Global Dental Liners And Bases Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

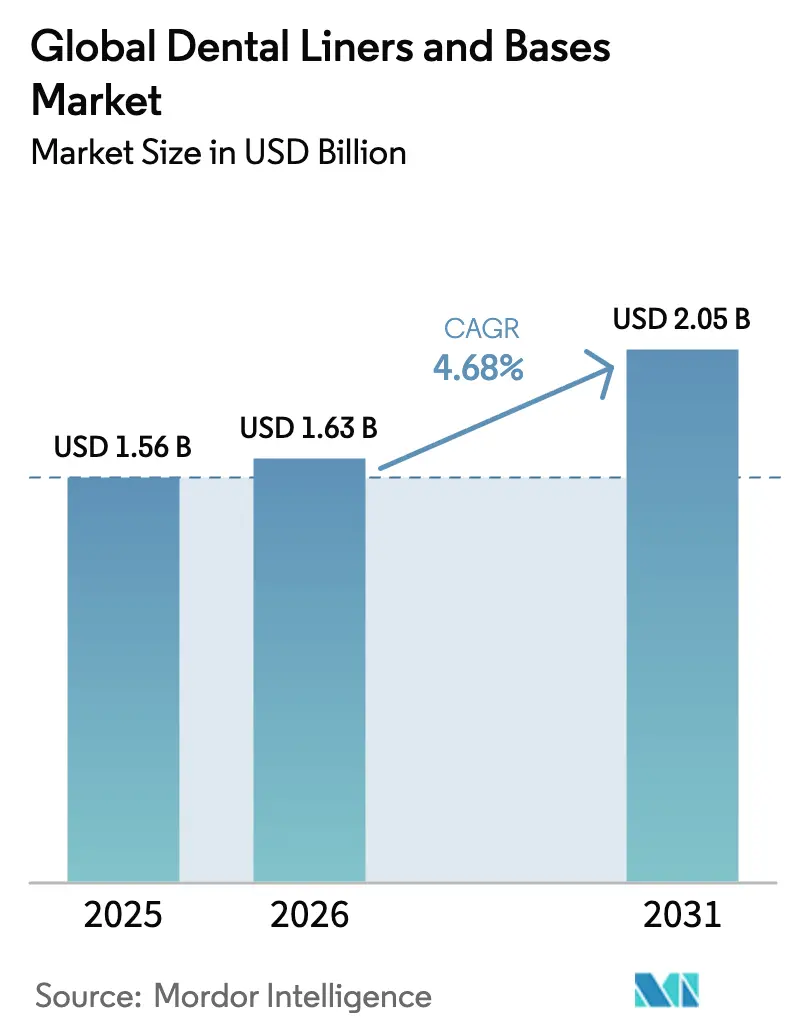

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

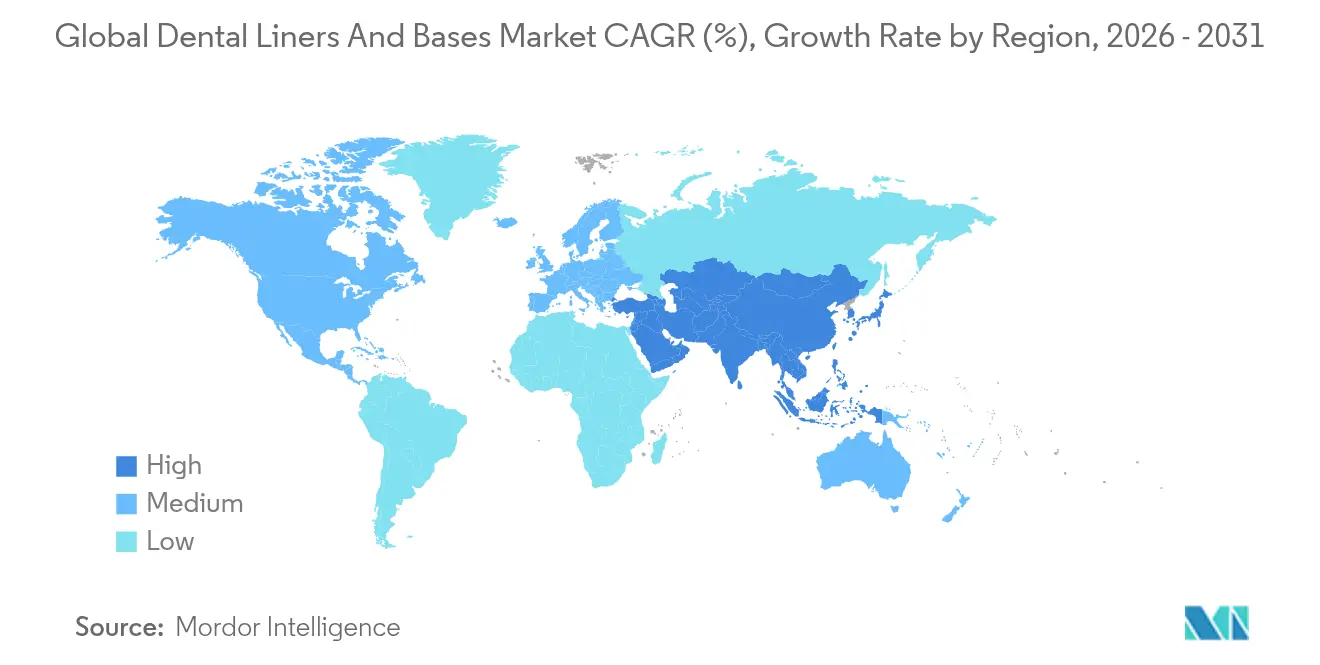

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Dental Liners And Bases Market Analysis by Mordor Intelligence

dental liners and bases market size in 2026 is estimated at USD 1.63 billion, growing from 2025 value of USD 1.56 billion with 2031 projections showing USD 2.05 billion, growing at 4.68% CAGR over 2026-2031. This performance anchors the sector as a steady-growth arena within restorative dentistry, propelled by the dual pull of material innovation and demographic need. Rising global caries incidence, rapid uptake of bio-active resin-modified glass ionomer (RMGI) systems, and stronger value-based care mandates are reshaping clinical protocols, while North America retains spending leadership and Asia-Pacific supplies volume momentum. Manufacturers are prioritising ion-releasing chemistries that extend the life of direct restorations, and clinics are upgrading chairside workflows to support minimally invasive treatment strategies. Geopolitical raw-material shocks and stricter biocompatibility rules remain near-term headwinds, but demand elasticity stays high because most restorative procedures require a liner or base regardless of macro-economic swings.

Key Report Takeaways

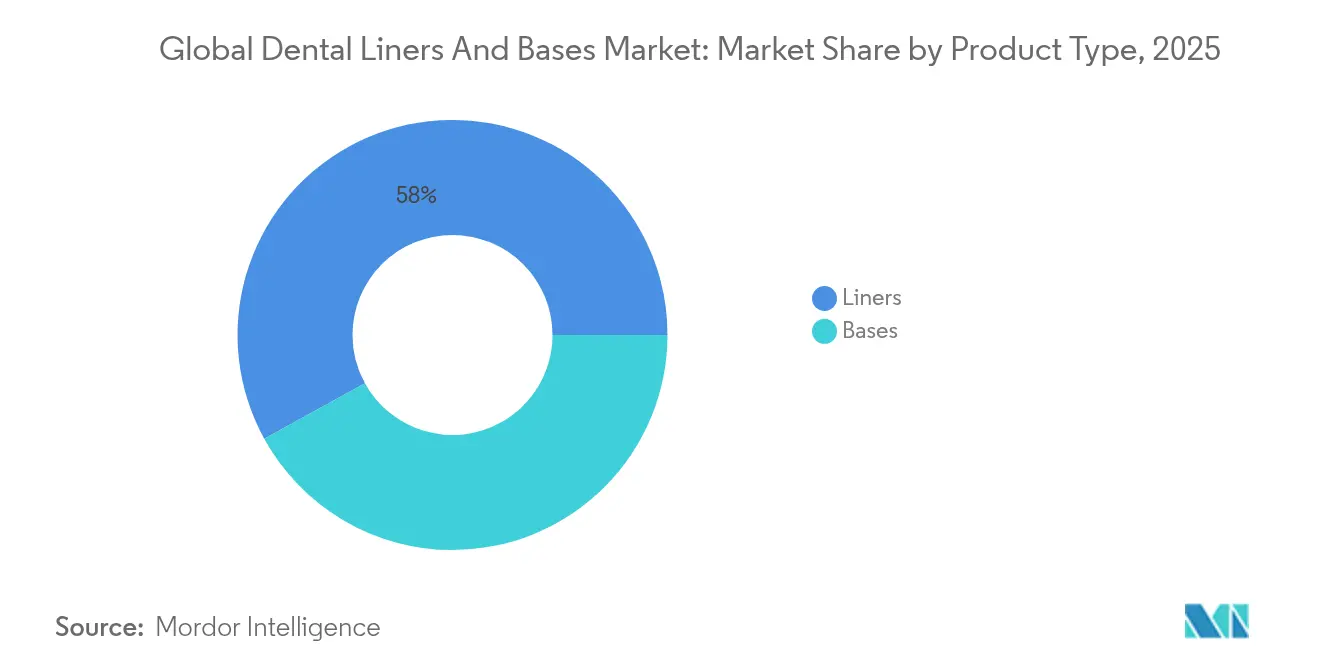

- By product type, liners captured 58.02% of the dental liners and bases market share in 2025.

- By material, glass ionomers held 33.92% of the dental liners and bases market size in 2025 while bio-active RMGI posted the fastest 5.32% CAGR through 2031.

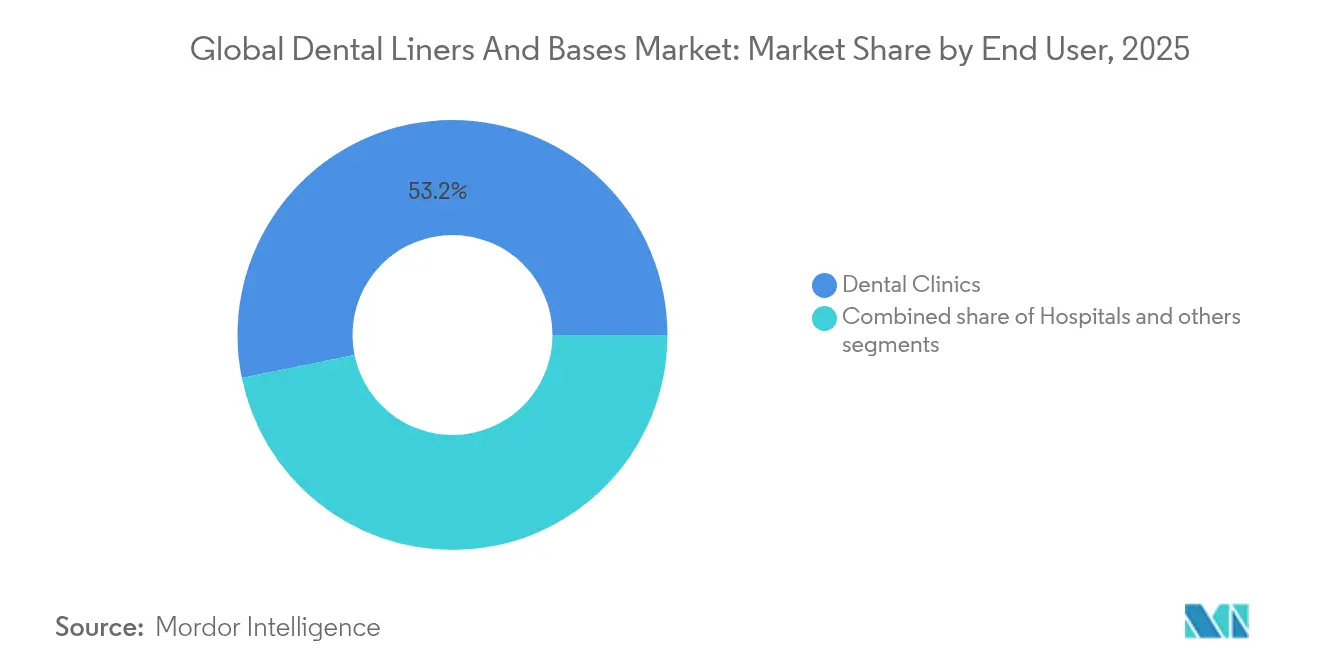

- By end user, dental clinics accounted for 53.21% revenue in 2025 and are expanding at a 5.64% CAGR to 2031.

- By geography, North America led with 41.88% revenue in 2025; Asia-Pacific is set to register the strongest 6.03% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Liners And Bases Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dental caries & restorative procedures | +1.2% | Global, with higher impact in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Growing geriatric edentulous population | +0.9% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Technological advances in bio-active & RMGI materials | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Shift to minimally-invasive ion-releasing liner systems | +0.7% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Dental tourism packages upgrading to premium liners/bases | +0.4% | Asia-Pacific core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Chairside CAD/CAM-optimised flowable liner workflows | +0.5% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries and Restorative Procedures

Age-standardised incidence for permanent-tooth decay climbed from 28,154 per 100,000 in 1990 to 29,896 in 2021 and is projected to reach 30,414 by 2030. The persistent disease burden drives liner utilisation because deep carious lesions mandate pulp-protective barriers before composite placement. Low- and middle-income countries contribute the sharpest case growth, yet high-income regions sustain procedure value through premium material adoption. Clinical trial data show that ion-releasing liners cut secondary-caries risk in posterior restorations over a three-year horizon. Health ministries are therefore endorsing liner use in public-sector treatment guidelines, reinforcing volume demand.

Growing Geriatric Edentulous Population

People aged 65 years and older now retain more natural teeth yet present with complex dentin changes that heighten restorative failure risk. A cross-sectional assessment of oral-frailty symptoms in seniors underscores the need for advanced pulp-capping agents during full-mouth rehabilitation. National insurance schemes across Europe and Japan reimburse liners in vital-pulp therapy, widening clinical usage. Bio-active formulations that trigger secondary-dentin formation align with preventive geriatrics, and their adoption is directly linked to lower retreatment outlays in long-term-care facilities.

Technological Breakthroughs in Bio-Active RMGI Chemistries

Latest RMGI platforms integrate pre-reacted glass technology that delivers sustained fluoride, calcium, and phosphate release without compromising flexural strength. Nano-silica reinforcement from natural diatom sources further boosts compressive-strength metrics by 22% while preserving film thickness. These gains solve legacy glass-ionomer fragility, encouraging clinicians to specify RMGI liners under bulk-fill composites in load-bearing posterior sites. Manufacturers that secure regulatory clearance under the FDA’s 2024 Dental Cements pathway enjoy accelerated time-to-market.

Shift Toward Minimally Invasive Ion-Releasing Protocols

Selective-caries-removal concepts limit dentin excavation, making thin-layer liners essential for pulp vitality. Bio-active calcium-silicate systems such as Biodentine outperform calcium-hydroxide liners in vitality preservation and dentin bridge thickness. These materials are now integrated into digital treatment plans where CAD/CAM software recommends liner thickness based on residual dentin mapping. Clinical guidelines from the American Academy of Operative Dentistry updated in 2025 formally endorse ion-releasing liners for deep preparations, accelerating practice-wide standardisation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cytotoxicity & solubility concerns for legacy materials | -0.6% | Global, with stricter enforcement in Europe and North America | Medium term (2-4 years) |

| Limited reimbursement in cost-sensitive economies | -0.4% | Asia-Pacific, Latin America, and MEA | Long term (≥ 4 years) |

| Emerging nanomaterial regulatory hurdles | -0.3% | Europe and North America, expanding globally | Short term (≤ 2 years) |

| Supply-chain volatility of specialty glass powders | -0.2% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cytotoxicity and Solubility Concerns with Legacy Chemistries

In-vitro studies reveal that resin-modified calcium-hydroxide products show concentration-dependent cytotoxicity against human pulp cells. Solubility issues plague older formulations, leading to marginal gaps and restoration failure. The European Medical Device Regulation now enforces expanded biocompatibility dossiers, compelling product reformulations that inflate development spend. Clinicians in paediatric dentistry are especially cautious, driving a gradual phase-out of high-solubility liners in favour of silica-reinforced alternatives

Limited Reimbursement in Cost-Sensitive Economies

Insurance packages in many emerging markets reimburse only basic restorative care, leaving advanced liner upgrades as out-of-pocket items. In India, where dental service revenue touched USD 600 million in 2024, subsidy ceilings still exclude bio-active liners. Similar gaps persist across Latin America, hampering penetration for premium formulations despite growing clinical awareness. Manufacturers respond with tiered product lines that keep ion-release capability but reduce ancillary features to meet unit-price thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liners Dominate High-Value Applications

Liners held 58.02% revenue in 2025 and maintain a 5.07% CAGR as they underpin nearly every deep-cavity restoration. This dominance reflects strict adherence to pulp-protection standards and the widespread clinical emphasis on thin-film barriers under composite resins. The dental liners and bases market size attributed to liners accounted for USD 0.91 billion in 2025, and higher viscosity variants are entering chairside CAD/CAM catalogues. Bases fulfil bulk build-up roles in extensive lesions, yet many new materials combine liner and base functionality, blurring categorical boundaries. Manufacturers therefore promote multi-purpose kits that reduce inventory points for clinics, streamlining procurement.

Second-generation liners embed antibacterial quaternary-ammonium monomers, and early studies indicate 28% lower secondary-caries recurrence versus conventional calcium-hydroxide products. As digital workflow adoption rises, liner dispensers equipped with RFID chips help track expiration and usage, linking material management to electronic health records. These workflow efficiencies reinforce demand for premium liners within the dental liners and bases market.

By Material: Glass Ionomers Retain Lead but Bio-Active RMGI Gains Speed

Glass ionomers captured 33.92% revenue in 2025 owing to trusted bonding affinity and fluoride-release profiles. However, the dental liners and bases market share for this class is gradually ceded to bio-active RMGI systems, which expand 5.32% annually. Clinicians favour RMGI for dual-cure handling that complements bulk-fill composite placement. Fluoride-release assessment shows Vitrebond emitting peak 2.4 µg/cm² in week one, outperforming chemical glass ionomer alternatives. Zinc-oxide-eugenol consumption declines amid concerns about eugenol-triggered polymerisation inhibition when used with resin composites. Calcium-silicate platforms such as Biodentine migrate from endodontic repair into routine liner indication, adding competitive tension within the dental liners and bases market.

By End User: Dental Clinics Accelerate Adoption of Digital-Material Combos

Dental clinics delivered 53.21% of 2025 revenue and are tracking a 5.64% CAGR. Their dominance reflects patient preference for single-visit procedures and the clinics’ agility in integrating digital scanning, milling, and flowable-liner delivery systems. Hospital settings focus on medically compromised cohorts who often need elaborate build-up protocols, sustaining baseline demand for high-strength bases. Academic centres remain innovation hubs that validate bio-active prototypes under controlled trials; collaborations such as Dentsply Sirona’s 2024 partnership with Alexandria University of 756 treatment centres exemplify this model.

Geography Analysis

North America commanded 41.88% revenue in 2025, supported by insurance coverage and early adoption of bio-active chemistries. The dental liners and bases market size for the region stood at USD 0.65 billion in 2025. The United States contributes the bulk share, buoyed by Medicare Part B expansions that reimburse restorative procedures when medically linked.

Asia-Pacific is the fastest-growing cluster at 6.03% CAGR. Rising middle-class expenditure, dental-tourism hubs in Thailand and India, and widespread private-practice investment in CAD/CAM platforms underpin momentum. China’s domestic manufacturers increase resin-modified glass ionomer output, trimming lead times for clinics. Japan’s super-aged society drives demand for biocompatible liners compatible with polypharmacy constraints. South-East Asian ministries scale school-sealant programmes, indirectly stimulating liner education campaigns that raise practitioner familiarity.

Europe shows resilient yet regulatory-tempered growth. The European Chemicals Agency proposal to tighten silica exposure limits compels process retrofits across liner plants, creating transitional supply tightness. Latin America and the Middle East & Africa record emerging-market gains, buttressed by dental tourism packages that bundle premium liners with implant services for international patients.

Competitive Landscape

Market structure is moderately fragmented. The top five suppliers hold an estimated about half of the combined revenue, leaving room for specialised entrants targeting bio-activity niches within the dental liners and bases market. Dentsply Sirona, 3M Solventum, GC Corporation, and Coltene dominate legacy portfolios, yet newer challengers such as Desktop Health drive resin-additive advances. Strategic pivots focus on R&D alliances with bioceramic startups and vertical integration of specialty glass powders to curb raw-material volatility.

Product pipelines spotlight ion-releasing chemistries that sustain caries-inhibiting conditions. 3M’s 2024 spin-off of Solventum sharpened investment in bio-compatible dental materials, freeing resources formerly shared with broader healthcare units. Dentsply Sirona extended its DS Academy coursework, training 6,000 clinicians on digital restorative workflows that integrate one-step liner placement.

M&A velocity rose in 2024. Patient Square Capital’s USD 4.1 billion acquisition of Patterson Companies consolidated North American distribution, promising wider access to premium liner lines. Straumann Group logged CHF 585.5 million Q3 revenue with 11.2% organic growth, driven by liner-related restorative kits in Asia-Pacific.

Regulatory evolutions shape competitive tactics. The FDA’s 2024 performance-based guidance for dental cements cut 510(k) timelines, favouring firms that already possess robust bench-testing infrastructures. EU proposals on silica drive R&D towards alternative fillers, and early patents signal potential substitution of calcium-phosphate nanopowders. Combined, these shifts create an innovation race centred on safety-plus-bioactivity attributes inside the dental liners and bases market.

Global Dental Liners And Bases Industry Leaders

3M

Envista Holdings Corporation (Kerr Corporation)

Dentsply Sirona

Den-Mat Holdings, LLC

GC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: FDA finalised safety-and-performance guidance for dental cements, streamlining submission pathways for bio-active products

- July 2024: Desktop Health validated Flexcera Smile Ultra+ resin for All-on-X provisionals, widening bio-active restorative applications

Global Dental Liners And Bases Market Report Scope

As per the scope of the report, dental liners and bases are used to protect the living pulp of the tooth from filling materials. It also provides chemical protection to prevent dangerous chemicals from the dental material from entering the pulp. The Dental Liners and Bases Market is Segmented by Material (Zinc Oxide Eugenol, Zinc Phosphate, Glass Ionomer, Calcium Hydroxide, and Other Materials), End User (Hospitals, Dental Clinics, and Research & Academic Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Liners |

| Bases |

| Glass Ionomer |

| Zinc Oxide Eugenol |

| Calcium Hydroxide |

| Resin-Modified Glass Ionomer |

| Others (Biodentine, bio-active) |

| Hospitals |

| Dental Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Liners | |

| Bases | ||

| By Material | Glass Ionomer | |

| Zinc Oxide Eugenol | ||

| Calcium Hydroxide | ||

| Resin-Modified Glass Ionomer | ||

| Others (Biodentine, bio-active) | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which product segment contributes the largest revenue?

Endoscopy devices generate 58.02% of 2025 sales due to their central role in diagnostics and therapy.

Which region is expanding the fastest?

Asia-Pacific shows a 6.03% CAGR through 2031 as infrastructure investment meets rising disease incidence.

How are AI tools affecting colonoscopy outcomes?

AI systems such as GI Genius deliver 99.7% sensitivity and cut adenoma miss rates by half, raising screening effectiveness.

Why are specialty clinics gaining share from hospitals?

Payers favor their lower cost per procedure and rapid turnover, and ASCs are projected to perform 44 million procedures by 2034.

What regulatory change most influences device availability in Europe?

The EU Medical Device Regulation extends recertification timelines to 20272028, requiring more extensive evidence before market entry.

Page last updated on: