Chromoblastomycosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

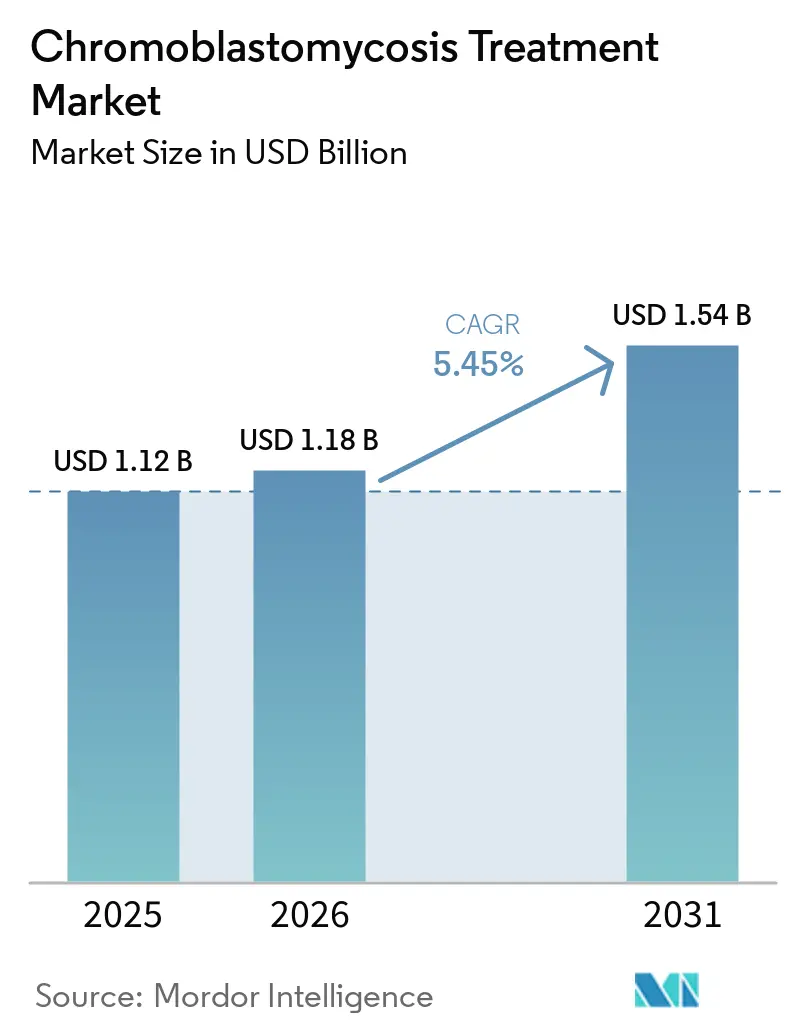

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

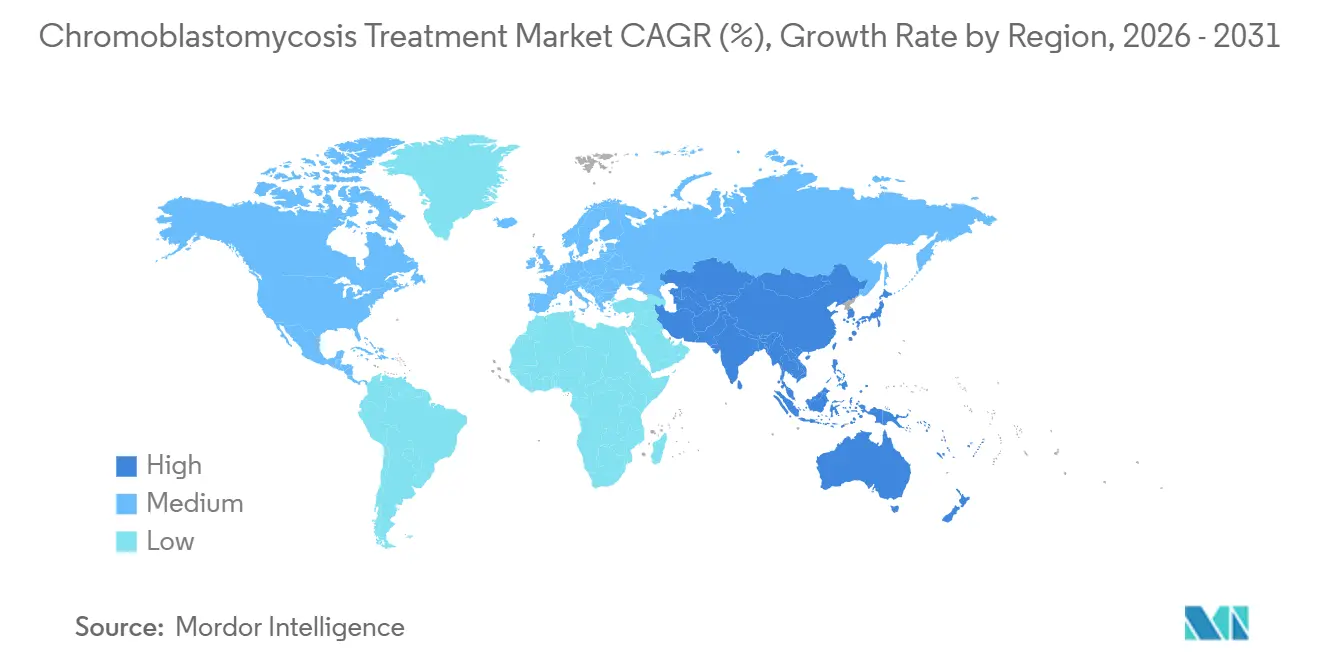

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chromoblastomycosis Treatment Market Analysis by Mordor Intelligence

The Chromoblastomycosis Treatment Market size is projected to expand from USD 1.12 billion in 2025 and USD 1.18 billion in 2026 to USD 1.54 billion by 2031, registering a CAGR of 5.45% between 2026 to 2031.

Rural and agricultural communities in tropical and subtropical regions have long faced challenges in accessing treatment for chromoblastomycosis. The World Health Organization's recognition of chromoblastomycosis as a neglected tropical disease and its inclusion in the NTD Road Map for 2025 to 2030 are driving improvements in diagnosis and treatment access in endemic regions. Enhanced surveillance and healthcare systems are uncovering previously undiagnosed cases, expanding the treatment base. The market is influenced by factors such as prolonged treatment durations, increased adoption of combination regimens, and the growth of outpatient specialist care, which support sustained drug usage. However, the market's growth depends on the ability of endemic countries to translate policy focus into actionable outcomes, including funded treatment pathways, improved diagnostics, and better adherence support.

Key Report Takeaways

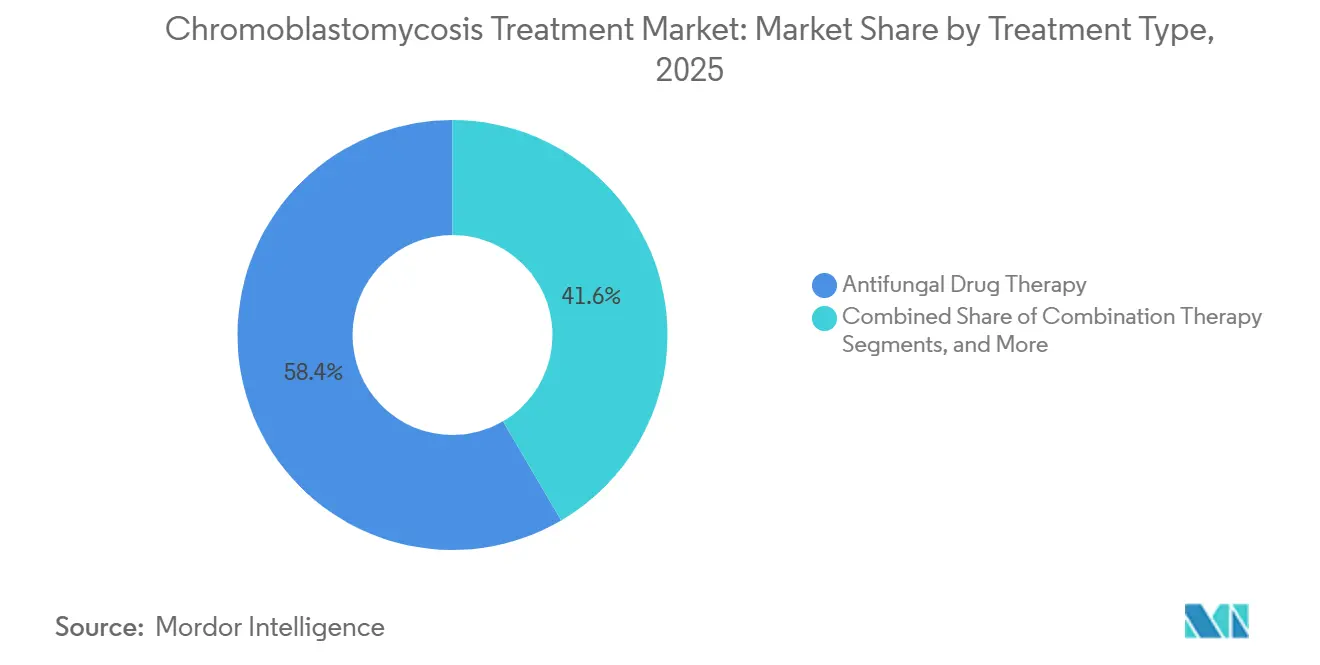

- By treatment type, antifungal drug therapy accounted for 58.45% of the chromoblastomycosis treatment market size in 2025, while combination therapy is projected to expand at a 5.66% CAGR through 2031.

- By drug class, azoles held 71.75% of the segment in 2025, led by itraconazole as the first-line therapy and posaconazole as the established second-line approved option.

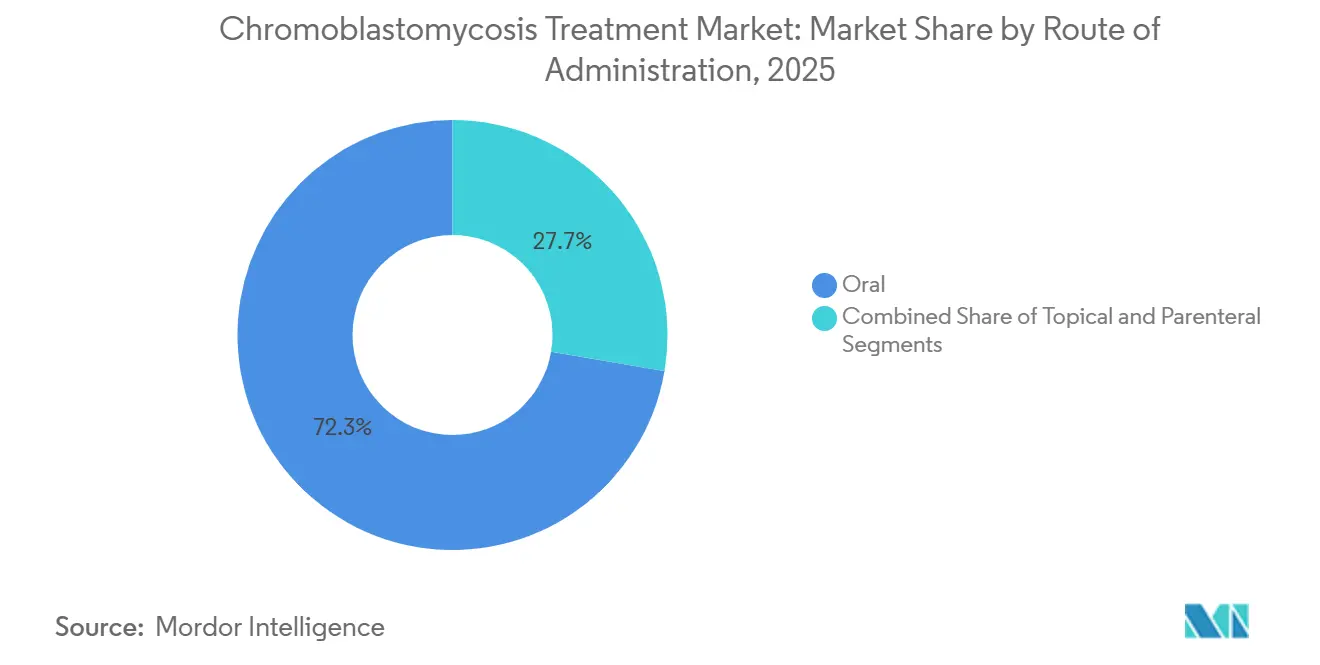

- By route of administration, oral formulations are projected to record a 6.55% CAGR through 2031, making them the fastest-growing administration route.

- By end user, hospitals held 46.93% of the chromoblastomycosis treatment market size in 2025, while dermatology clinics are projected to grow at a 6.12% CAGR through 2031.

- By geography, North America held 38.95% of the chromoblastomycosis treatment market share in 2025, while Asia-Pacific is projected to grow at a 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chromoblastomycosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Long-duration systemic antifungal therapy demand | +1.2% | Global | Medium term (2-4 years) |

| Diagnostic delay in endemic rural care pathways | +0.9% | Latin America, Sub-Saharan Africa, South Asia | Medium term (2-4 years) |

| Public procurement and donation models for itraconazole | +0.8% | Global (LMICs) | Long term (≥ 4 years) |

| Combination therapy use in refractory lesions | +1.1% | Global | Short term (≤ 2 years) |

| Underuse of species-level identification and susceptibility testing | +0.6% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Scarcity of affordable newer triazoles in endemic markets | +0.5% | Sub-Saharan Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Long-Duration Systemic Antifungal Therapy

The chromoblastomycosis treatment market benefits from the extended therapy durations required by most patients. Standard treatments last 8 to 36 months, with itraconazole typically administered at daily doses of 200 to 400 mg. This prolonged regimen results in significant cumulative drug demand for each patient episode. Itraconazole remains the primary agent for mild to severe cases, while terbinafine is frequently used in combination therapies. Cure rates for itraconazole monotherapy range from 15% to 80%, often necessitating extended treatments, second-line therapies, or combined regimens, further driving market demand. This trend ensures a consistent demand profile compared to acute infections, as consumption builds over extended periods.

Growing Use of Combination Therapy for Refractory Lesions

The market is witnessing a shift toward combination therapies for moderate to severe cases. Evidence shows improved outcomes when itraconazole is paired with terbinafine for Fonsecaea pedrosoi infections. DAT therapy, combining debulking, intralesional amphotericin B, and oral terbinafine, has emerged as a curative option for patients unresponsive to standard treatments. Adjunctive photodynamic therapy has demonstrated an 80% to 90% reduction in lesion size after six applications, highlighting the growing role of device-based modalities. Multi-modal approaches, such as combining cryotherapy, itraconazole, and topical 5-fluorouracil, are gaining clinical acceptance, achieving significant lesion clearance within months.

Persistent Diagnostic Delay in Endemic Rural Care Pathways

The diagnosed population in the chromoblastomycosis treatment market represents only a fraction of the actual disease burden. A Brazilian study from 2020 to 2025 revealed treatment delays ranging from 2 to 30 years due to limited access to dermatology services in rural areas. While global records documented 7,850 confirmed cases from 1914 to 2025, the true burden is estimated to exceed 10,000 cases, with Latin America accounting for 50% to 60%, Africa for approximately 1,875 cases, and Asia for around 1,394 cases.[1]World Health Organization, “Chromoblastomycosis,” World Health Organization, who.int Advances in molecular diagnostic methods, such as multiplex PCR, are expediting diagnoses and enabling earlier treatment, supporting market growth.

Public Procurement and Donation Models for Itraconazole

Public access initiatives are increasingly shaping the chromoblastomycosis treatment market, particularly in low-income endemic regions. Over 78 million individuals face challenges accessing itraconazole due to affordability and procurement gaps. Brazil’s Ministry of Health provides itraconazole free of charge for implantation mycoses, and similar models are being considered in countries like Madagascar, Venezuela, and India. WHO-led procurement and donation systems have distributed over 31 billion tablets since 2011, with nearly 1.5 billion tablets delivered in 2025 alone. Manufacturers entering public tender channels can unlock significant volumes in Latin America and sub-Saharan Africa, where access will drive market growth.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Long treatment duration and poor adherence | -1.8% | Global, highest impact in LMICs | Short term (≤ 2 years) |

| Limited clinical trial evidence and standardized guidelines | -1.2% | Global | Long term (≥ 4 years) |

| Low commercial incentive due to disease neglect and NTD status | -1.4% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Limited access to diagnostics and specialist dermatology care | -1.0% | Africa, South Asia, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long Treatment Duration and Poor Adherence

Poor adherence remains a significant challenge in the chromoblastomycosis treatment market. Daily or pulse itraconazole regimens, lasting 8 to 36 months, often face discontinuation due to costs, side effects, and the slow initial response of lesions. Interrupted therapy creates selective pressure, with studies showing higher itraconazole MICs in isolates during treatment, indicating resistance from incomplete cycles. This reduces clinical success and undermines the reliability of first-line therapy. Standard itraconazole's food-dependent absorption adds to challenges in lower-resource settings, while super-bioavailability itraconazole, developed to address this, remains unaffordable in many endemic areas.

Limited Clinical Trial Evidence and Standardized Guidelines

The chromoblastomycosis treatment market is constrained by limited clinical trial evidence and the absence of randomized controlled studies. No randomized trial has been conducted for any antifungal regimen, leaving practitioners reliant on case series, observational data, and expert judgment. This weak evidence base complicates regulatory clarity, reimbursement decisions, and the adoption of standardized protocols. The 2025 CDC Global Chromoblastomycosis Working Group emphasized the need for standardized guidelines and proposed the CURE ID platform to collect real-world evidence. However, progress is slow due to the geographically scattered disease burden and challenges in trial recruitment in under-resourced endemic areas.[2]Super-Bioavailability Itraconazole Versus Conventional Itraconazole in the Treatment of Endemic Mycoses, A Multicenter, Open-Label, Randomized Comparative Trial,” Journal of Clinical Microbiology via PMC, ncbi.nlm.nih.gov Without robust guidelines, the market will continue to rely on individualized treatment approaches over protocol-driven adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Combination Protocols Gaining Ground in Refractory Cases

In 2025, Antifungal Drug Therapy accounted for 58.45% of the chromoblastomycosis treatment market, highlighting the continued reliance on systemic azoles and allylamines for managing various disease severities. This includes itraconazole monotherapy for localized cases and complex oral regimens for chronic or severe lesions. Combination Therapy is projected to grow at a 5.66% CAGR from 2026 to 2031, driven by a shift toward multi-drug and multi-modal approaches when monotherapy proves insufficient.

Published evidence supports improved outcomes in moderate to severe cases when systemic drugs are combined with cryotherapy, laser treatments, or intralesional amphotericin B. Immunomodulatory agents like topical imiquimod are increasingly used alongside systemic azoles for challenging lesions, bridging infectious disease treatment and dermatology. While surgical excision and cryotherapy remain relevant for localized cases, the market is moving toward pharmaceutical-centered combinations, with physical modalities serving as complementary options. Drug-based protocols are expected to dominate the market during the forecast period.

By Drug Class: Azole Dominance Masking Undercurrent Shifts

Azoles held a 71.75% share of the chromoblastomycosis treatment market in 2025, reflecting their position as the leading drug class. Itraconazole remains the global first-line treatment, supported by established prescribing patterns in endemic regions. Posaconazole, the primary second-line azole, has regulatory approval for chromoblastomycosis and mycetoma, with case data showing successful outcomes in 9 of 11 patients.

Allylamines, led by terbinafine, are gaining traction due to their effectiveness in combination therapies and select monotherapy cases, with a 66% complete healing rate reported in F. pedrosoi infections over 12 months. Polyenes like amphotericin B are limited to severe cases due to toxicity concerns, while adjunctive agents such as flucytosine and topical imiquimod hold niche relevance. Drug repurposing efforts are identifying compounds with potential synergy with itraconazole, indicating gradual diversification within the market.

By Route of Administration: Oral Dominance Reinforced by Ambulatory Shift

Oral formulations are projected to grow at a 6.55% CAGR from 2026 to 2031, driven by their practicality for long treatment courses in outpatient and home-based care. This aligns with the broader shift toward ambulatory care models in endemic regions. Oral dosing remains the most scalable option for chronic care, given the extended treatment durations required.

Advancements in formulations, such as super-bioavailable itraconazole, have improved pharmacokinetics, addressing absorption variability challenges. Topical agents play a limited role due to poor penetration in deep infections, while parenteral therapies are reserved for severe cases in hospital settings. Generic oral itraconazole is expected to drive volume growth in regions like Brazil, India, Madagascar, and Venezuela, where public access models are critical.

By End User: Specialist Clinics Absorbing a Greater Share of Chronic Case Management

Hospitals accounted for 46.93% of the chromoblastomycosis treatment market in 2025, reflecting their role in managing severe cases requiring procedures, monitoring, or parenteral treatments. They remain essential for initial diagnosis and stabilization. However, Dermatology Clinics are projected to grow at a 6.12% CAGR through 2031, indicating a shift toward specialist outpatient settings for long-term management.

In countries like Brazil, reference centers for implantation mycoses are integrating diagnosis, drug dispensing, and follow-up into specialist outpatient models. Specialty Care Centers in North America and Europe manage travel-related and migration-linked cases. Teledermatology is expanding market reach by identifying cases in remote areas. As oral maintenance therapies become standardized, homecare and ambulatory care channels are expected to manage a larger share of stable moderate cases, reducing hospital dependency for chronic management.

Geography Analysis

In 2025, North America held a 38.95% share of the chromoblastomycosis treatment market, maintaining its position as the largest regional contributor. The region benefits from advanced dermatology infrastructure, access to branded azoles like posaconazole and voriconazole, and higher adoption of multi-drug combination protocols compared to many endemic low-income markets. The United States drives most of this value due to its academic medical centers specializing in travel-acquired and immigrant-associated cases. Canada and Mexico contribute smaller volumes, with Mexico’s northern semi-arid regions showing distinct infection patterns compared to humid-region diseases caused by Fonsecaea pedrosoi. Europe is also seeing a rise in non-endemic cases linked to migration from Africa and Latin America, highlighting challenges in timely diagnosis outside specialized tropical care.

Asia-Pacific is projected to grow at a 7.88% CAGR from 2026 to 2031, making it the fastest-growing region in the chromoblastomycosis treatment market. Improved case detection in India, China, South Korea, and Southeast Asia is addressing underreported cases. WHO data recorded 1,394 cases in Asia through 2024, including 169 in India and 71 in Japan, though the actual burden is likely higher due to incomplete surveillance. A 2026 study from Kerala identified F. nubica as the predominant species, emphasizing the need for region-specific treatment approaches. India’s strong generic pharmaceutical sector provides a cost-effective supply of itraconazole and terbinafine as diagnoses increase.

Latin America remains the primary disease-burden center in the chromoblastomycosis treatment market, with Brazil accounting for one of the largest national caseloads globally. Brazil’s public provision of itraconazole through a dedicated implantation mycoses program offers suppliers better volume visibility but limits premium pricing. Fonsecaea pedrosoi caused 84.1% of registered cases in Latin America and the Caribbean, enabling more standardized treatment protocols compared to Asia or Africa.

Competitive Landscape

In the chromoblastomycosis treatment market, generic first-line therapies dominate in volume, while specialist second-line antifungals command higher value. Indian firms, including Cipla, Sun Pharmaceutical Industries, Dr. Reddy’s Laboratories, Aurobindo Pharma, and Glenmark Pharmaceuticals, play a pivotal role in the supply chain for itraconazole and terbinafine, especially in endemic regions. Here, factors like pricing, distribution reach, and access to tenders overshadow brand identity. This dynamic ensures a competitive landscape at the first-line therapy level, with no single entity monopolizing prescriptions. Merck, however, carves out a unique niche with Noxafil. Posaconazole, under Noxafil, boasts explicit FDA and EMA endorsements for both chromoblastomycosis and mycetoma, bolstering its appeal in challenging refractory cases. This dichotomy between cost-effective generics and premium branded options shapes the market's current commercial landscape.

While pipeline activity is limited, its significance is underscored by the need for alternatives to azoles in resistant cases. SCYNEXIS emerges as a frontrunner in this arena. In January 2026, the company secured both FDA's Qualified Infectious Disease Product and Fast Track designations for SCY-247, targeting invasive fungal diseases. Though SCY-247 isn't currently designated for chromoblastomycosis, its unique mechanism and broad-spectrum potential position it as a viable future option, contingent on further evidence. Thus, the market still holds potential for innovations addressing refractory diseases outside the azole framework.

Efforts to improve delivery quality and accessibility are gaining momentum. Products enhancing itraconazole absorption in food-restricted or non-compliant patients could gain traction, addressing pharmacokinetic challenges. Research into repurposed molecules with synergistic effects against F. pedrosoi highlights the potential for academic and commercial collaborations to introduce adjunctive treatments. Companies combining affordability, tender access, and specialist credibility are best positioned to succeed in the chromoblastomycosis treatment market, ensuring relevance for generic manufacturers, branded azole players, and antifungal innovators alike.

Chromoblastomycosis Treatment Industry Leaders

Merck & Co., Inc.

Astellas Pharma Inc.

Pfizer Inc.

Gilead Sciences, Inc.

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SCYNEXIS, Inc. announced that the US FDA granted QIDP and Fast Track designations for SCY-247, its second-generation triterpenoid antifungal, ensuring a minimum of 10 years of market exclusivity post-approval.

- January 2026: SCYNEXIS initiated Phase 1 clinical dosing for SCY-247 in its IV formulation and plans to begin a Phase 2 oral study for invasive candidiasis later in 2026, with Phase 1 data showing promising safety and efficacy.

- May 2025: Cipla received approval to advance inhaled itraconazole dry powder (PUR1900) to Phase III clinical trials at a 40 mg dose, following successful Phase II results.

Global Chromoblastomycosis Treatment Market Report Scope

As per the scope of the report, chromoblastomycosis is a long-lasting skin fungal infection caused by contact with infected soil or wood. Treatment is challenging and requires a mix of antifungal medications, and in some cases, physical removal.

The chromoblastomycosis treatment market is segmented by treatment type, drug class, route of administration, end-user, and geography. By treatment type, the market includes antifungal drug therapy, surgical excision, cryotherapy, thermotherapy, and combination therapy. By drug class, the market is segmented into azoles, allylamines, polyenes, and adjunctive antifungal agents. By route of administration, the market is categorized into oral, topical, and parenteral. By end-user, the market is segmented into hospitals, dermatology clinics, specialty care centers, and homecare and ambulatory settings. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Antifungal Drug Therapy |

| Surgical Excision |

| Cryotherapy |

| Thermotherapy |

| Combination Therapy |

| Azoles |

| Allylamines |

| Polyenes |

| Adjunctive Antifungal Agents |

| Oral |

| Topical |

| Parenteral |

| Hospitals |

| Dermatology Clinics |

| Specialty Care Centers |

| Homecare And Ambulatory Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Antifungal Drug Therapy | |

| Surgical Excision | ||

| Cryotherapy | ||

| Thermotherapy | ||

| Combination Therapy | ||

| By Drug Class | Azoles | |

| Allylamines | ||

| Polyenes | ||

| Adjunctive Antifungal Agents | ||

| By Route Of Administration | Oral | |

| Topical | ||

| Parenteral | ||

| By End User | Hospitals | |

| Dermatology Clinics | ||

| Specialty Care Centers | ||

| Homecare And Ambulatory Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in chromoblastomycosis treatment demand?

Growth is tied to long treatment duration, rising case recognition in endemic regions, and wider use of combination therapy. The market is valued at USD 1.18 billion in 2026 and is projected to reach USD 1.54 billion by 2031 at a 5.45% CAGR.

Which treatment category leads current revenue generation?

Antifungal Drug Therapy leads with a 58.45% share in 2025 because systemic azoles and allylamines remain the core treatment approach across most disease severities.

Why is combination therapy gaining attention in difficult cases?

Combination regimens are being used more often in moderate and severe disease because published case evidence shows better lesion control and improved outcomes in refractory settings.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region with a 7.88% CAGR through 2031, supported by stronger case detection in countries such as India, China, and Indonesia.

Why do oral formulations remain so important?

Oral therapy is the most practical route for treatment courses that can last 8 to 36 months, and oral formulations are projected to grow at a 6.55% CAGR through 2031.

Which end-user setting is changing most quickly?

Hospitals still lead with 46.93% share in 2025, but Dermatology Clinics are growing faster at a 6.12% CAGR as long-term care shifts toward outpatient specialist management.

Page last updated on: