Dental Crowns And Bridges Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

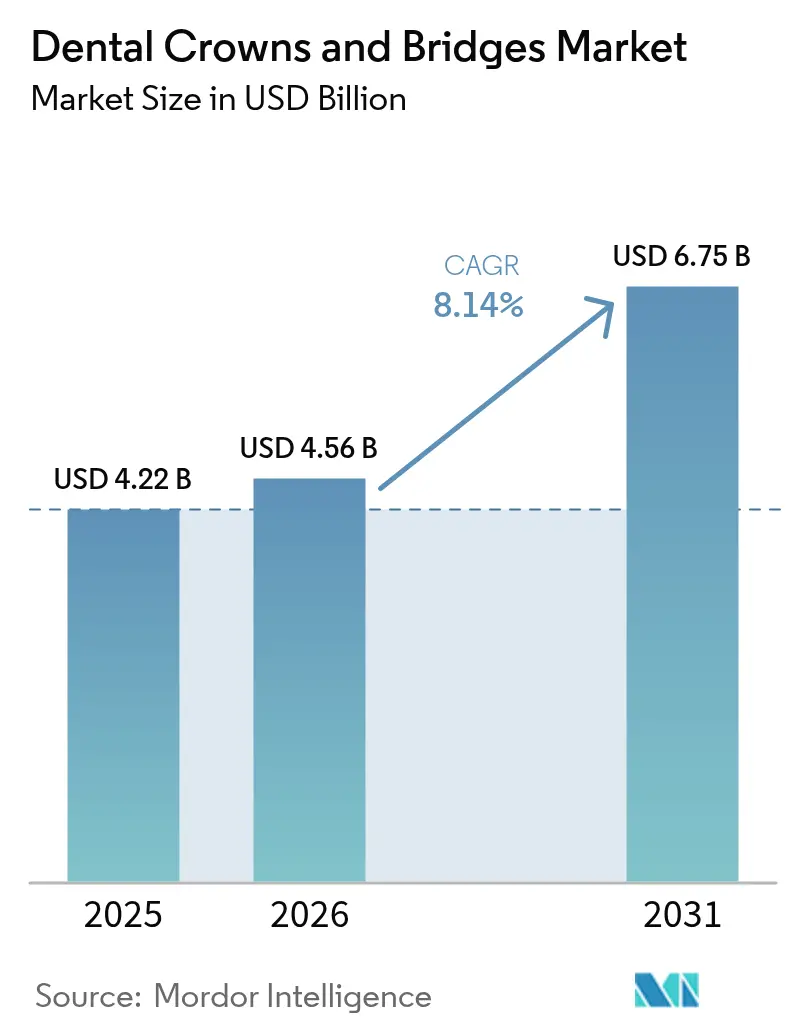

| Market Size (2026) | USD 4.56 Billion |

| Market Size (2031) | USD 6.75 Billion |

| Growth Rate (2026 - 2031) | 8.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

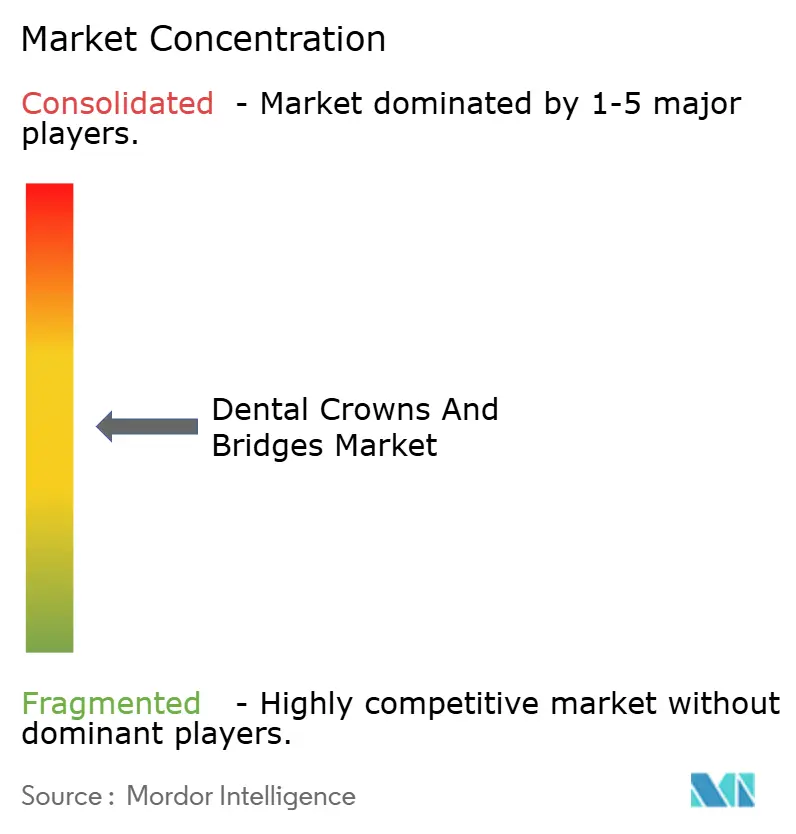

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Crowns And Bridges Market Analysis by Mordor Intelligence

The dental crowns and bridges market size was valued at USD 4.22 billion in 2025 and estimated to grow from USD 4.56 billion in 2026 to reach USD 6.75 billion by 2031, at a CAGR of 8.14% during the forecast period (2026-2031). An aging global population, a steady rise in edentulism, and continuing advances in chair-side digital workflows keep demand on an upward track. Zirconia restorations dominate current case volumes, while lithium-disilicate and multilayer ceramics push the aesthetic frontier. CAD/CAM production reduces laboratory bottlenecks and supports same-day treatment models that shorten chair time. Growing dental‐tourism corridors in Asia and Latin America add price flexibility, yet reimbursement gaps in many markets still restrain household uptake. Competitive intensity remains moderate as global implant and materials suppliers scale regional manufacturing to cut freight risk and shorten lead times.

Key Report Takeaways

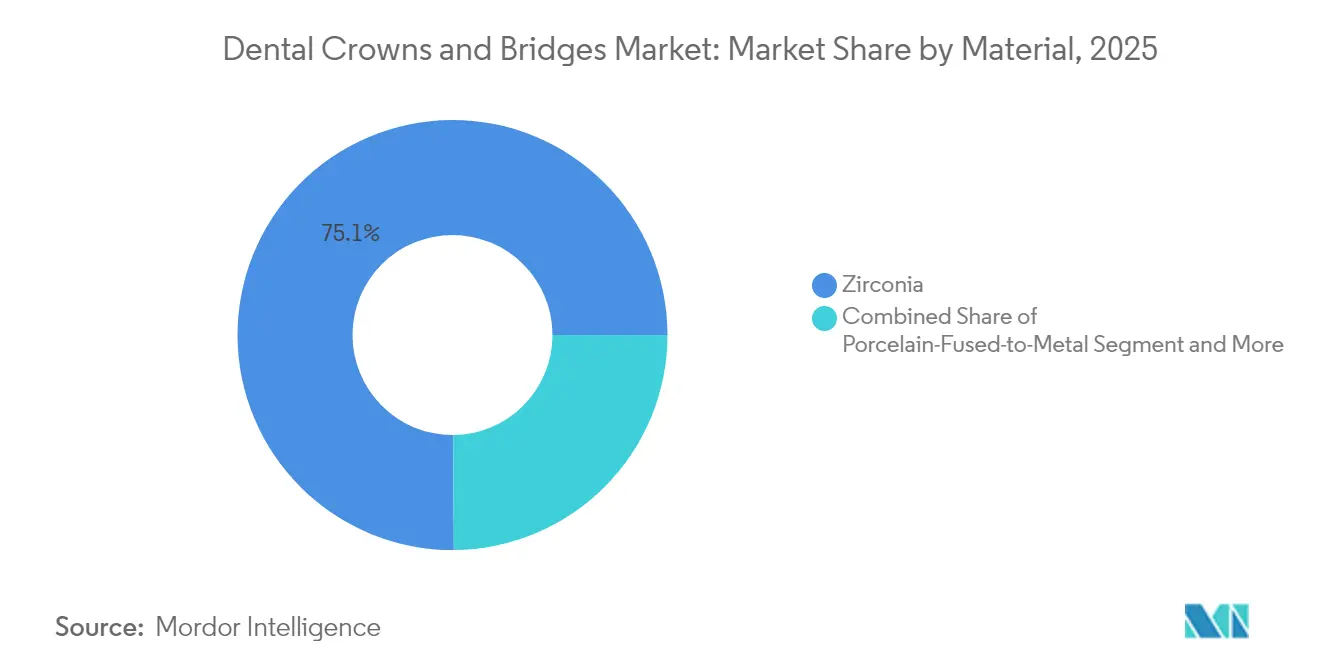

- By material, zirconia captured 75.10% of dental crowns and bridges market share in 2025; all-ceramic materials are forecast to expand at an 11.02% CAGR to 2031.

- By product, crowns led with 65.00% revenue share in 2025, while bridges are projected to advance at a 9.04% CAGR through 2031.

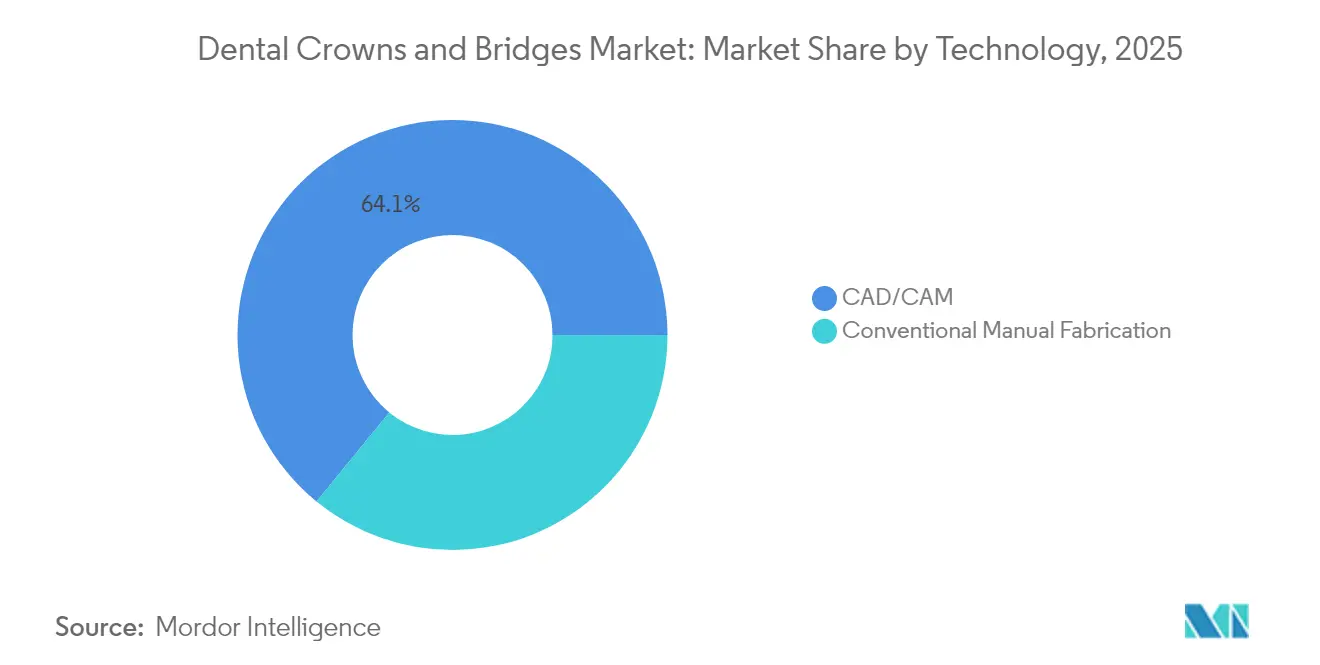

- By technology, CAD/CAM systems held 64.10% share of the dental crowns and bridges market size in 2025 and are set to grow at a 9.98% CAGR over the forecast period.

- By end user, dental clinics controlled 57.20% share in 2025; laboratories record the highest projected CAGR at 9.08% to 2031.

- By geography, North America accounted for 38.40% of dental crowns and bridges market share in 2025, whereas Asia-Pacific is expected to clock a 9.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Crowns And Bridges Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edentulism and tooth-decay prevalence | +2.1% | North America, Europe, global ageing clusters | Long term (≥ 4 years) |

| CAD/CAM and 3-D printing adoption | +1.8% | North America, Asia-Pacific | Medium term (2–4 years) |

| Aesthetic demand for cosmetic dentistry | +1.5% | Developed markets | Short term (≤ 2 years) |

| Shift to full-arch zirconia | +1.2% | North America, Europe, emerging Asia | Medium term (2–4 years) |

| Chair-side milling in tourism hubs | +0.9% | Asia-Pacific, Latin America | Medium term (2–4 years) |

| AI-enabled intra-oral scanning | +0.8% | Developed markets, global rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Edentulism & Tooth Decay in Ageing Populations

Longer life expectancy raises the volume of partial and full tooth loss, especially among lower-income seniors. Untreated caries rates approach 99% in specific older cohorts, while edentulism spans from 4.9% in the United States to 21.7% in select Canadian communities[1]Rakhee Patel, “Healthy Ageing and Oral Health: Priority, Policy and Public Health,” Nature, nature.com. Predictable replacement cycles for aging restorations add recurrent revenue on top of first-time treatments. A widening rural-urban divide in oral health fuels demand for value-engineered crown systems and community outreach programs. Public-health agencies increasingly link oral function to overall healthy-aging objectives, strengthening policy support for restorative interventions.

Accelerating CAD/CAM & 3-D Printing Adoption in Laboratories

Laboratory digitization cuts turnaround times and reduces remakes because digital files eliminate many manual variables. AI-assisted design software automates connector sizing and margin placement, letting technicians focus on complex custom work. Improved sintering ovens and hybrid milling-printing setups bring single-visit prosthetics into mainstream practice, easing inventory constraints and sharpening competitive differentiation. Investment outlays for scanners and five-axis mills remain high, yet volume growth improves payback periods and justifies further capital expenditure. Regional dental-tech clusters, such as those emerging in Shenzhen and Bengaluru, help laboratories access skilled staff and equipment service networks.

Rising Aesthetic Demand for Cosmetic Dentistry

Video conferencing platforms heightened self-perception of dental esthetics, nudging patients toward ceramic restorations that mimic natural translucency. Digital-smile-design software frames treatment expectations with predictive mock-ups, increasing case acceptance rates and opening premium pricing tiers. Lithium-disilicate veneers and mono-lithic zirconia crowns meet color-matching standards demanded by high-income demographics. Practices market “micro-esthetic” corrections, including line-angle recontouring, to younger cohorts, broadening the addressable base for all-ceramic crown units. As procedures remain largely elective, instalment financing and loyalty subscription plans gain traction in urban clinics.

Shift to Full-Arch Zirconia Driving Laboratory Throughput

Full-arch zirconia prostheses show 92.86% prosthetic success and 95.35% implant success over mid-term follow-up, with 78.57% patient satisfaction[2]Vincenzo Marchio, “Retrospective Analysis of Full-Arch Zirconia Rehabilitations on Dental Implants,” Applied Sciences, mdpi.com. Laboratories benefit from higher revenue per case and better equipment utilization when processing multi-unit frameworks. Implant manufacturers bundle prosthetic components, deepening vertical integration around digital-surgery guides and restorative solutions. Training courses on screw-retained full-arch protocols expand as clinicians target faster loading schedules. Lower chipping rates of multilayer zirconia reduce maintenance claims, strengthening clinical confidence in long-span work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost and weak reimbursement | -1.4% | Emerging markets, selected high-income segments | Short term (≤ 2 years) |

| Limited clinician awareness in emerging zones | -0.8% | Asia-Pacific, Latin America, Middle East-Africa | Medium term (2–4 years) |

| Stricter disposal rules on metallic waste | -0.6% | Europe, North America | Long term (≥ 4 years) |

| Zirconia-powder supply volatility | -0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost & Weak Reimbursement

Even in mature economies, private dental insurance pays about 50% of a medically necessary crown while cosmetic indications usually get no support[3]Delta Dental Plans Association, “2024 State of America’s Oral Health Report,” deltadental.com. The out-of-pocket hurdle pushes middle-income patients toward overseas clinics that price single crowns at USD 560 versus USD 1,729 in the United States, according to cross-border-care data. Domestic providers respond with savings plans and bundled implant-crown packages, yet price sensitivity remains acute in the younger workforce. Government schemes focus on emergency extractions rather than restorative work, slowing public-sector demand growth.

Zirconia-Powder Supply Volatility & Price Spikes

Dental-grade zirconia powder production sits with a limited set of processors that rely on energy-intensive sintering steps. Deviations in firing temperature alter translucency by measurable Delta E values, making quality control strict. Spot shortages during energy-price surges lifted global zirconia prices and squeezed laboratory gross margins. Larger suppliers hedge through multi-year contracts, but small labs carry higher inventory costs in response to supply swings. Alternative high-translucency alumina and resin hybrid materials enter catalogues, yet clinical adoption remains cautious.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Zirconia Dominance Drives Premium Positioning

Zirconia held 75.10% of dental crowns and bridges market share in 2025 due to its fracture toughness and shade adaptability. All-ceramic systems post the fastest 11.02% CAGR because lithium-disilicate ingots achieve enamel-like translucency in anterior zones. The dental crowns and bridges market depends on multilayer blocks that mimic dentine-to-enamel gradients, allowing laboratories to reduce staining steps and improve workflow efficiency. PFMs still serve cost-sensitive cases where insurers reimburse metal alloys more readily. Metal-free options, however, continue to cannibalize PFM demand as unit prices fall with milling-center scale economies.

Patient-specific choices override one-size solutions; 98% of dentists prefer zirconia in posterior crowns versus 61% in anteriors. High-translucency variants entering the pipeline blur the anterior-posterior divide and could lift zirconia’s penetration even further. Research into doped-zirconia stabilizers promises color stability without strength loss, catering to premium bridgework. Regulatory agencies emphasize material traceability, encouraging suppliers to invest in QR-coded batch tracking. Such safeguards build practitioner confidence and sustain the dental crowns and bridges market trajectory across developed and emerging economies.

By Product: Crown Leadership Faces Bridge Acceleration

Crowns led revenue with a 65.00% share in 2025, supported by broad indications from single-tooth fractures to root-canal restorations. The dental crowns and bridges market size for crowns segment is forecast to grow alongside rising molar endodontic therapy volumes. Bridges, however, show a faster 9.04% CAGR as implant-supported full-arch frameworks spread beyond specialist centers. Fixed-bridge prevalence reaches 17% among adults aged 75+, presenting an aging-related replacement cycle.

Income bands shape product mix. Higher-income households report 38% crown prevalence compared with 28% in lower-income tiers. This gap fuels innovation in value-engineered composite bridges designed for public clinic budgets. Hybrid screw-retained solutions combine the hygiene benefits of individual crowns with the stability of fixed bridges, improving periodontal outcomes. Such advances support sustained expansion of the broader dental crowns and bridges market through improved clinician confidence and patient satisfaction scores.

By Technology: CAD/CAM Transformation Accelerates

CAD/CAM systems accounted for 64.10% of total placements in 2025 and are advancing at 9.98% CAGR as intra-oral scanners replace conventional impressions. Practices with dual milling units recorded up to 145% productivity gains, shortening delivery time to a single session for simple posterior crowns. AI-driven margin detection improves fit and reduces adjustment appointments, enhancing chair utilization. Manual techniques remain relevant for highly customized veneering and combination cases but are gradually confined to boutique laboratories.

Digital adoption improves consistency and creates cloud-based file libraries that simplify long-term maintenance. Secondary restorations need only updated scans, cutting diagnostic steps and reinforcing patient loyalty. Materials science aligns with software progress as multi-physics simulation informs connector design for long-span bridges. The wider dental crowns and bridges market benefits from standardization that lowers remakes, builds patient trust, and boosts case volumes per clinic.

By End User: Clinic Consolidation Meets Laboratory Specialization

Dental clinics captured 57.20% revenue in 2025 owing to direct patient relationships and expanding DSO networks that optimize procurement. The dental crowns and bridges market size for laboratories is on track for strong 9.08% CAGR because complex zirconia bridge frameworks and high-volume print jobs suit centralized production. Hospitals contribute low but steady restorative demand linked to trauma and oncology reconstruction.

Laboratories evolve toward digital “super-centers” offering AI design, implant planning, and fully sintered zirconia delivery within 48 hours. Chair-side mills compete for single units, yet laboratories retain full-arch dominance by bundling prosthesis design with implant surgical guides. As DSOs grow, preferred-laboratory agreements stabilize throughput and anchor investment in advanced five-axis machinery. This interdependence anchors the growth of the dental crowns and bridges market while helping both parties spread capital costs.

Geography Analysis

North America remained the largest regional contributor with 38.40% share in 2025. High insurance penetration and established laboratory–practice integration support premium zirconia workflow adoption. Same-day dentistry is quickly moving from differentiator to baseline service, sustaining unit growth. Policy debate on Medicare dental benefits could unlock additional volumes but timing remains uncertain.

Europe presents balanced expansion as universal healthcare amplifies functional restorations across aging populations. Environmental regulations accelerate the shift from PFM to metal-free ceramics, incentivizing laboratories to pivot portfolios toward zirconia. Pan-European recall guidelines recommend crown replacement at defined wear thresholds, stabilizing refurbishment demand and cushioning cyclical downturns.

Asia-Pacific is the fastest-growing cluster at 9.39% CAGR, driven by rising middle-class disposable income and the draw of dental-tourism hubs offering up to 40% cost savings to international patients. The dental crowns and bridges market benefits from China’s implant resurgence and Vietnam’s emergence as an English-friendly treatment center. Government investments in public–private dental college tie-ups improve clinician availability and speed technology diffusion. Currency depreciation in Indonesia and Thailand further supports inbound patient flows seeking value treatments.

South America experiences uneven progress; Brazil’s public-sector programs focus on preventive measures whereas private clinics capture affluent demand for zirconia crowns. The dental crowns and bridges market in the region still faces supply volatility and training gaps that elevate prosthesis-remake rates in smaller centers. Middle East and Africa are nascent but promising. Gulf Cooperation Council states host state-of-the-art clinics targeting medical tourists, while Northern Africa promotes French-language care for European travelers. Local material distribution networks mature, lowering lead times for custom abutments and multi-layer blocks. Continued investment in hygienist education will be essential to unlock full market potential across the region.

Competitive Landscape

Global suppliers of implants, milling machinery, and CAD software set the competitive tempo. Straumann Group reported 11.2% organic growth in Q3 2024, supported by expanded digital offerings and strong Chinese implant demand. Focused acquisitions integrate intra-oral scanner lines and AI-planning tools into comprehensive chair-side ecosystems. Ivoclar combines zirconia discs with proprietary furnaces to ensure material–equipment synergy, raising switching costs for laboratories.

Mid-sized regional players differentiate on service responsiveness and localized training. German and Japanese milling-center networks provide overnight crown delivery to metropolitan clinics, balancing quality with quick turnaround. North American DSOs negotiate bulk-buy contracts that favor suppliers able to guarantee consistent lot quality and timely replenishment.

Emerging entrants foreground software innovation rather than traditional manufacturing. Cloud-based design platforms leverage machine learning to automate anatomic contouring. Subscription models lower entry barriers for small laboratories, distributing R&D costs across user bases. Sustainable-material research adds another vector of differentiation as laboratories in Scandinavia and Canada adopt recycling loops for leftover zirconia discs.

Dental Crowns And Bridges Industry Leaders

Dentsply Sirona

ZimVie Inc.

Ivoclar Vivadent

Solventum Corporation

Envista (Nobel Biocare)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Straumann Group started construction of a Brazil-based factory to localize implant and prosthetic production, reducing freight risk and import costs.

- January 2025: Ivoclar launched an integrated zirconia workflow that combines IPS e.max ZirCAD Prime materials with PrograMill PM7 units to compress lead times and boost unit consistency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the dental crowns and bridges market as the value generated from new, fixed prosthetic restorations that cap damaged teeth or span gaps created by missing teeth, fabricated from metals, porcelain-fused-metal, full ceramic, or zirconia and delivered through chairside or laboratory CAD/CAM as well as conventional techniques. According to Mordor Intelligence, functional repairs for implant abutments are included, whereas removable dentures, inlays, onlays, and orthodontic aligners remain outside the scope.

Scope Exclusion: Removable partial dentures and temporary composite veneers are not covered.

Segmentation Overview

- By Material

- Zirconia

- Porcelain-Fused-to-Metal (PFM)

- All-Ceramic (Lithium-disilicate, Feldspathic)

- Metals & Alloys (Gold, Titanium, Co-Cr)

- Others (Resin, Hybrid, Composite)

- By Product

- Crowns

- Bridges (3-unit, 4-unit, Maryland, Cantilever)

- By Technology

- CAD/CAM

- Conventional Manual Fabrication

- By End User

- Dental Clinics & Chains

- Hospitals

- Dental Laboratories

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured interviews with prosthodontists, dental lab owners, zirconia suppliers, and clinic groups across North America, Europe, and Asia-Pacific. These conversations validated adoption curves for same-day crowns, clarified chairside fee benchmarks, and confirmed average bridge replacement intervals, filling data gaps found in secondary sources.

Desk Research

Our team collected baseline statistics on edentulism prevalence, average procedure tariffs, and zirconia import volumes from tier-1 sources such as the World Health Organization oral health surveys, UN Comtrade, the American Dental Association Health Policy Institute, Eurostat, and key national trade associations. Company 10-K filings, investor decks, and regulatory submissions enriched the public record, while paid access to D&B Hoovers and Dow Jones Factiva helped us cross-check manufacturer revenues and shipment narratives. The sources listed are illustrative; numerous others informed data capture and verification.

A second pass mapped installed CAD/CAM milling capacity, material mix shifts, and regional demand signals through Questel patent libraries, Volza customs manifests, and global tender portals in Tenders Info, giving us early insight into technology penetration and price movements.

Market-Sizing & Forecasting

A single top-down build projects the eligible restorations pool by aligning tooth-loss incidence with treatment penetration and weighted procedure pricing, which are then corroborated through selective bottom-up supplier roll-ups and sampled laboratory invoice checks. Key variables in the model include CAD/CAM penetration, multilayer zirconia share, chairside turnaround time, elective cosmetic uptake, and average reimbursement levels. Multivariate regression against historical crown placements and disposable income guides the forecast, and scenario analysis cushions for material-cost swings. Where supplier rolls lack geography detail, we apply validated price corridors and procedure ratios from primary research before merging all outputs.

Data Validation & Update Cycle

Outputs face variance tests against independent indicators, a two-step peer review, and senior sign-off. We refresh every year, with interim updates triggered by events such as new regulatory approvals or reimbursement shifts, ensuring clients always receive the freshest view.

Why Mordor's Dental Crowns & Bridges Baseline Commands Reliability

Published estimates often diverge because firms select different inclusions, price anchors, and refresh cadences. We acknowledge these gaps so readers grasp the landscape before deciding.

Differences arise around counting pre-fabricated temporaries, valuing implant-borne crowns, and timing zirconia ASP updates. Some publishers freeze 2023 prices or extrapolate one-country samples, whereas our analysts update currency and price series annually and re-check service volumes with clinicians.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.22 Bn (2025) | Mordor Intelligence | - |

| USD 3.58 Bn (2025) | Global Consultancy A | Excludes implant-supported crowns; forecast freezes 2023 pricing |

| USD 4.48 Bn (2025) | Industry Tracker B | Counts temporary caps; applies uniform global ASP |

| USD 3.60 Bn (2024) | Regional Consultancy C | Relies on small European lab survey; no trade-data cross-check |

The comparison shows totals shift quickly when scope or price inputs move. By grounding our baseline in clear inclusions, annually refreshed prices, and double-sourced procedure volumes, Mordor Intelligence delivers a balanced, transparent figure that decision-makers can trace and replicate.

Key Questions Answered in the Report

What is the current value of the dental crowns and bridges market?

The dental crowns and bridges market size reached USD 4.56 billion in 2026 and is projected to grow at an 8.14% CAGR to USD 6.75 billion by 2031.

Which material dominates dental restorations today?

Zirconia leads with 75.10% market share because it combines high strength with natural tooth-like esthetics.

Why is Asia-Pacific the fastest-growing regional market?

Rising middle-class income, improving clinic infrastructure, and competitive dental-tourism pricing push Asia-Pacific growth to a 9.39% CAGR.

How are digital technologies shaping restorative workflows?

CAD/CAM systems and intra-oral scanners enable same-day crowns, cut manual error, and currently account for 64.10% of all restorations placed.

What restrains wider patient uptake of restorative dentistry?

High out-of-pocket costs and limited insurance coverage remain the primary barriers, especially for cosmetic indications.

Page last updated on: