developed markets. That said, route leadership no longer guarantees easy share expansion, because safety concerns and resistance awareness now shape prescribing decisions more directly than before. The oral segment therefore remains large, but the balance of advantage is less secure than it was when topical efficacy was weaker.

Topical therapy is projected to grow at a 5.25% CAGR through 2031, which shows how the dermatophytic onychomycosis treatment market is gradually moving toward route de-escalation where disease severity permits. This route benefits from improved formulation performance, lower concern around systemic monitoring, and better patient acceptance among older adults who are less suitable for oral therapy. The dermatophytic onychomycosis treatment market is seeing that effect more clearly in mild-to-moderate presentations, where physicians now have a stronger basis for choosing topical-first therapy than they had under older lacquer technologies. Japan adds an important regional signal, because updated 2025 skin fungal disease guidance incorporated stronger evidence for oral antifungals while also including new resistance data, which sharpened the oral versus topical decision rather than settling it in one direction. That kind of guidance change matters because it can shift route choice by patient profile, not just by molecule. Over time, this leaves the dermatophytic onychomycosis treatment market with a route mix that is likely to become more segmented by severity, age, and recurrence history.

By Treatment Type: OTC Momentum Signals a Consumer Health Pivot

Prescription products accounted for 62.24% of revenue in 2025, which kept them ahead in the dermatophytic onychomycosis treatment market because moderate-to-severe disease still requires clinician oversight and systemic treatment remains central in many cases. Prescription dominance is also reinforced by diagnostic uncertainty, since laboratory confirmation is still limited and prescribers remain cautious when deciding between observation, testing, and therapy escalation. In other words, the larger prescription position reflects clinical structure as much as commercial channel design. It also explains why branded innovation continues to focus on products that can satisfy both physician confidence and patient persistence. The prescription base therefore remains important for value capture in the dermatophytic onychomycosis treatment market even as consumer behavior starts to shift.

OTC products are projected to grow at a 6.52% CAGR through 2031, which makes them the faster treatment type as patients seek simpler and more independent care paths. This growth has been supported by OTC classification for 7 of Terclara’s 13 European regulatory approvals, which shows that better topical performance can unlock broader consumer access. The dermatophytic onychomycosis treatment market is also benefiting from teledermatology, because digital diagnosis and recommendation support allow patients to move toward treatment without a traditional in-person consultation in every case. Historically, OTC products suffered from weaker efficacy and lower confidence, but higher-penetration formulations are narrowing that gap and changing how consumers assess self-care options. This shift is especially relevant in mild and cosmetically bothersome cases, where patients often prefer convenience over intensive medical supervision. The faster OTC pace therefore signals a wider consumer health turn inside the dermatophytic onychomycosis treatment market rather than a simple channel expansion.

By Distribution Channel: Online Pharmacy Surge Reshapes Commercial Strategy

Retail pharmacies held 42.56% of revenue in 2025 and represented the largest channel in the dermatophytic onychomycosis treatment market because they remain the first practical touchpoint for many patients with mild or newly noticed nail symptoms. Pharmacists also help patients navigate OTC selection, visible symptom discussion, and referral to physicians when disease appears more severe or persistent. This physical channel advantage remains important in a category where product choice often follows visual judgment and where many consumers still value immediate product access. Retail locations therefore continue to anchor baseline demand in the dermatophytic onychomycosis treatment market even as digital channels grow faster. Drug stores and clinic-linked dispensing also remain relevant in severe or diabetic-foot cases that require specialist oversight and combination therapy handling.

Online pharmacies are forecast to expand at a 6.85% CAGR through 2031, which makes them the fastest distribution channel in the dermatophytic onychomycosis treatment market. Growth comes from 3 linked behaviors, discreet purchasing for a visible but sensitive condition, easier repeat ordering for long treatment periods, and teleconsultation links that reduce friction in obtaining advice or prescriptions. The importance of scale is already visible in Europe, where Redcare Pharmacy reported strong 2025 growth and outlined further expansion in 2026, showing that e-pharmacy platforms are becoming more influential in branded and repeat-use categories. For the dermatophytic onychomycosis treatment market, that means channel strategy is moving beyond shelf presence and into digital visibility, refill design, and integrated remote care. It also gives OTC and maintenance-oriented products a stronger route to consumer scale than they had in earlier years. As a result, online pharmacy growth is changing both access patterns and promotional priorities across the dermatophytic onychomycosis treatment market.

Geography Analysis

North America held 38.22% of global revenue in 2025 and therefore remained the largest regional contributor to the dermatophytic onychomycosis treatment market share. The region’s position rests on high disease prevalence, broad access to dermatology and podiatry care, and a mature formulary mix that includes both branded and generic antifungal options. The U.S. also shows the clearest treatment-conversion gap, because many diagnosed visits still do not progress to confirmatory testing or drug treatment, which leaves room for volume expansion if diagnosis improves. Europe follows with steadier expansion, supported by established prescription dermatology pathways, rising topical innovation, and a staggered regulatory pathway for efinaconazole across member states after the decentralized procedure was completed in 2024.

Asia-Pacific is the fastest-growing region, with the dermatophytic onychomycosis treatment market size in this geography projected to expand at a 6.65% CAGR through 2031. The region benefits from a combination that is harder to find in mature markets, rising diabetes burden, expanding private dermatology access, and wider use of government-backed telemedicine that helps underserved patients reach treatment pathways. Japan remains a key reference point because topical-first prescribing has historically been common among older patients who are less suitable for systemic treatment. Updated 2025 skin fungal disease guidance in Japan added new resistance information and stronger oral evidence, which is likely to make route choice more selective rather than uniformly topical-first. Kaken’s launch of an authorized generic efinaconazole nail solution in Japan and its China development activity show how regional companies are using intra-Asian pathways to extend dermatology assets across multiple markets[3]Kaken Pharmaceutical, “Partial Revisions of Long-Term Business Plan 2031,” Kaken Pharmaceutical, kaken.co.jp.

The Middle East and Africa and South America remain smaller contributors, but both are adding incremental demand to the dermatophytic onychomycosis treatment market as access improves. In MEA, GCC countries stand out for stronger OTC antifungal spending and consumer awareness, while South Africa offers the most structured pharmaceutical distribution base in sub-Saharan Africa. In South America, Brazil benefits from a growing private dermatology clinic network and broader prescription access, while more volatile reimbursement conditions in Argentina continue to favor generics over premium topical brands. Across both regions, wider online pharmacy use is helping reduce reliance on traditional brick-and-mortar constraints, which should gradually improve access for OTC and maintenance products.

Competitive Landscape

The dermatophytic onychomycosis treatment market remains fragmented, with no single company holding a major share by global value and no single strategy dominating all regions. Volume is still heavily influenced by generics, especially in terbinafine and ciclopirox, because physicians and health systems often favor lower-cost options in routine cases. At the same time, branded players keep premium niches where delivery performance, cosmetic acceptance, and OTC potential create reasons for patients to pay more. That balance leaves the dermatophytic onychomycosis treatment market open to both scale-based generic competition and innovation-led premium positioning.

One clear strategic pattern is regional partnership expansion around differentiated topical products. Moberg Pharma’s partnership with Karo Healthcare covers 19 European markets and is designed to roll out Terclara under the Lamisil brand where approvals allow, which gives the company scale without building a full standalone commercial base in each country. A second example comes from Almirall, which completed the decentralized approval procedure for efinaconazole in Europe and positioned itself to build a broader topical prescription franchise across major EU markets. A third example comes from Kaken Pharmaceutical, which commercialized an authorized generic efinaconazole in Japan while also progressing efinaconazole development in China through a local partner, showing a regionally efficient asset-extension model. These moves show that the dermatophytic onychomycosis treatment market is rewarding companies that can pair science, channel access, and regulatory reach rather than relying on molecule ownership alone.

The second broad strategy track is innovation against resistance and commoditization. As resistant dermatophytes become a clearer issue, novel mechanisms such as Vanda Pharmaceuticals’ Phase II HDAC inhibitor candidate VTR-297 are drawing attention because they can offer differentiation beyond the allylamine and azole classes. In parallel, companies with proprietary nail delivery technologies such as HPCH matrices or water-soluble lacquer systems are building a stronger commercial moat than firms that sell standard topical formats without delivery advantages. Moberg’s Phase III data in 817 patients has already become a visible benchmark for advanced topical efficacy, which raises the standard that future entrants may need to meet if they want premium positioning or OTC expansion in Europe.

Dermatophytic Onychomycosis Treatment Industry Leaders

Bausch Health Companies Inc.

Pfizer Inc.

Galderma S.A.

Novartis AG

Kaken Pharmaceutical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Almirall launched Jublia (efinaconazole 89 mg/mL topical solution) as the first topical triazole antifungal for onychomycosis in the German Rx dermatology market. Approved for patients aged 6 and older, Jublia competes directly with ciclopirox and oral terbinafine in Germany.

- September 2025: Kaken Pharmaceutical's authorised generic efinaconazole nail solution 10% began commercial sales in Japan, following its listing on the Japanese national drug pricing system in June 2025.

Global Dermatophytic Onychomycosis Treatment Market Report Scope

As per the scope of the report, dermatophytic onychomycosis treatment refers to the medical approaches used to eliminate fungal infections of the nails caused by dermatophyte fungi. This condition affects the toenails and fingernails, leading to discoloration, thickening, and brittleness of the nails.

The dermatophytic onychomycosis treatment market is segmented by medication into terbinafine, itraconazole, fluconazole, ciclopirox, amorolfine, and other medications. By product type, the market is categorized into tablets and nail paints. Based on the treatment route, it is divided into oral and topical treatments. By treatment type, the segmentation includes prescription and over-the-counter options. The market is further segmented by distribution channel into retail pharmacies, online pharmacies, drug stores, and other channels. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Terbinafine |

| Itraconazole |

| Fluconazole |

| Ciclopirox |

| Amorolfine |

| Other Medication |

| Tablets |

| Nail Paints |

| Oral |

| Topical |

| Prescription |

| Over-The-Counter |

| Retail Pharmacies |

| Online Pharmacies |

| Drug Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Medication | Terbinafine | |

| Itraconazole | ||

| Fluconazole | ||

| Ciclopirox | ||

| Amorolfine | ||

| Other Medication | ||

| By Product Type | Tablets | |

| Nail Paints | ||

| By Treatment Route | Oral | |

| Topical | ||

| By Treatment Type | Prescription | |

| Over-The-Counter | ||

| By Distribution Channel | Retail Pharmacies | |

| Online Pharmacies | ||

| Drug Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the dermatophytic onychomycosis treatment market by 2031?

The dermatophytic onychomycosis treatment market is projected to reach USD 3.14 billion by 2031 from USD 2.51 billion in 2026, at a CAGR of 4.55%.

Which region currently leads global demand for dermatophytic onychomycosis treatment?

North America led with 38.22% share in 2025, supported by strong dermatology access, podiatry infrastructure, and broad availability of oral and topical antifungal options.

Why is Asia-Pacific growing faster than other regions in fungal nail therapy?

Asia-Pacific is projected to grow at a 6.65% CAGR through 2031 because diabetes burden is rising, private dermatology access is widening, and telemedicine is helping convert underserved patients into treated patients.

Which drug segment holds the largest share and which is growing the fastest?

Terbinafine held 42.31% of segment revenue in 2025, while ciclopirox is forecast to grow fastest at a 6.38% CAGR through 2031 as improved delivery systems support stronger clinical performance.

How are OTC products changing treatment access for onychomycosis?

OTC products are growing at a 6.52% CAGR through 2031, helped by improved topical formulations, selected OTC reclassifications in Europe, and teledermatology pathways that lower access barriers for mild-to-moderate cases.

What is the biggest clinical risk affecting future treatment choices?

Resistance is becoming the key risk, especially with Trichophyton indotineae making up 38% of dermatophyte isolates referred to the UK National Mycology Reference Laboratory in 2024, which could shift therapy toward alternative mechanisms and newer formulations.

Page last updated on: