Global Dental Turbine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

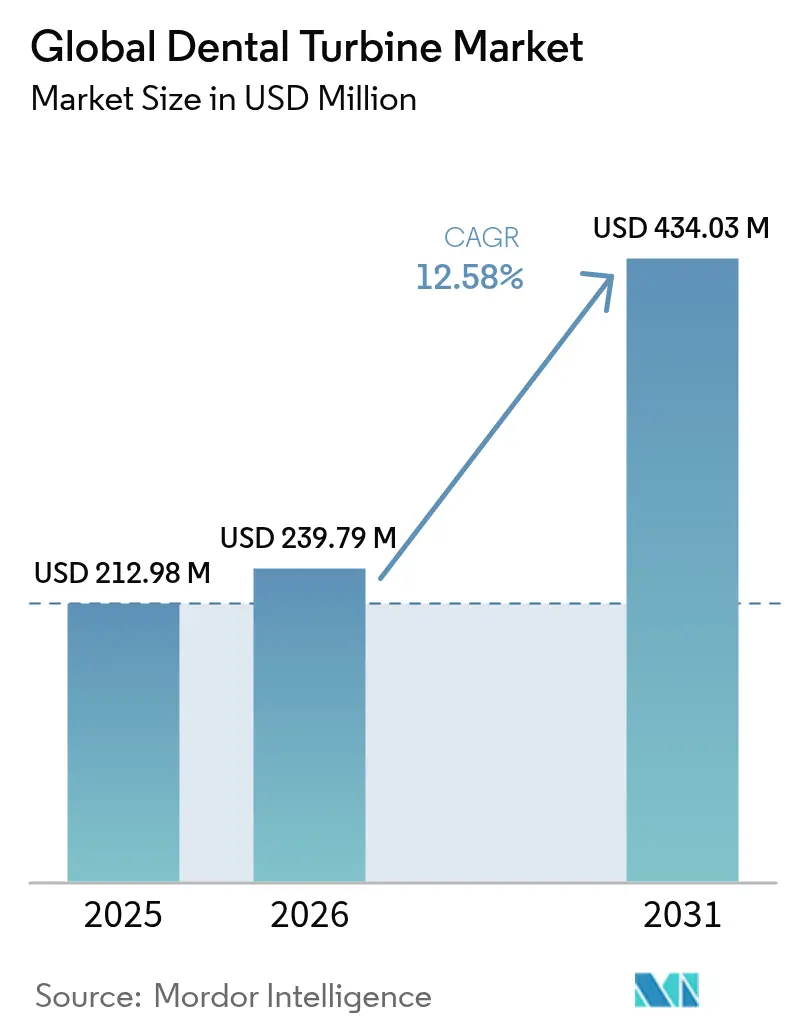

| Market Size (2026) | USD 239.79 Million |

| Market Size (2031) | USD 434.03 Million |

| Growth Rate (2026 - 2031) | 12.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Dental Turbine Market Analysis by Mordor Intelligence

The Dental turbine market size was valued at USD 212.98 million in 2025 and estimated to grow from USD 239.79 million in 2026 to reach USD 434.03 million by 2031, at a CAGR of 12.58% during the forecast period (2026-2031). Demand accelerates because infection-control upgrades became a permanent operating priority after the COVID-19 emergency, pushing clinics to adopt turbines that withstand repeated heat sterilization mandated by the Centers for Disease Control and Prevention. Uptake is further supported by digital dentistry investments that link turbines with chairside CAD/CAM systems, while subscription-based procurement models ease capital constraints for small practices. Electric and hybrid handpieces gain traction as empirical studies confirm their superior aerosol mitigation performance compared with air-driven tools. Competitive dynamics favor manufacturers that pair precision engineering with cloud-based maintenance analytics, creating added revenue from service contracts.

Key Report Takeaways

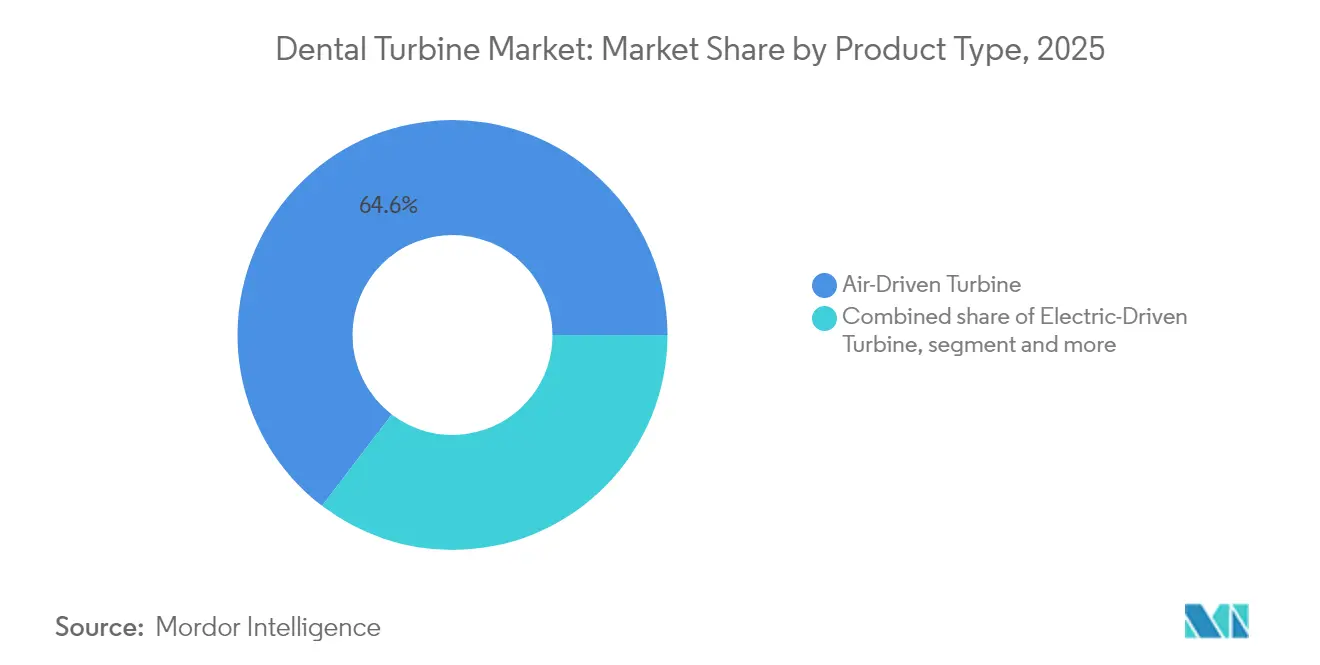

- By product type, air-driven turbines led with 64.62% of Dental turbine market share in 2025, whereas electric-driven units are on track for a 15.27% CAGR through 2031.

- By speed category, high-speed models dominated with 58.10% revenue share in 2025; low-speed variants are projected to expand at a 15.02% CAGR through 2031.

- By material, stainless-steel housings accounted for 62.45% of the Dental turbine market size in 2025, while titanium-alloy options are forecast to rise at 14.72% CAGR to 2031.

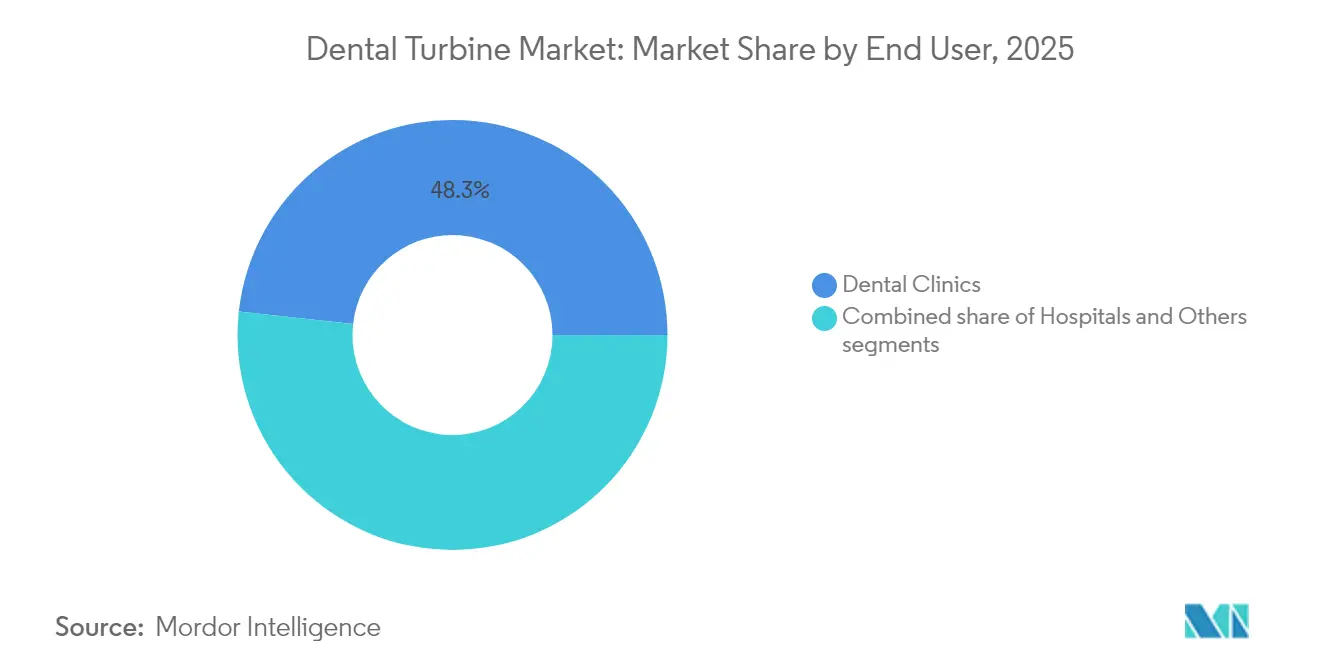

- By end user, dental clinics held 48.25% share of the Dental turbine market size in 2025, and the “Others” segment is growing at 15.68% CAGR to 2031.

- By distribution channel, traditional dealers retained 42.10% revenue share in 2025; online channels are advancing at a 15.95% CAGR through 2031.

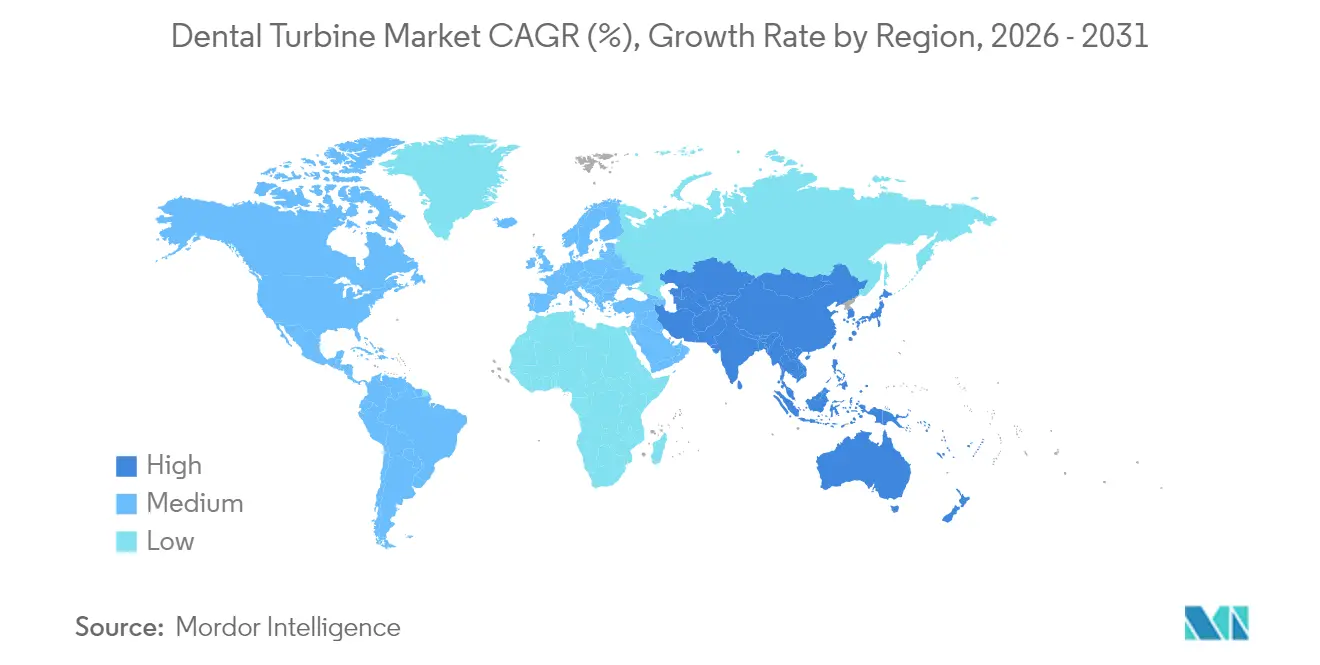

- By region, North America captured 39.30% of Dental turbine market share in 2025, while Asia-Pacific records the highest projected CAGR at 16.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Dental Turbine Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for cosmetic & minimally-invasive procedures | +2.1% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing global burden of dental caries & periodontal disease | +3.2% | Global, with highest impact in emerging markets | Long term (≥ 4 years) |

| Rapid adoption of electric & hybrid turbines for aerosol mitigation | +2.8% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| Integration with chairside CAD/CAM & digital workflows | +1.9% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Subscription-based "handpiece-as-a-service" procurement models | +1.5% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Emerging-market insurance expansion for restorative dentistry | +1.2% | APAC core, expanding to Latin America & MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cosmetic & Minimally-Invasive Procedures

Practices increasingly emphasize esthetic outcomes, driving a requirement for turbines that achieve smooth margins with low vibration. A 2024 survey reported that 81% of dentists view artificial intelligence as beneficial for cosmetic treatment planning, reinforcing demand for high-torque, precision instruments. Manufacturers respond with ergonomic designs such as KaVo’s EXPERTtorque E680 series, which provides 30 N bur retention and low noise to improve patient comfort. The shift is most visible in North America and Europe, where discretionary spending on elective dentistry remains high. Enhanced torque control supports minimally invasive approaches that preserve tooth structure, making the turbines integral to premium service offerings. Quieter operation also differentiates providers that market spa-like clinical environments.

Growing Global Burden of Dental Caries & Periodontal Disease

The World Health Organization links chronic oral infections with systemic conditions such as Alzheimer’s disease, prompting governments to prioritize restorative care that relies on high-performance turbines. Rising sugar consumption in urban Asia boosts untreated caries among youth, increasing procedure volumes in high-volume practices. Manufacturers extend warranty periods and reinforce key components so turbines withstand intensive daily cycles. Extended service intervals lower downtime for clinics confronting heavy caseloads, while durable bearings maintain cutting efficiency across repeated sterilization. Evidence of periodontal disease’s systemic impact elevates turbines from episodic tools to core infrastructure in public-health strategies aimed at reducing long-term treatment costs.

Rapid Adoption of Electric & Hybrid Turbines for Aerosol Mitigation

Peer-reviewed 2025 trials show that combining electric handpieces with high-volume evacuation reduces microbial aerosol concentration more effectively than traditional air-driven setups. Regulators and malpractice insurers promote technology that cuts airborne contamination, accelerating electric uptake in Europe and North America. Hybrid systems help clinics transition by offering air-line compatibility while adding direct-drive control that limits aerosol release. Evidence that high-speed rotation generates persistent micro-droplets has reoriented purchasing criteria toward infection-control performance. Manufacturer roadmaps prioritize sealed head designs and internal anti-retraction valves that maintain sterility under repeated sterilization.

Integration with Chairside CAD/CAM & Digital Workflows

In-office milling units costing USD 100,000 to USD 150,000 depend on precisely prepared margins to deliver accurate crowns in one visit. Turbines therefore require sensors that monitor torque and bur run-out in real time, feeding data into the digital workflow. Predictive maintenance alerts reduce unscheduled downtime, supporting the high patient-throughput model of digital dentistry. Early adopters are large group practices in the United States that standardize equipment across multiple sites, creating scale advantages for turbine makers with integrated software support. The resulting ecosystem locks clients into proprietary platforms, increasing switching costs and stabilizing revenue streams.

Restraints Impact Analysis of Global Dental Turbine Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & servicing costs of premium turbines | -1.4% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Viable substitutes (electric micromotors, laser dentistry) | -0.8% | Developed markets with advanced technology adoption | Medium term (2-4 years) |

| Noise-related occupational-health regulations | -1.1% | Europe & North America core, expanding globally | Medium term (2-4 years) |

| Stringent re-processing / sterilization turnaround times | -0.9% | Global, with highest compliance pressure in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Servicing Costs of Premium Turbines

Electric handpieces often exceed USD 5,000, stretching budgets for solo practices in Latin America and Southeast Asia. Total cost of ownership rises because improper lubrication and autoclave cycles shorten turbine life, with manufacturers attributing over 50% of failures to inadequate maintenance. Clinics lacking automated hygiene stations face additional labor costs and risk service-interrupting damage. Subscription leasing partially offsets upfront expense by bundling hardware, maintenance, and replacements into predictable fees, yet adoption remains limited to advanced markets.

Viable Substitutes (Electric Micromotors, Laser Dentistry)

Hard-tissue lasers eliminate mechanical contact and virtually all aerosols, challenging turbines in cavity preparations. Electric micromotors offer comparable cutting power at lower operating noise, appealing to practices focused on occupational-health compliance. Although substitute technologies carry higher initial costs, affluent patients increasingly request them. Turbine manufacturers counter through hybrid designs that integrate micromotor torque management while preserving familiar air-line connections, thereby broadening their value proposition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Dental Turbine Market Segment Analysis

By Product Type:

Electric Models Gain Infection Control EdgeElectric-driven units accounted for a smaller base but are on pace to expand at 15.27% CAGR through 2031, narrowing the gap with air-driven systems that held 64.62% Dental turbine market share in 2025. Clinics prioritize aerosol mitigation, and peer-reviewed data confirms plasma purification paired with electric turbines lowers airborne pathogen counts. Electric handpieces provide digitally controlled torque that prevents stalling during heavy cuts, enhancing chairside productivity.

Growth also reflects alignment with artificial-intelligence-enabled workflows embraced by 81% of surveyed dentists. Dental service organizations negotiate bulk contracts, accelerating volume shifts toward electric models. Hybrid turbines bridge the transition by using existing compressed-air infrastructure while embedding electric micro-motors to cut aerosol volume. As group practices standardize on closed-loop sterilization, equipment spec sheets increasingly favor sealed bearings and anti-retraction valves, reinforcing electric advantages.

By Turbine Speed:

High-Speed Dominance Faces Precision ChallengesHigh-speed models commanded 58.10% revenue in 2025, yet clinicians must manage pulp temperature rise at rotations above 200,000 rpm. Manufacturers incorporate ceramic ball bearings and advanced coolant ports to protect dentine near the pulp chamber, sustaining preference for high-speed options while addressing safety. Low-speed units remain indispensable for endodontics and finishing tasks, but their growth is tied to niche application volume rather than broad market shifts.

Precision dentistry trends favor variable-speed controls that allow practitioners to toggle between rough-cut and fine-finish in a single unit. KaVo’s Direct Stop Technology halts the bur within one second, minimizing over-prep in minimally invasive cases. Future upgrades may integrate haptic feedback that alerts when predefined depth settings are reached, embedding speed as a controllable parameter rather than a fixed specification.

By Material:

Stainless-Steel Reliability Meets Titanium InnovationStainless steel dominated with 62.45% of Dental turbine market size in 2025 because it withstands high-temperature autoclave cycles without deformation.Titanium-alloy housings, however, cut instrument weight by up to 25%, reducing hand-arm vibration and operator fatigue, and they are forecast to grow at 14.72% CAGR. Lighter handpieces align with occupational-health directives that limit exposure to repetitive stress injuries, especially among clinicians who perform long restorative sessions.

Titanium’s corrosion resistance also reduces micro-pitting that would otherwise harbor pathogens, supporting compliance with strict sterilization protocols. The shift to premium alloys drives complementary demand for compatible burs and lubricant formulations, extending value streams for suppliers. Cost remains a hurdle, so suppliers package titanium models with extended warranty and service bundles that justify price premiums through reduced long-term maintenance.

By End User:

Specialty Centers Drive Innovation AdoptionDental clinics retained 48.25% revenue share in 2025, yet specialty centers and mobile units are expanding at 15.68% CAGR as new care models emerge. Specialty providers adopt electric turbines early because infection control and procedural precision are crucial differentiators in implantology and cosmetic dentistry. Mobile clinics leverage lightweight, battery-compatible turbines to deliver care in schools and corporate campuses, widening addressable patient pools.

Hospitals purchase under centralized tender processes that emphasize cost over advanced specifications, tempering their growth rate. Conversely, dental service organizations operating across multiple states in the United States push unified vendor contracts, creating scale for premium turbine deployment. As national chains acquire solo practices, procurement shifts from personal preference to standardized technology bundles, accelerating innovation diffusion.

By Distribution Channel:

Digital Transformation Accelerates Online GrowthDealer networks captured 42.10% of 2025 revenue because they provide in-person handpiece servicing and loaner programs that clinics still value. Online platforms are projected to grow at 15.95% CAGR as e-procurement systems integrate with practice-management software that automates reorder triggers. Price transparency and direct manufacturer promotions on digital marketplaces appeal to cost-conscious small practices in Latin America and India.

Subscription models offered via cloud dashboards blur lines between sales and service by bundling turbines, sterilization cassettes, burs, and predictive maintenance alerts for a monthly fee. Marketplace data analytics inform manufacturers about real-time usage trends, enabling demand-driven production planning. Regulatory frameworks increasingly permit electronic documentation of device traceability, further supporting digital channel expansion.

Geography Analysis

North America Dental Turbine Market

North America maintained 39.30% Dental turbine market share in 2025, underpinned by FDA 510(k) regulations that enforce performance standards and encourage adoption of premium handpieces.Insurance reimbursement for advanced restorative procedures supports capital investment in electric turbines. Canada benefits from cross-border trade and dental tourism that funnels US-approved devices into its clinics with minimal additional certification.

APAC Dental Turbine Market

Asia-Pacific posts the highest CAGR at 16.05% through 2031 because India and China expand dental insurance to middle-income segments. Urban middle-class patients demand esthetic restorations delivered quickly, prompting clinics to install high-speed, lightweight turbines to maximize chair turnover. Domestic manufacturers in China offer cost-competitive stainless-steel models, while international brands target premium niches through authorized e-commerce channels.

Europe and United Kingdom Dental Turbine Market

Europe enjoys steady replacement cycles because equipment aging past mandatory sterilization test thresholds requires upgrading. Harmonized CE marking enables seamless product movement across the bloc, but post-Brexit rules add customs documentation for UK shipments. Manufacturers with EU-based production avoid supply-chain friction and can deliver replacement parts within 48 hours, maintaining customer loyalty in time-sensitive practices.

Regulatory Landscape

Regulation for dental turbines is anchored in medical-device quality systems and market-access pathways. In the United States, the FDA Quality Management System Regulation (QMSR) took effect on February 2, 2026, incorporating ISO 13485:2016 into 21 CFR Part 820. The change lifts the bar for design controls, documentation, and supplier management across turbine and handpiece manufacturers.

In Europe, Medical Device Regulation (EU MDR) compliance tightened further in 2026 through multiple system-level steps. The European Commission published Implementing Regulation (EU) 2026/977 on May 4, 2026, standardizing quality management and procedural requirements for notified body conformity assessments, and the EUDAMED UDI/Devices module became mandatory on May 28, 2026, with updated EMDN codes referenced to the 2026 revision. On June 4, 2026, the Court of Justice of the European Union (case C-10/24, related to dental device distribution due diligence) clarified that distributors must perform coherence checks on CE marking and regulatory documentation under MDR Article 14, increasing compliance oversight across the distribution layer that serves clinics and dealers.

Value Chain Analysis

The dental turbine value chain starts with high-precision component inputs and materials, then proceeds through turbine cartridge and handpiece assembly, regulatory and quality qualification, and multi-channel distribution with recurring aftermarket service. Critical sub-components include the spindle/chuck (collet), impeller, front and rear bearings, seals (O-rings), and small wear parts, with performance closely linked to bearing systems (often ceramic balls such as silicon nitride) and precision shafts (commonly stainless steels such as 440C). Compliance with ISO 14457 for high-speed air turbine handpieces shapes upstream design choices around air-flow and safety/performance requirements, and it reinforces tight process controls through machining, balancing, and assembly.

Manufacturing and sub-supply are specialized. Bearing and rotor suppliers serve both OEM brands and aftermarket cartridge assemblers, creating two parallel fulfillment routes into clinics: OEM new-handpiece sales and repair or refurbishment ecosystems that replace turbine cartridges and bearings to extend asset life. Downstream, sales flow through direct manufacturer channels, dental dealers and distributors that provide in-person service capacity, and online platforms that increasingly bundle equipment with maintenance and traceability documentation. The highest-friction nodes are precision bearing supply, clean assembly capability, and service-network coverage that supports sterilization-driven maintenance cycles and rapid turnaround for high-throughput dental clinics.

Competitive Landscape

The Dental turbine market is moderately fragmented. FDA submission complexity and sterilization testing costs deter new entrants, but niche players exploit gaps by offering subscription handpiece-as-a-service plans. October 2024 saw HuFriedyGroup acquire SS White Dental to gain bur technology that complements turbine lines, signaling convergence within the value chain.

Market leaders emphasize material science and digital connectivity rather than price. KaVo upgraded its EXPERTtorque series with ceramic bearings and IoT drift monitoring that alerts users before failure. NSK added titanium casings across its Ti-Max Z series, dropping handpiece weight to 72 g and positioning for ergonomic leadership. Emerging Chinese vendors aim at stainless-steel high-speed units priced 20% below European benchmarks, marking competitive pressure in entry-level segments.

Strategic alliances with distribution platforms increase product visibility in online channels. Dentsply Sirona integrates turbine performance data into its CEREC chairside system, binding consumable sales with hardware replacement cycles. Subscription financing models tested in the United States migrate to Western Europe as credit-rating platforms mature. Competitive positioning now hinges on total-cost-of-ownership value rather than upfront price alone.

Global Dental Turbine Industry Leaders

Dentsply Sirona, Inc

Nakanishi Inc

W&H Group

B.A. International

Bien Air

- *Disclaimer: Major Players sorted in no particular order

Global Dental Turbine Market Companies Covered in this Report

- Dentsply Sirona

- NSK (Nakanishi Inc.)

- KaVo Dental / Planmeca Group

- J. Morita Corp.

- Bien-Air Dental SA

- W&H Dentalwerk Bürmoos GmbH

- DentalEZ

- Sinol Dental

- Guilin Woodpecker Medical Instrument Co. Ltd.

- Lares Research

- B.A. International

- MK-dent GmbH

- The Yoshida Dental Mfg. Co. Ltd.

- Nouvag

- Brasseler USA

- Dentamerica Inc.

- TKD S.p.A.

- Beyes Dental Canada Inc.

Market Opportunities and Future Outlook

Opportunities concentrate around infection-control performance, safety features, and digital operatory integration, particularly as clinics upgrade equipment specifications. Product rollouts in 2026 point to these whitespace areas: NSK introduced Ti-Max Z990L/Z890L turbines with a Dynamic Power System and quick-stop functions (January 2026), and NSK Europe introduced QuickStop Bearings positioned to mitigate suck-back and intraoral entrapment risks (April 2026). This direction matches procurement shifts highlighted in the report toward sealed heads, anti-retraction measures, and sterilization-resilient designs that can be standardized across multi-site dental service organizations.

A second opportunity sits in value-added service and parts ecosystems that reduce total cost of ownership for high-speed instruments. Precision turbines depend on tightly specified bearing and rotor assemblies (often supplied by specialized component manufacturers), making predictive maintenance, cartridge-based repairs, and subscription-style procurement practical levers for clinics facing downtime and reprocessing demands. As online procurement channels expand and documentation and traceability requirements increase, manufacturers and distributors that bundle turbines with service logistics, spare-part availability, and digital maintenance analytics gain an operational advantage for clinics that prioritize uptime and consistent infection-control workflows.

Recent Industry Developments in Global Dental Turbine Market

- May 2026: Foshan Topmed Dental Co., Ltd. received FDA 510(k) clearance (K251389) for a high-speed air turbine handpiece. The clearance supports broader US commercialization pathways for cost-competitive air-driven units, while also reinforcing the importance of documented performance and quality controls for market access.

- February 2025: Nakanishi Inc. (NSK) introduced new operatory and surgical products including the Surgic Pro2 surgical micromotor and the Perio-Mate subgingival air polisher. The expanded portfolio supports cross-selling into clinic accounts that buy turbines and adjacent handpieces as integrated operatory toolkits.

- October 2024: HuFriedyGroup completed its acquisition of SS White Dental, adding bur technology that complements turbine and handpiece usage. The deal highlights value-chain convergence around cutting instruments and accessories, strengthening bundled offerings through expanded distribution reach.

Global Dental Turbine Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue generated from dental turbine handpieces used chair-side for rotary procedures in dentistry, including air-driven, electric, and hybrid turbines used across routine operative steps.

Scope exclusions: items such as implant surgical drills, laboratory bench motors, and consumables (for example, burs and bearings) are excluded.

Segments Covered in This Report

- By Product Type

- Air-Driven Turbine

- Electric-Driven Turbine

- Hybrid Air-Electric Turbine

- By Turbine Speed

- High-Speed

- Low-Speed

- By Material

- Stainless-Steel Housing

- Titanium-Alloy Housing

- Others

- By End User

- Hospitals

- Dental Clinics

- Others

- By Distribution Channel

- Direct Sales

- Dental Dealers / Distributors

- Online Platforms

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market guardrails and to avoid mixing adjacent dental device categories into one number. We review public sources that help frame dental procedure volumes and equipment adoption, such as the World Health Organization oral health updates, the US Centers for Disease Control and Prevention guidance on infection control, and national health statistics releases that discuss dental visits and provider capacity.

We also use technical and regulatory context from sources such as the US FDA device databases, peer-reviewed dental journals that discuss handpiece performance and sterilization practices, and trade association websites that track dentistry trends. Company annual reports, investor presentations, and reputable press coverage help confirm product line mix and regional exposure, and a paid subscription for company financials and news is used selectively when public reporting is limited. These examples are not exhaustive, and many other sources were reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test pricing, replacement cycles, and how demand moves across clinic types, which is where public sources are usually thinner. We spoke with manufacturers, distributors, service partners, and dental care providers across major regions, so the assumptions reflect actual purchasing behavior in chair-side turbine handpieces rather than only what companies or associations publish.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 19% | APAC: 43% |

| Mid tier: 43% | Functional/Unit leaders: 37% | EMEA: 32% |

| Smaller Players: 20% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

The core model uses a top-down approach where dental care activity and operatory equipment usage patterns are converted into an addressable demand pool for turbine handpieces, then translated into value using typical pricing bands. To keep the output realistic, we corroborate totals with selective bottom-up approximations, such as supplier revenue roll-ups, distributor channel checks, and sampled average selling price multiplied by estimated unit demand, and we adjust when we see clear gaps.

A few practical inputs that shape the math include the installed base of dental chairs and operatories, the share of procedures that use high-speed rotary tools, average replacement timing driven by maintenance and sterilization load, and regional pricing ranges by turbine type (air, electric, or hybrid). Where coverage is uneven, missing sub-areas are filled using proxy indicators that can be defended on a call, such as dentist density, clinic count trends, and import-export patterns for dental instruments. Forecasts are produced using scenario analysis supported by expert views on procedure recovery, clinic investment cycles, and pricing movement, then translated into year-by-year growth.

Data Validation & Update Cycle

Model outputs are checked against independent signals so the number stays aligned with what the market can plausibly absorb. We re-check any sharp jumps that cannot be explained by procedure mix, replacement timing, or pricing. Outliers are reviewed in more than one analyst pass, followed by a final internal review before release, and respondents are re-contacted when a key assumption changes or a data point conflicts with the broader evidence.

Reports are refreshed annually, and interim updates are done when material events occur, such as regulatory changes, supply disruptions, or step-changes in clinic spending. Before delivery, we run a fresh pass on inputs so clients receive an updated view that still ties back to the same repeatable calculation steps.

Mordor Intelligence's Dental Turbine Market Size Versus Other Published Estimates

Published market values for dental turbines often do not match because the scope can shift quietly, and the same device is sometimes counted under a broader handpiece bucket. Differences also come from how pricing is treated, whether replacement demand is separated from new chair installations, and how quickly assumptions are updated when clinic utilization changes.

Consumables such as burs and bearings sit outside Mordor Intelligence's scope, and that exclusion alone can pull totals down versus estimates that bundle recurring accessories into the same market. Some sources also lean on manufacturer shipment narratives without validating against procedure-driven demand signals, while others apply a single global ASP that does not reflect regional pricing dispersion and sterilization-driven replacement timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 239.79 M (2026) | |

| Trade Journal A | USD 1.42 B (2022) | Uses an earlier base year and tends to describe the category at a broader dental device level, which can blend turbines with adjacent powered handpieces and related accessories. |

| Regional Consultancy B | USD 1.66 B (2024) | Focuses on the wider dental turbine handpiece revenue pool with limited clarity on exclusions, and relies on generalized regional splits and ASP assumptions that can overstate chair-side turbine-only value. |

The spread across publishers mainly reflects what is counted as a turbine market in the first place, plus which year and pricing logic anchor the estimate. By keeping the included product set tight and cross-checking it with demand-linked signals like clinic activity and replacement cadence, we arrive at a number that is easier to trace and re-create when assumptions change.

Key Questions Answered in the Report

What is the current value of the Dental turbine market?

The Dental turbine market stands at USD 239.79 million in 2026.

Which product type is growing the fastest?

Electric-driven turbines are advancing at a 15.27% CAGR through 2031 due to superior aerosol mitigation.

Why is Asia-Pacific the fastest-growing region?

Insurance expansion, rising disposable income, and local manufacturing push the region to a 16.05% CAGR.

How do electric turbines improve infection control?

They generate fewer aerosols, incorporate sealed head designs, and pair with high-volume evacuators to cut airborne pathogens.

Page last updated on: